A New Algorithm to Simulate the First Exit Times of a Vector of Brownian Motions, with an Application to Finance

Chiu-Yen Kao

Department of Mathematical Sciences, Claremont McKenna College, USA. This author is partially supported by NSF DMS-1318364.

Email: Ckao@claremontmckenna.edu

Qidi Peng

Institute of Mathematical Sciences, Claremont Graduate University, USA

Email: Qidi.Peng@cgu.edu

Henry Schellhorn

Institute of Mathematical Sciences, Claremont Graduate University, USA

Email: Henry.Schellhorn@cgu.edu

Lu Zhu

Department of Accounting and Finance, University of Wisconsin, Eau Claire, USA

Email: zhul@uwec.edu

summary

We provide a new methodology to simulate the first exit times of a vector of Brownian motions from an orthant. This new approach can be used to simulate the first exit times of dimension higher than two. When at least one Brownian motion has non-zero drift, the joint density function of the first exit times in dimensions needs to be known, or approximated. However, when the drifts are all zero, a simpler simulation algorithm is obtained without using the joint density function.

Keywords and phrases: First exit times; Correlated Brownian motions; Gaussian copula; Multiple roots transformation

AMS Classification: 60G15; 60E05; 65C05; 65C30

1 Introduction

There are two main approaches to calculate the expected value of a function of joint first exit times of a process from a sufficiently regular domain in , whether bounded or unbounded. The first approach is to set up the problem as a partial differential equation. When the process is Brownian motion, this equation is of either elliptic or parabolic type. The second approach is Monte Carlo simulation. The simplest implementation of Monte Carlo method is to discretize the stochastic differential equation of the underlying process, using for instance the Euler scheme, and to simulate the process until it reaches the barrier, i.e., the boundary of the domain (we will discuss and apply this method in Section 3.2 and Section 4). We refer to this indirect method as Euler-based Monte Carlo. According to Fahim et al. [6], it is well known that numerical methods based on partial differential equations suffer from the curse of dimensionality: calculations and memory requirements typically increase exponentially as the dimension increases. This is not the case for Monte Carlo simulation, where calculations are in general independent of the dimension of the problem.

A hybrid class of approaches uses Monte Carlo method to simulate the first exit times directly, i.e., without first simulating the underlying process . There are two main advantages of this direct simulation approach, compared to Euler-based Monte Carlo. The first one relies on the fact that, in many applications, exit from a bounded domain is a rare event. It may take a very large amount of time (sometimes an infinite amount of time) for a process to reach the boundary. The traditional solution to this problem is to use importance sampling. For advantages and pitfalls of importance sampling in financial engineering, we refer to [7] and the references therein. Another solution, in case the importance sampling density is difficult to construct, is to use interacting particle systems as in [4]. However, we can avoid this problem with direct simulation of the first exit times. The second advantage is its accuracy compared to Euler-based Monte Carlo method. Euler-based Monte Carlo tends to overestimate the first exit time: since the process is discretized, the method misses an excursion, i.e., an outcome where the process is in the domain at two contiguous epochs, but outside the domain at some time in-between these epochs. We note however that there are some techniques by Broadie et al. [3], Huh and Kolkiewicz [9] and Shevchenko [20] to alleviate this problem.

It is worth noting that direct first exit time Monte Carlo algorithms are not plagued by these two problems mentioned above but relying on the following two principles. First, the joint density of the first exit times must be either known or approximated correctly. This problem is often solved by a partial differential equation method, and is quite a difficult analytical problem in high dimensions if the different components of the process are correlated. Secondly, exit times must be sampled from the joint distribution of the corresponding processes without, if possible, resorting to inversion and conditional Monte Carlo, which are very computationally intensive. For bounded domains, there is already rich literature. In [17] the bounded domain is approximated by a series of spheres; in [16] the bounded domain is approximated by a series of parallelepipeds. When the joint density of first exit times for general diffusions are unknown, the latter authors approximate the diffusion by a Brownian motion on small bounded domains. We note that these methods provide better approximation than the simple Euler-based Monte Carlo method does, since the barrier does not need to be corrected.

