Singular behavior of the leading Lyapunov exponent of a product of random matrices

Abstract.

We consider a certain infinite product of random matrices appearing in the solution of some and dimensional disordered models in statistical mechanics, which depends on a parameter and on a real random variable with distribution . For a large class of , we prove the prediction by B. Derrida and H. J. Hilhorst (J. Phys. A 16, 1641–2654 (1983)) that the Lyapunov exponent behaves like in the limit , where and are determined by . Derrida and Hilhorst performed a two-scale analysis of the integral equation for the invariant distribution of the Markov chain associated to the matrix product and obtained a probability measure that is expected to be close to the invariant one for small . We introduce suitable norms and exploit contractivity properties to show that such a probability measure is indeed close to the invariant one in a sense which implies a suitable control of the Lyapunov exponent.

Key words and phrases:

Product of Random Matrices, Lyapunov Exponent, Singular Behavior, Statistical Mechanics, Disordered Systems1. Introduction

1.1. Products of random matrices, Lyapunov exponents and statistical mechanics

Products of random matrices have appeared in the physics literature since Schmidt [22] introduced them to analyse a finite-difference equation with random coefficients proposed by Dyson [8] to study disordered harmonic chains. In the following years, probabilists and analysts began to investigate more general random matrix products, obtaining powerful results such as Furstenberg’s theorem (regarding the existence and implicit characterization of the leading Lyapunov exponent [9]) and Osoledets’ multiplicative Ergodic theorem [20], many of which also hold in the more general context of linear cocycles (see [26] for a recent review). The same difference equation studied by Dyson occurs as the Schrödinger equation for the Anderson tight-binding model in one dimension, and Furstenberg’s work played an important role in the first rigorous proofs of localization in this model (e.g. [14, 19]); random matrix product theory provides a unified framework for these otherwise disparate treatments [2]. Random-matrix-product studies of the one-dimensional Schrödinger equation have seen continued use in recent years to obtain further results about localization [3, 4].

The present work considers random matrices of the form

| (1.1) |

where is a constant and a sequence of positive, independent random variables with identical distribution . We will write for a random variable with distribution . This product of random variables, and the associated Lyapunov exponent(s), appear in various statistical mechanics models. For example, up to an unimportant factor, is the transfer matrix of the Ising model with , . Here randomness in corresponds to a random magnetic field and the free energy density (in the thermodynamic limit) is the leading Lyapunov exponent [5, Chapter 4] defined by

| (1.2) |

where denotes an operator norm (the limit is independent of the norm chosen); our results apply to part of the frustrated regime, where the magnetic field can have either sign with nonzero probability. Moreover, the free energy of the McCoy-Wu model in the thermodynamic limit can be expressed as an integral of the free energy of this model with respect to a parameter – which maps to in our notation – and the singular behavior comes from the values of (i.e. ) close to zero [23]. A similar matrix product also appears in the original treatment of the McCoy-Wu model [16].

1.2. Working definitions and main result

The classical theory of products of random matrices provides a technique for calculating as an ergodic average [2, 10]. Since ,

| (1.3) |

is a an element of , and assuming that and that is absolutely continuous with bounded support, it is easy to confirm that it satisfies the assumptions of [2, Chapter II, Prop. 4.3 and Th. 4.1], which shows that the Markov process on defined by

| (1.4) |

has a unique (and therefore ergodic) invariant probability measure . As already remarked for example in [7, 16], special features of the specific random matrices in question allow us to simplify the expression for . Firstly, since all the matrix elements are positive and (for fixed and , also assuming the support of is bounded away from 0) bounded from above and below, the limit is unchanged if we replace the vector norm in the last line of (1.2) with the scalar product with a fixed matrix element [10], i.e.

| (1.5) |

and using the pointwise ergodic theorem we can rewrite this

| (1.6) |

where and is an arbitrarily chosen vector in from the equivalence class .

Secondly, since the elements of the first row of are deterministic, the first component of is a deterministic function of , and the in the last line above is trivial. Parameterizing by with the choice , for the under consideration we have explicitly

| (1.7) |

where is obtained from by a change of variables; a simple computation shows that the Markov process defined by (1.4) corresponds to the one defined by the iteration

| (1.8) |

is then the unique stationary measury of this process.

All we have outlined up to now depends heavily on . The case of can be dealt with just observing that is conjugate to under the action of the diagonal matrix with eigenvalues and , and therefore . The case is however different: the invariant probability is not unique. In fact, all the invariant probabilities can be written as convex combination of the Dirac deltas at and , as can be seen by elementary arguments, and it is straightforward to see that .

Another fact that provides important context for our result is that, by applying the general result in [21], we see that is real analytic (see also [12, 15] that show behavior and Hölder continuity). The singular character of the matrices for is, as we just pointed out, apparent, but sharp results on the behavior of for approaching zero are lacking in the mathematical literature. However Derrida and Hilhorst [7] claim that when and

| (1.9) |

where is a positive constant and is the unique positive real solution of

| (1.10) |

Existence and uniqueness of follow from the convexity of the function , which takes value one with derivative at and value at .

The main result of the present work is a proof of (1.9), in the following form:

Theorem 1.1.

Let and be as defined above, with satisfying

-

(1)

and ;

-

(2)

There exist and with such that , and there is no smaller closed interval so that this is true;

-

(3)

The distribution of is absolutely continuous with respect to the Lebesgue measure, and its density is a continuously differentiable function.

