Karhunen–Loève expansions of Lévy processes

Abstract

Karhunen–Loève expansions (KLE) of stochastic processes are important tools in mathematics, the sciences, economics, and engineering. However, the KLE is primarily useful for those processes for which we can identify the necessary components, i.e., a set of basis functions, and the distribution of an associated set of stochastic coefficients. Our ability to derive these components explicitly is limited to a handful processes. In this paper we derive all the necessary elements to implement the KLE for a square-integrable Lévy process. We show that the eigenfunctions are sine functions, identical to those found in the expansion of a Wiener process. Further, we show that stochastic coefficients have a jointly infinitely divisible distribution, and we derive the generating triple of the first coefficients. We also show, that, in contrast to the case of the Wiener process, the coefficients are not independent unless the process has no jumps. Despite this, we develop a series representation of the coefficients which allows for simulation of any process with a strictly positive Lévy density. We implement our theoretical results by simulating the KLE of a variance gamma process.

1 Introduction

Fourier series are powerful tools in mathematics and many other fields. The Karhunen-Loève theorem (KLT) allows us to create generalized Fourier series from stochastic processes in an, in some sense, optimal way. Arguably the most famous application of the KLT is to derive the classic sine series expansion of a Wiener process on . Specifically,

| (1.1) |

where convergence of the series is in and uniform in , and the are i.i.d. standard normal random variables. The main result of this paper is to show that a square integrable Lévy process admits a similar representation as a series of sine functions; the key difference is that the stochastic coefficients are no longer normal nor independent.

The KLT applies much more generally and is thus an important tool in many fields. For example, we see applications of the KLT and Principal Component Analysis, its discrete time counterpart, in physics and engineering [8, 19], [16, Chapter 10], in signal and image processing [26], [7, Chapter 1], in finance and economics [2, 5, 13] and other areas. For interesting recent theses on the KLT from three different points of view see also [10] (probability and time series), [15, Chapter 7] (stochastic partial differential equations), and [27] (statistics).

Deriving the Karhunen–Lòeve expansion (KLE) of the type (1.1) for a square integrable stochastic process on requires two steps: first, one must solve a Fredholm integral equation to obtain the basis functions (c.f. the sine functions in Equation 1.1). Second, one must identify the distribution of the stochastic coefficients

| (1.2) |

In general, obtaining both the basis functions and the distribution of the stochastic coefficients is not an easy task, and we have full knowledge in only a few specific cases. Besides the Wiener process, the Brownian Bridge process, the Anderson–Darling process, and spherical fractional Brownian Motion (see [9] for the latter) are some examples. For further examples with derivation see [10, Chapter 1]. Non-Gaussian processes pose an additional challenge and the problem of deriving the KLE is usually left to numerical means (see e.g., [19]).

In this paper we derive all the elements of the KLE for a square integrable Lévy process on the interval . The result is timely since in many of the fields mentioned above, especially in finance, but recently also in the area of image/signal processing (see e.g., [25]), Lévy models are becoming increasingly popular. In Section 3 we show that the basis functions are sine functions, identical to those in (1.1), and that the first stochastic coefficients are jointly distributed like an infinitely divisible (ID) random vector. We identify the generating triple of this vector from which it follows that the coefficients are independent only when the process has no jumps, i.e., when the process is a scaled Wiener process with drift. Although simulating dependent multivariate random variables from a characteristic function is generally difficult, in Section 4 we derive a shot-noise (series) representation for

| (1.3) |

for those processes which admit a strictly positive Lévy density. This result, in theory, allows us to simulate the truncated KLE for a large class of Lévy models. We conclude by generating some paths of a -term KLE approximation of a variance gamma process.

To begin, we recall the necessary facts from the theory of Lévy processes and ID random vectors.