Simulating the first exit time from an unbounded domain is a slightly different problem. We focus on a particular application in finance: the simulation of the joint default times of a set of obligors. Black and Cox [2] were the first to model the default time of an obligor as the first time the value of the asset returns crosses a lower, constant barrier. There is however no upper barrier on . There have been many variations on this first exit time approach (which the finance literature refers to often as first passage time models). In [2], is a Brownian motion. Collin-Dufresne and Goldstein [5] use a more sophisticated model with mean-reversion in credit spreads. In the last ten years the interest has shifted, from examining a single obligor, to examining a large collection of obligors. Pools of large obligors were the building blocks of the credit default swaps which were heavily traded before the subprime crisis of . It is now recognized that part of the blame of this crisis should be ascribed to the poor risk management of these contracts. Indeed, the task of estimating the parameters of these high-dimensional processes and of simulating them is still recognized as a difficult problem (see [1]). The difficulty of the simulation part of the problem does not come from the complexity of the unbounded domain (usually, a plain orthant), but the complexity of simulating in high dimensions. Zhou [22] provides a formula for the expected first default time (i.e., the expected value of the minimum of the first exit times), which is valid only when . Metzler [13] derives the formula for the joint density of the first exit times when , based on earlier work by Iyengar [10]. We generalize this formula to take into account the cases that were not given in [13]. Metzler [12, 13] also develops an algorithm to simulate the first exit times when the underlying two-dimensional Brownian motion has zero drift. We remind the readers that this is a more general problem than merely finding the expected value of the first default time, as the price of several complicated derivatives cannot be described as a function of the latter. Compared to Metzler [12, 13], our algorithm can be applied in the following cases:

-

1.

and at least one Brownian motion has non-zero drift.

-

2.

and all the Brownian motions are with zero drifts.

The main idea of generating the vector of first exit times in this paper is to transform the joint first exit times to some joint Chi-squared variables and then to generate the latter vector starting from standard Gaussian vector. From (2.3) below we see that, the transformations to Chi-squared distribution have single roots when the drift parameter and multiple roots when . Hence our main results should be stated under two different scenarios: with drift and without drift. It is worth noting that, when the Brownian motions are correlated, our algorithm is not exact (except for two-dimensional Brownian motion with zero drift), however, statistical test and empirical study show that the error of simulation is acceptable in practice (see Sections 3.2 and 4).

The remainder of the paper proceeds as follows. In Section 2, we present our main theoretical results. The simulation of first exit times becomes the simulation of some ’basic’ random variables. When the drift vector of X is non-zero the ’basic’ random variables consist of uniform variables and Gaussian variables, and the simulation method depends on an explicit representation of the joint distribution of the first exit times, which is known only when . When the drifts are all zero, the method becomes simpler and much more powerful: the ’basic’ random variables are Gaussian, and the explicit representation of the joint distribution of the first exit times is not needed. Section 3 summarizes the algorithms. In Section 4, we present an application of our methodology to the first exit time problem in finance. We compare our results to Zhou’s analytical results [22] when , and to Euler-based Monte Carlo simulation when .

2 Main Results

2.1 Statistical Modeling

For some integer , let us consider , an - dimensional Brownian motion, i.e. for ,

| (2.1) |

where ’s are standard Brownian motions and are drift and volatility parameters respectively.

To introduce our estimation method let us start by some notation conventions:

-

•

Denote by the initial values.

-

•

Let be a vector of barriers. We assume that for all .

-

•

Let be the vector of first exit times of to the barriers . More precisely, for ,

We are mainly interested in the problem of generating the joint first exit times . Let us recall that its marginal density is well known in the literature: let be a Brownian motion with drift and variance with and let be some given barrier and be the waiting time until the process first exits the horizontal line . Conditional on and , has the probability density function (see for example [10]):

| (2.2) |

The function is in fact an inverse Gaussian density. Remark that, if , this density of first exit time is defective, i.e., . To overcome this inconvenience, we can generalize the density of first exit time as a mixture of distributions:

where denotes the characteristic function and is the Dirac measure.