Then there exist and such that

| (1.11) |

for and the positive real solution of (1.10).

Note that assumption (1) implies that . As we shall see, can be expressed explicitly given some information about the complex roots of (1.10), and our expression for is in agreement with [7].

The difficulty in proving Theorem 1.1 comes of course from the implicit characterization of . Identifying is identifying the invariant measure of a Markov chain which does not have any special properties which would allow an explicit expression. What has been exploited in [7] for (1.9) is, in a sense, the solvable character of the model for , but this limit is singular and taking advantage of it is by no means trivial, as we shall now explain.

1.3. The Derrida-Hilhorst approach

Let us review now the main argument of [7]. In view of (1.7), we look at the evolution of under the random iteration (1.8). Recalling that is supported on , we see that the mapping (1.8) takes into , and into , and therefore

| (1.12) |

Incidentally, it is straightforward to see also that has a density (e.g. by the argument used in Proposition 3.1 below); we will always denote the density of a measure with the same symbol, i.e. .

The Derrida-Hilhorst approach is based on a two regime argument:

-

I.

In the limit , the random recursion (1.8) takes the form

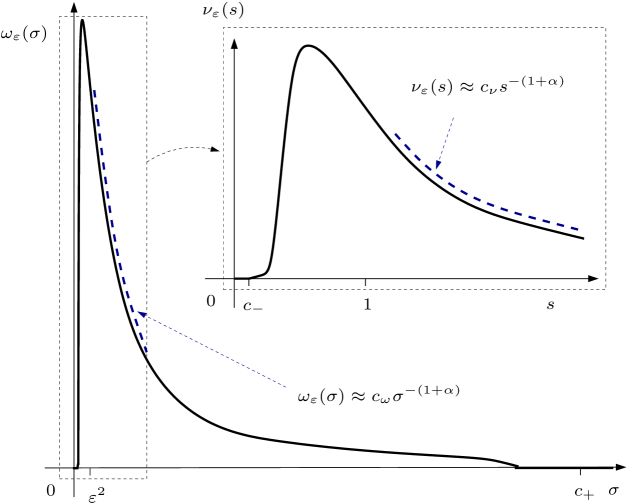

(1.13) which defines a Markov chain whose unique invariant probability is concentrated at zero, since which, for , converges almost surely to . However this chain has other invariant measures which cannot be normalized. If instead of considering the stationary probability measures we consider the stationary measures with the normalization for some suitable fixed , these should have a nontrivial limit given by one of the non-probability stationary measures of the limiting process (1.13), which we denote by . That is, for fixed and small, should be close to , for some positive , and because the limit for of concentrates in zero (see Figure 1 and (1.17)-(1.18)). For , the recursion (1.8) formally converges to the linear map , and the asymptotic behavior of should match that of a stationary measure of this map.

-

II.

Derrida and Hilhorst then analyse by blowing up the scale by . Namely, they consider

(1.14) with stationary probability denoted by , which, by (1.12), is supported in . By taking the limit we get to , which is linear but not straightforward to analyse. The claim for this chain is that it does have a unique invariant probability , supported on , whose tail behavior ( large) can be understood by studying the simpler map .

Therefore both the behavior of for small and the behavior for large are expected to be captured by the invariant measures of the random map on given by multiplication by . These measures have densities that satisfy and a simple computation shows that they can be written as

| (1.15) |

and where and are such that . Derrida and Hilhorst set forth arguments suggesting that the asymptotic behaviors we are after are given by the case that contains only , unique positive solution of , so

| (1.16) |

where and are positive constants: is fixed by the requirement that is a probability, is fixed by the normalization of the . Now the claim is that

| (1.17) |

where the symbol stands for approximately equal and can be evaluated by noting that the two terms should be essentially the same near , which using (1.16) gives

| (1.18) |

Now we can go back to (1.7), which can be computed using (1.17): for small,

| (1.19) |

1.4. Strategy of the proof and structure of the paper

The strategy for our proof is very much inspired by [7]. In short: we will construct a family of probability measures by pasting together and (essentially, the right-hand side of (1.17)) and use this to obtain an estimate of the Lyapunov exponent which can be shown to be correct to within a remainder term which is of the order indicated in Theorem 1.1 as .

But this approach faces two main difficulties: the rigorous construction and analysis of and to get to a definition of and (worse!) the fact in any case is not the invariant probability. Let us elaborate on this:

-

(1)

To define the right-hand side of (1.17) one needs to construct and control and . This work is in part already done for [6], but it is lacking for . Nevertheless, the road is paved for this analysis – notably, we are going to use Mellin transform techniques similar to those of [6] – and the difficulty that one needs to face are of technical nature.

-

(2)

More substantially, is not the invariant probability: we certainly expect it to be close to it, but in which sense and for what reasons? This step will be performed by introducing a family of norms that allows us to state in a precise and quantitative fashion that is one step approximately invariant. To use this to obtain meaningful estimates, we will show these norms are contracted by the action of the Markov Kernel; this provides an explicit estimate on the distance between and the invariant probability and, more important for us, the control is fine enough to pass to the functional of the invariant we are after: the Lyapunov exponent .

Now we are going to go more deeply into the strategy and, in particular, we explain the tools and the fundamental ideas to deal with item (2) of the list. For this we find more practical to work in the scale of regime II, even if this is to a large extent arbitrary. We introduce the map defined by

| (1.20) |

for all measurable bounded where

| (1.21) |

One readily checks that is the one step transition map for the law of the chain defined in (1.14), and hence .

