Simple Bayesian Algorithms for Best-Arm Identification

Abstract

This paper considers the optimal adaptive allocation of measurement effort for identifying the best among a finite set of options or designs. An experimenter sequentially chooses designs to measure and observes noisy signals of their quality with the goal of confidently identifying the best design after a small number of measurements. This paper proposes three simple and intuitive Bayesian algorithms for adaptively allocating measurement effort, and formalizes a sense in which these seemingly naive rules are the best possible. One proposal is top-two probability sampling, which computes the two designs with the highest posterior probability of being optimal, and then randomizes to select among these two. One is a variant of top-two sampling which considers not only the probability a design is optimal, but the expected amount by which its quality exceeds that of other designs. The final algorithm is a modified version of Thompson sampling that is tailored for identifying the best design.

We prove that these simple algorithms satisfy a sharp optimality property. In a frequentist setting where the true quality of the designs is fixed, one hopes the posterior definitively identifies the optimal design, in the sense that that the posterior probability assigned to the event that some other design is optimal converges to zero as measurements are collected. We show that under the proposed algorithms this convergence occurs at an exponential rate, and the corresponding exponent is the best possible among all allocation rules. It should be highlighted that the proposed algorithms depend on a single tuning parameter, which determines the probability used when randomizing among the top-two designs. Attaining the optimal rate of posterior convergence requires either that this parameter is set optimally or is tuned adaptively toward the optimal value. The paper goes further, characterizing the exponent attained on any problem instance and for any value of the tunable parameter. This exponent is interpreted as being optimal among a constrained class of allocation rules. Finally, considerable robustness to this parameter is established through numerical experiments and theoretical results. When this parameter is set to 1/2, the exponent attained is within a factor of 2 of best possible across all problem instances.

1 Introduction

This paper considers the optimal adaptive allocation of measurement effort in order to identify the best among a finite set of options or designs. An experimenter sequentially chooses designs to measure and observes independent noisy signals of their quality. The goal is to allocate measurement effort intelligently so that the best design can be identified confidently after a small number of measurements. Just as the multi-armed bandit problem crystallizes the tradeoff between exploration and exploitation in sequential decision-making, this “pure–exploration” problem crystallizes the challenge of efficiently gathering information before committing to a final decision. It serves as a fundamental abstraction of issues faced in many practical settings. For example:

-

•

Efficient A/B/C Testing: An e-commerce platform is considering a change to its website and would like to identify the best performing candidate among many potential new designs. To do this, the platform runs an experiment, displaying different designs to different users who visit the site. How should the platform decide what percentage of traffic to allocate to each website design?

-

•

Simulation Optimization: An engineer would like to identify the best performing aircraft design among several proposals. She has access to a realistic simulator through which she can assess the quality of the designs, but each simulation trial is very time consuming and produces only noisy output. How should she allocate simulation effort among the designs?

-

•

Design of Clinical Trials: A medical research organization would like to find the most effective treatment out of several promising candidates. They run a clinical trail in which they experiment with the treatments. The results of the study may influence practice for many years to come, and so it is worth reaching a definitive conclusion. At the same time, clinical trails are extremely expensive, and careful experimentation can help to mitigate the associated costs.111Interpreted the context of clinical trials, this paper’s results are stated in terms of the number of patients required to reach a confided conclusion of the best treatment. However, we will see that optimal rules from this perspective also allocate fewer patients to very poor treatments, potentially leading to more ethical trials (Berry, 2004). Multi-armed bandit models of clinical trails date back to Thompson (1933), but bandit algorithms lack statistical power in detecting the best treatment at the end of the trial (Villar et al., 2015). Can we develop adaptive rules with better performance?

We study Bayesian algorithms for adaptively allocating measurement effort. Each begins with a prior distribution over the unknown quality of the designs. The experimenter learns as measurements are gathered, and beliefs are updated to form a posterior distribution. This posterior distribution gives a principled mechanism for reasoning about the uncertain quality of designs, and for assessing the probability any given design is optimal. By formulating this problem as a Markov decision process whose state-space tracks posterior beliefs about the true quality of each design, dynamic programming could in principle be used to optimize many natural measures of performance. Unfortunately, computing or even storing an optimal policy is usually infeasible due to the curse of dimensionality. Instead, this work proposes three simple and intuitive rules for adaptively allocating measurement effort, and by characterizing fundamental limits on the performance of any algorithm, formalizes a sense in which these seemingly naïve rules are the best possible.

The first algorithm we propose is called top–two probability sampling. It computes at each time-step the two designs with the highest posterior probability of being optimal. It then randomly chooses among them, selecting the design that appears most likely to be optimal with some fixed probability, and selecting the second most likely otherwise. Beliefs are updated as observations are collected, so the top-two designs change over time. The long run fraction of measurement effort allocated to each design depends on the true quality of the designs, and the distribution of observation noise. Top–two value sampling proceeds in a similar manner, but in selecting the top-two designs it considers not only the probability a design is optimal, but the expected amount by which its quality exceeds that of other designs. The final algorithm we propose is a top-two sampling version of the Thompson sampling algorithm for multi-armed bandits. Thompson sampling has attracted a great deal of recent interest in both academia and industry (Scott, 2016; Tang et al., 2013; Graepel et al., 2010; Chapelle and Li, 2011; Agrawal and Goyal, 2012; Kauffmann et al., 2012; Gopalan et al., 2014; Russo and Van Roy, 2014), but it is designed to maximize the cumulative reward earned while sampling. As a result, in the long run it allocates almost all effort to measuring the estimated-best design, and requires a huge number of total measurements to certify that none of the alternative designs offer better performance. We introduce a natural top-two variant of Thompson sampling that avoids this issue and as a result offers vastly superior performance for the best-arm identification problem.

Remarkably, these simple heuristic algorithms satisfy a strong optimality property. Our analysis focuses on frequentist consistency and rate convergence of the posterior distribution, and therefore takes place in a setting where the true quality of the designs is fixed, but unknown to the experimenter. One hopes that as measurements are collected the posterior distribution definitively identifies the true best design, in the sense that the posterior probability assigned to the event that some other design is optimal converges to zero. We show that under the proposed algorithms, this convergence occurs at an exponential rate, characterize the exponent attained for each problem instance, and relate this to the best possible exponent among allocation rules.

To make a precise statement, it is important to highlight that the top-two algorithms described above depend on a tunable parameter; each method identifies the top-two designs and then flips a biased coin to decide which of these to sample. The paper’s theoretical results offer a fairly complete characterization of the asymptotic performance of these algorithms, and are summarized more precisely below.

-

1.

Optimality with tuning: For any problem instance and any choice of tuning parameter, the proposed top-two algorithms attain an exponential rate of posterior convergence. This exponent is carefully characterized. If the tuning parameter is stet optimally, the exponent is optimal among all possible adaptive allocation rules. Moreover, it is possible to attain this rate of convergence by adaptively adjusting the tuning parameter.

-

2.

Robustness with an unbiased coin: Uniformly across problem instances, the exponent attained by top–two sampling with an unbiased coin is within a factor of two of what could be attained by an optimal allocation rule. This robustness is further validated through numerical experiments: across fourteen problem instances top-two Thompson sampling with an unbiased coin offers similar performance to a version of top-two Thompson sampling that is applied with the best tuning parameter for that particular problem setting.

-

3.

Optimality among a restricted class of allocation rules for any tuning parameter: To simplify the discussion, imagine top–two sampling is applied with an unbiased coin. Then, as the number of measurements tends to infinity, exactly half of measurement effort is allocated to the best design. Now, consider any possible adaptive allocation rule, which, like top-two sampling, allocates half of measurement effort to the true best design asymptotically. There is no problem instance for which this alternative algorithm attains an exponential rate of posterior convergence exceeding that of the proposed top-two sampling algorithms. An analogous result applies when a biased coin is used.

It is worth elaborating on the third result described above, as it is the main insight that prompted this paper. We face the problem of adaptively allocating measurements among competing designs. We can imagine decomposing this problem into two parts: first the experimenter chooses which fraction of measurements to dedicate to what is believed to be the best design, and second, given this choice, she chooses how to adaptively allocate remaining measurements among the competing designs. Roughly speaking, this paper shows that the allocation among the remaining designs is handled automatically and optimally by very simple top-two sampling algorithms. This offers substantial new insight into the structure of best arm identification problems and effectively reduces the problem to the choice of a single tuning parameter–the bias of the coin used by the top-two sampling algorithms. The paper establishes a surprising degree of robustness to this tuning parameter, and shows it is possible to attain a fully optimal exponent by setting it adaptively. However, the proposed tuning method is complex, spoiling some of the elegance of the top-two sampling algorithms. The search for simpler methods stands as an interesting open question.