2 Facts from the theory of Lévy processes

The Lévy-Khintchine theorem states that every -dimensional ID random vector has a Fourier transform of the form

where

| (2.1) |

and where , is a positive semi-definite matrix, and is a measure on satisfying

| (2.2) |

The function is known as the cut-off function; in general, we need such a function to ensure convergence of the integral. An important fact is that up to a choice of , the generating triple uniquely identifies the distribution of . The Lévy-Khintchine theorem for Lévy processes gives us an analogously powerful result, specifically, for any -dimensional Lévy process we have

where is as in (2.1) and is uniquely determined, up to identity in distribution, by the triple . Following convention, we will refer to the function as the characteristic exponent of (resp. ) and will write (resp. ) if there is the potential for ambiguity. In one dimension we will write for the generating triple; the measure will always be referred to as the Lévy measure. When for some density function , we will write and refer to as the Lévy density. If we wish to be specific regarding the cut-off function we will write or for the generating triples.

In this article we will work primarily with one dimensional Lévy processes having zero mean and finite second moment; by this we mean that and for every . We will denote the set of all such Lévy processes by . One may show that the later condition implies that is twice differentiable. Thus, when we work with a process , we can express the variance of as

and the covariance of and as

For notational convenience we will set .

The existence of moments for both Lévy processes and ID random vectors can be equivalently expressed in terms of the Lévy measure. An ID random vector or Lévy process with associated Lévy measure has a finite second moment (meaning the component-wise moments) if, and only if,

| (Condition A) |

We will denote the class of ID random vectors with zero first moment and finite second moment by . The subset of which also satisfies

| (Condition B) |

will be denoted and will denote the analogous subset of . We remark that any (resp. ) necessarily has a representation of the form (resp. ). Additionally, any -dimensional necessarily has representation where has entries

and is the projection onto the -th component. Analogously, if then we have representation where .

3 The Karhunen–Loève theorem

Given a real valued continuous time stochastic process defined on an interval and an orthonormal basis for we might try to express as a generalized Fourier series

| (3.1) |

In this section, our chosen basis will be derived from the eigenfunctions corresponding to the non-zero eigenvalues of the integral operator ,

When the covariance satisfies a continuity condition it is known (see for example [8] Section 2.3.3) that the normalized set of eigenfunctions of is countable and forms a basis for . When we choose this basis in (3.1) we adopt the special notation for the stochastic coefficients. In this case, the expansion is optimal in a number of ways. Specifically, we have:

Theorem 1 (The Karhunen-Loève Theorem).

Let be a real valued continuous time stochastic process on such that and let and for each . Further, suppose is continuous on .

-

(i)

Then,

uniformly for . Additionally, the random variables are uncorrelated and satisfy and .

-

(ii)

For any other basis of , with corresponding stochastic coefficients , and any , we have

where and are the remainders and .

Going forward we assume the order of the eigenvalues, eigenfunctions, and the stochastic coefficients is determined according to .

According to Ghanem and Spanos [8] the Karhunen-Loève theorem was proposed independently by Karhunen [12], Loève [14], and Kac and Siegert [11]. Modern proofs of the first part of the theorem can be found in [1] and [8] and the second part – the optimality of the truncated approximation – is also proven in [8]. A concise and readable overview of this theory is given in [15, Chapter 7.1].

We see that although the KLT is quite general, it is best applied in practice when can determine the three components necessary for a Karhunen-Loéve expansion: the eigenfunctions ; the eigenvalues ; and the distribution of the stochastic coefficients . If we wish to use the KLE for simulation then we need even more: We also need to know how to simulate the random vector which, in general, has uncorrelated but not necessarily independent components.

For Gaussian processes, the second obstacle is removed, since one can show that the are again Gaussian, and therefore independent. There are, of course, many ways to simulate a vector of independent Gaussian random variables. For a process , the matter is slightly more complicated as we establish in Theorem 2. However, since the covariance function of a process differs from that of a Wiener process only by the scaling factor , the method for determining the eigenfunctions and the eigenvalues for a Lévy process is identical to that employed for a Wiener process. Therefore, we omit the proof of the following proposition, and direct the reader to [1, pg. 41] where the proof for the Wiener process is given.

Proposition 1.

