Lasso Guarantees for Time Series Estimation under Subgaussian Tails and -Mixing

Abstract

Many theoretical results on estimation of high dimensional time series require specifying an underlying data generating model (DGM). Instead, along the footsteps of wong2017lasso , this paper relies only on (strict) stationarity and -mixing condition to establish consistency of lasso when data comes from a -mixing process with marginals having subgaussian tails. Because of the general assumptions, the data can come from DGMs different than standard time series models such as VAR or ARCH. When the true DGM is not VAR, the lasso estimates correspond to those of the best linear predictors using the past observations. We establish non-asymptotic inequalities for estimation and prediction errors of the lasso estimates. Together with wong2017lasso , we provide lasso guarantees that cover full spectrum of the parameters in specifications of -mixing subgaussian time series. Applications of these results potentially extend to non-Gaussian, non-Markovian and non-linear times series models as the examples we provide demonstrate. In order to prove our results, we derive a novel Hanson-Wright type concentration inequality for -mixing subgaussian random vectors that may be of independent interest.

keywords:

[class=MSC]keywords:

1602.04265

and label=u1,url]http://www.foo.com t2Most of Zifan Li’s contribution to this work occurred while he was an undergraduate student at the University of Michigan.

1 Introduction

Efficient estimation methods in high-dimensional statistics (buhlmann2011statistics, ; hastie2015statistical, ) include methods based on convex relaxation (see, e.g., chandrasekaran2012convex ; negahban2012unified ) and methods using iterative optimization techniques (see, e.g., beck2009fast ; agarwal2012fast ; donoho2009message ). A lot of work in the past decade has improved our understanding of the theoretical properties of these algorithms. However, the bulk of existing theoretical work focuses on iid samples. The extension of theory and algorithms in high-dimensional statistics to time series data is just beginning to occur as we briefly summarize in Section 1.2 below. Note that, in time series applications, dependence among samples is the norm rather than the exception. So the development of high-dimensional statistical theory to handle dependence is a pressing concern in time series estimation.

The information age and scientific advances have led to explosions in large data sets, among which many exhibit temporal dependence. These can include, for example, data from micro-array experiments, dynamic social networks, mobile phone usage, high frequency stock market trading, daily grocery sales, etc. To gain insights into how variables interact with each other over time and/or to do forecasting, it is important to do a systematic analysis on all the variables simultaneously.

The vector autoregressive (VAR) family is popular choice to study the network of dynamic interactions among variables in high dimensions. Formally, given a -dimensional time series, , where , and for iid innovations , a VAR() model admits the representation

Sims proposed using the VAR model as a theory-free model for Granger causality sims1980macroeconomics . Theoretical foundations on using VAR comes from the Wold decomposition theorem which guarantees that any covariance-stationary time series can be approximated by a finite order autoregressive model (and a deterministic part). Empirically, VAR has proven to be a successful Granger causality framework in domain science applications. The variables in the VAR can represent: economic variables from temporal panel data where the panel of subjects can be individuals, firms, households, etc. cao2011asymptotic ; binder2005estimation ; macroeconomic variables, including government spending and taxes on economic output blanchard2002empirical ; stock price and volume hiemstra1994testing ; gene expressions in a dynamic regulatory network michailidis2013autoregressive ; or, regions of the brain from time course fMRI data krumin2010multivariate .

The set of coefficient matrices provides insights into the interrelationships among variables over time. For example, a non-zero -entry in reflects that likely has influence on after -steps. Under the high-dimensional settings, we are interested in a sparse predictor of the present observation using a linear combination of the past because we believe that not all variables will have a significant influence on every other variable. We consider the -regularized least squares, or lasso, estimation of the problem. When the data are truly sampled from a VAR, the lasso estimates are those of the VAR transition matrices. Otherwise, the lasso estimates the best sparse linear predictor of in terms of . Under stationarity (and finite 2nd moment conditions), the estimand is well defined even if the DGM is not a finite order VAR.

This paper provides finite sample parameter estimation and prediction error bounds for lasso in stationary processes with subgaussian marginals and geometrically decaying -mixing coefficients (Corollary 4). A previous work wong2017lasso proved lasso guarantees for -mixing times series with subweibull observations. To be specific, the subweibull parameter measures rate of probability tail decay while quantifies dependence among observations in the series (Assumptions 6 and 7 in wong2017lasso ). The pair characterizes the difficulty landscape of the lasso problem. For example, (independence) and (a.s. bounded) corresponds to an easy case while and a hard one. wong2017lasso provided lasso guarantees for the sets of such that . In this paper, the lasso results pertain to geometrically -mixing () time series with subgaussian observations (equivalent to subweibull with ). Together, we have lasso consistency results that cover the full spectrum of possibilities for the pair .

1.1 Overview of the Paper

This paper provides non-asymptotic lasso consistency guarantees of VAR estimation and prediction for data sampled from large classes of data-generating mechanisms (DGMs). This generalizes the current lasso theory from (1) Gaussian to subgaussian data, and from (2) requiring known parametric DGMs to weaker and more general mixing conditions which, roughly speaking, means that two observations far apart in time are approximately independent. The non-asymptotic rates of decay are close to being optimal. Our results rely on novel concentration inequality (Lemma 1) for -mixing subgaussian random variables that may be of independent interest. The inequality is proved by applying a blocking trick to Bernstein’s concentration inequality for iid random variables. All proofs are deferred to the appendix.

These guarantees serve to show that we can safely employ the VAR framework to do estimation and/or prediction on high-dimensional data sampled from a wide range of DGMs. To illustrate potential applications of our results, we present four examples. Example 1 considers a vanilla Gaussian VAR. Example 2 considers VAR models with subgaussian innovations. Examples 3 is concerned with subgaussian VAR models when the model is mis-specified. Finally, we go beyond linear models and introduce non-linearity in the DGM in Example 4. To summarize, our theory for lasso in high-dimensional time series estimation extends beyond the classical linear Gaussian settings and provides guarantees potentially in the presence of model mis-specification, subgaussian innovations and/or nonlinearity in the DGM.

