Stochastic PDEs with heavy-tailed noise

Abstract

We analyze the nonlinear stochastic heat equation driven by heavy-tailed noise on unbounded domains and in arbitrary dimension. The existence of a solution is proved even if the noise only has moments up to an order strictly smaller than its Blumenthal-Getoor index. In particular, this includes all stable noises with index . Although we cannot show uniqueness, the constructed solution is natural in the sense that it is the limit of the solutions to approximative equations obtained by truncating the big jumps of the noise or by restricting its support to a compact set in space. Under growth conditions on the nonlinear term we can further derive moment estimates of the solution, uniformly in space. Finally, the techniques are shown to apply to Volterra equations with kernels bounded by generalized Gaussian densities. This includes, for instance, a large class of uniformly parabolic stochastic PDEs.

| AMS 2010 Subject Classifications: | primary: 60H15, 60H20, 60G60 |

| secondary: 60G52, 60G48, 60G51, 60G57 |

Keywords: generalized Gaussian densities; heavy-tailed noise; Itô basis; Lévy basis; parabolic stochastic PDE; stable noise; stochastic heat equation; stochastic partial differential equation; stochastic Volterra equation

1 Introduction

In this paper we investigate the nonlinear stochastic heat equation

| (1.1) |

where is some random noise, the function is globally Lipschitz and is some given initial condition. In the theory of stochastic partial differential equations (stochastic PDEs) there are various ways to make sense of the formal equation (1.1). We refer to Peszat and Zabczyk (2007), Liu and Röckner (2015) and Holden et al. (2010) for detailed accounts within the semigroup, the variational and the white noise approach, respectively. Our analysis is based on the random field approach going back to Walsh (1986) where the differential equation (1.1) is interpreted as the integral equation

| (1.2) |

where is the heat kernel

| (1.3) |

is related to the initial condition via

and the integral with respect to is understood in Itô’s sense, see e.g. Bichteler and Jacod (1983), Walsh (1986) and Chong and Klüppelberg (2015).

There are multiple reasons for the broad interest in studying the stochastic heat equation (1.1): on the one hand, it is of great significance within mathematics because, for example, it has strong connections to branching interacting particles (see e.g. Carmona and Molchanov (1994), Dawson (1993) and Mueller (2015)) and it arises from the famous Kardar-Parisi-Zhang equation via the Cole-Hopf transformation (Corwin, 2012; Hairer, 2013). On the other hand, the stochastic heat equation has found applications in various disciplines like turbulence modeling (Davies et al., 2004; Barndorff-Nielsen et al., 2011), astrophysics (Jones, 1999), phytoplankton modeling (Saadi and Benbaziz, 2015) and neurophysiology (Walsh, 1981; Tuckwell and Walsh, 1983).

If is a Gaussian noise, the initial theory developed by Walsh (1986) has been comprehensively extended and many properties of the solution to the stochastic heat equation or variants hereof have been established, see Khoshnevisan (2014), for example. When it comes to non-Gaussian noise, the available literature on stochastic PDEs within the random field approach is much less. While the papers by Albeverio et al. (1998) and Applebaum and Wu (2000) remain in the -framework of Walsh (1986), Saint Loubert Bié (1998) is one of the first to treat Lévy-driven stochastic PDEs in -spaces with . The results are extended in Chong (2016) to Volterra equations with Lévy noise, on finite as well as on infinite time domains. In both Saint Loubert Bié (1998) and Chong (2016), one crucial assumption the Lévy noise has to meet is that its Lévy measure, say , must satisfy

| (1.4) |

for some . This a priori excludes stable noises, or more generally, any noise with less moments than its Blumenthal-Getoor index. Of course, if the noise intensity decreases sufficiently fast in space, for example, if it only acts on a bounded domain instead of the whole , this problem can be solved by localization, see Balan (2014) and Chong (2016). Also on a bounded space domain, Mueller (1998) considers the stochastic heat equation with spectrally positive stable noise of index smaller than one and the non-Lipschitz function (). To our best knowledge, the paper by Mytnik (2002), where the same function is considered with spectrally positive stable noises of index bigger than one, is the only work that investigates the stochastic heat equation on the whole with noises violating (1.4) for all . The purpose of this article is to present results for Lipschitz and more general heavy-tailed noises , including for all dimensions stable noises of index (with no drift in the case ).