The eigenvalues and associated eigenfunctions of the operator defined on with respect to are given by

| (3.2) |

A nice consequence of Proposition 1 and Theorem 1 is that it allows us to estimate the amount of total variance we capture when we represent our process by a truncated KLE. Using the orthogonality of the , and the fact that for each , it is straightforward to show that the total variance satisfies . Therefore, the total variance explained by a -term approximation is

By simply computing the quantity on the right we find that the first 2, 5 and 21 terms already explain , , and of the total variance of the process. Additionally, we see that this estimate holds for all independently of or .

The following lemma is the important first step in identifying the joint distribution of the stochastic coefficients of the KLE for . The reader should note, however, that the lemma applies to more general Lévy processes, and is not just restricted to the set .

Lemma 1.

Let be a Lévy process and let be a collection of functions which are in . Then the vector consisting of elements

has an ID distribution with characteristic exponent

| (3.3) |

where is the function with -th component , .

Remark 1.

With Lemma 1 and Proposition 1 in hand, we come to our first main result. In the following theorem we identify the generating triple of the vector containing the first stochastic coefficients of the KLE for a process . Although it follows that has dependent entries (see Corollary 2), Theorem 2, and in particular the form of the Lévy measure , will also be the key to simulating . Going forward we use the notation for the Borel sigma algebra on the topological space .

Theorem 2.

If with generating triple then with generating triple

where

is a diagonal matrix with entries

| (3.4) |

and is the measure,

| (3.5) |

where is the Lebesgue measure on and is the function

| (3.6) |

Proof.

We substitute the formula for the characteristic exponent (Formula 2.1 with and ) and the eigenfunctions (Formula 3.2) into (3.3) and carry out the integration. Then (3.4) follows from the fact that

and that the are therefore also orthogonal on .

Next we note that is a continuous function from to and is therefore measurable. Therefore, is nothing other than the push forward measure obtained from and ; in particular, it is a well-defined measure on . It is also a Lévy measure that satisfies Condition A since

| (3.7) |

where the final inequality follows from the fact that . Applying Fubini’s theorem and a change of variables, i.e.,

concludes the proof of infinite divisibility. Finally, noting that

shows that .

Remark 2.

We gather some fairly obvious but important consequences of Theorem 2 in the following corollary.

Corollary 1.

Proof.

(i) Since

and Condition A is satisfied by both and it follows that Condition B is satisfied for if, and only if, it is satisfied for . Formula 3.8 then follows from the fact that

(ii) Straightforward from the definition of in Theorem 2.

Also intuitively obvious, but slightly more difficult to establish rigorously, is the fact that the entries of are dependent unless .

Corollary 2.

If then has independent entries if, and only if, is the zero measure.

To prove Corollary 2 we use the fact that a -dimensional ID random vector with generating triple has independent entries if, and only if, is supported on the union of the coordinate axes and is diagonal (see E 12.10 on page 67 in [23]). For this purpose we define, for a vector such that , the sets

where we caution the reader that the symbol indicates the Cartesian product and not the Lévy measure of .

In the proof below, and throughout the remainder of the paper, will always refer to the function defined in (3.6), and to the -th coordinate of .

Proof of Corollary 2.

() The assumption implies our process is a scaled Wiener process in which case it is well established that has independent entries. Alternatively, this follows directly the fact that the matrix in Theorem 2 is diagonal.

() We assume that is not identically zero and show that there exists such that either or is strictly greater than zero.

Since there must exist such that one of and is strictly greater than zero; we will initially assume the latter. We observe that for , , the zeros of the function defined by

occur at points , and therefore the smallest zero is . From the fact that the cosine function is positive and decreasing on we may conclude that

where . Now, let be the vector with entries for . Then,

since for we have

But then,

| (3.9) |

If we had initially assumed that we would have reached the same conclusion by using the interval and . We conclude that is not supported on the union of the coordinate axes, and so does not have independent entries.