A simple componentwise simulation could be used when the Brownian motions are independent. When the vector of Brownian motions consists of correlated components, the problem of simulating the joint first exit times could be rather challenging and we mainly focus on this problem.

2.2 First Exit Times of Brownian Motions with General Drifts and Multiple Roots Transformation

Generally, we suppose that are correlated drifted Brownian motions with , for and . Using the property of inverse Gaussian vector, we introduce a transformation of ’s to Chi-squared random variables. More precisely, for , define the transformation as:

| (2.3) |

where denotes the Chi-squared distribution with one degree of freedom.

Now we are going to state the main results of this part. First we suppose takes any real value. The following proposition extends (2.3) to high dimension.

Proposition 2.1.

Note that through the remaining part of this paper we suppose that for all , , so that the density of is not defective. Now we explain our idea of simulation. By Proposition 2.1, we may consider using an inverse transform to simulate , however this inverse transform has multiple roots. Hence, by using a similar but more generalized method in [15], we are able to generate the first exit times approximately starting from the joint distribution of .

The following theorem outlines a simulation of the first exit times of correlated drifted Brownian motions.

Theorem 1.

Let be the vector of first exit times given in Proposition 2.1 and denote by its joint density. Let be a vector of Chi-squared random variables with one degree of freedom satisfying

For ,

-

•

if , set

(2.4) -

•

if , set

(2.5)

For and , define

and

where denotes the derivative of . Denote by the Lebesgue measure on . Let be any partition of interval satisfying

| (2.6) |

then we have

where is independent of .

It is very difficult to generate the random vector by its exact distribution since: the vector can not be exactly generated from a Gaussian copula. To show this fact we suppose and let be a Gaussian vector verifying , , then we should have (see [19], Lemma )

But numerical integration (for instance by using MATLAB) shows for some values of . For example, taking leads to . Although it is difficult to actually generate two dependent first exit times when they have distributions that are not from a standard multivariate distribution, however, we can expect to simulate data following the same marginal distribution and covariance structure via . More precisely, we introduce the following approximation:

Definition 2.1.

Two second order (i.e., with finite covariance matrix) random vectors and are said to be approximately identically distributed if for , their marginal distributions are equal: ; and their covariance matrices are identical:

We denote this relation by .

Note that nowadays in financial risk aggregation, elliptical copulas (including Gaussian copula) are widely used to simulate dependent data, since they provide a way to model correlated multivariate variables. In our case, we choose the Gaussian copula to generate first exit times following their exact means and covariance matrix. This is the so-called NORTA (normal-to-anything) method. Here we recall a nice result on the simulation of joint uniform random variables by following their covariance structure, starting from Gaussian vector:

Lemma 2.1.

Assume that have correlation , then there exist with correlation satisfying , and

where denotes the cumulative distribution function of the standard normal distribution.

This result is known as the exact relationship between Spearman correlation and Bravais-Pearson correlation (see for example [8]). The approximation given in Definition 2.1 and Lemma 2.1, allow us to simulate the first exit times in the following two situations:

- Case 1:

-

When , and the Brownian motions have non-zero drifts.

In this case the transformations have multiple roots and the explicit formula of , the joint density of can be derived. Hence one can determine the partitions given in (2.6) explicitly. The joint density of is given in the following:

Proposition 2.2.

Let be a two-dimensional Brownian motion respectively with drifts and . Then starting from , the joint density of the first exit times to the barriers is given as

-

1.

Let , and For ,

-

2.

For ,

where

and with denotes the modified Bessel function of the first kind of order .

Inspired by Lemma 2.1, we provide an approximation of the distribution of starting from a standard Gaussian vector :

Proposition 2.3.