1.1 Main Contributions

This paper makes both algorithmic and theoretical contributions. On the algorithmic side, we develop three new adaptive measurement rules. The top-two Thompson sampling rule, in particular, could have an immediate impact in application areas where Thompson sampling is already in use. For example, there are various reports of Thompson sampling being used in A/B testing (Scott, 2016) and in clinical trials (Berry, 2004). But practitioners in these domains typically hope to commit to a decision after definitive period of experimentation, and top-two Thompson sampling can greatly reduce the number of measurements required to do so. In addition, because of their simplicity, the proposed allocation rules can be easily adapted to treat problems beyond the scope of this paper’s problem formulation. See Section 8 for examples.

The paper also makes several theoretical contributions. Most importantly, it is of broad scientific interest to understand when very simple measurement strategies are the best possible. This paper provides sharp links between these top-two sampling rules and the limits of performance under any adaptive algorithm. In establishing these results, we exactly characterize the optimal rate of posterior convergence attainable by an adaptive algorithm, and provide interpretable bounds on this rate when measurement distributions are sub-Gaussian. The analysis also provides several intermediate results which may be of independent interest, including establishing consistency and exponential rates of convergence for posterior distributions with non-conjugate priors and under adaptive measurement rules. It should be highlighted, however, that the results do require some strong regularity properties on the prior distribution, and in particular only apply to priors defined over a compact set.

1.2 Related Literature

Sequential Bayesian Best-Arm Identification.

There is a sophisticated literature on algorithms for Bayesian multi-armed bandit problems. In discounted bandit problems with independent arms, Gittins indices characterize the Bayes optimal policy (Gittins and Jones, 1974; Gittins, 1979). Moreover, a variety of simpler Bayesian allocation rules have been developed, including Bayesian upper-confidence bound algorithms (Kaufmann et al., 2012; Srinivas et al., 2012; Kaufmann, 2016), Thompson sampling (Agrawal and Goyal, 2012; Korda et al., 2013; Gopalan et al., 2014; Johnson et al., 2015), information-directed sampling (Russo and Van Roy, 2014), the knowledge gradient (Ryzhov et al., 2012), and optimistic Gittins indices (Gutin and Farias, 2016). These heuristic algorithms can be applied effectively to complicated learning problems beyond the specialized settings in which the Gittins index theorem holds, have been shown to have strong performance in simulation, and have theoretical performance guarantees. In several cases, they are known to attain sharp asymptotic limits on the performance of any adaptive algorithm due to Lai and Robbins (1985).

The pure-exploration problem studied in this paper is not nearly as well understood. Recent work has cast this problem in a decision-theoretic framework (Chick and Gans, 2009). However, because the conditions required for the Gittins index theorem do not hold, computing an optimal policy via dynamic programming is generally infeasible due to the curse of dimensionality. Papers in this area typically focus on problems with Gaussian observations and priors. They formulate simpler problems that can be solved exactly – like a problem where only a single measurement can be gathered (Gupta and Miescke, 1996; Frazier et al., 2008; Chick et al., 2010) or a continuous-time problem with only two alternatives (Chick and Frazier, 2012) – and then extend those solutions heuristically to build measurement and stopping rules in more general settings.

For problems with Gaussian priors and noise distributions, the expected-improvement (EI) algorithm is a popular Bayesian approach to sequential information-gathering. Interesting recent work by Ryzhov (2016) studies the long run distribution of measurement effort allocated by the expected-improvement and shows this is related to the optimal computing budget allocation of Chen et al. (2000). This contribution is very similar in spirit to this paper, as it relates the long-run behavior of a simple Bayesian measurement strategy to a notion of an approximately optimal allocation. Unfortunately, EI cannot match the performance guarantees in this paper. In fact, under EI the posterior converges only at a polynomial rate, instead of the exponential rate attained by the algorithms proposed here and by the OCBA. See appendix C for a more precise discussion.

Classical Ranking and Selection.

The problem of identifying the best system has been studied for many decades under the names ranking and selection or ordinal optimization. A full review of this literature is beyond the scope of this article. See Kim and Nelson (2006), Kim and Nelson (2007) or Hong et al. (2015) for thorough reviews. Part of this literature focuses on a problem called subset-selection, where the goal is not to identify the best-design, but to find a fairly small subset of designs that is guaranteed to contain the best design. Beginning with Bechhofer (1954), many papers have focused on an indifference zone formulation, where, for user-specified , the goal is to guarantee with probability at least the algorithm returns the true arm mean as long as no suboptimal arm is within of optimal. Assuming measurement noise is Gaussian with known variance , one can guarantee this indifference-zone criterion by gathering total measurements, divided equally among the designs, and then returning the design with highest empirical-mean. For the case of unknown variances, Rinott (1978) proposes a two stage procedure, where the first stage is used to estimate the variance of each population, and the number of samples collected from each design in the second stage is scaled by its estimated standard deviation. In the machine learning literature, Even-Dar et al. (2002) studies the number of samples required by algorithms delivering –PAC guarantees. Such algorithms are sometimes said to ensure a specified probability of good selection in the terminology of the simulation optimization literature, a strictly stronger guarantee than an indifference zone guarantee (Ni et al., 2017). Even-Dar et al. (2002) show that when measurement noise is uniformly bounded, an –PAC guarantee is satisfied by a sequential elimination strategy that uses only samples on average. Mannor and Tsitsiklis (2004) provide a matching lower bound. Similar to minimax bounds, this shows the upper bound of Even-Dar et al. (2002) is tight, up to a constant factor, for a certain worst case problem instance. Indifference zone formulations of ranking and selection problems remains an area of active research. See for example Fan et al. (2016) and some of the references therein.

Since Paulson (1964), many authors have sought to reduce the number of samples required on easier problem instances by designing algorithms that sequentially eliminate arms once they are determined to be suboptimal with high confidence. See the recent work of Frazier (2014) and the references therein. However, in a sense described below, Jennison et al. (1982) show formally that there are problems with Gaussian observations where any sequential-elimination algorithm will require substantially more samples than optimal adaptive allocation rules. See Section 8 for modified top-two sampling algorithms designed for an indifference zone criterion.

The asymptotic complexity of best-arm identification.

We described attainable rates of performance on a worst-case problem instance characterized by Even-Dar et al. (2002) and Mannor and Tsitsiklis (2004). A great deal of work has sought “problem dependent” bounds, which reveal that the best-arm can be identified more rapidly when the true problem instance is easier. This is the case, for example, when some arms are of very low quality, and can be distinguished from the best using a small number of measurements. Asymptotic measures of the complexity of best-arm identification appear to have been derived independently in statistics (Chernoff, 1959; Jennison et al., 1982), simulation optimization (Glynn and Juneja, 2004), and, concurrently with this paper, in the machine learning literature (Garivier and Kaufmann, 2016). Each of these papers studies a slightly different objective, but each captures a notion of the number of samples required to identify the best-arm as a function of the problem instance – i.e. as a function the number of designs, each design’s true quality, and the distribution of measurement noise.

Glynn and Juneja (2004) build on the optimal-computing-budget allocation (OCBA) of Chen et al. (2000) to provide a rigorous large-deviations derivation of the optimal fixed allocation. In particular, assuming the design with the highest empirical mean is returned, there is a fixed allocation under which the probability of incorrect selection decays exponentially, and the exponent is optimal under all fixed-allocation rules. The setting studied by this paper is often called the “fixed-budget” setting in the recent multi-armed bandit literature. Unfortunately, it may be difficult to implement the allocation in Glynn and Juneja (2004) without additional prior knowledge. Later work by Glynn and Juneja (2015) provides a substantial discussion of this issue.

This paper was highly influenced by a classic paper by Chernoff (1959) on the sequential design of experiments for binary hypothesis testing. Chernoff’s asymptotic derivations give great insight into best-arm identification, which can be formulated as a multiple-hypothesis testing problem with sequentially chosen experiments, but surprisingly this connection does not seem to be discussed in the literature. Chernoff looks at a different scaling than Glynn and Juneja (2004). Instead of taking the budget of available measurements to infinity, he allows the algorithm to stop and declare the hypothesis true or false at any time, but takes the cost of gathering measurements to zero while the cost of an incorrect terminal decision stays fixed. He constructs rules that minimize expected total costs in this limit. Chernoff makes restrictive technical assumptions, some of which have been removed in subsequent work (Albert, 1961; Kiefer and Sacks, 1963; Keener, 1984; Nitinawarat et al., 2013; Naghshvar et al., 2013).

Jennison et al. (1982) study an indifference zone formulation of the problem of identifying the best-design. Like Chernoff (1959), they allow the algorithm to stop and return an estimate of the best-arm at any time, but rather than penalize incorrect decisions, they require that the probability correct selection (PCS) exceeds for every problem instance. Intuitively, the expected number of samples required by an algorithm satisfying this PCS constraint must tend to infinity as . In the case of Gaussian measurement noise, Jennison et al. (1982) characterize the optimal asymptotic scaling of expected number of samples in this limit. The recent multi-armed bandit literature refers to this formulation as the “fixed-confidence” setting.

