Stock loans with liquidation

A technical report commissioned by the Bank of Nova Scotia††thanks: The views expressed herein are solely those of the author and not

those of any other person or entity.

Abstract

We derive a “semi-analytic” solution for a stock loan in which the lender forces liquidation when the loan-to-collateral ratio drops beneath a certain threshold. We use this to study the sensitivity of the contract to model parameters.

1 Introduction

We study a stock loan contract in which the lender can force the client to liquidate. It was originally pointed out in [16] that stock loans are essentially American call options with negative interest rates. The negative rate appears since the contract is effectively discounted by , where , the loan interest rate, is generally larger than the riskless rate of return .

Concretely, a stock loan is a loan of size obtained from a financial firm (lender) by posting shares of an asset valued at as collateral. Such loans are usually nonrecourse in that if the stock price drops, the borrower (client) may simply forfeit ownership of the shares in lieu of repaying the loan. On the other hand, if the stock price rises, the client can regain their shares by repaying the loan (along with the accrued interest).

The liquidation clause is useful from the perspective of the lender as it reduces the amount of risk the lender is exposed to, simultaneously reducing the rational premium charged for the loan. We find that such loans are riskless in the absence of jumps, in which case neither lender nor client benefits from entering into such a loan (simultaneously motivating the need for a jump-diffusion model; in particular, we have chosen the HEM for its analytical tractability and ample freedom in shaping return distributions).

[16] studies a perpetual contract (i.e., one that does not expire) with dividends paid out to the lender. In this original model, the lender cannot take action once the contract is initiated. [17] studies stock loans under regime-switching. Optimal strategies for both perpetual and finite-maturity contracts subject to various dividend distribution schemes are studied in [6]. A model in which the asset is driven by a hyper-exponential jump-diffusion is considered in [4] for both perpetual and finite-maturity contracts. Some other works on stock loans are [10, 11, 9, 14, 7, 13, 15, 5, 8, 12].

2 Hyper-exponential model

Consider a stochastic process following a hyper-exponential model (HEM)

where is a (right-continuous) Poisson process with rate , is a standard Brownian motion, and is a sequence of i.i.d. hyper-exponential random variables with p.d.f.

We make the following assumption throughout:

Assumption.

, for all , for all , , , and are nonnegative integers not both equal to zero, and (subject to the convention ).

The Lévy exponent of the process is

In [2, Lemma 2.1 and Remark 2.3], it is shown that for any where

has real roots , , , , , and satisfying (omitting the subscript )

| (1) |

is a possibility, in which case there are only distinct roots.

3 Stock loans with liquidation

We consider a stock loan contract similar to [16]. At the initial time, the client borrows an amount from the lender using one share of the stock with initial price as collateral. The stock follows (in log space) the process defined in §2 with where is the risk-free rate, is the dividend rate, is the volatility, and . The loan is continuously compounded at the rate . At any (stopping) time , the client can choose to redeem the stock and pay back . If the loan-to-collateral ratio exceeds the level , the lender liquidates the loan, forcing the client to pay back . During the collateral period, stock dividends are collected by the lender.

Remark.

Transfer-of-title stock loans were shut down by the SEC and IRS between 2007-2012 and reclassified as fully taxable sales at inception (see also [1]). It stands to reason that the case of implies a transfer-of-title (since the lender receives the dividends), and hence is subject to tax considerations. The case of corresponds to dividends being immediately reinvested in the stock and returned to the client upon redemption, and is thus arguably the more relevant case for the current era. Other dividend distribution schemes are visited in [6].

If we assume that the client is able to pick a time to redeem the stock from , the set of stopping times, the value of this contract is

It is understood that the expression in the expectation is zero whenever . However, due to the presence of the stopping time , it is not a simple matter to show that the above is a free boundary problem with respect to . This makes the above problem difficult if we are seeking analytical solutions (see, e.g., [16, Proposition 3.1]). Instead, we consider the simpler

in which the client picks instead a level to stop at based on the loan-to-collateral ratio.

Assumption.

, , and .

The following is a trivial consequence of the definition of .

Lemma 1.

everywhere and for .

The following is a trivial, but interesting aside: it establishes that the client has no reason to take out a stock loan in the absence of (downward) jumps in the collateral value (equivalently, the lender is exposed to no risk).

Lemma 2.

If or , then everywhere.

Proof.

