The value of Side Information in the Secondary Spectrum Markets

Abstract

We consider a secondary spectrum market where primaries set prices for their unused channels. The pay-off of a primary then depends on the availability of channels for its competitors, which a primary might not have information about. We study a model where a primary can acquire this competitor’s channel state information (C-CSI) at a cost. We formulate a game between two primaries, where each primary decides whether to acquire the C-CSI or not and then selects its price based on that. We first characterize the Nash Equilibrium (NE) of this game for a symmetric model where the C-CSI is perfect. We show that the payoff of a primary is independent of the C-CSI acquisition cost. We then generalize our analysis to allow for imperfect estimation and cases where the two primaries have different C-CSI costs or different channel availabilities. Our results show interestingly that the payoff of a primary increases when there is estimation error. We also show that surprisingly, the expected payoff of a primary may decrease when the C-CSI acquisition cost decreases or primaries have different availabilities.

Index Terms:

Nash Equilibrium, Secondary Spectrum Access, Channel State estimation, Price Competition.I Introduction

| Notation | Significance |

|---|---|

| The highest price that a secondary is willing to pay for an available channel. | |

| Availability probability of primary . | |

| In the basic model . | |

| The C-CSI acquisition cost for primary . | |

| In the basic model . | |

| The C-CSI estimation accuracy. | |

| The transaction cost which the primary incurs only when it sells its channel. |

Spectrum sharing where license holders (primaries) allow unlicensed users (secondaries) to use their channels can enhance the efficiency of the spectrum usage. However, secondary access will only proliferate when it is rendered profitable to the primaries. We investigate a secondary spectrum market where there are competing primaries that want to lease their unused channels to secondaries in lieu of financial remuneration. In our setting, primaries can be wireless service providers or any other intermittent users of the spectrum (e.g. government agencies, TV broadcasters) or the infrastructure (e.g. access point owners) and secondaries can also be service providers or individual users. We assume the market operates in fixed time intervals. At the start of each interval, the primaries announce prices for their channels if they are available111The time-scale at which this market operates could range from seconds to hours depending on the underlying technology. The key assumption being that if a primary puts its channel up for sale, it commits to allowing the secondary to use that channel for the next interval.. Each secondary seeks to buy an available channel with the lowest price.

The availability of a channel varies randomly because of the usage statistic of a primary, e.g if a primary need to use a channel to serve its own traffic, the channel will be unavailable for sale222Availability could also depend on channel fading or interference levels over the time-scale at which the market operates.. When its channel is available, the profit or payoff that a primary can obtain will depend in part on the availability of the channels of other primaries in the market.

We consider a scenario where the primary can estimate the competitor’s channel state information (C-CSI) by incurring a cost. This C-CSI provides an estimate of the competitor’s channel state (CCS), which indicates if it is available for sale or not. The motivation behind considering such a scenario is the growing interest in incorporating spectrum measurements into various approaches for dynamic spectrum access. For example, a recent proposal is made by FCC to sense the occupancy of the 3.5 GHz band by environmental sensing capability (ESC) operators (e.g. Google, KeyBridge)[1]. The cost to acquire the C-CSI can be incurred in several ways. For example, i) the primary could need to devote resources throughout the location to sense the competitor’s channel and estimate its traffic patterns; this could cost the primary in terms of power consumption or processing resources. ii) Alternatively, the primary could incentivize users to collaboratively crowdsource such measurements using their own wireless devices (see e.g. [2, 3]). Here the cost to the primary is the payments to incentivize participation. iii) Finally, these estimates could be performed by a ‘third party’ that deploys a network of wireless spectrum sensors as in [4]333Another example of such a 3rd party sensing network is the ESC operators (e.g. Google, KeyBridge) in the 3.5 GHz as mentioned before. and uses these to sell “forecast” of the CCS to a primary. Additionally, there may be errors in this estimation due to traffic variability, noise and hidden terminal effects. Characterizing how the C-CSI costs and errors impact the competition between the primaries is the goal of this paper.

We now illustrate the challenges involved in analyzing this setting. A primary with an available channel needs to select whether to acquire the C-CSI and the price for its channel. However, while taking its own decision, a primary does not know whether its competitors decided to acquire the C-CSI or not. The importance of C-CSI is immense. For example, if the competitors’ channels are not available, a primary can sell its channel at the highest possible price due to a lack of competition. This suggests that a primary would want to acquire C-CSI. However, if the other primaries are available, the primary may have to select lower price because of the competition. This lower price may not be enough to cover the C-CSI acquisition cost. Hence, it is not a priori clear whether primaries will acquire the C-CSI.

The inherent uncertainty in the competitors’ decisions also complicates the pricing strategy of a primary. We now illustrate this when there are two primaries. If one primary () knows that the channel of the other primary () is available, ’s pricing decision depends on if also knows ’s availability or not, as this will in turn impact the competition it faces. On the other hand, if primary does not know ’s channel state, then it must balance between selecting a lower price, which will increase its probability of selling should the competitor be present, and a higher price, which will give it more revenue should be absent.

To address these issues, we focus on a market with two primaries (though some extensions to more primaries are addressed in Section VII). The restriction to two primaries is mainly done to simplify our analysis:- however, there are practical situations where this is a reasonable assumption444For example, if the primaries are wireless service providers, then in many places this market is dominated by only two such providers. Hence, wireless market with two players have been considered in [5, 6, 7, 8]. We study a non-cooperative game with the primaries as players. When its channel is available, each primary decides i) whether to acquire the C-CSI or not, and ii) a price. If the primary acquires the C-CSI, it may select different prices depending its estimate of the CCS. When the primary does not acquire the C-CSI, it has to select a price irrespective of the CCS. We characterize the Nash equilibrium (NE) strategies.

Basic Model: We first consider a basic model (Section LABEL:sec:basic_model) where the acquired C-CSI is equal to CCS. The channel availability probability and the C-CSI acquisition costs are the same for both the primaries. We introduce a class of strategies (Definition 4) and show that the NE strategy profile is of this form. In a strategy, a primary acquires the C-CSI, when the cost is below with probability (w.p.) , and does not acquire the C-CSI, otherwise. We allow the primaries to potentially randomize their prices given the C-CSI acquired. Using this characterization, several interesting properties of the NE are then shown. First, is increasing as the C-CSI cost decreases, but a primary never acquires C-CSI w.p.1. Second, increases in the uncertainty of the CCS. Third, we have the following counter-intuitive result: the ability to acquire C-CSI does not impact the expected payoff of a primary. Finally, we show that the equilibrium pricing strategy is indeed to randomize and we characterize the resulting price distributions.

Impact of the Estimation Error: We, subsequently, investigate the impact of C-CSI errors on the decision, payoff and the pricing strategy of a primary (Section IV). Conventional wisdom might suggest that errors in estimating the CCS should decrease the payoff. However, this is not definite because errors might also make primaries less aggressive in lowering their prices to compete against competitors when they acquire C-CSI, which could lead to higher profits. Interestingly, we show that this is indeed the case, i.e., the primary’s pay-off is higher with C-CSI errors.

We show that there again exists a type NE strategy, where the threshold decreases as the estimation error increases. Intuitively, increases in the error in estimating the CCS makes the acquisition of the C-CSI less attractive for larger costs. The probability again increases as the C-CSI cost decreases, but now the expected pay-off of a primary also increases.

The NE pricing strategies are again randomized. In the basic model, when the primary accurately estimates that the competitor’s channel is unavailable, it selects the highest possible price w.p. . However, when there are errors in C-CSI, the competitor’s channel may be available even when it estimates that it is not. Thus, a primary also selects a lower price.

Impact of Unequal C-CSI acquisition costs: We also investigate the setting where C-CSI acquisition costs may differ across the primaries (Section V). We show that strategies are NE for primary . Each primary has the same threshold but different probabilities , where is larger for the primary with the lower cost. The expected payoff of the primary with a higher cost is the same as it would have obtained if there was no provision of acquiring the C-CSI. In contrast to the basic model, the expected payoff of the primary with a lower cost is higher compared to the other primary.

The primaries again randomize their prices, where the primary with a lower cost chooses its price from a larger range when it acquires the C-CSI (and a smaller range when it does not). In contrast to the basic model, the primary with a higher acquisition cost also has a point mass at the highest price in the price distribution when it does not acquire the C-CSI, i.e., the primary with a higher acquisition cost selects higher prices with higher probabilities when it does not acquire the C-CSI.

Impact of heterogeneous availabilities: We next consider the impact of different availability probabilities across the primaries (Section VI). Again, we show that the NE strategy is of the form . In this case, the primary with a higher availability has a higher threshold and a higher probability of acquiring the C-CSI. The expected pay-off of the primary with a higher availability is greater, and interestingly, the expected pay-off of the other primary decreases as the cost for acquiring the C-CSI decreases which negates the conventional wisdom that the payoff of a primary should not decrease as the cost of acquiring the C-CSI decreases. We also show that the pricing strategy of each primary is randomized over a given interval. However, the primary which has a higher availability probability selects a price from a larger (smaller, resp.) interval when it acquires (does not acquire, resp.) the C-CSI.

Related Literature: Price selection in oligopolies has been extensively investigated in economics (dating back to the classic work of Bertrand[9]) as well as in the wireless setting. For wireless applications, we divide the entire genre of works in two parts: i) Papers in which prices are set via an auction (e.g. [10, 11]), and ii) Papers, such as ours, which model price competition as a non co-operative game ([12, 13, 14, 15, 16, 17, 18, 19, 20, 21, 22, 23, 24, 25, 26, 27, 28, 29, 30, 31, 32]). To the best of our knowledge, this paper is the first to include the option of acquiring the C-CSI in the strategy space of the players. Additionally, compared to the first category of papers, our model is readily scalable and a central auctioneer is not required. Most of the papers in the second category considered that the primary is aware of the competitor’s channel state, which is also the case in the classic Bertrand model [9]. The exceptions are some recent papers [26, 27, 33, 28, 30] which considered that the primaries can not acquire the C-CSI, so that each primary selects its price not knowing the CCS555 [30] considered that each player has private information such as capacity which is unknown to the competitor. Thus, this setting is equivalent to the setting where a primary can not know the channel availability of its competitor.. In contrast, we consider that primaries have the option of acquiring the C-CSI. A primary now needs to judiciously decide whether to acquire the C-CSI and selects a price based on the result of this decision. In our setting, a primary (, say) is also unaware whether the other primary has acquired the CSI of , while in [26, 27, 33, 28, 30] the primary knows that its channel state is unknown to other primaries. Naturally, these papers did not consider the impact of the C-CSI acquisition costs, estimation error and different channel availability probabilities.

