Bayesian Dividend Optimization and Finite Time Ruin Probabilities

Abstract

We consider the valuation problem of an (insurance) company under partial information. Therefore we use the concept of maximizing discounted future dividend payments. The firm value process is described by a diffusion model with constant and observable volatility and constant but unknown drift parameter. For transforming the problem to a problem with complete information, we derive a suitable filter. The optimal value function is characterized as the unique viscosity solution of the associated Hamilton-Jacobi-Bellman equation. We state a numerical procedure for approximating both the optimal dividend strategy and the corresponding value function. Furthermore, threshold strategies are discussed in some detail. Finally, we calculate the probability of ruin in the uncontrolled and controlled situation.

Keywords: dividend maximization, stochastic optimal control, filtering theory, viscosity solutions, finite time ruin probabilities

Mathematics Subject Classification (2010): 49L20, 91B30, 93E20

M. Szölgyenyi 🖂

Department of Financial Mathematics, Johannes Kepler University Linz, 4040 Linz, Austria

michaela.szoelgyenyi@jku.at

G. Leobacher

Department of Financial Mathematics, Johannes Kepler University Linz, 4040 Linz, Austria

S. Thonhauser

Department of Actuarial Science, University of Lausanne, 1015 Lausanne, Switzerland

1 Introduction

In this paper we are going to study the valuation problem of an (insurance) company. We assume that the firm value process is given by a Brownian motion with drift, and is absorbed when hitting zero.

In contrast to existing results, the drift parameter is modeled as an unobservable Bernoulli-type random variable and the company can only observe the evolution of its firm value.

In an insurance context de Finetti [6] proposed the expected discounted future dividend payments as a valuation principle for a homogeneous insurance portfolio. However, one can extend this concept to large companies, not necessarily being insurers. The accumulated dividends are described by an absolutely continuous process such that the company is capable of controlling its dividend rate with the aim of maximizing the expected value of accumulated discounted dividend payments.

In mathematical terms we face the problem of determining

where the controlled firm value, controlled by some dividend rate , and lifetime are given by

The drift parameter is a random variable with known distribution.

In this so-called Bayesian framework the company can only observe the wealth process and thus faces an optimal control problem under partial information.

The a-priori unknown drift parameter expresses the company’s uncertainty on the profitability of some business activities or an uncertainty on the general economic environment in addition to the basic risk represented by the Brownian component.

In the insurance context the unknown drift parameter can be interpreted as a residual uncertainty when using a diffusion

approximation of a classical risk reserve process instead of the original model.

For diffusion models with observable parameters this problem and several variants of it have been studied intensively, for example by

Shreve et al. [27], Jeanblanc-Piqué and Shiryaev [14], Radner and Shepp [23], and Asmussen and Taksar [2].

For an overview, the interested reader may consult Schmidli [26], Albrecher and Thonhauser [1], or Avanzi [3].

Two recent papers, Jiang and Pistorius [15], and Sotomayor and Cadenillas [28] deal with the dividend problem under a changing economic environment,

described by parameters driven by an observable Markov chain. However these models still assume full information and therefore differ from the model studied here.

The dividend maximization problem is also related to a pure optimal consumption problem of an economic agent. The agent is capable of controlling his/her consumption intensity.

Papers pointing towards optimal consumption problems arising in mathematical finance are Hubalek and Schachermayer [13] and Grandits et al. [12], maximizing expected accumulated utility of dividends, and expected utility of accumulated dividends, respectively.

In corporate finance a similar problem appears, sometimes in combination with an optimal stopping problem, in liquidity risk modeling.

There the firm value process corresponds to the cash reserve process of a

company, the market value of shares of which is given by expected future

dividend payments, for instance see Décamps and Villeneuve [7]. In this framework an

uncertain drift parameter is taken up in Décamps and Villeneuve [8],

where the solution of a special case of an associated singular control problem is presented.

Models with partial information - in particular hidden Markov models - appear

quite frequently in the literature on portfolio optimization problems, e.g., by

Karatzas and Zhao [17], Rieder and Bäuerle [24], and Sass and Haussmann [25],

whereas results relating to actuarial mathematics are more scarce. Gerber [11] uses a

Brownian motion with unknown drift for modeling the value of a single

insurance policy, of which it is a-priori not known whether it is a good or bad

risk. He answers the question of when to optimally cancel the policy, i.e.,

when the insurer should decide that the risk actually corresponds to a bad one.

For a diffusion risk reserve process with parameters generated by a hidden

Markov chain, partial differential equations associated to finite time ruin

probabilities are derived

by Elliott et al. [9].

The main contribution of the present paper is the complete analytical characterization of the

solution of the dividend maximization problem under partial information.

