\pkgdenoiseR: A Package for Regularized

Low-Rank Matrix Estimation

Julie Josse, Sylvain Sardy, Stefan Wager \Plaintitle\pkgdenoiseR a package for low rank matrix approximation \Shorttitle\pkgdenoiseR \Abstract

We introduce \pkgdenoiseR, an \proglangR package that provides a unified

implementation of several state-of-the-art proposals for regularized low rank matrix estimation,

along with automatic selection of the regularization parameters.

We also extend these methods to allow for missing values.

The regularization schemes discussed in this paper are built around singular-value shrinkage and

bootstrap-based stability arguments.

We illustrate how to use out package by applying it to several real and simulated datasets, and

highlight strengths and weaknesses of the different implemented methods.

\KeywordsLow-rank matrix estimation; singular values shrinkage; bootstrap; Stein Unbiased Risk Estimate; count data; correspondence analysis; clustering; missing values; matrix completion

\Address

Julie Josse

Department of Statistics

Agrocampus Ouest/ INRIA / Polytechnique

E-mail:

URL: http://julie.josse.com

1 Introduction

Consider the model where a data matrix with rows and columns is generated from some distribution with :

| (1) |

The statistical aim is to recover the signal from the noisy data. The low-rank assumption underlying model (1) has become very popular in recent years, and arises naturally in several different settings (Udell17). It gained traction in the machine learning community as a powerful way to address the problem of recommender systems, as exemplified by the famous Netflix challenge (Netflix).

The classical approach to this problem is to estimate the signal as the best rank- approximation to , for some adaptively chosen :

| (2) |

The solution is the truncated singular value decomposition (SVD) of the matrix at the order (Eckart:1936), namely

| (3) |

where are the singular values organized in decreasing order.

In recent years, however, there as been considerable interest in procedures that improve over the truncated SVD by further regularizing . These proposals include matrix soft-thresholding (CandesSURE:2013), adaptive trace norm regularization (sardy15), bootstrap-based regularized autoencoding for count data and other exponential family noise models (JosseWager), and estimators motivated by asymptotic expansions (Verbanck:RegPCA:2013; OS:2014); see Section 2 for a more detailed description. We implement all these methods in the \proglangR package \pkgdenoiseR. We give a particular attention to providing sensible choices of default parameters, automatic selection of the regularization parameters and ways to estimate the noise variance.

The package \pkgdenoiseR, available on CRAN, is the first to implement low rank matrix estimation methods in the \proglangR language. We describe in Section 3 the main functionalities of \pkgdenoiseR and give guidelines on the predilection regimes of each method. In the remaining sections, we go beyond published works as follows. In Section 4, we extend all methods to the incomplete case, and tackle the challenging task of selecting the regularization parameter(s) when missing values are present by extending the Stein unbiased risk estimation. As an aside, we propose a new highly competitive method to impute data and to complete count data. Finally, Section 5 carries out experiments and illustrates the potential of the methods to denoise data sets from different fields. More precisely, an unsupervised clustering is performed on a microarray data, correspondence analysis is used to visualize a documents-words data of the inaugural speeches of the U.S. Presidents, and matrix completion is applied on the “journal impact factors” data.

Software for regularized singular value decomposition is partially available. Soft-thresholding estimator with Stein unbiased risk estimation is implemented in \proglangMATLAB as a standalone file that is available at https://statweb.stanford.edu/~candes/SURE/. The asymptotic estimators of Raj and OS:2014 is available as a \proglangMATLAB software library which can be downloaded in https://purl.stanford.edu/kv623gt2817 and that includes a function to calculate the optimal singular value shrinkage with respect to the Frobenius operator and nuclear norm losses, both in known or unknown noise level. Many \proglangR packages implement versions of classical truncated SVD (online, fast, etc.), but as far as we know, no method for regularized low rank matrix estimation is available, which is the aim of \pkgdenoiseR. One should mention related packages on covariance matrix estimation with shrinkage strategies such as \pkgcovmat, (covmat) \pkgcorpcor (corpcor) or \pkgnlshrink (nlshrink). Packages on missing values are detailed in Section 4.