A large body of work in the recent machine learning literature has sought to characterize various notions of the complexity of best-arm identification (Even-Dar et al., 2002; Mannor and Tsitsiklis, 2004; Audibert and Bubeck, 2010; Gabillon et al., 2012; Karnin et al., 2013; Jamieson and Nowak, 2014). However, upper and lower bounds match only up to constant or logarithmic factors, and only for particular hard problem instances. Substantial progress was presented by Kaufmann and Kalyanakrishnan (2013) and Kaufmann et al. (2014), who seek to exactly characterize the asymptotic complexity of identifying the best arm in both the fixed-budget and fixed-confidence settings. Still, the upper and lower bounds presented there do not match. A short abstract of the current paper appeared in the 2016 Conference on Learning Theory. In the same conference, independent work by Garivier and Kaufmann (2016) provided matching upper and lower bounds on the complexity of identifying the best arm in the “fixed-confidence” setting. Like the present paper, but unlike Jennison et al. (1982), these results apply whenever observation distributions are in the exponential family and do not require an indifference zone.

The current paper looks at a different measure. We study a frequentist setting in which the true quality of each design is fixed, and characterize the rate of posterior convergence attainable for each problem instance. We also describe, as a function of the problem instance, the long-run fraction of measurement effort allocated to each design by any algorithm attaining this rate of convergence. These asymptotic limits turn out to be closely related to some of the aforementioned results. In particular, the optimal exponent given in Subsection 6.4 mirrors the complexity measure of Chernoff (1959). In the same subsection, this exponent is then simplified into a form that mirrors one derived by Glynn and Juneja (2004), and, for Gaussian distributions, one derived by Jennison et al. (1982).

Optimal Budget Allocations.

While the complexity measure we derive is similar to past work, the proposed algorithms differ substantially. The allocation rules proposed by Chernoff (1959), Jennison et al. (1982) and Glynn and Juneja (2004) are essentially developed as a means of proving certain rates are attainable asymptotically. To derive these policies, the authors begin with a thought experiment: assuming the experimenter actually knew the true quality of every arm, what proportion of measurements should she allocate to each arm in order to gather the most definitive evidence concerning the identity of the optimal arm. One approach to constructing such rules in practice is to use some fraction of samples to estimate the arm means and then apply the asymptotically optimal sampling proportions assuming these estimates to be correct. Such an approach dates back to at least the work of Kiefer and Sacks (1963), which followed Chernoff’s work on the sequential design of experiments.

Early authors made a point to highlight limitations of such an approach. Jennison et al. (1982) writes their proposed procedures “typically…do not have good small sample size properties. A better procedure would have several stages and a more sophisticated sampling rule.” In a 1975 review of the sequential design of experiments, Chernoff (1975) notes that asymptotic approaches to the optimal sequential design of experiments had been fairly successful in circumventing the need to compute Bayesian optimal designs via dynamic programming, but “the approach is very coarse for moderate sample size problems.” He writes that two-stage procedures of Kiefer and Sacks (1963), “sidestep the issue of how to experiment in the early stages,” while constructing the optimal allocations based on point estimates “treats estimates of based on a few observations with as much respect as that based on many observations.”

Closely related to these approaches is a large body of work on optimal computing budget allocations (OCBA) (Chen et al., 2000). Most of this literature studies problems with Gaussian observations. They derive an approximation to the optimal sampling proportions presented in Chernoff (1959), Jennison et al. (1982) and Glynn and Juneja (2004), which appears to simplify computation. This allocation is often stated to be optimal as the number of arms grows large; more rigorous results to this effect are established in interesting work by Pasupathy et al. (2015), who shows that the sampling ratios of the OCBA coincide with those of Glynn and Juneja (2004) in the limit of a sequence of problem instances in which the number of arms tends to infinity but all suboptimal arms’ means are bounded away from optimal by a fixed constant. Optimal budget allocations have been extended in various directions, for example to address Bayesian expected loss objectives (Chick and Inoue, 2001), the problem of identifying an optimum subject to stochastic constraints (Hunter and Pasupathy, 2013), and the problem of identifying the top alternatives (Chen et al., 2008). See Chen et al. (2015) for a more thorough review.

In this paper, we study simple adaptive allocation rules which, ostensibly, have no relation to the asymptotic calculations used to derive these optimal budget allocations. The main insight is that these simple algorithms automatically adapt their measurement effort in such a way that their long run behavior is deeply linked to the ratios suggested in the work of Chernoff (1959), Jennison et al. (1982), and Glynn and Juneja (2004). A major advantage of top-two sampling algorithms, however, is that asymptotic analysis is used only to give insight into the algorithms, and any approximations have no impact on their practical performance. A suite of experiments in Section 7 suggest the approach can substantially outperform the optimal allocations derived from asymptotic theory.

2 Problem Formulation

Consider the problem of efficiently identifying the best among a finite set of designs based on noisy sequential measurements of their quality. At each time , a decision-maker chooses to measure the design , and observes a measurement . The measurement associated with design and time is drawn from a fixed, unknown, probability distribution, and the vector is drawn independently across time. The decision-maker chooses a policy, or adaptive allocation rule, which is a (possibly randomized) rule for choosing a design to measure as a function of past observations . The goal is to efficiently identify the design with highest mean.

We will restrict attention to problems where measurement distributions are in the canonical one dimensional exponential family. The marginal distribution of the outcome has density with respect to a base measure , where is an unknown parameter associated with design . This density takes the form

| (1) |

where , , and are known functions, and is assumed to be twice differentiable. We will assume that is a strictly increasing function so that is a strictly increasing function of . Many common distributions can be written in this form, including Bernoulli, normal (with known variance), Poisson, exponential, chi-squared, and Pareto (with known minimal value).

Throughout the paper, will denote the unknown true parameter vector, and and will be used to denote possible alternative parameter vectors. Let denote the unknown best design. We will assume throughout that for so that is unique, although this can be relaxed by considering an indifference zone formulation where the goal is to identify an –optimal design, for some specified tolerance level .

Prior and Posterior Distributions.

The policies studied in this paper make use of a prior distribution over a set of possible parameters that contains . Based on a sequence of observations , beliefs are updated to attain a posterior distribution . We assume has density with respect to Lebesgue measure. In this case, the posterior distribution has corresponding density

| (2) |

where

is the likelihood function. While this formulation enforces some technical restrictions to facilitate theoretical analysis, it allows for very general prior distributions, and in particular allows for the quality of different designs to be correlated under the priors.

Optimal Action Probabilities.

Let

denote the set of parameters under which design is optimal, and let

| (3) |

denote the posterior probability assigned to the event that action is optimal. Our analysis will focus on , which is the posterior probability assigned to the event that an action other than is optimal. The next section will introduce policies under which as , and the rate of convergence is essentially optimal.

Further Notation.

Before proceeding, we introduce some further notation. Let denote the sigma algebra generated by . For all and , define

Each of these measures the effort allocated to design up to time .

3 Algorithms

This section proposes three algorithms for allocating measurement effort. Each depends on a tuning parameter , which will sometimes be set to a default value of . Each algorithm is based on the same high level principle. At every time step, each algorithm computes an estimate of the optimal design, and measures that with probability . Otherwise, we consider a counterfactual: in the (possibly unlikely) event that is not the best design, which alternative is most likely to be the best design? With probability , the algorithm measures the alternative . The algorithms differ in how they compute and . The most computationally efficient is the modified version of Thompson sampling, under which and and are themselves randomly sampled from a probability distribution.

We will see that asymptotically all three algorithms allocate fraction of measurement effort to measuring the estimated-best design, and the remaining fraction to gathering evidence about alternatives. The algorithms adjust how measurement effort is divided among these alternative designs as evidence is gathered, allocating less effort to measuring clearly inferior designs and greater effort to measuring designs that are more difficult to distinguish from the best.

3.1 Top-Two Probability Sampling (TTPS)

With probability , the top-two probability sampling (TTPS) policy plays the action which, under the posterior, is most likely to be optimal. When the algorithm does not play , it plays the most likely alternative , which is the action that is second most likely to be optimal under the posterior. Put differently, the algorithm sets , and .

3.2 Top-Two Value Sampling (TTVS)

We now propose a variant of top-two sampling that considers not only the probability a design is optimal, but the expected amount by which its quality exceeds that of other designs. In particular, we will define below a measure of the value of design under the posterior distribution at time . Top-two value sampling computes the top-two designs under this measure: and . It then plays the top design with probability and the best alternative otherwise. As observations are gathered, beliefs are updated and so the top two designs change over time. The measure of value is defined below.