Let be the first exit times of with correlation . Set with standard normal components satisfying:

| (2.11) |

Let

| (2.12) |

Let be independent of , . Then, the distribution of can be approximated by that of

| (2.13) |

in the sense that

where for , is defined in , and is given in .

This proposition is a straightforward consequence of Lemma 2.1 and Theorem 1 by taking . Hence we omit its proof. Note that in (2.11) the correlation

can be computed numerically by using the joint density of . Although calculating the correlation by numerical integration in two dimensions is as difficult as calculating the mean exit time, we emphasize that this calculation can be done offline, while exit time simulation usually is not. For instance, in Section 4, one is given a single model of joint asset returns, for which the correlation must be calculated once. However, several contingent claims can be written on these assets. The valuation of each of them requires an independent simulation, and every simulation shares the same value of , whose calculation does not need to be repeated. More importantly, as we will show in the next subsection, when only pairwise correlations need to be numerically calculated.

- Case 2:

-

When , and the Brownian motions are without drifts.

In this case the joint density of is generally unknown (or too complicated to get). We remark that it is not yet tractable in the literature to exactly simulate when its joint density is unknown. Fortunately, when all the drifts are vanishing, the transformations ’s have single roots, and as a consequence we have avoided the problem of selection among multiple roots of transform using the joint density of first exit times. An example of high dimensional simulation is given in Section 4.2. We are going to show the generating method for this case as well as the algorithms in the following sections.

2.3 First Exit Times of Brownian Motions with Zero Drift

When , the reduced joint density of in Proposition 2.2 and the exact simulation of are given in the following Theorem 2 (i). From Theorem 2 (ii), we see reduce to a single root transformations.

Theorem 2.

- (i)

-

The random vector has the following joint density:

-

1.

For ,

-

2.

For ,

-

1.

- (ii)

-

There exist two Chi-squared random variables verifying

such that, with probability ,

Theorem 2 is a straightforward consequence of Proposition 2.2 and Proposition 2.1, where one takes . Remark that Metzler [13] presented the joint density of only in the case when , . Here we have generalized his result to any real values of . Moreover, this theorem could provide a simple and fast simulation of the first exit times. We refer to the following corollary:

Corollary 2.1.

There exists a Gaussian vector with and

such that the distribution of can be approximated by that of

in the sense that

By using the property that the zero-mean Gaussian vector’s distribution is determined only by its covariance matrix, the result of Corollary 2.1 can be straightforwardly extended to high-dimensional correlated Brownian motions with zero drift.

Corollary 2.2.

Let the integer , let be any Gaussian vector satisfying,

and for different ,

| (2.14) |

where each pair is with parameters . Then the random vector can be approximated by

| (2.15) |

in the sense that

3 Algorithms and Statistical Tests

3.1 Algorithms of First Exit Times

Now we introduce a simulation algorithm of first exit times for Brownian motions. We are mainly interested in sampling the first exit times from correlated Brownian motions. The algorithms are given as follows:

- Case 1:

-

Two-dimensional Brownian Motions with Drifts.

For a general two-dimensional vector of Brownian motions, the algorithm can be provided based on Proposition 2.3.

-

1.

Generate a Gaussian vector satisfying (2.11).

- 2.

-

3.

Determine according to (2.12).

-

4.

Generate by using (2.13).

- Case 2:

-

-dimensional Brownian Motions without Drifts.

When the drift is zero, we supply an algorithm to simulate based on Corollary 2.2.

We emphasize that only pairwise correlations need to be numerically calculated. Thus, one of the main advantages of our algorithm is its little numerical complexity: rather than performing an -dimensional integration the algorithm performs a calculation of two-dimensional integrations.

