Securities Lending Strategies: Exclusive Valuations and Auction Bids

Ravi Kashyap

City University of Hong Kong / SolBridge International School of Business

Keywords: Securities Lending Exclusive Auction; First Price Auction; Bid Strategy; Valuation; Forecast; Uncertainty

JEL Codes: G11 Investment Decisions; G13 Contingent Pricing; C53 Forecasting and Prediction Methods / Simulation Methods

AMS Subject Codes: 91G20 Derivative securities; 91G60 Numerical methods; 60G25 Prediction theory

March 18, 2024

1 Abstract

We derive valuations of a portfolio of financial instruments from a securities lending perspective, under different assumptions, and show a weighting scheme that converges to the true valuation. We illustrate conditions under which our alternative weighting scheme converges faster to the true valuation when compared to the minimum variance weighting. This weighting scheme is applicable in any situation where multiple forecasts are made and we need a methodology to combine them. Our valuations can be useful either to derive a bidding strategy for an exclusive auction or to design an appropriate auction mechanism, depending on which side of the fence a participant sits (whether the interest is to procure the rights to use a portfolio for making stock loans such as for a lending desk, or, to obtain additional revenue from a portfolio such as from the point of view of a long only asset management firm). Lastly, we run simulations to establish numerical examples for the set of valuations and for various bidding strategies corresponding to different auction settings.

2 Introduction

Existing studies on securities lending fail to consider the full extent to which lending desks bridge the demand and supply gap by setting loan rates and managing inventory by finding securities externally or using the positions of other trading desks within the same firm (section 3.3 summarizes much of the existing literature in this space, from which we see that the actions of the lending desks are mostly ignored; appendix 11 provides an introductory background to securities lending). A more complete study on the effects of short selling must look to incorporate the actions of the main players and how they look to alter their cost structure or the demand/supply mechanisms by pulling the above levers (setting loan rates and managing inventory) they have at their disposal. In this paper and related works (Kashyap 2017), we derive various theoretical results that consider the modus operandi of the players in the lending space and supplement the results with practical considerations that can be operationally useful on a daily basis.

The securities lending business is a cash cow for brokerage firms. (D’Avolio 2002; Jones & Lamont 2002; and Duffie, Garleanu, & Pedersen 2002) have details on the mechanics of the equity lending market; (End notes 3 and 4) have further details on the historical evolution of securities lending. Lenders are assured of a positive spread on every loan transaction they make. Historically, the loan rates were determined mostly as a result of a bargaining process between parties taking the loan and traders on the securities lending desks. Recent trends due to increased competitive pressures among different players (lending desks and other intermediaries), the introduction of various third party agents that provide information and advice to beneficial owners (the actual asset owners who supply inventory to the lending desks), and the treatment of securities lending as an investment management and trading discipline, have compressed the spreads (difference between the rate at which lending desks acquire inventory and the rate at which they make loans) and forced lending desks to look for ways to improve their profit margins.

To aid this effort at profitability it is possible to: 1) develop different models to manage spreads on daily securities loans and aid the price discovery process; 2) improve the efficiency of the locate mechanism and optimize the allocation of inventory; 3) develop strategies for placing bids on exclusive auctions; 4) price long term loans as a contract with optionality embedded in them; 4) look at ways to benchmark which securities can be considered to be more in demand, or highly shorted, and use this approach to estimate which securities are potentially going to become “hot” or “special”, that is securities on which the loan rates can go up drastically and supply can get constrained. (Kashyap 2016) looks at some of these recent innovations being used by lending desks and also considers how these methodologies can be useful for both buy side and sell side institutions (that is, for all the participants involved).

In this paper, we derive valuations of a portfolio of financial instruments from a securities lending perspective. This valuation would reflect the value of the portfolio of securities if a certain percentage of the holdings had to be borrowed to cover corresponding short positions. The valuation exercise then becomes an effort at finding an annual rate to be paid to the actual owner of the portfolio of securities that are being offered as an exclusive. This value represents the fees that the participant getting the use of the exclusive (usually securities lending desks) hopes to earn by lending out the securities to their final end borrowers.

In the rest of this section (2.1), we discuss the structure of exclusive auctions and the mechanics of how they are carried out, including the use of visual aids to better illustrate the organization and interaction between the main players. Section 3 provides a deeper discussion of the motivation for exclusive auctions and the benefits it provides for the main participants. Section 3 also reviews many related papers in the securities lending literature where the bulk of the focus has been to study the effects of short selling on stock prices. This illustrates the complementary nature of our paper since we focus on understanding one of the means through which securities lending desks try to obtain inventory (that is securities lending exclusives) and provide tools to come up with a valuation for the same. Section 4 develops the theoretical and modeling aspects of an exclusive and provides the main valuation results. Section 5 summarizes the main auction theory results (which are collected from other papers) that are necessary to make an exclusive auction bid. This is done so that readers will find this paper as a complete reference on securities lending exclusives. As we clarify in the next section (2.1), before making an auction bid participants come up with a valuation and then shade the valuation to suit the type of auction they are participating in. Section 6 has numerical results based on simulations and great care has been taken to ensure that the results are close to what would be observed in an actual exclusive auction. Sections 7 and 8 have suggestions for improvements, extensions that are possible to the benchmark models derived here, assumptions that could be relaxed to incorporate more complex models and the conclusion.

2.1 Securities Lending Exclusive Structure

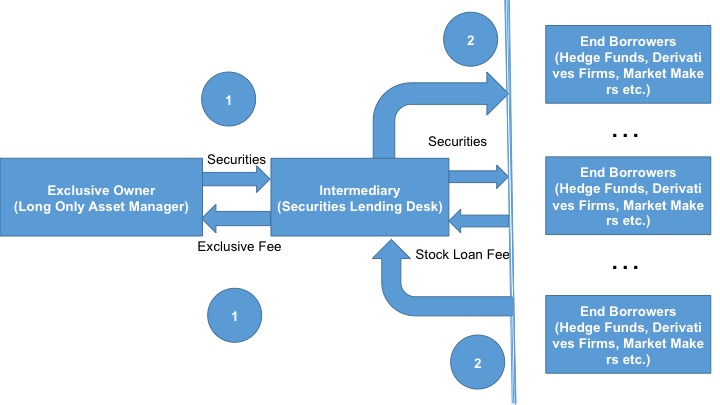

(Figure 1) is a typical exclusive arrangement showing how an intermediary (securities lending desk) sits between an exclusive owner (long only asset manager) and final end borrowers (hedge funds, derivative traders, market makers, etc.) who have short positions. The first portion of the figure (near the circle marked one) shows the exclusive contract arranged between the intermediary and the long only asset manager. This contract allows the intermediary exclusive use of the holdings of the asset manager for making stock loans. In return for being able to use the holdings of the asset manager, the intermediary pays an annual fee. The contract is usually made for a year (or multiple years in some instances) and the fees are fixed when the contract is initiated. The second half of the figure (near the circle marked two) shows the securities from the exclusive portfolio being used by the intermediary to make loans to the final end borrowers. The final end borrowers pay the stock loan fee or the borrow costs; though the intermediary can change this stock loan fee on a daily basis. The stock loans to end borrowers are usually shorter in duration compared to the exclusive contract.