2 Methods for low-rank matrix estimation

2.1 Singular values shrinkage

We start by considering direct extensions of the truncated SVD estimator (3) using singular value shrinkage. Perhaps the best known estimator of this type arises via the nuclear norm regularized method studied by Cai08:

where is the nuclear norm of the matrix . Algorithmically, this method is equivalent to soft-thresholding singular values in (3) (see Dono94b for definitions of hard and soft thresholding functions):

| (4) |

In other words, singular values smaller than a quantity are set to zero and the others are shrunk towards zero by an amount (in contrast to hard thresholding, where singular values are either unmodified or then set to zero). The number of non-zero singular values provides an estimation for the rank . Many studies (shabalin2013reconstruction; OS:2014; sardy15; JosseWager) showed both analytically and with simulations that the soft-thresholding estimator gives small mean squared error (MSE) to recover with low signal-to-noise ratio (SNR) but struggles in other regimes.

For more flexibility, the adaptive trace norm estimator (ATN) of sardy15 uses two regularization parameters to threshold and shrink the singular values:

| (5) |

This estimator denoted is the closed form solution to

where is a weighted nuclear norm with . ATN parametrizes a rich family of estimators and includes (3) and (4) as special cases. As an insight of its good behavior, the smallest singular values responsible for instability in (5) are more shrunk in comparison with the largest ones when .

The parameters can be selected with cross-validation. However, in the context of a Gaussian specialization of the low-rank model (1),

| (6) |

more computationally efficient tuning is possible using Stein unbiased estimate of the risk (Stein:1981). sardy15 extend the results of CandesSURE:2013 and propose the risk estimate

| (7) |

where the second term corresponds to the residuals sum of squares (RSS) whereas the last one is the divergence defined as

The expectation of the divergence corresponds to the degrees of freedom. Having a closed form expression for the divergence is computationnally convenient. Without it, the divergence could be approximated by finite differences, which is our approach with missing values in (19).

A limitation of SURE is that it requires knowledge of the noise scale . Inspired by generalized cross-validation (CravenWahba79), sardy15 derived generalized SURE

| (8) |

which does not require knowledge of .

The parameters are then estimated by minimizing (G)SURE. However, minimizing (G)SURE can prove to be difficult and unstable. The difficulty is due to the fact that (G)SURE is a piecewise smooth surface with occasionnal jumps as a function of , and the higher , the higher the jumps. The unstability of the (G)SURE selection is due to the fact that, although unbiased, the risk estimate has some variance. Consequently, in situation of low signal-to-noise ratio, the global minimum may occur at a value of that has poor estimation properties for the low rank matrix . SardySBITE2012 studied the smoothness and the minimization of SURE in regression, and sardy15 compared a SURE surface to the -loss surface in low rank matrix estimation.

Of course, minimizing over for (i.e., soft-thresholding) is easier than minimizing over . In addition, when estimation of is poor, SURE may lead to a poor selection of the regularisation parameter(s).

Nevertheless, the ATN estimator (5) has shown excellent recovery properties in experiments (sardy15; JosseWager), in particular in comparison with the soft-thresholding estimator (4). This is particularly true when the signal-to-noise ratio is moderate or high, in which case the minimum of (G)SURE over is close to the minimum of the (unknown) -loss and therefore leads to good estimation with ATN. For good rank recovery, sardy15 employed the quantile universal threshold (QUT) to select (Sardy16). The rationale of QUT is to select the threshold at the bulk edge of what a threshold should be to reconstruct the correct model with high probability under the null hypothesis that (the matrix with zeros for entries). Then they minimize GSURE() over .

