On distributions with fixed marginals maximizing the joint or the prior default probability, estimation, and related results

Abstract

We study the problem of maximizing the probability that (i) an electric component or financial institution does not default before another component or institution and (ii) that and default jointly within the class of all random variables with given univariate continuous distribution functions and , respectively, and show that the maximization problems correspond to finding copulas maximizing the mass of the endograph and the graph of , respectively. After providing simple, copula-based proofs for the existence of copulas attaining the two maxima and we generalize the obtained results to the case of general (not necessarily monotonic) transformations and derive simple and easily calculable formulas for and involving the distribution function of (interpreted as random variable on ). The latter are then used to characterize all non-decreasing transformations for which and coincide. A strongly consistent estimator for the maximum probability that does not default before is derived and proven to be asymptotically normal under very mild regularity conditions. Several examples and graphics illustrate the main results and falsify some seemingly natural conjectures.

keywords:

Copula , Dependence , Estimator , Graph , Endograph , Markov KernelMSC:

[2010] 60E05 , 28A50 , 91G701 Introduction

Suppose that and are (continuous) distribution functions of two random variables and modeling, e.g., (i) the default times of financial institutions or (ii) the lifetime of electronic components. Especially in the context of (i) the marginal distributions might be know or at least be estimated in standard ways, whereas the joint distribution is often unknown and harder to estimate. In such situations (particularly in the context of so-called credit default swaps) is seems natural to consider the worst-case scenario and study bivariate distribution functions in the Fréchet class of (the family of all bivariate distribution functions having marginals and ) with the following property: In case has distribution function the joint or prior default probability (i.e. the probability of the events and , respectively) is maximal within .

Translating to the class of copulas (see [17] and Section 2), maximizing the afore-mentioned probabilities means calculating

| (1) |

where is defined by , denotes the quasi-inverse of , the graph of , the so-called endograph of , the family of all two-dimensional copulas and the doubly stochastic measure corresponding to the copula .

It has been brought to our attention that formulas for the suprema in eq. (1) also follow from deep and much heavier machinery going back to Rüschendorf in [22]. In the current paper we provide (a) independent alternative simple, copula-based proofs and show the existence of copulas attaining the suprema (including the fact that it is possible to choose completely dependent). Complementing these results, (b) we calculate and also for general measurable, not necessarily monotonic transformations , (c) characterize for which non-decreasing we even have and, (d) derive a strongly consistent estimator for and show that the latter is asymptotically normal under mild regularity conditions.

The rest of the paper is organized as follows: Section 2 gathers some preliminaries and notations, and proves the afore-mentioned translation of the problem of maximizing the joint or prior default probability to the copula setting. The main results concerning the calculation of the maximum probabilities and various related questions are gathered in Sections 3 and 4, whereas in Section 5 we characterize the case for non-decreasing . Finally, Section 6 introduces an estimator for , shows consistency and studies its asymptotic distribution. Several examples and graphics illustrate the obtained results and the chosen approach.

2 Notation and Preliminaries

For every -dimensional random vector on a probability space we will write if has distribution function (d.f., for short) and let denote the corresponding distribution on the Borel -field of . For every univariate distribution function we will let denote the quasi-inverse of , i.e. . Note that for every we have if and only if , that for and continuous we have , i.e., is uniformly distributed on , and that the random variable coincides with with probability one. For further properties of we refer, for instance, to [10]. Given univariate distribution functions and , we will let denote the Fréchet class of and , i.e. the family of all two-dimensional distribution functions having and as marginals; will denote the corresponding class of probability measures on . and denote the Borel -fields on and , and the Lebesgue measure on and respectively. For every measurable transformation the push-forward of via will be denoted by , i.e., for every .

As already mentioned before, will denote the family of all two-dimensional copulas. For background on copulas we refer to [6, 20]. and will denote the upper and lower Fréchet-Hoeffding bounds, the product copula. will denote the uniform distance on ; it is well known that is a compact metric space and that is a metrization of weak convergence in . For every will denote the corresponding doubly stochastic measure defined via for all (and extended in the standard way to ), the class of all these doubly stochastic measures.

A Markov kernel from to is a mapping such that is measurable for every fixed and is a probability measure for every fixed . Given real-valued random variables on , a Markov kernel is called a regular conditional distribution of given if for every

| (2) |

holds -a.s. It is well known that for each pair of real-valued random variables a regular conditional distribution of given exists, that is unique -a.s. (i.e. unique for -almost every ) and that only depends on the distribution . Hence, given , we will denote (a version of) the regular conditional distribution of given by and refer to simply as Markov kernel of or Markov kernel of . Note that for every two-dimensional distribution function , its Markov kernel , and every Borel set the following disintegration formula holds ( denoting the -section of for every )

| (3) |

For we will directly consider the corresponding Markov kernel to be defined on . Considering that in this case eq. (3) implies that

| (4) |

holds for every , and that, additionally, every Markov kernel fulfilling eq. (4) obviously induces a unique element , it follows that there is a one-to-one correspondence between and the family of all Markov kernels fulfilling eq. (4). Notice that for eq. (4) also implies that holds for -almost every , so it is always possible to choose a (version of the) kernel fulfilling for every . For more details and properties of conditional expectation, regular conditional distributions, and disintegration see [14] and [15], various results underlining the usefulness of the Markov kernel perspective can be found in [6] and the references therein.