4 Shot-noise representation of

Although we have characterized the distribution of our stochastic coefficients we are faced with the problem of simulating a random vector with dependent entries with only the knowledge of the characteristic function. In general, this seems to be a difficult problem, even generating random variables from the characteristic function is not straightforward (see for example [6]). In our case, thanks to Theorem 2 we know that is infinitely divisible and that the Lévy measure has a special disintegrated form. This will help us build the connection with the so-called shot-noise representation of our vector . The goal is to represent as an almost surely convergent series of random vectors.

To explain this theory – nicely developed and explained in [20, 21] – we assume that we have two random sequences and which are independent of each other and defined on a common probability space. We assume that each is distributed like a sum of independent exponential random variables with mean 1, and that the take values in a measurable space , and are i.i.d. with common distribution . Further, we assume we have a measurable function which we use to define the random sum

| (4.1) |

and the measure

| (4.2) |

The function is defined by

| (4.3) |

where, as before, is the projection onto the -th component. The connection between (4.1) and ID random vectors is then explained in the following theorem whose results can be obtained by restricting Theorems 3.1, 3.2, and 3.4 in [20] from a general Banach space setting to .

Theorem 3 (Theorems 3.1, 3.2, and 3.4 in [20]).

Suppose is a Lévy measure, then:

-

(i)

If Condition B holds then converges almost surely to an ID random vector with generating triple as .

-

(ii)

If Condition A holds, and for each the function is non increasing, then

(4.4) converges almost surely to an ID random vector with generating triple .

The name “shot-noise representation” comes from the idea that can be interpreted as a model for the volume of the noise of a shot that occurred seconds ago. If is non increasing in the first variable, as we assume in case (ii) in Theorem 3, then the volume decreases as the elapsed time grows. The series can be interpreted as the total noise at the present time of all previous shots.

The goal is to show that for any process in whose Lévy measure admits a strictly positive density , the vector has a shot-noise representation of the form (4.1) or (4.4). To simplify notation we make some elementary but necessary observations/assumptions: First, we assume that has no Gaussian component . There is no loss of generality to this assumption, since if does have a Gaussian component then changes by the addition of a vector of independent Gaussian random variables. This poses no issue from a simulation standpoint. Second, from (2.1) we see that any Lévy process with representation , can be decomposed into the difference of two independent Lévy processes, each having only positive jumps. Indeed, splitting the integral and making a change of variable gives

| (4.5) |

where (resp. ) has Lévy density (resp. ) restricted to . In light of this observation, the results of Theorem 4 are limited to Lévy processes with positive jumps. It should be understood that for a general process we can obtain by simulating and – corresponding to and respectively – and then subtracting the second from the first to obtain a realization of .

Last, for a Lévy process with positive jumps and strictly positive Lévy density , we define the function

| (4.6) |

which is just the tail integral of the Lévy measure. We see that is strictly monotonically decreasing to zero, and so admits a strictly monotonically decreasing inverse on the domain .

Theorem 4.

Let be a strictly positive Lévy density on and identically zero elsewhere.

- (i)

-

(ii)

If with generating triple , then has a shot noise representation

(4.9) where and are as in Part and is defined as in (4.3).

Proof.

Rewriting (3.5) to suit our assumptions and making a change of variables gives, for any

Making a further change of variables gives

Since , so that , we may conclude that

From the definition of the function (Formula 3.6), and that of , it is clear that

| (4.10) |

is measurable and non increasing in absolute value for any fixed . Therefore, we can identify (4.10) with the function , the uniform distribution on with , and with . The results then follow by applying the results of Theorems 2 and 3 and Corollary 1.

Going forward we will write simply where it is understood that vanishes outside the interval .

Discussion

There are two fairly obvious difficulties with the series representations of Theorem 4. The first – this a common problem for all series representations of ID random variables when the Lévy measure is not finite – is that we have to truncate the series when (equivalently ). Besides the fact that in these cases our method fails to be exact, computation time may become an issue if the series converge too slowly. The second issue is that is generally not known in closed form. Thus, in order to apply the method we will need a function that is amenable to accurate and fast numerical inversion. In the survey [20] Rosiński reviews several methods, which depend on various properties of the Lévy measure (for example, absolute continuity with respect to a probability distribution), that avoid this inversion. In a subsequent paper [22] he develops special methods for the family of tempered -stable distributions that also do not require inversion of the tail of the Lévy measure. We have made no attempt to adapt these techniques here, as the fall outside of the scope of this paper. However, this seems to be a promising area for further research.