Furthermore, based on the analytical findings, we provide a numerical procedure for determining approximations of the optimal value function and dividend strategy. As a complement, following the path described by Elliott et al. [9],

we consider the associated finite time ruin probabilities for the uncontrolled and the controlled situation.

The paper is organized as follows. In Section 2 we give a

mathematical description of the model and the optimization problem. In Section

3 we derive, by means of filtering theory, an estimator for the

unknown drift parameter to overcome uncertainty. The applicability of the

dynamic programming approach and the associated Hamilton-Jacobi-Bellman (HJB)

equation for the filtered optimization problem are given in Section

4. Section 5 contains the complete theoretical

characterization of the optimal value function as the unique viscosity solution

of the associated HJB equation. As the proofs are rather technical, they have been moved to the Appendix. In Section 6 we describe a numerical method for

calculating approximations to the optimal value function and optimal dividend strategy.

Section 7 deals with the special class of threshold strategies, under which dividends are paid only

if the firm value process exceeds a certain threshold level. The finite time ruin probabilities are considered in Section 8.

Section 9 concludes the paper.

2 Preliminaries

In the whole paper we consider a filtered probability space carrying all stochastic quantities which will be introduced in the following.

As stated in the introduction, we assume that the firm value of a company is given by

| (1) |

with initial capital , where is the constant unobservable drift, , , is the constant and known volatility, and is a standard Brownian motion. The accumulated dividend process , , is assumed to admit a density , which is bounded, i.e., , , such that

| (2) |

Note that always corresponds to a certain strategy ,

but for avoiding an elaborate notation, we will not make that explicit as long as it causes no ambiguities.

For modeling a further uncertainty of the company’s firm value in addition to the Brownian component we assume that it is not possible

to observe the drift parameter directly, but we assume knowledge of its (initial) distribution .

We denote the uncontrolled firm value process by , which is given through

| (3) |

and obviously .

The observation filtration is the augmentation of the filtration generated by .

This means that the company is able to observe the evolution of its uncontrolled firm value and based on that decides on the dividend strategy,

or equivalently observes controlled firm value and accumulated dividends.

The value process associated with a dividend strategy is defined as

where is the time of ruin of

for the corresponding dividend strategy . depends on the strategy

via , and again we will not make this explicit if there is no danger of

confusion.

The optimal value process of the optimization problem under study is given by

where denotes the set of admissible controls, for which we take the set

of all -progressively measurable and -valued processes.

Naturally, an optimal strategy is characterized by .

Since we cannot observe the two sources and of uncertainty separately, we face a stochastic optimization problem under partial information.

For overcoming this difficulty we are going to derive an observable estimator for the drift parameter by means of filtering theory in the following section.

3 Filtering theory

Our aim is to rewrite (1) as

| (4) |

where is an observable estimator for at time and is a Brownian

motion w.r.t. our observation filtration.

Remark 3.1.

In Liptser and Shiryaev [21, p. 225] the maximum likelihood estimator for the unknown drift parameter in the present situation is given by . One may notice that this estimator only uses the information which is given by and does not consider the whole path up to time . In the following we are going to derive an alternative estimator for which is based on an application of Bayes’ rule. This estimator obeys an appealing representation in terms of a stochastic integral and induces natural boundary conditions for the optimization problem.

Using

and the law of total probability we arrive at

Now Bayes’ theorem allows us to determine

and to compute . Setting , we finally get

As a consequence we can state the following Lemma.

Lemma 3.2.

and are connected via

| (5) |

In particular, is adapted to the observation filtration.

From Liptser and Shiryaev [20, Theorem 9.1] we get that

is an -Brownian motion, sometimes referred to as innovation process. Therefore we can rewrite (1) and (3) as

| (6) | ||||

| (7) |

Due to (5), for all , where is the augmented filtration generated by and . Using Itô’s formula we derive (9), such that from now on we can consider the following system of state variables

| (8) | ||||

| (9) |

Remark 3.3.

Let be any progressively measurable bounded process. Equation (9) does not depend on and therefore has a solution by the well-known theorem on existence and uniqueness of solutions of SDEs with Lipschitz coefficients. See, for example, Krylov [18, Chapter 2, Theorem 7].

does not appear on the right hand side of (8), so this becomes just an ordinary integral.

4 The Hamilton-Jacobi-Bellman equation

In this section we will show that the dynamic programming approach is applicable for solving the optimization problem when considering

as state variables.

Remember the definition of the optimal value process

The system (8) and (9) describes autonomous state dynamics in the sense of [10, Section IV.5]. It is therefore natural to consider Markov controls in the following. Furthermore, due to the Markovian structure and the infinite horizon, we get that

a.s., where from now on and

denotes the optimal value function of the optimization problem. For a strategy we define

From now on we abbreviate the expectation given the initial values and by .