II System Model

We consider a secondary spectrum market with two primaries (players) and one secondary666If there are more than one secondary, then the decision of the primary is trivial, it will always sell its channel, thus, it will select the highest possible price and will never acquire the CSI. Our model can also accommodate the setting where the number of secondaries is not known a priori.. We first provide the basic system model in Section II-A and subsequently, we specify certain generalizations of the model in Section II-B. Commonly used notations are given in Table I.

II-A Basic Model

We consider a model in which spectrum leases occur over a sequence of fixed time-slots and focus on one such time-slot777Of course, in practice primaries and secondaries may take a longer term view, requiring a dynamic game model, but we leave such considerations for future work.. The duration of a time-slot could range from minutes to hours depending on the underlying technologies and other considerations (e.g., the overhead in running the market). Here the main consideration is that if a primary announces a price for its channel, it commits to allowing secondary usage of the channel for the next time-slot. The availability of a primary’s channel for sale will depend in part on the primary’s own traffic. We define a channel to be in state if it is available and otherwise, it is in state . 888Availability could also depend on the rate available to a secondary being large enough, which in turn might depend on estimates of fading and interference levels over the next time-slot. These can also be viewed as part of the CCS, though in such cases a better model might be to allow for the state of the channel to vary with the rate as in [27, 33] (see also Sect. VII). Each primary’s channel is available w.p. , where and is common knowledge. If C-CSI is not acquired, a primary is unaware of the realized state of its competitor.999In other words, this is viewed a Bayesian game in which the type of a primary is its channel state, and is the belief that each primary has about the type of its competitor, where here all beliefs are consistent and reflect the true type distribution.

If a primary’s channel is available, the primary can sell it for secondary use during the next time slot. In this case, it decides whether to acquire the C-CSI before deciding the price for its available channel. For example, if the market opens at time , then at time , a primary decides whether to acquire the C-CSI or not. By acquiring the C-CSI, a primary obtains an estimate of the competitor’s channel state (CCS) for the entire duration of the slot. The C-CSI estimation is accurate and thus, a primary knows the exact CCS. The primary incurs a cost if it estimates the C-CSI.101010Note that a primary (specially, if it is a wireless service provider) may already have some knowledge of its competitor (especially long-scale trends obtained via market research). However, in our scenario the primary needs to estimate the CCS on a smaller time scale (i.e., the slot duration at which the market operates). This short time-scale CCS is not readily available to operators. Hence, the primary needs to incur a separate cost to acquire the C-CSI.

Each primary then decides its price and posts it to the secondary at the beginning of the slot.111111Note that if the channel of a primary is unavailable, then the secondary will never buy the channel irrespective of its price If the channels of both the primaries are available for sale, then, the secondary will buy the lower priced channel. If the two available channels have the same price, then a secondary will choose either of them w.p. .

II-B Generalization of the Model

II-B1 Estimation Error

When a primary acquires the C-CSI, it estimates the CCS for the entire slot duration. Because of the channel fading, noise in the environment, the random variation of the usage pattern of the channel, that estimation may be erroneous. In Section IV, we consider such a setting where the estimated CCS is accurate only with probability . Specifically, if a primary acquires the C-CSI, then, it will estimate that the CCS is (, resp.) w.p. if the original CCS is (, resp.). Without loss of generality, we assume that121212If , then there is no point of estimating the CCS as the setting becomes equivalent to the setting where a primary does not know the channel state of its competitor. . Note that when , there is no estimation error and a primary accurately estimates the CCS, thus, the basic system model is a special case of this model.

II-B2 Different Costs of Acquiring the C-CSI

In Section V we generalize the basic model to allow each primary to incur a different cost, for acquiring the C-CSI.

II-B3 Different Channel Availability Probabilities

We generalize the basic model in Section VI by allowing each primary to have different availabilities .

II-C Payoff of a primary

If primary sets its price at and it decides to acquire the C-CSI, then, its payoff is

Note that when both the primaries incur the same cost to acquire the C-CSI, then we have .

When a primary does not acquire the C-CSI, then its payoff at price is

II-D Strategy of a Primary

If the channel of a primary is available131313If the channel of the primary is unavailable, then its decision is immaterial., it will take a decision where denotes incurring the cost to estimate the C-CSI and denotes not acquiring the C-CSI. Primary also sets a price for its available channel. Note that the primaries’ decisions are simultaneous so that no primary is aware of the decision of its competitor when making its own decision. If a primary selects , it selects a price using either a distribution or depending on whether it estimates the CCS as or , respectively. If a primary selects , then it does not acquire the C-CSI, so it only selects its price using a single distribution .

Definition 1.

The strategy of primary is where when , when , and is a probability mass function over the strategies .

The strategy of the primary other than is denoted as .

Definition 2.

denotes the expected payoff of primary when its channel is available, it uses strategy and the other primary uses strategy141414Note that we consider the expected payoff of a primary as the expected payoff conditioned on the channel of the primary being available. Naturally if the channel of the primary is unavailable, it will attain a payoff of and so its unconditional expected payoff is simply this quantity scaled by . .

II-E Solution Concept

We consider a non-cooperative game where each primary only wants to maximize its own expected payoff. We use the (Bayesian) Nash Equilibrium as a solution concept.

Definition 3.

A Nash equilibrium (NE) is a strategy profile such that no primary can improve its expected payoff by unilaterally deviating from its strategy151515In the language of Bayesian games, the expectation here is with respect to a player’s belief about the availability of the competitor’s channel (which as we have noted can be viewed as the competitor’s type). The belief about the competitor’s type (i.e. availability) also changes depending on the information the primary has. Given the consistent belief assumption, we simply refer to the resulting Bayesian Nash equilibrium as a NE in the following. [34]. Thus,

| (1) |

A strategy profile is symmetric if for any pair of players and .

III Results of the Basic Model

We, first, investigate the system model depicted in Section II-A. Note that this setting is a special case of each of the more generalized settings depicted in Sections II-B1,II-B2, and II-B3.

III-A Goals

Acquiring the CSI of the competitor has potential advantages. For example, if a primary knows that the channel of its competitor is unavailable, then, the primary can select a high price because of the lack of competition. However, a primary has to incur a cost to acquire the CSI. Thus, conventional wisdom suggests that as the cost of acquiring the CSI decreases, a primary should more frequently acquire the CSI and thereby gain a higher payoff in an NE. However, conventional wisdom is not definitive because of the following. The payoff of a primary (, say) also inherently depends on the decision of other primary (,say). If the primary decides to acquire the CSI of primary , then primary selects a lower price when the channel of primary is available, thus, in response161616In an NE, each player selects a best response strategy in response of the strategy of the other player., the primary also selects a lower price in the NE which reduces its payoff. On the other hand, acquiring the CSI of the competitor is also not ruled out either. This is because a primary may acquire the CSI of its competitor and take advantage of the extra information. Thus, it is not apriori clear whether a primary will acquire the CSI of its competitor. It is also not clear even if a primary decides to acquire the CSI at what values of it will do so. We resolve all the above quandaries.

The inherent uncertainty in the competitor’s decision also complicates the pricing strategy of the primary. If primary knows that the channel of primary is available, its pricing decision still depends on if primary also know that its channel is available; if not then the primary may randomize among multiple prices, enabling primary to charge a higher price. If primary knows that the channel of primary is available, primary selects a lower price, in response primary also selects a lower price. On the other hand, if the primary does not know the channel state of its competitor, then it may have to randomize over prices from an interval which is not known apriori. Thus, it is also not apriori clear how a primary will select its price. We also characterize NE pricing strategies.

III-B Results

III-B1 A class of Strategy for selecting

We first define a class of strategies for selecting .

Definition 4.

A strategy is a strategy where a primary selects

for . The probability may be a function of .

We show that in the basic model as well as in different generalizations, the NE strategy is a strategy where is a strictly decreasing function of . We also characterize , and in different generalizations of the basic model.

It is intuitive that in an NE, a primary will choose with a probability where is a decreasing function. It is also intuitive that when as the maximum expected payoff that a primary attains is . We, however, show that can be even for smaller values of . We also show that never becomes for any positive value of . We fully characterize the function and the value of the threshold above which a primary does not select .

III-B2 Main Results

Our main results are–

-

•

Regardless of the cost , there is no NE where both the players have full knowledge of each other’s channel states w.p. (Theorem 1). There is no NE where one primary has the complete knowledge of the channel state of its competitor, but the other does not (Theorem 2). Thus, a primary can only select , if the other primary randomizes between and .

-

•

We show that the unique NE strategy is a strategy where (Theorems 3 and 4). Note that increases when the uncertainty of the availability of the channel increases i.e. becomes closer to . Intuitively, when either is large or small, the uncertainty of the competitor’s channel decreases, thus, a primary selects for higher values of . We also characterize the value of as a function of and show that is a decreasing function of .

-

•

The expected payoff that a primary attains in any NE strategy profile is (Theorems 3 and 4). Thus, the expected payoff of a primary is independent of the value of . [26] shows that when a primary can not acquire the CSI of the competitor, then its payoff is . Thus, the provision of acquiring the CSI of the competitor does not impact the expected payoff of a primary.

-

•

Theorem 3 shows that when each primary selects , then each primary randomizes its price from the interval . Theorem 4 shows that when a primary selects (, resp.) and the channel of its competitor is available, then the primary selects its price from the interval (,resp.). Intuitively, as the uncertainty of the availability of the competitors increases, a primary selects a higher price. We also show that . Thus, a primary selects its price from a larger interval when it randomizes between and .

We now describe the results in details. We first state some price distributions and which we use throughout.

| (2) | ||||

| (3) | ||||

| (4) |

III-C Does there exist an NE where both primaries select ?

Theorem 1.

There is no Nash equilibrium where both the primaries choose w.p. .

Outline of the proof: Assume both players choose , so that they know each other’s channel state. Thus, the competition becomes similar to Bertrand Competition[34], i.e. if the channel of its competitor is unavailable, then the primary will set its price at the , otherwise it will set its price at the lowest value . Now, the probability with which the channel of a primary is available is . Thus, the expected payoff of a player is

| (5) |

Now consider the following unilateral deviation for a primary: Primary selects and sets its price at w.p. . The channel of primary will be bought when the channel of primary is not available for sale. Since primary decides not to incur the cost , thus, its expected payoff is

| (6) |

This is strictly higher than (5). Hence, the strategy profile can not be an NE.∎

The above theorem means that there will be at least one primary which will be unaware of its competitor’s channel state with a non-zero probability.

III-D Does there exist an NE where one selects and the other selects ?

Theorem 2.

