Optimal Auctions with Convex Perceived Payments

Abstract

Myerson derived a simple and elegant solution to the single-parameter revenue-maximization problem in his seminal work on optimal auction design assuming the usual model of quasi-linear utilities. In this paper, we consider a slight generalization of this usual model—from linear to convex “perceived” payments. This more general problem does not appear to admit a solution as simple and elegant as Myerson’s.

While some of Myerson’s results extend to our setting, like his payment formula (suitably adjusted), and the observation that “the mechanism is incentive compatible only if the allocation rule is monotonic,” others do not. For example, we observe that the solutions to the Bayesian and the robust (i.e., non-Bayesian) optimal auction design problems in the convex perceived payment setting do not coincide like they do in the case of linear payments. We therefore study the two problems in turn.

Myerson finds an optimal robust (and Bayesian) auction by solving pointwise: for each vector of virtual values, he finds an optimal, ex-post feasible auction; then he plugs the resulting allocation, which he first verifies is monotonic, into his payment formula. This strategy relies on a key theorem, that expected revenue equals expected virtual surplus, which does not hold in our setting. Still, we derive an upper and a heuristic lower bound on expected revenue in our setting. These bounds are easily computed pointwise, and yield monotonic allocation rules, so can be supported by Myerson payments (suitably adjusted). In this way, our bounds yield heuristics that approximate the optimal robust auction, assuming convex perceived payments.

In tackling the Bayesian problem, we derive a mathematical program that improves upon the default formulation in that it has only polynomially-many payment variables; however, it still has exponentially-many allocation variables and ex-post feasibility constraints. To address this latter issue, we also study the ex-ante relaxation, which requires only polynomially-many constraints, in all. Specifically, we present a closed-form solution to a straightforward relaxation of this relaxation. Then, following similar logic, we present a closed-form upper bound and a heuristic lower bound on the solution to the (ex-post) robust problem. As above, the resulting allocation rules can then be supported by Myerson payment rules, yielding faster heuristics than the greedy ones for approximating the optimal robust auction. Interestingly, all our closed-form solutions are rather intuitive: they allocate in proportion to values (or virtual values).

We close with experiments, the final set of which massages the output of one of the closed-form heuristics for the robust problem into an extremely fast, near-optimal heuristic solution to the Bayesian optimal auction design problem.

1 Introduction

In a seminal paper, Myerson [8] provides a simple and elegant solution to a fundamental problem in optimal auction design: the single-parameter revenue-maximization problem, assuming quasi-linear utilities with linear payments: i.e., , where is ’s private value, is his allocation, and is his payment to the auctioneer. Generally speaking, and are not expressed in the same units; hence, we can think of as a conversion factor, converting units of the good being allocated into units of payment (often, money). In this paper, we investigate the extent to which Myerson’s observations carry over to the case of convex “perceived”111There are two potential payments for bidders to consider in auction problems: those paid to the auctioneer, and those subtracted from in the bidders’ utility functions. In general, these two payments need not be equated. While we choose to label the former payments (made to the auctioneer) “actual,” and the latter, “perceived,” we could just as well have taken the perspective of the bidders in our naming, and referred to the former as “perceived,” and the latter as “actual.” We also considered referring to perceived payments instead as “costs” instead of payments, which they rightfully are. But as our results include a payment formula for these costs which closely relates to Myerson’s original payment formula, it seemed that qualifying the term payment would be more illuminating. payments. Specifically, we consider utilities of the form , where is a convex function that describes payments that perceives, which we distinguish from itself (’s “actual” payment to the auctioneer). Although our results apply to any convex function , as a concrete running example throughout this paper, we assume , for all bidders .

Our problem formulation is motivated by a reverse auction setting in which a government with a fixed budget is offering subsidies (in euros, say) to power companies in exchange for a supply of renewable energy (in watts, say). We assume the power companies’ utility functions take this form: , where is some fraction of the total budget in euros, and is some deliverable amount of power in watts. As already mentioned, is a conversion factor, in this case from euros to watts. The assumption that is convex reflects the fact that energy production costs may not be linear; for example, because of diseconomies of scale, it may be the case that as more energy is produced, further units become more and more expensive to produce.

Note that multiplying by yields a more familiar utility function—that of the forward auction setting: , with utility measured in units of power, rather than money. From this point of view, defining perceived payments can be interpreted as an assumption of risk aversion. A power company might be risk averse because it might be concerned that it has overestimated its own value, or it might worry that the government won’t actually deliver on the promised subsidies.

Another problem which also fits into our framework is the problem of allocating a fixed block of advertising time to retailers during the Superbowl. In this application, an advertiser’s utility is calculated by converting its allocation, in time, into dollars via its private value, and then subtracting the cost of production: . Here, dividing by yields the utility function , which, under the assumption that , again yields the interpretation that production costs are convex; for example, it may be the case that an advertisement that is three times as long as another takes nine times as long to produce.

In both of these problems, the auctioneer’s objective is to maximize its total revenue: , where is distributed according to some commonly known joint distribution. Specifically, in the energy problem, the government’s objective is to maximize the amount of power produced, subject to its budget constraint. In the advertising problem, the television network is seeking to maximize its revenue for selling a fixed block of advertising time during the Superbowl (or any other television program).

Summary of Results

In our setting, in which perceived payments are convex, some of Myerson’s observations, such as “the mechanism is incentive compatible only if the allocation rule is monotonic,” continue to hold. So does his payment formula (suitably adjusted).

But others do not. The solutions to the robust (i.e., non-Bayesian) and Bayesian optimal auction design problems (in the latter, incentive compatibility and individual rationality need only hold in expectation) do not coincide in our setting like they do in the linear-payment setting. Moreover, bidder surplus is no longer an upper bound on revenue, and expected revenue no longer equals expected virtual surplus.

We do show, however, that revenue can be upper bounded by a quantity we call pseudo-surplus, and that expected revenue can be heuristically lower bounded by expected virtual surplus. Because it is straightforward to compute these bounds (i.e., greedy algorithms suffice), we propose the following heuristic procedure for the robust optimal auction design problem: 1. solve greedily for a feasible allocation that achieves the upper or heuristic lower bound, and 2. plug that allocation into Myerson’s payment formula to ensure incentive compatibility and individual rationality. We show experimentally that the performance of these heuristics can be near-optimal, and that they are faster than solving the corresponding revenue-maximizing mathematical programs using standard solvers.

Our heuristic that lower bounds the solution to the robust optimal auction design problem also heuristically lower bounds the Bayesian problem, because in the latter the constraints are strictly weaker. Regardless, we prove a theorem for the Bayesian setting that allows us to simplify the revenue-maximizing mathematical program from one that has exponentially-many payment variables to one that has only polynomially-many.

Even so, a Bayesian optimal auction still involves exponentially-many allocation variables and requires satisfying exponentially-many ex-post feasibility constraints. To address this latter concern, we also study the ex-ante relaxation, which requires only polynomially-many constraints, in all. Specifically, we present a closed-form solution to a straightforward relaxation of this relaxation, which yields a closed-form upper bound on the ex-ante Bayesian problem. Intuitively, this solution allocates in proportion to virtual values.

Lastly, following similar logic, we present a closed-form upper bound and a heuristic lower bound on the solution to the (ex-post) robust problem. (Interestingly, these closed-form solutions allocate in proportion to values.) An analog of the aforementioned greedy heuristics then applies, in which the closed-form allocation rule is supported by Myerson payment rules, yielding closed-form heuristics that approximate the optimal robust auction. In our final set of experiments, we massage the output of one of these closed-form heuristics for the robust problem using the payment variables in the simpler formulation of the Bayesian problem to arrive at a near-optimal heuristic solution to the Bayesian problem, which is faster in practice than standard solvers (and faster than our greedy heuristic).

Related Work

Vickery [11] showed that auctions in which the highest bidder wins and pays the second-highest bid incentivizes bidders to bid truthfully. Myerson [8] showed that in the single-parameter setting, with the usual utility function involving linear payments, expected revenue is maximized by a Vickrey auction with reserve prices. Our setting is not captured by Myerson’s classic characterization because payments in our model are convex.

The technical difficulties that arise in our setting are similar in spirit to the ones faced by Pai and Vohra [9] when designing optimal auctions for budget-constrained bidders. If for some , then when . Additionally, if ever exceeds , utility quickly approaches . Therefore, we can interpret a utility function with convex perceived payments as a continuous approximation of that of a budget-limited agent whose utility is whenever her payment exceeds her budget.

Our model also has strong connections with the literature on optimal auctions for risk-averse buyers (see Maskin and Riley [7]), since the fact that utility is a concave function in terms of payments can be seen as a form of risk aversion. In fact, our model is captured by their generic formulation if the good to be allocated is indivisible. Optimal auctions for risk-averse bidders are notoriously hard to characterize in theory. Developing and testing theoretically-inspired heuristics may prove to be a fruitful alternative.

The idea of translating a reverse auction into a direct auction by multiplying utility by the private parameter was previously proposed in the literature on optimal contests (see, for example, Chawla, et al. [3] or DiPalantino and Vojnovic [4]).

Procuring services subject to a budget constraint is also the subject of the literature on budget-feasible mechanisms initiated by Singer [10]. However, in this literature, the service of each seller is fixed and the utility of the buyer is a combinatorial function of the set of sellers the buyer picks. In our setting, each seller can produce a different level of service (i.e., amount of energy) by incurring a different cost, so the buyer picks not only a set of sellers, but a level of service that each seller should provide as well. This renders the two procurement models incomparable.

Our model is also related to the parameterized supply bidding game of Johari and Tsitsiklis [6], where firms play a game in which they submit a single-parameter family of supply functions. There, the amount each firm is asked to produce is decided via a non-truthful mechanism, and efficiency at equilibrium is analyzed. Here, we consider the design of truthful mechanisms and we study a different objective, but we also restrict attention to single-parameter families of supply functions .

In principle, some of our problem formulations can be solved using Border’s characterization of interim feasible outcomes [2] and an ellipsoid type algorithm with a separation oracle. However, such mechanisms tend to be computationally expensive. Here, we seek fast allocation heuristics with potential economic justification, such as virtual-value-based maximizations. Virtual-value-maximizing approximations to optimal auction design were also studied recently by Alaei, et al. [1] in the context of multi-dimensional mechanism design, and from a worst-case point of view. Proving worst-case approximation guarantees for our heuristics is an interesting future direction.

We close this discussion of related work by pointing out that the case of a finitely divisible good, such as euros or seconds, which motivates the current work, lies along a continuum between an indivisible and an infinitely divisible good. An optimal solution that is subject to a discretization constraint (i.e., finitely divisible) can differ from a corresponding optimal continuous solution (i.e., infinitely divisible) by at most a discretization term. For a budget that is small relative to this discretization factor, the magniture of the error is large, so the budget behaves more like an indivisible good; but as a budget increases relative to the discretization factor, the magnitude of the error decreases, so the budget behaves more like an infinitely divisible good.

2 Our Model

Consider a reverse auction with bidders. Each bidder has a private type that is independently drawn from some distribution . Let be the set of all possible type vectors, and let be the distribution over type vectors . Let be a vector of bids, where the th entry is bidder ’s bid. For , we use the notation , where . Similarly, we use the notation , where , and , where .

Given vector of reports , a mechanism produces an allocation rule that typically depends only on those reports, together with a payment rule , which, in general, can depend on both the reports and the allocation rule. Where it is clear from context, we suppress dependence of the payment rule on , and write only . We also do the same for payment terms , which comprise payment rule , and refer to bidder ’s payment as .

We define bidder ’s utility function as , where is private information, known only to bidder , and is a function that converts payments, in units such as energy, to the units of the good being allocated, such as euros. If we assume , then maximizing the function also maximizes . Consequently, hereafter we assume forward utility functions of this form:

| (1) |

The shape of the utility function varies with the choice of : for example, it can be linear if we choose to be the identity function, or concave if we choose . Figures 1 and 2 plot sample utility functions for these two choices of .

For readability, we usually write instead of . Furthermore, we refer to the rule as the perceived payment rule, as these are payments the bidders impose upon themselves. Likewise, we think of as an actual payment rule, as these are payments the bidders actually pay to the auctioneer. (But we usually omit the descriptor “actual,” as what it modifies is the actual payment rule!)

With this general utility function in mind, we proceed to formulate the optimal auction design problem: we seek the revenue-maximizing, ex-post feasible auction in which it is optimal for bidders to bid truthfully, and it is rational for them to participate. Once again, Myerson solved this problem in the quasi-linear case, assuming linear payments.

2.1 Constraints

In this section, we formalize the constraints we will impose on an optimal auction design. Because we restrict our attention to incentive compatible auctions, where it is optimal to bid truthfully, we write instead of . (As usual, the variables comprise the perceived payment rule .)

A mechanism is called incentive compatible (IC) if each bidder maximizes her utility by reporting bids that are equal to values : , , and ,

| (2) |

Individual rationality (IR) ensures that bidders have non-negative utilities: , , and ,

| (3) |

Next, we define IC and IR in expectation (with respect to ). To do so, we introduce interim allocation and interim perceived payment variables, respectively: and . These variables comprise the interim allocation and perceived payment rules, and .

We call a mechanism Bayesian incentive compatible (BIC) if utility is maximized by truthful reports in expectation: and ,

| (4) |

Bayesian individual rationality (BIR) insists on non-negative utilities in expectation: and ,

| (5) |

We say a mechanism is ex-post feasible (XP) if it never overallocates: ,

| (6) |

Ex-ante feasibility (XA) is satisfied if, in expectation, the mechanism does not over-allocate:

| (7) |

Finally, we require that , , and .

2.2 Revenue Maximization

The robust revenue-maximization problem (RRM) is to maximize total expected payments (i.e., ), subject to IR, IC, and ex-post feasibility. RRM is expressed as a mathematical program in Section C.1.1. A typical relaxation of this problem insists on ex-ante feasibility only.

Likewise, the Bayesian revenue-maximization problem (BRM) is to maximize total expected payments subject to BIR, BIC, and ex-post feasibility (or ex-ante feasibility). BRM with ex-post feasibility is expressed as a mathematical program in Section C.2.1. BRM with ex-ante feasibility is expressed as a mathematical program in Section C.3.1.

In both RRM and BRM, there are exponentially-many ex-post feasibility constraints, and exponentially-many allocation and payment variables. However, revenue maximization subject to BIC and BIR but only ex-ante feasibility involves only one feasibility constraint and polynomially-many interim allocation and payment variables.

In this paper, we assume (or , for short). This choice of perceived payments yields quadratic constraints. While small instances of the quadratic programs that express BRM and RRM can be solved by standard mathematical programming solvers, this approach does not scale. We are interested in finding scalable algorithms that produce approximately-optimal solutions to these problems.

