MICROSCOPIC MODELS

FOR THE STUDY OF TAXPAYER AUDIT EFFECTS

Abstract - A microscopic dynamic model is here constructed and analyzed, describing the evolution of the income distribution in the presence of taxation and redistribution in a society in which also tax evasion and auditing processes occur. The focus is on effects of enforcement regimes, characterized by different choices of the audited taxpayer fraction and of the penalties imposed to noncompliant individuals. A complex systems perspective is adopted: society is considered as a system composed by a large number of heterogeneous individuals. These are divided into income classes and may as well have different tax evasion behaviors. The variation in time of the number of individuals in each class is described by a system of nonlinear differential equations of the kinetic discretized Boltzmann type involving transition probabilities.

I Introduction

In this paper a microscopic model is constructed and analyzed, suitable to describe the taxation process in a closed market society in conjunction with the occurrence of tax evasion and of some audit procedure. The focus is on effects on the population income distribution caused by different choices of the audited taxpayer fractions and by different subsequent penalties imposed to non-compliant individuals.

As a serious, long-standing problem, tax evasion has been the object of numerous studies. And being a genuinely interdisciplinary issue, it has been looked at from various viewpoints: social, economical, behavioral and psychological aspects have been explored by means of both experimental and theoretical methods. It is however only during the last decades that novel approaches have been developed, allowing the inclusion of more realism in the treatment of the problem. These approaches benefit from a significantly increased computing power and typically involve agent-based modelling and simulations. Their specificity is that they provide the possibility of taking into account the interactions of a large number of heterogeneous individual units. From the whole of these interactions, the emergence of some aggregate pattern can be deduced. Essentially in parallel also alternative approaches to socio-economic questions, which employ concepts and tools from statistical mechanics, have been designed by the physics community. The agent-based methodology and the “econophysics” field share the perspective of a complexity economics. Actually, a clear-cut distinction between the two research lines is not always possible; see 1 for a discussion and a list of references.

Also in this paper a complex system perspective is adopted. Indeed, the emergence of the aggregate pattern represented by the income distribution is obtained as the result of a multiplicity of interactions between single units. These interactions consist of monetary exchanges between pairs of individuals, payment of taxes, redistribution of the tax revenue, and payment of penalties. The approach we follow differs from the agent-based methods and from others in the econophysics literature. It is characterized by its mathematically founded nature. We build on our previous work and introduce a modified version of the model discussed in 2 and 3 (see also 4 and 5 ). Very briefly, we deal with society as with a system composed by a large number of heterogeneous individuals divided into classes which are distinguished by their average income. The mechanism according to which the individuals exchange money, pay taxes and benefit of some revenue redistribution (leaving the total wealth unchanged) is described through a system of nonlinear ordinary differential equations of the kinetic-discretized Boltzmann type, involving transition probabilities. The evolution equations are as many as the income classes. Each one describes the variation in time of the number of individuals in a class. The novel aspect in this paper, as discussed in detail in Section II below, is that we also incorporate in the equations some terms accounting for income tax audit process as well as for related penalty payments from non-compliant audited individuals. Looking at numerical solutions, we observe that in the long run they all tend to an equilibrium. This macro-level equilibrium represents the observable income distribution. We compare scenarios corresponding to cases in which different percentages of individuals are being audited and non-compliant audited individuals are differently fined. In all these cases, we evaluate the tax revenue and the Gini index. Our interest is to try and see whether it is more convenient to increase the severity of punishment or the number of audits. Of course, the model is somehow schematic and naive. Yet it allows explorative simulations and provides answers not obtainable by other means. We think it could help to better understand the consequences of different policies.