Remark 4.1.

From Krylov [18, Chapter 3, Theorem 5] we know that the optimal value function is continuous.

Lemma 4.2.

We have and uniformly in . Furthermore, is increasing in both parameters.

Proof.

Clearly, . On the other hand, we have , where

Since we always assume ,

and therefore such that

The last expectation can be computed using standard techniques: for every the process defined by is a martingale and the stopped process is a bounded martingale, such that , and hence . We therefore get , where

| (10) |

The monotonicity of with respect to both parameters follows from a pathwise argument similar to that above. Thereby one has to keep in mind the assumption . ∎

Formally applying Itô’s formula to gives

We now prove a version of the dynamic programming principle, or Bellman principle.

Proposition 4.3 (Bellman principle).

For every bounded stopping time we have

Proof.

Let be some -optimal strategy for , then

which proves that , since was arbitrary.

On the other hand, for any we have

where and are -optimal

and -optimal strategies for and

, respectively. From the continuity of

one can construct these strategies by a similar procedure as stated in

Azcue and Muler [4].

The concrete procedure for constructing is as follows.

Fix ,

and determine such that

for all

. Note that for an initial value with the strategy

is -optimal.

Choose grid points and such that the rectangles cover . Since is increasing with each parameter, we have that

whenever . Now, because of continuity of , the number and the grid points can be chosen such that

for all . Let be an -optimal strategy for ,

Note that also .

The strategies together with define the strategy for . For we get

Finally, we choose an -optimal strategy for the right hand side of the dynamic programming principle, i.e.,

Now we put everything together. For any strategy

where

Thus we have for any that , and therefore

Since was arbitrary, the proof is finished. ∎

Now, still under the assumption , we apply the dynamic programming principle and derive

Therefore,

and by letting we arrive at

Thus, the associated Hamilton-Jacobi-Bellman equation is given by

| (11) |

The HJB equation is a second order degenerate-elliptic PDE since

there is only one Brownian motion driving the two-dimensional process .

Now it remains to find appropriate boundary conditions. The ones for

and follow from the definition of and from

Lemma 4.2, respectively:

| (12) | ||||

| (13) |

The ones for , are obtained by solving the optimal control problem for known deterministic drift, as has been done in Asmussen and Taksar [2]. We give their solution with notation adapted to our setup:

| (14) |

where and

| (15) | ||||

| (16) | ||||

| (17) | ||||

| (18) | ||||

| (19) | ||||

| (20) | ||||

| (23) |

Remark 4.4.

We could give the parameters relative to , that is , , . Then cancels from all expressions in (15)–(23).

In other words: the qualitative behavior of the model only depends on the relative values between the parameters .

Remark 4.5.

For known deterministic drift the optimal strategy is of threshold type: no dividends are paid for , and for dividends are paid at maximum rate .

A numerical solution of the HJB equation will be presented in Section 6. We will see that the numerical results suggest that also in our Bayesian setup a threshold strategy is optimal.

5 Viscosity Solution Characterization

In this section we present the main theoretical results of this paper.

In the univariate setting, as described in Asmussen and Taksar [2],

it is possible to determine a smooth explicit solution of the associated HJB equation,

whereas in the present situation the HJB equation (11) hardly allows for such a solution.

As a consequence one needs to rely on numerical methods for obtaining a solution of the optimization problem

and the crucial theoretical basis is the uniqueness of a solution of (11).

Since a-priori the regularity of a solution is questionable, we need a weaker solution concept, which still allows to prove uniqueness.

Therefore, we characterize the optimal value function as the unique viscosity solution of (11),

since this concept also serves as a basis for numerical considerations.

Below we present the concept of viscosity solutions for the HJB equation under study.

A more detailed treatment can be found in Fleming and Soner [10] or Crandall et al. [5].

Denote

, and let

denote its boundary.

Definition 5.1.

(viscosity solution)

The derivation of (11) was done in a heuristic way. The following theorem shows that the optimal value function is indeed connected to it in a weak sense.

The uniqueness result is based on comparison, which is dealt with in the next theorem.

Remember that the optimal value function exhibits the following properties:

it is continuous on ,

bounded, i.e., , and

uniformly in .

Theorem 5.3 (Comparison).

Let and be a bounded and continuous viscosity subsolution and supersolution of (11),

respectively.

If on

and

uniformly in , then on .

As a corollary we get uniqueness of the viscosity solution of (11).

Corollary 5.4.

The optimal value function is the unique bounded viscosity solution of (11) with the given boundary conditions.

Proof.

Suppose there is another solution . Then since both and are subsolutions and supersolutions fulfilling the same boundary conditions we get that and . ∎

Finally we give a verification theorem.