3.2 A Statistical Test of the Algorithms

Although the simulation of the joint first exit times is approximate, it has been shown that the true distribution of the joint first times is quite similar to the one generated by using Gaussian copula. For example, Overbeck and Schmidt [18] compared a Gaussian copula model to a calibration time changed model using the fair basket default swap spreads data and showed that the results are quite close. From their numerical results, ”the seed variance of fair the first-to-default spread is less than and much smaller for the other spreads”; McLeish [14] established an estimator of the maxima of two correlated Brownian motions using some normal vector, and he showed that the approximation is remarkably accurate. In addition, Metzler [12] (Pages 50-51) has compared the true distribution of the first exit time of a 3-dimensional correlated Brownian motions (in this example the barriers are supposed to be equal) to the one from its corresponding Gaussian copula, and concludes that the first exit time in a ”correlated Brownian drivers” model is quite similar to the one in a Gaussian copula model. Here we use another statistical approach to compare our method to Monte Carlo’s method. More comparisons using numerical results are made in the next section. Recall that the Kolmogorov-Smirnov test (K-S test) is used to check the equality of probability distributions. In order to compare random vectors we take a high dimensional K-S test (see for instance [11]), programmed in MATLAB. Let be the random vector generated by using Monte Carlo algorithm and be the one generated by using transformation with multiple roots.

We set the parameters for , and the test’s significant level . realizations are generated by using each method. Now we set up the hypothesis:

The results presented in the following Table 1 show that we won’t reject the fact that with confidence when . However, the dispersion could be increasing when the dimension increases.

| Parameters | K-S Test Result by MATLAB |

|---|---|

| , | |

| , | |

| , |

4 Application to a Multiple-factor Model of Portfolio Default

The simulation of first exit times of Brownian motions has its interests in many credit risk applications. Let be the logarithm of the total value of the assets of firm , where . Assume that satisfies the stochastic differential equation (2.1). For , we denote by the correlation per unit of time between and .

The substantial decrease of a firm’s asset value is the main reason of the default of the firm. Black and Cox [2] defined the threshold value as the minimum asset value of the firm required by the debt covenants. If falls to the threshold value , the bond holder are entitled to a ’deficiency claim’ which can force the firm into bankruptcy. Zhou [22] defined the barrier as the logarithm of the sum of the short-term debt principal and one half of long-term debt principal of a firm. is the logarithm of the current total asset values of firms. With input parameters , we denote the output by , the probability that firms out of in a portfolio have defaulted by a time horizon . For simplicity, the subsequent numerical simulations are based on the assumption that the underlying Brownian motions have the same drift terms and standard deviations. Since, for financial products, most correlations lie between and , three different levels of correlations ( i.e., we denote by ) are examined in the following tables. Zhou [22]’s parameters are applied here: . Over a short horizon, quick default events are rare and the probabilities of multiple defaults could be extremely small, hence a long horizon (years) is used to overcome this problem. We present the multiple default probabilities using two different methods: our method and the Euler-based Monte Carlo algorithm. We compare them to the method in [22] (although our method is more general than Zhou’s result, we compare our method to his for accuracy), which is exact. In the following tables, the step size of the Euler-based Monte Carlo method is equal to and the total number of scenarios is . Note that the Monte Carlo method is always an alternative, however it becomes very computationally intensive when a large number of scenarios need to be performed.

4.1 Simulations of First Exit Times of Two-dimensional Correlated Brownian Motions

The examples without drift terms and with drift terms are both examined in the following Tables -. Three different level correlations are presented to demonstrate how the correlation of logarithm of asset value affects the default probability distribution. In Table 2, means the movements of two firms’ logarithm of asset value are weakly correlated with each other. The fact that shows these movements are strongly positively correlated. The simulation results illustrate the fact that the stronger are the assets’ correlations, the higher are the probabilities of multiple defaults. Zhou [22] indicated that the default correlation and the asset level correlation have the same sign which explains our results here. For instance, a drop in one firm’s asset value leads to a decrease in another firm’s asset value (which is closer to the default boundary), and then leads to a rise of probability of both firms’ defaults. If two firms’ asset values do not move towards the same direction, this behavior leads to a drop in likelihood of multiple default events.