More specifically, if is a homogeneous pure-jump Lévy basis with Lévy measure and is, say, a bounded deterministic function, we will prove in Theorem 3.1 the existence of a solution to (1.2) under the assumption that

for some and . Although the proof does not yield uniqueness in a suitable -space, we can show in Theorem 3.7 that our solution is the limit in probability of the solutions to (1.2) when either the jumps of are truncated at increasing levels or when is restricted to increasing compact subsets of . Furthermore, if with an exponent , the constructed solution has -th order moments that are uniformly bounded in space, see Theorem 3.8. Finally, in Theorem 3.10, we extend the previous results to Volterra equations with kernels bounded by generalized Gaussian densities, which includes uniformly parabolic stochastic PDEs as particular examples.

2 Preliminaries

Underlying the whole paper is a stochastic basis satisfying the usual hypotheses of right-continuity and completeness that is large enough to support all considered random elements. For we equip with the tempo-spatial predictable -field where is the usual predictable -field and is the Borel -field on . With a slight abuse of notation, also denotes the space of predictable, that is, -measurable processes . Moreover, is the collection of all satisfying for some . Next, writing and for , we equip the space with the usual topology induced by for and for . Further notations and abbreviations include for two -stopping times and (other stochastic intervals are defined analogously), for the total variation measure of a signed Borel measure , for the -th coordinate of a point and for . Last but not least, the value of all constants and may vary from line to line without further notice.

In this paper the noise that drives the equations (1.1) and (1.2) will be assumed to have the form

| (2.1) |

with the following specifications:

-

•

is an arbitrary Polish space equipped with its Borel -field,

-

•

,

-

•

is a -measurable function,

-

•

is a Gaussian space–time white noise relative to (see Walsh (1986)),

-

•

is a homogeneous Poisson random measure on relative to (see Definition II.1.20 in Jacod and Shiryaev (2003)), whose intensity measure disintegrates as with some -finite measure on .

Moreover, all coefficients are assumed to be “locally integrable” in the sense that the random variable

is well defined for all . In analogy to the notion of Itô semimartingales in the purely temporal case, we call the measure in (2.1) an Itô basis. We make the following structural assumptions on : there exist exponents (without loss of generality we assume that ), numbers , -stopping times , and deterministic positive measurable functions such that

-

M1.

for all and a.s.,

-

M2.

,

-

M3.

and for all with and .

If (resp. ), we can a.s. define (resp. ) for . In this case, we assume without loss of generality that (resp. ) is bounded by as well when .

Example 2.1

If is an Itô basis with , deterministic coefficients , and , and satisfies and , then is a homogeneous Lévy basis (and a space–time white noise) with Lévy measure . In this case, conditions M1–M3 reduce to the requirement that

| (2.2) |

with and . If (resp. ), (resp. ) is the drift (resp. the mean) of .

Regarding integration with respect to Itô bases, essentially, as all integrals are taken on finite time intervals, the reader only has to be acquainted with the integration theory with respect to Gaussian white noise (see Walsh (1986)) and (compensated) Poisson random measures (see Chapter II of Jacod and Shiryaev (2003)). But at one point in the proof of Theorem 3.1 below, we need the more abstract theory behind. So we briefly recall this, all omitted details can be found in e.g. Bichteler and Jacod (1983) or Chong and Klüppelberg (2015). The stochastic integral of a simple function is defined in the canonical way: if with , and , then

In order to extend this integral from the class of simple functions to general predictable processes, it is customary to introduce the Daniell mean

for and . A predictable function is called -integrable (or simply integrable if ) if there exists a sequence of simple functions in with as . In this case, the stochastic integral

exists as a limit in and does not depend on the choice of . It is convenient to indicate the domain of integration by or , for example. In the latter case, contrary to usual practice, the endpoint is excluded.

Although the Daniell mean seems to be an awkward expression, it can be computed or estimated effectively in two important situations: if is a strict random measure, that is, if it can be identified with a measure-valued random variable , then we simply have ; if is a local martingale measure, that is, for every the process has a version that is an -local martingale, then by the Burkholder-Davis-Gundy inequalities (in conjunction with Theorem VII.104 of Dellacherie and Meyer (1982)) there exists, for every , a constant such that

for all . Here is the quadratic variation measure of .