Theorem 5.5.

Remark 5.6.

Suppose one can construct a strategy such that is a supersolution with almost everywhere. Then Theorem 5.5 implies that and thus is the optimal strategy.

6 Policy iteration and numerical examples

In this section we describe a numerical scheme to compute an approximation to the optimal dividend policy and optimal value function.

We have already noted in Lemma 4.2 that, as becomes large, the optimal value function approaches uniformly in . For our algorithm we choose a large number and approximate the domain of the value function by . (In the numerical examples is chosen such that , where is defined by Equation (10) .) We impose the boundary conditions (12), (14), and

| (24) |

where are as defined by equations (17), (20), (23), and we may assume that . We thus have continuous boundary conditions and the ones for differ from by less than .

Next we define a grid in , , . We want to be able to put more grid points into regions which are of higher interest, that is, close to the values and, in the -direction, between and . More concretely, we choose bijective functions and we set , and , .

We use the following definitions, with , :

where , , and

Note that are continuously differentiable with in and that we get an evenly spaced grid for , , .

We start with a simple (threshold) strategy: let , and consider the Markov strategy , , i.e., dividends are paid at the maximum intensity , if the firm value exceeds the threshold level , otherwise no dividends are paid. We use policy iteration to improve the strategy.

More precisely, if a Markov strategy is given, we solve

where is the operator with differentiation operators replaced by suitable finite differences and is a finite difference approximation to differentiation with respect to . Then is the function that maximizes , that is , and the iteration stops as soon as .

The details of the method as well as proofs of convergence can be found in Fleming and Soner [10, Chapter IX].

We computed the optimal strategy and the corresponding value function for

the parameter choice , , ,

, and the following values of and :

B

In those examples the iteration stops after 3 steps and the resulting strategy turns out to be a threshold strategy with the threshold depending on the estimate of .

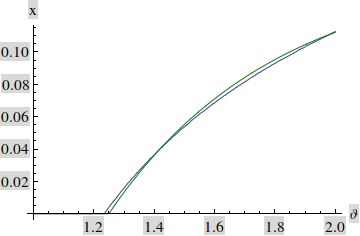

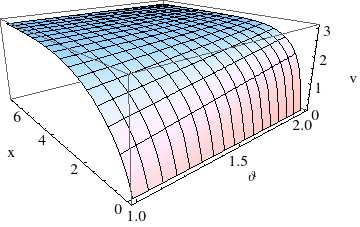

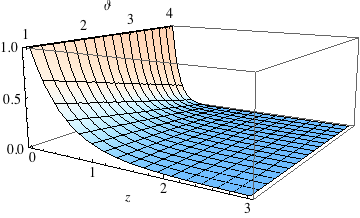

Figure 1 shows the threshold level (blue) in dependence of and, for comparison, also the corresponding classical threshold level (green) from equation (20). Interestingly, the difference between these levels can be substantial, both quantitatively and qualitatively.

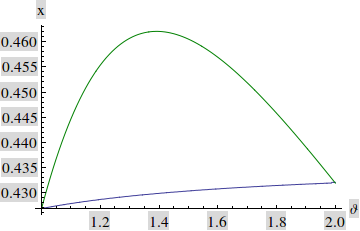

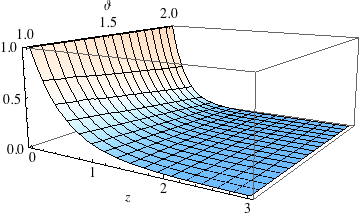

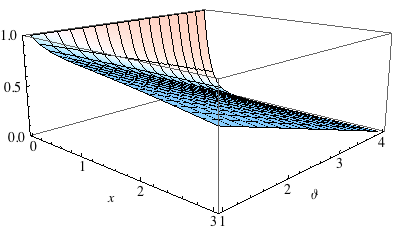

Figure 2 shows the value function corresponding to . We have refrained from showing the plots of the corresponding value functions for the other values of as they all look very similar to the one in Figure 2.

Remark 6.1.

Figure 2 suggests that the value function is smooth and that therefore it should even be a classical solution of the HJB equation. However, proving smoothness is beyond the scope of this paper, since the HJB equation is degenerate elliptic on the whole domain, i.e., the diffusion coefficient is singular, which is highly non-standard.

Remark 6.2.

All of our examples give threshold strategies as the optimal dividend strategy. The convergence results from Fleming and Soner [10, Chapter IX] imply that, at least for our parameter sets, we can compute an -optimal value function corresponding to a threshold strategy.

