Polynomial Diffusion Models for Life Insurance Liabilities

Abstract

In this paper we study the pricing and hedging problem of a portfolio of life insurance products under the benchmark approach, where the reference market is modelled as driven by a state variable following a polynomial diffusion on a compact state space. Such a model can be used to guarantee not only the positivity of the OIS short rate and the mortality intensity, but also the possibility of approximating both pricing formula and hedging strategy of a large class of life insurance products by explicit formulas.

JEL Classification: C02, G10, G19

Key words: life insurance liability, polynomial diffusion, benchmark approach, stochastic mortality intensity, benchmarked risk-minimization.

1 Introduction

The goal of this paper is to analyse the problem of pricing and hedging portfolios of life insurance liabilities under the new approach of combining the benchmark methodology and the existence of a polynomial diffusion state variable which moves on a compact state space and drives the reference market. We consider on the market OIS bonds as well as longevity bonds, both modelled as function of the state variable representing the underlying risk factors, possibly including macro-economic variables, environmental and social indicators. In this way we also introduce a dependence structure between OIS short rate and mortality intensity. Recent studies, see e.g. [35], [13] and [15], confirm the important role of this dependence structure when pricing life insurance liabilities.

The biggest advantage of polynomial diffusions is that they give explicit and tractable formula for conditional expectation of polynomial functions of state variable, see [23]. In our model, we focus in particular on the case when the state variable takes value in a compact state space, which is studied in detail in [32]. Under our model assumptions, the compactness of the state space guarantees the positivity of both OIS short rate and mortality intensity, as well as the possibility of using polynomial approximation for pricing and hedging life insurance liabilities. Nevertheless, the compactness of the state variable implies also the boundedness of OIS short rate and mortality intensity. However, the assumption of bounded short rate is not new to the literature (see e.g. [44], [25], [17], [2], [34] etc.), as well as the assumption of bounded mortality intensity (see e.g. [33]). This last assumption is also supported by recent statistical studies of mortality rates (see e.g. [19] and [31]) and can be understood in terms of confidence region (see [33]).

Unlike [23], we do not assume the existence of a state price density which is equivalent to the existence of a martingale measure. We work under the historical or real world probability measure and assume only the existence of a benchmark or numéraire portfolio, as proposed by E. Platen (see e.g. [39], [41], [42]). As pointed out by [28], this assumption equals the no unbounded profit with bounded risk condition, which is weaker than the classic risk-neutral condition of no free-lunch with vanishing risk (see e.g. [16]) equivalent to the existence of a martingale measure. The hybrid market composed by both financial and insurance market is intrinsically incomplete due to the presence of additional orthogonal sources of randomness given by the mortality risk. The securitization under the benchmark approach can be resolved by the so called benchmarked risk-minimizing method, see e.g. [40], [42], [20] and [6] for a single payoff. Here we extend the results in [6] of hedging in incomplete markets under the benchmark approach to the case of assets with dividend payments and analyse its relation with the real world pricing formula.

The paper is structured as follows. Section 2 provides a brief introduction of polynomial diffusions. Section 3 gives the basic model structure assumptions for a portfolio of life insurance policies under the intensity-based approach. A benchmark portfolio is assumed to exist. Benchmark portfolio, OIS bond and longevity bond are then modelled explicitly in terms of a possibly multi-dimensional state variable which follows a polynomial diffusion on a compact state space. The real world pricing formula is provided explicitly in Section 4 for all three building blocks of insurance products (pure endowment, term insurance, annuity) in the case of payoff given by polynomial functions of the state variable. We then show how these explicit results can be used to approximate more general forms of payment process. For the sake of simplicity, we derive explicitly the benchmarked risk-minimizing strategy and its polynomial approximation only for pure endowment contracts, since the other two cases are similar. In Section 5 we use a 2-dimensional state variable and calibrate our model to MSCI and LLMA index under linear specification of the inverse of benchmark and the longevity index. We show how this parsimonious specification can already produce a good fit to market data. In Appendix A we extend the real world pricing formula and the benchmarked risk-minimizing method to dividend payments and discuss their relationship.

2 Polynomial diffusion

In this section, we give a synthetic overview of the most important results for polynomial diffusions which will be used to model our market. For details about these processes, see [23].

Let be a compact set with non-empty internal part, called state space. Let denote the space of real symmetric matrices, and the convex cone of positive semidefinite symmetric matrices. For a given , we denote furthermore by the following finite-dimensional vector space

and by the dimension of . We consider a fixed time horizon and an -valued process , with the following dynamics

| (2.1) |

realized on a filtered probability space , with . is a -dimensional -Brownian motion, is a continuous function, , and are two fixed maps

such that

| (2.2) |

for all . The initial value is assumed to be constant and belonging to .

We consider the following operator associated to the process

defined by

| (2.3) |

Definition 2.1.

An -valued process satisfying (2.1) is called a polynomial diffusion on if

Lemma 2.2 of [23] shows that is a polynomial diffusion on if and only if (2.2) holds. In such case, for every fixed , its associated operator admits a unique matrix representation restricted to . That is, for each with coordinate representation

| (2.4) |

where is a fixed basis vector of and , we have

The following proposition gives one of the most important results for polynomial diffusions: the -martingale generated by a polynomial function of is again given by a polynomial function of the state variable with deterministic time-dependent coefficients.

Proposition 2.2 (Polynomial conditional expectation).

Proof.

See Theorem 3.1 of [23]. ∎

For the sake of simplicity, we introduce the notation

The following two theorems give some sufficient conditions on the state space , under which an -valued state variable admits weak uniqueness and existence.

Theorem 2.3.

Proof.

See Theorem 5.1 of [23]. ∎

Remark 2.4.

Theorem 2.5.

Let be a family of polynomials on . If the boundary of the state space is defined by these polynomials, i.e.

then the following conditions on the parameters and guarantee the existence of an -valued solution to (2.1):

-

1.

;

-

2.

on for each ;

-

3.

on for each .

Proof.

This theorem is a simplified version of Theorem 5.3 of [23]. ∎

3 The Setting

In this paper, we follow the intensity-based reduced-form approach (e.g. [10]) in order to describe life insurance derivatives linked to a portfolio of life insurance contracts.

We fix a finite time horizon with and a filtered probability space , with , . The filtration represents all the information flow available to the insurance company. is interpreted as the historical or real world probability measure. We consider a life insurance portfolio with policyholders (). For , the decease time of -th insured person is assumed to be a -measurable random time , , such that a.s., and for any . These last conditions mean that the decease of a policyholder does not occur in the first instant and may never occur during the considered time horizon . We denote the death counting process by ,

| (3.1) |

Furthermore, we assume where for , , , , . The filtration is called reference filtration. For each , the filtration is generated by the jump process of defined by with for every , i.e. the filtration represents the information through time relative to -th policyholder’s life status described by . All the filtrations are assumed to be complete and right-continuous. Every random variable for is clearly a -stopping time, but not necessary an -stopping time. We assume also that for each , and that and are -conditionally independent, i.e. for any and ,

This assumption can be interpreted in the following way. The life status of policyholders is influenced by some common systematic factors related to environmental, economic, social and financial conditions captured by the information flow represented by , but every policyholder has also his own purely individual or idiosyncratic decease factors (e.g. illness, accident etc.).

Moreover, we assume that

-

1.

The subfiltration of satisfies the so called -hypothesis, i.e. every -martingale is also a -martingale.

-

2.

For every , the following non-negative -submartingale , called conditional cumulative distribution function of

satisfies

and is absolutely continuous with respect to Lebesgue’s measure.

For every , the hazard process of

is well defined, absolutely continuous and increasing (see Lemma 6.1.2 of [10]). On one hand, this implies that, for every , avoids all -stopping times and is a -totally inaccessible stopping time (see [18]). On the other hand, the absolute continuity of implies the existence of a non negative -progressively measurable mortality intensity with integrable sample paths such that

We can take a -predictable version of , see Lemma 1.36 of [29]. For the sake of simplicity, we assume a homogeneous insurance portfolio where all policyholders have the same mortality rate and we denote the common conditional cumulative distribution function, hazard process and mortality intensity respectively by , and , i.e. , , for all . This happens for example when all policyholders belong to the same age cohort in the same country444The number of the reference population group is normally much bigger than .. We assume furthermore that there is a publicly accessible index based on mortality data of the given age group. According to [12], such index is modelled by the process , where

and is called survival index (or longevity index or longevity process) related to the given group of people555The assumption of a homogeneous portfolio can be easily relaxed and extended to the case of more population groups, subdivided by age cohorts, countries etc.. In that case, every group of people is assumed to have its correspondent longevity index and mortality intensity.. We stress that under our assumptions, the reference filtration gives information about the (common) mortality intensity , or equivalently the longevity index , but not about a single decease event itself. For , we introduce the process associated to the -th policyholder

| (3.2) |

Proposition 5.7 and Proposition 5.8 of [4] show that is a -martingale and satisfies

where is a -martingale defined by

Hence, is the -compensator of . In other words, the hazard process coincides up to with the so called -martingale hazard process of . Under the assumption of a homogeneous insurance portfolio, if we define the -martingale as

then

| (3.3) |

i.e. the -compensator of the death counting process is given by .

3.1 Market model

We assume that our reference market is frictionless and there are liquidly traded primary assets with price processes , , following real-valued continuous -semimartingales. The asset vector is denoted by . For now we do not specify the nature and the dynamics of these primary assets.

Remark 3.1.

We remark that primary assets are here assumed to be -adapted. Unlike in the credit risk context where products associated to a single default (e.g. bankruptcy of an important finance institution) are traded on the financial market over time, this is not the case of life insurance products based on the decease of single persons. However, primary assets can include some mortality/longevity index-linked securities, like longevity bond.