Finally, for , we define the space (resp. ) as the collection of all for which we have

for all (resp. for all ). Moreover, if is an -stopping time, we write (resp. ) if belongs to (resp. ).

3 Main results

In Saint Loubert Bié (1998) and Chong (2016), Equation (1.2) driven by a Lévy basis is proved to possess a solution in some space under quite general assumptions. The most restrictive condition, however, is that the Lévy measure has to satisfy

| (3.1) |

Although there is freedom in choosing the value of , there is no possibility to choose this exponent for the small jumps (i.e., ) and the big jumps (i.e., ) separately. So for instance, stable Lévy bases are always excluded. The main goal of this paper is to describe a way of how one can, to a certain extent, choose different exponents in (3.1) for the small and the large jumps, respectively. In fact, we can consider a slightly more general equation than (1.2), namely the stochastic Volterra equation

| (3.2) |

under the following list of assumptions.

-

A1.

For every we have that .

-

A2.

There exists such that for all .

-

A3.

The function is measurable and for all there exists with for all , where is the heat kernel (1.3).

-

A4.

The exponents and in M3 satisfy and .

-

A5.

If , we assume ; if , we also require that .

As it is usual in the context of stochastic PDEs, we call a solution to (3.2) if for all the stochastic integral on the right-hand side of (3.2) is well defined and the equation itself holds a.s. Two solutions and are identified if they are versions of each other.

Theorem 3.1.

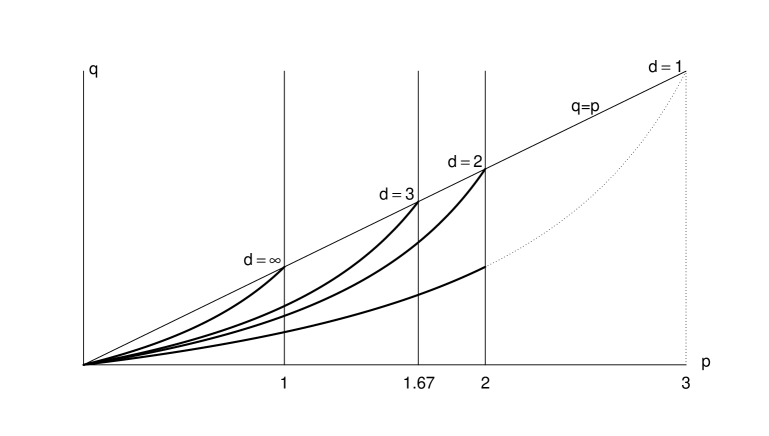

Figure 1 illustrates the possible choices for the exponents and such that Theorem 3.1 is applicable. For each dimension , the exponent must be smaller than and the exponent larger than , which corresponds to the area above the bold lines in Figure 1. If , the result is well known from Saint Loubert Bié (1998) and Chong (2016). So the new contribution of Theorem 3.1 pertains to the area above the bold lines and below the diagonal . As we can see, all stable noises with index (and zero drift if ) are covered: they are “located” infinitesimally below the line in the figure. Moreover, we observe that there exists a non-empty region below the diagonal that constitutes valid parameter choices for all dimensions : namely when and .

Put in a nutshell, the method of Saint Loubert Bié (1998) and Chong (2016) to construct a solution to (3.2) is this: first, one defines the integral operator that maps to

| (3.3) |

when the right-hand side is well defined, and to otherwise. Then one establishes moment estimates in such a way that becomes, at least locally in time, a contractive self-map on some -space. Then the Banach fixed point theorem yields existence and uniqueness of solutions. However, if , the problematic point is that the -th order moment of is typically infinite, while taking the -th order moment, which would be finite, produces a non-contractive iteration. The idea in this article to circumvent this is therefore to consider a modified Picard iteration: we still take -th moment estimates (in order to keep contractivity) but stop the processes under consideration before they become too large (in order to keep the -th moments finite). The following lemma makes our stopping strategy precise.

Lemma 3.2.

Let with some and define for the stopping times

| (3.4) |

where are the stopping times in M1. If is the number in M3 and , then a.s. for all and a.s. for .

Proof.