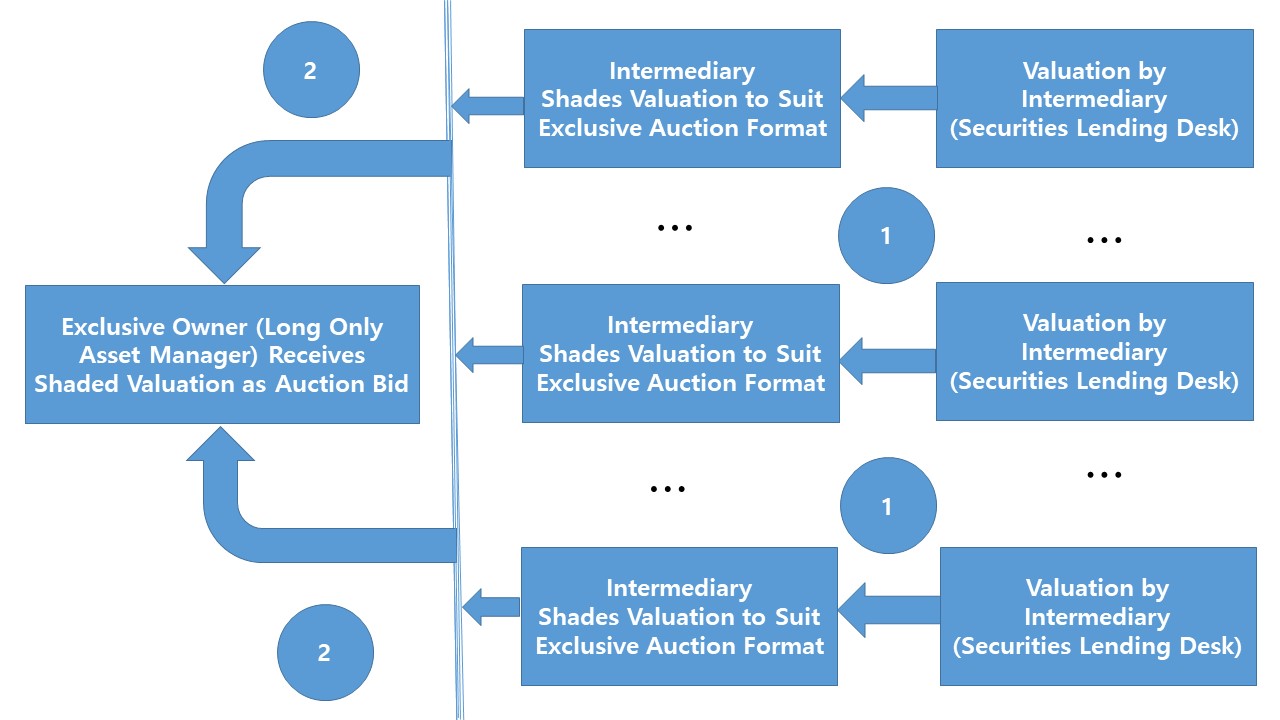

The first step (Figure 2; near the circle marked one) in the determination of the fixed fee paid by the intermediary to the exclusive portfolio owner is the valuation of the portfolio. Section 3 has details on the motivation for procuring such an exclusive contract and section 4 considers the valuation methodologies to arrive at a basis point estimate including various assumptions that would be realistic from a securities lending point of view. The long only asset manager (or an agent of the asset manager) conducts an auction where many interested intermediaries are invited to place bids for the holdings of the asset manager. Hence the valuation obtained in the first step is shaded to suit the many possible auction formats (Figure 2; near the circle marked two), which becomes the bidding strategy discussed in section 5. The winner of the auction is awarded the exclusive contract and the fixed fee is based on the winning bid. Sometimes, the holdings are distributed among a few of the top bidders and many rules are used to decide what fees apply and how much of the holdings each bidder gets. It helpful to think of the valuation of the portfolio as the initial step towards obtaining an auction bidding strategy which is the ultimate goal of the auction participants.

Example 1.

For example, if a portfolio with notional value 1 Billion USD was being offered as an exclusive contract via an auction. If a certain sell-side participant wishes to use this portfolio to lend to their end clients, he would estimate an annual rate based on, among other things, the securities lending loan rates of all the securities in that portfolio. Let us say the estimate turns out to be 25 basis points and the lending desk makes this their bid (without changing the valuation) and wins the auction, the lending desk would then pay 2.5 million USD (1 Billion times 25 basis points) to the exclusive portfolio owner. This example has many simplifying assumptions which are relaxed in the corresponding sections below.

An instance of this situation is when a large sovereign wealth fund sells exclusive securities lending rights to a broker-dealer. A broker-dealer may want to negotiate this type of contract to differentiate its service to client hedge-funds. The assets for which exclusive access is sought are typically difficult to trade, such as securities form a developing countries, or desirable as a bundle, such as the securities underlying an index. Hence, it becomes important to study the problem of using an auction to value exclusive access rights to a block of securities held by a buy-and-hold investor.

Such a valuation of any portfolio of financial instruments can be useful either to derive a bidding strategy for an exclusive auction or to design an appropriate exclusive auction mechanism, depending on which side of the fence a participant sits (whether the interest is to procure the rights to use a portfolio for making stock loans such as for a lending desk, or, to obtain additional revenue from a portfolio such as from the point of view of a long only asset management firm). The valuation of the portfolio being auctioned is subject to the information set available to the bidder or the auction designer. This information set would include among other things: the demand for the securities (say for example, shares being borrowed to short an equity instrument); any additional demand from the loan locates received (section 3 provides an explanation of the locate mechanism); the loan rates applicable to those securities; the duration of the loans; the frequency of loan turnover; the prices of the securities (stock price if the financial instrument is equity); and the internal inventory pool available to the bidder.

Given this scenario, the exclusive valuation can be viewed as an exercise to arrive at the properties of an entire portfolio (the macroscopic system) after factoring the many random characteristics of the individual securities in that portfolio (microscopic constituents). Some of the variables can be modeled as Geometric Brownian Motions (GBMs) with uncertainty introduced via suitable log-normal distributions and certain others can be represented using folded asymmetric normal distributions or by taking the absolute value of a normal distribution. This modeling approach allows the use of simulations to value an exclusive contract making it comparable to the pricing of a derivative contract. An exclusive (to be more precise, the revenue that can be derived from an exclusive) can then be viewed as a contingent claim on a portfolio, which enables the application of suitable option pricing techniques.

Different assumptions regarding the different variables would lead to different valuations. We derive heuristics to arrive at a set of valuations, with a pecking order that can help decide the aggressiveness regarding which of the valuations to chose from. A key result (Theorem 1) is a way to combine different valuations such that the aggregated valuation asymptotically arrives at the true value. This result is applicable to any problem where multiple forecasts are derived and we need a methodology to combine them. We show conditions under which our alternative weighting scheme converges faster to the true valuation when compared to the minimum variance weighting.

Once a valuation has been obtained, it is important to come up with the best strategy from an auction perspective. We use existing and well known auction theory results along with extensions from a related paper (Kashyap 2018). We start with the benchmark scenario where the buyers placing bids are assumed to have perfect and complete information, that is private only to them, regarding their valuation of the portfolio that is being auctioned. We consider the uniform distribution as the simplest scenario and extend that to a more realistic setting that considers the valuations to be log normally distributed. We further extend this by introducing uncertainty into the estimation of bidder valuations and their bidding strategy. The possibility of the number of bidders being unknown, the valuations from various bidders being correlated or the interdependent valuation framework and, a reserve price set by the auction seller are more complex extensions. Based on existing results, it is easily seen that the strategies of the bidders constitute a Nash equilibrium under suitable conditions.

Lastly, we run simulations to establish numerical examples for the set of valuations and for various bidding strategies corresponding to the different auction settings. The next generation of models and empirical work on securities lending activity would benefit by factoring in the methodologies considered here. Understanding the inner workings of securities lending players, including the provision of better tools and models to aid their efforts, could counter the recent concerns about risks in the securities lending space (End-note 6). In addition, the models developed here could be potentially useful for inventory estimation and for wholesale procurement of financial instruments and also non-financial commodities.

From the discussion thus far and as the paper deveops, it will become clear that exclusive valuation is an extremely challenging problem in terms of the many sources of uncertainty that it holds. Having better ways to manage this complexity, as illustrated in this paper, will be well rewarded since this is one of the least explored yet profit laden areas of modern investment management. For completeness, we provide a brief motivation for exclusive auctions before delving further into the mechanism of estimating an auction bid for exclusives.

3 Motivation for Exclusive Auctions

We can trace the origins of Exclusive Auctions to the early 2000s. (Duffie, Garleanu & Pedersen 2002) briefly mention an exclusive lending deal between Credit Suisse First Boston (CSFB) and California Public Employees Retirement System (CalPERS) in 2000. We could found any other reference on this topic in a serious academic paper. As with the rest of the securities lending industry, this practice is more prevalent for equity portfolios. As opposed to traditional arrangements between intermediary brokers and beneficial owners, where the loan rates on each security are negotiated periodically, an exclusive auction, as the name suggests, provides sole usage of a portfolio of securities, or to a portion of the portfolio, to the winner in an auction process for a certain time period. This arrangement is beneficial to both parties since the intermediary broker gets single ownership to the portfolio. Intermediaries can use the portfolio as part of their overall supply and even if the loan rates for a group of securities in the portfolio go up, the costs of sourcing these special stocks remains the same. Intermediaries look at exclusives as a source of locking up inventory for a certain time horizon. Beneficial owners get a guaranteed source of revenue and will not have the administration hassle of having to constantly create new loans. They will not have to deal with multiple intermediaries and can place their portfolio with an auction agent. Both parties do not need to negotiate or renegotiate loan rates on individual securities for the duration of the exclusive contract.