In the classical economic literature the combined effect of tax evasion, audits and payment of fines has been studied in detail in the context of representative-agent models (see e.g. the recent papers 6 and 7 . In this approach a rational agent, supposed to represent the behavior of the average individual, optimizes her/his choices considering several financial factors (capital, investment, consumption, time schedules, random character of the audit etc.). Also, in multi-agent-based models, the entire mechanism of taxation, audit and fines of certain real or fictional countries can be simulated taking into account their specific legislation, organization, forms of payment and annual deadlines 8 . Our approach is less sophisticated concerning the financial aspects, but its analytical character makes it more generally applicable than multi-agent simulations. To the best of our knowledge, the tools and informations provided by our approach are neither gained nor obtainable with the methods of the other complexity economics papers which deal with tax evasion. First of all, these papers typically focus on the changes, induced by imitation or by some audit procedure, of agent moral attitude and behavior (see e.g. 9 ; 10 ; 11 ; 12 ; 13 , and 14 and 15 , where also a review and a comparison of other references can be found). Furthermore, when the effect of some audit is taken into account, no deterrent effect substantiated by an economic penalty is considered. More in details, the models in 9 ; 10 ; 11 ; 12 ; 13 constitute a variant of the Ising model of ferromagnetism: each citizen is represented by a spin variable, which can be either in the tax compliant state or in the tax evader state (in 12 a third state for undecided people is considered as well). Citizens undergo transitions from to , due to imitation of their nearest neighbours or from to , due to tax audits. Indeed, an audit on an evader is assumed to have as a consequence the fact that she/he will remain honest for a certain number of steps. While helpful for the analysis of evasion phenomena in relation to local interaction and external controls, such an approach does not allow conclusions on the effect of evasion on the income distribution as does our model.

In the remainder of the paper we start in Section II with the proposal of a model structure capable of including the effects of some audit procedure; in practical terms we construct a system of ordinary differential equations governing the time evolution of a distribution function over the income variable. Then, in Section III we describe relevant features of numerical solutions of these equations. Finally, in Section IV we carry out a critical analysis, we draw conclusions and mention as well further improvements of the model to be possibly developed in future work.

II A model structure accounting for audit procedure

II.1 The base structure for building a suitable model

A structure corresponding to a system of nonlinear ordinary differential equations has been introduced in 3 to model taxation and redistribution in a society of individuals with different tax evasion behavior. This structure does not account for audit procedures, but we recall it here, because it represents the starting point for the construction of the model discussed in this paper. It is expressed by

| (1) |

with and . The equations in (1) refer to a society of individuals divided into a number of income classes and into a number of sectors characterized by different evasion behaviors. Specifically,

by the fraction of -individuals is meant, namely the fraction of individuals who belong to the -th income class and to the -th evasion behavior sector. The number of different individual groups is hence and we denote the vector . The -th income class is characterized by its average income , where . The total number of individuals as well as the tax evasion behavior of each individual is supposed to remain constant in time. In contrast, individuals may move through different income classes.

The definition and interpretation of the terms appearing on the r.h.s. of (1) and describing the variation in time of is as follows:

for any and any , the coefficient

| (2) |

expresses the probability that an -individual will belong to the group as a consequence of a direct interaction with an -individual. These coefficients satisfy for any fixed , ;

for any and any , the function

| (3) |

expresses the variation in the group due to the taxation and redistribution process associated to an interaction between an -individual with an -individual. These functions are continuous and satisfy for any fixed , and .

According to (1), the variation in time of the individual number is due to a whole of “microscopic” interactions: these include direct interactions of individuals who exchange money in pairs and indirect interactions which involve triplets of individuals and are related to payment of taxes and redistribution of the tax revenue. (see 4 or 5 for a detailed illustration of the mechanism).

Also a specific choice for the ’s and the ’s has been proposed in 3 . In the following lines we recall it briefly. To start with,

- let for be defined as

| (4) |

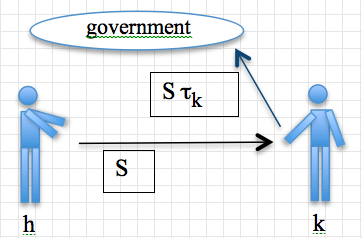

with the exception of the terms for , for , for , for and for . The coefficients (4) represent the probability that in an encounter between an individual of the -th income class and one of the -th class, the one who pays is the former, see also 5 ;

- let , with for all , denote an amount of money, namely the one which in each direct transaction one individual is supposed to pay to another;

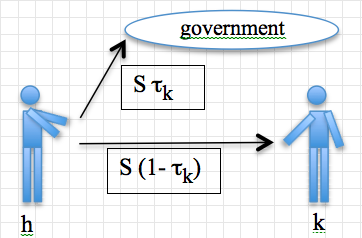

- also, let for and with denote the tax rate of the -th income class and let for and denote the effective tax rate111 In the kind of tax evasion considered in this paper the individual who receives money reports a minor amount than she should. In such a case, there is no advantage for the individual who pays., possibly reduced due to tax evasion, to be associated to any -individual; we assume that

where is a parameter in . Of course, corresponds to total evasion and to absence of evasion.