Later on we will need the analog of , but in regime I. So we introduce : given a (finite) measure on we write for the (dual) action of on , i.e. for every Borel subset of . Letting

| (1.22) |

we have

| (1.23) |

for all measurable bounded and this is of course an alternative way to define .

We also introduce the family of functionals on signed measures

| (1.25) |

where we have used the standard notation for the cumulative (tail) distribution and we take the occasion to introduce also the companion quantity :

| (1.26) |

where, in general, is again a signed measure on . Let us underline that, as is customary, by signed measure we mean a signed measure of finite total variation, that is the difference of two finite non negative measures.

We have the following:

Lemma 1.2.

For every , and all probability measures and , supported in , with and finite, we have

| (1.27) |

Moreover if there exists independent of such that for every with

| (1.28) |

Lemma 1.2 will be proven in Section 2 below. We draw the attention of the reader on the fact that the important estimate (1.28) is a contractivity property of with respect to for . In fact

| (1.29) |

from which it is apparent that (1.28) follows once we have the claimed contractive property of .

It should also be quite clear at this stage that the key is to find a test measure that makes suitably small, so we can apply (1.28) and then (1.27), with and . The test measure of course corresponds to presented informally in Section 1.3, although we will need to make a more precise definition, and we will find it convenient to do so in terms of distribution functions rather than densities since these appear more naturally in our arguments. In any case, building requires building first and and establishing properties of these two measures. This is done in Section 3 and Section 4: we postpone the overview of these two sections and complete the argument that we are outlining. In Section 5 we show in a rather straightforward way that

| (1.30) |

and in Section 5.1 we prove, on the basis of a much less straightforward computation, that

| (1.31) |

for all and for any chosen so that , cf. (1.10), is solved in the strip only by (as we shall see, the hypothesis that has a density largely suffices for the existence of such a ). Hence by using the two inequalities in Lemma 1.2 we get to

| (1.32) |

and then choosing so that

| (1.33) |

we obtain Theorem 1.1 with . This therefore concludes the argument.

Let us spend a few words on the content of Section 3 and Section 4: in Section 3 we show the existence of the fixed points and as weak limits: is a probability, but is instead an infinite measure which inherits the normalization for an appropriately chosen . As we have already pointed out in Section 1.3, the characterization of (existence, uniqueness and asymptotic properties of ) is well known [13], but we provide a (simple) proof for completeness and to introduce the methods used to show the existence of . In Section 4 we characterize the behaviour of for large and for small, including some control on the subdominant terms (thereby improving on the result of [13], which only applies to and only gives the leading order behavior): an explicit control of the type (for some ) on the ratio of the remainder to the leading term is crucial for our approach, as is clear from (1.29)-(1.32). The proof is based on the characterization of the domain of analyticity of the Mellin transforms of and . As shown in [6], the poles of the Mellin transform of are either roots of (1.10) or at integer translates of those roots (the latter are not important for our result); the relevant argument is summarized in Section 4.1 for completeness. We are not able to control the behavior of the Mellin transform well enough to use it to directly obtain an asymptotic expression for with control on the remainder, but we are instead able to do this (in Section 4.2) at the level of the primitive of and then then recover the desired result on by reinjecting the estimate into the fixed point equation satisfied by . We will also verify that there is a positive such that (1.10) has no other roots with , so that the subleading terms in the expansion are in fact smaller then the leading term by a factor . In Section 4.3 we use the same techniques as in Sections 4.1 and 4.2 to obtain similar results for the behavior of near .

1.5. Perspectives

Before embarking on the proof, we shall make a few remarks about the assumptions of Theorem 1.1 and perspectives for generalizations.

-

•

When (1.10) has complex roots with (not covered by the present result: as shown in Section 4, assumptions (2) and (3) of Theorem 1.1 ensure that complex roots have real part larger than ), the behavior in the intermediate regime can be given by a linear combination with the associated stationary measures, without violating the monotonicity of . In this situation the leading Lyapunov exponent may instead behave like

(1.34) where is a nonconstant periodic function, which has been obtained by an exact calculation for a specific choice of in [7].

-

•

It is probably natural to expect that Theorem 1.1 holds without conditions (2) and (3), assuming instead that there is a such that (1.10) has no complex solutions with (rather than deriving this using condition (3)), and that for some . Generalizing our approach in this fashion would at least complicate many of the estimates used and require, in particular, a new approach to the results in Section 4 on asymptotic behavior of and would be needed. If this could be done, the same methods might also be used to show that the log-periodic behavior in (1.34) holds for other distributions besides the special case where it has been obtained so far [6, 7]. All of this however is not straightforward.

-

•

The cases excluded by assumption (1) are discussed in [7]: by replacing with , as a corollary of Theorem 1.1 we obtain a similar result for distributions with and . The case remains of considerable interest, since it corresponds to the critical point of the statistical mechanical models discussed above, and obtaining more control over the behavior of as this condition is approached (along the lines of the discussion in [23]) appears to be worthwhile. The case where , on the other hand, should merely exhibit a weakening of the singularity at .

-

•

Finally, although we have focused on a concrete example of physical relevance, the method used here has the potential to generalize to matrices of other forms, most immediately other matrices whose off-diagonal entries are .