The holdings in the portfolio on certain key dates are provided to the intermediary brokers or the agent administering the auction to enable brokers to estimate the value of the portfolio from a lending perspective. The intermediary brokers shade this valuation of the portfolio to suit the auction mechanism and make bids accordingly. The bid is usually expressed as a certain number of basis points of the portfolio value at the time of auction, applicable annually or over the duration of the exclusive agreement. In addition to the exclusive bid, beneficial owners also sometimes charge transaction fees each time securities are taken out from the portfolio or added back.

Beneficial owners continue to manage their portfolio positions as per their investment mandates or according to their re-balancing guidelines or risk tolerances. This risk of turnover in the holdings is something that intermediaries need to factor in their exclusive bids. The agreements can stipulate certain criteria on the turnover of the holdings, which would require the exclusive fee to be reassessed. The huge size of the portfolios that are generally auctioned and the relatively small price of the exclusive fees, in comparison with the loan rates on individual securities, mean that winning an auction bid is an extremely profitable venture for intermediaries. In addition, by gaining access to an exclusive portfolio, intermediaries prevent competitors from having access to this source of inventory, almost acting like monopolists in supplying loans for certain hard to borrow instruments. This restricted supply enables loans to be priced higher. This phenomenon is partly offset when a portfolio is auctioned to more than one bidder, but still provides pricing power to the winners of the auction. This practice of spreading very large portfolios across three or four of the top bidders is becoming more common.

Sometimes, the lending desk could have access to shares available to others parts of the firm when it acts as a primer broker, operates derivative trading, proprietary trading or services private client accounts. This additional inventory is readily available to the firm as a side effect of having other business units or trading desks. The lending desks at various firms are expected to fully utilize this internal inventory before looking outside for additional supply. Complete utilization of this internal inventory would reduce the funding costs for the other business units and also make the loan rates charged by the firm cheaper than the loan rates of other lending desks, when it has significant internal inventory. The variation in the valuation of the exclusive across different firms would then primarily depend on the extent of the overlap of this internal supply with the holdings in the exclusive. The other source of variation would be the loan rates the lending desk applies to the loans it makes. Historically, the loans rates across different lending desks of different intermediaries have varied considerably due to the opaque nature of the transactions and the variable demand seen by individual desks. With centralized platforms, which consolidate and disclose rates across firms, coming into vogue loan rates have converged to a considerable extent.

Another piece of the puzzle is the locate requests received by the lending desk on a daily basis. These locate requests are sent by end borrowers, in advance of actually borrowing shares to short, to get an indication of the quantity of shares they can borrow. This is done to ensure that their shorting needs for the trading day can be met. The intermediary can fill either a portion or the entire locate request depending on its inventory situation and also depending on how many firms are sending it locates for that particular security for that trading day. But once a locate request is filled by a lending desk, they are expected to have that number of shares ready for the borrowing firm. A borrowing firm, on the other hand, can borrow as much of the filled locate amount as it chooses to. This mismatch between locate approvals and actual borrows then leads to another aspect of the lending business that can be optimized by implementing different variations of the Knapsack Algorithm (Martello & Toth 1987) and we consider this in another paper (Kashyap 2016). The conversion factor from locates to borrows can be estimated as part of the locate approval optimization. For the present purpose of estimating an exclusive value, we take this conversion factor as exogenously given. Lending desks have been considering charging a nominal fee based on the locate amount they agree to fill to discourage borrowers from sending in spurious locate requests, though this practice is yet to be formally institutionalized across the lending industry.

So in effect, the lending desk has a certain amount of borrows on the book at any time, which is matched by a combination of internal inventory and supply from beneficial owners. Excess demand arrives in the form of locate requests. Existing loan borrowers can increase their loan holdings via telephone or email, so the loan book can change without the means of locate requests. Managing loan turnover, returning or acquiring supply, locate fulfillment and negotiating the loan rates then constitute the primary loan management duties of the desk.

3.1 Exclusive Auctions Wallet Size

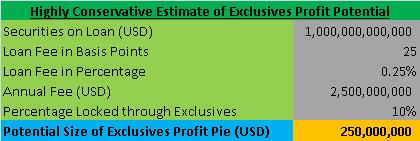

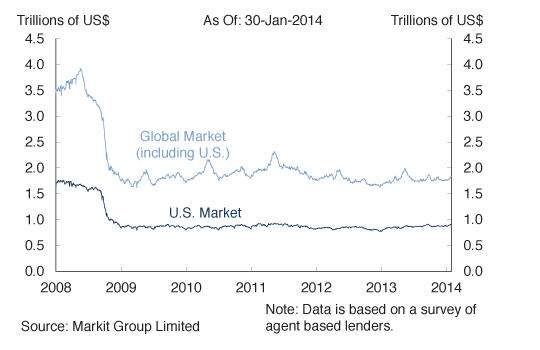

A rough estimate of the potential profits that could be accrued by indulging in exclusives is shown in Figure 3. The point to keep in mind is that this is a highly conservative and approximate estimate since we have used 1 Trillion USD as the notional amount of securities on loan and around 25 basis points as the loan fees in our estimate (End-note 6 mentions that the volume weighted average loan rate in the US is around 38 basis points; many other markets have much higher weighted average loan rates). The global securities on loan is around 2 trillion USD (Figure 4) and there are securities with loan rates of almost 25%. (Baklanova, Copeland & McCaughrin 2015; End-notes 5, 6) have more details on the size of the securities lending market. Even this simple back of the envelope calculation demonstrates that better techniques could go a long way in boosting profits in the exclusive auction process towards which, to the best of our knowledge, no prior work has been done that applies the use of quantitative methodologies.

USA

Asia Western

Europe

Western

Europe

3.2 Buy Side and Sell Side Perspective

The sell side here would be the collection of intermediary firms that source supply and lend it on to final end borrowers. The buy side here would have two segments of firms. One, the end borrowers who either have a proprietary trading strategy or hedging that requires shorting certain securities. Two, the beneficial owners who are long and provide supply to the intermediaries also fall under the buy side category. Depending on which side a firm falls under, they will find the below derivations useful, since it will affect the rates they charge or the rates they pay. These methodologies will also help auction designers, who operate on behalf of beneficial owners, formulate an appropriate mechanism that results in the best outcomes for their clients. This can provide transparency to the beneficial owners in terms of how the actual valuation of the portfolio might differ from the actual bids received and hence the actual proceeds.

As we will see in the section 4, valuation of this portfolio requires understanding uncertainty from numerous angles. As the participants try to find better and improved ways to contend with this uncertainty (Kashyap 2017), we will see that the profitability of using this mechanism might decrease for participants from both sides. This can lead us to believe that over time, as better valuation methods are used by the participants, in an iterative fashion, the profits will continue to erode. A key duty of lending desks is the management of collateral, which can lead to the movement of securities multiple times across many parties, exacerbating financial risk (End-note 8). Things can go drastically wrong even in simple environments (Sweeney & Sweeney 1977 has a discussion of chaos in a baby sitting monetary system with around 150 households), hence in a complex valuation of the sort that we are dealing with here, extreme caution should be the rule rather than the exception. (Kashyap 2017) looks at recent empirical examples related to trading costs where unintended consequences set in. With the above background in mind, let us look at how we could value an exclusive portfolio.

3.3 Related Literature

While the main results we develop for exclusive valuations are immediately applicable to equity instruments, the key distinction between consumption assets and investment assets [shorting generally applies only to investments assets, whereas consumption assets cannot be directly shorted] should tell us that our valuation methodologies can be used to transfer the rights on any bundle of investment assets. (Hull 2010) has a description of consumption and investment assets, specific to the price determination of futures and forwards; (Kashyap 2017, End-note 7) have a more general discussion. The price effect on consumption assets affects the quantity bought and consumed, whereas with investment assets (especially ones that can be shorted), the cyclical linkage between vacillating prices and increasing numbers of transactions is more readily apparent.

The primary focus on short selling is that activity in the shorting market can be used to predict future security returns. There are many studies that develop theoretical models and perform an application of these concepts to different data-sets, both public and proprietary. By looking at the below studies on securities lending, it becomes clear that there is hardly any paper that considers the motivations of the main players, the actions that arise due to these incentives and the impact of these actions on the securities lending market and no study at all on how to determine the value of exclusive auctions. The below studies can also be useful for understanding the importance of securities lending towards better portfolio performance (even if a portfolio has no short sales) and why more research towards uncovering the actions of the main players in the lending market can be helpful towards this goal.