The definition of TTVS depends on a choice of (utility) function , which encodes a measure of the value of discovering a design with quality . Two natural choices of are and . The paper’s theoretical results allow to be a general function, but we assume that it is continuous and strictly increasing. For a given choice of , and any , the function

provides a measure of the value of design when the true parameter is . It captures the improvement in decision quality due to design ’s inclusion in the choice set. Let

| (4) |

denote the expected value of under the posterior distribution at time . This can be viewed as the option-value of design : it is the expected additional value of having the option to choose design when it is revealed to be the best design. Note that the integral (4) defining is a weighted version of the integral defining . The paper will formalize a sense in which and are asymptotically equivalent as , and as a result the asymptotic analysis of top-two value sampling essentially reduces to the analysis of top-two probability sampling.

3.3 Thompson Sampling

Thompson sampling is an old and popular heuristic for multi-armed problems. The algorithm simply samples actions according to the posterior probability they are optimal. In particular, it selects action with probability , where denotes the probability action is optimal under under a parameter drawn from the posterior distribution.

Thompson sampling can have very poor asymptotic performance for the best arm identification problem. Intuitively, this is because once it estimates that a particular arm is the best with reasonably high probability, it selects that arm in almost all periods at the expense of refining its knowledge of other arms. If , then the algorithm will only select an action other than roughly once every 20 periods, greatly extending the time it takes until . This insight can be made formal; our results imply that Thompson sampling attains a only attains a polynomial, rather exponential, rate of posterior convergence. A similar reasoning applies to other multi-armed bandit algorithms. The work of Bubeck et al. (2009) shows formally that algorithms satisfying regret bounds of order are necessarily far from optimal for the problem of identifying the best arm.

With this in mind, it is natural to consider a modification of Thompson sampling that simply restricts the algorithm from sampling the same action too frequently. One version of this idea is proposed below.

3.4 Top-Two Thompson Sampling (TTTS)

This section proposes top-two Thompson sampling (TTTS), which modifies standard Thompson sampling by adding a re-sampling step. As with TTPS and TTVS, this algorithm depends on a tuning parameter that will sometimes be set to a default value of .

As in Thompson sampling, at time , the algorithm samples a design . Design is measured with probability , but, in order to prevent the algorithm from exclusively focusing on one action, with probability , an alternative design is measured. To generate this alternative, the algorithm continues sampling designs until the first time . This can be viewed as a top-two sampling algorithm, where the top-two are chosen by executing Thompson sampling until two distinct designs are drawn.

Under top-two Thompson sampling, the probability of measuring design at time is

This expression simplifies as the algorithm definitively identifies the best design. As , , and for each ,

In this limit, the true best design is sampled with probability . The probability is sampled given is not is equal to the posterior probability is optimal given is not.

3.5 Computing and Sampling According to Optimal Action Probabilities

Here we provide some insight into how to efficiently implement the proposed top-two rules in important problem classes. We begin with top-two Thompson sampling, which is often the easiest to implement. Note that given an ability to sample from , it is easy to sample from the posterior distribution over the optimal design . In particular, if is drawn randomly from the posterior, then is a random sample from . Either through the choice of conjugate prior distributions, or through the use of Markov chain Monte Carlo, it is possible to efficiently sample from the posterior for many interesting models. Algorithm 1 shows how to directly sample an action according to TTTS by sampling from the posterior distribution. It is worth highlighting that this algorithm does not require computing or approximating the distribution .

The optimal action probabilities and values are defined by -dimensional integrals, which may be difficult to compute in general even if the posterior has a closed form. Algorithm 2 shows how to approximate and using samples , which enables efficient approximations to TTPS and TTVS whenever posterior samples can be efficiently generated.

Thankfully, the computation of and simplifies when the algorithm begins with an independent prior over the qualities of the designs. To understand this fact, suppose are independently distributed and continuous random variables. Then

| (5) |

where denotes the PDF of and are the CDFs of . In particular, can be computed by solving a 1-dimensional integral. Based on this insight, Appendix B provides an efficient implementation of TTPS and TTVS for a problem with independent Beta priors and binary observations. That implementation approximates integrals like (5) using quadrature with points, and has the time and space complexity that scale as .

4 A Numerical Experiment

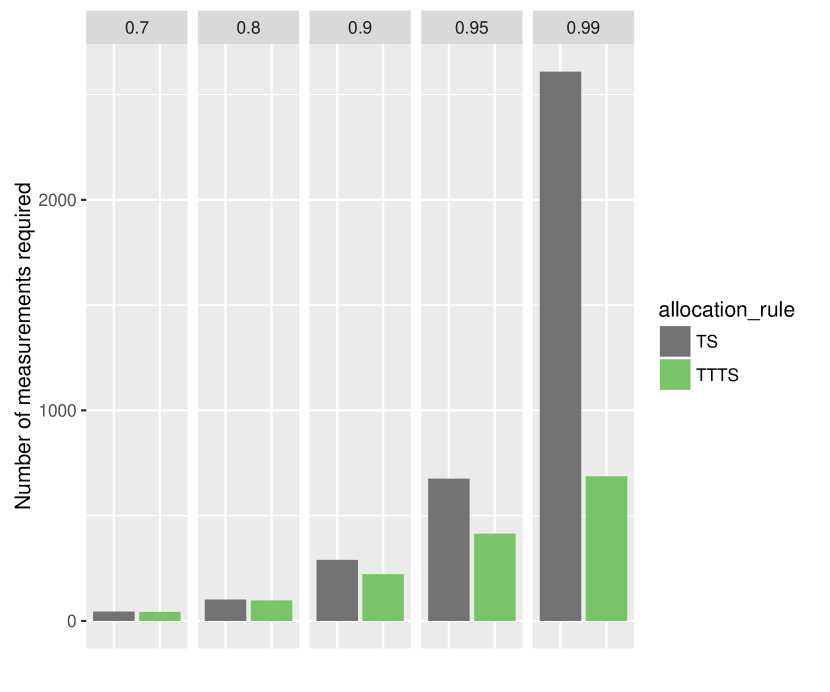

Some of the paper’s main insights are reflected in a simple numerical experiment. Consider a problem where observations are binary , and the unknown vector defines the true success probability of each design. Each algorithm begins with an independent uniform prior over the components of . The experiment compares the performance of top-two probability sampling (TTPS), top-two value sampling (TTVS)222TTVS is executed with the utility function , and top-two Thompson sampling (TTTS) with against Thompson sampling and a uniform allocation rule which allocates equal measurement effort ( to each design. The uniform allocation is a natural point of comparison, since is the most commonly used strategy in practice.

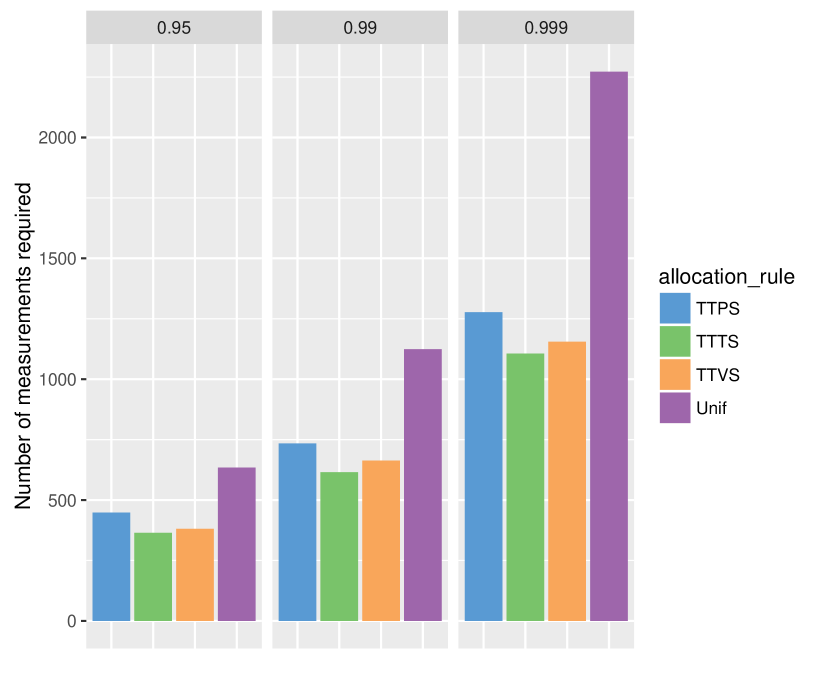

Figure 1 displays the average number of measurements required for the posterior to reach a given confidence level. In particular, the experiment tracks the first time when for various confidence levels . Figure 1 displays the average number of measurements required for each algorithm to reach each fixed confidence level, where the average was taken over 100 trials in Panel (a) and 500 in Panel (b). Even for this simple problem with five designs, the proposed algorithms can reach the same confidence level using fewer than half the measurements required by a uniform allocation rule. While all the top-two rules attain the same asymptotic rate of convergence, we can see that top-two probability sampling is slightly outperformed in this experiment. Panel (a) compares Thompson sampling to Top-Two Thompson sampling. TS appears to reach low confidence levels as rapidly as top-two TS, but as suggested in Subsection 3.3, is very slow to reach high levels of confidence. It requires over than 60% more measurements to reach confidence .95 and over 250% more measurements to reach confidence .99. TS requires an onerous number of measurements to reach confidence .999, and so we omit this experiment.