2. Estimating the Lyapunov exponent with almost-stationary points of

In this section we will prove Lemma 1.2. The assertions in (1.27) and (1.28) are separate. For brevity, we will take absolutely continuous to mean absolutely continuous with respect to the Lebesgue measure on . Recall that we denote absolutely continuous measures and their densities with the same symbol.

Proof of (1.27).

For any signed measure such that is bounded and , we can integrate (1.24) by parts to obtain

| (2.1) |

This applies to , giving

| (2.2) |

Noting that

| (2.3) |

for all and , this implies

| (2.4) |

that is, (1.27).

∎

We now move to (1.28). The bulk of the proof is in the following lemma.

Lemma 2.1.

For any probability measures supported on such that both and are finite and any ,

| (2.5) |

Proof.

Choosing , (1.20) becomes

| (2.6) |

Letting , we have . We can use this and the fact that is absolutely continuous to integrate by parts, obtaining

| (2.7) |

so that

| (2.8) |

Noting that

| (2.9) |

and

| (2.10) |

for and , we have

| (2.11) |

Since

| (2.12) |

the conclusion follows immediately. ∎

3. Existence of the limiting fixed points and

As alluded to in Section 1, the definitions of the maps and are perfectly valid for , and their fixed points in this limiting case play an important role in our proof. However, in this case the relationship of these operators to the random matrix product becomes singular, and we can no longer use the same techniques to establish the existence and uniqueness of these fixed points.

In this section, we use compactness and continuity arguments to establish these results. As already pointed out in the introduction, has already been built and (partly) studied elsewhere. Our indirect approach to , i.e. via , may appear a bit convoluted since can be approached directly as the invariant probability of a Markov chain. We draw however the attention of the reader on the fact that standard approaches, like Foster-Lyapunov criteria (see e.g. [17]), are rather involved – above all in the case of a non-countable state space – and yield a lot of information that we do not need. That is, following [17], we can find a Lyapunov function starting from the monotonicity properties of , under the action of the Markov kernel, as we do below for ; but then the completion of the proof requires verifying a “petite sets condition” (which is rather straightforward if one assumes that for every small , but in general becomes rather laborious) and the final result includes uniqueness and (time!) mixing properties. The approach in [11], on the other hand, cannot in general be directly applied to our Markov kernel: some iterated version of the kernel should be used. Once again the method also yields mixing. Our approach is not constructive and a priori it does not yield even uniqueness (for uniqueness is easily recovered, but uniqueness in reality is not even required for the rest of our proof to go thorough), but it is very concise, self-contained and it shoots for the information we really need. More importantly, a similar method also applies to the treatment of , which is not a probability measure, and which is therefore not covered by the more usual techniques.

Here and in the rest of this section all measures are Borel measures supported on .

Proposition 3.1.

There is a probability measure such that , and is absolutely continuous.

Proof.

Recall (1.12). We apply (1.20) to to obtain

| (3.1) |

Noting that for and , we see that

| (3.2) |

which, for , gives for all . Then by Markov’s Inequality, we also have , which implies that the are a tight family. As a result, Prohorov’s theorem implies that there is some sequence such that converges weakly. Calling the limit , we see that is a probability measure. For readability, we will denote , , in the following.

We now need to confirm that . We will do so by showing that weakly. We do this in two parts, by showing that converges weakly to and that tends to zero for every , uniformly in the choice of the probability measure .

Using (A.4) we write

| (3.3) |

The integrand on the right hand side is bounded above by one and goes to zero (Lebesgue-)almost surely, hence also almost surely. Then by dominated convergence the right hand side goes to 0 for all , and indeed weakly.

Then recalling (2.6), for any probability measure we have

| (3.4) |

where we recall that is the maximum of the density of and we have used the explicit definition (1.21) of to obtain

| (3.5) |

Since this bound is uniform in , it also implies that weakly. Together with , this implies that , and since we see that .

The situation will be similar for , once we have fixed the normalization to obtain a nontrivial limit. As a preliminary,

Lemma 3.2.

For any and , .

Proof.

By (A.4)

| (3.8) |

Set . By (1.12) we know that , but one can see also that for some . Observe in fact that (3.8) implies that

| (3.9) |

but for in the range of integration. But since we know that for every we obtain that is zero if , that is if .

We now claim that

| (3.10) |

In fact for we have (we can choose for some ), which, by (3.8), implies that for almost every in the support of , that is for almost every . But since is non increasing, we have that for every . This holds for every , so we obtain that for every , that is .

On the other hand, if then , which requires for some , which in turn implies that we have , because is non increasing and is increasing. So for every we have , that is . Therefore (3.10) is established.

We then fix a

| (3.12) |

and define by choosing the normalization

| (3.13) |

so that for all .

We now consider the space of positive -finite measures supported on equipped with the weak topology with respect to the bounded continuous functions whose support is bounded away from , that is the functions in that vanish in a neighborhood of zero. We do so because, while as we will see the limit point has total mass because of a singular behavior at zero.

We have the following crucial estimate:

Lemma 3.3.

There exist , and a decreasing sequence of positive numbers, with , defined in (3.12), such that for all and all .

Proof.

To begin with, note that for any and any ,

| (3.14) |

where we have first used that both since and are non increasing, so the composition of the two is non decreasing, and then that (and, again, the monotonicity of ).

We now define a sequence by setting and, for , for a chosen in : note that by (3.12). Note also that the map has and as fixed points: they are both hyperbolic, is attractive while is repulsive. By (3.12) we have , hence decreases to zero exponentially fast: , . Moreover by (3.14) (with and ) we have for

| (3.15) |

so that by observing that , by setting and recalling yields

| (3.16) |

and the proof is complete. ∎

Here is the main result about :

Proposition 3.4.