For positive , there is no NE where a primary selects w.p. and the other selects w.p. .

First, we provide the intuition behind the result. The primary (say, ) which selects tends to select lower prices with higher probability when it knows that the channel of the other primary is available. Thus, in response the primary (which selects ) selects higher prices with higher probabilities in order to gain a high payoff in the event that the channel of primary is unavailable since it knows that its probability of selling is very low in the event that the channel of primary is available. The primary can then gain a higher payoff by selecting and higher prices as it does not have to incur the cost . Hence, the primary has an incentive to deviate from its own strategy. The detailed proof is given below.

Proof.

Without loss of generality, assume that primary selects and primary selects . First, we discuss the pricing strategies of primaries and and calculate the expected payoff of primary , subsequently, we show that primary has an incentive to deviate.

When primary knows that the channel of primary is not available, then primary will be able to sell its channel at the highest possible price, thus, it will select w.p. and its payoff if . The above event occurs w.p. .

Now, we consider the case when the channel of primary is available. While deciding its price, primary only knows that the channel of primary is available w.p. . However, while selecting its price primary knows that the primary will know the channel state of primary if the channel of primary is available. Hence, when primary knows that the channel of primary is available, then the pricing decision becomes equivalent to the setting where primary knows that the channel of primary is available w.p. and primary knows that the channel of primary is available w.p. . The NE pricing strategy in the last setting has been studied in [26] and using Theorem 2 in [26] we have

Lemma 1.

By Lemma 1 when the channel of primary is available for sale, then expected payoff of primary at any

| (7) |

At , the payoff of primary will be strictly less than the expression in (7). On the other hand at , primary will get strictly a lower payoff compared to the payoff at a price just below since has a jump at . Hence, the maximum expected payoff to primary in this case is .

Thus, the expected payoff of primary is

| (8) |

Now, we show that if primary selects , then the primary can achieve strictly higher payoff. For , the expected payoff of primary at is

| (9) |

Thus, for every positive there exists a small enough such that at , it will attain strictly higher payoff than (8). Hence, if primary selects and the price w.p. then primary attains a strictly higher payoff. The result follows. ∎

III-E Does there exist an NE where both primaries select ?

Theorem 3.

Suppose that each primary selects the strategy ( is given in (2)).

The above strategy profile is the unique NE when .

However, the above is not an NE when .

We provide an intuition behind the result. When is high, if a primary selects , then it has to incur high cost compared to the potential gain it will achieve, thus, no primary has any incentive to deviate. When is low, if a primary deviates and selects , then it can gain higher payoff by taking advantage of the CSI of the other primary. Thus, the strategy profile fails to be an NE when is low. We prove that the strategy profile is an NE in Theorem 5. We show the uniqueness in Appendix.

Remark: The result shows that when the cost is high, in an equilibrium both the primaries select . It is obvious that if , then a primary will never opt for . The above theorem shows that even if , primaries will select .

III-F Does there exist an NE when is low?

Note from Theorems 1, 2 and 3 that if is low, then there is no NE strategy where each primary selects either or w.p. . Thus, at least one primary must randomize between and when is low.

Now, consider the following price distributions

and

where and are

| (10) |

Note that both and are continuous. In the following, we show that a strategy profile based on these distribution is a NE when is small enough.

Theorem 4.

Consider the following strategy profile: Each primary selects w.p. and w.p. where . When choosing , the primary selects its price according to when it knows that the channel state of the other primary is available, otherwise it selects w.p. . When choosing , the primary selects price according to .

The above strategy profile is the unique NE if .

The expected payoff that a primary attains in the NE strategy profile is .

The proof of the strategy profile is an NE is similar to the Theorem LABEL:thm:errormixedstrategy where we consider the CCS estimation may not be accurate. We prove the uniqueness in the Appendix.

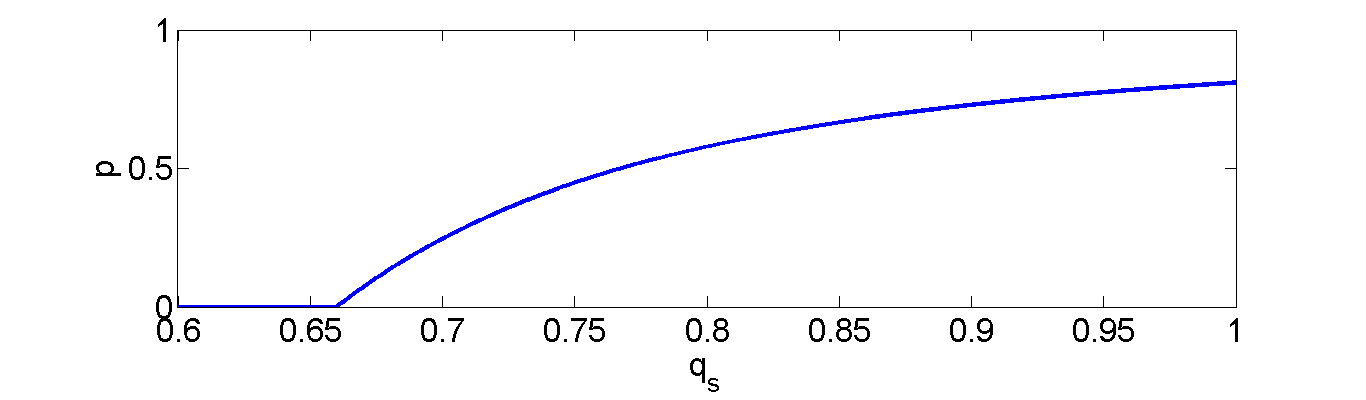

Example 1.

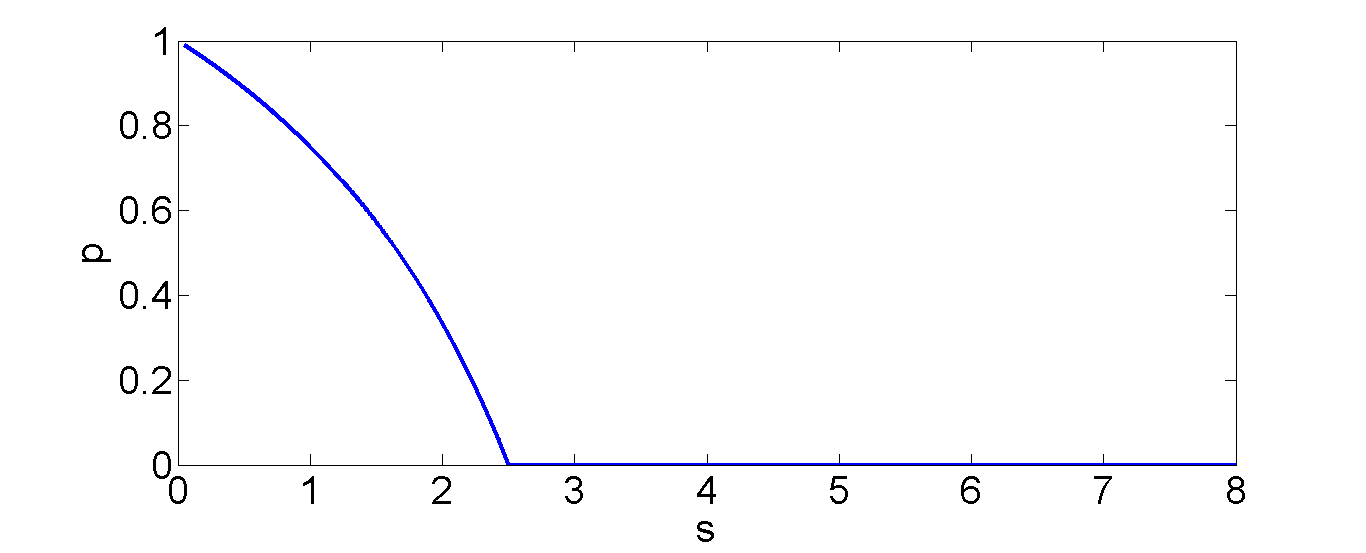

Discussion: Note from the above theorem that when is low there exists an NE where both the primaries randomize between and . It is also easy to discern that as decreases, increases and as , (Fig. 3). Thus, when the cost of obtaining the competitor’s CSI decreases, then the primaries will be more likely to acquire that information.

Note that is the measure of uncertainty, if the uncertainty if higher (i.e. ), then the threshold is also higher. A primary never selects if . By differentiating, it is easy to discern that when , then is maximized at (Fig. 3). Since , . Note also that decreases as increases. Intuitively, when increases, primaries tend to select only when the uncertainty of the availability of channel increases.

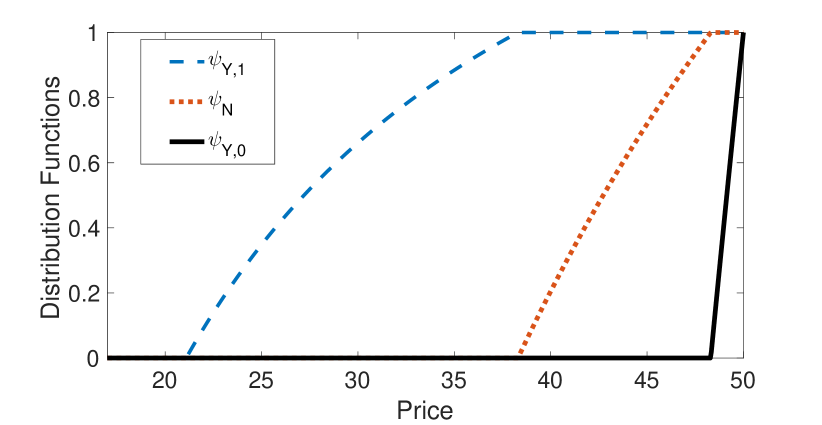

The support set of is and is . Thus, under a primary selects lower prices when the primary knows that the channel of its competitor is available compared to the setting where the primary is not aware of the channel state of its competitor. This is because in the former case the uncertainty of the appearance of the competitor is reduced.

Since increases as decreases, thus, from (10), increases as decreases. Thus, a primary selects its price from a larger interval when decreases. Also note that also increases as decreases. Thus, the support set of increases as decreases.

Theorems 3 and 4 imply that the expected payoff of a primary is . Note that when the primaries always know each other’s channel states, the competition becomes equivalent to the Bertrand competition [34] and the expected payoff is 171717It can also be obtained from (5). and when the primaries are constrained to select only , the expected payoff is again [26, 27]. Hence, our result also builds the bridge between the two extremes. Specifically, it shows that the cost or the availability of the competitor’s CSI does not impact the expected payoff.