Definition 3.2.

A trading strategy is a -valued -predictable -integrable process .

The space of all -valued -predictable -integrable processes is indicated by .

Definition 3.3.

A portfolio or value process associated to a trading strategy is defined by the following càdlàg optional process666We follow the definition given in [7].

It is called self-financing if

We note that according to our definition, for and , the variable represents the amount of -th primary asset held at time . We define the following set

Definition 3.4.

A benchmark or numéraire portfolio is a portfolio in the set , such that every portfolio when discounted by forms a -supermartingale, i.e.

In our framework, we assume only the existence of a numéraire portfolio denoted by and not necessarily the existence of an equivalent martingale measure. We note that according to our definition of benchmark (or numéraire) portfolio, we exclude that the benchmark may contain claims related to single deceases.

Definition 3.5.

We call benchmarked value the value of any security or portfolio when discounted by the benchmark portfolio and we denote it by process , i.e.

Since in our framework all primary assets are assumed to be continuous, the following result holds.

Proposition 3.6.

The benchmarked vector process of primary assets is a -local martingale.

Proof.

See e.g. [6]. ∎

The cash flow received by the policyholder from the insurer over time can be seen as a dividend payment which is usually modelled by a process of finite variation or more in general a -semimartingale. We denote by the benchmarked value of the cumulative liabilities of the insurer towards a policyholder, formally

| (3.4) |

We assume that is defined such that is square integrable777A process is square integrable if ..

Definition 3.7.

The following formula for a dividend process, which settles at time , is called real world pricing formula,

| (3.5) |

for .

This definition is a generalization of the so called ex-dividend price process (see e.g. [3] and [30]) which gives the current value of all future cash flow the insurer has to pay in the risk-neutral valuation context, i.e. when a martingale measure is assumed to exist. In the general case, if the existence of a martingale measure is not assumed, the benchmarked value of the price process corresponds to the benchmarked risk-minimizing price as we explain in Appendix A.

It is well known that the hybrid market extended with the introduction of insurance contracts is intrinsically incomplete even when the reference market is complete. This fact is due to the additional source of randomness given by mortality risk and the lack of liquidity in trading life insurance products based on single decease over time, which create an unhedgeable basis risk (see e.g. [8]). Hence in our setting we need to choose a hedging method for incomplete markets. The so called risk-minimizing method, which aims to find the optimal replicating strategy and minimizing the expected quadratic risk, appears to be a natural approach when market incompleteness is due to external source of randomness as discussed in [5]. It was originally introduced in [26] for a single payoff and then extended to dividend processes and applied to insurance contracts in e.g. [38], [37], [14], [4], [9] and [8]. However, the results in these papers require a risk-neutral contest. The relationship of benchmark approach and risk-minimization has been analysed in [42] and [6] for a single payoff. In Appendix A we show how this method can be easily reviewed to include dividend payments.

We now consider a state variable process representing the underlying risk factors, possibly including macro-economic variables, environmental and social indicators. Let be such that . Furthermore, we assume is given by a polynomial diffusion of the form

with

| (3.6) |

for , realized on the filtered probability space , where is a -dimensional -Brownian motion, is a continuous function, ,

for all and . The (compact) state space is given by

where is the state space of process and the state space of , respectively.

The following proposition shows that if is a compact set of , then is compact as well.

Proposition 3.8.

If there is a constant such that for every ,

then is uniformly bounded.

Proof.

Since is a linear function of , the -dynamics can be written as

with , , . In particular, we have

where and are respectively some matrix norms of and .

The Grönwall’s inequality yields

for all , with a suitable constant, i.e. is uniformly bounded. ∎

For the sake of simplicity, in the rest of this paper the degree of a generic polynomial function will be indicated by .

We model the benchmark portfolio as driven by the state variable in the following way

| (3.7) |

for every . We note that according to our definition (3.7), the benchmark portfolio is -adapted and continuous. In [23] a similar dynamics is specified for a state price density, here we choose to model the benchmark portfolio.

Now we assume that both risk-free OIS bond and longevity bond maturing at are among primary assets and we indicate their value processes respectively by and . In view of Proposition 3.6, we assume that their benchmarked value processes are continuous -true martingales. We stress that for compact state space , the restricted polynomial admits a strictly positive minimum value, i.e. there exists a strictly positive number such that

| (3.8) |

As we will see below, under our model assumptions the condition (3.8) ensures the continuity of both risk-free OIS bond and longevity bond, as well as the non-negativity of the risk-free short rate by adjusting the parameter .

A risk-free OIS bond maturing in is by definition a zero-coupon bond with unit payment at term of contract , whose value at is represented by

which can be explicitly calculated using (3.7) and Proposition 2.2,

where second equality follows by Lemma 6.1.1 of [10]. Due to (3.8), the process above is well-defined and continuous. Hence we have

| (3.9) |

We note that in our model the value of a OIS -bond in time is a ratio of polynomial functions of , with explicit deterministic time-dependent coefficients.

The risk-free short rate process can be explicitly calculated from the risk-free OIS bond dynamics (3.9), for

since when . In particular, the compactness of the state space and (3.8) provide that

has an upper bound and a lower bound uniformly in . By choosing , the short rate takes positive value in .

Following the definition in [12] and [11], a longevity bond maturing at is a index-linked zero-coupon bond with final payment at equal to the value of a given survival index at . Unlike the usual intensity-based approach, we model first the survival index and then derive the mortality intensity dynamics. We use the -component of the state variable to model the survival index

| (3.10) |

for every . The parameter will be used to adjust the value level of mortality intensity. The same argument as before leads to the existence of a strictly positive number such that

| (3.11) |

The formula for the mortality intensity can be obtained immediately

| (3.12) |

for all . Analogously to the case of risk-free short rate , thanks to the compactness of and the condition (3.11), we have that uniformly in the quantity

has an upper bound and a lower bound . If we set , the mortality intensity has then a positive value range .

Similar to the OIS bond case, under our assumption and by using definition (3.10) of survival index and Proposition 2.2, we can calculate explicitly the value of a -longevity bond at ,

| (3.13) | ||||

where in the second equality we use Lemma 6.1.1 of [10]. Condition (3.8) guarantees the continuity of the process above. Similar to the case of risk-free OIS bond , the value of longevity bond at time is also a polynomial rational function of the state variable with deterministic time-dependent coefficients.

4 Pricing and hedging life insurance liabilities

It is well known that most of life insurance liabilities can be modelled as a combination of the following three building blocks, which are particular cases of dividends:

-

•

Pure endowment contract: the insurer pays only if the policyholder survives until the maturity of the contract.

-

•

Term insurance contract: the payment is given only when the decease of the insured person occurs before or at .

-

•

Annuity contract: continuous cash flow is paid as long as the policyholder is alive or the contract is valid.

In the following sections, we compute the real world pricing formula and the benchmarked risk-minimizing strategy for the three building blocks, and show how the property in Proposition 2.2 gives explicit formulas in the case of polynomial payments, as well as a good approximation in the case of continuous payments. All theorems and notations are provided in Appendix A. For the sake of simplicity, we assume to invest only in the OIS bond and the longevity bond, i.e.

and calculate the explicit benchmarked risk-minimizing strategy only for pure endowment contract assuming that . The case of the other two building blocks is similar.

The following lemma will be used frequently.

Lemma 4.1.

Let be a polynomial in with coordinate representation

for , then for ,

Proof.

The first equality is given by the Itô’s formula and the second one is due to Proposition 2.2. ∎

4.1 Pure endowment

A pure endowment contract provides a payment at the term of contract if the insured person is still alive. For , its payoff at associated to -th policyholder is given by

where the value is assumed to be a -measurable and square integrable random variable. For a homogeneous portfolio of policyholders with the same payoff we have

The benchmarked cumulative payment is given by

for .

Let denote the price process given by the real world pricing formula (3.5) associated to a homogeneous portfolio of pure endowments. Under our model assumptions of Section 3, we have at time ,

where in the third equality we use Proposition 5.5 of [4] combined with Corollary 5.1.1 of [10]. Then the benchmarked value process associated to the benchmarked risk-minimizing strategy of the given portfolio is

for . Proposition 5.11 of [4] can be easily adapted to our case and together with (3.7) it shows that the benchmarked risk-minimizing strategy is given by with

| (4.1) |

for , where the vector process is obtained by the Galtchouk-Kunita-Watanabe decomposition of

| (4.2) |

where and is strongly orthogonal to .

The benchmarked cumulative cost process is

for , where is given by (3.3).

Now we consider the simplest case when the payoff is given by a polynomial function of the state variable, i.e.

In this case the pricing formula is reduced to

| (4.3) |

We note that this includes the realistic cases for an insurance contract with constant payoff , , or the one with an index-linked payoff, e.g. proportional to the survival index at time , that is , . In this case, we have

| (4.4) |

Lemma 4.1 applied to (4.4), (3.9) and (3.13) leads to the following decompositions

where . We define the 2-dimensional square matrix process

| (4.5) |

and the 2-dimensional vector process

satisfying

for all . Providing that the matrix is a.s. invertible for all , we have

for all . Then

hence for , the benchmarked risk-minimizing strategy is given by

and the benchmarked cumulative cost process is given by

If now we assume that the payoff is a generic continuous function of the state variable, i.e.

then it is not always possible to find an explicit form of the conditional expectation as in the polynomial case. This class includes a large family of longevity linked products, e.g. options on survival index or longevity bond. However, providing that the state space is compact, we can always find a uniform polynomial approximation of on E, i.e.

| (4.6) |

where the norm is defined by

for any . Proposition 4.3 shows that the sequence of pricing formulas related to provides a good approximation of the one related to .