The family is compact and every limit point satisfies , the support of is in and . Moreover there exists such that for every limit point we have

| (3.17) |

Proof.

The compactness of can be obtained by the Helly-Bray Lemma as follows: Consider in fact a decreasing sequence of numbers in that tends to . For every Borel subset of we set

| (3.18) |

with and by Lemma 3.3. Therefore is a family of sub-probabilities; hence it is relatively compact by the Helly-Bray Lemma, so also is relatively compact and of course is just . Via a diagonal procedure we can therefore extract from any sequence tending to zero a subsequence such that for every bounded continuous whose support is bounded away from .

The proposed properties of can now be confirmed directly, notably follows by the same argument used in Proposition 3.1 with the obvious changes, in particular noting that

| (3.19) |

and is easily found by using Lemma 3.3. Note in fact that Lemma 3.3 implies the practical formulation

| (3.20) |

and we see that any will do: explicit values of the positive constant and are given in the proof of Lemma 3.3. ∎

Finally, we note that

Lemma 3.5.

defined in Proposition 3.4 is absolutely continuous.

Proof.

From (1.23), we obtain

| (3.21) |

and, setting , , this becomes

| (3.22) |

Noting that

| (3.23) |

we see that is differentiable on with the bound

| (3.24) |

∎

4. Asymptotic behaviour of and

This section culminates in Lemmas 4.5 and 4.10, which will allow us to control the asymptotics of a number of integrals containing and , which appear in Section 5 below. We will do this by using Mellin transform techniques (see [1] for a review), which were applied to in [6]; the calculation is reproduced in Section 4.1.

Generically, the poles of the Mellin transform of a function correspond to the powers appearing in its asymptotic expansion at or ; however, except when it is known a priori that such an expansion exists, proving this requires some control on the behaviour of the Mellin transform for large imaginary argument. No suitable control is available here, but we shall see that the expansion holds in a distributional sense which will be adequate for our purposes, as proven in Section 4.2.

Finally, in Section 4.3, we show that the techniques of the previous two sections can be adapted with minor changes to obtain similar results for .

4.1. Mellin analysis of

Let

| (4.1) |

As noted in Section 1.4, we need to be such that , , and for all complex with other than . Let us confirm that there is actually a positive number satisfying these conditions. As a preliminary, we will need the following version of the Riemann-Lebesgue lemma:

Lemma 4.1.

Let be a continuously differentiable function with support , let be a compact interval, and let be a sequence of complex numbers such that and . Then

| (4.2) |

Proof.

Integrating by parts,

| (4.3) |

and the last integral is bounded uniformly given . ∎

Lemma 4.2.

There is a such that

| (4.4) |

Proof.

For any , let . cannot have any finite accumulation points, since is entire and not constant, so if is infinite it must also be unbounded. This would then imply the existence of a sequence such that , , and , which is in contradiction with Lemma 4.1.

We therefore know that is finite for any , and since for any we conclude that , and the result holds for any smaller than this quantity. ∎

Define a measure by

| (4.5) |

and let

| (4.6) |

is, up to a shift of the coordinate which we find convenient, the Mellin transform of . Among the calculations in [6], we find the following:

Lemma 4.3.

is analytic on the the set of complex numbers with , except for , which is a simple pole.

Proof.

Since is a probability measure whose support is contained in , it is clear that

| (4.7) |

for all complex with ; then on this region is given by a uniformly absolutely convergent integral of an analytic function and is therefore itself analytic. Similarly, recalling

| (4.8) |

we see that is an entire function (using the fact that the support of is bounded) with .

From the definition of as a translation of , we see that (1.20) implies

| (4.9) |

for all integrable (note that this is the stationarity condition of the iteration , cf. (1.14)).

Letting we have

| (4.10) |

The right hand side of (4.10) can be rewritten using the Mellin-Barnes integral

| (4.11) |

valid for , giving us

| (4.12) |

where we have used the exponential decay of the Gamma function in the imaginary direction to change the order of integration. This decay is also more than enough to allow us to move the contour of integration. For , the only poles of the integrand are those of , i.e. it has simple poles at . The residue of at is 1, so we have

| (4.13) |

for , which we further rewrite as

| (4.14) |

As a function of , the integral on the right hand side can be analytically continued into the right half-plane, so long as we maintain the condition and which prevents the contour of integration from encountering the poles of the Gamma functions. The right hand will have singularities only at the zeros of , i.e. the solutions of (1.10). We have already seen that is analytic for (indeed the apparent singularity in (4.14) at is removable, since also has a simple pole there). Since 0 and are the only such zeros with , all that remains is to prove that is not removable (it is obvious from (4.14) that it is then a simple pole).

Suppose that can be analytically continued at . Then the Taylor series of is absolutely convergent at some real with , giving

| (4.15) |

where the fact that all terms are positive on the support of has allowed us to exchange the sum and the integral. Then is given by a well-defined integral, and we can apply (4.10) to obtain

| (4.16) |

which is impossible if , since for . Since manifestly positive, we have obtained a contradiction. ∎

4.2. Asymptotics of

Returning to the definition of , (4.6), we can integrate by parts to obtain

| (4.17) |

for . Noting furthermore that we have

| (4.18) |

so that is the Mellin transform of with fundamental strip containing . We can use the inverse Mellin formula to convert this into a formula for , noting that by [25, Theorem 28] this formula is valid since is a continuous function (by Proposition 3.1) with bounded local variation (being bounded and monotone). This gives

| (4.19) |

for all and .