A nice feature of simulating a -dimensional KLE of a Lévy process via Theorem 4 is that we may increase the dimension incrementally. That is, having simulated a path of the -term KLE approximation of ,

| (4.11) |

we may derive a path of directly from as opposed to starting a fresh simulation. We observe that a realization of can be computed individually once we have the realizations of . Specifically,

when Condition B holds, with an analogous expression when it does not. Thus, if is our realization of we get a realization of via .

It is also worthwhile to compare the series representations for Lévy processes found in [20] and the proposed method. As an example, suppose we have a subordinator with a strictly positive Lévy density . Then, it is also true that

| (4.12) |

The key difference between the approaches, is that the series in (4.12) depends on , whereas the series representation of is independent of . Therefore, in (4.12) we have to recalculate the series for each , adding those summands for which . Of course, the random variables need to be generated only once. On the other hand, while we have to simulate only once for all , each summand requires the evaluation of cosine functions, and for each we have to evaluate sine functions when we form the KLE. However, since there is no more randomness once we have generated the second computation can be done in advance.

Example

Consider the Variance Gamma (VG) process which was first introduced in [17] and has since become a popular model in finance. The process can be constructed as the difference of two independent Gamma processes, i.e., processes with Lévy measures of the form

| (4.13) |

where . For this example we use a Gamma process with parameters and and subtract a Gamma process with parameters and to yield a VG process . Assuming no Gaussian component or additional linear drift, it can be shown (see Proposition 4.2 in [24]) that the characteristic exponent of is then

We observe that since

However, this is not a problem, since we can always construct processes by subtracting and from and respectively. We then generate the KLE of and add back to the result, and apply the analogous procedure for . This is true generally as well, i.e., for a square integrable Lévy process with expectation we can always construct a process by simply subtracting the expectation .

From (4.13) we see that the function will have the form

where is the exponential integral function. Therefore,

There are many routines available to compute ; we choose a Fortran implementation to create a lookup table for with domain . We discretize this domain into unevenly spaced points, such that the distance between two adjacent points is no more than 0.00231. Then we use polynomial interpolation between points.

When simulating we truncate the series (4.7) when ; at this point we have . Using the fact that the are nothing other than the waiting times of a Poisson process with intensity one, we estimate that we need to generate on average random variables to simulate and similarly for . We remark that for the chosen process both the decay and computation of are manageable.

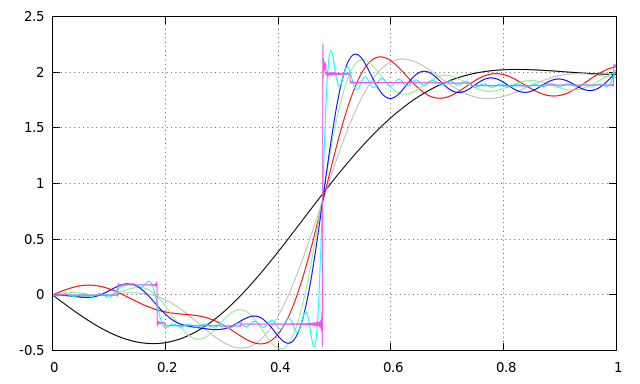

We simulate sample paths of for using the described approach. We also compute a Monte Carlo (MC) approximation of the expectation of by averaging over sample paths of the -term approximation. Some sample paths and the results of the MC simulation are depicted in Figure 1, where the colors black, grey, red, green, blue, cyan, and magenta correspond to equal to 5, 10, 15, 20, 25, 100, and 3000 respectively.