In the sequel will denote the class of all -preserving transformations , i.e., the class of all fulfilling , the subset of all bijective , and the subset of all piecewise linear, bijective . A copula will be called completely dependent if and only if there exists such that is a regular conditional distribution of (see [16, 25] for equivalent definitions and main properties). For every the induced completely dependent copula will be denoted by throughout the rest of the paper, will denote the family of all completely dependent copulas.

Following [6, 26], for every and every copula we will let denote the (generalized) -shuffle of , defined implicitly via the corresponding doubly stochastic measures by

| (5) |

for all . Notice that is a shuffle in the sense of [4] if , and that for it is a shuffle in the sense of [18] (to which we will refer as classical shuffle in the sequel) if .

We conclude this section with the afore-mentioned translation of the maximization problems to the copula setting and start with the following lemma which is straightforward to prove via disintegration and a Dynkin system argument.

Lemma 1.

Suppose that are continuous distribution functions, that has d.f. and copula , and let denote a Markov kernel of fulfilling for all . Then setting

| (6) |

for all defines a Markov kernel of .

Suppose now that is an arbitrary Borel-measurable mapping. In the sequel we will let and denote the graph and the endograph of respectively, i.e.

| (7) |

Lemma 1 allows to express as well as in terms of and the underlying copula . In order to prove a more general result and to simplify notation, given (continuous) and (measurable) we will write

| (8) |

in the sequel. In general, is only well-defined on - we will however, directly consider it as function on by setting and .

Theorem 2.

Suppose that are random variables on with joint distribution function , continuous marginals and and copula . Furthermore let be an arbitrary Borel-measurable mapping and define according to eq. (8). Then the following identities hold for :

| (9) |

Proof.

Using the fact that , change of coordinates, disintegration and Lemma 1 the second identity can be proved as follows:

Working with instead of the first identity follows in the same manner. ∎

3 Maximizing the mass of the endograph and the prior default probability

Suppose that and model default times and that are continuous. Considering then calculating obviously corresponds to finding (joint) distributions of maximizing the probability of a prior or joint default. To simplify notation in the sequel we will simply refer to the event as ‘prior default’ (of ) although corresponds to the prior and joint default. Notice that, setting and considering the pair the afore-mentioned maximization problem can be considered a special case of the more general situation studied in [8, 9]. Theorem 2 implies

| (10) |

as well as

| (11) |

whereby . Since is non-decreasing it is possible to derive a simple formula for and even construct a dependence structure for which coincides with . The following result holds:

Theorem 3.

Suppose that is non-decreasing. Then we have

| (12) |

Moreover, defining by , we have .

Proof.

Considering it follows that

holds for every and every , which implies that the left-hand side of (12)

is smaller than or equal to the right-hand side.

To prove the reverse inequality set .

For we have for every , so taking into account we are done, and

it suffices to consider . Compactness of implies the existence of a sequence

and a point such that and .

Using we get and, using monotonicity of

it follows that . Letting denote the rotation defined by

, obviously holds. Considering that for every we have (see Figure 1)

it follows immediately that

which completes the proof. ∎

Remark 4.

Corollary 5.

Suppose that are random variables with continuous distribution functions and respectively, set and , define by , and let denote the completely dependent copula induced by . Then for with we have .

Example 6.

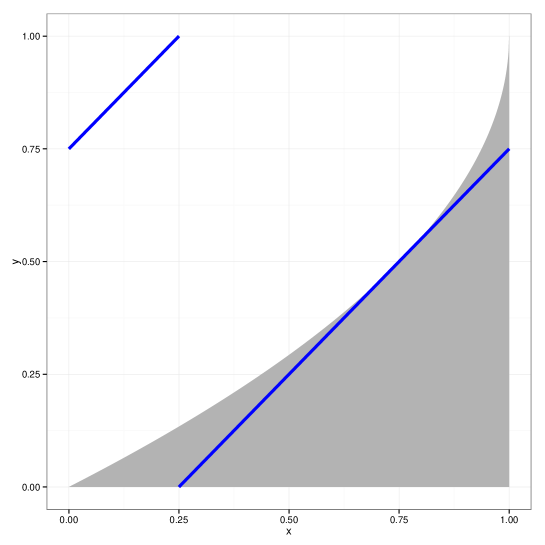

Suppose that the default times and are exponentially distributed with parameters and , respectively. It is straightforward to verify that in this case is given by , where . For the case of we have for every , so . Remarkably, for the case of the maximal mass of the endograph of and the maximal mass of the graph of coincide. In fact, applying Theorem 3, on the one hand we get

And on the other hand, according to Theorem 3 and Theorem 4 in [2] (also see [17, 24]) we have

| (13) |

where denotes the density of . Since the latter is given by we get and eq. (13) calculates to

For the special case of , which is depicted in Figure 1, we get

Example 7.