Before giving the expressions of the ’s and the ’s, we point out the following fact.

Remark 1. In a tax compliance case a direct interaction of an individual of the -th income class paying to one of the -th class, with this one paying the due tax, , to the government would be equivalent to that of the first individual paying an amount to the -individual and paying as well a quantity to the government. In a tax evasion case a direct interaction between a -individual paying to a -individual is equivalent to that of the -individual paying an amount to the -individual and paying as well a quantity to the government.

Among the coefficients , the only nonzero ones are:

| (5) | |||||

where the indices and take any value in and, as for the indices and , each term is defined only when it is meaningful: e.g., the second addendum on the r.h.s. in the second line of (5) is present only for and , whereas the third addendum is present only for and .

The functions take the form

| (6) | |||||

with denoting the Kronecker delta and, as in (5), with the understanding that each term is defined only when meaningful. We recall that, for technical reasons, the effective amount of money paid as tax is multiplied by .

Remark 2. As observed in 3 , conservation in time of both the number of individuals and the global income hold true for (1). Equivalently,

For any initial condition having non negative components , such that 222 The number is chosen here as a normalization value., a unique solution of exists, which is defined for all , satisfies and also

| (7) |

This implies that the right hand sides of system simplify; they are in fact polynomials of third degree.

The scalar function remains constant along each solution of system .

II.2 Incorporating audit procedure terms into the model

We are now ready to incorporate also the effects of some audit procedure into the model. Towards this aim we will introduce here two further parameters, by means of which the equations (1) will be suitably generalized. These parameters will be denoted by and . They represent respectively

-

•

the fraction of individuals in the society who are subject to an audit,

-

•

a multiplicative factor expressing the coefficient by which the amount of tax evaded has to be multiplied to give the wanted fine.

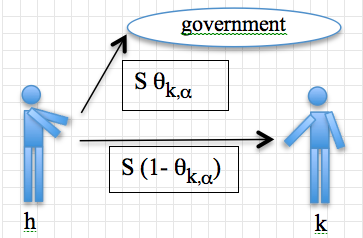

To explain the generalized equation form we argue as follows. First of all, it is convenient to split the r.h.s. of the equations into two parts, which represent respectively the contribution, both direct and indirect, of the non-audited and of the audited individuals. In the first part, all terms describing the binary and the ternary interactions are exactly as in the case without audit. The second part maintains the structure of the first one, but some coefficients in it are different. Arguing similarly as in Remark , we observe here that in the presence of an audit procedure in a case with possible tax evasion, a direct interaction between a -individual paying to a -individual can be thought of as equivalent to that of the -individual paying an amount to the -individual and paying as well a quantity to the government. Indeed, the final effect of the operation is that

- the -individual pays in total the amount ,

and

- the amount corresponding to the tax revenue related to this interaction is . If the -individual is tax compliant, i.e. , this amount coincides with ; otherwise, due to the fact that , this amount is greater than . (It would have been smaller than if evasion without audit had occurred).

We denote from now on by

the coefficients and the functions defined as in (5) and (6), with the difference that any appearing in (5) and (6) must be replaced by . Similarly to the ’s and ’s in (5) and (6), the coefficients and the functions satisfy

for any fixed , and .

The equations of the audit model can now be written. They take the form

| (8) | |||||

with and , with the terms on the right hand side reducing, in view of the Remark , to polynomials of third degree.

Remark 3. The penalty inflicted in this model refers to a single economic transaction: no reference is done to the accumulated capital for it to be paid. Accordingly, in order to guarantee non negativity of the quantity which a -individual pays in a generic transaction to a -individual, we have to impose some constraint on the parameter . We will assume from now on that

| (9) |

III Numerical solutions and results

It is a straightforward exercise to check that the two properties stated in Remark , i.e. the existence for a given initial condition of a unique solution satisfying and the conservation in time of the global income, hold true for the system as well. In addition, the running of several numerical solutions provides evidence of the following fact.

Property 1. If the parameters of the model (namely, , , the ’s, the ’s), the fraction of individuals with different behavior333 The fraction of individuals with a specific evasion behavior is assumed here to be the same in each income class. and are all fixed, then the solutions evolving from initial conditions , for which for any and ,

tend asymptotically to a same stationary distribution as .