1.2 Recent Work on High Dimensional Time Series

Because our predictive model is the VAR, we wish to mention that recently, basu2015regularized took a step forward in providing guarantees for lasso in finite lag Gaussian VAR models(see Example 1) in terms of their measure of stability. Their bounds are more general than the previous work (negahban2011estimation, ; loh2012high, ; han2013transition, ) by lifting the operator norm bound condition on the transition matrix. These operator norm conditions are restrictive even for VAR models with a lag of and never hold if the lag is strictly larger than 1! Therefore, the results of basu2015regularized are very interesting. But they do have limitations.

A key limitation is that basu2015regularized assumes that the VAR model is the true DGM which is critical in their analysis. The VAR model assumption, though popular, can be restrictive. For instance, the VAR family is not closed under linear transformations: if is a VAR process then may not expressible as a finite lag VAR (lutkepohl2005new, ). In Section 4, we provide an example (Example 3) of VAR processes where omitting a single variable breaks down the VAR assumption.

Many authors have contributed to the high-dimensional time series literature. We include a representative sample here. On the applied side, chudik2011infinite ; chudik2013econometric ; chudik2014theory use high-dimensional time series for global macroeconomic modeling. Methodological advances on high-dimensional time series estimation abound in the last decade. Although Lasso retains a significant presence, alternatives to lasso have been explored including quantile based methods for heavy-tailed data (qiu2015robust, ), quasi-likelihood approaches (uematsu2015penalized, ), two-stage estimation techniques (davis2012sparse, ) and the Dantzig selector (han2013transition, ; han2015direct, ).

Various authors have investigated the theoretical aspects of the topic with their own sets of assumptions on the underlying DGMs. Some of the earlier work (song2011large , wu2015high and alquier2011sparsity ) gave theoretical lasso guarantees assuming that RE conditions hold. However, as basu2015regularized pointed out, it is non-trivial to actually establish RE conditions in the presence of dependence. Both han2013transition and han2015direct studied the stable Gaussian VAR models while this paper covers wider classes of processes as our examples demonstrate. fan2016penalized considered the case of multiple sequences of univariate -mixing heavy-tailed dependent data. Under a stringent condition on the auto-covariance structure (please refer to Appendix D in wong2017lasso for details), the paper established finite sample consistency in the real support for penalized least squares estimators. In addition, under mutual incoherence type assumption, it provided sign and consistency. An AR(1) example was given as an illustration. Both uematsu2015penalized and kock2015oracle establish oracle inequalities for lasso applied to time series prediction. uematsu2015penalized provided results not just for lasso but also for estimators using penalties such as the SCAD penalty. Also, instead of assuming Gaussian errors, it assumed only that fourth moments of the errors exist. kock2015oracle provided non-asymptotic lasso error and prediction error bounds for stable Gaussian VARs. Both sivakumar2015beyond and medeiros2016 considered subexponential designs. sivakumar2015beyond studied lasso on iid subexponential designs and provide finite sample bounds. medeiros2016 studied adaptive lasso for linear time series models and provided sign consistency results. wang2007regression provided theoretical guarantees for lasso in linear regression models with autoregressive errors. Other structured penalties beyond the penalty have also been considered (nicholson2014hierarchical, ; nicholson2015varx, ; guo2015high, ; ngueyep2014large, ). zhang2015gaussian , mcmurry2015high , wang2013sparse and chen2013covariance consider estimation of the covariance (or precision) matrix of high-dimensional time series. mcmurry2015high and nardi2011autoregressive both highlight that autoregressive (AR) estimation, even in univariate time series, leads to high-dimensional parameter estimation problems if the lag is allowed to be unbounded.

2 Preliminaries

Lasso Procedure for Dependent Data

We describe our lasso procedure for estimation in dependent data. Given a stationary stochastic process of pairs where , we are interested in predicting given . In particular, given a dependent sequence , one might want to forecast the present using the past . A linear predictor is a natural choice for that purpose. To put it in the regression setting, we identify and . The pairs defined as such are no longer iid. Assuming strict stationarity, the parameter matrix of interest is minimizer of the mean squared error loss

| (2.1) |

Note that is independent of owing to stationarity. Because of high dimensionality (), consistent estimation is impossible without regularization. We consider the lasso procedure. The -penalized least squares estimator is defined as

| (2.2) |

where

| X | (2.3) |

The following matrix of true residuals is not available to an estimator but will appear in our analysis:

| W | (2.4) |

Matrix and Vector Notation

For a symmetric matrix M, let and denote its maximum and minimum eigenvalues respectively. For any matrix let M, , , , and denote its spectral radius , operator norm , entrywise norm , and Frobenius norm respectively. For any vector , denotes its norm . Unless otherwise specified, we shall use to denote the norm. For any vector , we use and to denote and respectively. Similarly, for any matrix M, where is the vector obtained from M by concatenating the rows of . We say that matrix M (resp. vector ) is -sparse if (resp. ). We use and to denote the transposes of and M respectively. When we index a matrix, we adopt the following conventions. For any matrix , for , , we define , and where is the vector with all s except for a in the th coordinate. The set of integers is denoted by .

For a lag , we define the auto-covariance matrix w.r.t. as . Note that . Similarly, the auto-covariance matrix of lag w.r.t. is , and w.r.t. is . The cross-covariance matrix at lag is . Note the difference between and : the former is a matrix, the latter is a matrix. Thus, is a matrix consisting of four sub-matrices. Using Matlab-like notation, . As per our convention, at lag , we omit the lag argument . For example, denotes .