2.2 Asymptotically optimal shrinkage

In certain asymptotic regimes, it is possible to go beyond the results presented above, and to derive optimal singular value shrinkage estimators that minimize expected loss. First, when both the number of rows () and columns () tend to infinity while the rank of the matrix stays fixed, shabalin2013reconstruction and OS:2014 consider asymptotics motivated by random matrix theory and show that the estimator the closest to the true signal in term of MSE has the following form,

| (9) |

where , , and is the indicator function (note that the restriction is without loss of generalization, since we can always apply this formula to the transpose of the matrix). If the noise variance is unknown, the authors suggested

| (10) |

where is the median of the singular values of and is the median of the Marcenko-Pastur distribution. OS:2014 also provided optimal shrinkers using other losses than the Frobenius one, namely the Operator and Nuclear losses.

In another asymptotic framework, considering and as fixed, but letting the noise variance tend to zero, Verbanck:RegPCA:2013 shows that the MSE-minimizing estimator has the following form:

| (11) |

Each singular value is multiplied by a quantity which can be seen as the ratio of the signal variance over the total variance. This estimator corresponds to a truncated version of the one suggested in Efron72. If the noise variance is unknown, the authors suggested

| (12) |

which corresponds to the residual sum of squares divided by the number of observations minus number of estimated parameters. The variance estimate requires a value for the rank , for instance estimated by cross-validation (Josse11b). This latter method has shown excellent empirical performances.

2.3 Bootstrap-based regularization for exponential family noise models

All previous estimators started from the point of view of the singular value decomposition. JosseWager suggested an alternative regularization based on the bootstrap. Given an observed matrix , the optimal rank linear estimator for would be

| (13) |

This estimator, however, is infeasible, as it involves computing an integral over an unknown data distribution.

To get around this issue, JosseWager propose replacing the draws from the unknown data-generating distribution with bootstrap draws , resulting in an estimator they call the stable autoencoder,

| (14) |

With Gaussian data as in (6), JosseWager advocate Gaussian parametric bootstrap , while with Poisson data , they recommend binomial thinning

Here is a regularization parameter controlling the amount of bootstrap noise. Both of these proposals are special cases of a Lévy bootstrap procedure that can be defined for any exponential family distribution (wager2016data).

Given a parametric bootstrap scheme, the problem (14) can equivalently be written as,

and the solution is

| (15) |

When, the noise is Gaussian as in model (6), is equal to a diagonal matrix with elements and (15) can also be written as a classical singular-value shrinkage estimator:

If instead we have count data and consider a Binomial model, is a diagonal matrix with row-sums of multiplied by . Due to the non-isotropic noise, the new estimator (15) does not reduce to singular value shrinkage: its singular vectors are also modified. This characteristic is unique and implies that the estimator will be better than the competitors that only shrink the singular values to recover the signal for models such as . The complexity of estimator is determined via that we estimate by cross-validation. This procedure requires to get from an incomplete data set, which will be described in Section 4.

In a second step, JosseWager showed that the performance of stable autoencoding can considerably be improved by iterating the procedure until reaching a fixed point of the proposed denoising scheme. Specifically, they iterate the procedure by replacing with the low rank estimate obtained from the optimal , and by solving with as described in Algorithm 1.

One advantage of the iterated stable autoencoder (ISA) is that it automatically produces low rank estimates ; thus, the practitioner only needs to specify a single regularization parameter , instead of having to choose both and with the original stable autoencoder (14). The procedure requires knowledge of for Gaussian models.

Finally, JosseWager extended their results and also used ISA to regularize correspondence analysis (CA) (green1984ca; green2007ca). CA is a powerful method to visualize contingency tables and consists in applying an SVD on the data transformation

| (16) |

where , , is the the total number of counts, and and are vectors containing the row and column sums of . This approach will be illustrated Section LABEL:sec:presi.

3 Low rank matrix estimation with denoiseR

3.1 Implemented methods

denoiseR is designed to estimate a low rank signal with the estimators described in the previous sections. Table 1 lists the methods (for Gaussian noise), their \proglangR names, some options, the selection rule for their regularization parameter(s) and their regime of predilection. Additionally, the functions \codeestim_sigma and \codeestim_delta are provided to respectively estimate the noise variance and the bootstrap noise for ISA.

