Timing Options for a Startup with Early Termination and Competition Risks

Abstract

This paper analyzes the timing options embedded in a startup firm, and the associated market entry and exit timing decisions under the exogenous risks of early termination and competitor’s entry. Our valuation approach leads to the analytical study of a non-standard perpetual American installment option nested with an optimal sequential stopping problem. Explicit formulas are derived for the firm’s value functions. Analytically and numerically, we show that early termination risk leads to earlier voluntary entry or exit, and the threat of competition has a non-trivial effect on the firm’s entry and abandonment strategies.

Keywords: startup, market entry, project abandonment, early termination, competition risk

JEL Classification: C41, G11, G13, M13

Mathematics Subject Classification (2010): 60G40, 62L15, 91G20, 91G80

1 Introduction

Over the past two decades, there have been a number of highly successful startup companies. Nevertheless, in general firms in their early stages require significant capital investment for research and development (R&D) and face tremendous amount risk that may force them to abandon the projects. Many startups may fail before they even sell a single unit of products. The risk of early termination may be due to demand uncertainty, technological challenges, regulatory changes, and other causes.

Another major risk factor for a startup is the emergence of a competitor. This is commonly seen in markets with very few major players, for example, Lyft’s entry to New York City to compete with Uber,111http://www.wsj.com/articles/lyft-revs-up-in-new-york-city-1448038672 and the launch of Apple music to rival Pandora and Spotify.222http://www.wsj.com/articles/apple-to-announce-new-music-services-1433183201 In effect, new competition may reduce the existing firm’s market share and thus revenue stream, as noted by Petersen and Bason (2001). In turn, this influences how long the firm can stay in the market.

In this paper, we propose a theoretical real option approach to better understand a startup firm’s strategies to voluntarily abandon a project or enter the market in face of early termination and competition risks. The arrivals of early termination and competition are modeled by exogenous independent exponential random variables. We analyze their combined impact on the firm’s optimal timing to enter or exit. Our valuation approach is a non-standard perpetual American installment option nested with an optimal sequential stopping problem.

Our main results are the analytic solutions for the firm’s sequential timing problems. We also investigate the impact of the early termination risk and the competitor’s potential entry on the firm’s value and the associated timing to enter and exit the market. Among our findings, the firm has a lower entry threshold and higher cancellation threshold when the early termination risk rises. On the other hand, competition risk may increase or decrease the firm’s abandonment level, depending on the impact on the new cash flow. We provide the necessary and sufficient condition for both cases. Numerical results are provided to illustrate these effects.

In the literature, Pennings and Lint (1997) study the empirical option value of an R&D project, and model the arrivals of new information that impact cash flows by exponential random variables. Lukas et al. (2016) propose an entrepreneurial venture financing model without competition risk by combining compound option pricing with sequential non-cooperative contracting. Kort and Wrzaczek (2015) apply a game-theoretic approach to study the incumbent’s over or under investment problem accounting for the threat of entry. Also, Restrepo et al. (2015) study a real option approach for sequential investments in the presence of expropriation risk. Davis et al. (2004) study the valuation of a venture capital as an installment option, while Ciurlia and Caperdoni (2009) and Kimura (2009) study the pricing of American installment put and call options. Our model can be viewed as a perpetual American-style installment compound option with three stopping times. The incubation period in our model is similar to the time-to-build in infrastructure investments, which also involves a timing option to start operation; see Dahlgren and Leung (2015). Kwon (2010) studies the firm’s decision to discard or invest in an aging technology with a declining profit stream with demand uncertainty. The theory of optimal stopping is applied to study project management with uncertain completion in Chi et al. (1997), and to develop strategies for drug discovery in Zhao and Chen (2009), among others. Sequential stopping problems also arise in other applications, such as participating a government subsidized program (Huisman and Thijssen (2013)), and trading under mean reversion (Leung and Li (2015a, b)).