Define and

In other words, forms a partition of into concentric spherical shells of Lebesgue measure . Then there exists a constant which is independent of and such that for all and . Next, observe that for all we a.s. have

If we show that the last expression is finite a.s., we can conclude, on the one hand, that a.s. for all . On the other hand, it also implies that for because then, for any , the left-hand side of the previous display would be as soon as is large enough. So with and using the Borel-Cantelli lemma, it remains to verify that

| (3.5) |

Indeed,

The last term is of order . Since , it is summable and leads to (3.5).

The stopping times in the previous lemma are reminiscent of a well established technique of solving stochastic differential equations driven by semimartingales (Protter, 2005). Here, if the jumps of the driving semimartingale lack good integrability properties, one can still solve the equation until the first big jump occurs, then continue until the next big jump occurs and so on, thereby obtaining a solution for all times. In principle, this is exactly the idea we employ in the proof of Theorem 3.1. However, in our tempo-spatial setting, the law of is typically not equivalent to the law of its truncation at a fixed level on any set : Infinitely many big jumps usually occur already immediately after time zero. This is the reason why in Lemma 3.2 above we have to take a truncation level that increases sufficiently fast in the spatial coordinate.

As a next step we introduce for each a truncation of by

| (3.6) |

An important step in the proof of Theorem 3.1 is to prove that (3.2) has a solution when is substituted by . To this end, we establish several moment estimates.

Lemma 3.3.

Let be arbitrary but fixed and the integral operator defined in the same way as in (3.3) but with instead of . Under M1–M3 and A1–A5 the following estimates hold.

-

(1)

For all there exists a constant such that for all and we have

(3.7) -

(2)

For all there exists a constant such that for all and with we have

Proof.

Both parts can be treated in a similar fashion. We only prove (1). Starting with the case , we use the fact that , and to decompose where

| (3.8) |

In the following denotes a positive constant independent of (but possibly dependent on , , and ). Recalling that unless , using the Burkholder-Davis-Gundy inequalities and applying the inequality for and to the Poisson integral, we deduce for all that

Next, by Hölder’s inequality, we obtain

which completes the proof for the case .

For we have by hypothesis . Therefore,

We need two further preparatory results. The first one is classic. Henceforth, we denote by the -dimensional normal distribution with mean vector and covariance matrix .

Lemma 3.4.

If is an -distributed random variable, then for every we have

The second lemma determines the size of certain iterated integrals. It is proved by a straightforward induction argument, which is omitted.

Lemma 3.5.

Let and . Then we have for every that ()

We are now in the position to prove the existence of a solution to (3.2) under the conditions of Theorem 3.1.

Proof of Theorem 3.1.

(i) We first prove that Equation (3.2) has a solution in when is replaced by as defined in (3.6). In order to do so, we choose the number in such a way that and , which is possible by hypothesis A4. For reasons of readability, we do not index the subsequent processes with in this part of the proof, but only later when the dependence on matters. We define a Picard iteration scheme by and

| (3.9) |

for . By Lemma 6.2 in Chong (2016) we can always choose a predictable version of . Then, since and for all and , Lemma 3.3(1) yields that for all and . Now define for , which by Lemma 3.3(2) satisfies

for all . If we iterate this times, we obtain for all (we abbreviate )

| (3.10) |

We take a closer look at the integrals with respect to . Define for and and . Then, by Hölder’s inequality, those integrals are bounded by

| (3.11) |

We observe that is the density of the -distribution, while is that of the -distribution. Here is the -dimensional identity matrix. Now let be independent random variables such that has an -distribution when and an -distribution when (with ). Then, with

we use Lemma 3.4 and the fact that and in order to derive

The last term no longer depends on and . Thus the last expression in (3.11) is bounded by

| (3.12) |

We insert this result back into (3.10) and apply Lemma 3.5 to obtain

| (3.13) |

valid for all . Together with our choice of (see the beginning of the proof), it follows that

implying that there exists some such that for every as . This solves (3.2) with instead of . Indeed, the previous calculations actually show that for every , forms a Cauchy sequence with respect to the Daniell mean . Therefore, it must converge to its limit with respect to the Daniell mean, pointwise for . In particular, the stochastic integrals with respect to converge to each other, showing that is a solution.

(ii) As a next step we define for the operators

| (3.14) | ||||||

| (3.15) |

hereby setting as soon as . Then apart from the solution we found in (i) there exists no which also satisfies and for which there exists some such that converges to in as . Indeed, by the same arguments as above one can show that is bounded by the right-hand side of (3.13) to the power of , possibly with another constant . So taking the limit proves .