(Duffie, Garleanu & Pedersen 2002) present a model of asset valuation in which short-selling is achieved by searching for security lenders and by bargaining over the terms of the lending fee. They provide a closed-form equilibrium solution, including the dynamics of the price, of the lending fees, and of the short interest. The price is elevated by the prospect of future lending fees, and may, in the beginning, be even higher than the valuation of the most optimistic agent. (Harrison & Kreps 1978; Morris 1996) obtain a similar result but explained due to speculative behavior, or the right that investors hold to resell securities, which makes them willing to pay more for it than they would pay if they were obliged to hold it forever. (Hong & Stein 2003) develop a theory of market crashes based on differences of opinion among investors, with a suggestion that short-sales constraints may play a bigger role than one might have guessed based on just the direct transactions costs associated with shorting.

(Diamond & Verrecchia 1987) provide a theoretical model which implies that the costs associated with short selling will squeeze liquidity traders out of such order flow. This has the effect of making short orders more informative than the population of regular sell orders. (Allen, Morris & Postlewaite 1993) show that even if there is a finite number of trading opportunities, the market price of a security can be above the present value of its future dividends, that is a bubble can persist in the presence of asymmetric information (or agents do not know the beliefs of other agents) with short-sales constraints. [For other theoretical work on the implications of short sale constraints for stock prices, see (Jarrow 1980) and (Scheinkman & Xiong 2003)].

The standard empirical approach to testing the relation between the shorting market and future stock returns relies on finding an appropriate measure of short sale constraints. This measure is usually obtained either from data on direct costs of shorting from the stock loan market, or by employing proxies for shorting demand or shorting supply. The idea behind looking at shorting demand is that some investors may want to short a stock but may be impeded by constraints; if one can measure the size of this group of investors, one can measure the extent of overpricing or the extent of private information left out of the market. The idea behind looking at shorting supply is that since shorting a stock requires one first to borrow the shares, a low supply of lend-able shares may indicate that short sale constraints are binding tightly.

(Aitken, Frino, McCorry & Swan 1998) build on prior research by extending the investigation of market reaction to short sales to an intraday framework in a setting where short trades are transparent shortly after the time of execution. Focusing on the Australian market, they find a significantly negative abnormal return in calendar time following short sales (initiated using both market and limit ask orders). (Bris, Goetzmann & Zhu 2007) analyze cross-sectional and time series information from forty-six equity markets around the world, to consider whether short sales restrictions affect the efficiency of the market, and the distributional characteristics of returns to individual stocks and market indices. They find some evidence that in markets where short selling is either prohibited or not practiced, market returns display significantly less negative skewness. However, at the individual stock level, short sales restrictions appear to make no difference.

(Boehmer, Jones & Zhang 2008) use a panel of proprietary system order data from the New York Stock Exchange to examine the incidence and information content of various kinds of short sale orders. Their findings indicate that institutional short sellers have identified and acted on important value-relevant information that has not yet been impounded into price. The results are strongly consistent with the emerging consensus in financial economics that short sellers possess important information, and their trades are important contributors to more efficient stock prices.

(Desai, Ramesh, Thiagarajan & Balachandran 2002) examine stocks on the NASDAQ and find that heavily shorted firms experience significant negative abnormal returns after controlling for market, size, book-to-market and momentum factors. The negative returns increase with the level of short interest, indicating that a higher level of short interest is a stronger bearish signals. (D’avolio 2002) describes the market for borrowing and lending U.S. equities and provides an empirical summary of conditions that can generate and sustain short sale constraints (defined as legal, institutional or cost impediments to selling securities short). (Cohen, Diether and Malloy 2007) examine the link between the shorting market and stock prices using proprietary data from an intermediary. They find that an increase in shorting demand leads to negative abnormal returns. (Kolasinski, Reed & Ringgenberg 2013) empirically show that search frictions are related to loan fee dispersion by examining the (Duffie, Garleanu & Pedersen 2002) model. [Other empirical studies include: (Jones & Lamont 2002; Reed 2002; Geczy, Musto, and Reed 2007; Mitchell, Pulvino & Stafford 2002; Ofek & Richardson 2003; and Ofek, Richardson, & Whitelaw 2003); among others.]

4 Exclusive Valuation

4.1 Valuation Setup

The objective of a rational risk neutral decision maker at the intermediary would be to maximize the profits, , by utilizing the shares available from the exclusive over the entire duration of the contract, extending from time period, (Eq. 1). We define all the variables as we introduce them in the text but section 12 has a complete dictionary of all the notation and symbols used in the main results. is the valuation of the exclusive for the duration of the contract. A trivial result when the valuation is zero, will lead to the maximum amount of profits, but it should be clear that very low valuations will not lead to securing the exclusive contract. Higher the valuation, higher the chances that the exclusive becomes less elusive. Hence the goal is to obtain maximum bounds for the valuation, above which it will not be profitable for the intermediary.

It is worth highlighting that the decision process of the intermediary (or the variables that he can directly influence or set) will only include the amount of shares he can take from the exclusive, , and the additional supply of shares that can be sourced from other beneficial owners, . Here, subscript denotes the security in the portfolio and the number securities ranges from . The other variables are taken as exogenous: , the holdings available in the Exclusive pool; , the rate on the stock loan charged by the intermediary; , the security price at a particular time; is the discount factor. This assumption is the most realistic scenario, but depending on the size of the exclusive and internal inventory the loan rates can further be taken as variables he can influence. What happens in practice is that there is usually a baseline for the loan rates and a spread is added on top of it. A deeper discussion of how loan rates are set, including the addition of a spread component, are taken up in a separate paper (Kashyap 2016).

We get two constraints (Eq. 2, 3) based on the properties of the different variables. One is that the amount of shares for a particular security taken from the exclusive is less than the total size of holdings in that security in the exclusive portfolio, . Clearly, is a trivial condition. The other one is that the loan book carried by the desk, (existing amount loaned out to external borrowers and hence can also be termed the borrow book; though certain intermediaries reserve the words “borrow book “to denote the amount they have borrowed from external lenders; in our paper we these terms interchangeably), , plus any additional demand received based on the Locate requests and the conversion rate of locates into borrows must equal (to be precise, it should be greater than) the sum of the Internal Inventory the intermediary holds based on the positions of all trading desks within the firm, , the total holdings in the exclusive, and the additional supply of shares, . Usually securities lending desks have a certain preferential treatment of different sources of inventory. Their primary source is the internal inventory, since lending it out would reduce the funding rate for their firm positions. The next source will be any exclusive arrangements, since a fee would need to be paid irrespective of whether these positions are used or not. The last resort is to obtain shares from external lenders. Only when the supply from a more preferred source is exhausted will a desk look to the next source on its list of suppliers.

| (1) |

| (2) | ||||

| (3) |

We can model the security prices, loan rates, the loan book, internal inventory and exclusive holdings as GBMs. For simplicity in the numerical results, we assume that the Weiner process governing each of these is independent. The loan book, the internal inventory and holdings represent number of shares, and hence are always positive making them good candidates to be modeled as GBMs. Security prices are commonly modeled as GBMs. In addition, our baseline models are diffusions without mean-reversion which we can justify since an exclusive contract is usually agreed for one to two years and the variables will not take on excessively large values in this duration (non-negative drift rates can grow a variable to infinity over time, but some of our variables have negative drift rates as well as we see in the numerical results in section 6.1). (Hull 2010) provides an excellent account of using GBMs to model stock prices and other time series that are always positive; See (Norstad 1999) for a discussion of the log normal discussion.

The borrow process is highly volatile, with the the order of magnitude of the change in the total amount of shares lent out over a few months being multiple times of the total amount carried at any point in time. The internal inventory can change significantly as well, though there would be less turnover compared to the borrow process. This would of course depend on which parts of the firm the inventory is coming from. The holdings of the exclusive are the least volatile of the three processes that govern shares (or at-least the intermediary would hope so). The volatility of inventory turnover (or any supply) can be a sign of the quality of the inventory and this can be used to come up with a rate accordingly (the rate here is the price of the inventory). This extension and other improvements where the loan rates and the internal inventory can be made endogenous as opposed to the present simplification where they are exogenous will be considered in a subsequent paper (Kashyap 2016).

| (4) |

| Geometric Brownian Motion | |||

The locate process is more precisely modeled as a Poisson process since it would be reasonably accurate to consider locates as discrete events occurring in time, that is, requests for a certain number of shares being received in a given time interval. Given that most of the time, the number and size of the share requests can be large, we would need to use a high value of the arrival rate, . Hence, we approximate this poison process as the absolute value of a normal distribution with appropriate units (Cheng 1949). This introduces a certain amount of skew, which is naturally inherent in this process.

| (5) | ||||

| Locate Process | (6) | |||

| (7) |

With the above variables and their properties, we consider ways in which we can simplify the system and obtain solutions that can aid in putting a numerical value on the portfolio of securities. In a complex system (1, 2, 3, 4, 5 and 8), deriving equations can be a daunting exercise, and not to mention, of limited practical validity. Hence, to supplements equations, we will employ simplifications that establish a few inequalities governing this system. Pondering on the sources of uncertainty and the tools we have to capture it, might lead us to believe that, either, the level of our mathematical knowledge is not advanced enough, or, we are using the wrong methods. The dichotomy between logic and randomness is a topic for another time.