This paper is organized as follows. In Section 2, we introduce the firm’s investment timing problems, and present our formulation. Then, we present the solutions of the optimal abandonment timing problem in Section 3, and the optimal entry timing problem in Section 4. In Section 5, we examine the effects of the early termination risk and competitor’s entry on the firm’s strategies. Section 6 concludes. All proofs are included in the Appendix.

2 Problem Formulation

In the background, we fix a complete probability space . The firm’s valuation is conducted under the historical probability measure , with a subjective discount rate , as in McDonald and Siegel (1986). We consider a startup firm that can enter a targeted market and generate a stochastic cash flow until the firm’s voluntary abandonment time. We assume that the firm acts as a price taker in this market. The cash flow is driven by a stochastic factor , satisfying

| (2.1) |

with drift and volatility . For instance, we can interpret as the prevailing market price of the goods/services sold by the firm. Let be the filtration generated by , and be the set of all stopping times with respect to .

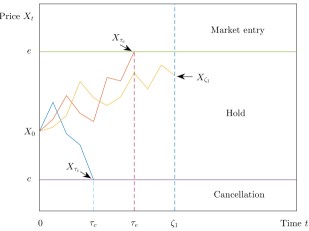

The firm seeks to maximize its net present value (NPV) by selecting the best time to enter the market. Prior to the entry, as depicted by Figure 1(a), the firm can cancel the project at time (bottom path), or is forced to abort the project due to early termination risk at time (middle path) during this incubation period. If either event occurs, the firm stops operation and generates no future cash flow. In the third scenario (top path), the firm avoids early termination and opts to enter the market at time .

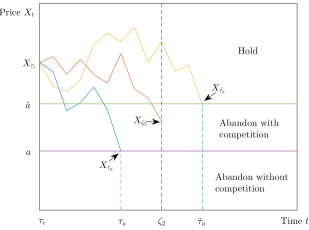

Figure 1(b) illustrates the scenarios after market entry. Given that the firm has entered the market, the firm can abandon the project before or after the competitor’s arrival time . In these two possible situations, the firm’s abandonment decision with or without competition, represented by the thresholds and respectively, can be different. For instance, the firm may have a higher abandonment threshold if there is competition in the market, i.e. (top and bottom paths). As such, the firm will stay in the market even when the price is below but above before the competitor arrives. In this case, as soon as the competitor enters suddenly at time , the firm’s abandonment level switches to the higher level above the current value of , forcing the firm to abandon immediately (middle path). The random times involved in our model are summarized in Table 1.

| Random times | Description |

|---|---|

| Firm’s cancellation time to forgo market entry | |

| Firm’s entry time | |

| Firm’s abandonment time after market entry without new competition | |

| Firm’s abandonment time after competitor’s entry | |

| Exogenous early termination time during the incubation period | |

| Competitor’s exogenous arrival time after the firm’s entry |

To formulate the firm’s timing problems, we first consider the scenario with a competition in the market post-entry period. In this case, we specify the profit stream by . Our model assumes a linear function: for all , where , . We can interpret the fraction as a reduction in revenue, and as the fixed cost when the firm faces new competition. In addition, let be the abandonment time after the competitor’s entry. To maximize its net present value (NPV), the firm solves the optimal stopping problem

| (2.2) |

where .

When the firm first enters the market, it generates a profit stream , where we assume for all , where represents the fixed cost. Then the firm operates till the abandonment time when facing no new competition. If the competitor arrives at (before the firm’s abandonment), then the firm’s NPV is exactly (see (2.2)). In other words, the firm will continue to generate the profit stream from time on, after having accumulated the profit stream up to . We assume that is an exponential random variable with parameter , independent of price process . Therefore, before new competition arrives, the firm’s maximized NPV is

| (2.3) |

which follows from the distribution of and law of iterated expectations. The derivation is provided in the Appendix A.1. As we can see, the value function in (2.2) becomes an input to the firm’s value function in (2.3).