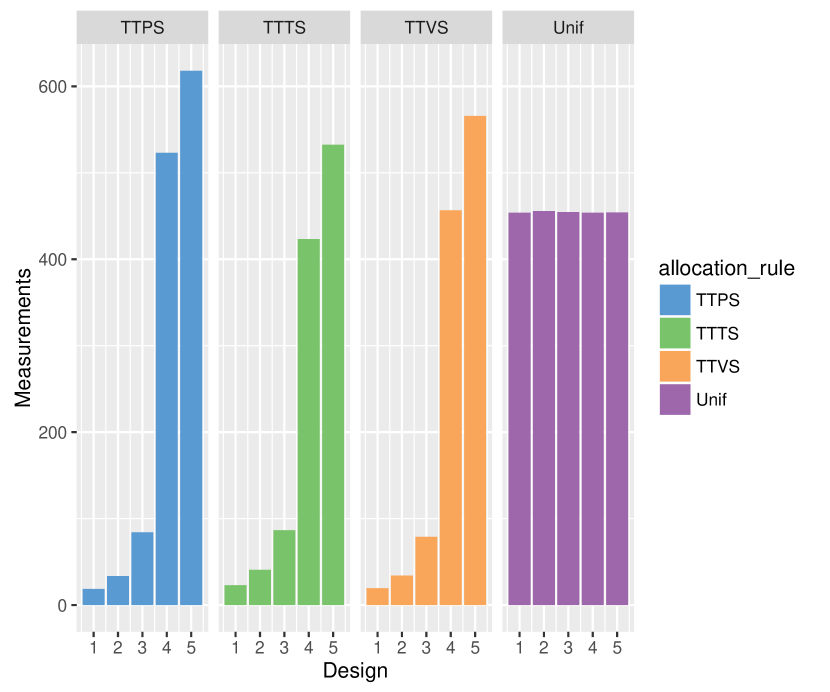

Figure 2 provides insight into how the proposed algorithms differ from the uniform allocation. It displays the distribution of measurements and posterior beliefs at the first time when a confidence level of .999 is reached. Again, all results are averaged across 500 trials. Panel (a) displays the average number of measurements collected from each design. It is striking that although TTTS, TTPS, and TTVS seem quite different, they all settle on essentially the same distribution of measurement effort. Because , roughly one half of the measurements are collected from . Moreover, fewer measurements are collected from designs that are farther from optimal, and most of the remaining half of measurement effort is allocated to design 4. Notice that using the same number of noisy samples it is much more difficult certify that than that , both because is closer to , and because observations from a Bernoulli distribution with parameter .4 have higher variance than under a Bernoulli distribution with parameter .1.

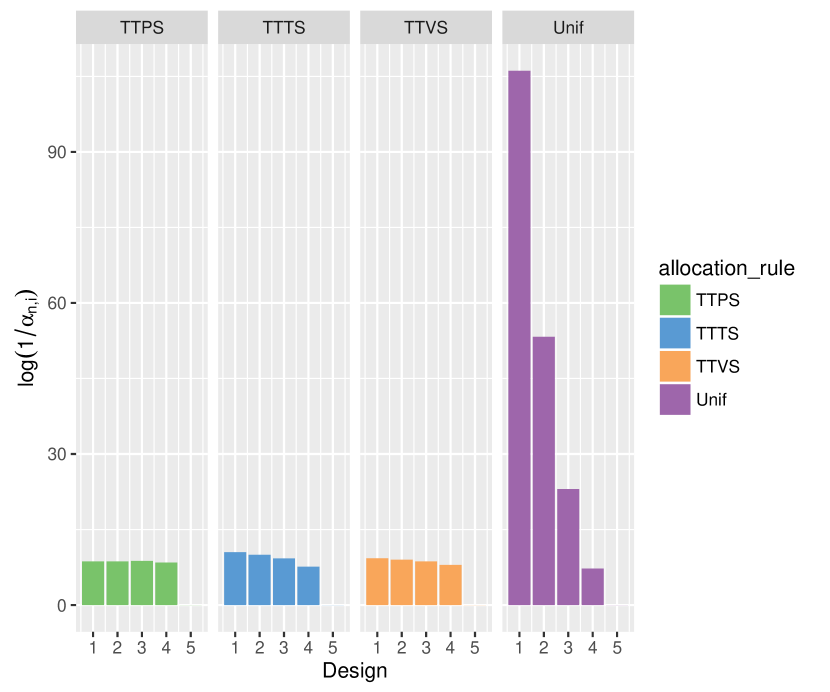

Panel (b) investigates the posterior probability assigned to the event that design is optimal. To make the insights more transparent, these are plotted on log-scale, where the value can roughly be interpreted as the magnitude of evidence that alternative is not optimal. By using an equal allocation of measurement effort across the designs, the uniform sampling rule gathers an enormous amount of evidence to rule out design 1, but an order of magnitude less evidence to rule out design 4. Instead of allocating measurement effort equally across the alternatives, TTTS, TTPS, and TTVS appear to exactly adjust measurement effort to gather equal evidence that each of the first four designs is not optimal.

Intuitively, in the long run each of the proposed algorithms will allocate measurement effort to design 5–the true best design–and to whichever other designs could most plausibly be optimal. If too much measurement effort has been allocated to a particular design, then the posterior will indicate that it is clearly suboptimal, and effort will be allocated elsewhere until a similar amount of evidence has been gathered about other designs. In this way, measurement effort is automatically adjusted to the appropriate level.

5 Main Theoretical Results

Our main theoretical results concern the frequentist consistency and rate of convergence of the posterior distribution. Recall that

captures the posterior mass assigned to the event that an action other than is optimal. One hopes that as the number of observations tends to infinity, so that the posterior distribution converges on the truth. We will show that under the TTTS, TTPS, and TTVS allocation rules, converges to zero an exponential rate and that the exponent governing the rate of convergence is nearly the best possible.

To facilitate theoretical analysis, we will make three additional boundedness assumptions, which are assumed throughout all formal proofs. This rules out some cases of interest, such the use of multivariate Gaussian prior. However, we otherwise allow for quite general correlated priors, expressed in terms of a density over a compact set. This stands in contrast, for example, to previous analyses of Thompson sampling, which tpyically rely heavily on the use of independent conjugate priors. Assumption 1 is used only in establishing certain asymptotic results concerning the rate of posterior concentration. Analogous results are easily established for certain unbounded conjugate priors333See for example Qin et al. (2017), which is a follow up to the current paper., but the author still has not identified the right technical conditions that generalize these results.

Assumption 1.

The parameter space is a bounded open hyper-rectangle , the prior density is uniformly bounded with

and the log-partition function has bounded first derivative with

The paper’s main results, as stated in the next theorem, characterize the rate of posterior convergence under the proposed algorithms, formalize a sense in which this is the fastest possible rate, and bound the impact of the tuning parameter . The statement depends on distribution-dependent constants and that are presented here but will be more explicitly characterized in Section 6.

The first part of the theorem shows that there is an exponent such that cannot converge to zero at a rate faster than under any allocation rule, and shows that TTPS, TTVS and TTTS attain this optimal rate of convergence when the tuning parameter is set optimally. This optimal exponent is shown to equal

where denotes the Kullback Leibler divergence between the observations distributions and . This can be viewed as the value of a game between two players. An experimenter first chooses a probability distribution over arms determining the frequency with which arms are measured. An adversary then chooses the worst case configuration of arm means, selecting an alternative that is hard to distinguish from under the measurement allocation , but under which the arm is no longer optimal.

The remainder of the theorem investigates the role of the tuning parameter . Part 2 shows that there is an exponent such that at rate under TTPS, TTVS, or TTTS with parameter , and this is shown to be optimal among a restricted class of allocation rules. In particular, we observe that controls the fraction of measurement effort allocated to the true best design , in the sense that as under each of the proposed algorithms. These algorithms attain the error exponent

which is analogous to except that the experimenter is constrained to measure the true best arm with fraction of measurement effort. A lower bound shows this exponent is optimal among a constrained class: precisely, on any sample path on which an adaptive algorithm allocates a faction of overall effort to measuring , the posterior cannot converge at rate faster than . In this sense, while a tuning parameter controls the long-run measurement effort allocated to the true best design, TTPS, TTVS, and TTTS all automatically adjust how remaining the measurement effort is allocated among the suboptimal designs in an asymptotically optimal manner.