Lemma 4.2.

Proof.

We first prove the a.s. approximation,

Similarly we have the approximation uniformly in for any ,

∎

We set where

| (4.7) |

for .

Proposition 4.3.

Proof.

Straightforward from Lemma 4.2. ∎

Now we prove that both the benchmarked risk-minimizing strategies and benchmarked cumulative cost processes associated to provide a good approximation of the ones associated to as well.

Lemma 4.4.

Let be a uniform polynomial approximation of the continuous function on as in (4.6) and for every we consider

| (4.8) |

with the following Galtchouk-Kunita-Watanabe decomposition

Let and be the two processes given by the Galtchouk-Kunita-Watanabe decomposition of in (4.2) with respect to , then

| (4.9) |

and

| (4.10) |

If the matrix process defined in (4.5) is such that, for all , is a.s. invertible with , then

| (4.11) |

and for all .

Proof.

Proposition 4.3 gives in particular the following convergence in ,

Since and are strongly orthogonal to the space , we have

which implies that

| (4.12) |

and

Moreover, for every , the Itô isometry yields

If the matrix is invertible for all a.s. with

then Cauchy–Schwarz inequality leads to

In particular we have for all by Lemma 4.1. Then (4.12) yields . ∎

Remark 4.5.

We note that if is given by a continuous function, via a convergence argument (similar to the one in Lemma 4.4) we obtain by Lemma 4.1 that the Galtchouk-Kunita-Watanabe decomposition of with projection on the subspace is given by

where is a predictable -integrable vector process, i.e. contains no orthogonal term even without the assumption .

Proposition 4.6.

Let be a uniform polynomial approximation of the continuous function on as in (4.6). If and are respectively the benchmarked risk-minimizing strategy and benchmarked cumulative cost process associated to , and are the ones associated to , then

| (4.13) |

| (4.14) |

If furthermore the matrix process given by (4.5) is a.s. invertible, then

| (4.15) |

Proof.

(4.13) and (4.15) are immediate consequence of (4.9) and (4.11) in Lemma 4.4. Now we prove the convergence in of the benchmarked cumulative cost process. We note

for every , where

Clearly

For the first addend, thanks to the compactness of the state space we have

for every , where is a suitable constant. This quantity turns to zero uniformly in thanks to (4.10) in Lemma 4.4.

For the second addend, since provides a pathwise approximation of uniformly in , the dominated convergence theorem together with the boundedness of the integrand process yields

that concludes the proof. ∎

4.2 Term insurance

A term insurance contract gives a positive payoff in the case of a policyholder’s decease before the term of contract. The payment process is assumed to be -predictable and square integrable. The amount paid at to the -th policyholder is given by

for . In the case of a homogeneous portfolio of policies, we have

The associated benchmarked payment process is

for .

We denote by the price process associated to a homogeneous portfolio of term insurance contracts. The real world pricing formula (3.5) together with (3.7) and (3.12) yields

where in the third equality we use Proposition 5.5 of [4] combined with Corollary 5.1.3 of [10]. We note that Corollary 5.1.3 of [10] requires that is a bounded process, but this hypothesis can be easily relaxed by using a localization argument together with the dominated convergence theorem for conditional expectation if is sufficiently integrable.

Now we assume

for , with a continuous function on the compact state space . Then the stochastic Fubini-Tonelli Theorem yields

for . As before, this expression can be approximated by explicated pricing formulas related to polynomial payoff.

Proposition 4.7.

Let be a sequence of polynomials functions which approximates uniformly the continuous function on . For every , we consider with

for every , where the polynomial functions and are given respectively by and . Then provide both a pathwise and approximation of uniformly in .

Proof.

Analogous to Proposition 4.3. ∎

4.3 Annuity

An annuity is a continuous cash stream paid by the insurer as long as the policyholder is alive. We denote its cumulated payoff value up to time by . The process is assumed to be a right continuous increasing -adapted and square integrable process, with and . The total payoff at associated to the -th policyholder is given by

| (4.16) |

the total payoff at of a homogeneous portfolio of annuity contracts is

The benchmarked cumulated payment process at time with is

Let denote the price process given by the real world pricing formula (3.5) for a homogeneous portfolio of annuity contracts. By (3.7) and (3.12) we have at

where in the third equality we use Proposition 5.5 of [4] and Proposition 5.1.2 of [10]. Proposition 5.1.2 of [10] requires that the process is bounded. As in Section 4.2, this condition can be relaxed using a localization argument combined with the theorem of dominated convergence for conditional expectation.

Remark 4.8.

We stress that under our assumption, if is furthermore a continuous process, then it is also an -predictable process. Therefore, according to (4.16) we have

That is, a homogeneous annuity portfolio can be considered as the sum of a homogeneous pure endowment portfolio and a homogeneous term insurance portfolio as defined in Section 4.1 and 4.2 respectively, where and . In particular, the linearity of the pricing formula yields

If now we assume

for , with a continuous function on the compact state space , then we have the following proposition.

Proposition 4.9.

5 A numerical example

We now consider a numerical example with calibration to real data. Set , throughout this section we assume that and . In particular is also bounded, see Proposition 3.8.

For a more detailed study of polynomial diffusions on unit ball we refer to [32]. In view of Theorem 2.1 of [32] we consider the following model dynamics,

where is a 1-dimensional Brownian motion,

with , and the parameters satisfy the following condition

equivalent to or

| (5.1) |

In particular the dynamics of component is given by

Furthermore we assume that the polynomials and are both linear and positive on , i.e.

| (5.2) |

| (5.3) |

where . A similar specification for can be found in [24].

Under these assumptions we have

with dynamics

where ,

where ,

For the sake of simplicity, we calibrate our model to the inverse of benchmark portfolio and the longevity index. The benchmark portfolio can be identified with a sufficiently diversified portfolio such as Morgan Stanley capital weighted world stock accumulation index, called MSCI world index (see discussion in [41] and [42]). For the second one we take data from LLMA index related to German population. The sample period ranges from January 1970 to January 2013 with 517 monthly observations of MSCI world index and 44 annual observations of Germany male graduated initial rate of mortality published by LLMA relating to the cohort of male population aged 20 in 1970.

The following table reports the summary statistics of the two data sets. The inverse of benchmark portfolio data is reported in basis points and longevity index data in percentages.

| Mean | Median | Std. | min | MAX | |

|---|---|---|---|---|---|

| () | 38.612 | 19.468 | 35.397 | 5.9441 | 134.31 |

| Longevity index () | 98.628 | 98.984 | 1.1337 | 95.606 | 99.803 |

We denote the model parameter vector by and the times of observation by , where . For every with we have a 1- or 2-dimensional observation vector . When both MSCI index and LLMA index are observable the measurement equation is given below. When only the MSCI index is observable, is reduced to the only first component. We have

where

and the measurement error vector is assumed888The same assumption can be found in [36] and in [24]. In a more general case is a random error vector with . to be

where indicate the measurement error variance associated to the inverse of benchmark portfolio and the one associated to the longevity index.

In view of [32] and under the assumption that the longevity index does not have relevant influence on the benchmark portfolio, the transition equation in discrete time of the first component of (unobserved) state variable for with can be approximated999See e.g. [21]. by,

where is a 1-dimensional error term of zero mean and unit variance, independent from . We note that and are (both conditionally and unconditionally) independent. Such approximation gives exact conditional and unconditional expectation and variance matrix of . Furthermore, it follows from the property given in Proposition 2.2 that the conditional expectation is an affine function of and the conditional variance is a second degree polynomial function of . To be more precise,

where

Following [36] we make the further assumption of approximating with a normal distribution error term independent from ,

| (5.4) |

The second component of state variable for any time has an explicit solution depending on ,

For equal to an observation time of the longevity index, it can be approximated by

where are the monthly values calculated by the transition equation (5.4) of .

Since both the inverse of the benchmark portfolio and the longevity index are affine functions of the state variable, if we ignore for now the state space restrictions101010See [36] for a more detailed discussion regarding this assumption., then we are in the case of a linear Gaussian state space model. Linear Kalman filter and maximum likelihood estimation are thus applicable under these approximations. We refer to [27] for a detailed description of the method. For the sake of simplicity, we apply linear Kalman filter and maximum likelihood estimation only to estimate parameters of the component. Since the longevity index can be considered as a linear regression of under our approximation, least squares estimation will be applied to estimate the remaining parameters of the component.

Let denote the information available at time regarding the benchmark portfolio, i.e.

For we denote

where is the optimal predictor of and is its mean square error. Analogously for we denote

For , the prediction step of linear Kalman filter is given by

with mean square error

and the update step is given by

where

The (approximated) log-likelihood function is given by

For with 111111We note that longevity index is only annually observable, thus can be updated only annually. the approximated value of is

| (5.5) |

We set such that conditions (5.2) and (5.3) are satisfied. In particular the assumption of forces the value of and to be (almost) equal to the first value of the inverse of benchmark portfolio and longevity index respectively.121212While our condition limits the choice of and , the values of and can be arbitrarily chosen, as soon as (5.2) and (5.3) are fulfilled. A different choice of and will result in a scaling of the state variable . See also Theorem 5 of [24].