The uniqueness statement in part (ii) of the proof above can also be formulated for (3.2).

Theorem 3.6.

Of course, this uniqueness result is quite weak: it does not say much about how other potential solutions to (3.2) compare with the one we have constructed. Let us explain why we are not able to derive uniqueness in, say, although the Picard iteration technique — via the Banach fixed point theorem — usually yields existence and uniqueness at the same time. The reason is simply the following: on the one hand, the stopping times from Lemma 3.2 allow us to obtain locally finite -estimates. On the other hand, as one can see from Lemma 3.3, an extra factor appears in these estimates. So for any with the right-hand side of (3.7) increases faster in than the input . Consequently, we cannot find a complete subspace of containing on which the operator is a self-map, which is a crucial assumption for the Banach fixed point theorem.

Nevertheless, the next result demonstrates that the solution constructed in Theorem 3.1 is the “natural” one in terms of approximations.

Theorem 3.7.

Let be the solution process to (3.2) as constructed in Theorem 3.1 where the stopping times are given by (3.4). Furthermore, consider the following two ways of truncating the noise :

-

(1)

, -

(2)

.

In both cases, if denotes the unique solution to (3.2) with replaced by that belongs to for all (see Theorems 3.1 and 3.5 in Chong (2016)), then we have for all and

From another point of view, Theorem 3.7 paves the way for simulating from the solution of (3.2). In fact, in Chen et al. (2016) different methods are suggested for the simulation of (3.2) with the noise as given in the first part of the previous theorem. The approximations in that paper were shown to be convergent in an -sense. Thus, letting increase in parallel, these approximations will then converge to the solution of (3.2) with the untruncated noise , at least in .

Proof of Theorem 3.7.

(i) We first prove the case (1). Let , and be fixed. Then the arguments in the proof of Theorem 3.1 reveal that

where is given by (3.9) and is defined in the same way but with instead of , and is the measure specified through (3.6) with replaced by . Therefore, it suffices to prove that for every we have as . To this end, we observe that

| (3.16) |

Furthermore, since is fixed and the function grows at most polynomially in for any , it follows that for all when is chosen large enough (we may assume that ). Therefore, recalling the notation , we obtain for

Using slightly modified calculations, one can derive the final bound also for and show that

with a constant independent of . Plugging these estimates into (3.16), we obtain by iteration for all ( and )

The integrals in the last line do not depend on and would be defined even without the indicator function. Hence they converge to as by dominated convergence.

(ii) If is defined as in (2), we first notice that for every there exists such that a.s. where

Therefore, Theorem 3.5 in Chong (2016) which states that there exists a unique solution to (3.2) with noise that belongs to for all automatically implies that this solution is also the unique one that belongs to for all . The actual claim is proved in basically the same way as in (1), except that in the moment estimate of one has to replace the indicator by , which obviously does not effect the final convergence result.

Until now, the solution to (3.2) that we have constructed in Theorem 3.1 only has finite -th moments, locally uniformly in space and locally uniformly in time until for any and . But does possess any finite moments until where is the original stopping time from hypothesis M1? If is a Lévy basis, this would be the question whether has finite moments up to any fixed time without stopping. Furthermore, under which conditions do they remain bounded and not blow up in space? The next theorem provides a sufficient condition for these statements to be true.

Theorem 3.8.

We need an analogue of Lemma 3.3 for moments of order .

Lemma 3.9.

Proof.

In principle the proof follows the same line of reasoning as Lemma 3.3. If , the idea is to split the Itô basis into three parts:

The -th moments of the integrals against the first two parts can be estimated as in Lemma 3.3. Since replaces , the factor can be omitted throughout. For the integral against the third part in the decomposition above, its -norm is bounded by its -norm, which can be treated as in Lemma 3.3. Again, the factor is not needed because the jump sizes are at most . Next, if but , we can proceed in the same way except that we replace the first and second part in the decomposition of by

respectively. Finally, if , we have that

The result then follows in a similar way if we switch to the -th moment for the first term. The statement regarding is evident because the estimates above hold for all measures with only a subset of jumps of .

Proof of Theorem 3.8.