III-G Welfare of the Secondaries

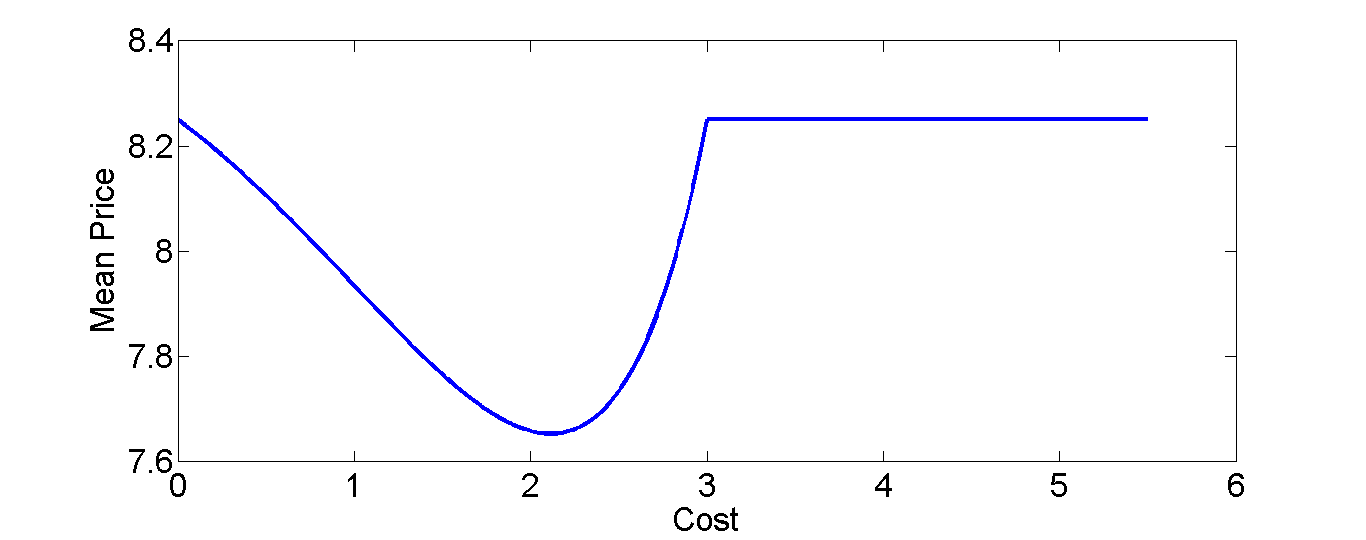

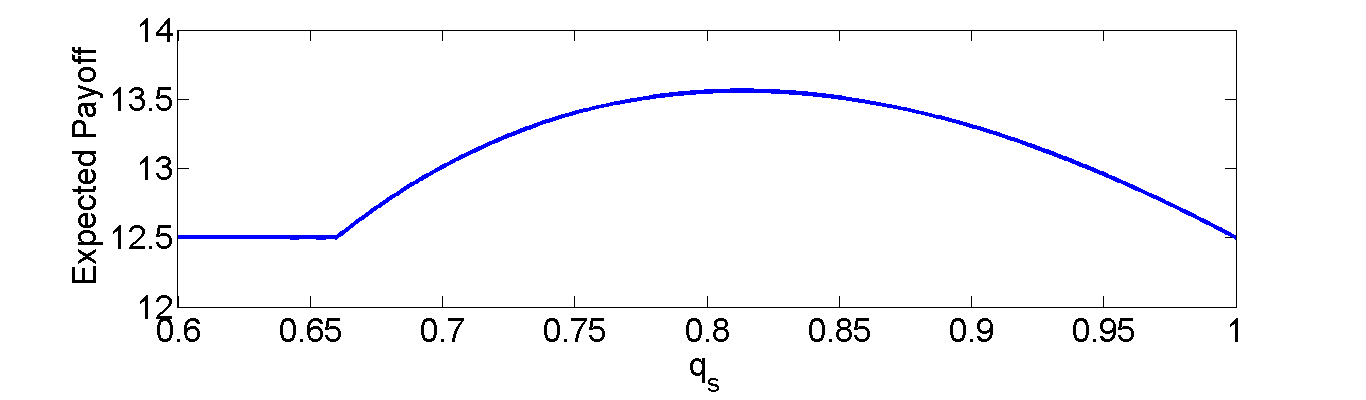

Fig. 4 shows the variation of the expected price paid by the secondary. Initially, the expected price decreases as the C-CSI acquisition cost increases. The expected price reaches the minimum value, and then increases with the increase in . When i.e. the primaries select w.p. , the expected price is the same in the setting with i.e. when the primaries select w.p. . Fig. 4 shows that the expected price paid by the secondary is minimum at a positive cost; the minimum is not attained when which negates the conventional wisdom. Note that the expected payoffs of the primaries are independent of the cost . Thus, the expected social welfare which is the sum of the expected payoffs of the primaries and the expected utility of the secondary (which is the negative of the price paid by the secondary) is in fact minimum at .

IV Impact of Error in the Estimation

We, now, investigate the impact of the estimation error. Towards this end, we consider the system model specified in Section II-B1. Specifically, if a primary estimates the CSI of its competitor, the estimation is accurate only with probability ().

IV-A Goals

The impact of error in the estimation on the decision and the payoff of each primary is not apriori clear. The conventional wisdom suggests that the error in the estimation should decrease the payoff. However, the conventional wisdom is not definitive because of the following. If there is an error in estimating the channel state of the competitor, then, the primary selects a higher price even when it estimates that the channel state of the primary is , thus, in response, the primary selects a higher price without reducing the winning probability, which may increase the payoff. It also remains to be seen whether the expected payoff of a primary is independent of like in the basic model. Even if the selection of belongs to the class (Recall Definition 4), the dependence of and on the estimation error is also not apriori clear.

The pricing strategy also depends on the estimation error. For example, when the estimation error is , then a primary selects a high price when the estimated channel state of the competitor is as the channel of the competitor is unavailable. However, when there is an error in estimated channel state, the actual channel state may not be even when the estimated channel state is . Thus, a higher price may reduce the probability of winning and a lower price may reduce payoff in the event of a selling. Our goal is to characterize the pricing strategies of the primaries.

IV-B Main Results

We now summarize our main findings in this section here–

-

•

We show that the NE strategy is a strategy (Definition 4) with (Theorems 5, 6). Note that in the basic model, we have also seen type strategy for selecting . However, due to the estimation error, the threshold is different compared to the basic model. The threshold decreases as decreases i.e. primaries select w.p. for larger values of . Intuitively, the uncertainty regarding the channel state increases as the estimation error increases, thus, the uncertainty of the channel state increases even when primary selects . A primary is more reluctant to select . Hence, primary selects w.p. for smaller values of . We also characterize as a function of and show that decreases monotonically with .

-

•

The expected payoff of each primary is strictly higher than when a primary randomizes between and (i.e. ) and . In the basic model, we have shown that the expected payoff of each primary is irrespective of the value of . Thus, the error in estimation increases the payoff of each primary which negates the conventional wisdom that expected payoff of a primary should increase as the estimation error decreases. The payoff of each primary also increases with the decrease in when . Hence, in contrast to the basic model, the expected payoff of each primary depends on the value of .

-

•

In NE pricing strategy:

-

–

When a primary selects and estimates that the channel state of its competitor is , then it selects its price from the interval .

-

–

When a primary selects , then it selects its price from the interval .

-

–

When a primary selects and estimates that the channel state of its competitor is , then it selects its price from the interval .

If , a primary always selects w.p. when the primary selects and the channel state of the competitor is since the primary will always be able to sell its channel because of the unavailability of its competitor. However, when , there is a potential error in the estimation, thus, a primary randomizes among prices from an interval even when the primary estimates that the channel state of its competitor is . Also note that when a primary estimates that the channel state of its competitor is (,resp.), then its competitor is more likely to be available (unavailable, resp.), hence, the primary selects lower (higher, resp.) prices compared to the setting where a primary selects .

-

–

IV-C High

First, we state some results which we use throughout this section. Note that when a primary decides to estimate the CSI of its competitor, it estimates the channel state of its competitor is w.p. and the primary estimates the channel state of its competitor is w.p. . Note that when , then the above probabilities becomes and respectively. If a primary estimates that its competitor’s channel state is , then the actual channel state is w.p.

| (11) |

Similarly, if a primary estimates that its competitor’s channel state is , then the actual channel state of its competitor is w.p.

| (12) |

Note that when , then both the above probabilities become .

Our main result in this section shows that

Theorem 5.

There exists a NE where each primary selects w.p. if . In the NE pricing strategy, each primary selects its price according to (described in (2)). The expected payoff of each primary is .

Proof.

We show that a primary does not have any profitable unilateral deviation when the other primary follows the strategy prescribed in the theorem. Towards this end, we, first, show that under the maximum expected payoff of a primary is (Step i). It is attained when the primary follows the strategy (Step ii). Subsequently, we show that if the primary selects , then its expected payoff is at most which will show that the primary does not have any profitable unilateral deviation (Step iii).

Step i: At any price the expected payoff of a primary is

| (13) |

A price strictly less than will fetch a payoff strictly less than (by (4)). Thus, the maximum expected payoff of a primary under is .

Step ii: Note from (13) that a primary attains the maximum expected payoff when it selects its price from the interval .

Step ii: Now, we show that if primary selects , it can not get a strictly higher payoff when . Towards this end, we show that when a primary selects and estimates that the channel state of the other primary is , then it will attain a maximum expected payoff of (Step ii.a). Subsequently, we show that if the primary selects estimates that the channel state of the competitor is , then it will attain a maximum expected payoff of (Step ii.b.). Finally, we show that the expected payoff of the primary is at most when it selects (Step ii.c.).

Step ii.a: Suppose that the primary selects and estimates that the channel state of primary is . Using (11) the expected payoff of primary at any price is

| (14) |

Note that . Since when , thus, the above is maximized at , hence, the maximum expected payoff that primary can attain when it estimates the channel state of its competitor is is

| (15) |

Step ii.b: Now, suppose that the primary estimates that the channel state of primary is . Using (12) the expected payoff of primary at any price in this case is

| (16) |

The above is maximized at . Hence, the maximum expected payoff that a primary can attain is

| (17) |

Step ii.c: Note that a primary estimates that the channel state of primary is w.p. and the channel state of primary is w.p. . The primary also incurs the cost of when it selects . Hence, from (IV-C) and (IV-C) the maximum expected payoff that primary can attain by selecting is

| (18) |

However, since , thus the maximum expected payoff that a primary can attain by selecting is . Hence, a primary does not have any profitable unilateral deviation. ∎

Note that the threshold increases as increases. Intuitively, as increases, the uncertainty regarding the channel state of the competitors reduces, thus, a primary tends to select for a smaller range of the values of .