3 Myerson’s Payment Formula

We start by providing a straightforward adaptation of Myerson’s payment formula [8] to the case where the utilities are of the concave form of interest.

For consistency with our implementations,222True to our profession—computer science—we have implemented all mechanisms discussed in this paper. we describe our contributions under the assumption that type distributions are discrete, but our theoretical results are in no way contingent on this assumption. Specifically, we assume the distribution of values is drawn from the discrete type space , of cardinality , where for , and we let . Furthermore, let be the probability of , let be the probability of , and let be the probability of .

Myerson’s payment theorem, which takes as a starting point the bidders’ utility functions (i.e., Equation (1)), applies immediately to the perceived payment rules and :

Theorem 3.1.

Assume bidders’ utilities take the form of Equation (1). A mechanism is IC and IR iff for each bidder :

-

•

the allocation rule is monotone, i.e., and , ; and

-

•

the perceived payment rule is given by: and ,

(8) where .

Likewise, in the Bayesian setting, a mechanism is BIC and BIR iff for each bidder :

-

•

the allocation rule is monotone, i.e., , ; and

-

•

the perceived payment rule is given by: ,

(9) where .

Remark 3.2.

The monotonicity of the allocation rule ensures that the perceived payment rule is also monotonic. Specifically, the perceived payment associated with a bidder of type is at least as great as the perceived payment associated with a bidder of type :

But as our goal is to maximize revenue, we are interested not in the bidders’ perceived payments, but rather in the actual payments to the auctioneer, namely , the latter of which is comprised of variables . In the robust problem, the generalization is straightforward: since , it follows that is simply the square root of .

In the Bayesian problem, however, need not equal , because . Nonetheless, in Section 6, we successfully derive an interim payment function for which , so that is the square root of .333In Algorithms 7) and 10, the payment rule , is comprised of variables .

Corollary 3.3.

Under the assumptions of Theorem 3.1, for ,

| (10) |

Likewise, given an interim payment function such that , then

| (11) |

Myerson’s payment formula is immensely powerful. It gives rise to a procedure for optimal auction design that at first glance borders on the miraculous. The procedure is thus: First, solve for an allocation rule that optimizes your objective (surplus, revenue, what have you), subject only to ex-post feasibility. Second, check for monotonicity. If the optimal allocation rule is indeed monotonic, then you are home free; you need only plug that allocation rule into Myerson’s payment formula and you will have imposed incentive compatibility and individual rationality without sacrificing one ounce of optimality!. In other words, given a monotone allocation rule, IC and IR are yours for the taking. That is the essence of Myerson’s approach, and something we exploit heavily in this work.

4 Robust vs. Bayesian Optimal Auctions

Another of the more surprising facts that Myerson discovered about the optimal auction design problem (assuming linear perceived payments) is that the total expected revenue in the robust and Bayesian problems are equivalent. It is clear that the value of a solution to BRM must be at least that of RRM, since the objectives are the same while BRM’s constraints are weaker. It is the other direction, namely that the value of a solution to BRM never exceeds that of RRM, which is surprising. This latter relies on the assumption that perceived payments, and hence utilities, are linear, and therefore does not hold in our setting with convex perceived payments, and hence concave utilities, which we now proceed to show via counterexample.

4.1 Robust Revenue Bayesian Revenue

We begin our analysis of BRM vs. RRM with convex perceived payments by demonstrating via example that solutions to BRM can strictly exceed those of RRM when . Therefore, an optimal solution to RRM does not generally yield an optimal solution to BRM, although it does yield an immediate lower bound.

Example 4.1.

Suppose we have symmetric bidders, where for each bidder , , and for each value , .

RRM

Our goal is to maximize revenue, while satisfying IC, IR, and the ex-post feasibility constraints. This mathematical program appears in Section C.1.1.

We know from IR that is upper-bounded by . So when , . So we can set , for all .

When one bidder, say , has type , and the other bidder has type , we maximize total payments by setting .

When both bidders have type , by Equation (10), . Therefore, total payments are maximized when .

Thus, in the robust problem, the following allocation is optimal:

Computing payments according to Equation (10) yields:

Therefore, the total expected revenue in the robust problem is:

BRM

Our goal is to maximize revenue, while satisfying BIC, BIR and the ex-post feasibility constraints. This mathematical program appears in Section C.2.1.

We know from BIR that is upper-bounded by . So when , . So we can set , which implies that , for all . Additionally, since , this also means that , for all .

When , we want to maximize so that we can maximize , as this will maximize the payments the auctioneer collects when a bidder has type . For bidder 1:

We can set to , which leaves only to be determined. Since the setting is symmetric, we can also set , leaving also to be determined.

Rewriting the BIR constraints using payment terms explicitly, we have

Equivalently,

Combining the inequalities yields

Subject to this constraint, we can maximize total payments,

by equating each of the four payment terms, so that .

In summary, the following payment rule maximizes revenue:

This payment rule implies a symmetric allocation in which . Therefore, this BRM problem can be solved using the same allocation rule as the corresponding RRM problem:

Furthermore, the interim allocation rule is given by:

From this interim allocation rule, we derive the interim payment rule according to Equation (11):

Observe that , for all ; likewise for 100.

Finally, the total expected revenue in the Bayesian problem (which we can compute using either the or the ) is:

Since , it follows that . Thus, we conclude that the value of the optimal solution to a Bayesian problem can exceed the value of the optimal solution to the corresponding robust problem, assuming convex perceived payments, and hence concave utilities. ∎

Remark 4.2.

More generally, with two types, and , the total expected robust revenue is , while the total expected Bayesian revenue is , making BRM greater than RRM by a factor of

An open question at present is how bad this ratio becomes as the number of types increases.

Remark 4.3.

Until now, we have not discussed the possibility of randomized auctions. Randomization is not necessary in the linear-payment setting because there always exists an optimal allocation rule that is integral. But in our examples, the optimal allocation rule is fractional. While a fractional allocation rule does not pose a problem in the case of an infinitely divisible good, in the case of an indivisible good, strictly more revenue can be obtained by interpreting the allocations as probabilities, and then allocating that one good at random based on these probabilities: i.e., randomization adds power assuming convex perceived payments.

Likewise, in our case—the case of a finitely divisible good (i.e., a budget)—randomization again adds power, assuming convex perceived payments. However, that power decreases as the discretization factor decreases with respect to the budget. Specifically, for a discretization factor of (say €0.01), given a budget of (say 1 million euro), the potential gain due to randomization is at most (which is €, in our example). (We prove this claim in Appendix A.)

4.2 Robust Pseudo-surplus Bayesian Pseudo-surplus

In addition to noting the equivalence of revenue in the robust and Bayesian (linear perceived payment) problems, Myerson also noted the equivalence of bidder surplus in these two problems. Bidder surplus is a quantity of interest in the usual setting with linear perceived payments, even when studying revenue maximization, because bidder surplus upper bounds revenue. In our convex perceived payment setting, however, bidder surplus does not upper bound revenue (see Example 5.1). Nonetheless, we introduce a quantity we call pseudo-surplus, which does upper bound revenue (in both the robust and the Bayesian problems).

When perceived payments are linear, so that , IR implies that . The quantity on the left-hand side of this inequality is called bidder ’s surplus. Taking expectations and summing over all bidders yields expected bidder surplus as an upper bound on expected revenue:

| (12) |

When perceived payments are quadratic, so that , IR implies that . We call the quantity on the left-hand side of this inequality bidder ’s (robust) pseudo-surplus. After taking expectations and summing over all bidders, as above, we find that expected revenue is upper bounded by expected bidder pseudo-surplus:

| (13) |

Likewise, in the Bayesian problem, by BIR, and , . When perceived payments are quadratic, if there exists an interim payment function such that , as in Corollary 3.3, then , so that . We call the quantity on the left-hand side of this inequality bidder ’s Bayesian pseudo-surplus. After taking expectations and summing over all bidders, as usual, we find that expected revenue is upper-bounded by expected bidder Bayesian pseudo-surplus:

| (14) |

Remark 4.4.

Bayesian pseudo-surplus is at least as great as robust pseudo-surplus:

The following example, which builds on Example 4.1, shows that the pseudo-surplus bounds (Equations (13) and (14)) are tight, meaning revenue can equal pseudo-surplus in both the robust and Bayesian problem settings.

Example 4.5.

We continue using the framework of Example 4.1.

In the robust problem, revenue equals pseudo-surplus:

Similarly, in the Bayesian problem, revenue equals pseudo-surplus:

∎

In Example 4.1, revenue in the Bayesian problem exceeds revenue in the robust problem. But in Example 4.5, revenue equals pseudo-surplus in both the robust and Bayesian problems. Therefore, Bayesian pseudo-surplus exceeds robust pseudo-surplus. In other words, while pseudo-surplus in a Bayesian problem is always at least that of pseudo-surplus in the corresponding robust problem (potentially greater objective function; weaker constraints), Bayesian pseudo-surplus can strictly exceed robust pseudo-surplus.

In summary, both revenue and pseudo-surplus in the Bayesian and the corresponding robust problems are not generally equal in the convex perceived payment setting as they are in the linear perceived payment setting. (In the linear perceived payment setting, because of linearity, there is no distinction between Bayesian and robust surplus; there is only surplus.) Consequently, we are unable to proceed as Myerson did, and solve for an optimal auction in the robust problem formulation as a means of finding an optimal auction in the corresponding Bayesian setting. Instead, we are forced to address these two problems separately.

5 Robust Revenue Maximization

The first problem we tackle is robust revenue maximization (RRM). Recall the power of Myerson’s payment characterization (Theorem 3.1): the problem of optimal auction design can be reduced to the problem of finding an optimal feasible allocation, where feasible here means only ex-post feasible; then if the resulting allocation is monotonic, IC and IR can be had for free, by assigning the appropriate payments, thereby resulting in an optimal auction. This is precisely the approach we take here.

We have already established an upper bound on revenue (namely, pseudo-surplus). The present exercise will lead us to an algorithm for finding an ex-post feasible allocation that optimizes that upper bound, which, when saddled with Myerson payment rule, yields a heuristic procedure that approximates RRM from above. Likewise, this exercise will also lead us to a heuristic lower bound, along with an analogous algorithm for computing an ex-post feasible allocation that optimizes that heuristic lower bound, which, along with Myerson payment rule, yields a heuristic procedure that approximates RRM from below.

In Appendix B, we also derive an alternative, as-of-yet non-operational, (tight) upper bound on expected revenue.

5.1 Pseudo-Surplus Maximization

Although Myerson ultimately applied his payment formula to compute payments in a revenue-maximizing auction, his formula applies equally well to computing payments in a surplus-maximizing auction. While maximizing surplus is not the eventual goal of this work (recall our example in which the government wished to maximize power: i.e., revenue), we can nonetheless use Myerson’s approach to find a pseudo-surplus-maximizing auction in our setting, in a manner analogous to finding a surplus-maximizing auction in the usual quasi-linear setting with linear perceived payments.

Our present objective is surplus, in the usual quasi-linear setting. Observe the following:

| (15) |

This equality holds because is independent of any other . Consequently, surplus (the left-hand side) can be maximized by proceeding pointwise (the right-hand side), in which an optimal allocation is determined for each in turn.

Recall that Myerson reduced the problem of optimal auction design to the problem of finding an optimal ex-post feasible allocation (assuming monotonicity). It is straightforward to enforce ex-post feasibility and simultaneously maximize the objective function pointwise: given , simply allocate to , breaking ties randomly. (Pseudocode for this pointwise approach is presented in Algorithm 1.444In the case of an indivisible good, this pseudocode can be interpreted as defining a randomized mechanism that allocates uniformly at random to exactly one of the highest bidders. In the case of an infinitely divisible good, fractionally, in proportion to the number of bidders tied for the highest bid. In the case of interest, namely a finitely divisible budget , any error in a discrete approximation as compared to the continuous (i.e., infinitely divisible) case, assuming discretization factor , is upper-bounded by .) Since the resulting allocation is monotone (higher values are allocated more), it can be plugged in to Myerson’s payment rule to arrive at an IC, IR, ex-post feasible surplus-maximizing auction (see Algorithm 2). Doing so yields Vickrey’s famous second-price auction [11].

Like surplus, pseudo-surplus can be maximized pointwise, because once again

| (16) |

Given , the function is non-decreasing and concave. Consequently, we can find an ex-post feasible allocation that maximizes by invoking the equi-marginal principle [5], which states that it is optimal (up to discretization error) to allocate greedily until supply is exhausted. That is, assuming , we calculate

and then allocate to , breaking ties randomly. Since the resulting allocation rule is monotone—higher values are more likely to be allocated—it can be plugged into Myerson’s payment rule (as we have extended it to the convex perceived payment setting) to obtain an optimal IC, IR, and ex-post feasible pseudo-surplus-maximizing auction. This heuristic procedure—1. greedily solve for an allocation rule that optimizes pseudo-surplus (an upper bound), and 2. support that allocation rule with Myerson’s payment rule—approximates RRM from above.

Generalizing slightly, Algorithm 3 solves (up to some set discretization factor , and for ) the following mathematical program, which we call Program , for “concave”: given a vector of constants and ,

| (17) | |||||

| subject to | (18) | ||||

| (19) | |||||

Using Algorithm 3, Algorithm 4 produces a pseudo-surplus maximizing IC, IR, XP auction.

Example 5.1.

Suppose there are bidders, with , for all bidders . When bidder utilities are quasi-linear, surplus maximization prescribes that we assign to a bidder whose type is maximal, and to all other bidders . By Myerson’s payment rule (Equation (8) with ), this allocation rule yields payments and for . Therefore, surplus and revenue are both , making surplus a tight upper bound on revenue.

When perceived payments are convex with , an integral allocation may not be optimal. Pseudo-surplus and revenue are both maximized when for all bidders , and by Myerson’s payment rule (Equation (10)), all bidders pay . Pseudo-surplus and revenue are both , so analogous to the quasi-linear case, pseudo-surplus is a tight upper bound on revenue in our convex perceived payment setting.

Interestingly, in this example, bidder surplus, is not an upper bound on revenue, because . Thus, unlike in the usual setting with linear perceived payments, where bidder surplus upper bounds revenue, revenue in the convex perceived payment setting can actually exceed bidder surplus. ∎

Algorithm 3 applies the equi-marginal principle specifically to the sum of square root functions, subject to ex-post feasibility. But this algorithm works equally well when applied to the sum of any concave functions. In fact, when the concave functions are differentiable, as in Equations (17), (18), and (19), this program can be solved in closed form (see Section 7.2). But Algorithm 3 remains applicable and Algorithm 4 finds a pseudo-surplus maximizing IC, IR, XP auction, even in cases where the concave functions are not differentiable.

The two subroutines presented above—pointwise maximization and the equi-marginal principle—are both used in the next section when we revisit Myerson’s virtual values.