The final part of the theorem shows that the constrained exponent is close to the largest possible exponent whenever is close to the optimal value. The choice of is particularly robust: is never more than a factor of 2 away from the optimal exponent.

Theorem 1.

There exist constants such that exists, is unique, and the following properties are satisfied with probability 1:

-

1.

Under TTTS, TTPS, or TTVS with parameter ,

Under any adaptive allocation rule,

-

2.

Under TTTS, TTPS, or TTVS with parameter ,

Under any adaptive allocation rule,

-

3.

and

This theorem is established in a sequence of results in Section 6. The lower bounds in parts 1 and 2 are given respectively in Propositions 6 and 7. Proposition 8 shows the top-two rules attain these optimal exponents. Part 3 is stated as Lemma 3 in Section 6.

5.1 An upper bound on the error exponent

Before proceeding, we will state an upper bound on the error exponent when that is closely related to complexity terms that have appeared in the literature on best–arm identification (e.g. Audibert and Bubeck (2010)). This bound depends on the gaps between the means of the different observation distributions.

We say that a real valued random variable is –sub–Gaussian if so that the moment generating function of is dominated by that of a zero mean Gaussian random variable with variance . Gaussian random variables are sub-Gaussian, as are uniformly bounded random variables. The next result applies to both Bernoulli and Gaussian distributions, as each can be parameterized with sufficient statistic .

Proposition 1.

Suppose the exponential family distribution is parameterized with and that each , if , then is sub-Gaussian with parameter Then

where for each ,

is the difference between the mean under and the mean under .

This shows that decays at asymptotic rate faster than so convergence is rapid when there is a large gap between the means of different designs. In fact, Proposition 1 replaces the dependence on times the smallest gap with a dependence on , which captures the average inverse gap. This rate is attained only by an intelligent adaptive algorithm which allocates more measurement effort to designs that are nearly optimal and less to designs that are clearly suboptimal. In fact, the next result shows that the asymptotic performance of uniform allocation rule depends only on the smallest gap and therefore even if some designs could be quickly ruled out, the algorithm can’t leverage this to attain a faster rate of convergence.

Proposition 2.

If and for each ,

under a uniform allocation rule which sets for each and .

5.2 Consistent Tuning of

Our previous results show that if the top-two sampling algorithms are applied with the optimal problem dependent tuning parameter , then these algorithms attain the optimal rate of posterior convergence . Unfortunately is is typically unknown, and so we also investigate robustness to the choice of , both in theory as in Theorem 1 above, and in simulation experiments presented in Section 7. Still, a natural question is whether this tuning parameter can be adjusted in a dynamic fashion to converge on . We begin the study of such extensions in this subsection.

First, note that it is easy to extend the definition of each top to sampling algorithm so that they use an adaptive sequence of tuning parameters . For example, top-two probability sampling identifies and and then chooses among these with respective probabilities and . The next lemma confirms that, if applied with such a sequence of tuning parameters such that , the top-two sampling algorithms attain the optimal convergence rate .

Proposition 3.

Suppose TTTS, TTVS, TTPS are applied with an adaptive sequence of tuning parameters where for each , is measurable. Then, with probability 1, on any sample path on which ,

The next lemma confirms that such consistent tuning is possible. The method for tuning , presented Algorithm 3, simply solves numerically for the optimal value of assuming that the true values of the parameters are given by their respective posterior means.

Unfortunately, this tuning method is complex, spoiling some of elegance of the top-two sampling algorithms. A significant open question is whether simpler methods for adapting could be adopted.

Lemma 1.

Under TTTS, TTPS, or TTVS with an adaptive sequence of tuning parameters adjusted according to Algorithm 3, almost surely. Therefore .

6 Analysis

6.1 Asymptotic Notation.

To simplify the presentation, it is helpful to introduce additional asymptotic notation. We say two sequences and taking values in are logarithmically equivalent, denoted by , if as . This notation means that and are equal up to first order in the exponent. With this notation, Theorem 1 implies the top-two sampling rules with parameter attain the convergence rate . This is an equivalence relation, in the sense that if and then . Note that , so that the sequence with the largest exponent dominates. In addition for any positive constant , , so that constant multiples of sequences are equal up to first order in the exponent. When applied to sequences of random variables, these relations are understood to apply almost surely.

It is natural to wonder whether the proposed algorithms asymptotically minimize expressions like , which account for how far some designs are from optimal. We note in passing, that

for any positive costs , and so any such performance measures are equal to first order in the exponent. Similar observations have been used to justify the study of the probability of incorrect selection, rather than notions of the expected cost of an incorrect decision (Glynn and Juneja, 2004; Audibert and Bubeck, 2010).

6.2 Posterior Consistency

The next proposition provides a consistency and anti-consistency result for the posterior distribution. The first part says that if design receives infinite measurement effort, the marginal posterior distribution of its quality concentrates around the true value . The second part says that when restricted to designs that are not measured infinitely often, the posterior does not concentrate around any value. The posterior converges to the truth as infinite evidence is collected, but nothing can be ruled out with certainty based on finite evidence.

Proposition 4.

With probability 1, for any if , then, for all

If is nonempty, then

for any collections of open intervals ranging over .

This result is the key to establishing that under each of the proposed algorithm. The next subsection gives a more refined result that allows us to to characterize the rate of convergence.

6.3 Posterior Large Deviations

This section provides an asymptotic characterization of posterior probabilities for any open set and under any adaptive measurement strategy. The characterization depends on the notion of Kullback-Leibler divergence. For two parameters , the log-likelihood ratio, , provides a measure of the amount of information provides in favor of over . The Kullback-Leibler divergence

is the expected value of the log-likelihood under observations drawn . Then, if the design to measure is chosen by sampling from a probability distribution over ,

is the average Kullback-Leibler divergence between and under .

Under the algorithms we consider, the effort allocated to measuring design , , changes over time as data is collected. Recall that captures the fraction of overall effort allocated to measuring design over the first periods. Under an adaptive allocation rule, is function of the history and is therefore a random variable. Given that measurement effort has been allocation according to , quantifies the average information acquired that distinguishes from the true parameter . The following proposition relates the posterior mass assigned to to , which captures the element in that is hardest to distinguish from based on samples from .

Proposition 5.

For any open set ,

To understand this result, consider a simpler setting where the algorithm measures design in every period, and consider some with . Then the log-ratio of posteriors densities

can be written as the sum of the log-prior-ratio and the log-likelihood-ratio. The log-likelihood ratio is negative drift random walk: it is the sum of i.i.d terms, each of which has mean

Therefore, by the law of large numbers, as , , or equivalently, the ratio of the posterior densities decays exponentially as

This calculation can be carried further to show that if the designs measured () are drawn independently of the observations () from a fixed probability distribution , then

| (6) |

Now, by a Laplace approximation, one might expect that the integral is extremely well approximated by integrating around a vanishingly small ball around the point

These are the main ideas behind Proposition 5, but there are several additional technical challenges involved in a rigorous proof. First, we need that a property like (6) holds when the allocation rule is adaptive to the data. Next, convergence of the integral of the posterior density requires a form of uniform convergence in (6). Finally, since changes over time, the point changes over time and basic Laplace approximations don’t directly apply.

6.4 Characterizing the Optimal Allocation

Throughout this paper, an experimenter wants to gather enough evidence to certify that is optimal, but since she does not know , she does not know which measurements will provide the most information. To characterize the optimal exponent , however, it is useful to consider the easier problem of gathering the most effective evidence when is known. We can cast this as a game between two players:

-

•

An experimenter, who knows the true parameter , chooses a (possibly adaptive) measurement rule.

- •

-

•

How can the experimenter gather the most compelling evidence? A rule which is optimal asymptotically should maximize the rate at which as

In order to drive the posterior probability to 1, the decision-maker must be able to rule out all parameters in under which the optimal action is not . Our analysis shows that the posterior probability assigned to is dominated by the parameter that is hardest to distinguish from under . In particular, by Proposition 5,

as Therefore, the solution to the max-min problem

| (7) |

represents an asymptotically optimal allocation rule. As highlighted in the literature review, the max-min problem (7) closely mirrors the main sample complexity term in Chernoff’s classic paper on the sequential design of experiments (Chernoff (1959)).

Simplifying the optimal exponent.

Thankfully, the best-arm identification problem has additional structure which allows us to simplify the optimization problem (7). Much of our analysis involves the posterior probability assigned to the event some action is optimal. This can be difficult to evaluate, since the set of parameter vectors under which is optimal

involves separate constraints. Consider instead a simpler problem of comparing the parameter against . For each define the set

under which the value at exceeds that at . Since, ignoring the boundary of the set, ,

and therefore

| (8) |

This yields an analogue of (7) that will simplify our subsequent analysis. Combining (8) with Proposition 5 shows the solution to the max-min problem

| (9) |

represents an asymptotically optimal allocation rule. Because the set involves only a constraints on and , we can derive an expression the inner minimization problem over in terms of the measurement effort allocated to and . Define

| (10) |

The next lemma shows that the function arises as the solution to the minimization problem over in (9). It also shows that the minimum in (10) is attained by a parameter under which the mean observation is a weighted combination of the means under and . Recall that, for an exponential family distribution is the mean observation of the sufficient statistic under .