The expected payoff of each primary is identical and equal to . Since both the players select , thus, the expected payoff does not depend on in this case.

IV-D Low

Now, we show that there exists a NE where each primary randomizes between and when . Towards this end, we introduce some distribution functions parameterized by . The significance of is shown later.

| (19) |

| (20) |

and, when , then

| (21) |

if , then

| (22) |

where is the heaviside step function or unit step function and

| (23) |

and

| (24) |

It is easy to discern that all the above distribution functions are continuous when . When , then only is discontinuous which has a jump of at . Also note that the structures of and are similar (i.e. variation with is the same). However, their support sets, the scaling parameters (i.e. ), and the constants (i.e , ) are different.

When , the values of the parameters in (IV-D) are greatly simplified which are given by–

| (25) |

Thus, and are the highest when . Intuitively, when , a primary knows that the channel state of its competitor is unavailable w.p. if the primary estimates that the channel state of the competitor is . Thus, the primary selects w.p. .

Now, we are ready to state the main result of this section.

Theorem 6.

Consider the following strategy profile: Each primary selects w.p. and w.p. where satisfies the following equality

| (26) |

where and are given in (IV-D). While selecting , each primary selects its price from (given in (19)) if the estimated channel state of the other primary is and each primary selects its price from (given in (IV-D)) if the estimated channel state of the other primary is . While selecting , each primary selects its price using (given in (IV-D)).

The above strategy profile is an NE when . The above strategy profile is unique in the class of symmetric NE strategies. The expected payoff that each primary gets is .

Discussion: Note that when , we know from Theorem 4 that the strategy profile is unique one among all strategy profiles not only symmetric ones. There is no equilibrium where both the players select w.p. even when (we have already shown the above for in Theorem 1).

Now, we show that there exists a unique solution of (26) in in the interval when .

Observation 1.

There exists a unique solution in of the equation (26) when . As decreases increases.

Proof.

First noe that (26) can be written as

Using (IV-D) we can rewrite the above as

| (27) |

First, we show that the left hand of (IV-D) is strictly increasing in (Step i). Next, we show that when , the left hand side of (IV-D) is less than the right hand side and when , the left hand side of (IV-D) is greater than the right hand side (Step ii). Since the left hand side of (IV-D) is continuous in and strictly increasing in , there exists a unique solution of (IV-D). The last part easily follows as the right hand side of (IV-D) decreases with , the left hand side of (IV-D) is strictly increasing in and independent of . Now, we show steps i and ii.

Step i: By differentiating the left hand side of (IV-D) we can show that

| (28) |

is strictly increasing in when . On the other hand, it is easy to discern that is non-decreasing in when . Thus, the left hand side of (IV-D) is strictly increasing in .

Step ii: When , then the value of left hand side of the equation (IV-D) is

| (29) |

Now, . Since , thus, the left hand side of (IV-D) is less than the right hand side.

Now when , then the left hand side of (IV-D) is

| (30) |

Since , thus, the left hand side of (IV-D) is greater than the right hand side.

Since the left hand side of (IV-D) is continuous function of , thus, by intermediate value theorem there exists a solution in the interval . ∎

Next, we show that the expected payoff of a primary is a strictly greater than when and the payoff increases with the decrease in .

Lemma 2.

When , increases with the decrease in and is strictly greater than when .

Proof.

Now, it is easy to discern that is strictly increasing in when . Now, increases with the decrease in (by Observation 1) when . Hence, is a strictly decreasing function in when .

When , then (by (IV-D)). Since is strictly increasing in when and , hence . ∎

Note from Theorem 6 that the expected payoff attained by a primary under the NE is . From (IV-D) note that when . Thus, the above lemma entails that the expected payoff of each primary increases when there is an error in estimating the channel state of the competitor. This contradicts the conventional wisdom that the payoff should increase with the decrease in error in the estimation. In Section IV-B we have already explained the apparent reason behind this result.

The above lemma entails that the expected payoff increases as decreases when . Note that when , the expected payoffs of primaries are independent of which we have already seen in the basic model (Section LABEL:sec:basic_model).

Note that when , then has a jump of size i.e. a primary will select w.p. as the primary will always be able to sell its channel. However, when , then a primary selects its price using a continuous distribution from the interval where . We have already explained the reason behind this in Section IV-B.

IV-D1 Proof of Theorem 6

Before digging into the details of proof, we state few more results which we use throughout. Note from (IV-D) that

| (31) |

Since , thus, by cross multiplication, it is easy to see that

| (32) |

We show that primary can not gain higher profit by deviating from the strategy prescribed in Theorem 6 when primary follows the strategy prescribed in Theorem 6. This will complete the proof. Toward this end, we first show that when primary selects and it estimates that the channel state of its competitor is , then it will attain a maximum expected payoff of . The maximum expected payoff is attained when it follows the strategy (Step i). Subsequently, we show that under , when the primary estimates the channel state as , then the maximum expected payoff that primary can attain is and it is attained when the primary follows the strategy (Step ii). Subsequently, we show that the maximum expected payoff that primary can attain under is and it is attained when primary follows the strategy (Step iii). Subsequently, we show that when primary selects , then its maximum expected payoff is and it is attained when the primary follows the strategy (Step iv). Finally, we show that the maximum expected payoff of primary is and it is attained if primary follows the strategy profile (Step v).

Step i: Suppose that primary selects and estimates that the channel state of primary is . We show that the maximum expected payoff attained by the primary is and this is attained only when the primary selects its price from the interval . Toward this end, we first show any price in the interval will fetch an expected payoff of (Step i.a.). Subsequently, we show that if primary selects a price from the interval and it will fetch an expected payoff of less than in Step i.b. and Step i.c. respectively. Note that at any price less than will fetch a strictly lower payoff compared to the price at as primary does not select any price lower than or equal to . Thus, this will complete step i.

Step i.a: Here, we are considering the scenario where primary estimates that the channel state of primary is . Under , when the primary estimates that the channel state of primary is , then the probability that the channel state of primary is is

| (33) |

Suppose that primary selects a price in the interval . When the channel state of primary is it will select a price less than or equal to only if it selects , it estimates the channel state of primary as and selects a price less than or equal to .The primary selects w.p. . Now, when the channel of primary is available, then primary estimates the channel state of primary as w.p. and selects a price less than or equal to w.p. . The channel state of primary is with probability given in (33). Hence, the expected payoff of primary when its channel is available and selects a price in the interval is

| (34) |

Step i.b.: Now, suppose that primary selects a price . Note that if the channel of primary is available, it will select a price less than or equal to if if one of the following occurs–i) primary selects and estimates the channel state of primary is , ii) primary selects and selects a price less than or equal to . (i) occurs with probability and (ii) occurs with probability . Since primary estimates that the channel state of primary is , thus, the probability that the true state of the channel of primary is indeed is given by (33). Thus, the probability that the primary will select a price less than or equal to is

Thus, at , the expected payoff of primary is–

| (35) |

Since , the co-efficient is negative. Thus, the above is maximized at . Using (IV-D) , the above expression is thus, upper bounded by

| (36) |

Step i.c: From steps i.a. and i.b. we have already shown that when the maximum expected payoff of primary is at a price in the interval . When , (from (IV-D)). Thus, it shows that when , the maximum expected payoff of primary is indeed

Now, we consider the case where and primary selects price . When the channel of primary is available, then primary selects a price less than or equal to if one of the following occurs–i) it selects and estimates that the channel state of primary is , ii) primary selects , iii) primary selects , estimates that the channel state of primary is and selects a price less than or equal to . (i) occurs with probability since the channel of primary is available. (ii) occurs with probability . (iii) occurs with probability (since the channel of primary is available). On the other hand the probability that the channel of primary is available is given by (33). Hence, the probability that primary selects a price less than or equal to is

Thus, at any price , the expected payoff of primary is

| (37) |

By (32) the co-efficient of is negative, thus, the maximum of the above expression is attained at . Thus, the expected payoff at is upper bounded by expected payoff at . From (IV-D1) (which also gives the expected payoff at ) we have already bounded the expected payoff at which is . Hence, the maximum expected payoff that primary can attain in this case is and it is attained at any price in the interval .

Step ii: Suppose that primary estimates that the channel state of primary is . When , then the channel of primary is unavailable with probability . Hence, primary will attain the highest possible payoff at and the payoff is (by (IV-D)). Thus, we consider the case when . We show that the maximum expected payoff attained by primary is and it is attained at any price in the interval . Towards this end, we first show that any price from the interval will fetch an expected payoff of (Step ii.a.). Subsequently, we show that any price in the interval and will fetch an expected payoff of at most (Steps ii.b. and ii.c. resp.). Any price less than will fetch a payoff which is strictly less than the payoff at , thus, this will complete Step ii.

Step ii.a: When primary estimates that the channel state of primary is , then the probability that the channel state of primary is is

| (38) |

Suppose that primary selects a price in the interval . If the channel of primary is available, then, the primary will select a price less than or equal to if one of the following occurs–i) it selects and estimates that the channel state of primary is , ii) primary selects , iii) primary selects , estimates that the channel state of primary is and selects a price less than or equal to . (i) occurs with probability since the channel of primary is available. (ii) occurs with probability . (iii) occurs with probability (since the channel of primary is available). On the other hand the probability that the channel of primary is available is given by (38) as primary estimates that the channel state of primary is . Hence, the probability that primary selects a price less than or equal to is

Hence, the expected payoff of primary at is

| (39) |

Step ii.b.: Now, suppose primary selects a price in the interval . When the channel of primary is available, then primary selects a price less than or equal to if one of the following occurs–i) primary selects and estimates the channel state of primary is , ii) primary selects and selects a price less than or equal to . (i) occurs with probability and (ii) occurs with probability . Given that the primary estimates that the channel state of primary is , the probability that channel of primary is available is given by (38). Thus, the probability that primary selects a price less than or equal to is given by

| (40) |

Hence, the expected payoff of primary at is

| (41) |

By (32) the above is maximized at . Hence, the maximum possible expected payoff is

| (42) |

Step ii.c.: Now, suppose that primary selects a price in the interval . Now, if the channel of primary is available, then it selects a price less than or equal to if it selects , estimates that the channel state of primary is and selects a price less than or equal to . The above occurs with probability . The probability that the channel state of primary is given that the primary estimates that the channel state of primary is is given by (38). Hence at the expected payoff of primary is

By (32) the above is maximized at . Thus, the expected payoff at any is upper bounded by the expected payoff at . Now, from (IV-D1) (which also gives the expected payoff at ) we have already shown that the expected payoff at is upper bounded by . Hence, the maximum expected payoff attained by primary in this case is and it is attained at price in the interval .