5.2 Myerson’s Virtual Values

In his seminal work on optimal auction design, Myerson proved that expected revenue can be expressed as something he called expected virtual surplus, which he defined in terms of virtual values. Myerson used this theorem to reduce the problem of finding an optimal robust auction to pointwise optimization in virtual value space. In this section, we restate Myerson’s theorem and algorithm for discrete, rather than continuous, types. In the next section, we go on to use virtual values to heuristically lower bound revenue when perceived payments are convex, and utilities hence concave.

Following Section 3, we assume bidder ’s type space is , of cardinality , where for , and we let . We also assume the probability of type is given by cumulative distribution function and corresponding probability mass function .

Using this notation, here is the definition of virtual values for discrete distributions:

| (20) |

We abbreviate the virtual value by . We also use the shorthand , when for some .

Using the discrete version of Myerson’s payment formula (Theorem 3.1), and following a similar analysis to that of Myerson [8], we arrive at the following theorem.

Theorem 5.2.

By Theorem 5.2, when perceived payments are linear (i.e., ), each bidder’s expected (actual) payment is equal to his expected virtual surplus. Furthermore, total expected revenue is equal to total expected virtual surplus:

| (22) |

Mimicking Equations (15) and (16), virtual surplus (the right-hand side of Equation (22)) can be maximized in the same pointwise fashion as surplus and pseudo-surplus:

| (23) |

Furthermore, by Equation (22), maximizing virtual surplus also maximizes revenue. So, in fact, Myerson’s virtual value theorem (Theorem 5.2) gives rise to a pointwise method (Algorithm 5) for finding a revenue-maximizing ex-post feasible allocation rule: for each , simply allocate to one of the bidders with the highest virtual value.

The next question, then, is: is this allocation rule monotone? If so, we can apply Myerson’s payment formula to arrive at a mechanism that is also IC and IR. But there is nothing that guarantees that the resulting allocation rule is monotone; the rule depends on virtual values, while monotonicity is a constraint on values. So, we need one further assumption on the bidders’ type distributions to ensure monotonicity of virtual values in values: i.e., for all bidders , whenever . This assumption is called regularity. Assuming regularity, pointwise optimization of virtual surplus yields a monotonic allocation rule, and Algorithm 5 yields a solution to RRM in the linear perceived payment case.

Remark 5.3.

The auction that falls out of Algorithm 5 can be interpreted as one with per-bidder reserve prices. Restricting the search to positive virtual values (Algorithm 1, Line 5) ensures that the winning bidder’s bid exceeds not only the second-highest bid, but in addition the smallest value for which his inverse virtual value function is zero. Plugging the resulting allocation into Myerson’s payment formula then dictates that the winning bidder pay the maximum of the second-highest bid and the inverse of his virtual value function at zero,555When the inverse is not a singleton, he pays the minimum value in this set. the latter of which functions as his reserve price.

5.3 Heuristic Lower Bound

In the more general case of convex perceived payments, expected revenue does not equal expected virtual surplus. Nonetheless, for , we can derive bounds on expected revenue in terms of expected virtual surplus. One operational upper bound is pseudo-surplus; we present a second, non-operational upper bound expressed in terms of virtual surplus in Appendix B. Here, we present a heuristic lower bound, also in terms of virtual surplus, which lends itself to a heuristic procedure that approximates RRM.

Theorem 5.4.

If bidders’ utilities take the form of Equation (1) and is quadratic (i.e., ), then expected payments can be lower-bounded as follows:

| (24) |

Proof.

First, observe the following:

| (25) | ||||

| (26) | ||||

| (27) |

Example 5.5.

Although Theorem 5.4 is actually a claim about expectations, let us make the stronger assumption that for all and ,

| (35) |

equivalently, . Now, letting , it also holds that ; equivalently, . Summing over all bidders and then taking expectations yields:

| (36) |

which gives us a new heuristic objective of maximizing the right-hand side of Equation (36). As usual, we optimize this expression in a pointwise fashion subject to ex-post feasibility.

Given , the function is non-decreasing and concave. Consequently, we can find an ex-post feasible allocation that maximizes by invoking the equi-marginal principle [5]. That is, we calculate

and then allocate to . Assuming regularity, the resulting allocation rule is monotone (higher values are allocated more), so it can be plugged into Myerson’s payment rule (as we have extended it to the convex perceived payment setting) to obtain an optimal IC, IR, and ex-post feasible revenue-maximizing auction. This heuristic procedure—1. greedily solve for an allocation rule that optimizes the heuristic lower bound, and 2. support that allocation rule with Myerson’s payment rule—approximates RRM from below. (See Algorithm 6.)

Example 5.6 (Reserve bids).

Suppose the bidders have values drawn from a uniform distribution, where , and , for each bidder and . In an optimal auction, values that have negative corresponding virtual values are rejected. Since , the minimum for which is . So, given , the allocation variable can only be positive if .

If we insist upon an integral allocation rule (as in the case of an indivisible good, for example), so that exactly one bidder is allocated with , must bid at least , in which case pays . When is even, , so . Assuming linear perceived payments, so that , it follows that ; assuming convex perceived payments, so that , it follows that .

When we allow for a fractional allocation rule, must again bid at least to be allocated. If, for example, , then . When is even, , so . Assuming linear perceived payments, so that , it follows that ; assuming convex perceived payments, so that , it follows that .

N.B. In this example, if, when allowing for a fractional (or randomized) allocation rule, two bidders are both allocated , they both pay , and total revenue () exceeds total revenue in the case of an integral allocation rule only (). ∎

6 Bayesian Revenue Maximization

We now turn our attention to the problem of Bayesian revenue maximization in our convex perceived payment setting. With a bit more effort, we are again able to apply Myerson’s payment rule, but unlike in the robust case, the logic employed here is not merely a straightforward generalization or application of Myerson’s original reasoning. Specifically, we produce a smaller mathematical program than the default revenue-maximizing one: whereas the default program has exponentially-many payment variables, ours has only polynomially-many; but it still has exponentially-many allocation variables and ex-post feasibility constraints.

Our strategy is as follows: First we show that in our search for an optimal Bayesian auction, it suffices to restrict our attention to auctions in which each bidder’s payment is a (deterministic) function of his type alone, irrespective of other bidders’ types. Second, since by design this interim payment function is such that , by Corollary 3.3, is given by Equation (11).

Consider a (possibly randomized) auction, Auction , where denotes bidder ’s payment in auction . (Here, is the outcome of some randomization device.) We define another (deterministic) auction, Auction , with payment rule for some function that depends only on . More specifically,

| (37) |

Lemma 6.1.

An arbitrary allocation , together with the corresponding payment rule or , satisfies BIC, BIR, and ex-post feasibility for Auction if and only if it satisfies BIC, BIR, and ex-post feasibility for Auction .

Proof.

An arbitrary allocation satisfies ex-post feasibility for Auction if and only if satisfies ex-post feasibility for , as these set of constraints are identical in both auctions. The BIC and BIR constraints, however, can differ across the two auctions because payments can differ. Nonetheless, we now proceed to show that an arbitrary allocation satisfies BIC and BIR for Auction if and only if it satisfies these properties for Auction .

Since

| (38) | ||||

| (39) | ||||

| (40) | ||||

| (41) |

it follows that

| (42) | ||||

| (43) | ||||

| (44) | ||||

| (45) | ||||

| (46) |

Therefore, for all bidders and values ,

| (47) |

and

| (48) |

In other words, (and the corresponding payment rule ) is BIC and BIR for Auction if and only if it is BIC and BIR for Auction . ∎

Lemma 6.2.

The total expected revenue of Auction is at least that of Auction .

Proof.

Let denote the expected revenue of Auction , and let denote the expected revenue of Auction . By Jensen’s inequality, since the square root is a concave function,

| (49) | ||||

| (50) | ||||

| (51) |

it follows that

| (52) | ||||

| (53) | ||||

| (54) | ||||

| (55) | ||||

| (56) |

In other words, the expected revenue of Auction is at least that of Auction . ∎

These two lemmas establish that in our search for an optimal auction, it suffices to restrict our attention to auctions like Auction in which each bidder’s payment is a (deterministic) function of his type alone. Furthermore, since , it follows by Corollary 3.3 that is given by Equation (11): i.e.,

| (57) |

These two lemmas together with this final observation establish the follow theorem:

Theorem 6.3.

Remark 6.4.

We close this section with a heuristic for approximating BRM. Analogous to Algorithm 6, which describes a method to approximate RRM from below, Algorithm 7 approximates BRM from below. The only difference between these two algorithms is that Algorithm 6 uses Equation (10) to determine payments, whereas this new heuristic uses Equation (11).

7 Closed-Form Solutions

Next we present closed-form solutions to three mathematical programs of interest. The first problem we study is the ex-ante relaxation of BRM, which requires only polynomially-many constraints. We present an intuitive, closed-form solution to a relaxation of this relaxation, which yields a closed-form upper bound on the ex-ante Bayesian problem.

This solution also upper bounds RRM. Nonetheless, we derive a tighter upper bound in closed form. Specifically, the second two programs we discuss in this section optimize the upper and heuristic lower bounds we derived for RRM, subject to the usual ex-post feasibility constraints. While both these programs can both be solved greedily (Algorithm 3), we derive closed-form solutions, assuming the payment function is differentiable.

In searching for a near-optimal auction, all three of these problems optimize allocation variables. Interestingly and intuitively, all our closed-form solutions allocate in proportion to value (or virtual value). Consequently, the resulting allocation rules are all monotone,666assuming regularity which means that they support Myerson payments, and yield approximately-optimal auctions.

7.1 A Relaxation of the Ex-Ante Relaxation of BRM

Recall Theorem 5.4: Expected payments, when bidders have quasi-linear utility functions as described by Equation (1) and , can be lower-bounded as follows:

| (59) |

Following similar logic, and taking expectations throughout, yields a similar lower bound:

| (60) |

Like Equation (59), Equation (60) is a claim about expectations. Still, let us make the stronger assumption that for all ,

| (61) |

equivalently, . Now, letting , it also holds that ; equivalently, . Taking expectations and then summing over all bidders yields:

| (62) |

which gives us a new heuristic objective of maximizing the right-hand side of Equation (62). Note that this new objective cannot be maximized in a pointwise fashion, because the various value vectors cannot be treated independently in an ex-ante problem. On the contrary, all the various allocations interact through the one ex-ante feasibility constraint.

Although we cannot maximize pointwise, we can still approximate a solution to the ex-ante relaxation by solving a mathematical program with this heuristic objective function and the relevant feasibility constraints. We go one step further and propose the following heuristic program as a means of approximating an optimal allocation:

| (63) | ||||

| subject to | (64) |

This heuristic program ensures only ex-ante feasibility, but drops the constraints that the interim allocation variables lie in the range (and indeed, they need not in the ensuing solution). Interestingly, we can solve this program in closed form.

Theorem 7.1.

The optimal solution to this heuristic program (call it Program ) is to allocate in proportion to virtual values:

| (65) |

Under the regularity assumption, this proportional allocation is monotone, so can be supported by Bayesian (i.e., BIC and BIR) payments.

Proof.

Let , and rewrite Program as follows:

| (66) | |||||

| subject to | (67) | ||||

| (68) | |||||

Call this new program Program .

Now consider the Lagrangian of Program , dropping the positivity constraints as they are redundant:

| (69) |

By the Karush-Kuhn-Tucker conditions, the partial derivative of the Lagrangian with respect to each must equal :

| (70) |

In other words, .

At any optimal solution, Constraint (67) will be tight, since otherwise we could increase the objective value by increasing some for which by an infinitesimal amount. So:

| (71) |

Replacing with in Equation (71) yields:

| (72) |

so that

| (73) |

Now substituting into Equation (70), we arrive at a closed-form solution to Program :

| (74) |

Equivalently, the optimal solution to Program takes the form:

| (75) |

Finally, observe that for all bidders ,

| (76) |

Therefore, the closed-form solution to Program takes the intuitive form:

| (77) |

∎

7.2 A Closed-form Upper and Heuristic Lower Bound on RRM

In this section, we present closed-form solutions to two mathematical programs that upper and (heuristically) lower bound RRM. In the first, the objective function is pseudo-surplus, an upper bound on revenue. The second uses as an objective function the heuristic lower bound we derived for RRM based on virtual values (Equation (36)). Solving these programs in closed form yields solutions that allocate in proportion to value. Such monotonic allocation rules can be supported via Myerson’s payment rule.

Theorem 7.2.

The optimal solution to Program is

| (78) |

where , whenever there exists at least one positive entry in .

Proof.

Bidders whose constants are negative are not allocated, and bidders whose constants are zero have no impact, so we restrict our attention to bidders with positive constants. That is, it suffices to allocate assuming we are given instead of .

The derivative of the contribution of bidder is

| (79) |

Equating derivatives for bidders and (as per the equi-marginal principle), we get

| (80) |

The common terms can be removed, and after raising the expressions to the power, we can simplify to

| (81) |

Therefore, bidder ’s allocation in terms of bidder is

| (82) |

Plugging this expression into the ex-post feasibility condition yields:

| (83) |

It is always optimal to allocate until when there is at least one bidder with a positive constant, so the ex-post feasibility constraint can be written as

| (84) |

Therefore, bidder is allocated as follows:

| (85) |

∎

The following corollary is immediate:

Corollary 7.3.

The optimal solution to Program when is

| (86) |

where , whenever there exists at least one positive entry in .

When the constants are values, the objective function in program is pseudo-surplus. When the constants are virtual values, the objective function in program is our heuristic lower bound. Consequently, Theorem 7.2 immediately gives rise to closed-form solutions to these two mathematical programs of interest.

Corollary 7.4.

The following allocation is optimal when and (i.e., when the objective function is pseudo-surplus):

| (87) |

where , when there exists at least one positive entry in .

Corollary 7.5.

The following allocation is optimal when and (i.e., when the objective function is our heuristic lower bound):

| (88) |

where , when there exists at least one positive entry in .

Corollaries 7.4 and 7.5 gives rise to respective variants of Algorithm 4, Algorithm 6, and Algorithm 7: in each algorithm, simply replace the call to the equi-marginal principle solver with the corresponding closed form. Like their counterparts, these heuristics, which employ closed-form solutions instead of greedy ones, and then plug the resulting allocation rules into Myerson’s payment formula, approximate optimal auctions.

Remark 7.6.