method function option regularization parameter required setting Soft threshold (4) \codeadashrink gamma.seq=1 with SURE or QUT yes low SNR Soft threshold (4) \codeadashrink gamma.seq=1 with GSURE no low SNR ATN (5) \codeadashrink with SURE or QUT yes medium,high SNR ATN (5) \codeadashrink with GSURE no good overall Asympt (9) \codeoptishrink method=ASYMP yes , Low-noise (11) \codeoptishrink method=LN yes ISA (Algo 1) \codeISA with CV no moderate SNR

The different methods have been extensively compared using simulations in sardy15 and JosseWager. The simulations highlighted that the proposed methods have different strengths and weaknesses. The soft-thresholding estimator (4) behaves well in low SNR settings, but struggles in other regimes. The other estimators, ISA (Algorithm 1), Asympt (9), Low-noise (11), with non-linear singular-value shrinkage functions are more flexible and perform well expect when the SNR is low. The estimators Asympt and Low-noise provide good recovery in their asymptotic regimes. With two regularization parameters and , the ATN estimator (5) is flexible and can adapt well to the signal-to-noise ratio. Often, the two-dimensional SURE criterion identifies a minimum that leads to good estimation. On occasion, the SURE surface is a rather erratic function of and , causing the estimator to perform poorly, in particular in low signal-to-noise ratio. Estimation of the noise variance has necessarely an impact on the results and suggested methods accurately estimate the noise variance in their respective regime but may struggle in others. Nevertheless, the ATN estimator, with its procedure to select the regularization parameters, performs best overall.

Based on these experiments, we recommend the following strategy for regularized low rank matrix estimation. If one of the asymptotic regimes discussed in Section 2.2 appears plausible, the user should use \codeoptishrink with either the \codeASYMPT or \codeLN option. In other settings, for Gaussian noise, if the noise variance is unknown, ATN with GSURE should be used, as it does not require an estimate of . If GSURE encounters any difficulties, we suggest first estimating the variance (with the method that is the most plausible given the data at hand) and then using ATN with SURE. ISA is recommended for non-Gaussian noises. Finally, ATN with gives good indication for rank estimation. ISA also tends to estimate the rank accurately except when the signal is nearly indistinguishable from the noise while the soft-thresholding tends to over-estimate the rank.

The next subsection provides the arguments of the different functions. We start with ATN and GSURE as recommended and then describe how to perform ATN with SURE. Soft-thresholding is included in the package as it is a classical method.

3.2 Using denoiseR with Gaussian noise

After installing the \pkgdenoiseR package, we load it. First, we generate a data set of size of rank according to model (6) with the function \codeLRsim. The amount of noise is defined by the argument \codeSNR. This function returns the simulated data in \codeX, the signal in \codemu and the standard deviation of the noise in \codesigma.

R> library("denoiseR") R> Xsim <- LRsim(n = 200, p = 500, k = 10, SNR = 4)

Then, we denoise the data with ATN (5) using the function \codeadashrink as follows: {CodeInput} R> ada.gsure <- adashrink(Xsimmu.hat {CodeOutput} R> ada.gsureλ, γn ×pγλ^μ_(λ, γ)μσ^2kkσσ^2(λ, γ)λγλXλ^QUTγ^γ

3.3 Using denoiseR for non-Gaussian noises

We recommand \codeISA for such a situations, with the following options: {CodeInput} ISA <- function (X, sigma = NA, delta = NA, noise = c("Gaussian", "Binomial"), transformation = c("None","CA"), svd.cutoff = 0.001, maxiter = 1000, threshold = 1e-06, nu = min(nrow(X), ncol(X)), svdmethod = c("svd", "irlba"), center = TRUE)

The CA transformation (16) can be obtained by setting the argument \codetransformation = "CA"; by default it is \codetransformation = "NONE". In the CA case, the noise model is set to \codenoise = "Binomial" by default.

If the argument \codedelta is not specified, it is set to by default. Otherwise, it is estimated for the Binomial noise by repeated learning cross-validation using the function \codeestim_delta: {CodeInput} R> estim_delta (X, delta = seq(0.1, 0.9, length.out = 9), nbsim = 10, noise = "Binomial",transformation = c("None", "CA"), pNA = 0.10, maxiter = 1000, threshold = 1e-08)) This function returns a matrix \codemsep with the prediction error obtained for varying from 0.1 to 0.9, as well as the value of minimizing the mean squared errors prediction in the object \codedelta. The argument \codepNA indicates the percentage of missing values inserted and predicted and the argument \codenbsim the number of times this process is repeated.