We are specifically interested into the effects of different audit policies on the lung run income distribution. Hence, we compare various scenarios emerging in correspondence to different percentages of the audited individuals and different penalty coefficients .

To obtain numerical solutions, one has to fix the parameters of the model. We list next the specific choice we carried out in this connection and then we’ll give account of the output of a number of numerical solutions.

We took the number of income classes , the number of behavioral sectors , the average incomes for , the unit amount of exchanged money , and the tax rates

| (10) |

with and 444 These are the values of the minimal and of the maximal tax rate relative to IRPEF in Italy.. Also, we considered the case in which each one of the three evasion-type behavioral sectors contains exactly one third of the population. We report below the results obtained in correspondence to

(i) cases in which

-

•

the first sector consists of compliant individuals,

-

•

the second sector consists of individuals who use to evade half of the taxes they should,

-

•

the third sector consisting of individuals who use to evade three quarters of the taxes they should,

corresponding to the choice of the parameters

| (11) |

and

(ii) cases in which there is less evasion and specifically the evasion rate is half the evasion rate of the previous cases, namely cases in which

-

•

the first sector consists of compliant individuals,

-

•

the second sector consists of individuals who use to evade one quarter of the taxes they should,

-

•

the third sector consisting of individuals who use to evade three eights of he taxes they should,

corresponding to the choice of the parameters

| (12) |

For each of the two situations described by the parameter choices and we considered a range of different cases corresponding to different values of the parameters and . In fact, we ran several sets of simulations, with each set characterized by the value of the constant global income. We evaluated the Gini index and the tax revenue relative to the stationary distribution reached in the long run by the solutions of the systems for different values of and . We recall here that

-

•

the Gini index provides a measure of the extent to which a distribution - here, the income distribution - deviates from a perfectly equal one. It is graphically represented by the area between the Lorenz curve (which plots the cumulative income share of a population on the axis against the distribution of the population on the axis) and the line of perfect equality. It takes values in , where represents the complete equality and the maximal inequality;

-

•

the tax revenue is the income collected by the government through taxation. Here, we calculate in fact the tax revenue in the unit time as

where denotes the fraction of individuals in the -th income class, -th sector at equilibrium.

The results of the simulations are all qualitatively consistent with those summarized in Tables III and III. The variations of the values of given there are very small, but, one should not forget that they just provide the tax revenue in the unit time. The tax revenue of a definite period coincides with a sum of contributions of this kind. Looking at the numbers contained in Tables III and III, one may notice at a first glance that

for fixed , the tax revenue increases and the Gini index decreases as increases,

for fixed , the tax revenue increases and the Gini index decreases as increases.

The data in this table refer to the asymptotic stationary income distributions of systems characterized by different values of the fraction of audited individuals and of the penalty multiplicative factor , in cases in which the total income is and . The value of the Gini index and of the tax revenue is provided in each case. Their value in the case with no evasion would be respectively: GI = and TR = , and in the case with evasion, but no audit GI = and TR = . Gini Index 0.382193 0.382086 0.381979 0.381873 0.381766 0.380873 0.380614 0.380355 0.380099 0.379844 0.37959 0.379187 0.378789 0.378394 0.378003 0.378345 0.377809 0.377281 0.37676 0.376247 0.377138 0.376479 0.375833 0.375198 0.374577 Tax Revenue

The data in this table refer to the asymptotic stationary income distributions of systems characterized by different values of the fraction of audited individuals and of the penalty multiplicative factor , in cases in which the total income is and . The value of the Gini index and of the tax revenue is provided in each case. Their value in the case with no evasion would be respectively: GI = and TR = , and in the case with evasion, but no audit GI = and TR = . Gini Index 0.373611 0.373568 0.373526 0.373483 0.373441 0.373084 0.37298 0.372876 0.372773 0.37267 0.372567 0.372404 0.372242 0.372081 0.371921 0.372061 0.371841 0.371624 0.371408 0.371194 0.371565 0.371291 0.371021 0.370754 0.37049 Tax Revenue