If values are continuous as in Myerson’s original paper, then Equation (8) is

| (89) |

which, letting , simplifies to

| (90) | ||||

| (91) | ||||

| (92) | ||||

| (93) | ||||

| (94) |

Since Equation (94) gives an upper bound that is proportional to the marginal gain in log-surplus, we expect that extracting more revenue from bidder will become more difficult as bidder ’s type increases. We see this explicitly when computing derivatives. Specifically, perceived payment changes by

| (95) |

while actual payment changes by

| (96) |

8 Experiments

We close this paper with some experimental results implemented in MATLAB demonstrating the performance of our methods in different settings. As a baseline, we used IBM’s ILOG CPLEX Optimization Studio to solve RRM and BRM optimally. In comparison, we used our heuristic procedures to generate heuristic lower bounds on total expected revenue, for auctions that satisfy all the relevant constraints. We also computed pseudo-surplus (ensuring ex-post feasibility only) to give upper bounds on total expected revenue; but we did not compute accompanying payments, so we did not ensure IC and IR or BIC and BIR. Finally, we also solved the ex-ante relaxation of BRM to obtain a nearly instantaneous upper bound on solutions to all our problems.

All programs were run on a system with an Intel Core i5 3.5 GHz processor and 8 GB of RAM. We compared total expected revenue and run time for different numbers of bidders. The number of bidders we used was limited by processing time and memory constraints.

In all simulations, bidders were symmetric, meaning for all bidders and . We studied three different bidder distributions: categorical, uniform, and binomial.

While most of our heuristics are powerful enough to apply to any convex function (not only ), our experiments are restricted to this case because, to our knowledge, CPLEX (for MATLAB) can only handle objective functions and constraints that are linear, quadratic, or integer.