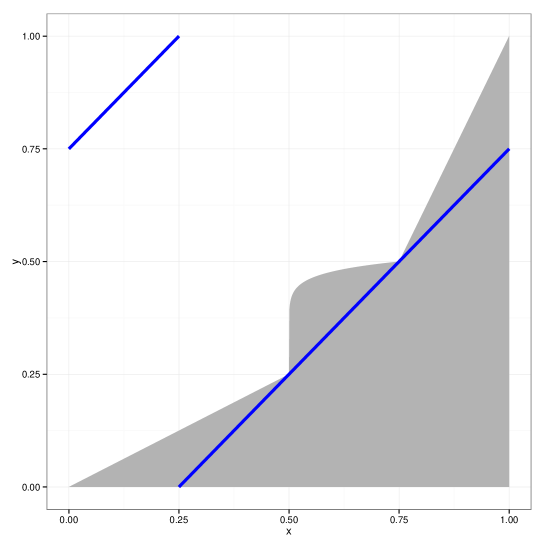

Based on Example 6 it might seem natural to conjecture that the equality holds for a much bigger class of non-decreasing transformations fulfilling for every . Since counterexamples are easily constructed for the case where is singular ( for some with ) and the case where has discontinuities, the conjecture reduces to strictly increasing, continuous transformations . For every the transformation , defined by

is easily verified to be homeomorphism with for every (see Figure 2 for the case ). Applying Theorem 3 we get , however, either by graphical arguments or by using Theorem 3 and Theorem 4 in [2] it is straightforward to verify that , so the conjecture is wrong.

Although monotonicity is crucial in the proof of Theorem 3 it is even possible to calculate

for the case of arbitrary measurable (not necessarily monotonic) transformations (as before ). Letting denote an arbitrary measurable transformation, we will now directly concentrate on the quantity

| (14) |

and prove a simple formula for only involving the d.f. of , defined by

| (15) |

We start with two simple lemmata that will be used in the proof of the main results.

Lemma 8.

Proof.

Considering and using we get

for every and every , from which the first inequality follows immediately.

Proving the existence of fulfilling can be done as follows: For every

we can find with . Compactness of implies the existence of a subsequence

and some with . If we are done since

. Suppose therefore that

and let be arbitrary. Then there exists an index such that , hence

, holds for all . Considering yields , hence,

using right-continuity of we get .

Finally, suppose that is non-decreasing. We want to show that

| (17) |

It follows directly from the construction that holds for every implying

for every and hence

which completes the proof. ∎

Lemma 9.

Suppose that are measurable transformations. Then the following two assertions hold:

-

1.

For we have .

-

2.

If and , then holds.

Proof.

To prove the first assertion set and . Considering that obviously

as well as holds for every , the desired inequality follows immediately.

To prove the second assertion let be defined by and fix .

Since obviously , defining yields a doubly stochastic measure which corresponds to

a copula (which, in turn, is easily seen to be the transpose of the -shuffle of ).

Defining by , follows

and, using disintegration, we get

Since was arbitrary it follows immediately that . ∎

Slightly modifying the ideas in the first Section of [23] it can be shown that for each measurable there exists a non-decreasing function (called the non-decreasing rearrangement of ) and a -preserving transformation such that

| (18) |

holds. Based on Lemma 8 we can now prove the following main result of this section:

Theorem 10.

Suppose that is measurable. Then we have

| (19) |

Proof.

Letting denote the operator studied in [26] and implicitly defined via

and using disintegration as well as change of coordinates we get that

| (20) | |||||

holds for every , implying . Again using and the fact that is -preserving, it is straightforward to verify that and have the same d.f., i.e. holds. Therefore, applying Lemma 8 yields

| (21) |

from which the desired equality follows immediately. ∎

According to Theorem 3 the completely dependent copula fulfills , so eq. (20) implies . By definition of we have

| (22) |

so coincides with the completely dependent copula and the following corollary holds:

Corollary 11.

Suppose that is measurable. Then there exists a completely dependent copula such that .

Having found a simple analytic formula for the maximal mass of we now derive the analogous result for the minimal mass and set

| (23) |

Given the aforementioned results, the subsequent corollary does not come as a surprise:

Corollary 12.

For every measurable transformation the following equality holds:

| (24) |

Proof.

We first concentrate on the strict endograph , defined by

Defining by for every and we obviously have that is monotonically increasing and that . Lemma 9 yields and Corollary 11 implies the existence of a copula with . Altogether we get

so considering shows that . Having this, considering

yields eq. (24). ∎

We close this section with two examples - the first one shows that is not necessarily attained whereas the second one focuses on a non-monotonic transformation for which copulas attaining and can easily be constructed.

Example 13.

For Corollary 12 yields . There is, however, no copula fulfilling , i.e. contrary to , there are situations, in which is not attained for any copula. Suppose, on the contrary, that fulfills . Then, defining by and setting , we have , so, holds for every . The latter implies , which is a contradiction since .

Example 14.