4.2 Benchmark Valuation or Zero Profits Upper Bounds

To obtain an upper bound for the profits, we note that if the cash flows received from the loans made using the shares from the exclusive exactly balance out the payments to be made to the exclusive portfolio owner, we would have zero profits. If this is the criteria under which we obtain zero profits, then it becomes the maximum value one would be willing to pay for the exclusive contract; any actual valuation for the exclusive should be less than this zero profit valuation: . Here, we need to remember that we only use exclusives when the total demand faced by the lending desk is higher than the internal inventory available to the desk. This can be written as, . Combining it with the constraint (Eq. 2, ), that is we cannot obtain shares greater than the total size of the holdings in the exclusive, gives us a result captured in the below proposition.

Proposition 1.

The zero profits upper bound for the valuation is given by

| (8) |

Proof.

See appendix 13.1. ∎

An immediate takeaway from this expression, which has immense intuitive appeal, is that the higher the valuation lesser will be the extent of overlap between the internal inventory and the exclusive holding. Checking this historical overlap between internal inventory and exclusive holdings can be an excellent complement to the valuation expressions we derive.

A standard theoretical approach to solving (Eq. 8) or obtaining a closed forum solution, is presently unknown to the best of our knowledge, given the number of GBMs the system incorporates. An alternate approach would be to estimate the parameters of all the random variables from historical data and run simulations that would provide the required exclusive valuation. It is worth keeping in mind that the intermediary firm or the beneficial owner will have access to a historical time series of some of the variables and hence can estimate the actual process for the various variables. Though either party will not know the time series of all the variables with certainty and hence would need to substitute the unknown variables purely with a simulation based process similar to what we have used in section 6.1. (Campbell, Lo, MacKinlay & Whitelaw 1998; Lai & Xing 2008; Cochrane 2009) are handy resources on using maximum likelihood estimation (MLE) and generalized method of moments (GMM) for parameter estimation. A simplification is to assume that the variables are independent. While a realistic calculation might show that these variables are correlated, such a simplification provides an excellent benchmark for our valuation exercise; (Gujarati 1995; Hamilton 1994) discuss time series simplifications and the need for parsimonious models . A backward induction based computer program, which simulates the randomness component of the variables involved, can calculate the value of the exclusive based on the above expression (Eq. 8).

4.3 Valuation with Transaction Costs

It is not uncommon to have a transaction cost, , when securities are taken out or put back into an exclusive portfolio. Hence, it is useful to have a valuation expression, , after incorporating transaction costs.

Proposition 2.

The valuation expression that captures transaction costs is given by

| (10) |

Here,

Proof.

See appendix 13.2. ∎

It is trivial to see that,

| (11) |

In a similar vein, we can also arrive at an expression for transaction costs when the charges to Take and Give are different. We don’t derive that here, since that is usually a rarity. Alternately, (Erdos and Hunt 1953) derive results regarding the change of signs of sums of random variables which can provide approximations for transaction costs.

4.4 Other Conservative Valuation Inequalities to Supplement Equations

We now provide various methods to come up with more conservative estimates of the valuation. We call these conservative valuations because they underestimate the potential benefit or profits such a valuation would bring. As we can see from (Eq. 9), there are two variables that can be useful towards this end. First, we can set or when excess demand is zero (other alternatives are lower values of ), giving us a conservative valuation, ,with zero excess demand,

| (12) |

Instead of using the rates at which the desk makes loans to borrowers, we can use the rate at which it finds supply from other beneficial owners. Sometimes, where no other supply is available a theoretical rate is used by lending desks. The different possible variations here would depend on the different types of rates (possibly due to different levels of spread) a lending desk would use on a daily basis and also store historically. We show two variations one which has a lower value of the loan rates, , and another combines zero excess demand with the lower value of the loan rates , ,

| (13) |

| (14) |

This gives the following pecking order of valuations for the exclusive.

| (15) |

| (16) |

The intermediary can decide on their level of aggressiveness and choose which of the valuations they wants to use, depending on how many exclusives they already have, the extent of overlap with their internal inventory, the number of special names in the exclusive portfolio and the volatility of the time series of daily profits from the exclusive. Such a tiered approach is found to be more practical rather than having an exact valuation since there are too many sources of uncertainty and the noise or the variance of any exact valuation number would tend to be high.

4.5 Historical Valuations

Given the complexity and the number of variables to be estimated (Eqs: 1, 2, 3, 4, 5 and 8), a simple heuristic would be utilize the historical time series of each of the variables and then use that as a possible guide to the calculation of the exclusive value. The theoretical justification for using the actual historical series directly to value the exclusive without first resorting to parameter estimations and then running simulations using the estimated distribution parameters is that there are errors introduced during the estimation which are then compounded while doing the simulations (Kashyap 2017). The pecking order shown above (Eqs: 11, 15 and 16) can be arrived at using the historical time series as well. Using this, we can also arrive at the time series of the daily profits that would accrue to the intermediary. The volatility of the daily value of the exclusive can be suggestive in terms of how aggressive one should be in picking one of the valuation tiers. Any of the historical valuations can be represented as below, where and denote the start and end of the time series such that ,

| (17) |

New valuation time series can be created by adding transaction costs or alternate rates, or other combinations. Armed with this set of valuations, , the bidder can combine them using the method we shown in the next sub-section (4.6).

4.6 Variance Weighted Combined Valuation

A valuation is nothing but a forecast of future value or benefits that we hope to derive from any object. There is a huge amount of literature on combining forecasts starting with the seminal paper by (Bates & Granger 1969). For different methods of combining forecasts including recent developments and surveys on the topic see: (Granger & Ramanathan 1984; Granger 1989; Clemen 1989; Timmermann 2006; Hsiao & Wan 2014; Conflitti, De Mol & Giannone 2015; Chan & Pauwels 2018). (Smith & Wallis 2009) has a formal explanation of the forecast combination puzzle, that simple combinations of point forecasts are repeatedly found to outperform sophisticated weighted combinations in empirical applications. The minimum variance weights for the valuation among a set of valuations are given by . We give a proof that this is the minimum variance weighting as the number of valuations increases in appendix 13.3.6.

In theorem 1 we show an alternative weighting scheme that combines the valuations using the variance of the individual valuation time series. We derive the conditions under which it converges to the true valuation faster than the minimum variance combination. Hence, the results in this section are applicable to problems where multiple forecasts are obtained and we need a technique to weight the forecasts to come up with a single value. This shows that this weighting methodology could have wide usage outside of the securities lending or even the financial industry.

We argue that under certain conditions of finite variance and finite valuation of each individual time series we get closer to the true valuation as the number of individual time series considered in the aggregation gets larger. For simplicity of notation, in this section we let each individual time series be represented by with corresponding variances and the true valuation by .

Theorem 1.

If each of the valuations and the variances of the valuations are finite, ; the covariances are zero, ; no single one dominates the sum, expressed as,

and the following combination of the valuations and variances is uniformly bounded, that is for any real number ,

Then when each of the individual valuations are weighted using the scheme shown below (sum of the variance of all other valuations divided by the total variance times the number of valuations) the expression below asymptotically converges in probability () to the true valuation.

When the valuations have different expected values we have the result,

This alternative weighting scheme converges faster to the true valuation than the minimum variance weighting scheme when the following conditions hold,

Proof.