ISA can also be applied with \codenoise = "Gaussian" for model (6). If is not specified, it is estimated by default with the function \codeestim_sigma using the argument \codemethod = "MAD". The option \codemaxiter corresponds to the maximum number of iterations of \codeISA whereas \codethreshold is for assessing convergence (difference between two successive iterations). It is possible to specify \codesvdmethod = "irlba" to use a fast SVD which is particularly useful when dealing with large matrices. In this case, the number of computed singular values can be specified with the argument \codenu.

ISA returns the estimation in \codemu.hat, the number of non-zero singular values in \codenb.eigen, the results of the SVD of the estimation in \codelow.rank and the number of iterations taken by \codeISA in \codenb.iter.

4 Missing values

We extend and implement here all estimators to the presence of missing data. As an aside, we get new ways to impute data. Both extensions of ATN and ISA are new. Another side contribution is to extend SURE to missing values.

4.1 Iterative imputation

Low rank matrix estimation using (3) or (4) has been extended for an incomplete data set (JosseHusson12; Trevor15) by replacing the least squares criterion by a weighted least squares

| (17) |

where when is missing and 1 otherwise and stands for the elementwise multiplication. In the \proglangR package \pkgsoftImpute (softimpute), Trevor15 solved equation (17) using an iterative imputation algorithm. Such an algorithm starts by replacing the missing values by initial values such as the mean of the non-missing entries, then the estimator is computed on the completed matrix and the predicted values of the missing entries are updated using the values given by the new estimation. The two steps of estimation and imputation are iterated until empirical stabilization of the prediction. At the end, since the algorithm denoises the signal but also imputes the missing entries, it can be seen as a matrix completion and single imputation method (Schafer97; Little02). We follow the same rationale and define iterative imputation algorithms for ATN in Algorithm 2. The iterative ISA algorithm can readily be defined.

Iterative ATN and ISA have not been investigated theoretically yet, but a simulation study in Section 4.3 shows that the good empirical properties observed in the complete case seem to extend to the missing data case.

4.2 SURE with missing values

The \proglangR package \pkgsoftImpute (softimpute) does not provide a method to select the regularization parameter but suggests using cross-validation. In \pkgdenoiseR, we suggest a selection of the regularization parameters with missing values based on the Stein unbiased risk estimate. In the complete case, we used SURE as an alternative to cross-validation as it is less computationaly costly. SURE is designed to select the parameters that minimize the risk of the estimator. Since no close form solution is available for the divergence of the estimator when missing values are present, SURE has, as far as we know, never been defined with missing values. We circumvent the problem by adapting the SURE formula (7) criterion for missing values: the first term is replaced by , where the number of missing cells; the second term is replaced by the RSS on the observed values , where is the estimation and imputation obtained with Algorithm 2; the third term involving the divergence is calculated using finite differences with

| (18) |

where a small variation near machine precision and is the matrix of size with 0 except a 1 at position . Consequently, is obtained by first applying the iterative algorithm 2 to the data matrix with added to its entry and then by keeping the estimated value for the entry . The resulting SURE formula for missing values is

| (19) |

GSURE (8) can readily be extended to missing values to deal with unknown noise variance. SURE with finite differences was also discussed in Ramani08 and Gab14. The former used it for a variety of estimators and appreciated the “black-box" aspect of the technique since no knowledge of the functional form of the estimators is required to compute it, while the latter focused on the gradient of SURE criteria to optimize it with quasi-Newton algorithms.