For it is straightforward to find a non-decreasing mapping and a -preserving transformation such that eq. (18) holds. In fact, defining by

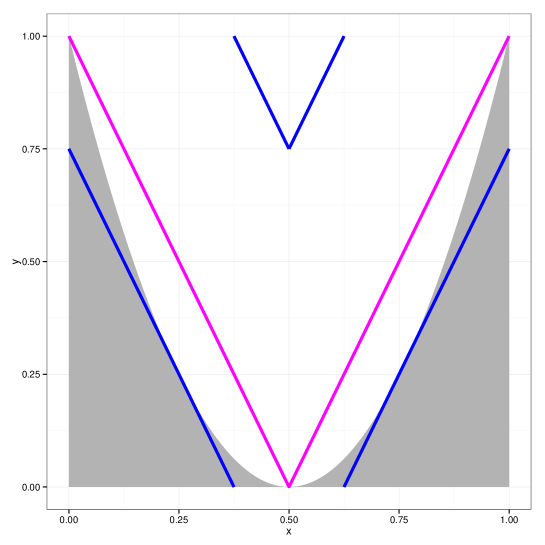

and considering we immediately get . Using eq. (22), and setting , it follows that is -preserving and that fulfills . Considering that for we obviously have , we get which coincides with . Figure 3 depicts the supports of the copulas and as well as the endograph of .

4 Maximizing the mass of the graph and the joint default probability

In what follows will denote a general non-decreasing transformation. Since the values at the (at most countably many) discontinuity points of are irrelevant for the maximization problem we will, however, assume that the non-decreasing transformation is right-continuous (or left-continuous if this simplifies technical arguments). For every such there exists a set with such that is differentiable at every (see, e.g., [21]). In the sequel we will set for every and directly consider as integrable function on without explicit mentioning. Letting denote the measure on generated by via , it follows that is (a version of) the Radon-Nikodym derivative of the absolutely continuous component of w.r.t. (see [21, Chapter 7]). Consequently, for every interval we have

| (25) |

Inequality (25) becomes a chain if equalities for all intervals if and only if is absolutely continuous. Define a new measure on by setting

| (26) |

For a given interval we distinguish the following two cases: (i) If the preimage is of the form then using ineq. (25) it follows that

(ii) If is of the form then again by ineq. (25) we get

Having this, the following simple lemma (which will be used in the proof of the main result of this section) is straightforward to prove:

Lemma 15.

Suppose that is right-continuous and non-decreasing and let be defined according to eq. (26). Then holds for every . In particular, is absolutely continuous w.r.t. and the corresponding Radon-Nikodym derivative fulfills -a.e.

Proof.

Fix and . By construction of the Lebesgue measure there exists a family of compact intervals fulfilling as well as . Using it follows that

from which, considering that was arbitrary, we immediately get . The remaining assertions are straightforward consequences of Radon-Nikodym theorem ([21]). ∎

As by-product of the results in [2] we know that for the case of non-singular (i.e. absolutely continuous w.r.t. ) there exists a copula such that, firstly, for every and, secondly,

holds. If is not non-singular, there is no copula fulfilling for every - nevertheless it is possible to find a copula (we write instead of to avoid confusion with completely dependent copulas) assigning maximal mass to and it is possible to derive a very simple formula for the maximal mass:

Theorem 16.

Suppose that is non-decreasing. Then there exists a copula such that the following equality holds:

| (27) |

Proof.

We proceed in several steps and set for every . As first step we show that for every copula the mapping , defined by , fulfills -a.e. Letting denote the set of all Lebesgue points of (see [21]) and setting it follows that . For every and sufficiently small, using disintegration and monotonicity of we get

from which, considering we directly get . Since was arbitrary and by construction, the desired inequality holds for every . As direct consequence we get

and the theorem is proved if we can show that there exists a copula fulfilling

.

We distinguish three cases (and, as before, assume w.l.o.g. that is right-continuous):

(i) If we get a.e.

Since is the Radon-Nikodym derivative of the absolutely continuous component of the measure mentioned at the beginning of

this section, considering it follows that is absolutely continuous with density and that

a.e. Hence and , and setting yields the desired result .

(ii) The case is trivial since every absolutely continuous copula fulfills .

(iii) In the remaining case of we can proceed as follows: Define a measure on by setting

and extending in the standard way ([14, 15, 21]) to full . Letting denote the projections onto the first and second coordinate, respectively, for every we get

as well as

whereby the last inequality follows from Lemma 15. As direct consequence both and are absolutely continuous measures whose densities fulfill a.e. and we have . Defining by

yields absolutely continuous distribution functions and fulfilling . Finally, let be defined by

| (29) | |||||

and set . Considering and the fact that and are two-dimensional measure-generating functions by construction, it is now straightforward to show that is a copula. In fact, the property follows via

and the remaining boundary conditions are easily verified too. Since we obviously have this completes the proof. ∎

Notice that in the case of we could have also defined by

whereby is an arbitrary (not necessarily absolutely continuous) copula, worked with and used the fact that in this case holds. As a consequence we get the following corollary:

Corollary 17.