To get asymptotics from this expression we will need to displace the contour of integration further to the right, which requires some control on the growth of . We can obtain this from (4.14) as follows:

Lemma 4.4.

For large,

| (4.20) |

uniformly for for any .

Proof.

Fix some so that . Then recalling (see (4.7)), (4.14) yields

| (4.21) |

Lemma 4.1 shows that as , and examining the proof we see that the convergence is in fact uniform, so the first ratio on the right hand side is uniformly .

Using Stirling’s series and then the expansion for , we have

| (4.22) |

where the first expression holds for large uniformly in [24] and the second holds uniformly over compact sets. Thus for large,

| (4.23) |

uniformly for . Plugging this into (4.21) and estimating using (4.22), we obtain the desired result. ∎

Along with Lemma 4.3, this allows us to displace the contour in (4.19) to obtain

| (4.24) |

for all and any where denotes the residue of at and for some . If the integral on the right hand side were absolutely convergent, it would be . Unfortunately this is not the case; however all is not lost.

Denoting the value of this integral by and noting that it is independent of within the specified interval, for any we can choose and obtain

| (4.25) |

noting that the integrals are uniformly convergent and recognizing the resulting expression as an integral around a closed contour. This establishes that the Mellin transorm of on the strip containing is , and [18, Theorem 11.10.1] gives an expression for the unique distribution with that property:

| (4.26) |

The bounds on the growth of form Lemma 4.4 are sufficient to take one of the derivatives inside the integral, giving where

| (4.27) |

and Lemma 4.4 suffices for this integral to be absolutely convergent. As a result there is a constant such that

| (4.28) |

for all .

Noting that the definition of is such that , can use this to obtain:

Lemma 4.5.

There is a function and a constant such that

| (4.29) |

where

| (4.30) |

for .

Proof.

Taking (4.29) as a definition of with , then we obtain Equation (4.29) with . Then recalling that and writing out the action of as in Equation (A.6), we obtain

| (4.31) |

where we have used and cancelled a factor of . Using the generalized binomial theorem,

| (4.32) |

where the series on the right-hand side is absolutely convergent for ; then using the fact that is a probability measure with support and ,

| (4.33) |

where the sum is absolutely convergent for .

As for the other term in Equation (4.31), we can make the change of variables , use the fact that has a density to integrate by parts, and estimate using Equation (4.28) to obtain

| (4.34) |

Substituting this and Equation (4.33) into Equation (4.31), we obtain Equation (4.30).

∎

4.3. Asymptotics of

Defining a measure by applying the change of variables to , or in other words , then from the corresponding properties of it is clear that is absolutely continuous and supported within .

Lemma 4.6.

There is a such that is analytic for , and has an analytic continuation for apart from the points where with .

Proof.

The control on the growth of at the origin demonstrated in Theorem 3.4 there is some such that for all with the integral in the definition (4.35) of is absolutely convergent, and therefore defines an analytic function of .

Equation (A.1) with implies that satisfies

| (4.36) |

Then using the identity

| (4.37) |

(obtained from the formula for the Mellin transform of the Beta function, and valid for ), (4.36) can be rewritten

| (4.38) |

Displacing the contour of integration to the right across the pole of at and rearranging, we obtain the counterpart of (4.14),

| (4.39) |

for . The integral on the right-hand side can be analytically continued in so long as the contour of integration is displaced to maintain the condition and , allowing the whole expression to be analytically continued as well, apart from the zeros of . Note that although , the associated pole is removable, thanks to the factor of . ∎

The fact that we have little control over the value of will make using this result inconvenient when we attempt to repeat the analysis of Section 4.2, but we can refine the result as follows:

Lemma 4.7.

The integral

| (4.40) |

is absolutely convergent whenever .

Proof.

Let

| (4.41) |

Suppose . Then from Lemma 4.6, is the only pole of on the positive real axis, so is analytic at and there is a such that the Taylor series of at converges on an open disk containing . The Taylor series of at is

| (4.42) |

Since on the support of , we can exchange the sum and integral whenever the Taylor series is absolutely convergent. In particular, there is some for which this is true, and we have

| (4.43) |

contradicting the definition of .

This proves convergence on the real line; to extend to complex numbers, we simply note that

| (4.44) |

∎

We can confirm that actually is a pole of in the same way as we did for in the previous section, using (4.36) to obtain

| (4.45) |

so that since for the integral must diverge there.

The relationship of to is slightly simpler than what we saw in the previous sections: for we can integrate (4.35) by parts to obtain

| (4.46) |

Repeating the proof of Lemma 4.7 we see that the integral on the right hand side is absolutely convergent for all and this expression holds everywhere on that half-plane by analytic continuation.

Remark 4.8.

In particular, since ,

| (4.47) |

and since is a nonnegative, nonincreasing function this implies (and therefore also ) for .

Noting that is continuous and monotone, we can apply the inverse Mellin formula to obtain

| (4.48) |

for all where is continuous and all .

In order to displace the contour of integration in (4.48) as we did with (4.19), we again need a little control over the growth of for large imaginary arguments. This can be obtained in nearly the same way as was done for in Lemma 4.4:

Lemma 4.9.

For large with fixed,

| (4.49) |

Proof.