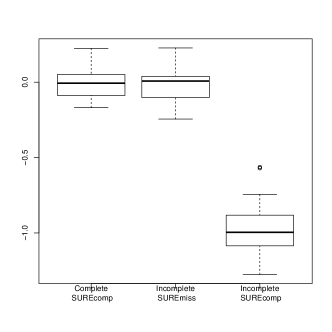

To assess the validity of our proposal, we check that (19) is an unbiased estimate of the risk on a simulation for (i.e., the soft-thresholding estimator) and known noise variance . We consider a complete data generated according to (6) with 50 rows, 30 colums, rank and SNR of 0.5. Then, for a given value of , we compute the complete estimator (4), its risk MSE = MSE and the estimator of the risk with SURE (7). Next, we create 20% missing entries completely at random and impute the missing values with using the iterative ATN algorithm described in Section 4.1. To estimate the corresponding risk, we use either SURE (19) to take imputation into account (working only on the observed values) or SURE which treats the imputed data as if they were real observations. We repeat this procedure one hundred times and represent the distribution of the difference between the true loss and SURE in Figure 1. As expected, SURE is an unbiased estimate of the risk in the complete case (left), and we see that our risk estimate (19) corrects well the biasedness of a simple SURE formula employed as if the imputed data were observations (right). Comparable results were obtained with other matrix sizes and values of and .

Despite the theoritical soundness of this approach, we should remark that it is computationaly heavy so that the computional advantage over cross-validation advocated in the complete case is no longer so clear. We investigate this point in the next section.

4.3 Application to matrix completion

A small simulation study shows the potential of the iterative ATN algorithm to impute data. We use data sets that differ in terms of number of observations , number of variables and relationships between variables. More precisely, the first two data sets are generated from model (6) with rank , respectively equal to 3 and 2, whereas the Parkinson data set (Buhlmann12) is known for its nonlinear relationships between variables. Next, we insert 20% of missing values according to the two mechanisms missing completely at random (MCAR) and missing at random (MAR) (Little02). For the former, we simply insert missing values uniformally whereas for the latter, we put missing values in one variable say when the values of another variable say is greater than the upper quartile of . We use this approach for different variables and different quartile until reaching a desired percentage of missing entries. The detail is available in the associated code provided as supplementary material.

We impute the data with the following methods:

-

•

ATN based on GSURE.

-

•

soft thresholding (17) by softimpute.

-

•

random forests (RF) by Buhlmann12.

-

•

based on Gaussian distribution by mice; Buur12. Imputation is obtained using iterative imputation with multiple regressions.

-

•

a baseline imputation with the mean of the variables on the observed values.

We then compute the squared error of prediction, and repeat the process 50 times. Table 2 reports the mean squared errors of prediction. Since, no method is available to select the regularization parameter in \pkgsoftImpute, we generate a grid for and use its oracle value, by minimizing the mean squared errors prediction. We generate multiple imputed datasets in \pkgmice and take the average for single imputation. The code to reproduce the simulations is available as supplementary materials.

Data scale ATN softImp RF mice Mean Simulation 1 30 50 3 (1.e-5) 60/62 67/67 62/65 NA/NA 68/71 Simulation 2 41 10 2 (1.e-3) 9/10 11/22 33/191 10/13 223/471 Parkinson 195 22 (1) 111/95 219/85 79/47 NA/NA 111/95

The small simulation results show that the proposed methods have strengths and weaknesses. The first two methods, namely ATN and softImpute, have errors in the same range of magnitude but with a slight advantage for ATN. This behavior is expected since ATN often improves on softImpute for complete case data (sardy15; JosseWager). Both methods perform best under model (6) but struggle with non-linear relationships. Indeed, the imputation for both methods is based on low rank assumption and linear relationship between variables. Conversely, imputation with random forests can cope with non-linearity in the Parkinson data. However, despite its recent popularity (Buhlmann12; Doove14; Shah14), imputation with random forests breaks down for small sample size and MAR cases, as already observed in Audigier13, because extrapolation and prediction outside of range of data seems difficult with random forests. The imputation based on regression (mice) breaks down when smaller than and for Parkinson data. These results are not surprising since the properties of an imputation method depend on the inherent characteristics of the method. Regression based imputation methods also encounter difficulties when the variables are highly correlated. Some imputation based on ridge regression have been suggested in mice to tackle this issue.