Note that in this case, for -almost all such that . Therefore, for any stopping time , and hence for -almost all such that . It follows that

Returning to our objective, define a drift-adjusted process by with Lévy exponent . Letting , we can write

| (2) |

For fixed values of and , we may compute the expectation

| (3) |

using Proposition 5 of the appendix (see, in particular, expression (7)). Before we can do so, we must ensure the finitude of the expectation.

Assumption.

Either (i) or (ii) and .

Subject to the above, [4, Theorem 3.1] holds, repeated below for convenience.

Proposition 3.

.

Lemma 4.

4 Numerical results

4.1 Algorithm

Using Proposition 5 of the appendix, a direct computation shows that the expectation in (2) is continuous as a function of . This inspires the algorithm below for approximating at . We write to stress the dependence of (defined in (2)) on . Below, is given by .

-

Stock-Loan

1 2if 3 for 4 5 6return

4.2 Lender’s perspective

To aid our understanding, we also consider the contract from the lender’s perspective. In particular, let be the map satisfying . This equation has the interpretation that the client retains ownership of the stock (initially valued at ) and is short the contract . Conversely, the lender is long the contract . Simple algebra along with the fact reveals

| (4) |

From the form (4), it is easy to see that includes dividend flows to the lender (the case in which dividends are immediately reinvested in the stock and returned to the client upon prepayment is equivalent to taking ; we refer to [6, Section 3] for an explanation).

4.3 Jump risk

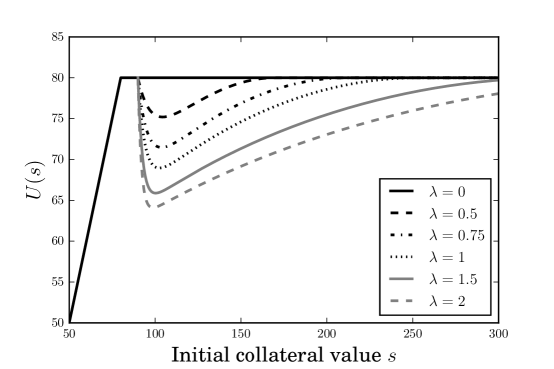

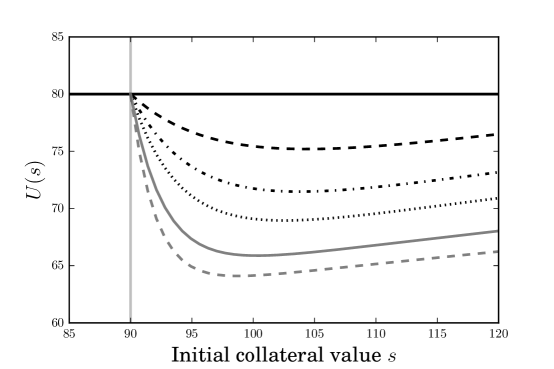

Figure 1 shows the stock loan value under varying jump arrival rates . As stipulated by Lemma 2, in the absence of jumps, the loan is riskless (i.e. , or equivalently, ). However, as increases, the lender is exposed to more risk. This coincides with our intuition: as the probability of a downward jump is increased, so too is the probability that jumps below the loan value .

The lender is exposed to the most risk at a point between and . This is explained as follows:

-

If the collateral is very close to , the event that a downward jump brings below the loan value before the lender is able to liquidate is unlikely.

-

If the collateral is very large and the client chooses to prepay, the lender can retrieve the loan value in its entirety.

| Parameter | Value | |

|---|---|---|

| Model | Double exponential () | |

| Risk-free rate | ||

| Dividend rate | ||

| Volatility | ||

| Loan interest rate | ||

| Initial collateral value | ||

| Loan value | ||

| Liquidation ratio | ||

| Jump arrival rate | ||

| Mean up-jump scaling factor | ||

| Mean down-jump scaling factor | ||

| Up-jump probability | ||

| Down-jump probability | ||

4.4 Rational values

Denote by an up-front premium. At time zero, the client essentially exchanges the amount for a stock loan [16]. It follows that and are required to satisfy the following identity to preclude arbitrage:

| (5) |

Table 2 computes some rational values of , and satisfying (5).

| 30 | 40 | 50 | 60 | 70 | 80 | 90 | 100 | |

|---|---|---|---|---|---|---|---|---|

| 30 | 39.29 | 47.26 | 54.51 | 61.35 | 69.09 | 90 | 100 | |

| 0 | 0.71 | 2.74 | 5.49 | 8.65 | 10.91 | 0 | 0 |

| 30 | 40 | 50 | 60 | 70 | 80 | 90 | 100 | |

|---|---|---|---|---|---|---|---|---|

| 28.79 | 36.53 | 43.77 | 50.70 | 57.42 | 64.14 | 90 | 100 | |

| 1.21 | 3.47 | 6.23 | 9.30 | 12.58 | 15.86 | 0 | 0 |

Note that for , the rational premium is (see Figure 1 for further intuition). In this case, neither client nor lender has any reason to enter into the contract. For where , the rational premium is , as the contract is exercised immediately. It stands to reason that the only region of interest is . Parameterizations in which (i.e. the free boundary is “collapsed”) are, therefore, uninteresting.