A Brief Introduction to the -Mixing Condition

There are various approaches to quantity and control dependence across observations in a stationary time series. Popular ones include physical and predictive dependence measures (wu2005nonlinear, ), spectral analysis (basu2015regularized, ; priestley1981spectral, ; stoica1997introduction, ) and mixing coefficients (bradley2005basic, ). We opt for the -mixing coefficients route in this paper because the -mixing coefficients of a process are preserved under measurable transformations (please see Fact 1 for details) and at the same time, many interesting processes such as Markov and hidden Markov processes satisfy a -mixing condition (vidyasagar2003learning, , Sec. 3.5).

Mixing conditions (bradley2005basic, ) are well established in the stochastic processes literature as a way to allow for dependence in extending results from the iid case. The general idea is to first define a measure of dependence between two random variables (that can vector-valued or even take values in a Banach space) with associated sigma algebras . In particular,

where the last supremum is over all pairs of partitions and of the sample space such that for all . Then for a stationary stochastic process , one defines the mixing coefficients, for ,

The -mixing condition has been of interest in statistical learning theory for obtaining finite sample generalization error bounds for empirical risk minimization (vidyasagar2003learning, , Sec. 3.4) and boosting (kulkarni2005convergence, ) for dependent samples. There is also work on estimating -mixing coefficients from data (mcdonald2011estimating, ). Before we continue, we note an elementary but useful fact about mixing conditions, viz. they persist under arbitrary measurable transformations of the original stochastic process.

Fact 1.

Consider any -mixing stationary process . Then, for any measurable function , the stationary sequence of the transformed observations is also -mixing in the same sense with its mixing coefficients bounded by those of the original sequence.

3 Main Results

We start with introducing two well-known sufficient conditions that enable us to provide non-asymptotic guarantees for lasso estimation and prediction errors – the restricted eigenvalue (RE) and the deviation bound (DB) conditions. The bulk of the technical work in this paper boils down to establishing, with high probability, that the RE and DB conditions hold under the subgaussian -mixing assumptions (Propositions 2 and 3). In the classical linear model setting (see, e.g., Chap. 2.3 in hayashi2000econometrics ) where sample size is larger than the dimensions (), the conditions for consistency of the ordinary least squares (OLS) estimator are as follows: (a) the empirical covariance matrix and invertible, i.e., , and (b) the regressors and the noise are asymptotically uncorrelated, i.e., .

In high-dimensional regimes, bickel2009simultaneous , loh2012high and negahban2012restricted have established similar consistency conditions for lasso. The first one is the restricted eigenvalue (RE) condition on (which is a special case, when the loss function is the squared loss, of the restricted strong convexity (RSC) condition). The second is the deviation bound (DB) condition on . The following lower RE and DB definitions are modified from those given by loh2012high .

Definition 1 (Lower Restricted Eigenvalue).

A symmetric matrix satisfies a lower restricted eigenvalue condition with curvature and tolerance if

Definition 2 (Deviation Bound).

We will show that, with high probability, the RE and DB conditions hold for dependent data that satisfy Asumptions 1–5 described below. We shall do that without assuming any parametric form of the data generating mechanism. Instead, we will assume a subgaussian tail condition on the random vectors and that they satisfy the geometrically -mixing condition.

3.1 Assumptions

Assumption 1 (Sparsity).

The matrix is -sparse, i.e. .

Assumption 2 (Stationarity).

The process is strictly stationary: i.e., ,

where “” denotes equality in distribution.

Assumption 3 (Centering).

We have, and .

The thin tail property of the Gaussian distribution is desirable from the theoretical perspective, so we would like to keep that but at the same time allow for more generality. The subgaussian distributions are a nice family characterized by having tail probabilities of the same as or lower order than the Gaussian. We now focus on subgaussian random vectors and present high probabilistic error bounds with all parameter dependences explicit.

Assumption 4 (Subgaussianity).

The subgaussian constants of and are bounded above by and respectively. (Please see Appendix A for a detailed introduction to subgaussian random vectors. )

Classically, mixing conditions were introduced to generalize classic limit theorems in probability beyond the case of iid random variables (rosenblatt1956central, ).

Assumption 5 (-Mixing).

The process is geometrically -mixing, i.e., there exists some constant such that

The -mixing condition allows us to apply the independent block technique developed by yu1994rates . For examples of large classes of Markov and hidden Markov processes that are geometrically -mixing, see Theorem 3.11 and Theorem 3.12 of vidyasagar2003learning . In the independent blocking technique, we construct a new set of independent blocks such that each block has the same distribution as that of the corresponding block from the original sequence. Results of yu1994rates provide upper bounds on the difference between probabilities of events defined using the independent blocks versus the same event defined using the original data. Classical probability theory tools for independent data can then be applied on the constructed independent blocks. In Appendix C, we apply the independent blocking technique to Bernstein’s inequality to get the following concentration inequality for -mixing random variables.

Lemma 1 (Concentration of -Mixing Subgaussian Random Variables).

Remark 1.

The three terms in the bound above all have interpretations: the first is a concentration term with a rate that depends on the “effective sample size” , the number of blocks; the second is a dependence penalty accounting for the fact that the blocks are not exactly independent; and the third is a remainder term coming from the fact that may not exactly divide . The key terms are the first two and exhibit a natural trade-off: increasing worsens the first term since decreases, but it improves the second term since there is less dependence at larger lags.

3.2 High Probability Guarantees for the Lower Restricted Eigenvalue and Deviation Bound Conditions

We show that both lower RE and DB conditions hold, with high probability, under our assumptions.

Proposition 2 (RE).

Proposition 3 (Deviation Bound).

Remark 2.

Since is a free parameter, we choose it to be arbitrarily close to zero so that scales at a rate arbitrarily close to . However, there is a price to pay for this: both the initial sample threshold and the success probability worsen as we make very small.