Compared to the analytical results in [22], our method is not completely unbiased, but the results are very promising when . In fact from Tables 2-5, the estimated value of our method has an error rate less than . When , our numerical results (Tables 6-7) show that the error rate is less than . However, in practice we rarely consider the case , since it is quite artificial (see [18]).

| Our Method | Zhou (2001) | Euler-based | |

|---|---|---|---|

| Our Method | Zhou (2001) | Euler-based | |

|---|---|---|---|

| Our Method | Zhou (2001) | Euler-based | |

|---|---|---|---|

| Our Method | Zhou (2001) | Euler-based | |

|---|---|---|---|

| Our Method | Zhou (2001) | Euler-based | |

|---|---|---|---|

| Our Method | Zhou (2001) | Euler-based | |

|---|---|---|---|

4.2 First Exit Times Simulations for High-dimensional Correlated Brownian Motions

We note that our method is roughly as good as Euler-based Monte Carlo method. This is important, as the method in [22] is not applicable in higher dimensions. Some simulation results of first exit times for high-dimensional Brownian motions are listed in Table 8. The subsequent simulations are based on the simple examples without drift terms. Since Zhou’s results can not work on higher dimensional cases, only Monte Carlo method is used here. For simplicity, all the correlations are set to be . For instance, the correlation matrix of three firms’ logarithm of asset value where in Table 8 is

The simulation results are consistent with the fact that the Monte Carlo method tends to under-estimate the multiple defaults probabilities. According to [4], when the number of firms increases, this estimation could have larger deviation. However, compared to the results in [22] which can not calculate multiple default probabilities for more than two firms, the new proposed method can be advantageously expanded to high dimensional Brownian motions. In Table 8, the error rate of our estimation compared to Monte Carlo algorithm is less than , which is acceptable in practice.

| Our Method | Euler-based | |

|---|---|---|

5 Conclusion

A new numerical algorithm is proposed to solve the first exit times of a vector of Brownian motions with zero and non-zero drifts. Compared to the methods in [12, 13] and Zhou’s analytical and numerical results, the advantages of our method are the following: When , our algorithms can take into account drifts and can be easily extended to high dimensions, especially when the drifts are zero. As a consequence, our method allows calculating the expected value of more general functions of the first exit times, not constrained to the minimum of the latter, which is the traditional advantage of simulation.

6 Appendix

6.1 Proof of Theorem 1.

Let be a vector of first exit times with parameters . We assume that and for and the joint density of is . Hence, still by [21], is the solution of the following equation:

| (6.1) |

Notice that for , , the equation

has roots (can be surplus) ,

-

•

if , set

-

•

if , set

(6.2)

The remaining problem is choosing one among the roots according to the observed value of the Chi-squared vector . We explain how this process can be taken. For a particular root , we compute the probability of choosing it. Let be arbitrarily small and let be the inverse image of . For , let the intervals be disjoint for each and contain the -th root of equation : . Notice that we should choose as the observation of if for . Therefore the probability of choosing the particular root is given as

Observe that as . Hence letting denote the probability measure which depends on and letting , by a similar principle to L’Hôpital’s rule (see Equation (3) in [15]), we get

where we recall that and for and any ,

Let be equal to the observation of Chi-squared vector defined in (6.1) and let be the root labeled of (6.1), then the ’probability’ (it is a random variable) of choosing this root is given as

It remains to generate the probability distribution . It can be simulated by generating an independent uniform random variable and the following random partition of interval :

with for almost every , . This is equivalent to (2.6). Finally

and

6.2 Proof of Proposition 2.2.

Notice that we derive the idea from the seminal work by Iyengar [10]. Unfortunately, this work contains errors. Metzler [13] provided the correct formula of the two-dimensional first exit times joint density, however the one with non-zero drift with drift is not explicitly given. In this section we provide a relatively closed form of the joint density. Our work also extends the joint density of first exit times in [13] to the case where the barriers could be any real values. First we assume that for , . The main idea is to transform the Brownian motions to independence (see [10]). By such a linear transformation, the first exit time remains invariant when the Brownian motion starts from to the barrier . Hence, without loss of generality, we only consider the barriers as horizontal axis . Define by

be the transformation of the vector of Brownian motions with correlation and variances to the independent standard Brownian motions. Denote the latter by and . After transformation , the horizontal barrier line remains the same and turns to be the line . Note that the notations are exactly the same as mentioned in the joint density of . The explicit form of joint density depends on the conditions and .