Lemma 2.

For any and probability distribution over

In addition, each is a strictly increasing concave function satisfying

where is the unique solution to

Lemma 2 and equation (9) immediately imply

| (11) |

This result essentially shows that the earlier form of hte exponent, which is similar to a problem complexity measure in Chernoff (1959), is equivalent to the large deviations exponent suggested in Glynn and Juneja (2004). The function captures the effectiveness with which one can certify using an allocation rule that measures actions and with respective frequencies and . Naturally, it is an increasing function of the measurement effort allocated to designs and . For given and , when , reflecting that is easier to distinguish from than .

Example 1.

(Gaussian Observations) Suppose each outcome distribution is Gaussian with unknown mean . Then direct calculation using Lemma 2 shows

To understand this formula, imagine we use a deterministic allocation rule that collects and observations from and . Let and denote the respective sample means. The empirical difference is normally distributed where and . Standard Gaussian tail bounds imply that as , , and so appears to characterize the probability of error.

The next proposition formalizes the derivations in this section, and states that the solution to the above maximization problem attains the optimal error exponent. Recall that denotes the measurement effort assigned design at time .

Proposition 6.

Let denote the optimal solution to the maximization problem (11). If for all , then

Moreover under any other adaptive allocation rule,

This shows that under the fixed allocation rule error decays as , and that no faster rate of decay is possible, even under an adaptive allocation.

An Optimal Constrained Allocation.

Because the algorithms studied in this paper always allocate –fraction of their samples to measuring in the long run, they may not exactly attain the optimal error exponent. To make rigorous claims about their performance, consider a modified version of the error exponent (11) given by the constrained max-min problem

| (12) |

This optimization problem yields the optimal allocation subject to a constraint that –fraction of the samples are spent on . The next subsection will show that TTTS, TTPS, and TTVS attain the error exponent . The next proposition formalizes that the solution to this optimization problem represents an optimal constrained allocation. In addition, it shows that the solution is the unique feasible allocation under which is equal for all suboptimal designs . To understand this result, consider the case where there are three designs and . If , then , reflecting that it is more difficult to certify that than . The next proposition shows it is optimal to decrease and increase , until the point when . Instead of allocating equal measurement effort to each alternative, it is optimal to adjust measurement effort to gather equal evidence to rule out each suboptimal alternative. The results in this proposition are closely related to those in Glynn and Juneja (2004), in which large deviations rate functions take the place of the functions .

Proposition 7.

The solution to the optimization problem (12) is the unique allocation satisfying and

If for all , then

Moreover under any other adaptive allocation rule, if then

almost surely.

The following lemma relates the constrained exponent to .

Lemma 3.

For and any ,

Therefore .

6.5 Convergence of Top-Two Algorithms

Instead of attempting to directly solve the optimization problem (11), this paper focuses on simple and intuitive sequential strategies. These algorithms have the potential to explore much more intelligently in early stages, as they carefully measure and reason about uncertainty. While they ostensibly have no connection to the derivations earlier in this section, we establish that remarkably all three automatically converge to the unknown optimal allocation. This is shown formally in the next result.

We are now ready to establish the paper’s main claim, which shows that TTTS, TTPS, and TTVS each attain the error exponent .

Proposition 8.

Under the TTTS, TTPS, or TTVS algorithm with parameter , , where is the unique allocation with satisfying

Therefore,

To understand this result, imagine that is very large, and . If the algorithm has allocated too much measurement effort to a suboptimal action , with for a constant , then it must have allocated too little measurement effort to at least one other suboptimal design . Since much less evidence has been gathered about than , we expect . When this occurs, TTTS, TTPS and TTVS essentially never sample action until the average effort allocated to design dips back down toward . This seems to suggest that the algorithm cannot allocate too much effort to any alternative, but that in turn implies that it never allocates too little effort to measuring any alternative.

6.6 Asymptotics of the Value Measure

The proof for top-two value sampling relies on the following lemma, which shows that the posterior value of any suboptimal design is logarithmically equivalent to its probability of being optimal.

Lemma 4.

For any ,

Note that by this lemma,

and so all of the asymptotic results in this could be reformulated as statements concerning the value assigned to suboptimal alternatives under the posterior.

The lemma is not so surprising, as differs from only because of the function . The term dominates this integral as , since it tends to zero at an exponential rate in whereas is a fixed function of .

7 Further Simulation Experiments

This section presents further simulation results. The focus is not on competitive benchmarking across the wide array of algorithms that have been proposed by researchers in statistics, operations research and computer science. While this could be enormously valuable, carrying out such experiments in a fair manner has proved challenging, as these algorithms are often derived under differing modeling assumptions and differing problem objectives, as well as with numerous tuning parameters that muddle comparisons. We instead aim here to focus on gaining clear insight into two questions. Namely:

-

1.

How robust is the performance of the proposed top-two sampling algorithm to the choice of tuning parameter? Precisely, across a range of problem instances, how does top-two sampling with the default choice of compare relative to an omniscient version of the algorithm, which uses the optimal tuning parameter for that instance?

-

2.

How do top-two sampling algorithms, which need to learn and adapt to the long run optimal sampling proportions on each problem instance , perform relative to an omniscient policy that knows and tracks the ideal sampling proportions on each problem instance?

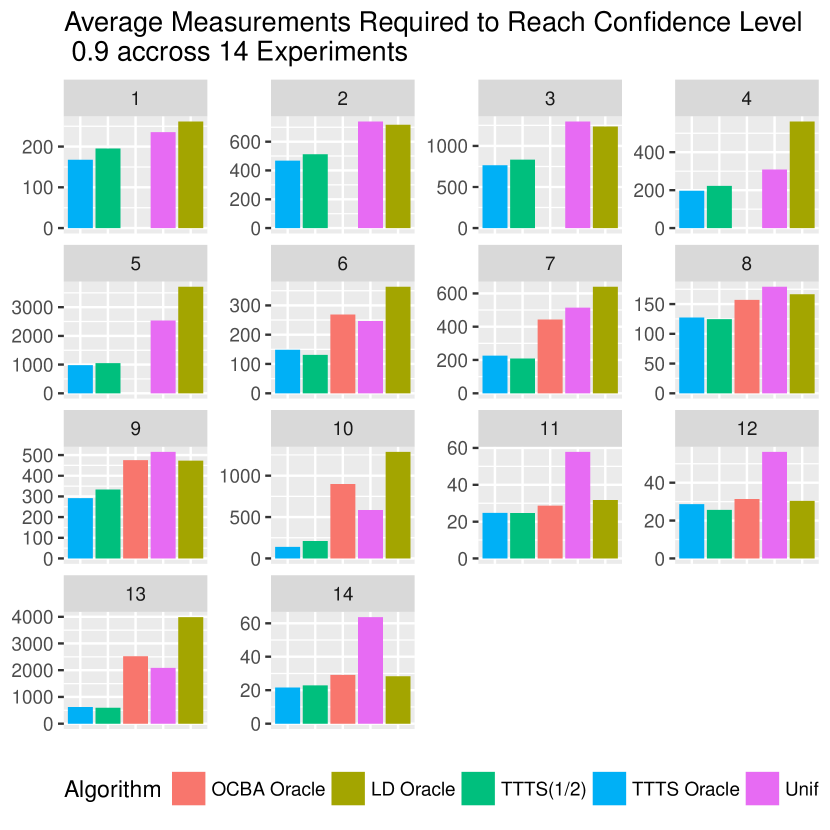

This section presents simulation results across 14 problem settings. To reduce computational burden, as well as simplify the presentation of the results, the section focuses on top-two Thompson sampling and omits the other two variants of top-two sampling. The results reveal strong performance of top-two Thompson sampling with the ad-hoc choice of tuning parameter . Interesting, this method also consistently, and often substantially, outperforms the oracle policy .