3.3 Estimation and Prediction Errors

The guarantees below follow easily from plugging the RE and DB constants from Propositions 2 and 3 into a “master theorem” (Theorem 5 in Appendix B). Similar results are well-known in the literature (e.g., see bickel2009simultaneous ; loh2012high ; negahban2012restricted ). The extra generality here, which is critical for the analysis in this paper, comes from allowing the response vector and regressors to potentially be in different dimensions and the object of estimation to be a matrix.

Corollary 4 (Lasso Guarantee under Subgaussian Tails and -Mixing).

Suppose Assumptions 1–5 hold. Let and be as defined in Propositions 2 and 3 and . Let be a free parameter. Then, for sample size

we have with probability at least

the lasso estimation and (in-sample) prediction error bounds

| (3.1) | |||

| (3.2) |

hold with

where

Remark 3.

The condition number of plays an important part in the literature of lasso error guarantees (loh2012high, , e.g.). Here, we see that the role of the condition number is replaced by that now serves as the “effective condition number.”

4 Examples

We explore applicability of our theory beyond just linear Gaussian processes using the examples below. In the following examples, we identify and for . For the specific parameter matrix in each Example below, we can verify that Assumptions 1–5 hold (see Appendix E) for details. Therefore, Propositions 2 and 3 and Corollary 4 follow. Hence we have all the high probabilistic guarantees for lasso on data generated from DGM potentially involving subgaussianity, model mis-specification, and/or nonlinearity.

Example 1 (Gaussian VAR).

Transition matrix estimation in sparse stable VAR models has been a popular topic in recent years (davis2015sparse, ; han2013transition, ; song2011large, ). The lasso estimator is a natural choice for the problem.

We state the following convenient fact because it allows us to study any finite order VAR model by considering its equivalent VAR() representation. See Appendix E.1 for details.

Fact 2.

Every VAR() process can be written in VAR() form (see e.g. (lutkepohl2005new, , Ch 2.1)).

Therefore, without loss of generality, we can consider VAR() model in the ensuing Examples.

Formally a first order Gaussian VAR() process is defined as follows. Consider a sequence of serially ordered random vectors , that admits the following auto-regressive representation:

| (4.1) |

where A is a non-stochastic coefficient matrix in and innovations are -dimensional random vectors from with and .

Assume that the VAR() process is stable; i.e. . Also, assume A is -sparse. In here, .

Example 2 (VAR with Subgaussian Innovations).

Consider a VAR() model defined as in Example 1 except that we replace the Gaussian white noise innovations with subgaussian ones and assume .

For example, take iid random vectors from the uniform distribution; i.e. . These will be independent centered isotropic subgaussian random vectors, giving us we a VAR() model with subgaussian innovations. If we take a sequence generated according to the model, each element will be a mean zero subgaussian random vector. Note that .

Example 3 (VAR with subgaussian Innovations and Omitted Variable).

We will study estimation of a VAR(1) process when there are endogenous variables omitted. This arises naturally when the underlying DGM is high-dimensional but not all variables are available (perhaps they are not observable or measurable) to the researcher to do estimation or prediction. This also happens when the researcher mis-specifies the scope of the model.

Notice that the system of the retained set of variables is no longer a finite order VAR (and thus non-Markovian). This example serves to illustrate that our theory is applicable to models beyond the finite order VAR setting.

Consider a VAR(1) process such that each vector in the sequence is generated by the recursion below:

where , , , and are partitions of the random vectors and into and variables. Also,

is the coefficient matrix of the VAR(1) process with -sparse, -sparse and . for are iid draws from a subgaussian distribution; in particular we consider the subgaussian distribution described in Example 2.

We are interested in the OLS -lag estimator of the system restricted to the set of variables in . Recall that

We show in the appendix that is sparse.

Example 4 (Multivariate ARCH).

We will explore the generality of our theory by considering a multivariate nonlinear time series model with subgaussian innovations. A popular nonlinear multivariate time series model in econometrics and finance is the vector autoregressive conditionally heteroscedastic (ARCH) model. We chose the following specific ARCH model for convenient validation of the geometric -mixing property; it may potentially be applicable to a larger class of multivariate ARCH models. Consider a sequence of random vector generated by the following recursion. For any constants , , , and A sparse with :

| (4.2) | ||||

where are iid random vectors from some subgaussian distribution and clips the argument to stay in the interval . We can take innovations to be iid random vectors from uniform distribution as described in Example 2. Consequently, each will be a mean zero subgaussian random vector. Note that , the transpose of the coefficient matrix A here.