-

1.

For , this shows . Following the argument of Metzler [13], the joint density of is given as

where

- (i)

-

, with being the transpose of and being the Euclidian norm.

- (ii)

-

By easy computation, we can get , , as in Proposition 2.2, with .

- (iii)

-

is the polar coordinates of the transformation of the exit position .

- (iv)

-

By Iyengar [10] and Metzler [13],

is the density of time for to first exit from the line and

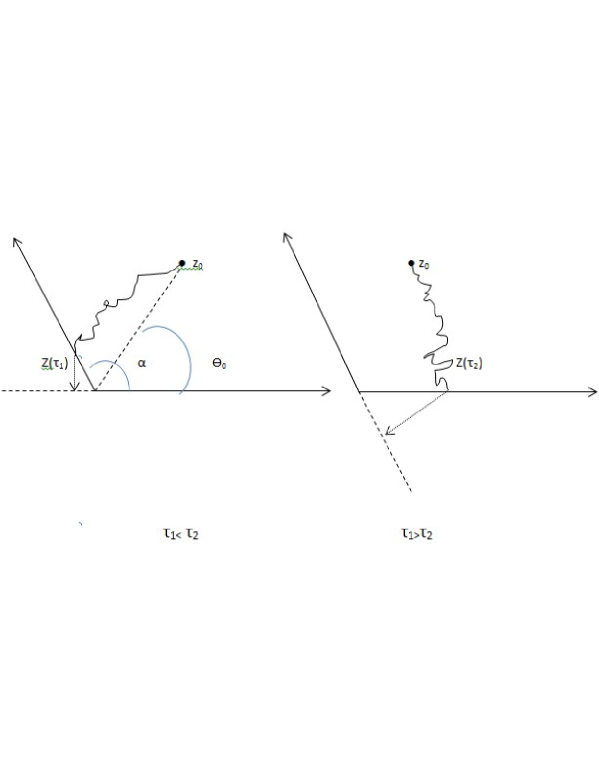

is in fact the inverse Gaussian density on which denotes the remaining time for to first exit its barrier, once exits. By martingale property, this event can be regarded as the first exit time of a standard Brownian motion with drift , starting from , to the barrier (see Fig. for ).

-

2.

For (this shows ), the joint density can be obtained in a similar way:

where we just need to remark that and the latter inverse Gaussian density (on ) denotes the remaining time for to first exit its barrier, once exits. It can be further regarded as the first exit time of a standard Brownian motion with drift , starting from , until the barrier .

Now it suffices to simplify the above two formulae. For example, let us simplify the first one: when ,

When , we can pursue the same approach to simplify the expression (see Fig. for ). Finally, we get

-

1.

For ,

-

2.

For ,

(6.4)

Now we are going to derive the most generalized density, where the barriers could be any real values. To this end we first observe that, when , , there exists a function such that

By using the symmetric property of Brownian motion, when for or , we notice that

where is a Brownian motion with drift starting from . Therefore the first exit times of with drifts , starting from to the barriers are almost surely equal to the first exit times of , starting from the initial values to the barriers . Remark that

Finally, we have for all , ,

For any , , plugging the arguments

6.3 Proof of Corollary 2.1.

To prove Corollary 2.1, we rely on Lemma 2.1 and the following lemma which is known as a consequence of Sklar’s Theorem:

Lemma 6.1.

Let be the cumulative probability distribution function of , then .

Now we are ready to prove Corollary 2.1. Since

then by Lemma 6.1,

has marginal distribution . Observe that for any , . Then the correlation of can be given by using the joint density of :

Therefore by Lemma 2.1, there exists a Gaussian vector such that (2.1) holds. By the fact that for ,

and by observing that , Corollary 2.1 holds.