Since the structure of the data is not known in advance, one could use cross-validation and select the method which best predicts the removed entries. Nevertheless, we argue that many data sets have a good low rank approximation (Udell17), so that imputation based on SVD often proves accurate.

However, ATN requires to select regularization parameters with GSURE which is computationaly costly as it uses finite differences. To investigate the gain of using GSURE instead of cross-validation, we perform additional simulations under model (6) varying size of the data, rank and percentage of missing entries. We report a subset of the results in Table 3.

10% missing 20% missing MSE time MSE time MSE time MSE time RF 0.074 0.168 0.0719 1.451 0.159 0.303 0.156 0.508 Mean 0.141 0.001 0.1264 0.001 0.262 0.000 0.259 0.001 ATN 0.052 132.572 0.0567 8371.077 0.111 248.359 0.126 462.570 ATN CV 0.053 5.314 0.0571 63.076 0.113 11.009 0.127 9.986

Although ATN with GSURE still gives the smallest MSEs, the method is extremelly costly and takes more time than ATN with cross-validation (we implemented a 10-fold cross validation) which gives MSEs in the same order of magnitude. Imputation with random forests is also reported: it is known to be slow, but still faster than ATN. However, as observed in Table 2, ATN still provides the best prediction of missing values and improves on the competitors (Random forests, SoftImpute, mice).

Table 4 shows that, in very difficult settings, ATN with GSURE may encounter more difficulties than ATN with CV. Ef2004 shows that both approaches have advantages and drawbacks but that SURE may offer better accurancy when the model is correct.

(30,50) MSE time RF 0.110 1.451 Mean 0.135 0.001 ATN 0.127 8371.077 ATN CV 0.060 63.076

4.4 Implementation

To perform the iterative ATN algorithm on an incomplete data, we use the \codeimputeada function with the following options: {CodeInput} R> imputeada(X, lambda = NA, gamma = NA, sigma = NA, method = c("GSURE", "SURE"), gamma.seq = seq(1, 5, by=.1), method.optim = "BFGS", center = "TRUE", scale = "FALSE", threshold = 1e-8, nb.init = 1, maxiter = 1000, lambda0 = NA)

If the argument \codelambda and \codegamma are not specified, they are estimated with \codemethod = "GSURE" or \codemethod = "SURE". Contrarily to the complete case, the argument \codemethod = "QUT" is not available. Moreover one must specify the variance of the noise when using the argument \codemethod = "SURE" (19) because estimation of with missing values is not available yet. The outputs are the same as for complete data. In addition, the function outputs a completed data matrix in \codecompleteObs.

5 Exploratoration and visualization using denoiseR

5.1 Unsupervised clustering on a tumors data

Unsupervised clustering is often applied on denoised data to better identify the clusters (Paghuss10). We illustrate the difference in clustering results after denoising either with truncated SVD or ATN on tumors data. The data consist of 43 brain tumors of four different types defined by the standard world health organization (WHO) classification (O, oligodendrogliomas; A, astrocytomas; OA, mixed oligo-astrocytomas and GBM, glioblastomas) and 356 continuous variables corresponding to the expression data. We start with the classical approach which consists in performing a clustering method on the denoised data estimated with truncated SVD (3) by means of the \pkgFactoMineR package which implements principal components methods, unsupervised clustering methods and visualization tools. First, we estimate the rank by cross-validation (Josse11b) with the function \codeestim_ncp. Then, we perform the truncated SVD at using the \codePCA function. Finally, we use a hierarchical clustering on the matrix with the \codeHCPC function. The number of clusters is automatically determined based on the increase of between-clusters variance (Paghuss10)(page 185). More details on these functions can be found in FactoJSS. Figure LABEL:fig:cluster (left) represents the scores of the observations on the first two dimensions of variabilities (the matrix UD). The points are then coloured with respect to their clusters.

R> data(tumors) R> nb.ncp <- estim_ncp(tumors[ , -ncol(tumors)]) R> res.pca <- PCA(tumors, ncp = nb.ncp