Let and be the process defined in (3.9). Then, because we have with , Lemma 3.9 implies that for every we have

with a constant independent of and . Since , we can apply Lemma 6.4 in Chong (2016) to deduce

Since is the limit in of as and is piecewise equal to , the assertion follows and belongs to for all .

How do the results and methods described above extend to more general equations than (3.2), for example, when satisfies A3 with some other kernel than the heat kernel? Immediately one notices the following difference between the case and : while in the former case one obtains existence and uniqueness as soon as

| (3.17) |

for all (see Chong (2016), Theorem 3.1), we need to put a much stronger assumption in the latter case. Namely, since an extra factor appears in each iteration step in the proof of Theorem 3.1, the kernel must decay faster in than any polynomial. Thus, our methods will not work merely under an integrability assumption like (3.17). For example, fractional equations as considered, for example, in Balan (2014), Peszat and Zabczyk (2007) or Wu and Xie (2012) are outside the scope of this paper when . However, our results can be extended to quite general parabolic stochastic PDEs. More precisely, consider the partial differential operator given by

| (3.18) |

with and suitable bounded continuous functions . Under regularity conditions (see Peszat and Zabczyk (2007), Theorem 2.6, and Eidelman and Zhitarashu (1998), Theorem VI.2), the operator (3.18) admits a fundamental solution satisfying

| (3.19) |

for with some strictly positive constants and independent of . With this at hand, we can now extend the previous results to incorporate the case where satisfies (3.19). In fact, we can go one step further and consider kernels bounded by generalized Gaussian densities (Gómez et al., 1998) of the form

| (3.20) |

for some parameters and a constant chosen in such a way that becomes a probability density function on for every fixed .

Theorem 3.10.

Proof.

The only step that has to be modified in the proofs when the heat kernel is replaced by is the estimation of the integrals in (3.11). Because

and

we obtain in the end instead of (3.12) the bound

and instead of (3.13) the estimate

By (3.21) we can choose in such a way that such that the previous bound converges to as tends to infinity.

Acknowledgement

I wish to thank Jean Jacod for his constructive comments and suggestions.

References

- Albeverio et al. (1998) S. Albeverio, J.-L. Wu, and T.-S. Zhang. Parabolic SPDEs driven by Poisson white noise. Stoch. Process. Appl., 74(1):21–36, 1998.

- Applebaum and Wu (2000) D. Applebaum and J.-L. Wu. Stochastic partial differential equations driven by Lévy space–time white noise. Random Oper. Stoch. Equ., 8(3):245–259, 2000.

- Balan (2014) R.M. Balan. SPDEs with -stable Lévy noise: A random field approach. Int. J. Stoch. Anal., 2014. Article ID 793275, 22 pages.

- Barndorff-Nielsen et al. (2011) O.E. Barndorff-Nielsen, F.E. Benth, and A.E.D. Veraart. Ambit processes and stochastic partial differential equations. In G. Di Nunno and B. Øksendal, editors, Advanced Mathematical Methods for Finance, pages 35–74. Springer, Berlin, 2011.

- Bichteler and Jacod (1983) K. Bichteler and J. Jacod. Random measures and stochastic integration. In G. Kallianpur, editor, Theory and Application of Random Fields, pages 1–18. Springer, Berlin, 1983.

- Carmona and Molchanov (1994) R.A. Carmona and S.A. Molchanov. Parabolic Anderson Model and Intermittency. American Mathematical Society, Providence, RI, 1994.

- Chen et al. (2016) B. Chen, C. Chong, and C. Klüppelberg. Simulation of stochastic Volterra equations driven by space–time Lévy noise. In M. Podolskij, R. Stelzer, S. Thorbjørnsen, and A.E.D. Veraart, editors, The Fascination of Probability, Statistics and their Applications, pages 209–229. Springer, Cham, Switzerland, 2016.

- Chong (2016) C. Chong. Lévy-driven Volterra equations in space and time. J. Theor. Probab., 2016. In press.

- Chong and Klüppelberg (2015) C. Chong and C. Klüppelberg. Integrability conditions for space–time stochastic integrals: Theory and applications. Bernoulli, 21(4):2190–2216, 2015.

- Corwin (2012) I. Corwin. The Kardar-Parisi-Zhang equation and universality class. Random Matrices: Theory Appl., 1(1):76 pages, 2012.