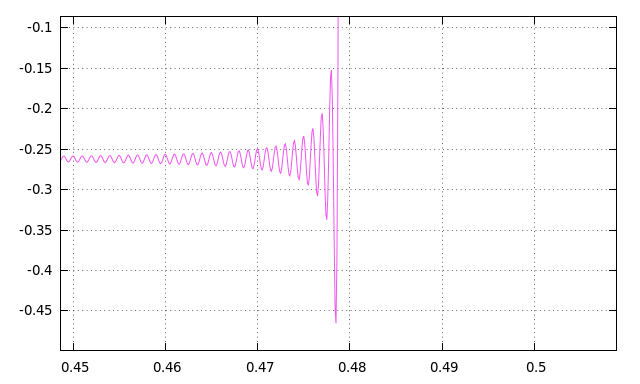

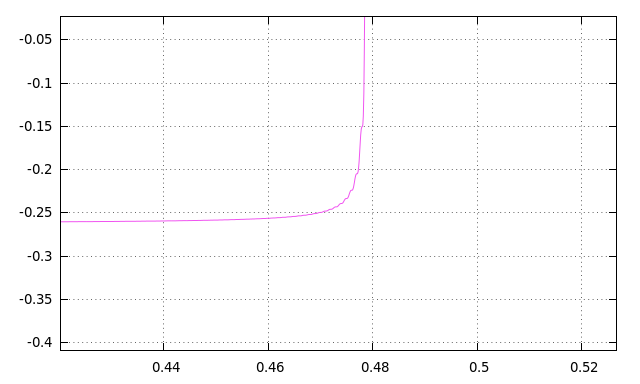

In Figure 1a we show the sample paths resulting from a simulation of . We notice that the numerical results correspond with the discussion of Section 3: the large movements of the sample path are already captured by the 5-term approximation. We also notice peaks resulting from rapid oscillations before the bigger “jumps” in the higher term approximations. This behaviour is magnified for the 3000-term approximation in Figure 1b. In classical Fourier analysis this is referred to as the Gibbs phenomenon; the solution in that setting is to replace the partial sums by Cesàro sums. We can employ the same technique here, replacing with , which is defined by

It is relatively straightforward to show that converges to in the same manner as (as described in Theorem 1 (i)). In Figure 1c we show the effect of replacing with on all sample paths, and in Figure 1d we show the approximation – now the Gibbs phenomenon is no longer apparent.

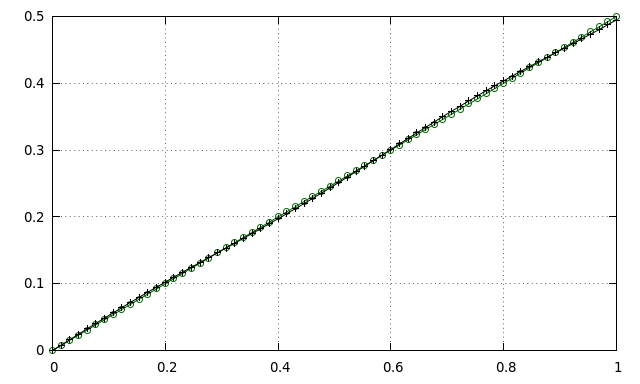

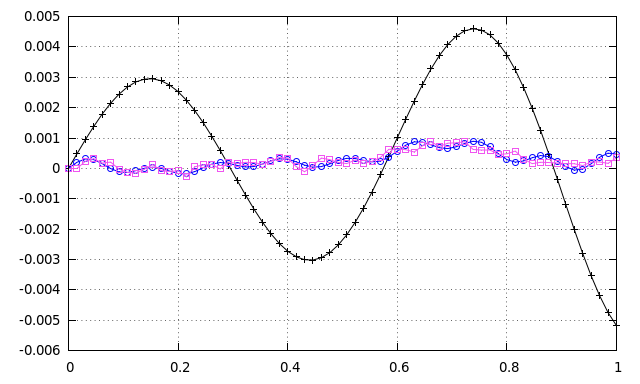

In Figure 1e we show the MC simulation of (black +) plotted together with (green ). We see the 5-term KLE already gives a very good approximation. In Figure 1f we also show the errors for (black +), (blue ), and (magenta ). Again we have agreement with the discussion in Section 3: little is gained in our MC approximation of by choosing a KLE with more than 25 terms. Recall that a KLE with 25 terms already captures more than 99% of the total variance of the given process.