During the incubation period, the firm has to pay the operating cost over time. For simplicity, we let for all , with constants . The firm may choose to cancel the project at time , but could end up terminating it early at the exogenous time , which is an exponential random variable with parameter , independent of price process and . If the firm avoids cancellation and termination, then it will enter the market at time . Therefore, the firm’s pre-entry value function is given by

| (2.4) |

The last step (2.4) is derived similarly to (2.3); see Appendix A.1.

3 Optimal Abandonment Timing Problem

We first analyze the firm’s exit problem represented by in (2.2). If , then we have

| (3.1) |

The last equality holds due to and . As a result, it is optimal for the firm to never exit the market if , with an infinite NPV.

Therefore, in the rest of the paper, we consider the non-trivial case . To facilitate our presentation, we define the constants

| (3.2) |

Proposition 3.1.

The firm’s optimal timing to abandon is given by the first time the value function reaches zero. This occurs when , so we have

| (3.5) |

In particular, the optimal abandonment threshold is slightly smaller than the ratio , but note that for . That means that, even if the firm is currently incurring a loss, it does not immediately abandon but will wait for the profit to improve in the future. When the price falls further to the lower level , then the firm will decide to abandon. The explicit expression of is amenable for sensitivity analysis, which we summarize as follows.

Corollary 3.2.

The optimal threshold is increasing in , , and decreasing in , , .

From Proposition 3.1, we see that is increasing and becomes nearly linear when is large since the term () diminishes to zero. In fact, it’s dominated by the linear part, even if is close to (see the proof of Corollary 3.3 in Appendix A).

Corollary 3.3.

is increasing convex in . In addition, when is sufficient large, is increasing in , , and decreasing in , .

Next we turn to the optimal abandonment problem . The explicit solution of will become the input to the problem for . We derive the optimal threshold-type strategy. Let denote the abandonment price level before new competition arrives. New competition will bring about a reduction in revenue for the firm, described by the fraction . If the revenue impact is low, then the firm will choose to stay longer in the market and exit in a lower threshold, and thus we expect . In contrast, when the firm’s revenue is significantly reduced, then it is more likely that the firm will experience a negative cash flow, and may be forced to leave the market earlier. This means that the post-competition threshold is higher than the pre-competition level . As is intuitive, the aforementioned first and second cases correspond to, respectively, the large and small values of . As we show below, the two cases are separated by the critical value of , defined by

| (3.6) |

where as in (3.2).

Proposition 3.4.

The firm’s pre-competition optimal abandonment problem (2.3) is solved as follows:

(I) If and , then there exists a unique such that

| (3.7) |

The value function is given by

| (3.8) |

(II) If , or and , then there exists a unique such that

| (3.9) |

The value function is given by

| (3.10) |

In both cases (I) and (II), the firm’s optimal abandonment time without competition is given by

| (3.11) |

The coefficients in above expressions are given by

| (3.12) | ||||

| (3.13) | ||||

| (3.14) | ||||

| (3.15) | ||||

| (3.16) | ||||

| (3.17) |

Proposition 3.4 gives the exact conditions to determine the ordering of the thresholds and . As an example, let so that the post-competition profit stream be proportional to , i.e. . Proposition 3.4 indicates that , and thus we have in case (II). In this example, the firm will have a smaller profit stream after the competitor’s arrival. To compensate the reduction in profit, the firm opts to stay longer in the market with the competitor and exit at a lower threshold.

To determine which case applies, the simple first step is to check whether is larger than or not. If , it falls into case (II). Otherwise, we need to check the values of the parameters and (see (3.6)). Note if , then , which can be seen directly from (3.6). Next, Corollary 3.5 describes the behavior of and its sensitivity in the arrival rate of competition .

Corollary 3.5.

Suppose , then we have . Moreover, is strictly decreasing with respect to , and it admits a limit

| (3.18) |

This also leads to the curious question: under what conditions does the abandonment level stay unchanged after the competitor’s entry? From the proof of Proposition 3.4 in the Appendix, we see that if and only if and . As a concrete example, let and , then . This is intuitive since in this case the competitor’s entry does not affect the firm’s profit stream, and thus its abandonment timing.