Then we can displace the contour in (4.48) to obtain

| (4.51) |

valid for some , since Lemma 4.7 implies that is the only pole of in the right half plane.

As before, the integral on the right hand side of (4.51) is not absolutely convergent, but is equal to the derivative of a function given by an absolutely convergent integral, in this case

| (4.52) |

This expression is manifestly is (in particular , since ), and we can use this to obtain the counterpart of Lemma 4.5:

Lemma 4.10.

There is a function and a constant such that

| (4.53) |

and

| (4.54) |

as .

The proof is the same as Lemma 4.5, apart from a few details.

Proof.

Letting and and recalling that , we obtain the expansion (4.53) from Equation (4.51). Then using writing out the stationarity condition as in (A.3), we have

| (4.55) |

after cancelling a factor of and noting that . By the generalized binomial theorem,

| (4.56) |

where the sum is absolutely convergent for ; then we have

| (4.57) |

for .

5. An approximately stationary point

This section is devoted to the proof of Theorem 1.1. Following the strategy outlined in Section 1.4 we introduce a measure which is changed only slightly (as measured by ) by the action of . Applying Lemma 1.2, we see that this implies that is close to the stationary measure in a way which allows us to use it to estimate the Lyapunov exponent .

Proof of Theorem 1.1. For each , in view of introducing the probability define a measure by

| (5.1) |

or equivalently

| (5.2) |

where , so that (see (4.29) and (4.53))

| (5.3) |

In Section 5.1 below, we will show that

| (5.4) |

This will be done by using the definition of as a piecewise expression in terms of the stationary measures and to write out the above distance as an integral of terms with approximate calculations due to the presence of differences either of the form or , or of the form of the left hand side of Equation (5.3).

We cannot apply Lemma 1.2 immediately, because is not a probability measure. However using Lemma 4.5 and Lemma 4.10,

| (5.5) |

and thus if we define a probability measure

| (5.6) |

we have

| (5.7) |

Now we write

| (5.8) |

The last two terms can be bounded as follows:

| (5.9) |

where we have used Lemma 4.5 for the last estimate, and similarly

| (5.10) |

using Remark 4.8 to conclude that the other boundary term is zero and using Lemma 4.10 to estimate the final integral. Combining the last three equations and taking into account the correction from (5.5), we obtain

| (5.11) |

The integral appearing here is finite:

| (5.12) |

for and defined in Section 4.3 (noting in particular that the support of is contained in ). We can then apply Lemma 1.2, using (5.7) and (5.11), and the proof of Theorem 1.1 is complete, modulo of course establishing (5.4) to which all the rest of the section is devoted, with

| (5.13) |

∎

Remark 5.1.

Any change in the normalization of is cancelled by a change in , so this definition of is indeed independent of this normalization.

5.1. Quasi-stationarity estimates for : proof of (5.4)

Writing out the definitions of and and using the stationarity properties and we obtain

| (5.14) |

and by (A.6) and (A.4) we can rewrite (5.14) as

| (5.15) |

We can simplify this somewhat by restricting to ; then whenever , and therefore . Then writing out the definition of in (5.1) and (5.2), we have

| (5.16) |

where we have used the observation that is equivalent to since to simplify the indicator functions.

Rewriting the s as s, and using (which can be checked from (A.5) and (A.2)) in the first line

| (5.17) |

We can then use the Triangle inequality to split up the integrals into four parts, obtaining

| (5.18) |

where the fact that and for the relevant implies that the first two integrands are non negative.

Let us now examine the four terms in (5.18) in turn. The first one can be rewritten (mainly using the fact that the integrand is nonnegative)

| (5.19) |

As for the first integral on the right hand side, noting that

it can be estimated using Lemma 4.10 as

| (5.20) |

for . Multiplying by , we see that the first term in (5.19) is .

The second integral on the rightmost side of (5.19) can be written as

| (5.21) |

The first integral in the final expression is similar to the one estimated in (5.20), apart from the presence of a factor of order , and so the whole term is . As for the second term, by integrating by parts and then applying Lemma 4.10 in the same fashion as (5.20), it can be bounded in the following way:

| (5.22) |

Then the right hand side of (5.21) is (since ), and so the second term on the right hand side of (5.19) is when the prefactor is included. We already obtained an estimate of the same order for the first term, so we arrive at the estimate

| (5.23) |

for the first term on the right hand side of (5.18).

The next term is fairly similar:

| (5.24) |

Noting that

and so

| (5.25) |

the first integral on the right hand side of (5.24) can be estimated as follows:

| (5.26) |

where we have used Lemma 4.5 and observed that , as , uniformly for . Consequently, the corresponding term in (5.24) is

The inner part of the second integral on the rightmost side of (5.24) can be rewritten as

| (5.27) |

where the second to last inequality uses the observation that implies , and the final estimate uses (cf. (3.2) and line right after). With this we see that the right hand side of (5.24) is (noting ).

We rewrite the third term in (5.18) using Lemmas 4.5 and 4.10 and the triangle inequality,

| (5.28) |

Noting that

| (5.29) |

and thus

| (5.30) |

we see that

| (5.31) |

and therefore the first term on the right hand side of (5.28) is .

The remaining terms in (5.28) can be estimated easily using Lemmas 4.5 and 4.10, and they are either or . In the second and third terms, due to the bounded support of the inner integral is nonzero unless . The integrands are both uniformly on the domain of integration for , so both terms are of order

| (5.32) |

In the last two terms, the inner integral is again zero unless , but the integrand is now of order , so these terms are of order

| (5.33) |

Summing up, the right hand side of (5.28) is .