5 Simulations

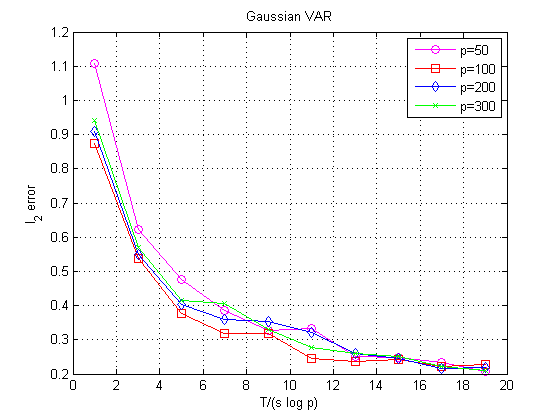

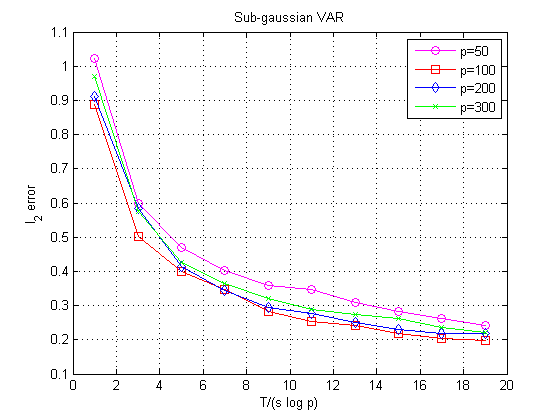

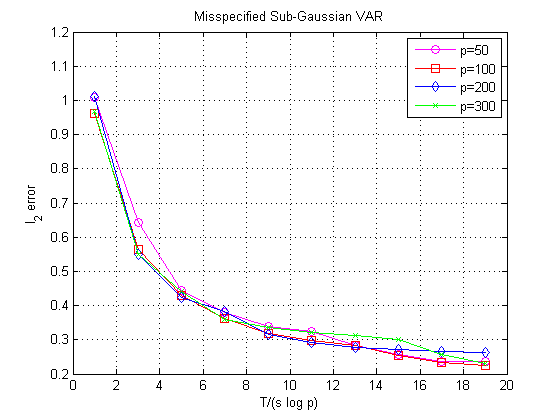

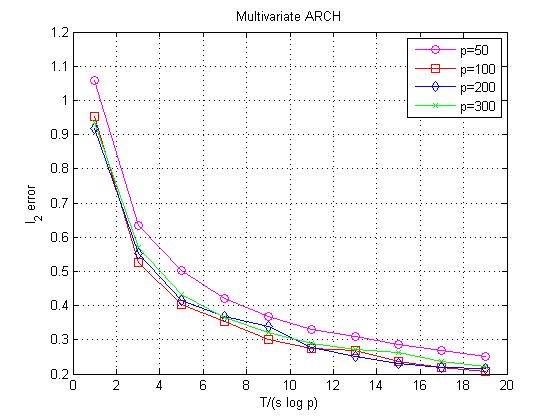

Corollary 4 in Section 3 makes a precise prediction for the parameter error . We report scaling simulations for Examples 1–4 to confirm the sharpness of the bounds.

Sparsity is always , noise covariance matrix , and the operator norm of the driving matrix set to . The problem dimensions are . Top left, top right, bottom left and bottom right sub-figures in Figure 1 correspond to simulations of Examples 1, 2, 3 and 4 respectively.

In all combinations of the four dimensions and Examples, the error decreases to zero as the sample size increases, showing consistency of the method. In each sub-figure, the parameter error curves align when plotted against a suitably rescaled sample size () for different values of dimension . We see the error scaling agrees nicely with theoretical guarantees provided by Corollary 4.

Appendix A Subgaussian Constants for Random Vectors

The subgaussian and subexponential constants have various equivalent definitions, we adopt the following from rudelson2013hanson .

Definition 3 (Subgaussian Norm and Random Variables/Vectors).

A random variable is called subgaussian with subgaussian constant if its subgaussian norm

satisfies .

A random vector is called subgaussian if all of its one-dimensional projections are subgaussian and we define

.

Definition 4 (Subexponential Norm and Random Variables/Vectors).

A random variable is called subexponential with subexponential constant if its subexponential norm

satisfies .

A random vector is called subexponential if all of its one-dimensional projections are subexponential and we define

Fact 3.

A random variable is subgaussian iff is subexponential with .

Appendix B Proof of Master Theorem

We present a master theorem that provides guarantees for the parameter estimation error and for the (in-sample) prediction error. The proof builds on existing result of the same kind (bickel2009simultaneous, ; loh2012high, ; negahban2012restricted, ) and we make no claims of originality for either the result or for the proof.

Theorem 5 (Estimation and Prediction Errors).

Proof of Theorem 5.

We wil break down the proof in steps.

Appendix C Proofs for Subgaussian Random Vectors under -Mixing

Proof of Lemma 1.

Following the description in yu1994rates , we divide the stationary sequence of real valued random variables into blocks of size with a remainder block of length . Let and be sets that denote the indices in the odd and even blocks respectively, and let to denote the indices in the remainder block. To be specific,

Let be a collection of the random vectors in the odd blocks. Similarly, is a collection of the random vectors in the even blocks, and a collection of the random vectors in the remainder block. Lastly,

Now, take a sequence of i.i.d. blocks such that each is independent of and each has the same distribution as the corresponding block from the original sequence . We construct the even and remainder blocks in a similar way and denote them and respectivey.

() denote the union of the odd(even) blocks.

For the odd blocks: ,

Where the first inequality follows from (yu1994rates, , Lemma 4.1) with . By Fact (3), the corresponding subexponential constant of each where is the subexponential norm because of fact 3. With this, the second inequality follows from the Bernstein’s inequality (Proposition (7)) with some constant .

Then

So,

Taking the union bound over the odd and even blocks,

For , it reduces to

For the remainder block, since has subexponential constant at most , we have

Together, by union bound

∎

Proof of Proposition 2.

Recall that the sequence form a -mixing and stationary sequence.

Now, fix a unit vector .

Define real valued random variables . Note that the mixing rate of is bounded by the same of by Fact 1. We suppress the subscript of the subgaussian constant here, and refer it as .

We can apply Lemma 1 on . Set . We have,

Using Lemma F.2 in basu2015regularized , we extend the inequality to hold for all vectors , the set of unit norm -sparse vectors. We have

The constant is defined as .

Recall , the above concentration can be equivalently expressed as

Finally, we will extend the concentration to all to establish the lower-RE result. By Lemma 12 of loh2012high , for parameter , w.p. at least

we have

This implies that

w.p. .

Now, choose set . Let’s choose that, for some , and . Then,

Where To ensure , we require

With these specifications, We have for probability at least

that

Now, choose since it optimizes the rate of decay in the tolerance parameter. Also, choose ; this ensures that .

In all, for w.p. at least

∎

Proof of Proposition 3.

Recall .

By lemma condition (3), we have

By first order optimality of the optimization problem in (2.1), we have

We know

Therefore,

This suggests proof strategy via controlling tail probability on each of the terms , and . Assuming the conditions in lemma 3, we can apply lemma 1 on each of them. We have to figure out their subgaussian constants.

Let’s define and . We have to figure out the constants and .