The following table reports the calibrated parameters.

| 14.98581 | -0.79506 | 1.25299 | 5.18417 | -5.87517 | -5.05117 |

The correspondent values of , which adjust the short rate and mortality intensity level, and the log-likelihood value are reported below.

| L | ||

|---|---|---|

| 4.6068 | 0.0045607 | 2347.5 |

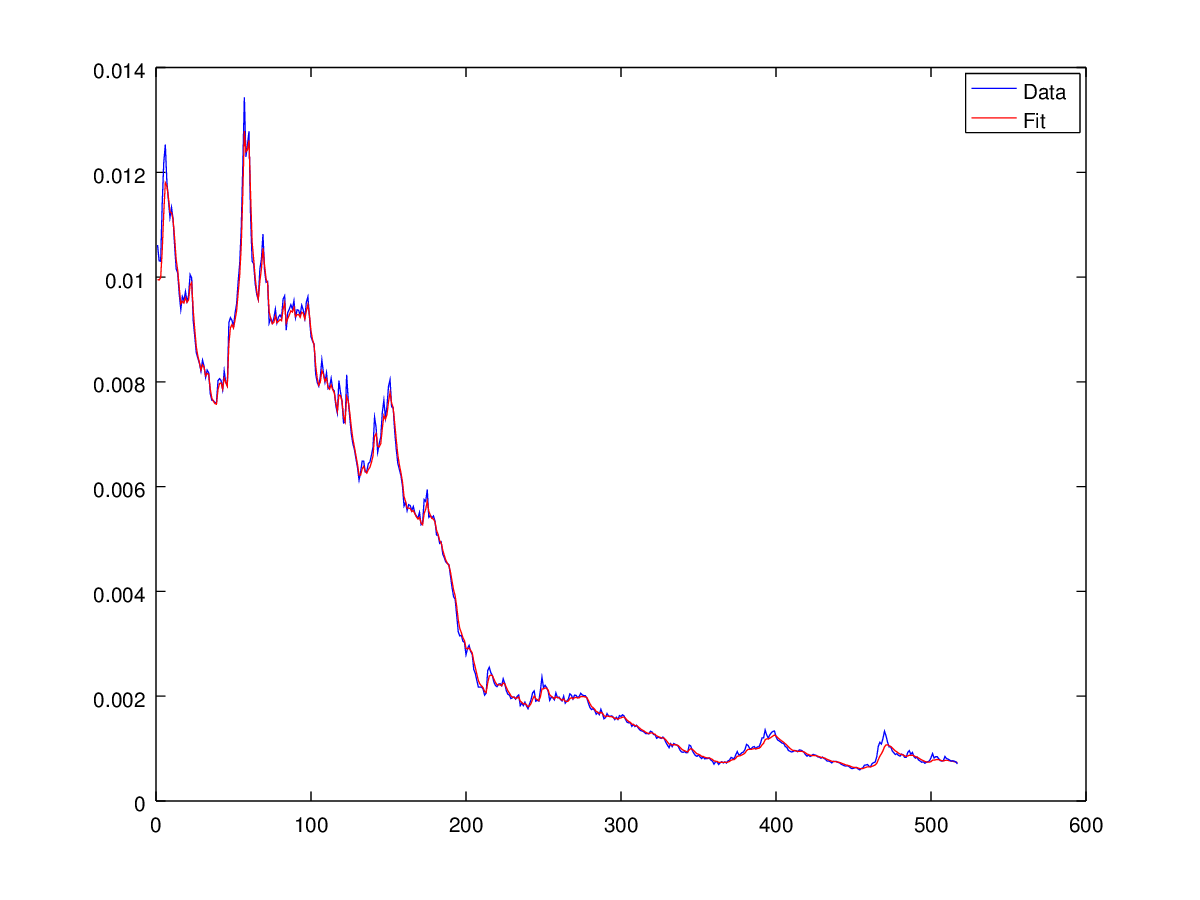

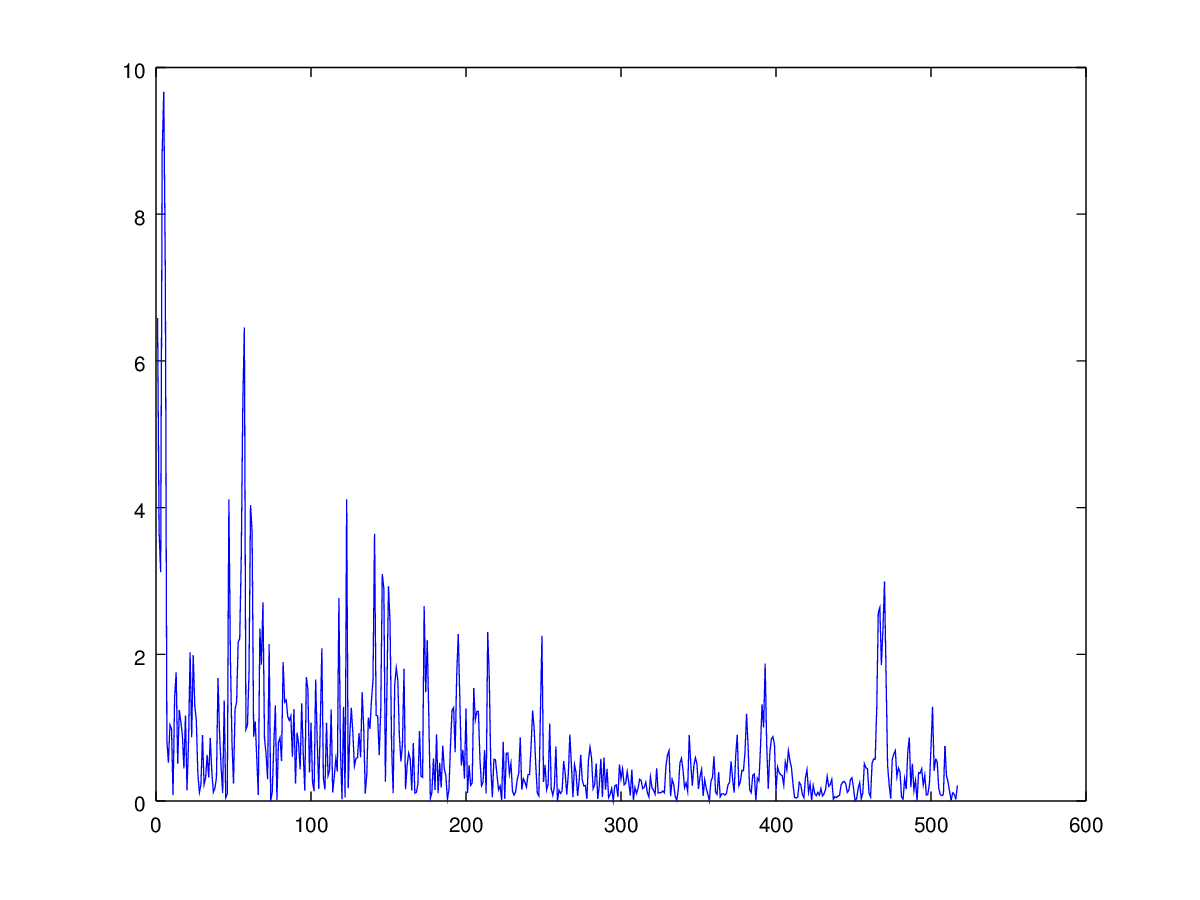

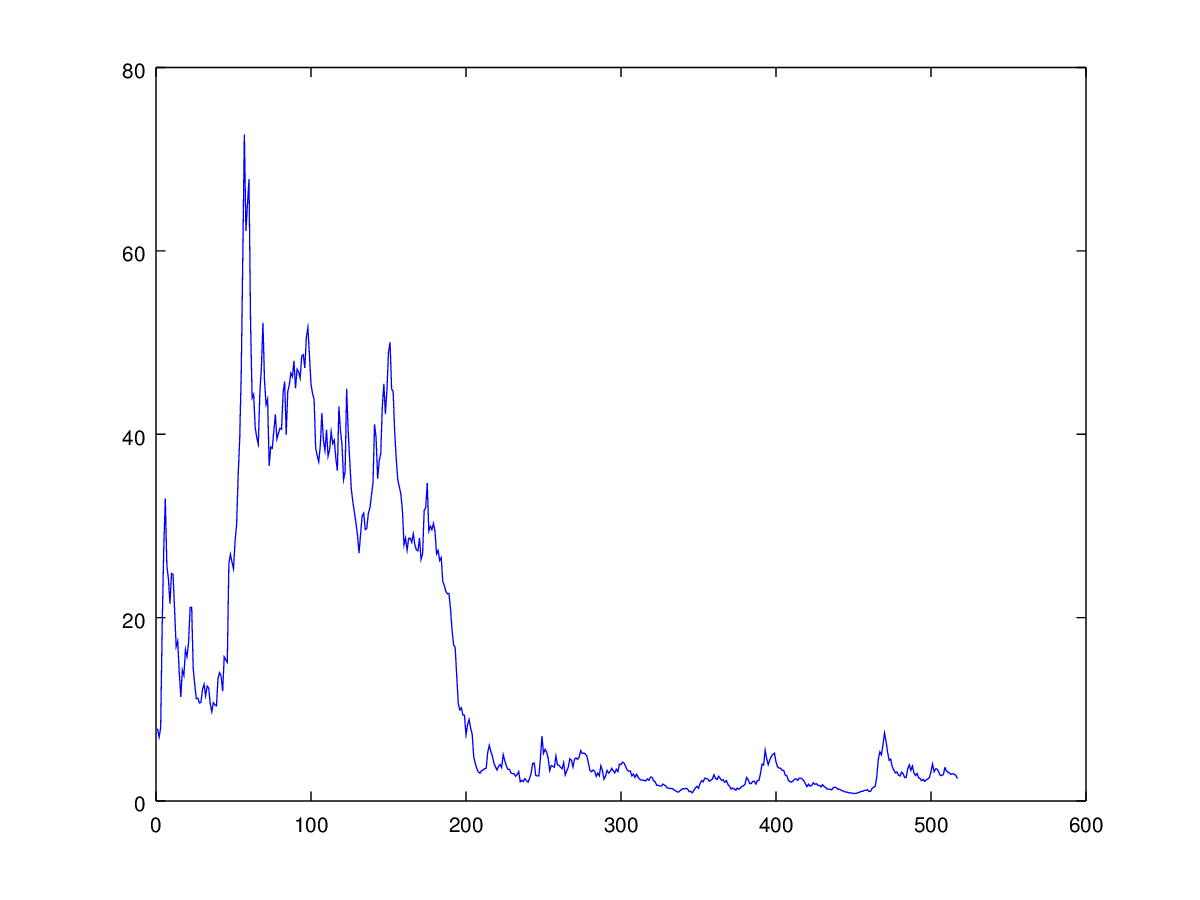

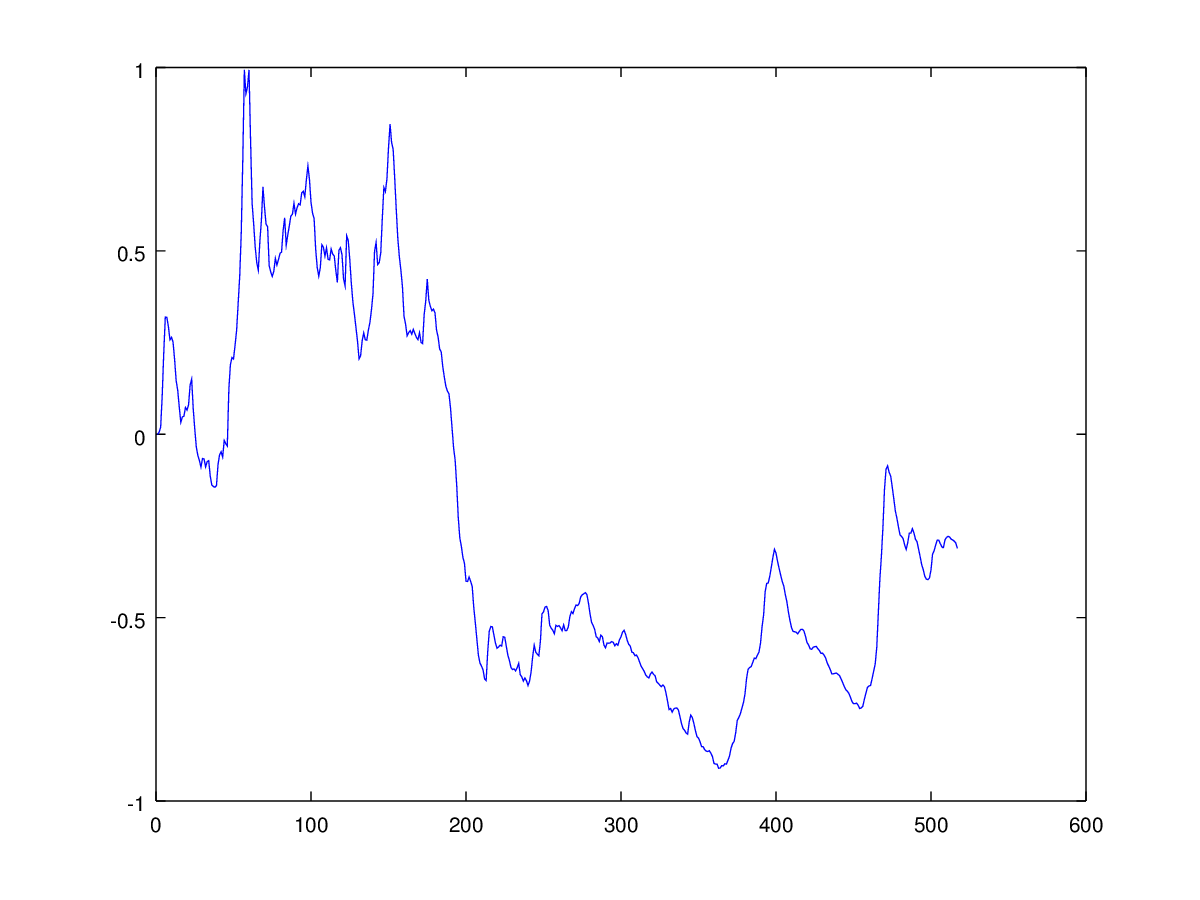

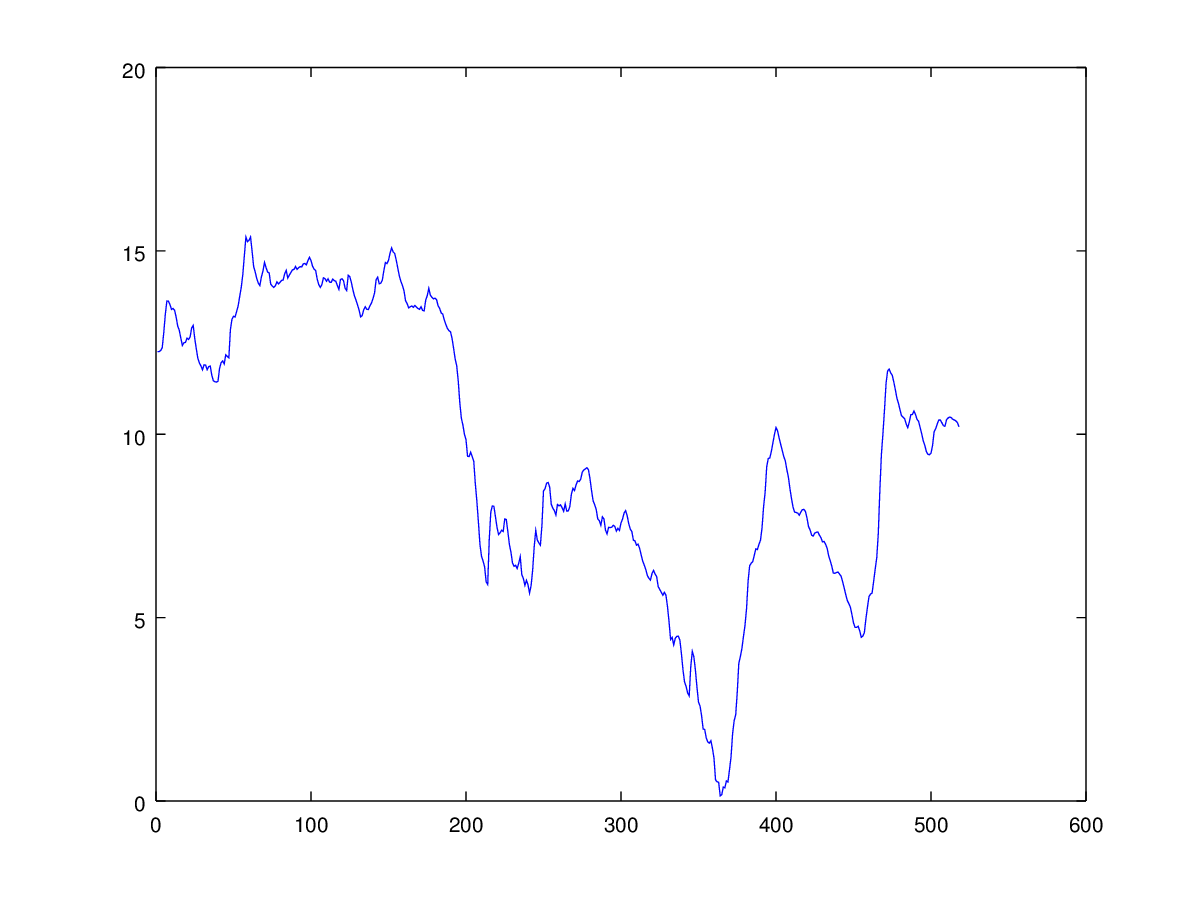

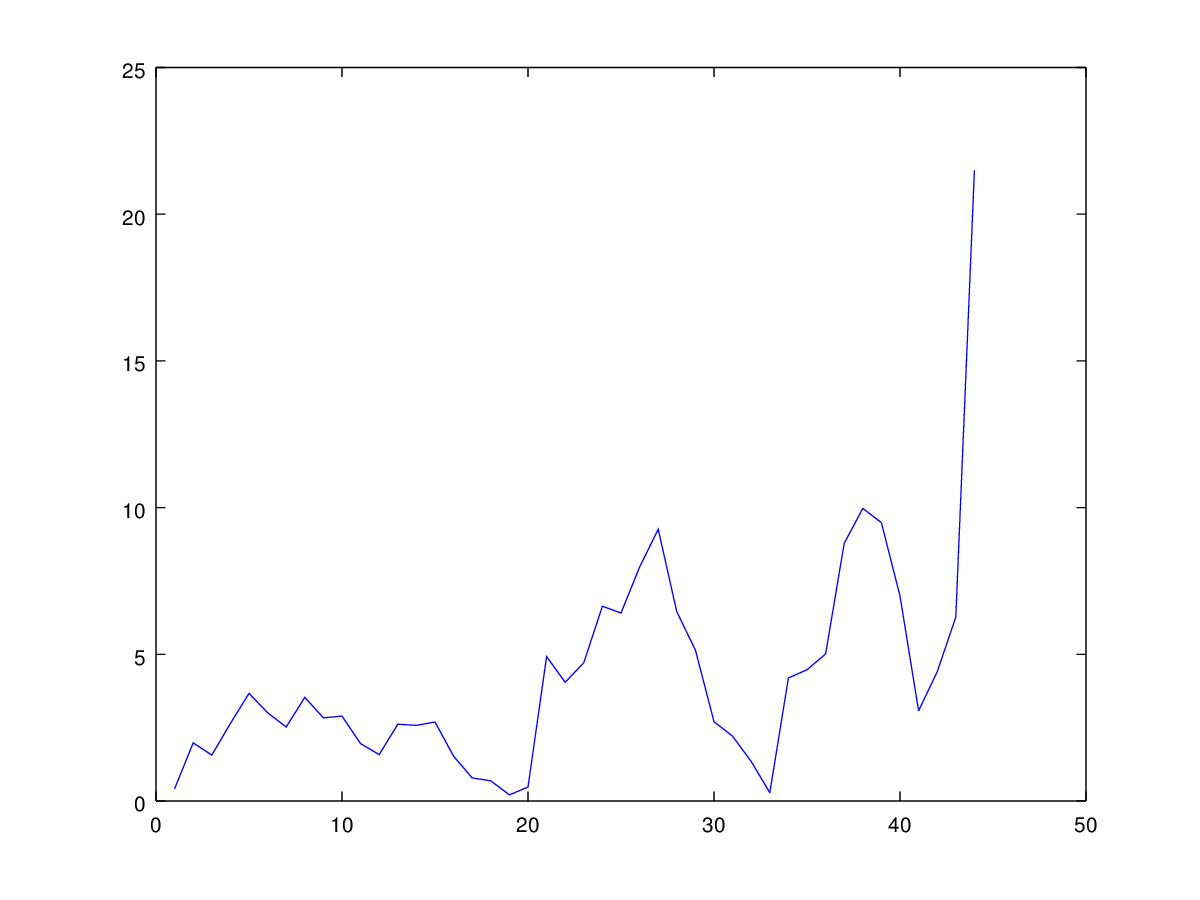