See appendix 13.3 for the proofs, including expressions for the variance of the aggregated valuations (both the alternative weighting and minimum variance schemes) and the corresponding asymptotic result showing that the variance of the combined valuation as is zero. ∎

Similar to the minimum variance weighting, our alternative weighting scheme has an intuitive and practical appeal since the time series with a higher variance is set a lower weight in the combined valuation. But if we have many valuations and we find that the conditions for faster convergence are satisfied our alternative scheme becomes more desirable. This means the more expressions we are able to derive for the valuations and combine them, the better will be our estimation. Of course, it becomes important to ensure that we do not have redundant valuation expressions that are just multiples of one other; but valuations that would be good candidates to vary and create newer time series are the ones that differ by capturing the different possible variations in any of the variables that can affect the valuation outcome. This result has a certain theoretical significance since it shows that when any object has multiple valuations, where each valuation might arise due to slightly different assumptions; a combination using our technique gets closer to the true valuation faster.

Alternately, the intermediary can subjectively select a particular valuation to suit the institutional setup or relevance depending on the preferences at the intermediary (whether their internal inventory tends to be large or they are looking to have many exclusives in place expecting greater future demand and so on). Either way, once a final valuation has been obtained the next step is to prepare for an auction process and pick a strategy that will shade the value to suit the mechanics of different auction situations.

5 Auction Strategy

Once we have the valuation from the previous section (4), it is important to look at different auction formats and the specifics of how an intermediary would tailor bids to adapt to the particular auction setting. From the perspective of the owner of the exclusive portfolio, he would use the valuation and the auction setting to understand the potential revenue opportunity. We consider a few variations in the first price sealed bid auction mechanism. The key auction theory results we use, including the proofs for some of the extensions of core auction theory results to real life applications, are from (Kashyap 2018). The results we discuss below are not new, but we provide them for completeness and also because they are important for the numerical calculations in section 6.2.

The literature on Auction Theory is vast and deep. The following standard and detailed texts on this topic might aid the interested reader: (Klemperer 2004; Krishna 2009; Menezes & Monteiro 2005; and Milgrom 2004). Additional references are (Laffont, Ossard & Vuong 1995; Milgrom & Weber 1982); for using numerical techniques (Miranda & Fackler 2002) or approximations to the error function (Chiani, Dardari and Simon 2003) . (Ortega-Reichert 1967; and Harstad, Kagel & Levin 1990) derive the expression when there is uncertainty about the number of bidders. (Levin & Ozdenoren 2004; and Dyer, Kagel & Levin 1989) are other useful references. (Lebrun 1999) derives conditions for the existence of an asymmetric equilibrium with more than two bidders.

A bidding strategy is sensitive to assumed distributions of both the valuations and the number of bidders. This is seen from the expression for the bid strategy in (Lemma 1). As a benchmark bidding case, it is illustrative to assume that all bidders know their valuations and only theirs and they believe that the values of the others are independently distributed according to the general distribution . is the valuation of bidder . This is a realization of the random variable which bidder and only bidder knows for sure. , is symmetric and independently distributed according to the distribution over the interval . is increasing and has full support, which is the non-negative real line , hence in this formulation we can have . is the continuous density function of . is the total number of bidders. When there is no confusion about which specific bidder we are referring to, we drop the subscripts such as in the valuation . , is the random variable that denotes the highest value, say for bidder 1, among the other bidders. is the highest order statistic of . is the distribution function of . That is, and is the continuous density function of or . is the expected payment of a bidder with value . is an increasing function that gives the strategy for bidder . We let . We must have . is the strategy of all the bidders in a symmetric equilibrium. We let is the valuation of any bidder. We also have .

Lemma 1.

The symmetric equilibrium bidding strategy for a bidder, the expected payment of a bidder and the expected revenue of a seller are given by

Equilibrium Bid Function is,

Expected ex ante payment of a particular bidder is,

Expected revenue, , to the seller is

We consider two distributions for shading the valuation to formulate a bidding strategy: Uniform and Log-normal. The two distribution types we discuss can shed light on the other types of distributions in which only positive observations are allowed. The uniform distribution is well uniform and hence is ideal when the valuations (or sometimes even the number of bidders) are expected to fall equally on a finite number of possibilities (Corollary 1). This serves as one extreme to the sort of distribution we can expect in real life.

Corollary 1.

The symmetric equilibrium bidding strategy when the valuations are distributed uniformly is given by

Here, since we are considering the uniform distribution.

The other case is a log-normal distribution which centers around a value and the chance of observing values further away from this central value become smaller. Asset prices are generally modeled as log-normal, so financial applications, including an exclusive valuation would benefit from this extension. The absence of a closed form solution for the log-normal distribution forces us to develop a rough theoretical approximation (Corollary 2) and improve upon that significantly using non-linear regressions (Remark 1; Eq. 18). This works well for our particular application, since the valuations are generally small, of the order of a few basis points. A detailed discussion of the the log-normal approximation, including the accuracy of the regression results, suggested values for the regression coefficients and the sensitivity of the bid strategy to the valuation, the parameters of the valuation distribution and the number of bidders is provided in (Kashyap 2018).

Corollary 2.

The symmetric equilibrium bidding strategy when the valuations are small, of the order less than one, and distributed log-normally, can be roughly approximated as

Here, , is the standard normal cumulative distribution and where, . since we are considering the log-normal distribution.

When the number of bidders are large the above expression for the uniform distribution (Corollary 1) does not depend on the number of bidders, that is . Comparing the bidding strategy with respect to the distribution of valuations in the two cases, the uniform distribution when the number of bidders are large and the log-normal distribution theoretical approximation (Corollary 2) we see that: 1) both do not depend significantly on the number of bidders and 2) the bid is larger with a uniform distribution.

Remark 1.

A better approximation for the log-normal distribution can be obtained using non-linear regression to find the constant, , and the power coefficients, ,, and in the expression below,

| (18) |

In many auction settings, the auction seller can set a minimum bid to ensure that he is guaranteed a minimum amount of revenue. This minimum bid is known as the reserve price. Our valuation techniques can help auction sellers come up with a reserve price. Clearly, if the reserve price is too high, many potential bidders will shy away from participating in the auction. But setting a reserve price, ensures that the bid strategies need to be higher to ensure successfully winning the auction (Lemma 2).

Lemma 2.

The symmetric equilibrium bidding strategy when the valuation is greater than the reserve price, , of the seller, , is

For a general distribution,

When the valuations are distributed uniformly, the bid strategy with a reserve price is given in (Corollary 3),

Corollary 3.

The symmetric equilibrium bidding strategy when the valuation is greater than the reserve price of the seller, , and valuations are from an uniform distribution,

When the valuations are distributed log-normally, the bid strategy with a reserve price is given in (Corollary 4),

Corollary 4.

The symmetric equilibrium bidding strategy when the valuation is greater than the reserve price of the seller, , and valuations are from a log normal distribution,

The following result can aid auction sellers in finding an optimal reserve price (Lemma 3),

Lemma 3.

The optimal reserve price for the seller, must satisfy the following expression,

Here, seller has a valuation,

When there is uncertainty about how many interested bidders there are, we denote the potential set of bidders as . is the set of actual bidders. All potential bidders draw their valuations independently distributed according to the general distribution . Also, is the probability that any participating bidder, is facing other bidders or the probability that he assigns to the event that he is facing other bidders. This implies that there is a total of bidders, . is the probability of the event that the highest of values drawn from the symmetric distribution is less than , his valuation and the bidder wins in this case. is the equilibrium bidding strategy when there are a total of exactly bidders, known with certainty. The overall probability that the bidder will win when he bids is

| (19) |

Hence the equilibrium bid for an actual bidder when he is unsure about the number of rivals he faces is a weighted average of the equilibrium bids in an auction when the number of bidders is known to all. (McAfee & McMillan 1987b) is one of the most well known and early generalizations to allow the number of bidders to be stochastic.

Lemma 4.