(d) Mitigated Gibbs phen. (e) and MC sim. of (f) MC Err.

Author’s acknowledgements

My work is supported by the Austrian Science Fund (FWF) under the project F5508-N26, which is part of the Special Research Program “Quasi-Monte Carlo Methods: Theory and Applications”. I would like to thank Jean Bertoin for explaining his results in [3] to me. This helped me extend identity (3.3) of Lemma 1 from functions to functions. Further I would like to thank Alexey Kuznetsov and Gunther Leobacher for reading a draft of this paper and offering helpful suggestions.

Appendix A Additional proof

Proof of Lemma 1.

We give a proof for continuously differentiable first and then prove the general case. Accordingly, we fix , a collection of continuously differentiable defined on , and a Lévy process with state space . Instead of proving identity (3.3) directly for we will prove that

| (A.1) |

where is the process defined by and is the vector with entries

It is clear that is a Lévy process, that , and that (3.3) corresponds to the special case . We focus on this more general result because it will lead directly to a proof of infinite divisibility. We begin by defining

| (A.2) |

which are -point, right-endpoint Riemann sum approximations of the random variables . By the usual telescoping sum technique for Lévy processes we can write

where the random variables are independent and each distributed like . This allows us to rearrange the sum according to the random variables , gathering together those with the same index. Therefore, we have

We notice that the term in brackets on the right-hand side is a -point, right-endpoint Riemann sum approximation for the integral of over the interval . Let us therefore define

| (A.3) |

as well as the -dimensional vectors and consisting of entries and respectively. We observe that

| (A.4) |

where we have used the dominated convergence theorem to obtain the first equality, and the independence of the to obtain the final equality. Further, we get

by using the left-endpoint Riemann sums. We note that uniformly in since

| (A.5) |

where the last estimate follows from the well-known error bound for the absolute difference between an -point, right end-point Riemann sum and the integral of a function over . Then, by the continuity of , for any we may choose an appropriately large such that

This proves (A.1) and therefore also (3.3) for functions.

To establish the infinite divisibility of we note that (A.1) shows that and that is therefore a positive definite function for every since it is the characteristic function of the random vector . Positive definiteness follows from Bochner’s Theorem (see for example Theorem 2.13 in [4]). Also, we clearly have since . By Theorem 2.15 in [4] these two points combined show that is the characteristic exponent of an ID probability distribution, and hence is an ID random vector.

Now one can extend the lemma to functions by exploiting the density of in . In particular, for each we can find a sequence of functions which converges in to . Then,

showing that uniformly in . This shows that for each the functions , with , are uniformly bounded on , so that the dominated convergence theorem applies and we have

| (A.6) |

On the other hand, is a.s. bounded on , so that

a.s.. Therefore converges a.s. and consequently also in distribution to . Together with (A.6), this implies that for each

| (A.7) |

Therefore, (3.3) is also proven for functions in . Since each has an ID distribution Lemma 3.1.6 in [18] guarantees that is also an ID random vector.

References

- [1] R.B. Ash and M.F. Gardner. Topics in stochastic process. Academic Press, New York–San Francisco–London, 1975.

- [2] M. Benko. Functional data analysis with applications in finance. PhD thesis, Humbolt–Universistät zu Berlin, 2006.

- [3] J. Bertoin. Some elements on Lévy processes. In C.R. Rao and D.N. Shanghag, editors, Stochastic Processes: Theory and Methods. Elsevier Science B.V., Amsterdam, The Netherlands, 2001.

- [4] B. Böttcher, J. Wang, and R. Schilling. Lévy matters III. Lévy-type processes: Construction, approximation and sample path properties. Springer, Berlin–Heidelberg–New York–London–Paris–Tokyo–Hong Kong–Barcelona–Budapest, 2013.