If such a behavior is definitely reasonable form a qualitative point of view, the added value of the model is given by the quantitative aspect. One can for example estimate the amount of money collected in correspondence to different choices of the parameters and . And, as illustrated in the next lines, also values of these parameters different from those appearing in the tables above can be taken into account. Indeed, looking more carefully at the Tables III and III, one realizes that both the Gini index and the tax revenue values depend linearly on and depend linearly on . In other words, one finds that both the Gini index and the tax revenue may be approximated by bilinear functions of the variables and . One can then employ a least squares method to find a surface coinciding with the graph of a bilinear function555 That a bilinear function as in (13) already provides a good approximation, it can be checked by trying and looking instead for a function . When this is done and a least squares procedure is performed, the resulting coefficients of and turn out to be of to magnitude order less than each other coefficient in the expression of .

| (13) |

best fitting the discrete data available. In this connection, denote

and

Searching, for example with reference to Table III, values of the coefficients in (13), to which a minimum of

| (14) |

corresponds, and constructing with these values the function in (13), one finds for it the expression

In conjunction with an estimate of the auditing costs, this allows to calibrate the parameters and so as to have effective auditing and fine. Indeed, by fixing a reasonable value of the expected tax revenue, say , one may look for the coordinates and which satisfy

| (15) |

This equation defines a curve and, as the next formulae show, each of the coordinates can be expressed as a function of the other one:

| (16) | |||||

where . The equations can give some insight as how to fix the parameters and in an appropriately balanced way, i.e. in such a way that neither nor are too large.

IV Critical analysis and conclusions

This paper proposes a dynamic model for the description of processes of taxation, redistribution and auditing in the presence of tax evasion, possibly occurring in different measure. The focus is on the effects of different enforcement regimes on the income distribution. According to the model here formulated, the main role to this end is played by two parameters: one of them, , expresses the fraction of audited taxpayers; the other one, , is the coefficient by which the amount of owed tax must be multiplied to give the tax fraud penalty. The model fits in with a complex system perspective: society is treated as a large collection of heterogeneous individuals, divided into income classes and characterized by different compliance and non-compliance behaviors. Total wealth is supposed to remain constant in time and the evolution of the income distribution is described by a system of nonlinear ordinary differential equations which involve transition probabilities. The long-run solutions obtained with a number of numerical simulations show stationary aggregate-level income distributions emerging from the whole of individual interactions.

An aspect of interest of this model is the possibility of employing it as an “explorative” tool. Simulations corresponding to different conceivable values of the mentioned parameters can provide insight as to whether it is more convenient to increase the severity of punishment or the number of audits. Indeed, they allow to forecast the emergence of different scenarios. Vice versa, the model can be also used to derive, in correspondence to a reasonable desired value of the tax revenue, the relation between the parameters and which are compatible with . And this, combined with the intent of keeping under control the values of these parameters, can suggest convenient choices of these parameters.

The tax audits and fines described by our model can be considered as only moderately “punitive”. We assume that tax evaders, if found guilty in an audit, must pay a fine which cuts their gain in the current transaction, while the rest of their wealth is not affected and their evasion habits also remain unchanged. This limitation of the model can be lifted in a more general version; actually, in the general formulation of the equations (1) the elements of the transition matrices are not restricted to be proportional to (namely, different from zero only if ) as is the case in the particular model investigated here. On the other hand, considering the amount of the fines, it is easy to check that the persistence of the individuals’ evasion behavior is coherent with their subjective perception of economic advantage. In fact, even when the audits have maximum frequency () and largest penalty rate (), if also evaders know this in advance, they may conclude that it is still more convenient for them to evade and risk to pay the fine.

From the point of view of the state administration the audits can produce a remarkable increase in the tax revenue. For instance, considering again the maximum audit frequency and maximum penalty, and assuming evasion levels equal to , and in the three behavioral sectors as in Table III, the increase in the tax revenue with respect to the case of no audits is about . As pointed out in Section III, the dependence of this figure on the parameters and is approximately linear, so a hypothetical policy-maker could use the model and some additional information on the costs of the audits in order to assess the most convenient audits/fines policy. We recall that the taxation level implemented in our model is quite realistic: comparing “pre-redistribution” values of (those obtained when taxation terms are switched off) with the values after redistribution 16 it turns out that we are quite close to the real data of the United States (while, for instance, economies like Germany and Denmark exhibit a markedly larger redistribution gap).