Step iii: In Step (i), we have shown that under if primary estimates that the channel state of primary is , then the maximum expected payoff is . In Step (ii), we have shown that if primary estimates that the channel state of primary is , then the maximum expected payoff is . Primary estimates that the channel state of primary is w.p. and the channel state of primary is w.p. . Thus, under , the maximum expected payoff that primary can attain is

| (43) |

We have already shown that the payoff is achieved when primary follows the strategy prescribed in the theorem.

Step iv: Now, we show that under , the maximum expected payoff that primary can attain is and it is attained at every price in the interval . Toward this end, we first show that if primary selects a price from the interval it will fetch an expected payoff of (Step iv.a). Subsequently, we show that if the primary selects any price from the interval or it can only get an expected payoff of at most (Step iv.b. and Step iv.c. resp.).

Step iv.a: Suppose that primary selects a price . When the channel of primary is available, then primary selects a price less than or equal to if one of the following occurs–i) primary selects and estimates the channel state of primary is , ii) primary selects and selects a price less than or equal to . (i) occurs with probability and (ii) occurs with probability . Now, when primary selects it only knows that the channel of primary is available w.p. . Thus, the expected payoff of primary at is

| (44) |

Step iv.b: Note that when , then . Thus, we consider the case when . Suppose primary selects a price in the interval . If the channel of primary is available, then, the primary will select a price less than or equal to if one of the following occurs–i) it selects and estimates that the channel state of primary is , ii) primary selects , iii) primary selects , estimates that the channel state of primary is and selects a price less than or equal to . (i) occurs with probability since the channel of primary is available. (ii) occurs with probability . (iii) occurs with probability (since the channel of primary is available). When primary selects , it only knows that the channel of primary is available w.p . Thus, the expected payoff of primary at is

Since , the above is maximized at . Thus, using (31), the above expression is upper bounded by

| (45) |

where the last equality follows from (IV-D).

Step iv.c: Now, suppose that primary selects a price in the interval . Now, if the channel of primary is available, then it selects a price less than or equal to if it selects , estimates that the channel state of primary is and selects a price less than or equal to . The above occurs with probability . The channel of primary is available w.p. . Thus, at any price in the interval the expected payoff of primary is

Since , the above is maximized at . Thus, using (IV-D), the maximum expected payoff is

| (46) |

Again the last equality follows from (IV-D).

Hence, the maximum expected payoff attained by primary under is . This is attained at any price in the interval which we have shown in Step iv.a.

Step v: Thus, either under or under , the maximum expected payoff that primary can attain is . Hence, any randomization between and will also yield an expected payoff of . Primary can attain the payoff of following the strategy profile. Hence, primary does not have any unilateral profitable deviation. Hence, the result follows. ∎

IV-E Numerical Results

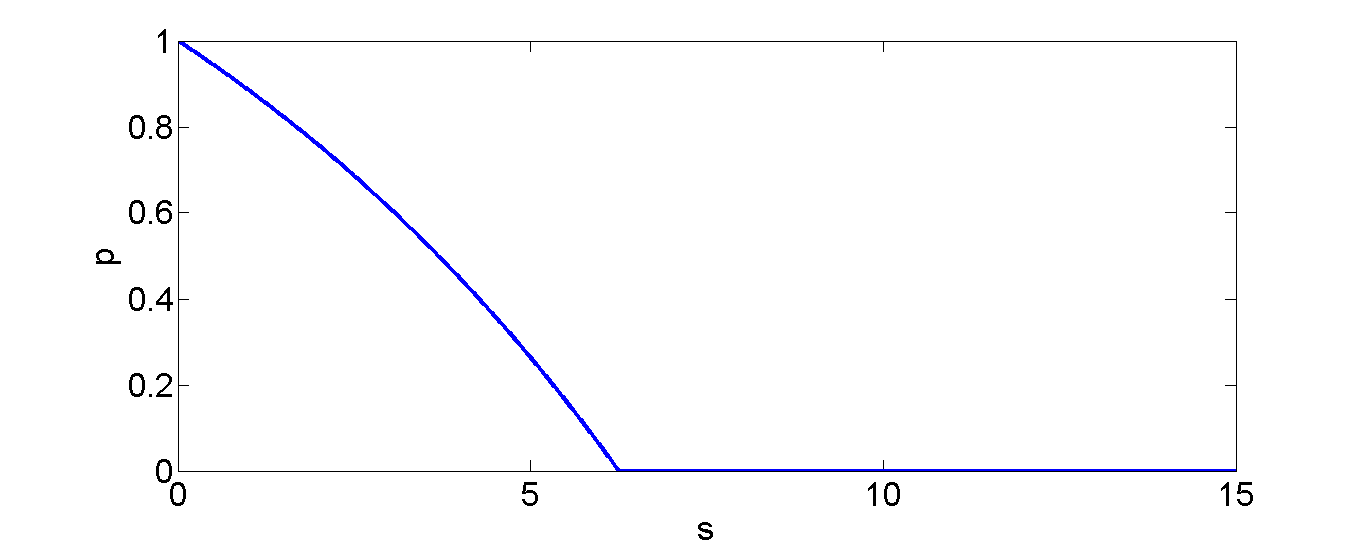

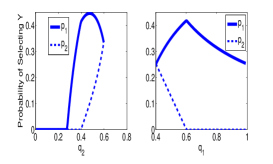

Fig. 7 shows that the probability with which a primary selects increases as increases. Intuitively, when increases, the uncertainty of the channel state of the competitor decreases when a primary selects , thus, the primary selects with a higher probability. Additionally, Fig. 7 shows that the increment of is sub-linear with .

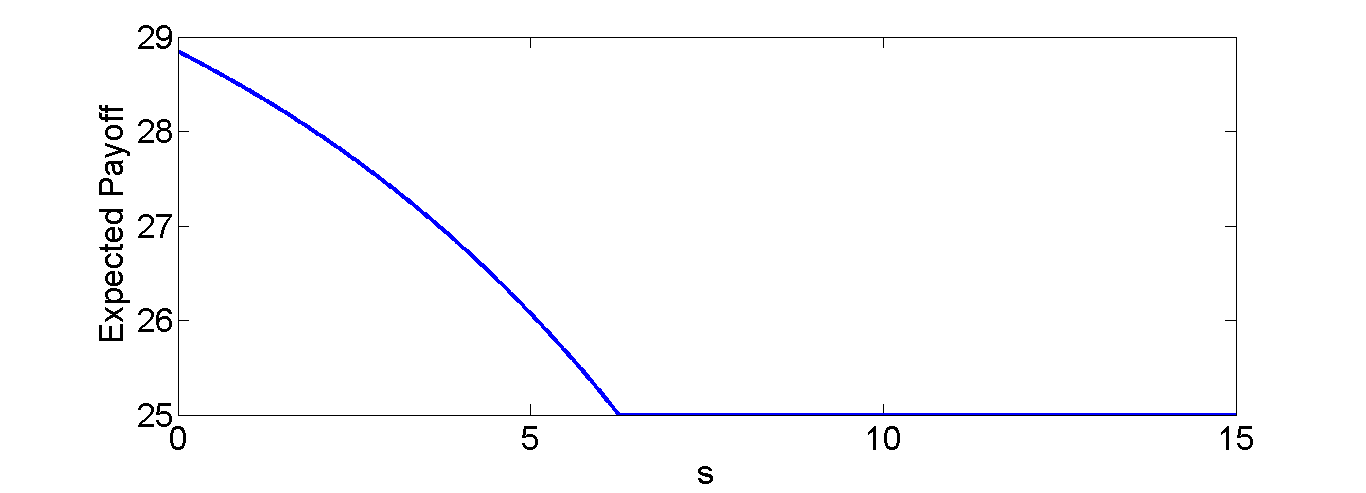

Fig. 7 shows the variation of the expected payoff of a primary with . When , a primary selects w.p. , hence, the expected payoff is for . The expected payoff increases as increases when . After that the payoff decreases and ultimately the expected payoff again becomes equal to when . Thus, the payoff of a primary is higher when there is an error in estimation of the channel state compared to the setting where there is no error in estimation which negates the conventional wisdom that the payoff should increases with the decreases in the error in the estimation. We have already provided the potential reasons behind this behavior in the section IV-B.

Fig. 7 shows the variation of the expected payoff of a primary with . Note from Lemma 2 that the expected payoff of a primary increases as decreases when a primary selects with a positive probability. Fig. 7 verifies the above result. Specifically, as increases, the expected payoff decreases when . Additionally, the expected payoff decreases sub-linearly. When , a primary only selects and attains an expected payoff of , thus, the payoff becomes independent of in this regime.

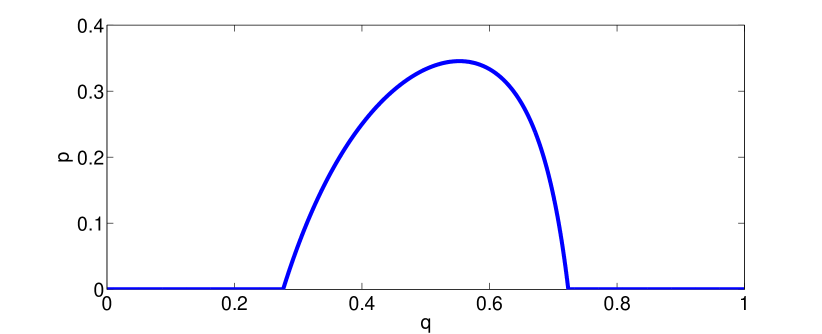

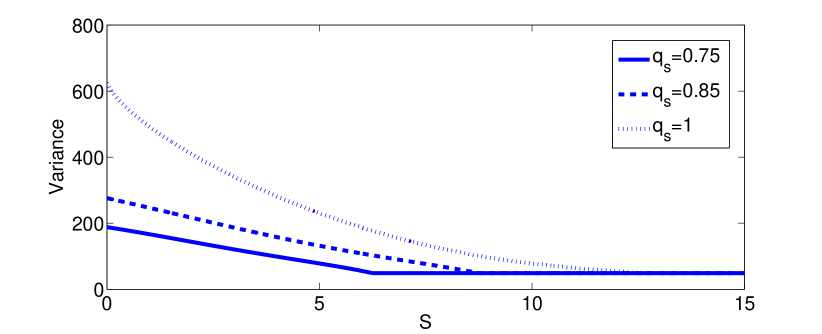

Fig. 10 shows that , the probability with which a primary selects increases as decreases. When , then the primary selects w.p. i.e. . Additionally, Fig. 10 shows that decreases sub-linearly as increases.