- [5] R. Cont and J. Da Fonseca. Dynamics of implied volatility surfaces. Quantitative finance, 2(1):45–60, 2002.

- [6] L. Devroye. An automated method for generating random variates with a given characteristic function. Siam J. Appl. Math., 46(4):698–719, 1986.

- [7] R.D. Dony. Karhunen–Loève Transform. In K.R. Rao and P.C. Yip, editors, The transform and data compression handbook. CRC Press., Boca Raton, U.S.A., 2001.

- [8] R. G. Ghanem and P.D. Spanos. Stochastic finite elements: A spectral approach. Springer–Verlag, New York–Berlin–Heidelberg–London–Paris–Tokyo–Hong Kong–Barcelona, 1991.

- [9] J. Istas. Karhunen–Loève expansion of spherical fractional brownian motions. Statistics and Probability Letters, 76(14):1578 – 1583, 2006.

- [10] S. Jin. Gaussian processes: Karhunen–Loève expansion, small ball estimates and applications in time series modes. PhD thesis, University of Delaware, 2014.

- [11] M. Kac and A.J.F. Siegert. An explicit representation of a stationary Gaussian process. Ann. Math. Stat., 18:438–442, 1947.

- [12] K. Karhunen. Über lineare Methoden in der Wahrscheinlichkeitsrechnung. Amer. Acad. Sc. Fennicade, Ser. A, I, 37:3–79, 1947.

- [13] G. Leobacher. Stratified sampling and quasi-Monte Carlo simulation of Lévy processes. Monte-Carlo methods and applications, 12(3–4):231–238, 2006.

- [14] M. Loéve. Fonctions aleatoires du second ordre. In P. Lévy, editor, Processus stochastic et mouvement Brownien. Gauthier Villars, Paris, 1948.

- [15] W. Luo. Wiener chaos expansion and numerical solutions of stochastic partial differential equations. PhD thesis, California Institute of Technology, 2006.

- [16] C. Maccone. Deep space flight and communications. Springer–Praxis, Berlin–Chichester, 2009.

- [17] D.B. Madan and E. Seneta. The variance gamma (v.g.) model for share market returns. The Journal of Business, 63(4):511–524, 1990.

- [18] M. M. Meerschaert and H. Scheffler. Limit distributions for sums of independent random vectors: Heavy tails in theory and practice. John Wiley & Sons, Inc., New York, 2001.

- [19] K.K. Phoon, Huang H.W., and S.T. Quek. Simulation of strongly non-Gaussian processes using Karhunen–Loeve expansion. Probabilistic Engineering Mechanics, 20:188–198, 2005.

- [20] J. Rosiński. On series representations of infinitely divisible random vectors. The Annals of Probability, 18(1):405–430, 1990.

- [21] J. Rosiński. Series representations of Lévy processes from the perspective of point processes. In O.E. Barndorff-Nielsen, T. Mikosh, and S. Resnick, editors, Lévy processes: Theory and Applications. Birkhäuser, Boston–Basel–Berlin, 2001.

- [22] J. Rosiński. Tempering stable processes. Stochastic processes and their applications, 117(6):677–707, 2007.

- [23] K. Sato. Lévy procseses and infinitely divisible distributions. Cambridge University Press, Cambridge–New York–Melbourne–Cape Town–Singapore–São Paulo, 1999.

- [24] P. Tankov and R. Cont. Financial Modelling with Jump Processes. Chapman and Hall/CRC, Boca Raton–London–New York–Washington,D.C., 2004.

- [25] M. Unser and P.D. Tafti. An introduction to sparse stochastic processes. Cambridge University Press, Cambridge, 2014.

- [26] M.L. Unser. Wavelets, filterbanks, and the Karhunen-Loeve transform. In Signal Processing Conference (EUSIPCO 1998), 9th European, pages 1–4. IEEE, 1998.

- [27] L. Wang. Karhunen–Loève expansions and their applications. PhD thesis, The London School of Economics, 2008.