Each of the fourteen experiments investigates a different problem setting as described in Table 1 below. The problems are divided between those with binary observations and those with standard Gaussian observation noise . For the binary experiments an independent uniform prior is used, while an independent prior is used for the second experiment. We consider several types of configurations for the arm means. Experiments 10-14 present randomly drawn instances, where each was sampled independently for standard normal distribution. These were drawn using the numpy.random.normal function with seeds 1,2,3,4 and 5, respectively. In the configurations labeled “ascending”, the arm means increase from lowest to highest with uniform separation between the arms. The slippage configuration was included specifically to investigate cases where top-two sampling performs poorly. In such settings, an equal allocation across arms attains an exponent that is quite competitive, as there are no very poor arms that can be easily ruled out using fewer samples. In addition, the exponent attained by TTTS with can be farther from the optimal than under other problem instances. The ratio of exponents is displayed for each instance.

| Noise | Configuration | True Arm Means | |||

|---|---|---|---|---|---|

| 1 | Binary | Slippage | 5 | (0.3, 0.3, 0.3, 0.3, 0.5) | 1.12 |

| 2 | Binary | Slippage | 10 | (0.3, 0.3, 0.3, 0.3, 0.3, 0.3, 0.3, 0.3, 0.3, 0.5) | 1.26 |

| 3 | Binary | Slippage | 15 | (0.3, 0.3, 0.3, 0.3, …, 0.3, 0.3, 0.3, 0.3, 0.5) | 1.34 |

| 4 | Binary | Ascending | 5 | (0.1, 0.2, 0.3, 0.4, 0.5) | 1.01 |

| 5 | Binary | Ascending | 10 | (0.05, 0.1, 0.15, 0.2, 0.25, 0.3, 0.35, 0.4, 0.45, 0.5) | 1.01 |

| 6 | Gaussian | Ascending | 5 | (-0.5, -0.25, 0, 0.25, 0.5) | 1.01 |

| 7 | Gaussian | Ascending | 10 | (-0.5, -0.5, -0.5, -0.5, -0.5, -0.5, -0.25, 0, 0.25, 0.5) | 1.03 |

| 8 | Gaussian | Slippage | 5 | (0, 0, 0, 0, 0.5) | 1.11 |

| 9 | Gaussian | Slippage | 10 | (0, 0, 0, 0, 0, 0, 0, 0, 0, 0.5) | 1.25 |

| 10 | Gaussian | Random | 10 | (-2.3, -1.1, -0.8, -0.6, -0.5, -0.2, 0.3, 0.9, 1.6, 1.7) | 1.00 |

| 11 | Gaussian | Random | 10 | (-2.1, -1.8, -1.2, -1.1, -0.9, -0.8, -0.4, -0.1, 0.5, 1.6) | 1.10 |

| 12 | Gaussian | Random | 10 | (-1.9, -0.6, -0.5, -0.4, -0.3, -0.1, -0. , 0.1, 0.4, 1.8) | 1.19 |

| 13 | Gaussian | Random | 10 | (-1.6, -1.1, -1. , -0.6, -0.4, 0.1, 0.3, 0.5, 0.6, 0.7) | 1.01 |

| 14 | Gaussian | Random | 10 | (-0.9, -0.6, -0.3, -0.3, -0.3, 0.1, 0.2, 0.4, 1.6, 2.4) | 1.04 |

Figure 3 displays the average number of measurements required for the posterior to reach a given confidence level. In particular, the experiment tracks the frist time when for confidence levels and . All results are averaged over 400 trials.

The “Large deviations oracle,” labeled “LD oracle” in Figure 3, implements the optimal fixed allocation as prescribed by large deviations theory. At each time , the algorithm constructs the target proportions and plays the arm that is most under-sampled relative to these proportions. For problems with Gaussian noise, the optimal computing budget allocation (OCBA) of Chen et al. (2000) is a widely used approximation to the fixed allocation . The algorithm labeled OCBA oracle implements the true sampling proportions specified by Chen et al. (2000) for each problem instance. We also compare the uniform, or equal allocation, TTTS with tuning parameter and TTTS Oracle, which is TTTS with the optimal problem dependent tuning parameter .

At a high level, there are two key findings from these experiments. In all cases, sample size comparisons refer to the confidence level .

-

1.

Top-two Thompson sampling with tuning parameter 1/2 generally offers similar performance to top-two Thompson sampling with the optimal tuning parameter . The most significant separation in performance was on slippage configurations, where TTTS with optimal tuning parameter saved up to 15% of samples on average. On most other instances, using the optimal tuning parameter offered no improvement.

-

2.

The large deviations oracle and the OCBA oracle were consistently, and sometimes dramatically, outperformed. Each one required least 19% more samples on average than for all 14 experiments. In their worst experiments, the LD oracle and OCBA oracle used respectively more than 200% and 300% the average number of samples used by .

The second finding may be quite surprising to some readers. There is a quite a large literature that aims to implement optimal large deviations allocations derived in Glynn and Juneja (2004), or a simpler approximation to these in the Gaussian case known as the OCBA (Chen et al., 2000). Such approaches have also been extended to a number of related problem settings. A major challenge, however, is that the allocations cannot be directly implemented as they require knowledge of the true problem instance . Researchers typically implement an approach that solves for the optimal budget allocation under point estimate of , aiming to converge to the prescribed optimal sampling proportions as rapidly as possible. Here, we instead compete against an oracle that knows and carefully follows the asymptotically optimal sampling proportions for each problem instance. Even these oracle policies are significantly outperformed by Top-two Thompson with the an ad-hoc choice of tuning parameter.

It is an open question to formalize the reasons for this empirical finding. It is worth offering some possible intuition, however. First, the oracle allocations are based on a number of approximations, including tail approximations to the posterior of each arm and certain union bounds or Bonferonni approximations. By contrast, Thompson sampling uses exact samples from the posterior distribution, and may more accurately reflect uncertainty in early stages. Second, even if the oracle allocations know the true-arm means, they do not adapt in response to unusual observations. Thompson sampling, on the other hand is fully adaptive, and can gather fewer samples from an arm if early samples provide strong evidence that arm is suboptimal. Some of the benefits of adaptivity are suggested in .

8 Extensions and Open Problems

This paper studies efficient adaptive allocation of measurement effort for identifying the best among a finite set of options or designs. We propose three simple Bayesian algorithms. Each is a variant of what we call top-two sampling, which, at each time-step, measures one of the two designs that appear most promising given current evidence. Surprisingly, these seemingly naive algorithms are shown to satisfy a strong asymptotic optimality property.

Top two sampling appears to be a general design principle that can be extended to address a variety of problems beyond to the scope of this paper. To spur research in this area, we briefly discuss a number of extensions and open questions below.

Top-Two Sampling Via Constrained MAP Estimation.

Here we present a version of top-two sampling that uses MAP estimation. This can simplify computations, as MAP estimates can be computed without solving for the normalizing constant of the posterior density . Consider the following procedure for selecting a design at time :

-

1.

Compute and set .

-

2.

Compute and set .

-

3.

Play with respective probabilities .

The first step uses MAP estimation to make a prediction of the best design, while the second uses constrained MAP estimation to identify the alternative design that is most likely to be optimal when is not. Many of the asymptotic calculations in the previous section appear to extend to this algorithm, but proving this formally is left as an open problem.

Indifference Zone Criterion.

Suppose our goal is to confidently identify an –optimal arm, for a user specified indifference parameter . Much of the paper investigates the set of parameters under which arm is optimal, and studies the rate at which . Now, let us instead consider the set of parameters

under which is –optimal. It is easy to develop a variety of modified top-two sampling rules under which rapidly. For example, we can extend TTPS as follows: set . Define to be the alternative design that is most likely to be optimal and offer an –improvement over . A top-two Thompson sampling approach might instead continue sampling until and then set .

Top –arm identification.

Suppose now that our goal is to identify the top designs. Consider choosing a design to measure at time by the following steps:

-

1.

Sample and compute the top designs under .

-

2.

Continue sampling until the top designs under differ from those under .

-

3.

Identify the set of designs that are in the top under or under , but not under both. Choose a design to measure by sampling one uniformly at random from this set.

This is the natural extension of top-two Thompson sampling to the top- arm problem. In fact, when , this is exactly TTTS with . I conjecture that like the case where , this algorithm attains a rate of posterior convergence within a factor of 2 of optimal for general . The optimal exponent for this problem can be calculated by mirroring the steps in Subsection 6.4.

Extremely Correlated Designs.

While our results apply in the case of correlated priors, the proposed algorithms may be wasteful when there are a large number of designs whose qualities are extremely correlated. As an example, consider an extension of our techniques to a pure-exploration variant of a linear bandit problem. Here we associate each action with a feature vector and seek an action that maximizes . The vector is unknown, but we begin with a prior and see noisy observations of whenever action is selected. To apply top-two sampling to this problem, we should modify the algorithm’s second step. For example, under top-two Thompson sampling, we usually begin drawing a design according to , and then continue drawing designs until . These are played with respective probabilities . But even if , their features may be nearly identical. A more natural extension of top-two Thompson sampling would modify the second step, and continue sampling , until a sufficiently different action is drawn – for example until the angle between and exceeds a threshold.

Tuning .

The most glaring gap in this work may be arbitrary choice of tuning parameter . Optimal asymptotic rates can be attained by adjusting this parameter over time by solving for an optimal allocation as in (11). It is an open problem to instead develop simple algorithms that set automatically through value of information calculations, or avoid the need for such a parameter altogether.

Adaptive Stopping.