A priori one could think that audits and fines should have a positive effect on the reduction of economic inequality and correspondingly of the Gini index . According to our model, however, such effect is small: the decrease of when the audit frequency and penalty ratio are increased is only of the order of . In contrast, the decrease of following a diminution of the evasion level 2 or a weighted redistribution of welfare in favor of the poor classes 16 is of the order of or more. In view of the strong dependence of the tax revenue on and , this is a further confirmation that the relation between the Gini index and the tax revenue is not simple, and is influenced by several factors. In 16 , for instance, we found that when the gap in the tax rates varies from - to - , the tax revenue decreases and so does the Gini index (arguably because, although the rich pay more and the poor less, the largest part of the tax revenue still comes from the poor and middle classes). On the other hand, when the welfare redistribution parameters are changed in favor of the poor classes, the tax revenue increases and decreases. Besides, we would like to recall that in the presence of a high level of tax evasion even the sizeable increase of the Gini index does not adequately reflect the injustice actually present in the society; we found in 3 for instance that with an evasion level of tax evaders can enjoy an average wealth gap up to ca. with respect to non-evaders.

Finally, we emphasize again that the model requires a condition: in fact, its two main parameters cannot be totally arbitrary. They have to satisfy a constraint, which for simplicity has been expressed here as the need of the inequalities and to hold true, although more general formulations are possible. It would be desirable to get rid of this condition. Pointing to directions of possible future research, we also observe that a relevant step forward would be the inclusion in the model of the possibility for individuals of changing behavioral type in time for different reasons, among which e.g. auditing experience.

References

- (1) C. Schinckus, Between complexity of modelling and modelling of complexity: an essay of econophysics, Physica A 392, 3654-3665 (2013).

- (2) M.L. Bertotti, G. Modanese, Micro to macro models for income distribution in the absence and in the presence of tax evasion, Appl. Math. Comput. 244, 836–846 (2014).

- (3) M.L. Bertotti, G. Modanese, Mathematical models describing the effects of different tax evasion behaviours, submitted (2015).

- (4) M.L. Bertotti, G. Modanese, From microscopic taxation and redistribution models to macroscopic income distributions, Physica A 390, 3782–3793 (2011).

- (5) M.L. Bertotti, G. Modanese, Exploiting the flexibility of a family of models for taxation and redistribution, Eur. Phys. J. B 85, 261 (2012).

- (6) R. Levaggi, F. Menoncin, Tax audits, fines and optimal tax evasion in a dynamic context, Econ Lett 117, 318—321 (2012).

- (7) R. Levaggi, F. Menoncin, Dynamic tax evasion with audits based on conspicuous consumption, preprint (2015).

- (8) K.M. Bloomquist, M. Koehler, A large-scale agent-based model of taxpayer reporting compliance, J. Artif. Soc. Soc. Simul. 18, 20 (2015).

- (9) G. Zaklan, F. Westerhof, D. Stauffer, Analysing tax evasion dynamics via the Ising Model, J Econ Interact Coord 4, 1-14 (2009).

- (10) S. Hokamp, M. Pickhardt, Income tax evasion in a society of heterogeneous agents: evidence from an agent-based model, International Economic Journal 24, 541–553 (2010).

- (11) S. Hokamp, G. Seibold, Tax compliance and public goods provision. An agent-based econophysics approach, CEJEME 6, 217-236 (2014).

- (12) N. Crokidakis, A three-state kinetic agent-based model to analyse tax evasion dynamics, Physica A 414, 321-328 (2014).

- (13) F.W.S. Lima, Tax evasion dynamics and non equilibrium Zaklan model with heterogeneous agents on square lattice, Int. J. Mod. Phys. C 26, 1550035 (8 pages) (2015).

- (14) K.M. Bloomquist, Multi-agent based simulation of the deterrent effects of taxpayer audits, Proceedings. Annual Conference on Taxation and Minutes of the Annual Meeting of the National Tax Association, National Tax Association 97, 159-173 (2004).

- (15) K.M. Bloomquist, A Comparison of Agent-Based Models of Income Tax Evasion, Social Science Computer Review 24, 411-425 (2006).

- (16) M.L. Bertotti, G. Modanese, Microscopic models for welfare measures addressing a reduction of economic inequality, Complexity, Article first published online, doi: 10.1002/cplx.21669 (2015).