7 Threshold strategies

The solution for the case where the drift of the uncontrolled wealth process is deterministic as well as the numerical treatment of the Bayesian case suggest that the optimal dividend strategy is of threshold type, that is, there is a threshold level such that as soon as the wealth process exceeds the threshold level, dividends are paid at the maximum rate.

The numerical treatment for the Bayesian case further suggests that the threshold level depends on the estimate for . In this section we formally define threshold strategies of this type and we give sufficient conditions under which they are admissible. We then proceed with giving a sufficient condition on a threshold strategy for being optimal. Of course one would also like to know whether there always exists at least one optimal strategy of threshold type. Unfortunately, this question has to remain open for the time being.

Definition 7.1.

Let be a continuous function and let , , where are defined in (20).

A threshold strategy with threshold level is given by

First, we have to clarify whether threshold strategies are admissible. The system (8), (9), with replaced by a stationary Markov strategy, reads

| (25) | ||||

| (26) |

A priori it is far from obvious that there exists a solution to the system (25), (26) if is a general measurable function. If is Lipschitz in both variables, then a solution exists by the classical theorem on existence and uniqueness of solutions of SDEs, see, e.g., [18, Chapter 2, Theorem 7]. But our threshold strategies do not fall in that category. In Leobacher et al. [19] it is shown that the system (8), (9) has a unique strong maximal local solution, if is a threshold strategy with a threshold function , satisfying

for some constant . The latter condition means that the diffusion must not be parallel to the discontinuity of the drift. Since in our case is a continuous function on a compact interval, this condition is equivalent to . Furthermore, as the diffusion coefficients are Lipschitz and the drift of is bounded, we can apply [19, Theorem 3.3] and get that the system (25), (26) even has a unique strong global solution until the time . Therefore, threshold strategies are indeed admissible if is sufficiently regular. In case of a threshold level like the one in Figure 1 where for small values of we have , and then the curve grows monotonously, is clearly not sufficiently smooth. However, in that particular case that does not pose a problem, since equals zero at the point of the kink and the process is stopped once it reaches zero, i.e., when we have ruin. Thus we need not consider solutions starting in that point or passing through it.

The above discussion is summarized in the following definition and the subsequent lemma:

Definition 7.2.

Lemma 7.3.

Let be a function satisfying

-

1.

is continuous;

-

2.

, ;

-

3.

on any interval on which holds, is and .

Then .

In the following we give a characterization of value functions corresponding to optimal threshold strategies.

Definition 7.4.

A function fulfills in the viscosity sense, if for all and for all such that is a minimum of and , we have .

In other words, in the viscosity sense, if is a viscosity supersolution of .

Definition 7.5.

A function fulfills () in the viscosity sense, if

for all and for all such that is a minimum of with .

Remark 7.6.

-

1.

As for previous definitions of “viscosity sense” we have for that [() in the viscosity sense] [() ].

-

2.

Note that [ ] [) ].

In the following we denote the value function coming from a threshold strategy

as and

, with .

As in Asmussen and Taksar [2] one can not guarantee enough smoothness of for an arbitrary

threshold strategy.

Therefore we characterize as a viscosity solution of an appropriate PDE.

Lemma 7.7.

Proof.

The following theorem provides the link between the value of a threshold strategy and the HJB equation (11).

Theorem 7.8.

Let a threshold level exist with and () in the viscosity sense.

Then is a viscosity solution of (11).

Proof.

First, we show that if is a viscosity subsolution of (27), it is also a viscosity subsolution of (11).

Since is a viscosity subsolution of (27), it holds that , in and for all where ,

We have to show that

holds in the same points . Therefore, it is enough to show that

which is equivalent to

If , we need that , which is obviously true. If , we need that . Since , this holds, too.

So is a viscosity subsolution of (11).

It remains to show that if is a viscosity supersolution of (27), it is also a viscosity supersolution of (11).

Since is a viscosity supersolution of (27), it holds that , in and for all where it holds that

We have to show that

holds in the same points . Hence, we need that

If or , we get and , respectively. Therefore, we have to show that , if and , if . Hence, we need that .

From the statement of the theorem we have that () in the viscosity sense,

which is actually equivalent to what we need. Thus, is a viscosity supersolution of (11).

Altogether, is a viscosity solution of (11). ∎

Corollary 7.9.

Let be like in Theorem 7.8. Then .

Altogether, we now know that if with a threshold level and corresponding value function such that in the viscosity sense, then and is the optimal control strategy.

8 Finite time ruin probabilities

In this section we will determine the finite time ruin probability of the uncontrolled process

where , for all .

abbreviates the probability given the initial values and .

Furthermore, we will consider the finite time ruin probability of our

controlled process, assuming that the control variable follows a threshold

strategy as defined in Section 7. So

where , and .