Now,

| by definition of subgaussian random vector | ||||

| by stationarity |

Therefore,

| (C.1) |

Take

| (C.3) |

For , set and . Applying lemma 1 three times with subgaussian constant , we have

By union bound,

To ensure proper decay in the probability, we require

With

where

∎

Lemma 6.

For any subgaussian random vector and non-stochastic matrix A. We have

Proof.

We have,

∎

Appendix D Bernstein’s Concentration Inequality

We state the Bernstein’s inequality (vershynin2010introduction, , Proposition 5.16) below for completeness.

Proposition 7 (Bernstein’s Inequality).

Let be independent centered subexponential random variables, and . Then for every and every , we have

where is an absolute constant.

Appendix E Verification of Assumptions for the Examples

E.1 VAR

Formally a finite order Gaussian VAR() process is defined as follows. Consider a sequence of serially ordered random vectors , that admits the following auto-regressive representation:

| (E.1) |

where each is a non-stochastic coefficient matrix in and innovations are -dimensional random vectors from . Assume and .

Note that every VAR(d) process has an equivalent VAR(1) representation (see e.g. (lutkepohl2005new, , Ch 2.1)) as

| (E.2) |

where

| (E.3) |

Because of this equivalence, justification of Assumption 5 will operate through this corresponding augmented VAR representation.

For both Gaussian and sub-Gaussian VARs, Assumption 3 is true since the sequences is centered. Second, . So Assumption 1 follows from construction.

For the remaining Assumptions, we will consider the Gaussian and sub-Gaussian cases separately.

Gaussian VAR

satisfies Assumption 4 by model assumption.

To show that is -mixing with geometrically decaying coefficients, we use the following facts together with the equivalence between and and Fact 1.

Since is stable, the spectral radius of , , hence Assumption 2 holds. Also the innovations has finite first absolute moment and positive support everywhere. Then, according to Theorem 4.4 in tjostheim1990non , is geometrically ergodic. Note here that Gaussianity is not required here. Hence, it also applies to innovations from mixture of Gaussians.

Next, we present a standard result (see e.g. (liebscher2005towards, , Proposition 2)).

Fact 4.

A stationary Markov chain is geometrically ergodic implies is absolutely regular(a.k.a. -mixing) with

So, Assumption 5 holds.

Sub-Gaussian VAR

When the innovations are random vectors from the uniform distribution, they are sub-Gaussian. That are sub-Gaussian follows from arguments as in Appendix E.3 with set to be the idenity operator in this case. So, Assumption 4 holds.

To show that satisfies Assumptions 2 and 5, we establish that is geometrically ergodic. To show the latter, we use Propositions 1 and 2 in liebscher2005towards together with the equivalence between and and Fact 1.

To apply Proposition 1 in liebscher2005towards , we check the three conditions one by one. Condition (i) is immediate with , and is the Lebesgue measure. For condition (ii), we set , to be the Lebesgue measure, and the minimum “distance” between the sets and . Because is bounded and Borel, is finite. Lastly, for condition (iii), we again let , to be the Lebesgue measure, and now the function and the set where . Then,

-

•

Recall from model assumption that ; hence,

-

•

For all ,

-

•

For all ,

Now, by Proposition 1 in liebscher2005towards , is geometrically ergodic; hence will be stationary. Once it reaches stationarity, by Proposition 2 in the same paper, the sequence will be -mixing with geometrically decaying mixing coefficients. Therefore, Assumptions 2 and 5 hold.

E.2 VAR with Misspecification

Assumptions: Assumption 3 is immediate from model definitions. By the same arguments as in Appendix E.1, are stationary and so is the sub-process ; Assumption 2 holds. Again, satisfy Assumption 5 according to Appendix E.1. By Fact 1, we have the same Assumptions hold for the respective sub-processes in both cases. Assumption 4 holds by the same reasoning as in Appendix E.1.

To show that , consider the following arguments. By Assumption 2, we have the auto-covariance matrix of the whole system as

Recall our definition from Eq. (2.1)

Taking derivatives and setting to zero, we obtain

| (E.4) |

Note that

by Assumptions 2 and the fact that the innovations are iid.

Naturally,

Remark 4.

Notice that is a column vector and suppose it is -sparse, and is -sparse, then is at most -sparse. So Assumption 1 can be built in by model construction.

Remark 5.

We gave an explicit model here where the left out variable was univariate. That was only for convenience. In fact, whenever the set of left-out variables affect only a small set of variables in the retained system , the matrix is guaranteed to be sparse. To see that, suppose and has at most non-zero rows (and let to be -sparse as always), then is at most -sparse.

Remark 6.

Any VAR() process has an equivalent VAR(1) representation (Lutkepohl 2005). Our results extend to any VAR() processes.

E.3 ARCH

Verifying the Assumptions.

To show that Assumption 5 holds for a process defined by Eq. (4.2) we leverage on Theorem 2 from liebscher2005towards . Note that the original ARCH model in liebscher2005towards assumes the innovations to have positive support everywhere. However, this is just a convenient assumption to establish the first two conditions in Proposition 1 (on which proof of Theorem 2 relies) from the same paper. Our example ARCH model with innovations from the uniform distribution also satisfies the first two conditions of Proposition 1 by the same arguments in the Sub-Gaussian paragraph of Appendix E.1.

Theorem 2 tells us that for our ARCH model, if it satisfies the following conditions, it is guaranteed to be absolutely regular with geometrically decaying -coefficients.

-

•

has positive density everywhere on and has identity covariance by construction.

-

•

because .

-

•

,

-

•

So, Assumption 5 is valid here. We check other assumptions next.

Mean is immediate, so we have Assumption 3. When the Markov chain did not start from a stationary distribution, geometric ergodicity implies that the sequence is approaching the stationary distribution exponentially fast. So, after a burning period, we will have Assumption 2 approximately valid here.