If is non-decreasing and , then for every copula there exists a copula such that

| (30) |

We now turn to the general problem of calculating

for general measurable, not necessarily monotonic . Analogous to the case of we first show that rearranging non decreasingly as does not change the maximum mass, i.e., holds. Doing so, we will work with the so-called -operator (see [6, Definition 5.4.6]) , defined by

| (31) |

for all . It is straightforward to verify (see [5, 6]) that is well-defined, that for all we have , as well as , where denotes the star-product going back to [3]. Furthermore, considering it follows immediately that setting

for all and and extending in the standard way to defines a Markov kernel of w.r.t. the second coordinate (see [11] and [19] for Markov kernels of multivariate copulas). Since is the product measure of and , applying Fubini’s theorem we get that

| (32) |

holds for every .

Theorem 18.

Suppose that is measurable and, as before, let with denote the non-decreasing rearrangement of . Then holds.

Proof.

(i) For arbitrary , working with , using disintegration and change of coordinates we get

from which the inequality follows immediately.

(ii) To prove we use the -operator and proceed as follows.

Letting denote the completely dependent copula induced by , eq. (32) simplifies to

| (33) |

Considering we obviously have , so it follows that

Having this, using disintegration and the fact that altogether we get

Considering the fact that was arbitrary the desired inequality follows and the theorem is proved. ∎

Remark 19.

In the proof of Theorem 18 the only properties needed were that is -preserving and that we have - the fact that is non-decreasing was not used. Consequently, for arbitrary measurable and arbitrary -preserving , setting we have .

Choosing , where denotes the copula maximizing the mass of the graph of the non-decreasing rearrangement of directly yields the following result.

Corollary 20.

For every measurable transformation there exists a copula fulfilling .

Combining Theorem 18 and Corollary 17 shows that the identity

| (34) |

holds for every measurable . In most situations, however, the integral in eq. (34) is intractable, in particular since calculating the rearrangement itself is a nontrivial endeavor. Calculating for general measurable transformations in the last section, the cumulative distribution function of plays an important role - we will show now that the same is true for and derive a very simple formula only involving .

Lemma 21.

Suppose that is non-decreasing and let denote the distribution function of . Then holds.

Proof.

Let denote the set of all discontinuities of and set . Then and are at most countably infinite and for every copula and we have . Setting obviously is injective on and for every we have , implying

Letting and denote the corresponding sets for it is straightforward to verify that for every we have if, and only if . Having this the desired result follows easily: In fact, letting denote a copula with and considering the transpose we immediately get

Since the other inequality follows in the same manner the desired equality is proved. ∎

Considering that and have the same distribution function and applying Lemma 21 yields a handier version of eq. (34):

Corollary 22.

For every measurable the following equality holds:

| (35) |

Notice that in case is non-decreasing and continuous and fulfills -almost everywhere according to eq. (17) , i.e., no copula assigns mass to . This result is not surprising - considering the fact, however, that in the language of Baire categories a ‘typical’ monotonic function is singular (as established in [28]) we could infer that copulas assign no mass to ‘typical’ monotonic functions, which seems quite counterintuitive. In [2, Theorem 3] it was shown that for every non-singular there exists a copula such that the singular component of is concentrated on and that we have for -almost every . Based on Theorem 16 and Theorem 18 we can give a necessary and sufficient condition for the existence of a copula fulfilling for every in terms of the non-decreasing rearrangement of and in terms of absolute continuity of .

Corollary 23.

Suppose that is measurable, let denote its non-decreasing rearrangement and its distribution function. Then the following conditions are equivalent:

-

(a)

There exists a copula fulfilling for -almost every .

-

(b)

for -almost every .

-

(c)

is absolutely continuous.

-

(d)

is absolutely continuous.

Proof.

It is clear that (c) and (d) are equivalent so it suffices to prove , which can be done as follows. (i) Let be a copula assigning maximum mass to as constructed in the proof of Theorem 16. Letting denote a version of the Markov kernel of fulfilling for -almost every and considering we get

| (36) |

so (b) implies (a).

The implication is a direct consequence of the fact that for every with

and an arbitrary copula fulfilling (a) we have

from which follows immediately.

(iii) Simplifying notation set and suppose now that is absolutely continuous. We want to show that for

-almost every . Since is non-decreasing,

considering that and that is an interval for every , it follows that is either empty or a degenerated

interval consisting of one single point, so is necessarily strictly increasing on . Additionally, for every we obviously have

. Assume that (if holds proceed with the function that coincides with on and fulfills ).

Letting denote the Radon-Nikodym derivative of w.r.t.

we may w.l.o.g. assume for every . The function , defined by

is non-decreasing and

fulfills

| (37) |

Choose with in such a way that is differentiable at every and fulfills and that is differentiable at every . For every applying the chain rule together with equ. (37) yields

hence . This completes the proof since . ∎

Remark 24.

Again using the -operator allows for a direct proof of the implication of Corollary 23: Suppose that is arbitrary but fixed. Applying eq. (33) to the set for every we get

so, using disintegration

follows. Suppose now that fulfills for every . Using the fact that is -preserving we get that if, and only if . Since for obviously holds, the latter implies , so we can find a version of the kernel of the copula such that holds for -almost every . Having this, proceeding analogously to (36) directly yields condition (a).