The finite time ruin probability is denoted as

Trivially, for , the finite time ruin probabilities and are both equal to 1. Subsequently, we will tacitly assume that .

Remark 8.1.

For constant and observable a classical application of Girsanov’s theorem and the reflection principle yields that the finite time ruin probability of the uncontrolled process is given by

where is the cumulative distribution function of the standard normal distribution (cf. Karatzas and Shreve [16, p. 197]).

Now we want to calculate the finite time ruin probability for unobservable .

In Elliott et al. [9] results from filtering theory are applied to a general

hidden Markov model and a PDE is derived, the solution of which is proven to be

the finite time survival probability. We apply a different filter to overcome

uncertainty, but after that, we

use a similar result for our processes and . From the finite time survival probability we easily get the finite time ruin

probability, which is just the complementary probability.

Let

be the infinitesimal generator of and let ,

where is the indicator function of the domain .

Furthermore, let

be the infinitesimal generator of and let .

Then the following theorem, similar to Elliott et al. [9, Theorem 4.1], holds.

Theorem 8.2.

-

1.

If is a smooth solution to

(28) with initial condition

and boundary conditions

and , is the solution of the PDE for fixed , then

-

2.

If is a smooth solution to

(29) with initial condition

and boundary conditions

and , is the solution of the PDE for fixed , then

Proof.

Similar to the proof of Elliott et al. [9, Theorem 4.1]. ∎

Remark 8.3.

From the finite time survival probability we easily get the finite time ruin probability

We solved the PDEs numerically. Note that in our computations the boundary conditions for the -variable are the numerical solutions of the corresponding PDEs for fixed and , respectively.

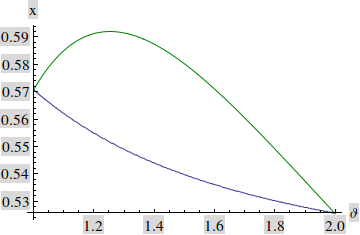

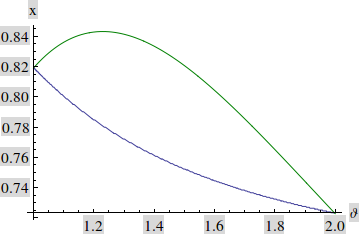

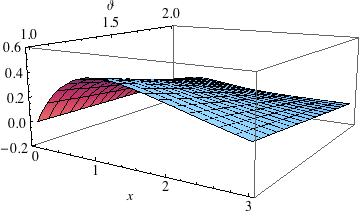

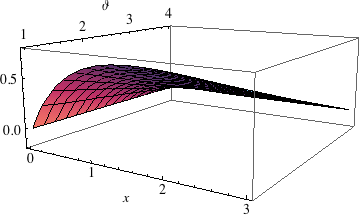

Figure 3 shows the finite time ruin probability in the uncontrolled and the controlled situation for the parameter choices , , , and , , , and , , . The boundary curve coincides with the deterministic situation, where , . One can see that, depending on the estimate of , the difference between the controlled and the uncontrolled situation varies.

Remark 8.4.

Note that for the uncontrolled process an alternative way to calculate is

9 Conclusion and open problems

We have presented a dividend optimization problem under partial information where the drift coefficient of the diffusion firm value process is a-priori unknown. We have shown how the drift coefficient can be estimated and we have derived the HJB equation for the stochastic optimal control problem.

It turns out that the optimal value function of the problem is the unique viscosity solution of the HJB equation, which allows for a numerical treatment of the problem. The numerical method gives an approximation to the optimal dividend policy and the corresponding value function. The treated examples suggest that threshold strategies are the optimal ones and we have discussed those strategies in more detail.

Finally, we have derived a PDE for the finite time ruin probability in our model

and we have computed concrete examples numerically,

both for the uncontrolled and controlled process.

As already mentioned in Section 7, a proof that there is always an optimal strategy of threshold type is yet to be found. The results of the numerical calculations suggest that this is the case. In addition, the plots of the corresponding value functions look smooth, so that one may have the hope that it is actually a classical solution to the HJB equation. Due to the degeneracy of the diffusion coefficient, a proof for this is beyond reach at the moment. We formulate the following conjectures:

Conjecture 1.

Conjecture 2.

Let denote the optimal threshold for the non-Bayesian case and let be our optimal threshold function. From Figure 1 one would guess that

-

1.

; in particular, if then does not depend on the Bayesian estimator;

-

2.

if , then is strictly increasing and strictly concave;

-

3.

if , then is strictly decreasing and strictly convex.

Appendix A Supplementary proofs

Proof of Theorem 5.2.

We have to show that is both a viscosity sub- and supersolution.

is a viscosity supersolution: Let , and such that .

From the dynamic programming principle we have

for any fixed .