Appendix A Some useful identies

Here are some useful identities: recall the definitions (1.20), (1.26) and (1.23). Setting , we obtain

| (A.1) |

for all , and this is another way to define the action of on . Of course is one if is a probability measure, but in general is not normalized. In making use of (A.1) it is helpful to note that

| (A.2) |

Observing that for , we also see that

| (A.3) |

Moreover

| (A.4) |

where

| (A.5) |

In fact, is defined also by the first equality in (A.4), or by equating the left-most and right-most expressions. It is useful to note that (A.4) and (A.1) can be rewritten (using for and for )

| (A.6) |

for every .

Acknowledgements

The authors wish to thank Gunter Stoltz and an anonymous referee for their comments that lead to improvements both in the presentation of the results and in some of the arguments of proof.

References

- [1] Bertrand, J., Bertrand, P., and Ovarlez, J. The Mellin Transform. In A.D. Poularikas, editor, The Transforms and Applications Handbook, chapter 11. Boca Raton: CRC Press, 2nd edition, 2000.

- [2] Bougerol, P. and Lacroix, J. Products of random matrices with applications to Schrödinger operators, volume 8 of Progress in Probability and Statistics. Boston, MA: Birkhäuser, 1985.

- [3] Comtet, A., Texier, C., and Tourigny, Y. Products of random matrices and generalised quantum point scatterers. J. Stat. Phys. 140 427, 2010.

- [4] Comtet, A., Texier, C., and Tourigny, Y. Lyapunov exponents, one-dimensional Anderson localization and products of random matrices. J. Phys. A 46 254003, 2013.

- [5] Crisanti, A., Paladin, G., and Vulpiani, A. Products of random matrices in statistical physics, volume 104 of Springer Series in Solid-State Sciences. Berlin: Springer-Verlag, 1993.

- [6] de Calan, C., Luck, J.M., Nieuwenhuizen, T.M., and Petritis, D. On the distribution of a random variable occurring in D disordered systems. J. Phys. A 18 501, 1985.

- [7] Derrida, B. and Hilhorst, H.J. Singular behaviour of certain infinite products of random matrices. J. Phys. A 16 2641, 1983.

- [8] Dyson, F.J. The dynamics of a disordered linear chain. Phys. Rev. 92 1331, 1953.

- [9] Furstenberg, H. Noncommuting random products. Trans. Amer. Math. Soc. 108 377, 1963.

- [10] Furstenberg, H. and Kesten, H. Products of random matrices. Ann. Math. Statist. 31 457, 1960.

- [11] Hairer, M. and JC, M. Yet another look at Harris’ ergodic theorem for Markov chains. In R. Dalang, M. Dozzi, and F. Russo, editors, Seminar on Stochastic Analysis, Random Fields and Applications VI., volume 63 of Progress in Probability, pages 109–117. Birkhäuser, 2011.

- [12] Hennion, H. Dérivabilité du plus grand exposant caractéristique des produits de matrices aléatoires indépendantes à coefficients positifs. Ann. Inst. H. Poincaré Probab. Statist. 27 27, 1991.

- [13] Kesten, H. Random difference equations and renewal theory for products of random matrices. Acta Math. 131 207, 1973.

- [14] Kunz, H. and Souillard, B. Sur le spectre des opérateurs aux différences finies aléatoires. Comm. Math. Phys. 78 201, 1980.

- [15] Le Page, E. Regularity of the first characteristic exponent of products of independent random matrices, and applications. Annales de l’Institut Henri Poincaré, Probabilités et Statistiques 25 109, 1989.

- [16] McCoy, B.M. and Wu, T.T. Theory of a two-dimensional Ising model with random impurities. I. Thermodynamics. Phys. Rev. 176 631, 1968.

- [17] Meyn, S. and Tweedie, R. Stability of Markovian Processes I: criteria for discrete-time chains. Adv. Appl. Prob. 24 542, 1992.

- [18] Misra, O. and Lavoine, J. Transform Analysis of Generalized Functions, volume 119 of North-Holland Mathematics Studies. Amsterdam: Elsevier, 1986.

- [19] Molchanov, S. The structure of eigenfunctions of one-dimensional disordered systems. Izv. Acad. Sci. USSR 2 70, 1978.

- [20] Oseledets, V.I. A multiplicative ergodic theorem. Characteristic Ljapunov exponents of dynamical systems. Tr. Mosk. Mat. Obs. 19 179, 1968. English: Trans. Moscow Math. Soc. 19 179.

- [21] Ruelle, D. Analycity properties of the characteristic exponents of random matrix products. Adv. Math. 32 68, 1979.

- [22] Schmidt, H. Disordered One-Dimensional Crystals. Phys. Rev. 105 425, 1957.

- [23] Shankar, R. and Murthy, G. Nearest-neighbor frustrated random-bond model in d=2: Some exact results. Phys. Rev. B 36 536, 1987.

- [24] Spira, R. Calculation of the Gamma function by Stirling’s formula. Math. Comp. 25 317, 1971.

- [25] Titchmarsh, E.C. Introduction to the theory of Fourier integrals. Oxford: Clarendon Press, 1948.

- [26] Viana, M. Lectures on Lyapunov Exponents. Cambridge Studies in Advanced Mathematics. Cambridge (UK): Cambridge University Press, 2014.