The equilibrium strategy when there is uncertainty about the number of bidders is given by

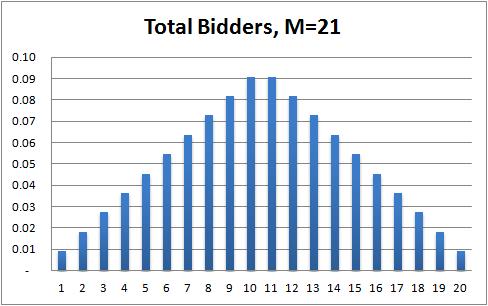

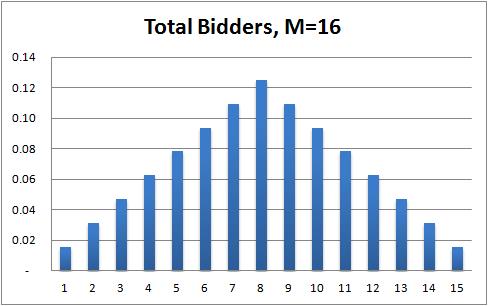

When bidding for an exclusive, an intermediary, will expect most of the other major players to be bidding as well. Invariably, there will be some drop outs, depending on their recent exclusive bidding activity and some smaller players will show up based on the composition of the portfolio being auctioned. It is a reasonable assumption that all of the bidders hold similar beliefs about the distribution of the number of players. Hence, for the numerical results, we construct a symmetric discrete distributions of the sort shown in (Figure 5). This formulations of a positive symmetric discrete distribution is likely to be followed by the total number of auction participants, and we incorporate this into auction theory results. We show that such a distribution satisfies all the properties of a probability distribution function as part of the proof for Lemma 5 (Kashyap 2018). It is to be noted that this symmetric discrete distribution comes under the family of triangular distributions (End-note 9). We can easily come up with variations that can provide discrete asymmetric probabilities. For simplicity, we use the uniform distribution for the valuations and set . The below result follows from a bidding strategy that incorporates the use of the discrete symmetric distribution.

Lemma 5.

The bidding strategy and the formula for the probability of facing any particular total number of bidders under a symmetric discrete distribution would be given by,

We note that can also be written as,

This discrete distribution can also be a possibility for the valuations themselves, since the set of prices of assets or valuations can be from a finite set. But given the distribution, developing a bidding strategy based on this discussion is trivial and hence is not explicitly considered here. Lastly, the case of interdependent valuations are to be highly expected in real life; but practical extensions for this case are near absent both in the literature and in practice. In appendix 15, we provide extensions when the valuations of the bidders are interdependent and incorporate the corresponding results into a final combined realistic setting. We also provide additional results when bidders hold asymmetric beliefs in appendix 15. These results can be useful extensions to aid the profit maximization goals of exclusive auction participants depending on the assumptions they wish to make regarding their environment and can be useful for bidders and auctions sellers during the wholesale procurement of other financial instruments.

6 Numerical Results

6.1 Data-set Construction

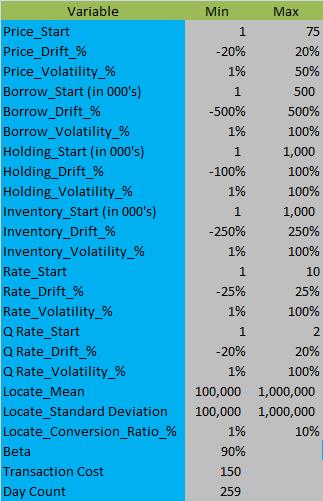

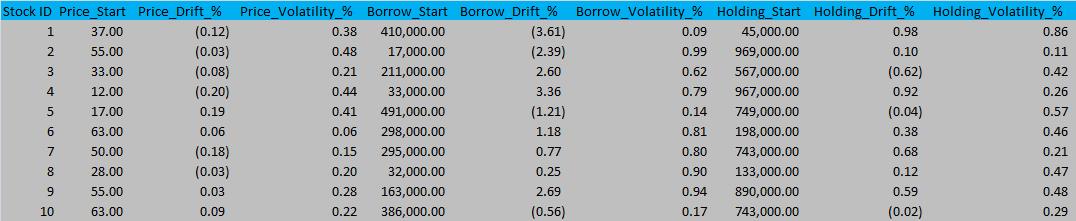

As noted earlier in section 4.1, given the number of random variables involved and the complexity of the system, the computational infrastructure required to value an exclusive can be tremendous. A typical exclusive portfolio can have anywhere from a few hundred to upwards of a thousand different securities. It is therefore simpler to use the historical time series and calculate the valuation from the corresponding formula derived in section 4.5. To demonstrate numerical results we simulate the historical time series. We pick a sample portfolio with one hundred different hypothetical securities and we come up with the time series of all the variables involved (Price, Quantity Borrowed, Exclusive Holding, Inventory Level, Loan Rate, Alternate Loan Rate) by sampling from suitable log normal distributions. It is worth noting that the mean and standard deviation of each time series are themselves simulations from other appropriately chosen uniform distributions (Figure 6). The locate process can be modeled as a Poisson distribution with appropriately chosen units. Though we consider the simpler alternative by letting it be the absolute value of a normal distribution as justified in section 4.1. The mean and standard deviation of the locate distribution for each security are chosen from another appropriately chosen uniform distribution.

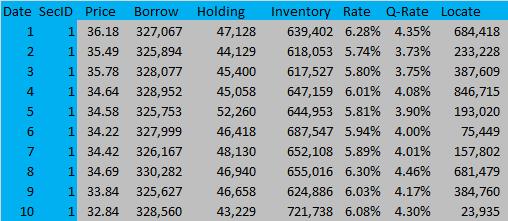

The simulation seed is chosen so that the drift and volatility we get for the variables (mean and standard deviation for the locate process) are similar to what would be observed in practice. For example in Figure 6, the price and rate volatility are lower than the volatilities of the borrow and other quantities, which tend to be much higher; the range of the drift for the quantities is also higher as compared to the drift range of prices and rates. This ensures that we are keeping it as close to a realistic setting as possible, without having access to the historical time series. The volatility and drift of the variables for each security are shown in Figure 7. The length of the simulated time series is one year or 252 trading days for each security. A sample of the time series of the variables generated using the simulated drift and volatility parameters is shown in Figure 8. The full time series used for the calculations is available upon request.

6.2 Model Testing Results

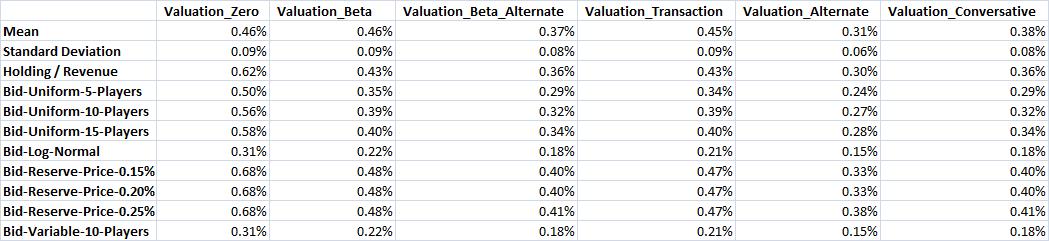

To summarize the results of the testing we show the summary statistics and the matrix of portfolio valuations under different valuation criteria and auction settings in (Figure 9). The columns from one to six denote the following valuations respectively. The first and second rows are the mean and standard deviation of the daily valuations. The third row indicates the valuation over the entire time period under consideration. The fourth, fifth and sixth row indicate the valuations when the valuations of the other bidders are distributed uniformly and there are 5,10 or 15 other bidders respectively. The seventh row indicates the log-normal assumption for the valuations of the other bidders. The eight, ninth and tenth rows are when there are reserve prices set by the auction seller of 15, 20 and 25 basis points respectively with ten other bidders. The eleventh row indicates the case when we have uncertainty about the number of bidders and a total of ten bidders are distributed according to the discrete symmetric distribution in (Figure 5).

We see that the valuation ranges from 30 to 50 basis points under different valuation schemes. The exclusive holding value varies between 1 billion to 2 billion over the time period under consideration. We have not considered currency rates for simplicity, but a real portfolio could hold securities traded in different currencies introducing foreign exchange rate uncertainty into the mix. When we repeat the simulations with different seed values, the results could vary outside this range, but are not drastically different. The combined valuation based on the result in theorem 1 is around 34 basis points. This shows that the valuation with the lowest variance, which is 30 basis points (Valuation_Alternate: third row, fifth column in Figure 9) has a greater influence on the combined valuation due to its higher weight in the aggregation. This makes practical sense since a valuation with lesser variance will provide more stable revenue streams. We have not provided the auction bidding strategies based on this combined valuation, but these can be easily calculated if someone wishes to proceed down that route.