4 Optimal Entry Timing Problem

We now analyze the firm’s optimal entry timing problem defined in (2.4). Suggested by Figure 1(a), the firm can choose to cancel the project, enter the market, or wait at anytime during the incubation period. This leads us to determine the upper and lower thresholds, and , for entry and cancellation by the firm.

Proposition 4.1.

Remark 4.2.

To our best knowledge, the above system of nonlinear equations do not admit explicit solutions. Even in the simpler perpetual American installment call/put option problem studied in Ciurlia and Caperdoni (2009); Kimura (2009), similar systems of equations arise and no explicit solutions are given. Nevertheless, these equations can be solved efficiently by standard root-finding methods, such as the Newton-Raphson method, available in many computational softwares.

The value function depends on the early termination risk parameter as we can see from in (4.2) and the coefficients in (4.3)-(4.6). We observe from (4.1) that equals to for . Therefore, the competition risk, which exists after the firm’s entry, has an indirect effect on the firm’s decisions prior to entering the market since , and thus and , depend on . Moreover, noticing that appears in (4.3)-(4.6), enters the system of equations for and indirectly through the value function that is tied to . As a result, both and depend on .

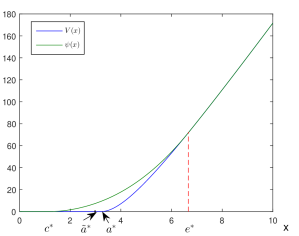

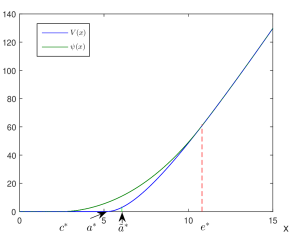

Figure 2 shows the value functions and , along with four thresholds , , , and . From both panels, we see that and are both increasing in as a higher expected net present value is attained at a higher price level. The value function dominates due to the timing option (to enter the market) embedded in . If the firm chooses to enter immediately at some , then we have . This occurs for . By checking the condition in Proposition 3.4, we have and , and in turn, in Figure 2(a) while in Figure 2(b). In other words, the left and right panels represent case (I) with and case (II) with in Proposition 3.4 respectively.

Also, we observe that the cancellation threshold is smaller than both post-entry abandonment thresholds and . During the incubation period, the option to enter induces the firm to be willing to incur a loss in order to wait for the opportunity to enter the market. However, once the firm has entered the market, the entry option vanishes, and the firm demands more profit to stay in the market, and will exit at a level higher than .

5 Sensitivity Analysis

In this section, we examine the effects of the early termination risk and the competitor’s arrival on the firm’s optimal strategies. Common parameters are of the same values as in Figure 2.