Applying Itô’s formula to , noting that the stochastic integrals are martingales, dividing by and letting gives

Since was arbitrary we get

So is a viscosity supersolution.

is a viscosity subsolution: For let with .

Let be the density of an -optimal dividend

policy, i.e., and denote the firm

value coming from as . Furthermore, let

, and such that .

where we applied Itô’s formula and used that the stochastic integrals are martingales. Now, we divide by and let . Since and . Thus,

Since , we get

So V is also a viscosity subsolution.

In total is a viscosity solution of the HJB equation. ∎

Proof of Theorem 5.3.

We are going to prove the statement of the theorem by contradiction, using standard arguments from [5] and [22] adapted to our specific situation.

Suppose there exists such that

Since and are assumed to be bounded, we have

Now on we already have by assumption, and uniformly in . Because of that and the continuity of and , we have that the maximum of needs to be attained at an interior point of with finite -component. Therefore there exists and , such that

Define for ,

for . The function is again continuous and it attains a maximum on its compact domain at some point . Furthermore we have

The sequence on is bounded, therefore there exists a subsequence which converges to some value when . At the same time is bounded as well which implies that

is bounded as . This implies that in the limit , and directly from the inequality above we have

and . In addition we obtain, at least along another subsequence and

.

Without loss of generality we can assume that we already deal with the convergent subsequence

and, since is an interior point, that .

In the following step we are going to apply Ishii’s Lemma in the form it is stated in [5, Theorem 3.2].

For this purpose we set

for . We have that attains a maximum in . At these points we have

and with denoting the identity matrix we can write

From [5, Theorem 3.2] we obtain, for every , that there exist symmetric matrices and such that , which is the so-called superjet of at , and , which is the so-called subjet of at . In particular these matrices fulfill:

Choosing and taking the square of the matrix explicitly we get

| (34) |

Before using these super-subjet properties, we are going to derive a bound for the second order terms occurring in the HJB equation.

Define and write

Now we are going to use inequality (34),

| (39) | ||||

| (40) |

The super-subjet notions appear in an equivalent formulation of the viscosity solution property based on second-order super and subdifferentials,

see [10, Lemma 4.1, p. 211] or [5, Section 2].

Since is a viscosity subsolution of (11), the statement

is equivalent to the existence of a subsolution test function at with first derivative equal to and second

derivative equal to .

At the same time the statement is equivalent to the existence of

a supersolution test function, again with the first derivative given by and second derivative equal to .

Therefore, from the subsolution property of and the supersolution property of (using the above-mentioned derivatives for the respective test functions) we derive

Rearranging and using (40) yields

In the above inequality the left-hand side converges to as . Since at the same time (other terms are bounded), the right-hand side converges to , resulting in the contradiction , which concludes the proof of the theorem. ∎

Proof of Theorem 5.5.

Let be an admissible strategy and let . Then

After taking expectations, the stochastic integral vanishes. Therefore,

Let . Since fulfills

we can choose large enough such that

and hence

Therefore we get

Letting , we get by dominated convergence

As was arbitrary, we further get

and hence

From the supersolution property we have that . Thus we have, by Fatou’s Lemma,

So for each control , dominates the value function. Taking the supremum over in the derivation, we get equality in the HJB equation and therefore

which completes the proof. ∎

References

- Albrecher and Thonhauser [2009] H. Albrecher and S. Thonhauser. Optimality Results for Dividend Problems in Insurance. RACSAM Revista de la Real Academia de Ciencias Exactas, Fisicas y Naturales. Serie A. Matematicas, 103(2):295–320, 2009.

- Asmussen and Taksar [1997] S. Asmussen and M. Taksar. Controlled Diffusion Models for Optimal Dividend Pay-Out. Insurance: Mathematics and Economics, 20(1):1–15, 1997.

- Avanzi [2009] B. Avanzi. Strategies for Dividend Distribution: A Review. North American Actuarial Journal, 13(2):217–251, 2009.

- Azcue and Muler [2005] P. Azcue and N. Muler. Optimal Reinsurance and Dividend Distribution Policies in the Cramér-Lundberg Model. Mathematical Finance, 25(2):261–308, 2005.

- Crandall et al. [1992] M. Crandall, H. Ishii, and P. Lions. User’s Guide to Viscosity Solutions of Second Order Partial Differential Equations. Bulletin of the American Mathematical Society, 27(1):1–67, 1992.

- de Finetti [1957] B. de Finetti. Su un’impostazione alternativa della teoria collettiva del rischio. Transactions of the XVth International Congress of Actuaries, 2:433–443, 1957.

- Décamps and Villeneuve [2007] J.-P. Décamps and S. Villeneuve. Optimal dividend policy and growth option. Finance Stoch., 11(1):3–27, 2007.