- Davies et al. (2004) I.M. Davies, A. Truman, and H. Zhao. Stochastic heat and Burgers equations and the intermittence of turbulence. In R.C. Dalang, M. Dozzi, and F. Russo, editors, Seminar on Stochastic Analysis, Random Fields and Applications IV, pages 95–110. Birkhäuser, Basel, 2004.

- Dawson (1993) D. Dawson. Measure-valued Markov processes. In P.L. Hennequin, editor, École d’Été de Probabilités de Saint Flour XXI - 1991, pages 1–260. Springer, Berlin, 1993.

- Dellacherie and Meyer (1982) C. Dellacherie and P.-A. Meyer. Probabilities and Potential B. North-Holland, Amsterdam, 1982.

- Eidelman and Zhitarashu (1998) S.D. Eidelman and N.V. Zhitarashu. Parabolic Boundary Value Problems. Birkhäuser, Basel, 1998.

- Gómez et al. (1998) E. Gómez, M.A. Gómez-Villegas, and J.M. Marín. A multivariate generalization of the power exponential family of distributions. Commun. Stat. Theory Methods, 27(3):589–600, 1998.

- Hairer (2013) M. Hairer. Solving the KPZ equation. Ann. Math., 178(2):559–664, 2013.

- Holden et al. (2010) H. Holden, B. Øksendal, J. Ubøe, and T. Zhang. Stochastic Partial Differential Equations. Springer, New York, 2nd edition, 2010.

- Jacod and Shiryaev (2003) J. Jacod and A.N. Shiryaev. Limit Theorems for Stochastic Processes. Springer, Berlin, 2nd edition, 2003.

- Jones (1999) B.J.T. Jones. The origin of scaling in the galaxy distribution. Mon. Not. R. Astron. Soc., 307(2):376–386, 1999.

- Khoshnevisan (2014) D. Khoshnevisan. Analysis of Stochastic Partial Differential Equations. American Mathematical Society, Providence, RI, 2014.

- Liu and Röckner (2015) W. Liu and M. Röckner. Stochastic Partial Differential Equations: An Introduction. Springer, Cham, Switzerland, 2015.

- Mueller (1998) C. Mueller. The heat equation with Lévy noise. Stoch. Process. Appl., 74(1):67–82, 1998.

- Mueller (2015) C. Mueller. Stochastic PDE from the point of view of particle systems and duality. In R.C. Dalang, M. Dozzi, F. Flandoli, and F. Russo, editors, Stochastic Analysis: A Series of Lectures, pages 271–295. Birkhäuser, Basel, 2015.

- Mytnik (2002) L. Mytnik. Stochastic partial differential equation driven by stable noise. Probab. Theory Relat. Fields, 123(2):157–201, 2002.

- Peszat and Zabczyk (2007) S. Peszat and J. Zabczyk. Stochastic Partial Differential Equations with Lévy Noise. Cambridge University Press, Cambridge, 2007.

- Protter (2005) P.E. Protter. Stochastic Integration and Differential Equations. Springer, Berlin, 2nd edition, 2005.

- Saadi and Benbaziz (2015) N. El Saadi and Z. Benbaziz. On the existence of solutions for a nonlinear stochastic partial differential equation arising as a model of phytoplankton aggregation. Preprint available under arXiv:1507.06784 [math.AP], 2015.

- Saint Loubert Bié (1998) E. Saint Loubert Bié. Étude d’une EDPS conduite par un bruit poissonnien. Probab. Theory Relat. Fields, 111(2):287–321, 1998.

- Tuckwell and Walsh (1983) H.C. Tuckwell and J.B. Walsh. Random currents through nerve membranes. Biol. Cybern., 49(2):99–110, 1983.

- Walsh (1981) J.B. Walsh. A stochastic model of neural response. Adv. Appl. Probab., 13(2):231–281, 1981.

- Walsh (1986) J.B. Walsh. An introduction to stochastic partial differential equations. In P.L. Hennequin, editor, École d’Été de Probabilités de Saint Flour XIV - 1984, pages 265–439. Springer, Berlin, 1986.

- Wu and Xie (2012) J.-L. Wu and B. Xie. On a Burgers type nonlinear equation perturbed by a pure jump Lévy noise in . Bull. Sci. Math., 136(5):484–506, 2012.