5.1 Early Termination

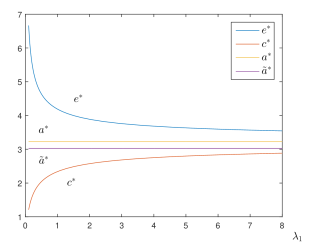

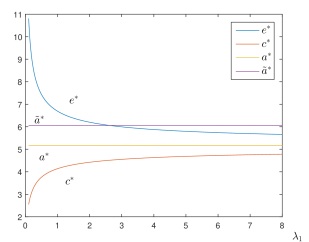

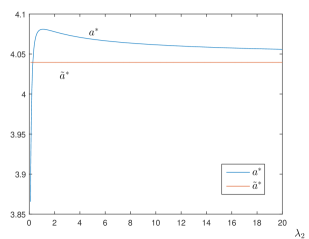

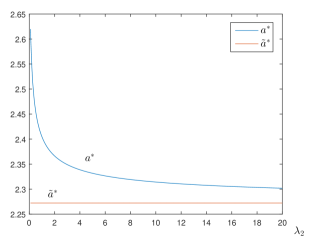

First, we conduct a sensitivity analysis of the thresholds with respect to the early termination rate . As is seen in Figure 3, the pre/post-competition abandonment levels do not change with since the firm has already entered the market. For the entry and cancellation thresholds, we see that decreases but increases as increases. In other words, a high early termination risk induces the firm to enter the market early, even if that means capturing a lower profit stream upon entry. Moreover, the firm may also cancel the project earlier because the expected profitability is reduced by the higher termination risk. In Figure 3, we also observe that the threshold is higher than while is lower than .

Figures 3(a) and 3(b) depict the two cases and respectively. The impact of early termination risk is different in these two scenarios. If the competitor’s entry causes a significant shrinkage in the firm’s profit as in case (II), then the post-competition abandonment level will be higher than the pre-competition one . Also, the firm’s entry level is decreasing in . In Figure 3(b), we see that will eventually fall below but stay above . In this case, whenever the competitor enters, the firm switches its abandonment level to the higher level . This forces the firm to abandon immediately involuntarily if the current value of is below .

5.2 Competition Risk

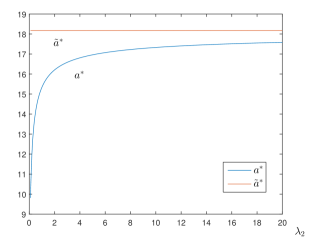

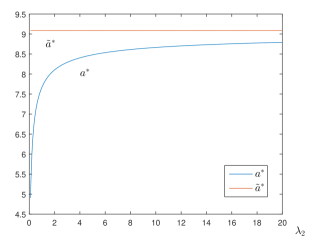

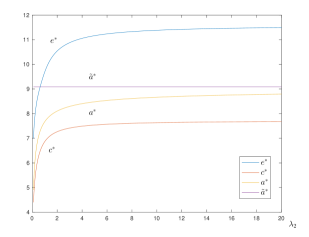

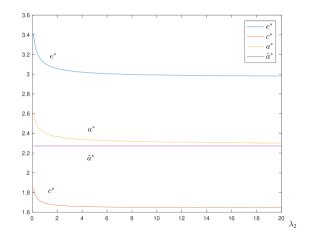

The risk of competition will influence the firm’s pre-competition exit strategy, described by , in a non-trivial way. We discuss the four scenarios of different sensitivities in Figure 4. In the following discussion, we keep in mind that doesn’t depend on and is decreasing in by Corollary 3.5.

Figure 4(a) illustrates the first scenario with . This corresponds to case (II) in Proposition 3.4, where we have shown that for all . In addition, is increasing in , which means that the firm will choose to exit early under the threat of competitor’s entry.

For the remaining three scenarios in Figures 4(b)-4(d), we have . By Corollary 3.5, we have for all . In Figure 4(b), is again increasing in . In this figure, we have , which belongs to case (II) in Proposition 3.4, and thus .

Figure 4(c) shows that is first increasing then decreasing in . This is because the constant is first larger than but then smaller than as increases. Therefore, as increases, it changes from case (II) to case (I) in Proposition 3.4. That explains why is smaller than at first, and the relation reverses for large .

Lastly, in Figure 4(d) we have , which corresponds to case (I) in Proposition 3.4. We have shown that for all . In contrast to the other scenarios, the pre-competition threshold is decreasing and approaches as increases. In this scenario, the impact of the competitor’s entry on the firm’s profit is much less than in other scenarios, as indicated by the higher value of .

In summary, scenarios (a), (b), and the first part of scenario (c) belong to case (II), in which the competitor’s potential entry will lead to a significant profit reduction. Therefore, the firm exits early by selecting a higher pre-competition abandonment threshold as the competitor’s arrival rate increases. The opposite happens to scenario (d) and the second part (large ) of scenario (c). As increases, which means high risk of facing competition in the future, the firm tries to stay longer before the competitor’s entry to make more profits in case of the potential significant loss afterwards. This results in a decreasing pre-competition abandonment threshold .