In particular, note the discontinuity occurring at (Figure 1), corresponding to liquidation. In the event that the free boundary is collapsed, , and this discontinuity is removed.

- Acknowledgements

-

The author thanks Shuqing Ma of the Bank of Nova Scotia and Peter Forsyth, Kenneth Vetzal, and George Labahn of the University of Waterloo.

Appendix A Laplace transform of first passage time to two barriers

We require an expression for the Laplace transform of a process to two flat barriers and with . Formally, let

A generalization of the Laplace transform of is studied in [3]. A trivial modification of the authors’ result is repeated below.

Proposition 5.

Let be a nonnegative measurable function such that

are integrable for all and . Let and . Let be an matrix given by

| (6) |

where and are the real roots of satisfying (1) and . If is nonsingular,

| (7) |

where is a row vector defined as

and is a column vector such that where

References

- [1] Financial Industry Regulatory Authority. Stock-based loan programs: What investors need to know. http://www.finra.org/investors/alerts/stock-based-loan-programs-what-investors-need-know. (Accessed September 2016).

- [2] Ning Cai. On first passage times of a hyper-exponential jump diffusion process. Oper. Res. Lett., 37(2):127–134, 2009.

- [3] Ning Cai, Nan Chen, and Xiangwei Wan. Pricing double-barrier options under a flexible jump diffusion model. Oper. Res. Lett., 37(3):163–167, 2009.

- [4] Ning Cai and Lihua Sun. Valuation of stock loans with jump risk. J. Econom. Dynam. Control, 40:213–241, 2014.

- [5] Wenting Chen, Liangbin Xu, and Song-Ping Zhu. Stock loan valuation under a stochastic interest rate model. Comput. Math. Appl., 70(8):1757–1771, 2015.

- [6] Min Dai and Zuo Quan Xu. Optimal redeeming strategy of stock loans with finite maturity. Math. Finance, 21(4):775–793, 2011.

- [7] Matheus R. Grasselli and Cesar Gómez. Stock loans in incomplete markets. Appl. Math. Finance, 20(2):118–136, 2013.

- [8] Tim Leung, Kazutoshi Yamazaki, and Hongzhong Zhang. Optimal multiple stopping with negative discount rate and random refraction times under Lévy models. SIAM J. Control Optim., 53(4):2373–2405, 2015.

- [9] Zongxia Liang and Weiming Wu. Variational inequalities in stock loan models. Optim. Eng., 13(3):459–470, 2012.

- [10] Zongxia Liang, Weiming Wu, and Shuqing Jiang. Stock loan with automatic termination clause, cap and margin. Comput. Math. Appl., 60(12):3160–3176, 2010.

- [11] Guangying Liu and Yongqing Xu. Capped stock loans. Comput. Math. Appl., 59(11):3548–3558, 2010.

- [12] Xiaoping Lu and Endah R. M. Putri. Semi-analytic valuation of stock loans with finite maturity. Commun. Nonlinear Sci. Numer. Simul., 27(1-3):206–215, 2015.

- [13] A. Pascucci, M. Suárez-Taboada, and C. Vázquez. Mathematical analysis and numerical methods for a PDE model of a stock loan pricing problem. J. Math. Anal. Appl., 403(1):38–53, 2013.

- [14] Tat Wing Wong and Hoi Ying Wong. Stochastic volatility asymptotics of stock loans: valuation and optimal stopping. J. Math. Anal. Appl., 394(1):337–346, 2012.

- [15] Tat Wing Wong and Hoi Ying Wong. Valuation of stock loans using exponential phase-type Lévy models. Appl. Math. Comput., 222:275–289, 2013.

- [16] Jianming Xia and Xun Yu Zhou. Stock loans. Math. Finance, 17(2):307–317, 2007.

- [17] Qing Zhang and Xun Yu Zhou. Valuation of stock loans with regime switching. SIAM J. Control Optim., 48(3):1229–1250, 2009.