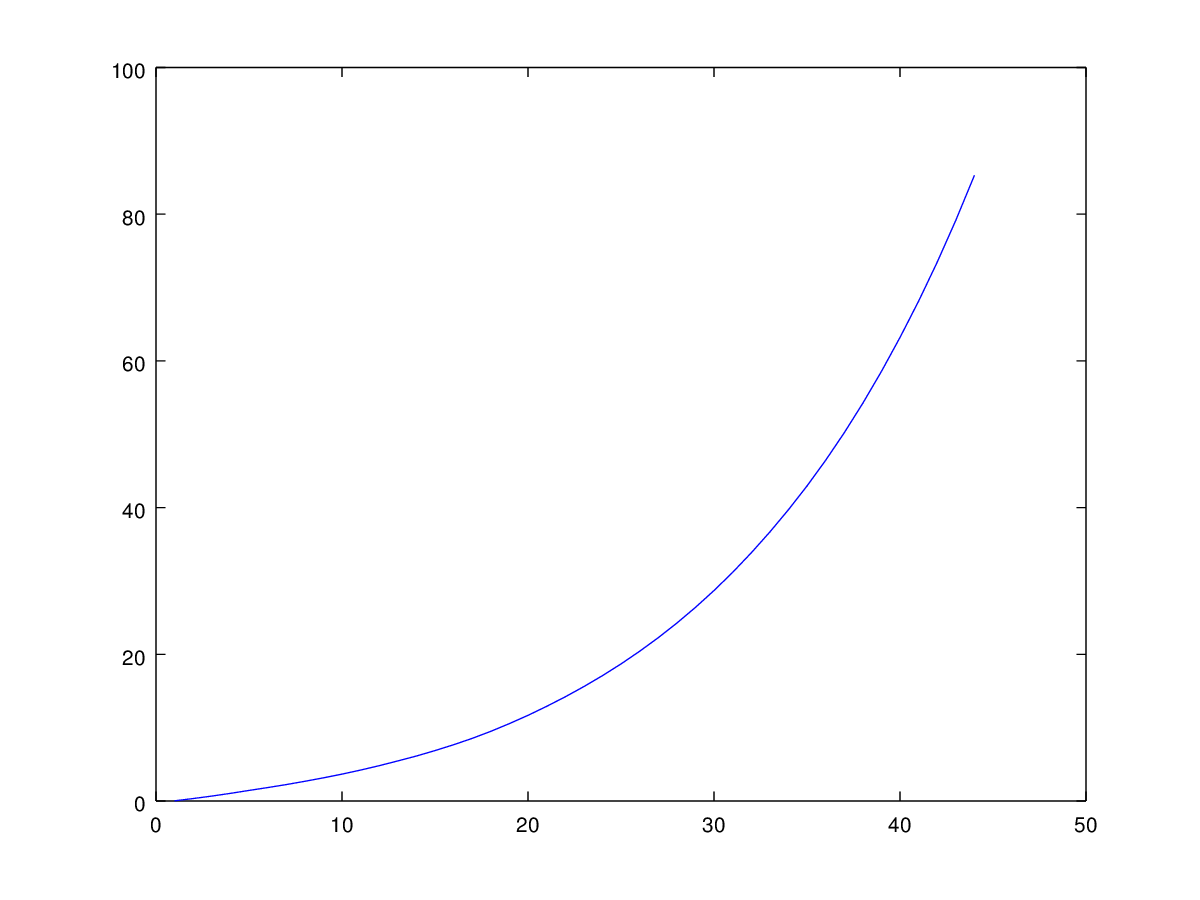

Figure 1 1(a) plots the observed inverse of benchmark portfolio data and the fit produced by Kalman filter. Figure 1 1(b) and 1(c), with unit in basis point, shows respectively the pricing error generated by Kalman filter and the root mean square pricing error (RMSE) computed over 100 Monte Carlo replications. Figure 1 1(d) displays time series of estimated state variable component underlying the benchmark portfolio dynamics and taking value in the compact interval . Figure 1 1(e) displays time series of estimated short rate adjusted by the level parameter and thus taking only positive values. The simulated samples consist of 517 monthly time series observations from January 1970 to January 2013.

We note that one dimensional component , with a mean RMSE equal to 15.24 bps, is already good enough to explain the inverse of benchmark portfolio dynamics structure and to produce a reasonable fit to the observed data. In particular the fit behaves better in the tail, which is a desirable situation as we are fitting the inverse of LLMA world index value.