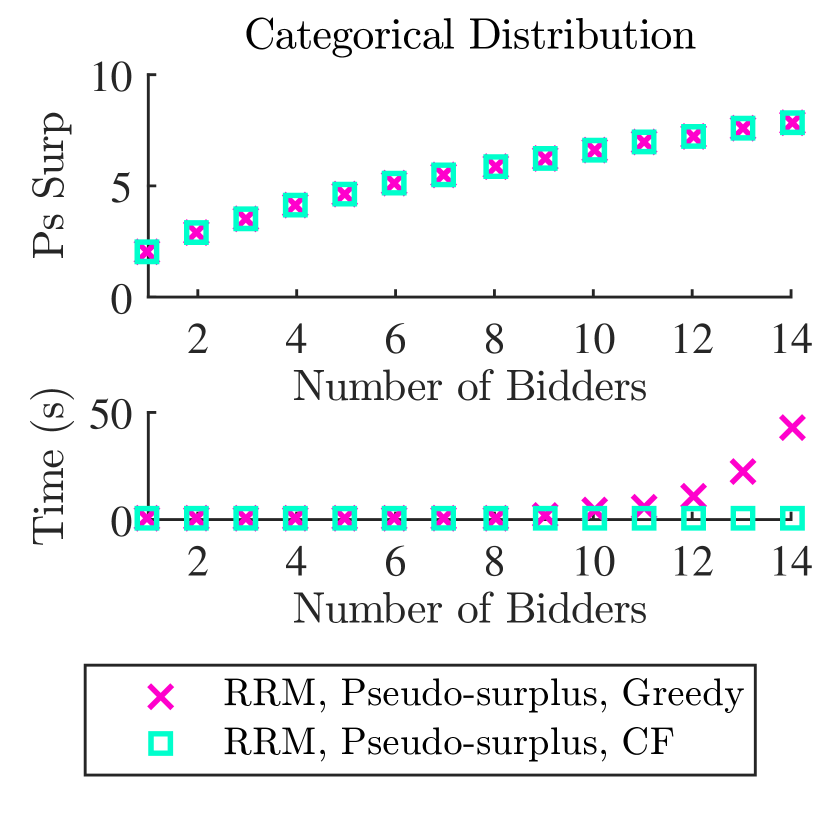

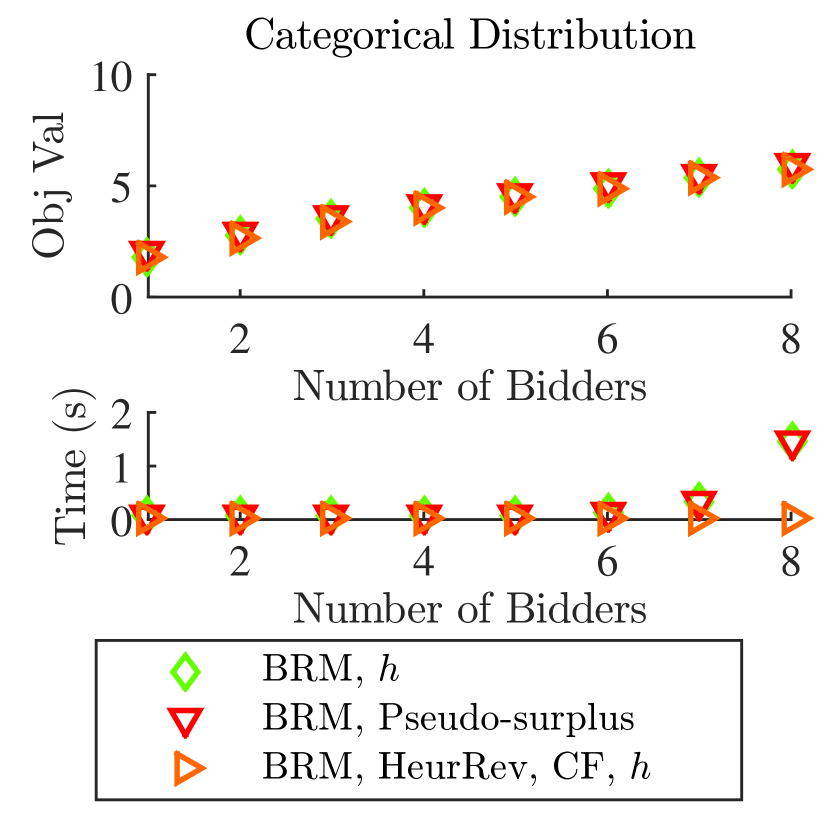

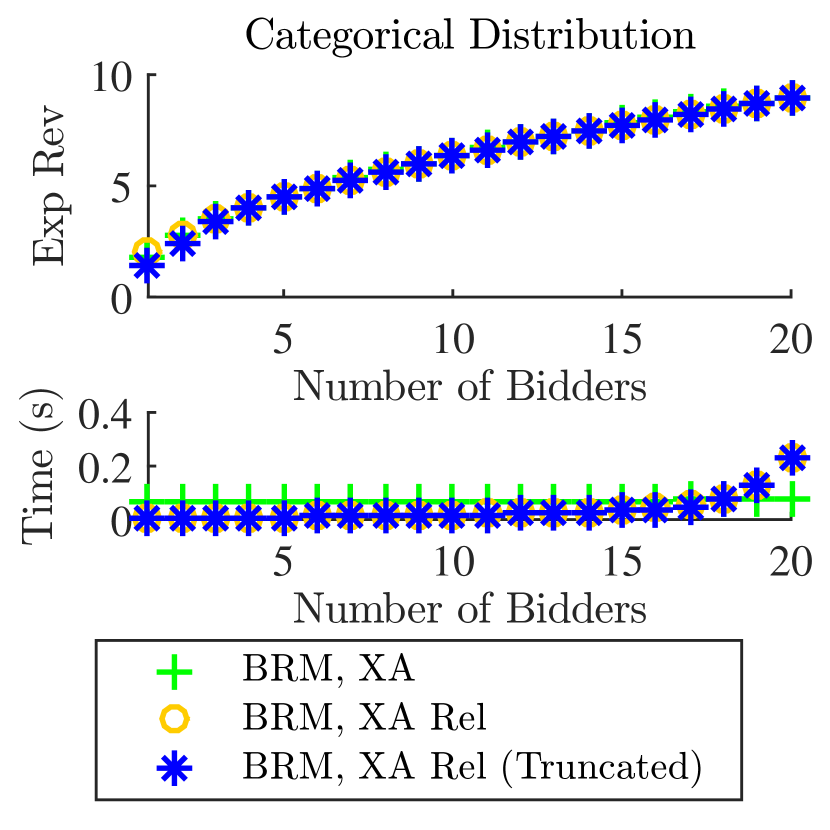

Categorical Distribution

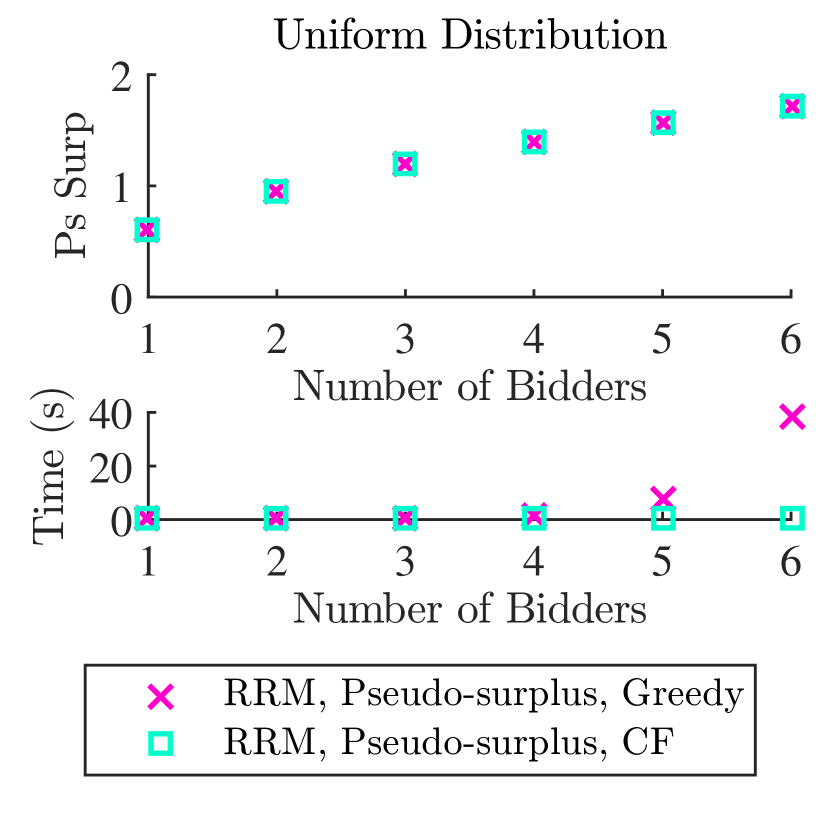

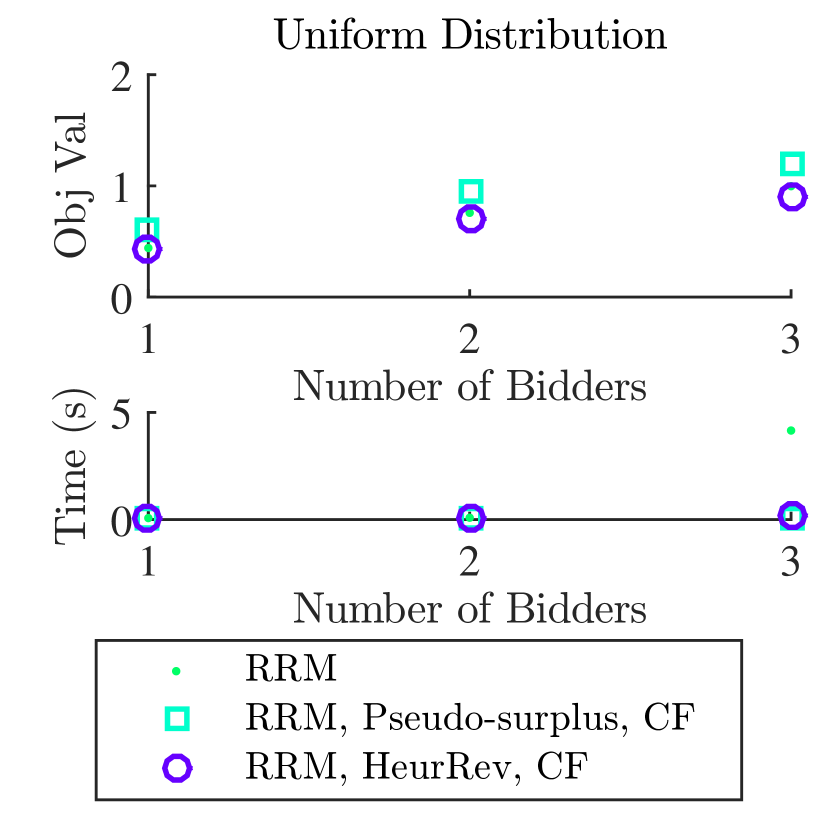

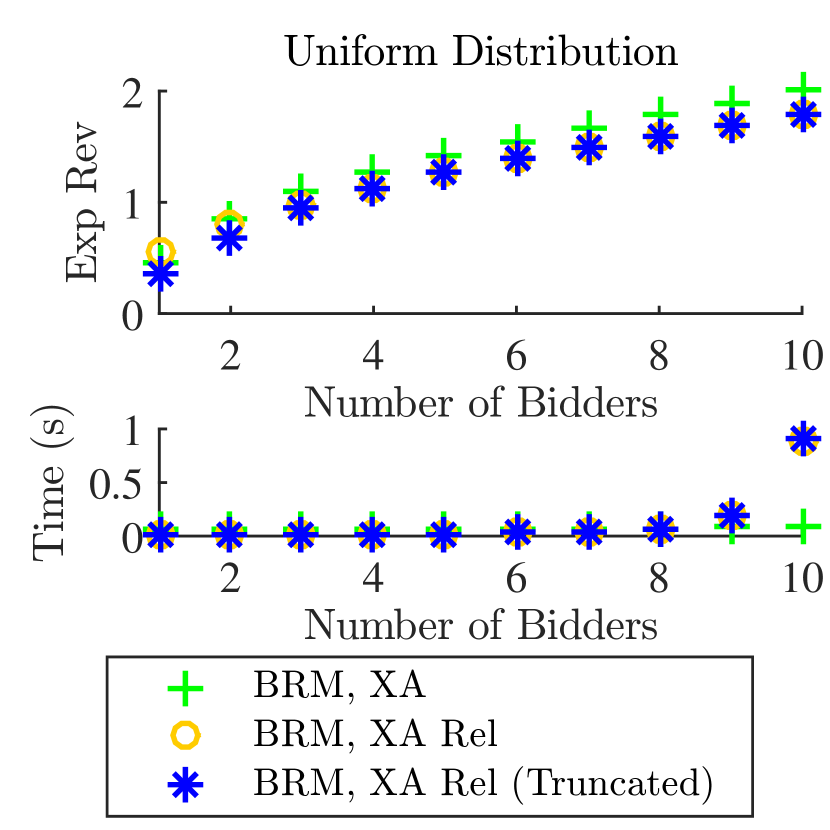

Uniform Distribution

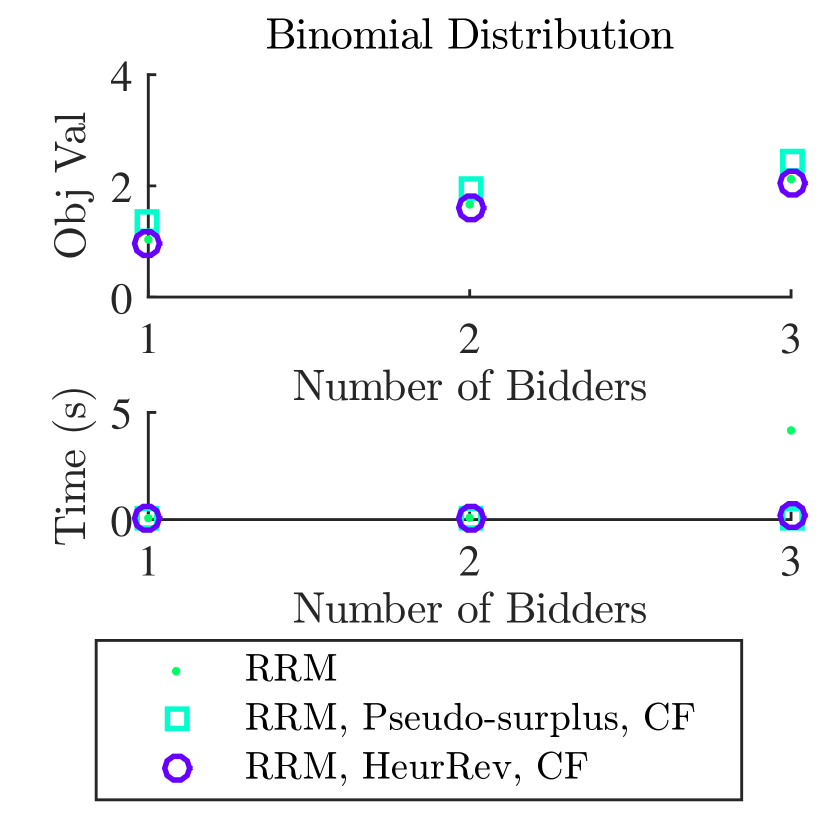

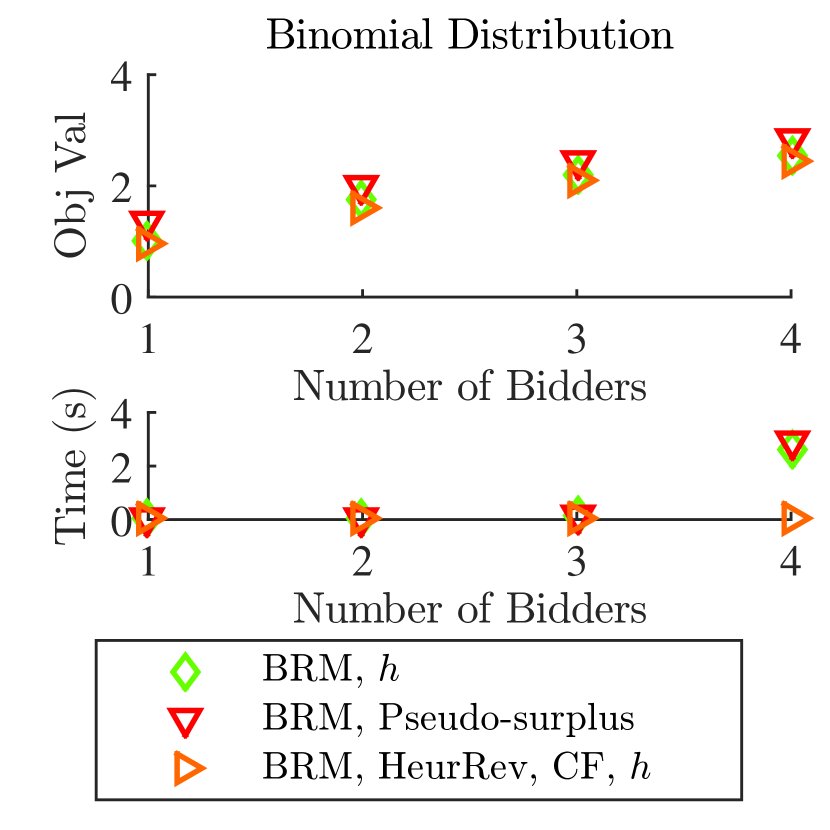

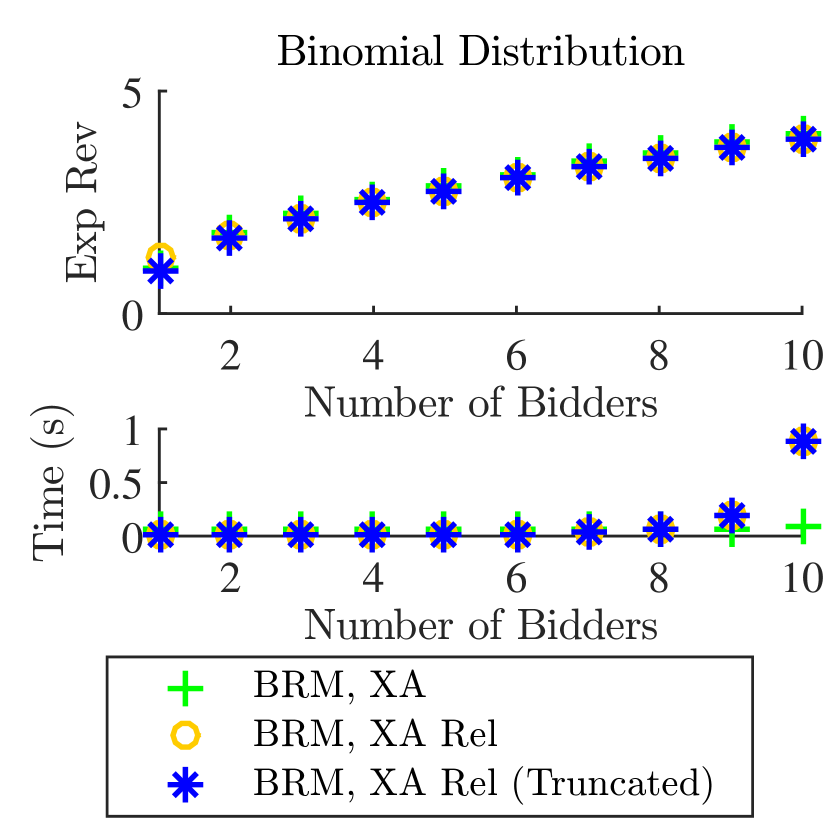

Binomial Distribution

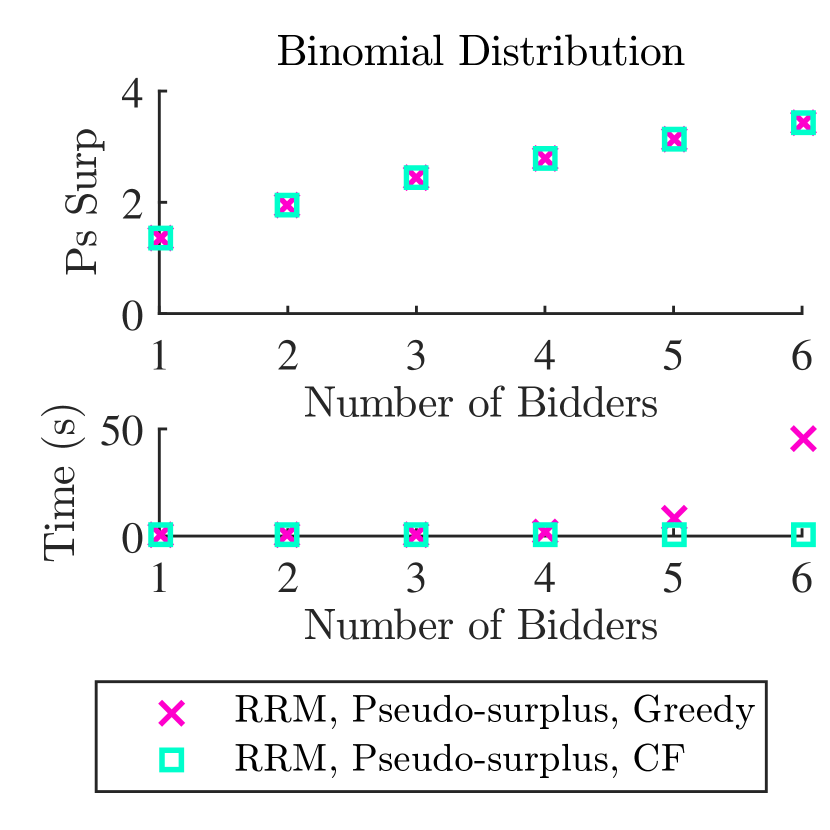

8.1 Pseudo-surplus in the Robust Problem

We optimize pseudo-surplus in the robust problem (see Section C.1.2). We report the results of the following two methods:

Both methods achieve the optimal pseudo-surplus, but using Algorithm 8 (the closed form), we achieve this value more quickly than when using Algorithm 4 (the greedy method).

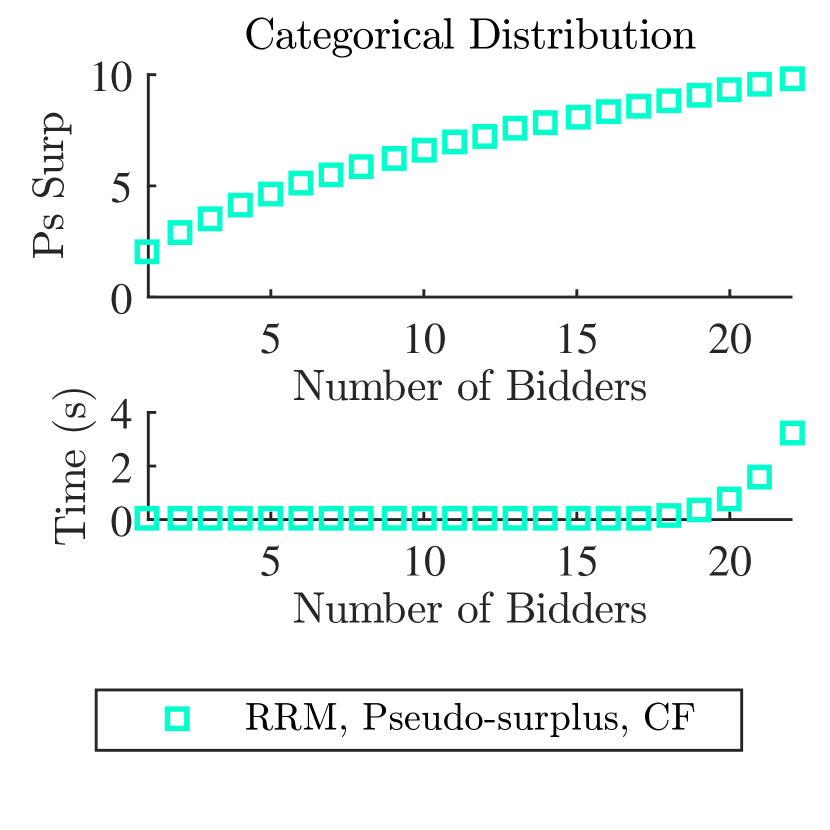

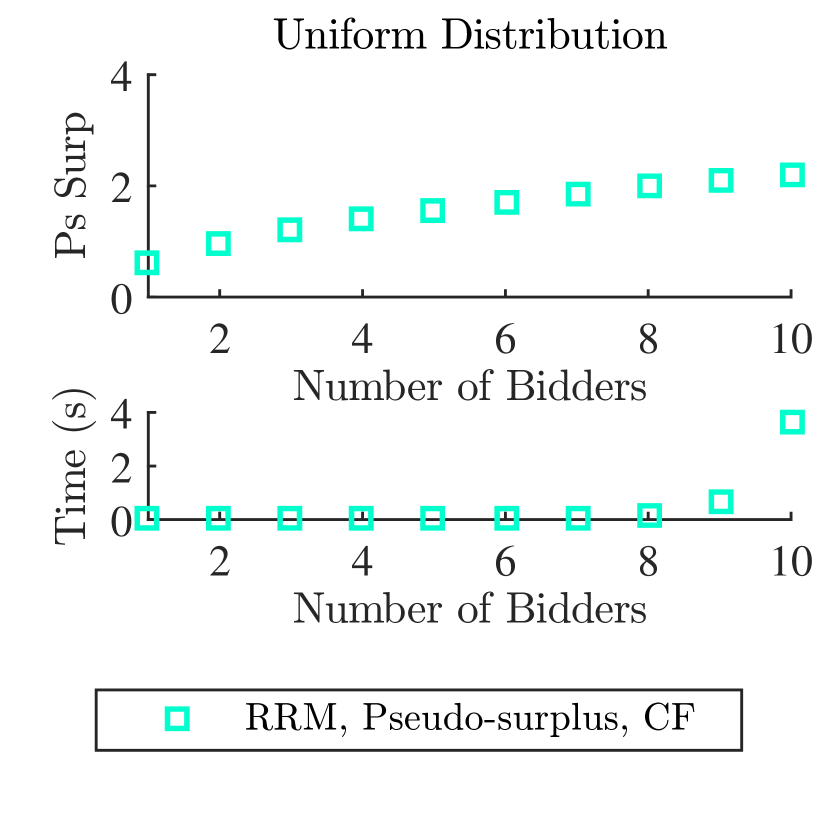

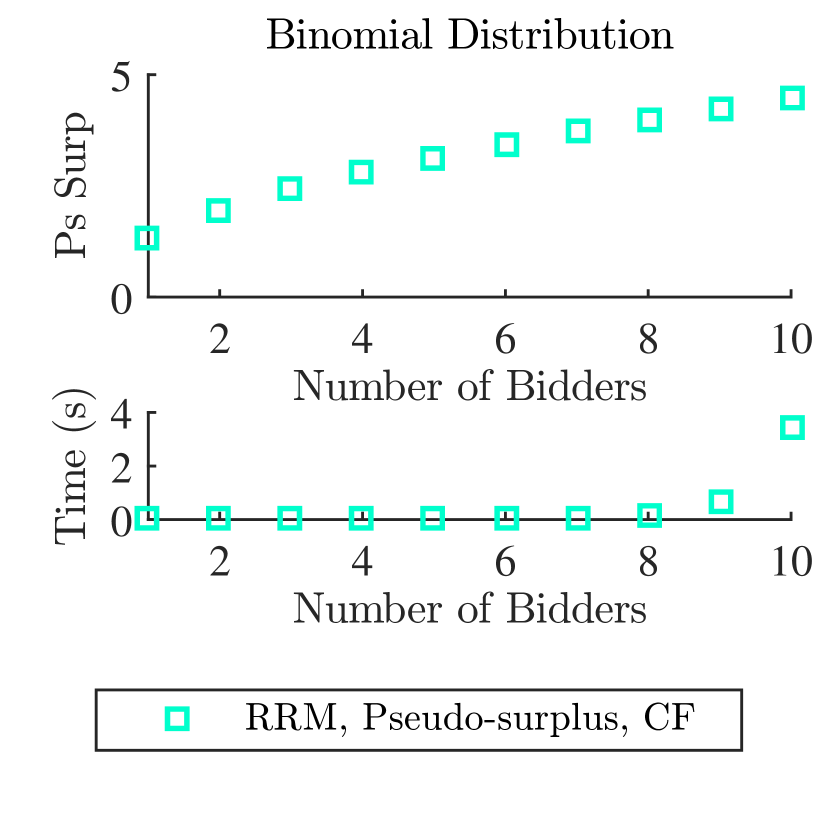

8.2 Pseudo-surplus Scaling in the Robust Problem

We optimize pseudo-surplus in the robust problem, ensuring ex-post feasibility (see Section C.1.2), to see how it scales with the number of bidders. We report the results of the following:

-

•

(MATLAB) Total expected pseudo-surplus using Algorithm 8 (the closed form), but without calculating payments.