Fig. 10 shows the variation of the variance of the price selected by a primary with and . Note that the variance decreases as decreases. Thus, when a primary selects with a higher probability, the price volatility is lower. When , each primary selects w.p. , thus, the variance becomes independent of . This is because , the price selection strategy from which a primary selects its price when , is independent of . Note that Fig. 10 also shows that the variance also decreases as decreases. Intuitively, as decreases, a primary selects with a higher probability, thus, the variance decreases. Note that buyers in general do not like a market where the prices have higher variances. Thus, when is low or is high, a buyer may not like the setting.

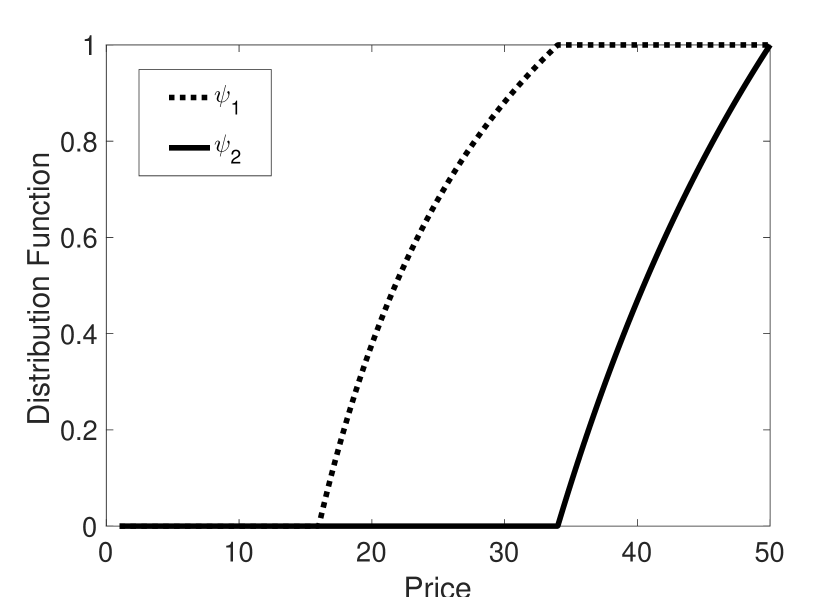

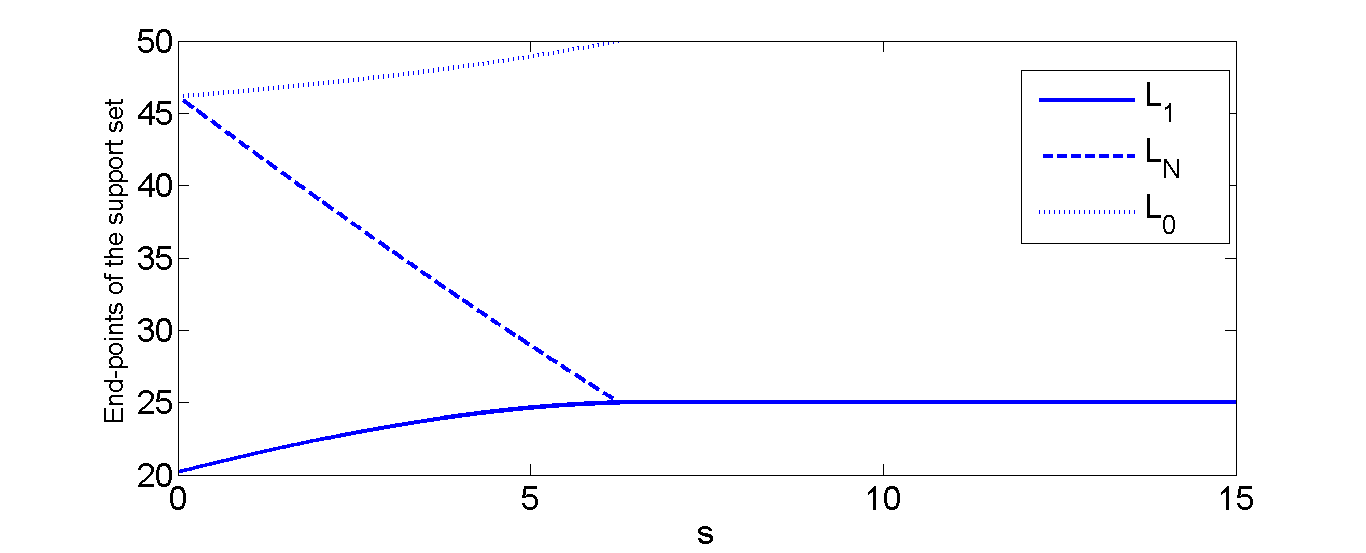

Fig. 12 shows the variations of the end-points of the support sets of the price distributions. Note that when , as primaries select with probability. As increases, and increase as primaries select with positive probability; primaries select prices from a larger interval when it selects as increases. Note that the lower end-point of , ( in the figure) also increases as increases. Thus, the price interval from which a primary selects its price decreases as increases. Intuitively, as increases, a primary selects with a lower probability, thus the support also decreases. When , the primary only selects , thus, and .

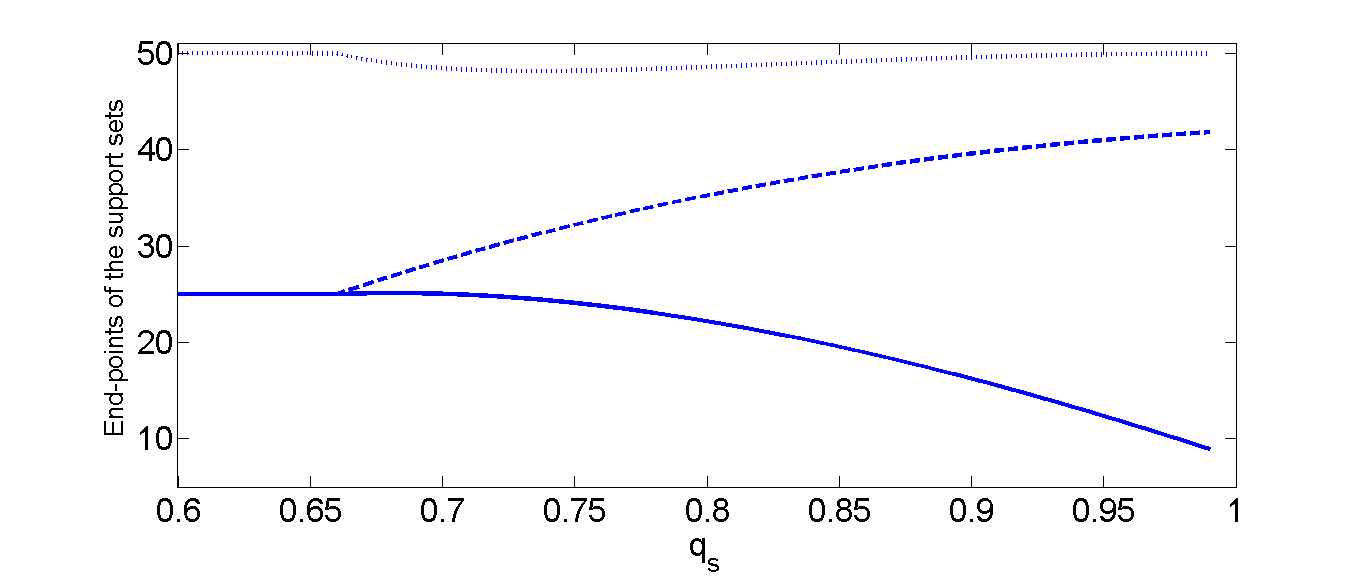

Fig. 12 shows the variation of the end-points of the support sets of the price distributions. When , primaries only select . Thus, and . When , primaries select with positive probabilities. decreases as increases. Thus, a primary selects a lower price when it selects and estimates that the channel state of the competitor is . Intuitively, as increases, the uncertainty reduces, thus, the competitor’s channel is more likely to be available when a primary estimates that the channel state of the primary is . Hence, the primary selects a lower price. Since primary selects when , decreases initially. However, increases when becomes very high. Note that when is very high, then a primary is aware that the channel of the competitor is more likely to be unavailable, hence it selects a high price. Thus, is close to when is very high. Note also that increases with . Intuitively, when increases, a primary selects with a lower probability, thus, a primary selects its price from a shorter interval when it selects .

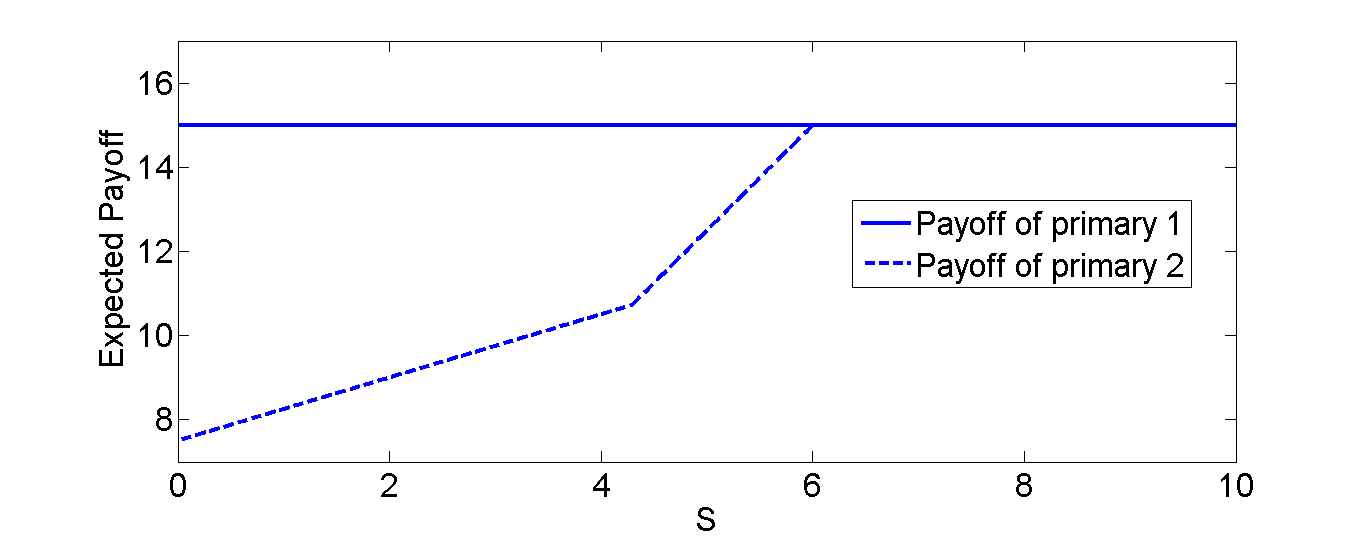

V Unequal Costs

We, now, investigate the generalization of the basic model where each different primaries incur different costs to acquire the CSI of their respective competitors depicted in Section II-B2. Primary incurs the cost to acquire the CSI of its competitor. Without loss of generality we assume that .