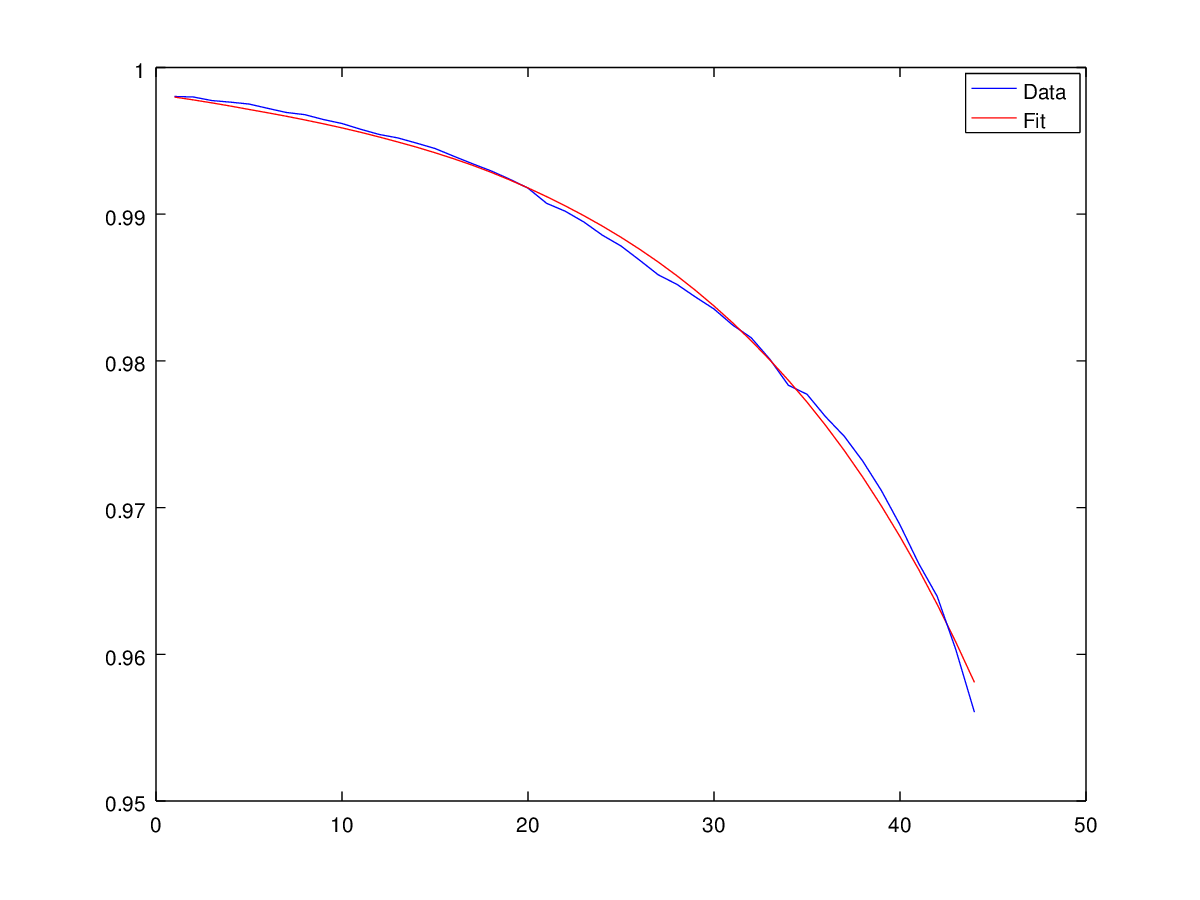

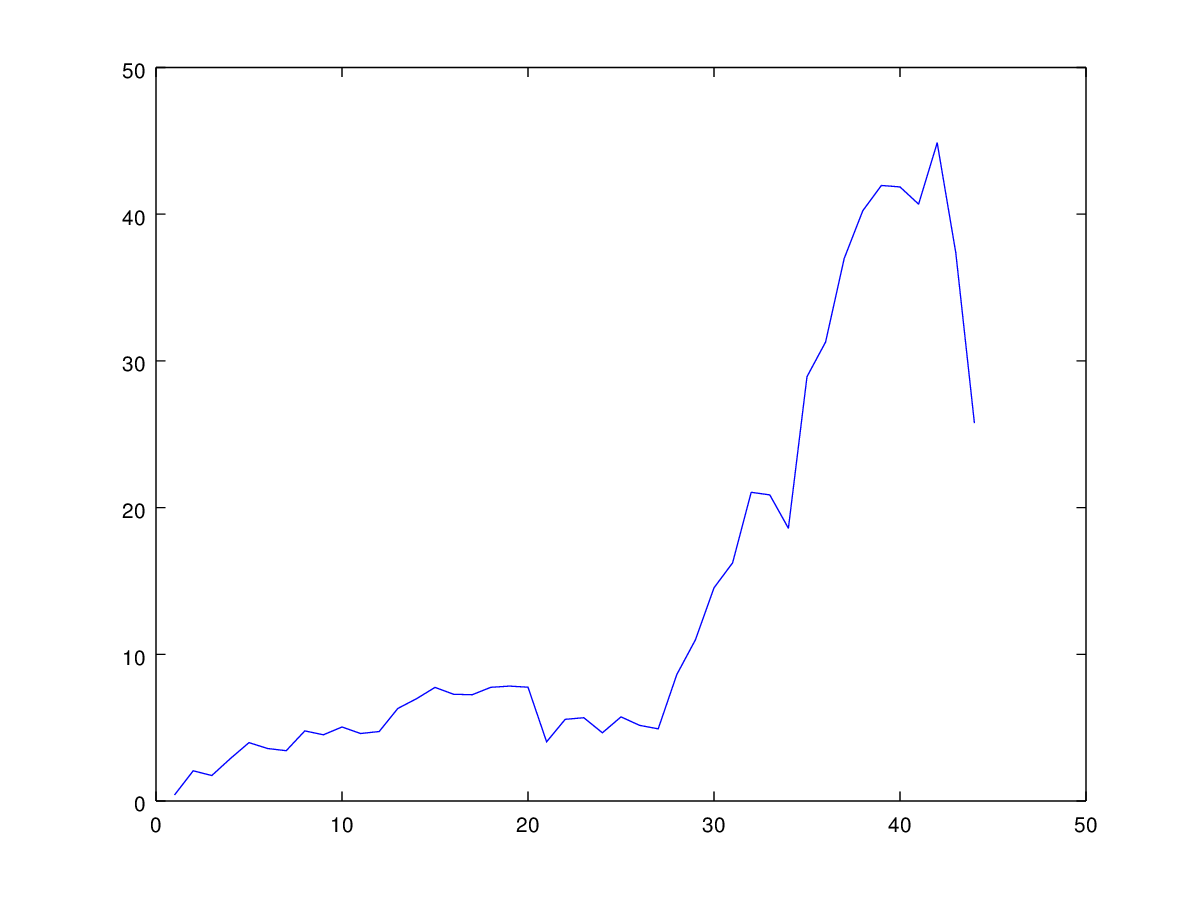

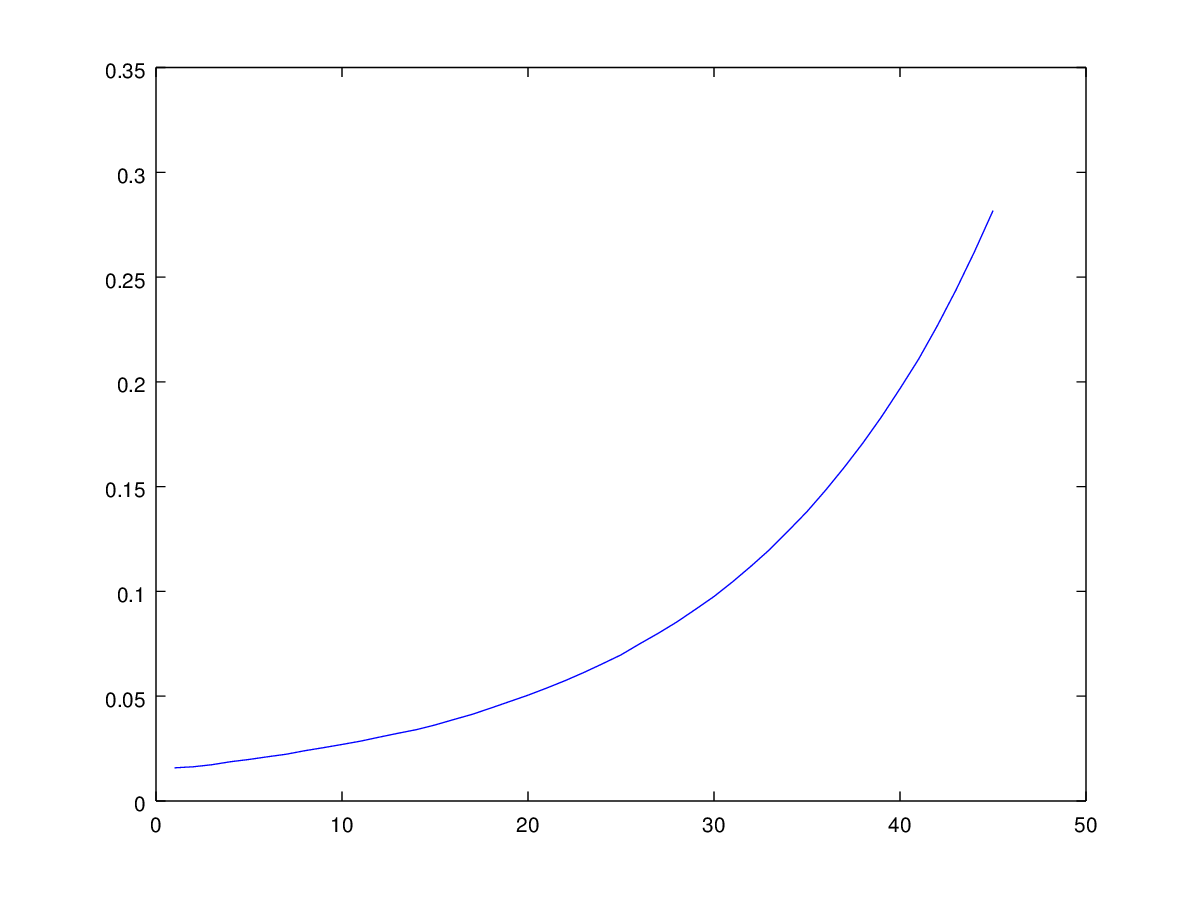

Similarly Figure 2 2(a) plots the observed longevity index data and the fit produced by (5.5) with estimated parameter sets. Figure 22(b) and 2(c), with unit in basis point, show respectively the pricing error associated to (5.5) and the root mean square pricing error (RMSE) computed over 100 Monte Carlo replications. Figure 22(d) displays time series of estimated state variable component . Figure 22(e) displays time series of estimated mortality intensity .

The simulated samples consist of 44 annual time series observations from January 1970 to January 2013.

The absence of the diffusion term in the dynamics produces rather smooth paths for and consequently for the longevity index fit. This is reasonable as longevity index data has very light oscillations along the trend, with a mean RMSE value of 15.39 bps. However, the poor data set of the longevity index, with always less than 50 annual observations for one age cohort, and the long time frame between two consecutive data can be a drawback for calibration.

6 Conclusion

We consider a polynomial diffusion state variable on compact state space to model the hybrid financial-insurance market. We include a dependence structure between OIS short rate and mortality intensity and are able to guarantee their positivity when needed. The model is parsimonious and analytically tractable. By following the benchmark approach we compute optimal premium as well as risk-minimizing strategy for life insurance liabilities. We complete our theoretical analysis by a calibration of a particular model specification to real data. As showed in Section 5, we obtain a good fitting to the MSCI and LLMA index also in the parsimonious case of a two-dimensional state variable under linear polynomial specification.

Appendix A Benchmarked risk-minimization for payment streams

We give here the general definitions and results of the benchmarked risk-minimizing method for payment streams by following mainly [6] and [4] for the presentation.

We introduce first the following Hilbert spaces

with norms given respectively by

for and . Lemma 3.4 of [4] (or Lemma 2.1 of [45]) shows that is a stable subspace of . In particular, for every we have

Definition A.1.

An -admissible strategy is a process such that

-

(1)

,

-

(2)

the associated benchmarked value process with

is in .

Now we fix a process as defined in (3.4) which models the benchmarked cumulative payments towards a policyholder.

Definition A.2.

The benchmarked cumulative cost process of a -admissible strategy associated to is defined by

Definition A.3.

The risk process of an -admissible strategy is defined by

Definition A.4.

An -admissible strategy is called benchmarked risk-minimizing for if

-

(1)

-a.s.,

-

(2)

-a.s. for every and for any -admissible strategy such that -a.s., -a.s. for all .