5 When and coincide

The results in the previous two sections allows to characterize all non-decreasing functions for which the maximum mass of the graph and the maximum mass of the endograph coincide:

Theorem 25.

Suppose that is non-decreasing and let denote the set of all points at which is differentiable. Then the following two assertions are equivalent.

-

(a)

.

-

(b)

and there exists a point such that the following conditions hold:

-

(i)

is absolutely continuous on ,

-

(ii)

fulfills ,

-

(iii)

fulfills .

-

(i)

Proof.

We may, w.l.o.g., assume that is left-continuous.

(I) Suppose that fulfills the second assertion. It follows immediately from

condition (i) that for every we have , hence, by condition (ii), the mapping

is non-increasing on and we have . Additionally, condition (iii) implies that is non-decreasing on

, from which, using Theorem 3 we altogether get

Taking into account that (i)-(iii) also imply

the desired equality follows.

(II) On the other hand, if holds, then again by Theorem 3,

left-continuity of and Theorem 16, there exists some such that

holds. Considering together with the fact that it follows immediately that has to fulfill as well as

The latter, however, implies that is absolutely continuous on and that fulfills (ii) and (iii). ∎

Considering that every convex function with fulfills the properties listed in condition (b) of Theorem 25 we immediately get the following result:

Corollary 26.

If is convex and fulfills then holds.

According to Corollary 26, given a non-decreasing transformation , convexity and is sufficient for . The two conditions are, however, far from being necessary - the following example shows that equality can also hold for non-decreasing transformations that are not even locally convex.

Example 27.

Let denote a set with such that and hold for every non-empty open interval (for a possible construction see [12, Lemma 3.1]). Define the function by for every . Then is strictly increasing, , , is absolutely continuous and holds for -almost every (see [21]). There exists a unique fulfilling and the properties of imply that is not convex on any non-degenerated subinterval of . Based on define a new transformation by

It is straightforward to verify that is a strictly increasing homeomorphism of , which fulfills all properties stated in assertion (b) of Theorem 25. is, however, obviously not convex on any non-degenerated subinterval of (since its derivative is not non-decreasing on any non-empty open interval).

Remark 28.

Let be non-decreasing and right-continuous, and assume that holds. According to Theorem 25 in order to have the transformation needs to be absolutely continuous on the interval - on the interval , however, (interpreted as univariate measure-generating function) may be also have a non-degenerated discrete and/or singular component on as long as holds -almost everywhere on .

Remark 29.

The proof of Theorem 25 also shows that for non-decreasing all copulas with fulfill the following three conditions:

Again working with non-decreasing rearrangements and using the previous results yields the following corollary:

Corollary 30.

For every measurable the following two conditions are equivalent (as before denotes the non-decreasing rearrangement and the set of all points at which is differentiable):

-

(a)

.

-

(b)

and there exists some such that the following two properties hold:

-

(i)

is absolutely continuous on ,

-

(ii)

fulfills ,

-

(iii)

fulfills .

-

(i)

6 Estimating the maximum probability of a prior default

Throughout this section we assume that and are univariate continuous distribution functions, let be defined by on and set and , which implies that is left-continuous on . Notice that for such there exists some (not necessarily unique) with . If and are independent samples of and , respectively, then it seems natural to estimate by where and are the empirical distribution functions corresponding to and . We are now going to show that is a strongly consistent estimator for and start with the following simple lemma.

Lemma 31.

Suppose that and are continuous univariate distribution functions. Then with probability one holds for every continuity point of . In particular converges to -almost everywhere.

Proof.

Glivenko-Cantelli theorem implies that with probability we have uniform convergence of to and of to . Applying Lemma 21.2 in [27] it follows that for every continuity point of we have from which the desired result follows by a straightforward application of the triangle inequality. ∎

Theorem 32.

Suppose that and are continuous distribution functions and let and be independent samples of and , respectively. Then with probability one we have , i.e. is a strongly consistent estimator of .

Proof.

According to Lemma 31 we may assume that converges to -almost everywhere. (i) Fix and suppose that fulfills . Then there exists some such that is a continuity point of and according to Lemma 31 we can find an index such that , hence

for every . Considering that was arbitrary

follows.

(ii) Suppose now that holds for some

. Without loss of generality (choose an appropriate subsequence if necessary) we may assume that

Then for every there exists some with and we can find an index such that for every we have and

Compactness of implies the existence of a subsequence with limit . Now, choose so that is a continuity point of and holds. Choose in such a way that and that for every . According to Lemma 31 we can find another index in such a way that and that for every . Then for we altogether get

a contradiction to the definition of . This shows and the proof is complete. ∎

As final step we will now show that under mild regularity conditions on (or, equivalently on and ) the estimator is asymptotically normal. To derive asymptotic normality we will apply the functional Delta method (see [27]) and build upon the following two lemmata, whereby as in [27] and will denote the family of all cadlag functions endowed with the uniform distance :

Lemma 33.

Define by and suppose that is differentiable at . Then is Hadamard differentiable at tangentially to the set of tuples where is continuous at , with derivative fulfilling .