While the closed-form method is nearly instantaneous when the number of bidders is small, it cannot escape the fact that there are exponentially-many allocation variables. (The behavior of the closed-form solution for the heuristic lower bound—see Section 8.3—is identical as we scale the number of bidders.)

8.3 Heuristic Lower Bound in the Robust Problem

We optimize the heuristic lower bound ensuring ex-post feasibility (see Section C.1.3). We report the results of the following two methods:

Both methods achieve the optimal objective value, but using Algorithm 9 (the closed form), we achieve this value more quickly than when using Algorithm 6 (the greedy method).

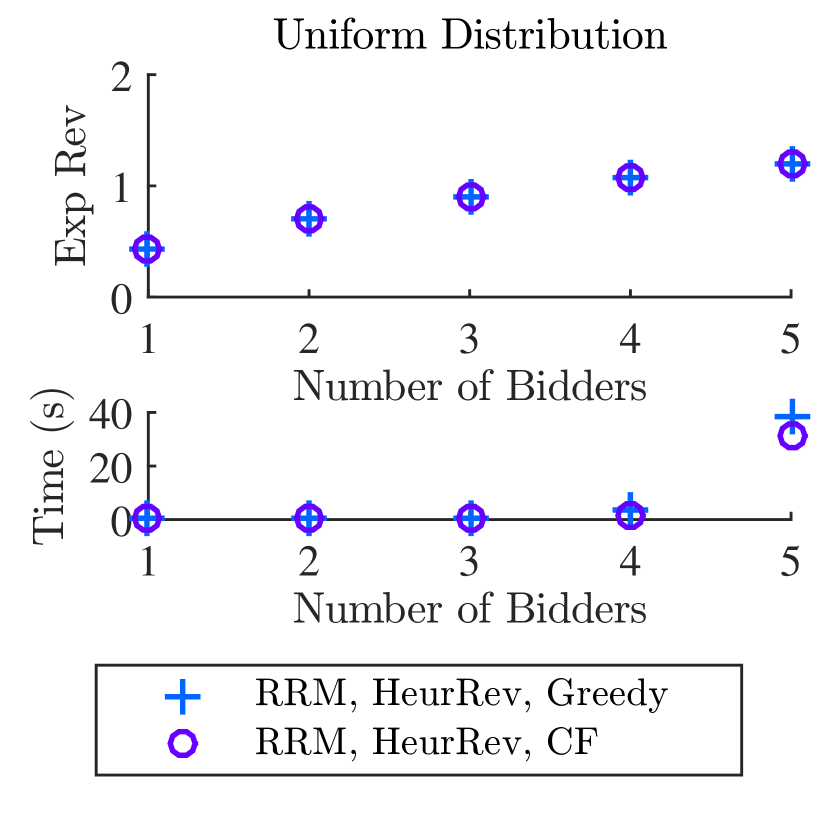

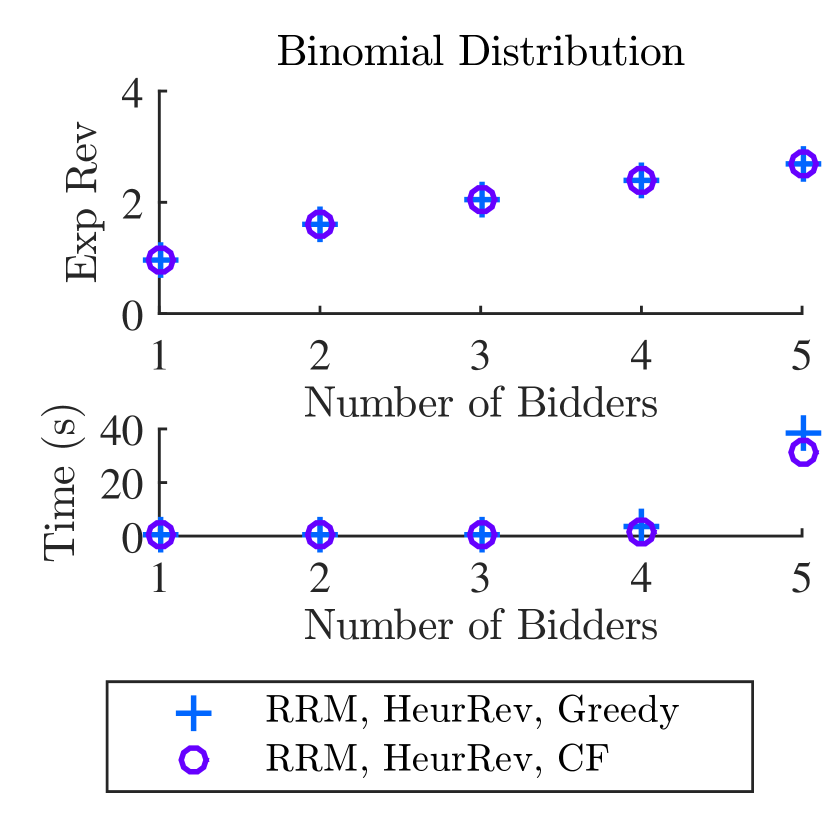

8.4 Heuristic Revenue in the Robust Problem

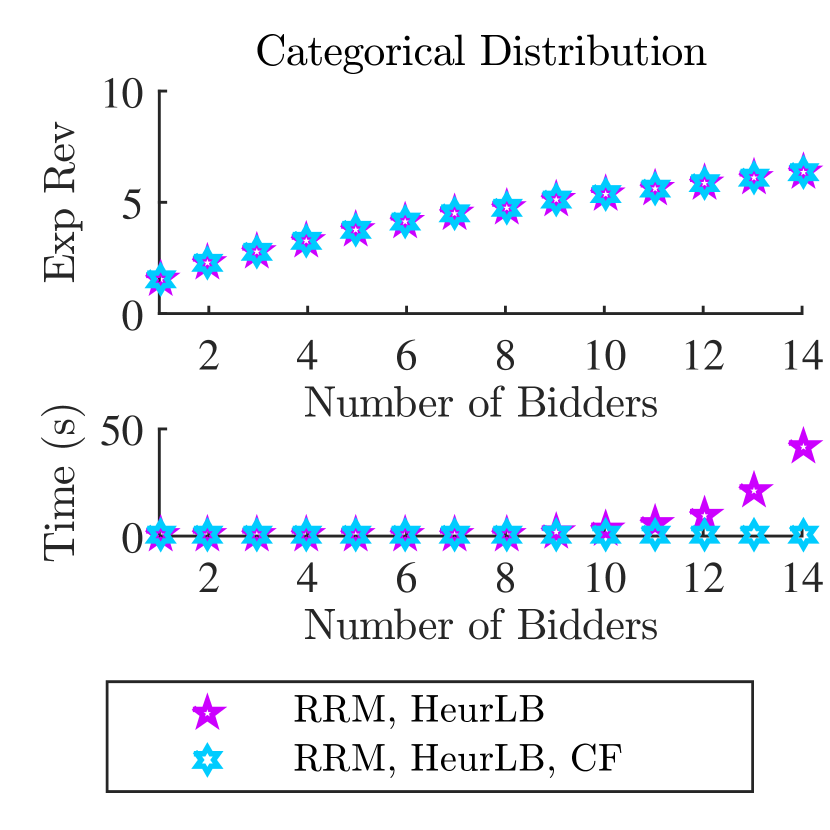

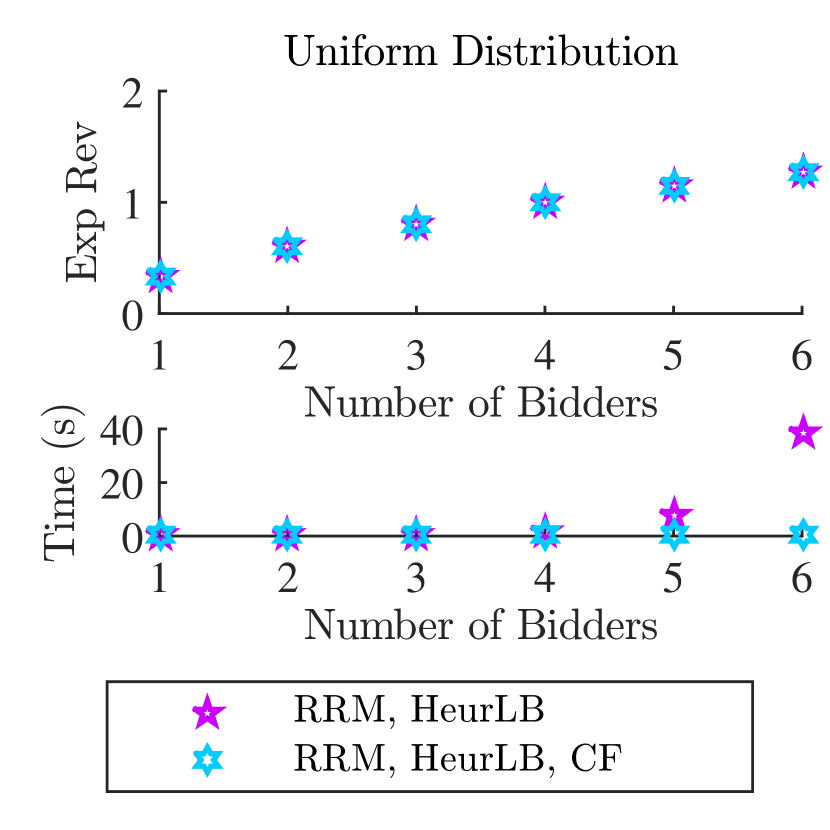

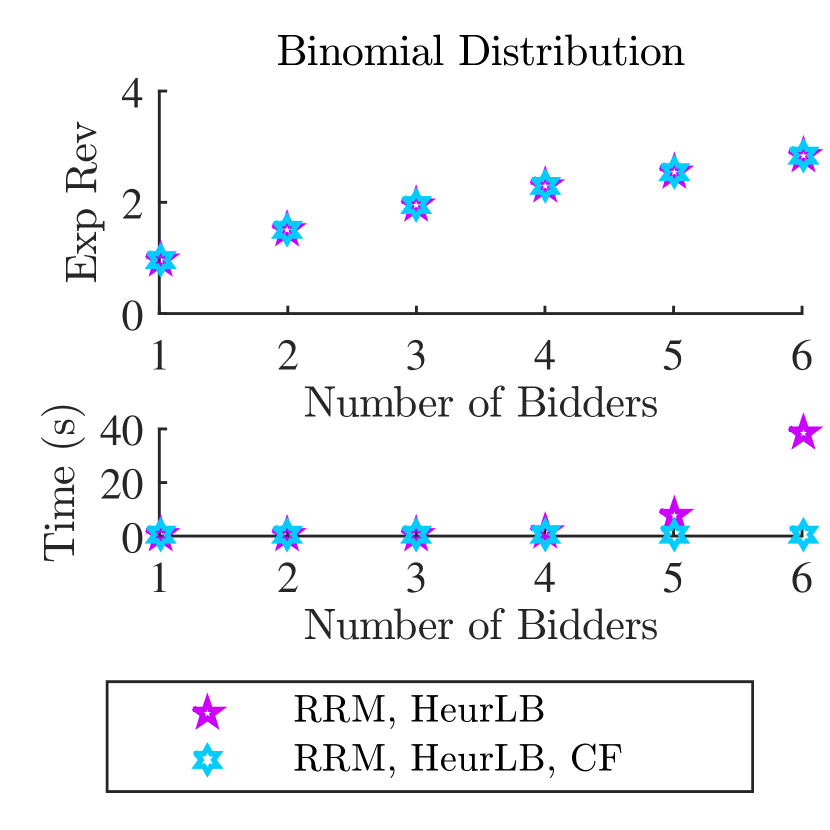

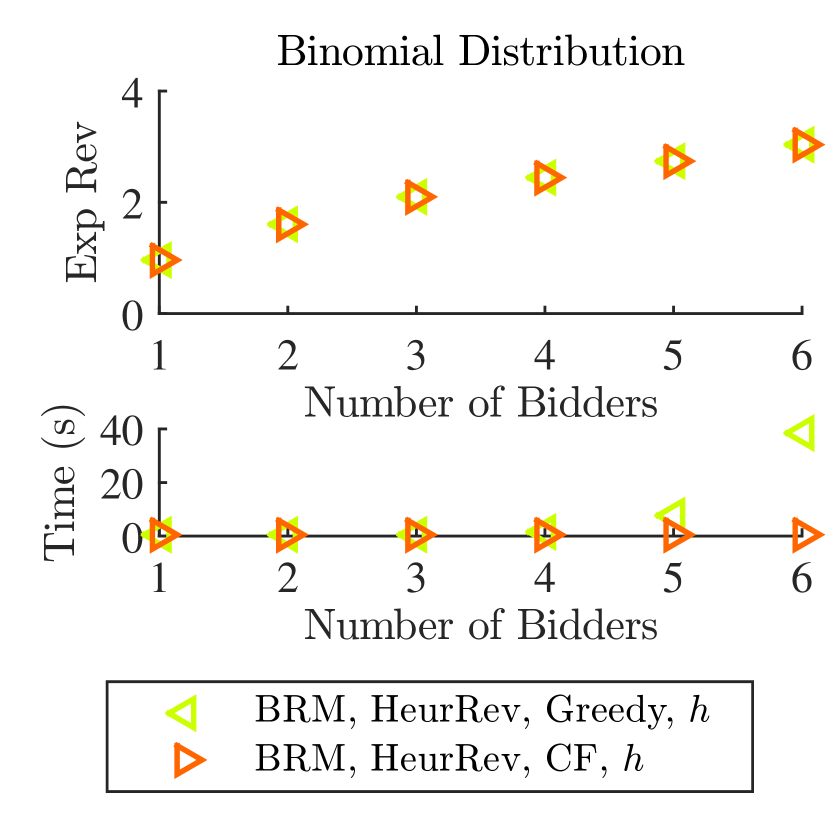

We first optimize our heuristic lower bound in the robust problem (see Section C.1.3). Next, we plug the resulting allocation rule into into Myerson’s formula to compute robust payment rule (Equation (10)), and then total expected heuristic revenue. Varying the optimization technique, we report the results of the following two methods:

- •

- •

Our choice of discretization factor in our greedy implementation is sufficiently fine that both methods achieve the same objective value. Moreover, the run times of the two methods are not noticeably different, because both are dominated by the exponential number of robust payment calculations. Both these runs are noticeably slower than the pseudo-surplus and heuristic lower bound runs, which perform no payment calculations at all.