Lemma A.5.

The benchmarked cumulative cost process of any benchmarked risk-minimizing strategy is a -martingale.

Lemma A.6.

The benchmarked value process associated to a benchmarked risk-minimizing strategy for is given by

The following theorem gives the solution of the benchmarked risk-minimizing problem.

Theorem A.7.

Let

| (A.1) |

be the Galtchouk-Kunita-Watanabe decomposition141414See [1] for an overview of Galtchouk-Kunita-Watanabe decomposition. of , where is the projection of on the space with and is -strongly orthogonal to . The unique benchmarked risk-minimizing strategy for is given by . The associated benchmarked cumulative cost process is

and the benchmarked value process is

As the classic risk-minimizing strategy, the crucial point of the solution of the benchmarked risk-minimizing strategy is finding the Galtchouk-Kunita-Watanabe decomposition (A.1).

We stress that, the orthogonal projection provided by the decomposition (A.1) shows that every benchmarked cumulative payment has a perfectly hedgeable part and a totally unhedgeable part covered by the benchmarked cumulative cost process . Furthermore, according to Lemma A.6, the benchmarked value process associated to the unique benchmarked risk-minimizing strategy for a given benchmarked cumulative payment process coincides with the benchmarked value of the real world pricing formula given in (3.5), i.e.

The benchmarked hedging problem and its relation with the real world pricing formula have already been studied in [5] and [6] in the case of a -claims , i.e. when the dividend process is given by

with a square integrable -measurable random variable. The real world pricing formula is reduced to

which is the original definition of fair price given in e.g. [42] for a -claim . In this case, if the -claim admits a self-financing strategy, then thanks to the supermartingale property of the benchmark portfolio in Definition (3.4), corresponds to the least expensive self-financing portfolio which replicates .

References

- [1] J. P. Ansel and C. Stricker. Décomposition de Kunita-Watanabe. Séminaire de Probabilités de Strasbourg, 27:30–32, 1993.

- [2] A. Antonov and M. Spector. Analytical approximations for short rate models, 2010. Available at SSRN: http://ssrn.com/abstract=1692624 or http://dx.doi.org/10.2139/ssrn.1692624.

- [3] K. Back, T.R. Bielecki, C. Hipp, S. Peng, and W. Schachermayer. Stochastic Methods in Finance. Lectures given at the C.I.M.E.-E.M.S. summer school held in Bressanone/Brixen, Italy, July 6-12, 2003. Springer, 2004.

- [4] J. Barbarin. Risk-minimizing strategies for life insurance contracts with surrender option, 2007. Available at SSRN: http://ssrn.com/abstract=1334580 or http://dx.doi.org/10.2139/ssrn.1334580.

- [5] F. Biagini. Evaluating hybrid products: the interplay between financial and insurance markets. In R. Dalang, M. Dozzi, and F. Russo, editors, Stochastic Analysis, Random Fields and Applications VII, Progress in Probability 67. Birkhäuser Verlag, 2013.

- [6] F. Biagini, A. Cretarola, and E. Platen. Local risk-minimization under the benchmark approach. Mathematics and Financial Economics, 8(2):109–134, 2014.

- [7] F. Biagini and M. Pratelli. Local risk minimization and numéraire. Journal of Applied Probability, 36(4):1126–1139, 1999.

- [8] F. Biagini, T. Rheinländer, and I. Schreiber. Risk-minimization for life insurance liabilities with basis risk. Mathematics and Financial Economics, 10(2):151–178, 2016.

- [9] F. Biagini and I. Schreiber. Risk-minimization for life insurance liabilities. SIAM Journal on Financial Mathematics, 4:243–264, 2013.

- [10] T. R. Bielecki and M. Rutkowski. Credit Risk: Modelling, Valuation and Hedging. Springer-Finance, Springer, second edition, 2004.

- [11] D. Blake, A. J. G. Cairns, and K. Dowd. Living with mortality: Longevity bonds and other mortality-linked securities. British Actuarial Journal, 12:153––228, 2008.

- [12] A. J. G. Cairns, D. Blake, and K. Dowd. Pricing death: frameworks for valuation and securitization of mortality risk. ASTIN Bulletin, 36(1):79–120, 2006.

- [13] M. Dacorogna and M. Cadena. Exploring the dependence between mortality and market risks. SCOR Papers, 2015.

- [14] M. Dahl and T. Møller. Valuation and hedging of life insurance liabilities with systematic mortality risk. Insurance: Mathematics and Economics, 39(2):193––217, 2006.

- [15] G. Deelstra, M. Grasselli, and C. Van Weverberg. The role of the dependence between mortality and interest rates when pricing guaranteed annuity options, 2015. Available at SSRN: http://ssrn.com/abstract=2667939 or http://dx.doi.org/10.2139/ssrn.2667939.

- [16] F. Delbaen and W. Schachermayer. A general version of the fundamental theorem of asset pricing. Mathemathische Annalen, 300(1):463–520, 1994.

- [17] F. Delbaen and H. Shirakawa. An interest rate model with upper and lower bounds. Asia-Pacific Financial Markets, 9(3):191–209, 2002.

- [18] C. Dellacherie and P.A. Meyer. Probabilities and Potential B: Theory of Martingales. Amsterdam: North Holland, 1982.

- [19] L. Demetrius. Mortality plateaus and directionality theory. Proceedings of the Royal Society B: Biological Sciences, 268(1480):2029–37, 2001.

- [20] K. Du and E. Platen. Three-benchmarked risk minimization for jump diffusion markets. Quantitative Finance Research Centre, Research Paper No. 296, 2011. Available at SSRN: http://ssrn.com/abstract=2170169 or http://dx.doi.org/10.2139/ssrn.2170169.

- [21] J. C. Duan and J. G. Simonato. Estimating and testing exponential-affine term structure models by Kalman filter. Review of Quantitative Finance and Accounting, 13(2):111–135, 1999.

- [22] R. Durrett. Stochastic Calculus: A Practical Introduction. Probability and Stochastics Series. CRC Press, Boca Raton, FL, 1996.

- [23] D. Filipović and M. Larsson. Polynomial diffusions and applications in finance. Finance and Stochastics, 2016. Forthcoming.

- [24] D. Filipović, M. Larsson, and A. B. Trolle. Linear-rational term structure models. Journal of Finance, 2016. Forthcoming; Swiss Finance Institute Research Paper, 14-15.

- [25] B. Flesaker and L.P. Hughston. Positive interest. Risk, 9(1):46–49, 1996.

- [26] H. Föllmer and D. Sondermann. Hedging of non-redundant contingent claims. In W. Hildenbrand and A. Mas-Colell, editors, Contributions to Mathematical Economics, pages 205–223. North Holland, 1986.

- [27] A. C. Harvey. Forecasting, Structural Models and the Kalman Filter. Cambridge University Press, New York, 1989.

- [28] H. Hulley and M. Schweizer. -on minimal market models and minimal martingale measures. In C. Chiarella and A. Novikov, editors, Contemporary Quantitative Finance. Essays in Honour of Eckhard Platen, pages 35–51. Springer, 2010.

- [29] J. Jacod. Calcul Stochastique et Problèmes de Martingales. Springer-Verlag, 1979.

- [30] F. Jamshidian. Valuation of credit default swaps and swaptions. Finance and Stochastics, 8(3):343–371, 2004.

- [31] S. F. Jarner and E. M. Kryger. Modelling adult mortality in small populations: the Saint model. ASTIN Bulletin, 41(02):377–418, 2011.

- [32] M. Larsson and S. Pulido. Polynomial preserving diffusions on compact quadric sets, 2015. Available at http://arxiv.org/abs/1511.03554.

- [33] J. Li and A. Szimayer. The uncertain mortality intensity framework: pricing and hedging unit-linked life insurance contracts. Insurance: Mathematics and Economics, 49:471–486, 2011.

- [34] N. Lima and N. Privault. Analytic bond pricing for short rate dynamics evolving on matrix Lie groups. Quantitative Finance, 16(1), 2016.

- [35] X. Liu, R. Mamon, and H. Gao. A comonotonicity-based valuation method for guaranteed annuity options. J. Computational Applied Mathematics, 250:58–69, 2013.

- [36] J. Lund and F. Alle. Non-linear Kalman filtering techniques for term-structure models. Working paper, Aarhus School of Business, 1997.

- [37] T. Møller. Risk-minimizing hedging strategies for insurance payment processes. Finance and Stochastics, 5:419–446, 1998.

- [38] T. Møller. Risk-minimizing hedging strategies for unit-linked life insurance contracts. ASTIN Bulletin, 28(1):17–47, 1998.

- [39] E. Platen. A benchmark framework for risk management. In Stochastic Processes and Applications to Mathematical Finance, pages 305–335. World Scientific, 2004.

- [40] E. Platen. Diversified portfolios with jumps in a benchmark framework. Asia-Pacific Financial Markets, 11(1):1–22, 2004.

- [41] E. Platen. A benchmark approach to finance. Mathematical Finance, 16(1):131––151, 2006.

- [42] E. Platen and D. Heath. A Benchmark Approach to Quantitative Finance. Springer, Berlin, 2006.

- [43] L. C. G. Rogers and D. Williams. Diffusions, Markov Processes and Martingales. Cambridge University Press, 1994.

- [44] E. Schlogl and D. Sommer. On short rate processes and their implications for term structure movements, 1994. Available at SSRN: http://ssrn.com/abstract=5768.

- [45] M. Schweizer. A guided tour through quadratic hedging approaches. In Option Pricing, Interest Rates and Risk Management, pages 538–574. Cambridge University Press, Cambridge, UK, 2001.