References

- [1] Anonymous (2009). In defense of the Gaussian copula. Economist, April 29.

- [2] Black, F. and Cox, J. C. (1976). Valuing corporate securities: some effects of bond indenture provisions. Journal of Finance, 31 (2), 351-367.

- [3] Broadie, M., Glasserman, P. and Kou, S. (1997). A continuity correction for discrete barrier options. Mathematical Finance, 7 (4), 325-348.

- [4] Carmona, R., Fouque, J. P. and Vestal, D. (2009). Interacting particle systems for the computation of rare credit portfolio losses. Finance and Stochastics, 13 (4), 613-633.

- [5] Collin-Dufresne, P. and Goldstein, R. S. (2001). Do credit spreads reflect stationary leverage ratios? The Journal of Finance, 56 (5), 1929-1957.

- [6] Fahim, A., Touzi, N. and Warin, X. (2011). A probabilistic numerical method for fully nonlinear parabolic PDEs. The Annals of Applied Probability, 21 (4), 1322-1364.

- [7] Glasserman, P. and Li, J. (2005). Importance sampling for portfolio credit risk. Management Science, 51 (11), 1643-1656.

- [8] Hotelling, H. and Pabst, M. R. (1936). Rank correlation and tests of significance involving no assumption of normality. Annals of Mathematical Statistics, 7 (1), 29-43.

- [9] Huh, J. and Kolkiewicz, A. (2008). Computation of multivariate barrier crossing probability and its applications in credit risk models. North American Actuarial Journal, 12 (3), 263-291.

- [10] Iyengar, S. (1985). Hitting lines with two-dimensional Brownian motion. SIAM Journal on Applied Mathematics, 45 (6), 983-989.

- [11] Lopes, R. H. C. (2007). The two-dimensional Kolmogorov-Smirnov test. XI International Workshop on Advanced Computing and Analysis Techniques in Physics Research, Proceedings of Sciences.

-

[12]

Metzler, A. (2008). Multivariate first passage models in credit risk. Ph. D.

Dissertation, University of Waterloo. https://uwspace.uwaterloo.ca/bitstream/handle/10012/

4090/thesisadammetzler.pdf?sequence=1 - [13] Metzler, A. (2010). On the first passage problem for correlated Brownian motion. Statistics and Probability Letters, 80 (5), 277-284.

- [14] McLeish, D. L. (2004). Estimating the correlation of processes using extreme values. Fields Institute Communications, 44, 447-467.

- [15] Michael, J. R., Schucany, W. R. and Haas, R. W. (1976). Generating random variates using transformations with multiple roots, The American Statistician, 30 (2), 88-90.

- [16] Milstein, G. N. and Tretyakov, M. V. (1999). Simulation of a space-time bounded diffusion, Annals of Applied Probability, 9 (3), 732-779.

- [17] Muller, M. E. (1956). Some continuous Monte Carlo methods for the Dirichlet problem. The Annals of Mathematical Statistics, 27 (3), 569-589.

- [18] Overbeck, L. and Schmidt, W. (2005). Modeling default dependence with threshold models. Journal of Derivatives, Summer 10-19.

- [19] Peng, Q. (2011). Statistical inference for hidden multifractional processes in a setting of stochastic volatility models. Ph. D. Dissertation, University Lille . https://ori-nuxeo.univ-lille1.fr/nuxeo/site/esupversions/c56bf4f8-263c-4dc2-9196-85e5ef5d22e1

- [20] Shevchenko, P. V. (2003). Addressing the bias in Monte Carlo pricing of multi-asset options with multiple barriers through discrete sampling. The Journal of Computational Finance, 6, 1-20.

- [21] Shuster, J. (1968). On the inverse Gaussian distribution function. Journal of the American Statistical Association, 63 (324), 1514-1516.

- [22] Zhou, C. (2001). An analysis of default correlations and multiple defaults, The Review of Financial Studies, 14 (2), 555-576.