Proof.

Let , and such that for sufficiently small . Then using Taylor’s formula we get

where in the last step we used continuity of at . ∎

Lemma 34.

Define by , consider and set . Furthermore let be differentiable at with . Then is Hadamard differentiable at tangentially to where and are continuous at , with derivative fulfilling

Proof.

As a consequence of [27, Lemma 21.3], the map defined by is Hadamard differentiable at tangentially to the set of functions where is continuous at , with derivative fulfilling . According to Lemma 33 the map defined by is Hadamard differentiable at tangentially to the set of tuples where is continuous at , with derivative fulfilling . It hence follows from the Chain rule for Hadamard derivatives (see [27, Theorem 20.9]) that the transformation is Hadamard differentiable as well, which completes the proof. ∎

Given an interval , let denote the set of all restrictions of distribution functions on to , and the subset of consisting of all distribution functions of probability measures assigning mass to . Furthermore let denote the family of all continuous functions on . The following corollary works analogously to Lemma 21.4 in [27].

Corollary 35.

-

1.

Let and let be continuously differentiable on the interval for some , with the derivative of being strictly positive. Then defined by is Hadamard differentiable at tangentially to .

-

2.

Let have compact support and let be continuously differentiable on with the derivative of being strictly positive. Then defined by is Hadamard differentiable at tangentially to .

In both cases the derivative is the map

The next result is immediate from [1]:

Lemma 36.

Define as . Let be such that there exists a unique with . Then is Hadamard differentiable at tangentially to the set of functions with derivative given by .

We now show that under mild regularity conditions on (or, equivalently on and ) the estimator is asymptotically normal.:

Theorem 37.

Let and be the empirical distribution functions of two independent random samples and from (absolutely continuous) distribution functions and , respectively and let . If is such that there exists a unique with and are such as in Corollary 35, then for ,

is asymptotically normal with mean and variance

where .

Proof.

According to Donsker’s Theorem (see [27]) converges in distribution to in the space , for a pair of independent Brownian Bridges and . The sample paths of the two limit processes are continuous, since both, and , are continuous. By Corollary 35, Lemma 36 and the Chain Rule for Hadamard derivatives is Hadamard differentiable tangentially to the range of the limit processes. Applying the functional delta method yields that the sequence is asymptotically equivalent to the derivative of evaluated at , i.e., to . Asymptotic normality now follows from the central limit theorem. ∎

Theorem 37 considered uniqueness of the point attaining the infimum, the following final result considers the other extreme case where each point is a minimizer:

Theorem 38.

Let and be the empirical distribution functions of two independent random samples and and let . If are both then converges to (with being a standard Brownian Bridge) and thus has density .

The following final example illustrates Theorem 37.

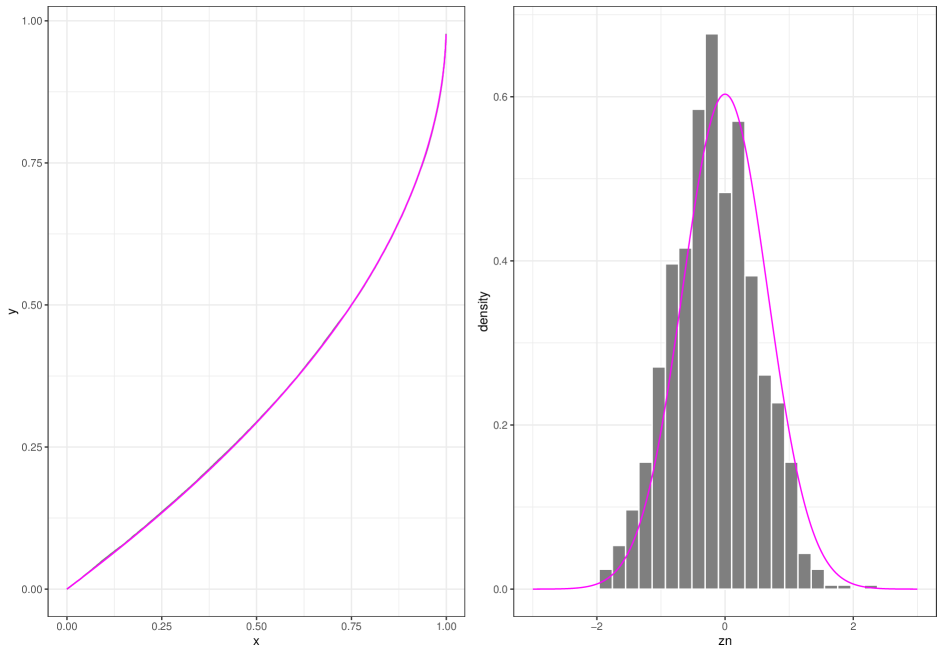

Example 39 (Example 6 continued).

Consider the setting from Example 6 for the case and . Then it is straightforward to verify that all assumptions of Theorem 37 are fulfilled, that is the unique minimizer, that , and that the asymptotic variance is given by . The right panel in Figure 4 depicts a histogram of samples of the random variable calculated by randomly drawing independent samples and from and of size , respectively.