- Décamps and Villeneuve [2012] J.-P. Décamps and S. Villeneuve. A Bayesian Adaptive Singular Control Problem Arising from Corporate Finance, 2012. Slides of a talk given at Swissquote Conference on Liquidity and Systemic Risk, November, EPFL, Lausanne, Switzerland.

- Elliott et al. [2011] R. Elliott, T. Siu, and H. Yang. Ruin Theory in a Hidden Markov-Modulated Risk Model. Stochastic Models, 27(3):474–489, 2011.

- Fleming and Soner [2006] W. Fleming and H. Soner. Controlled Markov Processes and Viscosity Solutions. Stochastic Modelling and Applied Probability. Springer, second edition, 2006.

- Gerber [1977] H. Gerber. On Optimal Cancellation of Policies. ASTIN Bulletin, 9(1):125–138, 1977.

- Grandits et al. [2007] P. Grandits, F. Hubalek, W. Schachermayer, and M. Žigo. Optimal Expected Exponential Utility of Dividend Payments in a Brownian Risk Model. Scandinavian Actuarial Journal, 2:73–107, 2007.

- Hubalek and Schachermayer [2004] F. Hubalek and W. Schachermayer. Optimizing Expected Utility of Dividend Payments for a Brownian Risk Process and a Peculiar Nonlinear ODE. Insurance Math. Econom., 34(2):193–225, 2004.

- Jeanblanc-Piqué and Shiryaev [1995] M. Jeanblanc-Piqué and A.N. Shiryaev. Optimization of the Flow of Dividends. Russian Math. Surveys, 50(2):257–277, 1995.

- Jiang and Pistorius [2012] Z. Jiang and M. Pistorius. Optimal Dividend Distribution under Markov Regime Switching. Finance and Stochastics, 16(3):449–476, 2012.

- Karatzas and Shreve [1991] I. Karatzas and S.E. Shreve. Brownian Motion and Stochastic Calculus. Graduate Texts in Mathematics. Springer-Verlag, New York, second edition, 1991.

- Karatzas and Zhao [2001] I. Karatzas and X. Zhao. Bayesian Adaptive Portfolio Optimization. In Options Pricing, Interest Rates and Risk Management. Cambridge University Press, 2001.

- Krylov [1980] N.V. Krylov. Controlled Diffusion Processes. Applications of Mathematics. Springer, 1980.

- Leobacher et al. [2013] G. Leobacher, M. Szölgyenyi, and S. Thonhauser. On the Existence of Solutions of a Class of SDEs with Discontinuous Drift and Singular Diffusion. 2013. Submitted, arXiv:1311.6226.

- Liptser and Shiryaev [1977] R.S. Liptser and A.N. Shiryaev. Statistics of Random Processes I - General Theory. Applications of Mathematics. Springer, 1977.

- Liptser and Shiryaev [2000] R.S. Liptser and A.N. Shiryaev. Statistics of Random Processes II - Applications. Applications of Mathematics. Springer, second edition, 2000.

- Pham [2009] H. Pham. Continuous-Time Stochastic Control and Optimization with Financial Applications. Stochastic Modeling and Applied Probability. Springer, 2009.

- Radner and Shepp [1996] R. Radner and L. Shepp. Risk vs. Profit Potential: A Model for Corporate Strategy. Journal of Economic Dynamics and Control, 20(8):1373–1393, 1996.

- Rieder and Bäuerle [2005] U. Rieder and N. Bäuerle. Portfolio Optimization with Unobservable Markov-Modulated Drift Processes. Journal of Applied Probability, 42:362–378, 2005.

- Sass and Haussmann [2004] J. Sass and U. Haussmann. Optimizing the Terminal Wealth under Partial Information: the Drift Process as a Continuous Time Markov Chain. Finance and Stochastics, 8:553–577, 2004.

- Schmidli [2008] H. Schmidli. Stochastic Control in Insurance. Probability and its Applications. Springer, 2008.

- Shreve et al. [1984] S.E. Shreve, J.P. Lehoczky, and D.P. Gaver. Optimal Consumption for General Diffusions with Absorbing and Reflecting Barriers. SIAM Journal on Control and Optimization, 22(1):55–75, 1984.

- Sotomayor and Cadenillas [2011] L. Sotomayor and A. Cadenillas. Classical and Singular Stochastic Control for the Optimal Dividend Policy when there is Regime Switching. Insurance: Mathematics and Economics, 48:344–354, 2011.

- Wheeden and Zygmund [1977] R. Wheeden and A. Zygmund. Measure and Integral: An Introduction to Real Analysis. Pure and Applied Mathematics. Marcel Dekker Inc., 1977.