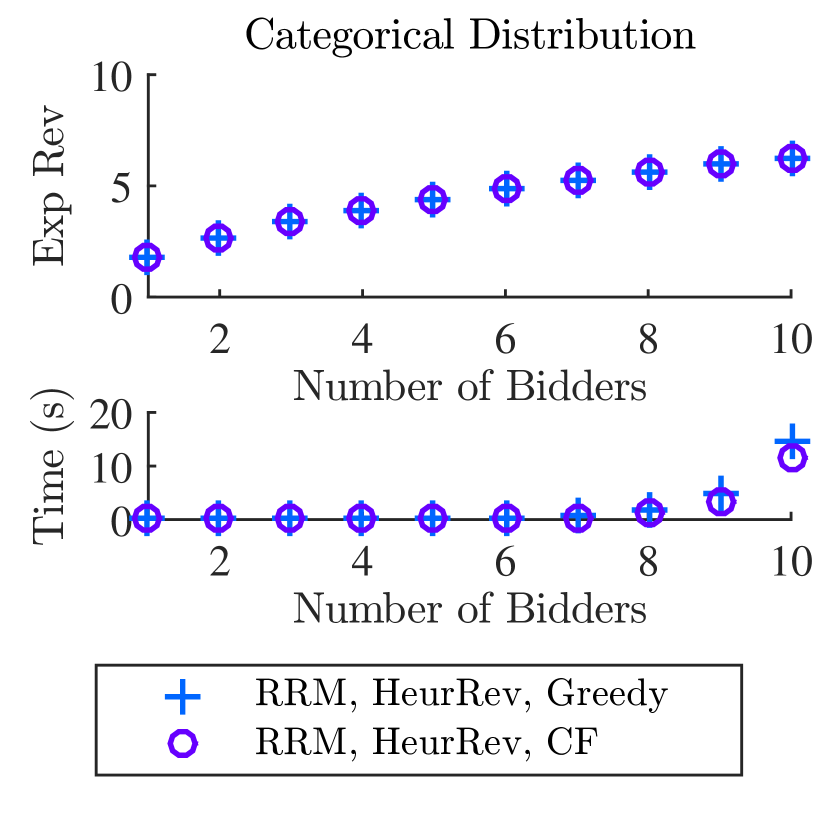

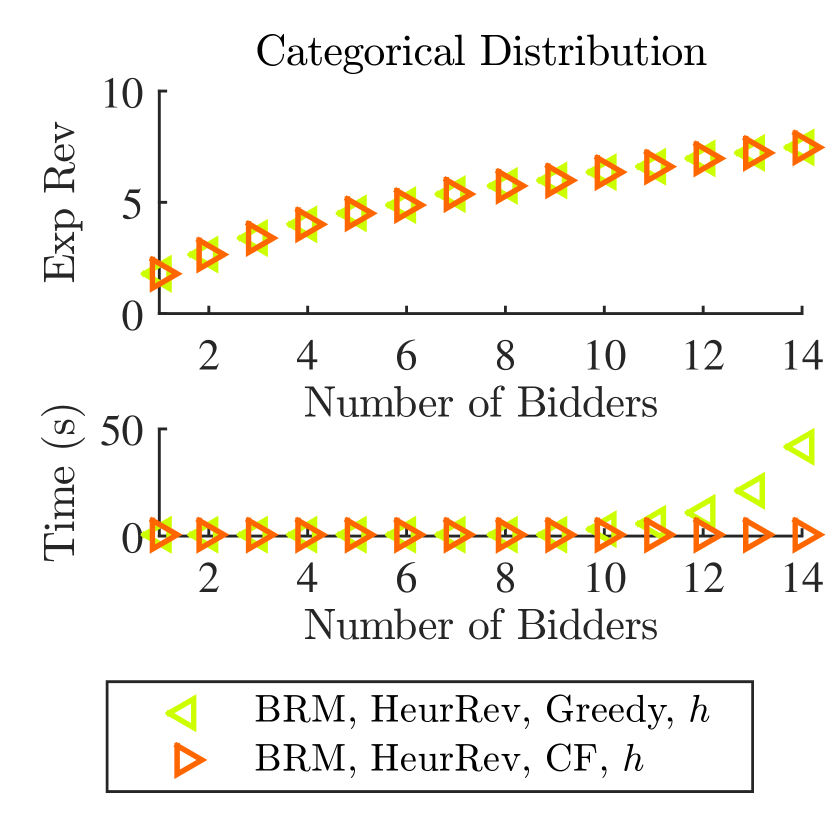

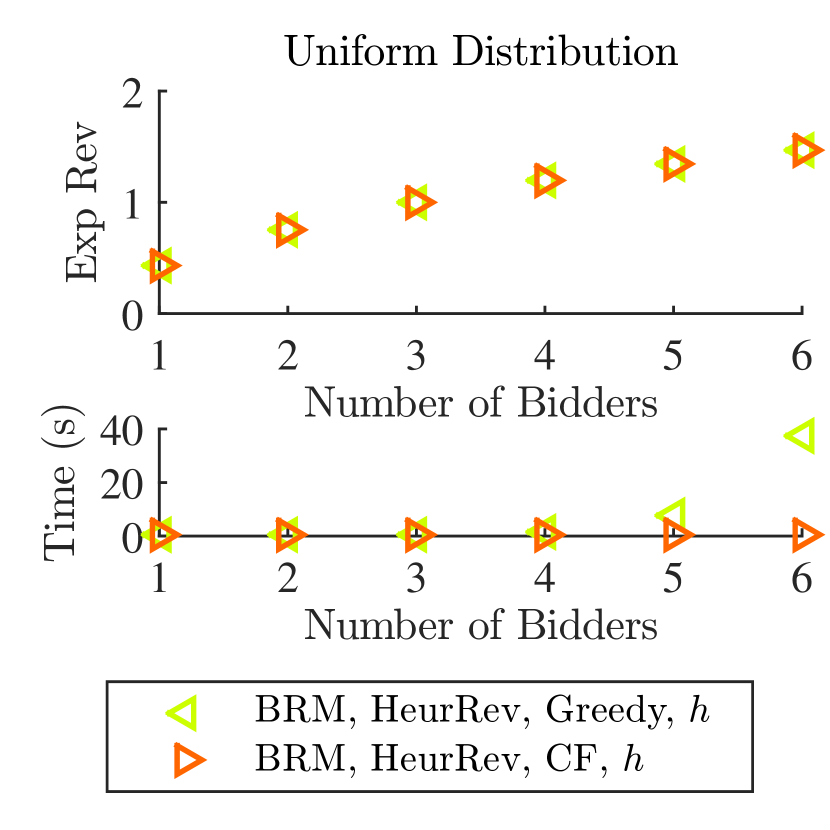

8.5 Heuristic Revenue in the Bayesian Problem

We first optimize our heuristic lower bound in the robust problem (see Section C.1.3). Next we collapse the resulting allocation rule into an interim allocation rule . Finally, we plug into Myerson’s formula to compute Bayesian payment rule (Equation (11)), and then total expected heuristic revenue. Varying the optimization technique, we report the results of the following two methods:

- •

- •

As above, our choice of discretization factor in our greedy implementation is sufficiently fine that both methods achieve the same objective value. But this time, using Algorithm 10 (the closed form), we achieve this value much more quickly. This is because there are only polynomially-many payment calculations in the Bayesian problem, so the speed up achieved by the closed-form method is not eviscerated by expensive payment calculations.

8.6 Heuristic Lower Bound and Heuristic Revenue: Robust vs. Bayesian

We compare the heuristic lower bound in the robust problem; total expected heuristic revenue in the robust problem; and total expected heuristic revenue in the Bayesian problem. We report the results of the following three methods:

- •

- •

- •

According to the theory developed in this paper, the heuristic lower bound in the robust problem should not exceed the heuristic revenue in the robust problem, which in turn should not exceed the heuristic revenue in the Bayesian problem. Our experiments are consistent with these claims, and further provide examples where the heuristic revenue in the robust problem strictly exceeds the heuristic lower bound, and where the heuristic revenue in the Bayesian problem strictly exceeds that of the robust problem.

Moreover, the Bayesian heuristic runs significantly faster than the robust heuristic; this difference can be attributed to the computation of polynomially- instead of exponentially-many payments. (The heuristic lower bound computes no payments at all.)

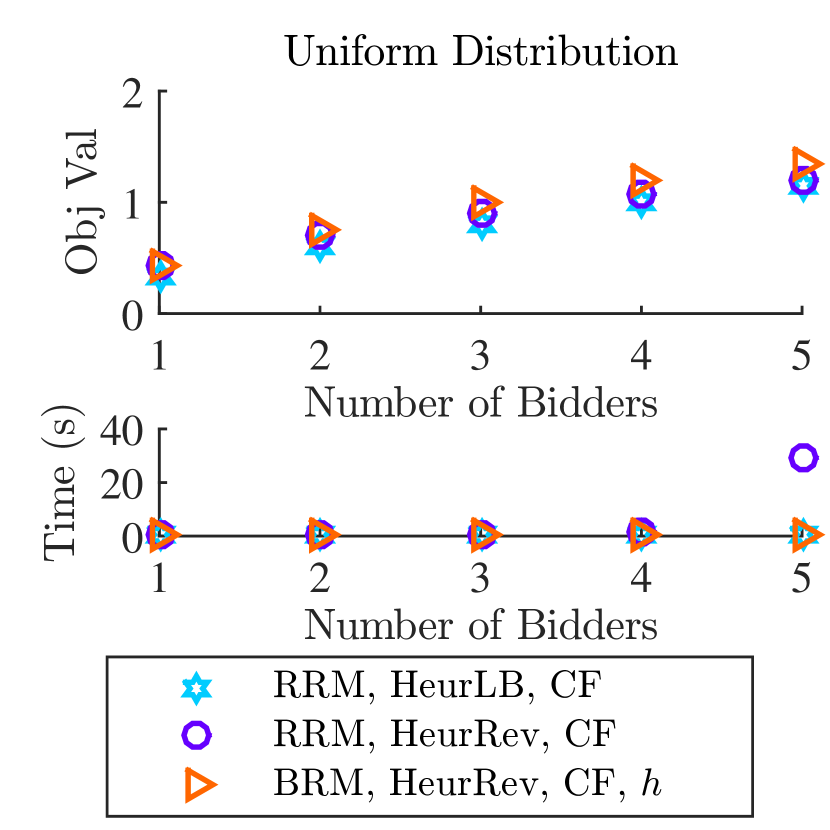

8.7 Revenue, Pseudo-Surplus, and Heuristic Revenue in the Robust Problem

We report the results of the following:

-

•

(CPLEX) Total expected revenue in the robust problem (see Section C.1.1).

- •

- •

CPLEX solves the robust problem optimally, while the other two programs do not. Furthermore, when there are very few bidders (e.g., 1 or 2), CPLEX solves RRM just as fast as MATLAB solves for pseudo-surplus or the heuristic revenue. But as the number of bidders grows, CPLEX does not scale. The heuristic revenue appears to approximate the value of RRM as determined by CPLEX quite well, and it scales better than CPLEX.

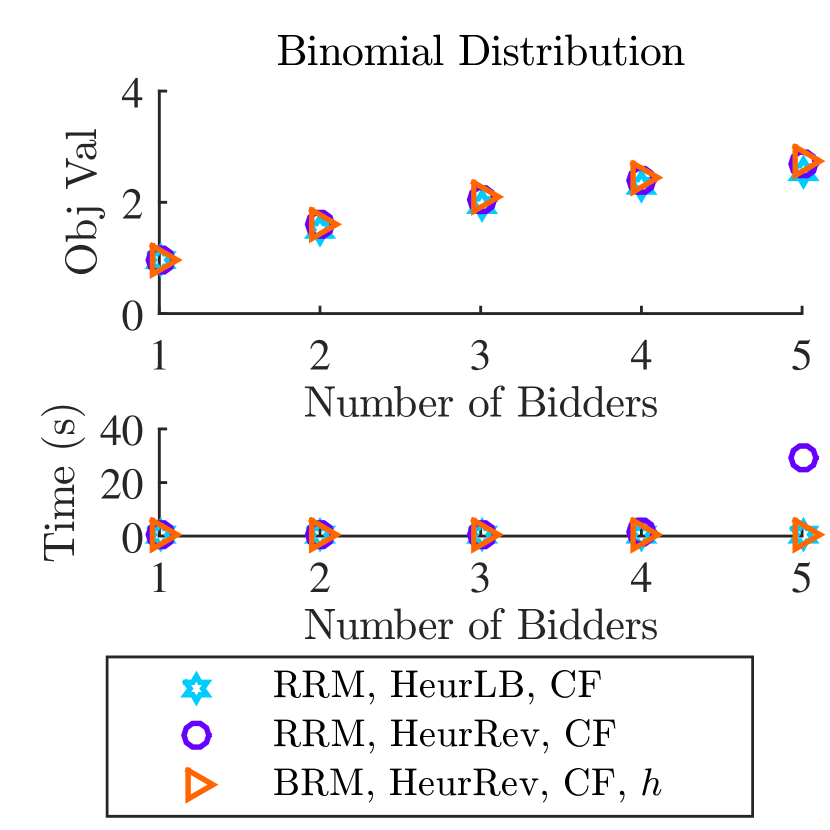

8.8 Revenue, Pseudo-Surplus, and Heuristic Revenue in the Bayesian problem

We report the results of the following:

- •

-

•

(CPLEX) Total expected pseudo-surplus in the Bayesian problem (see Section C.2.3).

- •

CPLEX solves the Bayesian problem optimally, while the other two programs do not. Furthermore, when there are very few bidders (e.g., 1, 2, or 3), CPLEX solves BRM just as fast as CPLEX solves for pseudo-surplus or MATLAB solves for the heuristic revenue. But as the number of bidders grows, CPLEX does not scale. The heuristic revenue appears to approximate the value of BRM as determined by CPLEX quite well, and it scales better than CPLEX.