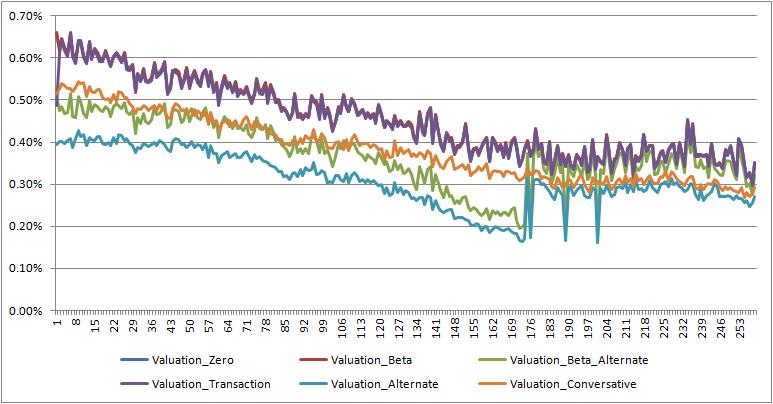

We easily verify some results well known in the auction literature (Krishna 2009): 1) As the number of bidders bidding uniformly increases, the bid increases; 2) Setting a reserve price results in higher bids. The bid with a discrete symmetric distribution as the number of bidders goes higher is comparable to the crude theoretical approximation for the log normal distribution, which does not depend on the number of bidders (Corollary 2). The Comparative Statics of the valuation with changes in Beta are shown in Figures 10. As the subjective discount factor decreases, the valuation increases since the effect of the discounting is higher on the holding levels than on the revenue. A time series graph of the different valuations are shown in Figure 11. We have successfully utilized the heuristic expression for the valuation of exclusives using real historical data in making auction bids. As compared to the sample numbers shown here with simulated data, when the historical observations are used we get somewhat similar results.

7 Improvements to the Model

Numerous improvements to the model are possible. (Cobb, Rumi & Salmerón 2012; and Nie & Chen 2007) derive approximate distributions for the sum of log normal distribution which highlight that we can estimate the log normal parameters from the time series of the valuations and hence get the mean and variance of the valuations. A longer historical time series will help to get better estimates for the volatility of the valuation. This can be useful to decide the aggressiveness of the bid. Another key extension can be to introduce jumps in the stochastic processes. This is seen in stock prices to a certain extent and to a greater extent in the borrow, holding and inventory processes.

We have assumed that the stochastic processes governing the stocks in the exclusive portfolio, the loan rates, the number of shares available internally, as well as the number of shares available for loan from other external borrowers are all independent. A more realistic assumption of positive correlations between some of these processes would make the results more realistic and appealing. Such a modification can be incorporated into our framework but would require non trivial alternations to the equations and numerical computations (Heston 1993; Oksendal 2013).

A key extension can be to introduce jumps in the stochastic processes (Merton 1976; Kou 2002). This is seen in stock prices to a certain extent (Yan 2011) and to a greater extent in the borrow, exclusive holdings, availability and inventory processes. Another improvement would be to use stochastic volatility for the stock prices (Hagan, Kumar, Lesniewski & Woodward 2002).

The auction theory aspects combine standard results with new extensions (Kashyap 2018) for the log-normal case, the interdependent case and a combined realistic setting with uniform distributions. Instead of the bidding strategies we have considered, we can come up with a parametric model that will take the valuations as the inputs and the bid as output. The parameters can depend on the size of the portfolio, the number of securities, the number of special securities, the number of markets, the extent of overlap with the internal inventory, and where available, the percentile rankings of the historical bids for previous auctions, which auction sellers do reveal sometimes.

A significant amount of theoretical work could be pursued related to the variance weighted combination of the valuations (section 4.6). In our example, we have considered valuations over the same time horizon for the same portfolio. But extensions could look into combining valuations or forecasts which are done over multiple horizons and even across multiple objects with similar characteristics.

A key open question is to decide which of the valuations to use for the bidding strategy if we do not opt to combine them based on our variance weighting (section 4.6). This aspect will require views on how the loan rates might evolve and which securities in the exclusive pool will stay special or might become special, and hence can be used to pick either a more aggressive or a less aggressive valuation. In a subsequent paper (Kashyap 2016), we will look at how we can systematically try and establish expectations on loan rates and which securities might become harder to borrow and hence have higher profit margins on the loans. The locate conversion ratio can also be the result of profit maximization when the Knapsack algorithm (Martello & Toth 1987) is used to allocate the locates.

8 Conclusion

We have looked at methodologies to value securities portfolios from a securities lending perspective. The weighting scheme we have used to combine multiple valuations can be useful in any situation where multiple forecasts are made and we need a methodology to combine them. We have derived conditions under which our alternative weighting scheme converges faster to the true valuation when compared to the minimum variance weighting. We have then looked at various bidding strategies that would be relevant to an exclusive auction. From a related paper (Kashyap 2018), we have used closed form solutions where such a formulation exists and in situations where approximations and numerical solutions are required we have utilized those. The paper presents a theoretical foundation supplemented with numerical results for a largely unexplored financial business. The results from the simulation confirm the complexity inherent in the system, but point out that the heuristics we have used can be a practical tool for bidders and auction sellers to maximize their profits. The models developed here could be potentially useful for inventory estimation and for wholesale procurement of financial instruments and also non-financial commodities.

9 Acknowledgments and End-notes

-

1.

Dr. Yong Wang, Dr. Isabel Yan, Dr. Vikas Kakkar, Dr. Fred Kwan, Dr. William Case, Dr. Srikant Marakani, Dr. Qiang Zhang, Dr. Costel Andonie, Dr. Jeff Hong, Dr. Guangwu Liu, Dr. Andrew Chan, Dr. Humphrey Tung and Dr. Xu Han at the City University of Hong Kong provided advice and more importantly encouragement to explore and where possible apply cross disciplinary techniques. The faculty members of SolBridge International School of Business provided patient guidance and valuable suggestions on how to further this paper.

-

2.

Numerous seminar participants, particularly at a few meetings of the econometric society and various finance organizations, provided helpful suggestions. The views and opinions expressed in this article, along with any mistakes, are mine alone and do not necessarily reflect the official policy or position of either of my affiliations or any other agency.

-

3.

“An Introduction to Securities Lending” by Mark C Faulkner, which may be downloaded at www.spitalfieldsadvisors.com, was commissioned by the UK Securities Lending and Repo Committee, the International Securities Lending Association, the London Stock Exchange, the London Investment Banking Association, the British Bankers’ Association and the UK Association of Corporate Treasurers and was welcomed by the National Association of Pension Funds and the Association of British Insurers. It was first published in 2004.(Securities Lending One)

-

4.

“An Introduction to Securities Lending (Australia)” is the Australian adaptation of the UK publication focused on the UK markets, entitled “An Introduction to Securities Lending” by Mark C Faulkner in (End-note 3). This adaptation was commissioned by the Australian Securities Lending Association Limited (ASLA). (Securities Lending Two)

-

5.

The value of available inventory as of June 22, 2015, stands at $13.22 trillion, according to a new info-graphic on the global securities finance market from DataLend. Of the available inventory worldwide, $1.72 trillion was out on loan. The value of equity on loan was $851 billion, while fixed income on loan stood at $876 billion. Some 41,673 unique securities were out loan, according to the info-graphic, yielding an estimated gross revenue of $19.2 million per day on average, which equates to $2.26 billion for the first half of 2015. The US is still the largest market with $954 billion out on loan as of 22 June. Canada is the closest market in size, with an estimated $131 billion of securities out on loan. Despite its size, the US commands a fee of 38 basis points (volume-weighted average, year to date), whereas Hong Kong, which has $28.8 billion out on loan, yields fees of 210 basis points. (Securites Lending Three)

-

6.

As the potential risks of securities lending are discussed and debated by the Financial Stability Oversight Council (FSOC), the U.S. Treasury’s Office of Financial Research (OFR), and the Financial Stability Board (FSB), it is important to try to understand both the overall size of the securities lending market and the share of it attributable to different participants. Based on one estimate from the FSOC the percentage is typically around these values (Retirement and Pension, Mutual Funds, Endowments, Insurance: 50%, 35%, 8%, 6%). (Securites Lending Four).

-

7.

Despite the several advances in the social sciences and in particular economic and financial theory, we have yet to discover an objective measuring stick of value, a so called, True Value Theory. While some would compare the search for such a theory, to the medieval alchemist’s obsession with turning everything into gold, for our present purposes, the lack of such an objective measure means that the difference in value as assessed by different participants can effect a transfer of wealth. This forms the core principle that governs all commerce that is not for immediate consumption in general, and also applies specifically to all investment related traffic which forms a great portion of the financial services industry. Although, some of this is true for consumption assets; because the consumption ability of individuals and organizations is limited and their investment ability is not, the lack of an objective measure of value affects investment assets in a greater way and hence investment assets and related transactions form a much greater proportion of the financial services industry. Consumption assets do not get bought and sold, to an inordinate extent, due to fluctuating prices, whereas investment assets will.

-

8.