Remark 40.

Based on simulations we conjecture that working with Bernstein approximations or splines it might be possible to derive strongly consistent estimators for too. We plan to tackle this question in the near future.

Acknowledgments

The third and the fourth author gratefully acknowledge the support of the WISS 2025

project ‘IDA-lab Salzburg’ (20204-WISS/225/197-2019 and 20102-F1901166-KZP).

References

- [1] J. Cárcamo, A. Cuevaz, L.-A. Rodríguez: Directional differentiability for supremum-type functionals: statistical applications, Bernoulli 26, 2143-2175 (2020). (see https://arxiv.org/abs/1902.01136)

- [2] F. Durante, J. Fernández Sánchez, W. Trutschnig: On the singular components of a copula, J. Appl. Probab. 52, 1175-1182 (2015).

- [3] W.F. Darsow, B. Nguyen, E.T. Olsen: Copulas and Markov processes, Illinois J. Math. 36, 600-642 (1992).

- [4] F. Durante, P. Sarkoci, C. Sempi: Shuffles of copulas, J. Math. Anal. Appl. 352, 914-921 (2009).

- [5] F. Durante, E.P. Klement, J. Quesada-Molina, P. Sarkoci: Remarks on Two Product-like Constructions for Copulas, Kybernetika 43, 235–244 (2007).

- [6] F. Durante, C. Sempi: Principles of Copula Theory, Chapman and Hall/CRC, 2015.

- [7] J. Elstrodt: Mass- und Integrationstheorie, Springer, (1999).

- [8] P. Embrechts, G. Puccetti: Bounds for functions of dependent risks, Finance and Stoch 10, 341-352 (2006).

- [9] P. Embrechts, G. Puccetti: Bounds for functions of multivariate risks, J. Multivariate Anal. 97, 526-547 (2006).

- [10] P. Embrechts, M. Hofert: A note on generalized inverses, Math. Method. Oper. Res. 77, 423-432 (2013).

- [11] J. Fern\a’andez S\a’anchez, W. Trutschnig: Conditioning based metrics on the space of multivariate copulas and their interrelation with uniform and levelwise convergence and Iterated Function Systems, Journal of Theoretical Probability 28, 1311-1336 (2015).

- [12] J. Fern\a’andez S\a’anchez, W. Trutschnig: Some members of the class of (quasi-) copulas with given diagonal from the Markov kernel perspective, Comm. Stat. A–Theor. 45, 1508-1526 (2016).

- [13] E. Hewitt, K. Stromberg: Real and Abstract Analysis, Springer Verlag, Berlin Heidelberg, (1965).

- [14] O. Kallenberg: Foundations of modern probability, Springer Verlag, New York Berlin Heidelberg, (1997).

- [15] A. Klenke: Probability Theory - A Comprehensive Course, Springer Verlag, Berlin Heidelberg, (2007).

- [16] H.O. Lancaster: Correlation and complete dependence of random variables, Ann. Math. Stat. 34, 1315-1321 (1963).

- [17] J.F. Mai, M. Scherer: Simulating from the copula that generates the maximal probability for a joint default under given (inhomogeneous) marginals, in Topics from the 7th International Workshop on Statistical Simulation ed. V. Melas, S. Mignani, P. Monari, and L. Salmaso, Springer Proceedings in Mathematics & Statistics 114, pp. 333-341, 2014.

- [18] P. Mikusínski, H. Sherwood, M.D. Taylor: Shuffles of Min, Stochastica 290, 61-74 (1992).

- [19] T. Mroz, S. Fuchs, W. Trutschnig: How simplifying and flexible is the simplifying assumption in pair-copula constructions - analytic answers in dimension three and a glimpse beyond, Electronic Journal of Statistics 15, 1951-1992 (2021).

- [20] R.B. Nelsen: An Introduction to Copulas, Springer, New York, (2006).

- [21] W. Rudin: Real and Complex Analysis, McGraw-Hill International Editions, Singapore, (1987).

- [22] L. Rüschendorf: Random Variables with Maximum Sums, Advances in Applied Probability, Vol. 14, No. 3, 623-632 (1982).

- [23] J.V. Ryff: Measure Preserving Transformations and Rearrangements, J. Math. Anal. Appl. 31, 449-458 (1970).

- [24] H. Thorisson: Coupling, stationarity, and regeneration, Probability and its Applications, Springer-Verlag, New York, (2000).

- [25] W. Trutschnig: On a strong metric on the space of copulas and its induced dependence measure, J. Math. Anal. Appl. 384, 690-705 (2011).

- [26] W. Trutschnig, J. Fernández Sánchez: Some results on shuffes of two-dimensional copulas, J. Stat. Plan. Infer. 143, 251-260 (2013).

- [27] A.W. van der Vaart: Asymptotic Statistics, Cambridge Series in Statistical and Probabilistic Mathematics, Cambridge University Press, (2000).

- [28] T. Zamfirescu: Most Monotone Functions are Singular, The American Mathematical Monthly 88(1), 47-49 (1981)