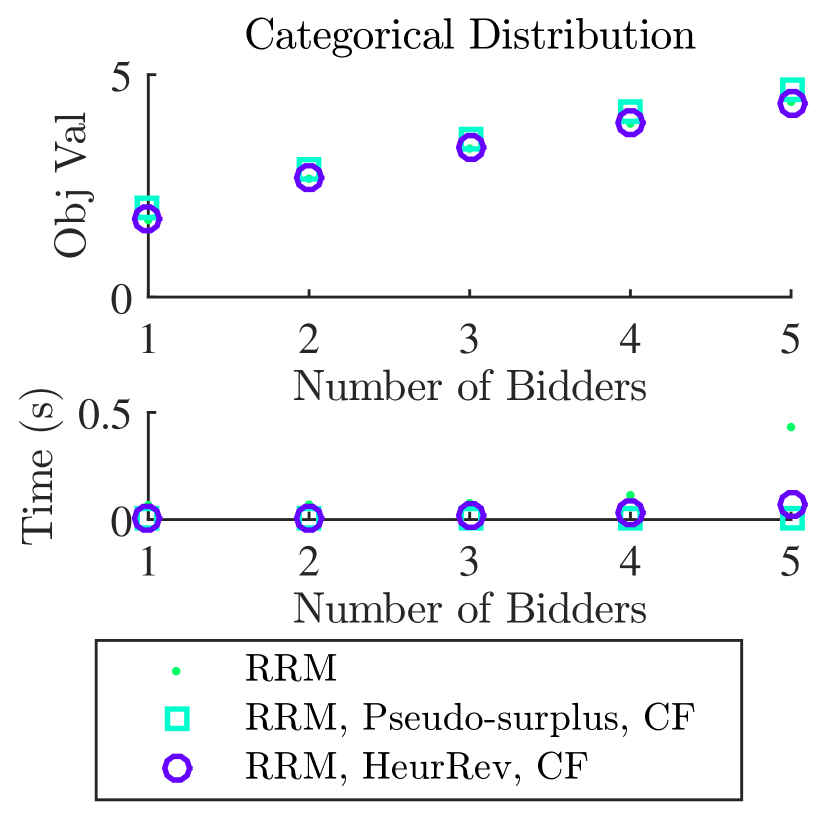

8.9 BRM Ex-Ante

We report the results of the following:

-

•

(CPLEX) Total expected revenue of the BRM ex-ante relaxation (see Section C.3.1).

- •

- •

For the BRM ex-ante relaxation, a problem with only polynomially-many variables and constraints, even CPLEX, which is optimal, appears to scale just fine with the number of bidders. Indeed, while the approximations are faster than CPLEX on small problems, their run time eventually grows, while CPLEX does not.

9 Conclusion and Future Work

We analyzed optimal auctions where bidder utilities are quasi-linear, but defined in terms of convex, instead of the usual linear, payments. We adapted Myerson’s analysis to this setting when it is required that constraints always hold (i.e., the robust problem) and when it is required only that they hold in expectation (i.e., the Bayesian problem). We showed that total expected revenue in the Bayesian problem can exceed the total expected revenue in the robust problem, and consequently, we analyzed each problem in turn.

In the robust setting, we developed upper and lower bounds on total expected revenue that can be computed easily using the equi-marginal principle. In the Bayesian setting, we derived a payment formula that lends itself to a mathematical program that involves fewer variables than a straightforward implementation of the optimal auction problem. Additionally, we derived closed-form solutions to a relaxation of the Bayesian ex-ante problem, as well as problems that seek robust upper and lower bounds.

Based on our analysis, we derived heuristics that approximate solutions to both the robust and Bayesian revenue maximization problems. With three different distributions, we saw through experiments that our heuristics produce solutions that are close to optimal, and scale better than the mathematical programming solver we used. However, our experiments thus far were restricted to quasi-linear utility functions with quadratic perceived payments. In the future, we hope to run experiments with a wider class of payment functions, beyond quadratic, and possibly even develop theory that goes beyond convex entirely. Additionally, we hope to prove guarantees about our heuristics, to further characterize their quality.

10 Acknowledgments

This research was supported by NSF Grant #1217761 and Microsoft Research. Amy and Takehiro would also like to thank Jason Hartline and Tim Roughgarden for always being willing to help as we grappled with the details of Myerson’s seminal work.

Appendix A The Discretization Effect

Let be an optimal allocation rule in an arbitrary auction design problem, and let be an optimal allocation rule in the corresponding discretized problem, with discretization factor . For all bidders , let be such that

| (97) |

The optimal values and our approximation are related by a residual vector , each entry of which can be be positive, negative, or zero:

| (98) | ||||

| (99) |

To determine s, we use the method of least squares. Specifically, we minimize the square of the residual -norm:

| (100) |

To do so, we take derivatives with respect to :

| (101) |

Setting the right-hand side of this equation to 0 yields the following intuitive result:

| (102) |

Enforcing the constraint that must be integral leaves two possible candidate s:

| (103) |

In either case,

| (104) |

Therefore, the residual from bidder is bounded above by . Likewise, the total residual is bounded above by .

Having established a method of determining , we now describe how using can impact the total expected perceived payment. Let and be the perceived payments resulting from the allocation rules and , respectively. First, we show that the difference in expected the perceived payment from bidder when using instead of is . Then, we conclude that the total expected perceived payment is .

Lemma A.1.

The difference in bidder ’s expected perceived payment when using instead of is : i.e., .

Proof.

We can express the difference between and in terms of virtual values:

| (105) | ||||

| (106) | ||||

| (107) | ||||

| (108) |

∎

Corollary A.2.

The difference in total expected perceived payment when using instead of is : i.e., .

En route to deriving the difference in total expected revenue from using allocation rule instead of , we present the following lemma, which argues that the maximum difference in perceived payment from bidder is .

Lemma A.3.

The difference in bidder ’s perceived payment when using allocation rule instead of is : i.e., .

Proof.

Without loss of generality, assume . Allocation variables and can differ by at most , so the difference between and is maximized when , for an arbitrary value , and , for . Now

| (109) | ||||

| (110) | ||||

| (111) | ||||

| (112) | ||||

| (113) | ||||

| (114) | ||||

| (115) |

Therefore, the difference in perceived payments is . ∎

Having established Lemma A.3, we now show that discretization affects the expected revenue collected from bidder by , and total expected revenue by .

Lemma A.4.

The difference in expected revenue from bidder when using instead of is : i.e.,

Proof.

First, we construct payment rules and . We choose and , for all and , so that

| (116) | ||||

| (117) |

Likewise, for .

Corollary A.5.

The difference in total expected revenue when using instead of is : i.e., .

To summarize, in our setting, where a budget is finitely divisible by a factor , so that allocations are multiplicative factors of , in the usual linear case, where , total expected revenue is within of optimal. Furthermore, in the case of quadratic perceived payments, total revenue is within of optimal.

Appendix B Another Upper Bound

While non-operational as of yet, we present an easy-to-derive upper bound on revenue for completeness.

Lemma B.1.

Expected payments, when bidders have quasi-linear utility functions as described by Equation (1) and , can be upper-bounded as follows:

| (128) |

Proof.

Applying Theorem 5.2 to concave utilities with yields:

By Jensen’s inequality (since squaring is a convex function):

Combining the two equations and taking square roots completes the proof. ∎

Appendix C Program Descriptions

We describe the programs implemented, including the number of variables and constraints. Let , so that , for all bidders .

C.1 RRM Mathematical Programs

C.1.1 RRM

Mathematical Program

| (129) | |||||

| subject to | (130) | ||||

| (131) | |||||

| (132) | |||||

| (133) | |||||

| (134) | |||||

Variables

For each bidder , and for each , there are variables and . The total number of variables is .

Constraints

The total number of constraints is .

-

•

Ex-post feasibility. This requires equations.

-

•

Lower and upper bounds on . This requires equations.

-

•

Monotonicity. There are vectors and comparisons per bidder; so equations per bidder, and equations in all.

-

•

Payment formula. This requires equations.

C.1.2 RRM, Upper Bound (Pseudo-Surplus)

Mathematical Program

| (135) | |||||

| subject to | (136) | ||||

| (137) | |||||

| (138) | |||||

| (139) | |||||

Variables

For each bidder and for each , there are variables . The total number of variables is .

Constraints

The total number of constraints is .

-

•

Ex-post feasibility. This requires equations.

-

•

Lower and upper bounds on . This requires equations.

-

•

Monotonicity. There are vectors and comparisons per bidder; so equations per bidder, and equations in all.

C.1.3 RRM, Lower Bound (Heuristic)

Mathematical Program

| (140) | |||||

| subject to | (141) | ||||

| (142) | |||||

| (143) | |||||

| (144) | |||||

Variables

For each bidder and for each , there are variables . The total number of variables is .

Constraints

The total number of constraints is .

-

•

Ex-post feasibility. This requires equations.

-

•

Lower and upper bounds on . This requires equations.

-

•

Monotonicity. There are vectors and comparisons per bidder; so equations per bidder, and equations in all.

C.2 BRM, Ex-post Mathematical Programs

C.2.1 BRM, Ex-post

This program does not use Equation (11) to compute payments. Instead, it attempts to maximize revenue by relating and terms.

Mathematical Program

| (145) | |||||

| subject to | (146) | ||||

| (147) | |||||

| (148) | |||||

| (149) | |||||

| (150) | |||||

| (151) | |||||

| (152) | |||||

| (153) | |||||

Variables

For each bidder , and for each and , there are variables and . The total number of variables is .

Constraints

The total number of constraints is .

-

•

Ex-post feasibility. This requires equations.

-

•

Lower and upper bounds on . This requires equations.

-

•

Relating with . This requires equations.

-

•

Relating with . This requires equations.

-

•

Relating with . This requires equations.

-

•

Monotonicity. This requires equations.

-

•

Payment formula. This requires equations.

C.2.2 BRM, Ex-post, Simplified

This program uses Equation (11) to compute payments.

Mathematical Program

| (154) | |||||

| subject to | (155) | ||||

| (156) | |||||

| (157) | |||||

| (158) | |||||

| (159) | |||||

| (160) | |||||

Variables

For each bidder , and for each and , there are variables . The total number of variables is .

Constraints

The total number of constraints is .

-

•

Ex-post feasibility. This requires equations.

-

•

Lower and upper bounds on . This requires equations.

-

•

Relating with . This requires equations.

-

•

Monotonicity. This requires equations.

-

•

Payment formula. This requires equations.

C.2.3 BRM, Ex-post, Upper Bound (Pseudo-Surplus)

Mathematical Program

| (161) | |||||

| subject to | (162) | ||||

| (163) | |||||

| (164) | |||||

| (165) | |||||

| (166) | |||||

Variables

For each bidder and for each and , there are variables . The total number of variables is .

Constraints

The total number of constraints is .

-

•

Ex-post feasibility. This requires equations.

-

•

Lower and upper bounds on . This requires equations.

-

•

Relating with . This requires equations.

-

•

Monotonicity. This requires equations.

Remark C.1.

The BRM, ex-post, lower bound (heuristic) mathematical program has constraints that are identical to these, but differs in its objective function, which involves virtual values instead of values:

| (167) |

C.3 BRM Ex-ante Mathematical Programs

C.3.1 BRM, Ex-ante

Mathematical Program

| (168) | |||||

| subject to | (169) | ||||

| (170) | |||||

| (171) | |||||

| (172) | |||||

| (173) | |||||

Variables

For each bidder , and for each , there are variables and . The total number of variables is .

Constraints

The total number of constraints is .

-

•

Ex-ante feasibility. This requires equations.

-

•

Lower and upper bounds on . This requires equations.

-

•

Monotonicity. This requires equations.

-

•

Payment formula. This requires equations.

C.3.2 BRM, Ex-ante Relaxation

Mathematical Program

| (174) | |||||

| subject to | (175) | ||||

| (176) | |||||

| (177) | |||||

Variables

For each bidder , and for each , there are variables . The total number of variables is .

Constraints

The total number of constraints is .

-

•

Ex-ante feasibility. This requires equations.

-

•

Lower bounds on . This requires equations.

-

•

Monotonicity. This requires equations.

References

- Alaei et al. [2013] Saeed Alaei, Hu Fu, Nima Haghpanah, and Jason Hartline. The simple economics of approximately optimal auctions. In Foundations of Computer Science (FOCS), 2013 IEEE 54th Annual Symposium on, pages 628–637. IEEE, 2013.

- Border [1991] Kim C. Border. Implementation of reduced form auctions: A geometric approach. Econometrica, 59(4):pp. 1175–1187, 1991. ISSN 00129682. URL http://www.jstor.org/stable/2938181.

- Chawla et al. [2012] Shuchi Chawla, Jason D Hartline, and Balasubramanian Sivan. Optimal crowdsourcing contests. In Proceedings of the Twenty-Third Annual ACM-SIAM Symposium on Discrete Algorithms, pages 856–868. SIAM, 2012.

- DiPalantino and Vojnovic [2009] Dominic DiPalantino and Milan Vojnovic. Crowdsourcing and all-pay auctions. In Proceedings of the 10th ACM conference on Electronic commerce, pages 119–128. ACM, 2009.

- Gossen [1854] Hermann Heinrich Gossen. Entwickelung der gesetze des menschlichen verkehrs, und der daraus fliessenden regeln für menschliche handeln. F. Vieweg, 1854.

- Johari and Tsitsiklis [2011] Ramesh Johari and John N. Tsitsiklis. Parameterized supply function bidding: Equilibrium and efficiency. Operations Research, 59(5):1079–1089, 2011.

- Maskin and Riley [1984] Eric Maskin and John Riley. Optimal auctions with risk averse buyers. Econometrica, 52(6):pp. 1473–1518, 1984. ISSN 00129682. URL http://www.jstor.org/stable/1913516.

- Myerson [1981] Roger B Myerson. Optimal auction design. Mathematics of Operations Research, 6(1):58–73, 1981.

- Pai and Vohra [2014] Mallesh M. Pai and Rakesh Vohra. Optimal auctions with financially constrained buyers. Journal of Economic Theory, 150:383 – 425, 2014. ISSN 0022-0531. doi: http://dx.doi.org/10.1016/j.jet.2013.09.015. URL http://www.sciencedirect.com/science/article/pii/S0022053113001701.

- Singer [2014] Yaron Singer. Budget feasible mechanism design. SIGecom Exch., 12(2):24–31, November 2014. ISSN 1551-9031. doi: 10.1145/2692359.2692366. URL http://doi.acm.org/10.1145/2692359.2692366.

- Vickrey [1961] William Vickrey. Counterspeculation, auctions, and competitive sealed tenders. The Journal of finance, 16(1):8–37, 1961.