V-A Goals

The impact of different acquisition costs on the payoff of each primary and the frequency with which each primary selects is not apriori clear. For example, primary which has a lower acquisition cost of CSI, can gain more compared to primary by acquiring the CSI of primary by paying a lower cost. However, primary also acquires the CSI of primary and selects a lower price when the channel of primary is available, thus, primary also selects a lower price in response, which in turn reduces the payoff of primary . The pricing decision of each primary also depends on the frequencies with which each primary selects . We resolve all these quandaries.

V-B Results

We summarize our main findings here–

-

•

The NE strategy is of the form for primary with . Note that is the same as the basic model, however, since different primaries have different acquisition costs, s are different. For example, when , then primary selects w.p. , but primary does not select . Even when , then primary selects where as .

-

•

The difference in the acquisition costs lead to different payoffs for the primaries. In contrast to the basic model, primary attains a higher payoff compared to the expected payoff of primary when primary selects with a positive probability (i.e. ) (Theorems 8, 9). The expected payoff of primary becomes close to the payoff of the primary as the difference between and decreases. The expected payoff of primary is in fact independent of . The expected payoff of the primaries are the same when , as both of them only select .

-

•

Primary selects its price from the interval (, resp.) , when the primary selects (, resp.) and the channel of the competitor is available. However, there are also some differences in the pricing structure compared to the basic model because of different acquisition costs. Primary selects with a positive probability when it selects when and the probability decreases as the difference between and decreases (Theorems 9). Thus, the primary has a discontinuity at in contrast to the basic model where primaries select prices from continuous distribution. Additionally, we show that . Thus, primary selects lower prices when it selects and the channel of primary is available. On the other hand, when primary selects , its selects higher prices with higher probabilities.

V-C High

Our first result in this section shows that

Theorem 7.

When , then in the unique NE, both the primaries select w.p. and select their prices according to (given in (2)). Both the primaries attain an expected payoff of .

The proof is similar to the proof of Theorem 3, thus, we omit it here.

Note that since , . Thus, the above theorem shows that the expected payoff of primaries are identical when s are sufficiently high as both the primaries select .

V-D Low , high

Now, we consider the setting where , but . We show that there exists a NE where primary randomizes between and , and primary selects .

We first introduce some pricing distributions which we use throughout this section–

| (47) |

| (48) |

| (49) |

where

| (50) |

and

| (51) |

| (52) |

clearly has a jump at as . From the expression of one may think that has a jump at . We first rule out the above possibility.

Observation 2.

does not have any jump except at .

Proof.

First, note that since , thus, has a jump at .

Next, we show that does not have any jump at . The continuity of at any other point can easily be observed.

The continuity of and can be easily concluded. Note that the variations of , and are similar they differ only in the support and the scaling parameters.

Now, we are ready to state the main result of this section.

Theorem 8.

Consider the following strategy profile: Primary selects w.p. and w.p. ( is given in (51)) and primary selects w.p. . While selecting , if the channel of primary is available, then primary selects its price according to , otherwise it selects w.p. . While selecting , primary selects its price according to . Primary selects its price according to .

The above strategy profile is the unique NE when and . The expected payoff that primary attains is and the expected payoff of primary is .

Discussion: Note that when and , the payoff of primary is higher compared to the primary . Apparently, when is low, then primary takes advantage of the acquired CSI and gains more compared to primary . Primary can not do the same as the cost is high. The expected payoff of primary also increases with the decrease in . Note that the threshold above which primary only selects is ; the threshold is the same for both the players.

The probability increases with decrease in , hence, primary is more likely to select with the decrease in .

Since increases as decreases. also increases as decreases (from (52)) . Thus, has larger support as decreases.

Under , primary selects a price from the interval when the channel of primary is available; under , primary selects a price from the interval . Hence, primary selects higher price under as the uncertainty of the CSI of other primary increases. Also note that overlaps both with and .

Also note that has a jump at . Thus, primary selects with a positive probability. Intuitively, primary selects with a higher probability. Thus, primary knows the channel state of primary with a higher probability and thus and selects a lower price. In response, primary has two options– i) selects a high price with high probability ( at least it can gain more when the channel of the primary is not available), ii) selects a low price ( it can increase the probability of winning). Our result shows that primary selects the first option.

V-D1 Proof of Theorem 8

First, we show that there is no profitable deviation for primary when primary follows the prescribed strategy stated in Theorem 8 (Case I), subsequently, we show that there is also no profitable deviation for primary when primary follows the prescribed strategy stated in Theorem 8 (Case II).

Case I: In the first step (i), we show that primary can attain a maximum expected payoff of under . Next in step (ii), we show that primary can attain a maximum expected payoff of under . Finally in step (iii), we show that primary attains the maximum expected payoff following the strategy which will show that primary does not have any profitable unilateral deviation.

Step (i): Primary selects . Suppose that the channel of primary is available, then primary will know that w.p. . At any such that the primary gets under is

| (55) |

If primary selects a price strictly less than , then, its payoff is strictly less than .

Now, at any , the expected payoff of primary in this setting is

| (56) |

Since , thus, the supremum is attained at . Now from (52), the maximum value is

| (57) |

Since has a jump at , thus, the expected payoff at is strictly less than the value at a price close to . Hence, when the channel of primary is available, then the maximum expected payoff that primary can attain at is and it is attained at any price in the interval .

Now, when the channel of primary is unavailable, the expected payoff of primary is . Hence, the maximum expected payoff that primary attains in is

| (58) |

Step (ii) Now suppose primary selects and a price such that . Primary selects a price less than if the channel of primary is available and selects a price less than or equal to (it occurs w.p. ). By the continuity of in the interval , the expected payoff of primary at is

| (59) |

Since has a jump at , thus, the expected payoff of primary is strictly less at a price close to compared to . Thus, the expected payoff of primary at is strictly less than .

Now, at any such that , the expected payoff of primary under is

| (60) |

The supremum is attained at . Putting the value of from (52) we obtain

| (61) |

The expected payoff at a price strictly less than will fetch a payoff which is strictly less than the payoff attained at . Thus, primary can attain at most an expected payoff of under . The maximum expected payoff is attained at any price in the interval .

Step (iii): Hence, we show that the primary can attain an expected payoff of under either or . Thus, any randomization between and will also give an expected payoff of . Now, under the strategy profile the expected payoff is also , hence, primary does not have any profitable deviation.

Case II: Now, we show that primary does not have any profitable deviation when primary selects the prescribed strategy stated in the theorem. Towards this end, we first show in Step (i) that any price in the interval will give an expected payoff of to primary when it selects , subsequently, we show that any price in the interval will also provide an expected payoff of to primary when it selects . In step (iii), we show that any price will give a strictly lower payoff compared to when it selects . Finally in step (iv), we show that if primary selects , then it can only get a payoff of at most when . This will show that primary attains the maximum expected payoff of and it is attained when it selects and selects a price in the interval .

Step (i): Note that when primary can select a price less than only when the channel of primary is available and primary selects , thus, at any such that , the expected payoff of primary is

| (62) |

Step (ii) When , then primary selects a price lower than only if the channel of primary is available and either it selects or while selecting it selects a price less than . Hence, the expected payoff of primary is

| (63) |

(iii) At any price less than will fetch a payoff which is strictly less than . However, . Thus, the expected payoff of primary is strictly less than at any price less than . Hence, primary can only attain a maximum expected payoff of and it is attained at the prices in the interval .

(iv) Now, suppose primary selects . If the channel of primary is available, then at any , it will get an expected payoff of

| (64) |

Since , thus the above is maximized at , and the maximum expected payoff is since .

Now, if primary selects a price in the interval when the channel of primary is available, then the expected payoff of primary is

Thus, primary attains an expected payoff of at most when it selects and the channel of primary is available.

Now, when the channel of primary is unavailable the payoff that primary earns is . Hence, the maximum expected payoff that primary can earn by selecting is

| (65) |

when , thus, the primary attains at most a payoff of . Hence, primary also does not have any profitable deviation.∎

V-E Low

Lastly, we show that if then, there exists an NE where primary also randomizes between and .

Again, we introduce some price distribution functions

| (66) |

| (67) |

| (68) |

and

| (69) |

where

| (70) |

The values of and are

| (71) |

Since , . Note that only depends on . Using the values of and , we obtain from (V-E)

| (72) |

and

| (73) |

We also use the above equalities throughout this section.

It is easy to discern that and are continuous. Now, we show that is also continuous.

Observation 3.

is a continuous function.

Proof.

Next, we show that is continuous everywhere but at .

Observation 4.

is continuous except at .

Proof.

Since , thus, it is easy to discern that has a jump at .

Now, we show that does not have a jump at . It is easy to discern that can not have a jump at any other point.

From (73), we have

| (74) |

Thus, the left hand limit at is

| (75) |

Now, the right hand limit and the value of at is

| (76) |

Hence, does not have a jump at . ∎

Note that though has a jump at , the variation of with is similar to the other distributions and .

Now, we are ready to state the main result in this section.

Theorem 9.

Consider the following strategy profile: Primary selects w.p. and w.p. and primary selects w.p. and w.p. where and are given in (71). While selecting , primary selects its price according to when the channel of primary is available and will select the price if the channel of primary is unavailable; while selecting , primary selects its price according to .

The above strategy profile is the unique NE when . The expected payoff that primary attains is and primary attains is .

Discussion: Since , thus, the expected payoff of primary is higher compared to primary . Since , thus by Theorem 8 the expected payoff of primary is lower compared to the setting where . Note also that the payoff of primary decreases with , but increases with . Thus, if decreases it only impacts the payoff of primary , it does not affect the payoff of primary . The payoff of primary also becomes closer to the payoff of primary as becomes closer to and ultimately becomes equal when which we have already seen in Section III where we analyze the scenario when both the primaries have identical cost to acquire the CSI of their respective competitors i.e. .

(,resp.) increases with the decrease in (, resp.). Thus, primaries are more likely to select as the cost decrease. When , then , and when , then . Since , thus, . Primary is more likely to select compared to primary .