The sub-Gaussian constant of given is bounded as follows: for every ,

| by Lemma 6 | ||||

The second inequality follows since and a standard result that

Fact 5.

Let be a random vector with independent, mean zero, sub-Gaussian coordinates . Then is a sub-Gaussian random vector, and there exists a positive constant for which

The forth inequality follows since the sub-Gaussian norm of a bounded random variable is also bounded.

We will show below that . Hence, sparsity (Assumption 1) can be built in when we construct our model 4.2.

Since is invertible, we have .

Acknowledgments

We thank Sumanta Basu and George Michailidis for helpful discussions, and Roman Vershynin for pointers to the literature. We acknowledge the support of NSF via a regular (DMS-1612549) and a CAREER grant (IIS-1452099).

References

- [1] Alekh Agarwal, Sahand Negahban, and Martin J Wainwright. Fast global convergence of gradient methods for high-dimensional statistical recovery. The Annals of Statistics, 40(5):2452–2482, 2012.

- [2] Pierre Alquier, Paul Doukhan, et al. Sparsity considerations for dependent variables. Electronic journal of statistics, 5:750–774, 2011.

- [3] Sumanta Basu and George Michailidis. Regularized estimation in sparse high-dimensional time series models. The Annals of Statistics, 43(4):1535–1567, 2015.

- [4] Amir Beck and Marc Teboulle. A fast iterative shrinkage-thresholding algorithm for linear inverse problems. SIAM journal on imaging sciences, 2(1):183–202, 2009.

- [5] Peter J Bickel, Ya’acov Ritov, and Alexandre B Tsybakov. Simultaneous analysis of lasso and dantzig selector. The Annals of Statistics, pages 1705–1732, 2009.

- [6] Michael Binder, Cheng Hsiao, and M Hashem Pesaran. Estimation and inference in short panel vector autoregressions with unit roots and cointegration. Econometric Theory, 21(4):795–837, 2005.

- [7] Olivier Blanchard and Roberto Perotti. An empirical characterization of the dynamic effects of changes in government spending and taxes on output. the Quarterly Journal of economics, 117(4):1329–1368, 2002.

- [8] Richard C Bradley. Basic properties of strong mixing conditions. a survey and some open questions. Probability surveys, 2(2):107–144, 2005.

- [9] Peter Bühlmann and Sara Van De Geer. Statistics for high-dimensional data: methods, theory and applications. Springer Science & Business Media, 2011.

- [10] Bolong Cao and Yixiao Sun. Asymptotic distributions of impulse response functions in short panel vector autoregressions. Journal of Econometrics, 163(2):127–143, 2011.

- [11] Venkat Chandrasekaran, Benjamin Recht, Pablo A Parrilo, and Alan S Willsky. The convex geometry of linear inverse problems. Foundations of Computational mathematics, 12(6):805–849, 2012.

- [12] Xiaohui Chen, Mengyu Xu, and Wei Biao Wu. Covariance and precision matrix estimation for high-dimensional time series. The Annals of Statistics, 41(6):2994–3021, 2013.

- [13] Alexander Chudik and M Hashem Pesaran. Infinite-dimensional VARs and factor models. Journal of Econometrics, 163(1):4–22, 2011.

- [14] Alexander Chudik and M Hashem Pesaran. Econometric analysis of high dimensional VARs featuring a dominant unit. Econometric Reviews, 32(5-6):592–649, 2013.

- [15] Alexander Chudik and M Hashem Pesaran. Theory and practice of GVAR modelling. Journal of Economic Surveys, 2014.

- [16] Richard A Davis, Pengfei Zang, and Tian Zheng. Sparse vector autoregressive modeling. arXiv preprint arXiv:1207.0520, 2012.

- [17] Richard A Davis, Pengfei Zang, and Tian Zheng. Sparse vector autoregressive modeling. Journal of Computational and Graphical Statistics, (just-accepted):1–53, 2015.

- [18] David L Donoho, Arian Maleki, and Andrea Montanari. Message-passing algorithms for compressed sensing. Proceedings of the National Academy of Sciences, 106(45):18914–18919, 2009.

- [19] JianQing Fan, Lei Qi, and Xin Tong. Penalized least squares estimation with weakly dependent data. Science China Mathematics, 59(12):2335–2354, 2016.

- [20] Shaojun Guo, Yazhen Wang, and Qiwei Yao. High dimensional and banded vector autoregressions. arXiv preprint arXiv:1502.07831, 2015.

- [21] Fang Han and Han Liu. Transition matrix estimation in high dimensional time series. In Proceedings of the 30th International Conference on Machine Learning (ICML-13), pages 172–180, 2013.

- [22] Fang Han, Huanran Lu, and Han Liu. A direct estimation of high dimensional stationary vector autoregressions. Journal of Machine Learning Research, 16:3115–3150, 2015.

- [23] Trevor Hastie, Robert Tibshirani, and Martin Wainwright. Statistical learning with sparsity: the lasso and generalizations. CRC Press, 2015.

- [24] Fumio Hayashi. Econometrics. Princeton University Press, 2000.

- [25] Craig Hiemstra and Jonathan D Jones. Testing for linear and nonlinear granger causality in the stock price-volume relation. The Journal of Finance, 49(5):1639–1664, 1994.

- [26] Anders Bredahl Kock and Laurent Callot. Oracle inequalities for high dimensional vector autoregressions. Journal of Econometrics, 186(2):325–344, 2015.

- [27] Michael Krumin and Shy Shoham. Multivariate autoregressive modeling and granger causality analysis of multiple spike trains. Computational intelligence and neuroscience, 2010:10, 2010.

- [28] Sanjeev Kulkarni, Aurelie C Lozano, and Robert E Schapire. Convergence and consistency of regularized boosting algorithms with stationary -mixing observations. In Advances in neural information processing systems, pages 819–826, 2005.

- [29] Eckhard Liebscher. Towards a unified approach for proving geometric ergodicity and mixing properties of nonlinear autoregressive processes. Journal of Time Series Analysis, 26(5):669–689, 2005.

- [30] Po-Ling Loh and Martin J Wainwright. High-dimensional regression with noisy and missing data: Provable guarantees with nonconvexity. The Annals of Statistics, 40(3):1637–1664, 2012.

- [31] Helmut Lütkepohl. New introduction to multiple time series analysis. Springer Science & Business Media, 2005.

- [32] Daniel J Mcdonald, Cosma R Shalizi, and Mark J Schervish. Estimating beta-mixing coefficients. In International Conference on Artificial Intelligence and Statistics, pages 516–524, 2011.

- [33] Timothy L McMurry and Dimitris N Politis. High-dimensional autocovariance matrices and optimal linear prediction. Electronic Journal of Statistics, 9:753–788, 2015.

- [34] Marcelo C Medeiros and Eduardo F Mendes. -regularization of high-dimensional time-series models with non-gaussian and heteroskedastic errors. Journal of Econometrics, 191(1):255–271, 2016.

- [35] George Michailidis and Florence d’Alché Buc. Autoregressive models for gene regulatory network inference: Sparsity, stability and causality issues. Mathematical biosciences, 246(2):326–334, 2013.

- [36] Yuval Nardi and Alessandro Rinaldo. Autoregressive process modeling via the lasso procedure. Journal of Multivariate Analysis, 102(3):528–549, 2011.

- [37] Sahand Negahban and Martin J Wainwright. Estimation of (near) low-rank matrices with noise and high-dimensional scaling. The Annals of Statistics, pages 1069–1097, 2011.

- [38] Sahand Negahban and Martin J Wainwright. Restricted strong convexity and weighted matrix completion: Optimal bounds with noise. The Journal of Machine Learning Research, 13(1):1665–1697, 2012.

- [39] Sahand N Negahban, Pradeep Ravikumar, Martin J Wainwright, Bin Yu, et al. A unified framework for high-dimensional analysis of -estimators with decomposable regularizers. Statistical Science, 27(4):538–557, 2012.

- [40] Rodrigue Ngueyep and Nicoleta Serban. Large vector auto regression for multi-layer spatially correlated time series. Technometrics, 2014.

- [41] William Nicholson, David Matteson, and Jacob Bien. VARX-L: Structured regularization for large vector autoregressions with exogenous variables. arXiv preprint arXiv:1508.07497, 2015.

- [42] William B Nicholson, Jacob Bien, and David S Matteson. Hierarchical vector autoregression. arXiv preprint arXiv:1412.5250, 2014.

- [43] Maurice Bertram Priestley. Spectral analysis and time series. 1981.

- [44] Huitong Qiu, Sheng Xu, Fang Han, Han Liu, and Brian Caffo. Robust estimation of transition matrices in high dimensional heavy-tailed vector autoregressive processes. In Proceedings of the 32nd International Conference on Machine Learning (ICML-15), pages 1843–1851, 2015.

- [45] Murray Rosenblatt. A central limit theorem and a strong mixing condition. Proceedings of the National Academy of Sciences of the United States of America, 42(1):43, 1956.

- [46] Mark Rudelson and Roman Vershynin. Hanson-wright inequality and sub-gaussian concentration. Electronic Communications in Probability, 18(82):1–9, 2013.

- [47] Christopher A Sims. Macroeconomics and reality. Econometrica: Journal of the Econometric Society, pages 1–48, 1980.

- [48] Vidyashankar Sivakumar, Arindam Banerjee, and Pradeep K Ravikumar. Beyond sub-gaussian measurements: High-dimensional structured estimation with sub-exponential designs. In Advances in Neural Information Processing Systems, pages 2206–2214, 2015.

- [49] Song Song and Peter J Bickel. Large vector auto regressions. arXiv preprint arXiv:1106.3915, 2011.

- [50] Petre Stoica and Randolph L Moses. Introduction to spectral analysis, volume 1. Prentice hall Upper Saddle River, NJ, 1997.

- [51] Dag Tjøstheim. Non-linear time series and markov chains. Advances in Applied Probability, pages 587–611, 1990.

- [52] Yoshimasa Uematsu. Penalized likelihood estimation in high-dimensional time series models and uts application. arXiv preprint arXiv:1504.06706, 2015.

- [53] Roman Vershynin. Introduction to the non-asymptotic analysis of random matrices. arXiv preprint arXiv:1011.3027, 2010.

- [54] Mathukumalli Vidyasagar. Learning and generalisation: with applications to neural networks. Springer Science & Business Media, second edition, 2003.

- [55] Hansheng Wang, Guodong Li, and Chih-Ling Tsai. Regression coefficient and autoregressive order shrinkage and selection via the lasso. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 69(1):63–78, 2007.

- [56] Zhaoran Wang, Fang Han, and Han Liu. Sparse principal component analysis for high dimensional vector autoregressive models. arXiv preprint arXiv:1307.0164, 2013.

- [57] Kam Chung Wong and Ambuj Tewari. Lasso guarantees for -mixing heavy tailed time series. arXiv preprint arXiv:1708.01505, 2017.

- [58] W. B. Wu and Y. N. Wu. High-dimensional linear models with dependent observations, 2015. under review as per http://www.stat.ucla.edu/~ywu/papers.html. Accessed: October, 2015.

- [59] Wei Biao Wu. Nonlinear system theory: Another look at dependence. Proceedings of the National Academy of Sciences of the United States of America, 102(40):14150–14154, 2005.

- [60] Bin Yu. Rates of convergence for empirical processes of stationary mixing sequences. The Annals of Probability, pages 94–116, 1994.

- [61] Danna Zhang and Wei Biao Wu. Gaussian approximation for high dimensional time series. arXiv preprint arXiv:1508.07036, 2015.