Despite different behaviors of , there is a common phenomenon that approaches as increases. The intuitive explanation is as follows. When the competition risk is very high, the firm will adjust its abandonment level in order not to be affected too much when the competitor eventually enters. That means that the firm’s abandonment level before the competitor’s entry will be close to the post-competition abandonment level .

In addition to , the entry and cancellation thresholds and are also affected by the competitor’s arrival rate after the firm’s market entry. In two scenarios, Figure 5(a) and Figure 5(b) respectively take the same parameters as Figure 4(b) and Figure 4(d), so they represent respectively case (II) and (I) in Proposition 3.4. Figure 5(a) shows that both and are increasing in under case (II). In particular, the entry threshold is seen to be lower than the abandonment threshold when is small, but then surpasses it for large . In this case, the competitor’s arrival will lead to a significant post-entry profit reduction. Therefore, as is intuitive, the firm requires a higher entry level to ensure a higher post-entry profit so as to make the entry worthwhile. Nevertheless, under case (I), Figure 5(b) shows that both and are decreasing in . In other words, when the post-entry competition arrival is not expected to have a significant impact on profit, the firm will opt to enter the market earlier at a lower entry threshold.

6 Concluding Remarks

We have developed a model to evaluate the timing options to enter or exit a given market for a startup firm. Our model accounts for the risks of early termination prior to market entry, as well as the risk of new competition that may reduce the firm’s future profit stream. Our analytic solutions allow for instant computation of the firm’s optimal expected NPV and the associated optimal timing strategies. We have provided explanation on the non-trivial combined effect of early termination and competition risks on the firm’s entry and pre-competition abandonment decisions.

There are a number of directions for future research. For tractability, we have chosen to work with a lognormal model. Alternatively, we will consider in future work other dynamics for the underlying price process, such as jump diffusions or mean-reverting processes, such as the Cox-Ingersoll-Ross, and exponential Ornstein-Uhlenbeck processes (Leung et al. (2014), Leung et al. (2015)). For a startup, it is also useful to choose between equity and debt financing and examine the implications to the firm’s investment and bankruptcy decisions (see, e.g. Tian (2011)). Another natural extension of our model is to incorporate sequential random arrivals and departures of competitors.

Appendix A Appendix

In this appendix, we provide the proofs of all the propositions and corollaries presented above.

A.1 Proof of Equations (2.3) and (2.4)

Recall that is the filtration generated by . We re-state equation (2.3), and apply the tower property to get

| (A.1) |

The arrival time is exponentially distributed and independent of , so the first term inside the expectation (A.1) can be written as

| (A.2) |

A.2 Proof of Proposition 3.1

Proof.

We consider a candidate stopping time , where . In the stopping region , from the definition of and (2.2). In the continuation region , satisfies the following ODE:

| (A.4) |

with boundary conditions:

| (A.5) |

A.3 Proof of Corollary 3.2

Proof.

First, we define the ratio:

| (A.9) |

From (A.9) and the expression of in (3.4), we know that increases in and thus increases in .

Next, we differentiate with respect to . Let , then

| (A.10) |

Since , we have and thus decreases with respect to .

In addition,

| (A.11) |

Therefore and indicate that decreases in and thus decreases in .

Finally, that decreases in and increases in can be directly inferred from (3.4). ∎

A.4 Proof of Corollary 3.3

Proof.

We take the first and second derivatives of , namely,

| (A.12) |

In turn, implies and for all . In addition, when is sufficient large, the first part of is negligible and its sensitivity with respect to the parameters can be deduced from (3.3). ∎

A.5 Proof of Proposition 3.4

To prove Proposition 3.4, we first establish the following lemmas.

Lemma A.1.

Let such that

| (A.13) |

then there exists unique , such that , if and only if and . If , then .

Proof.

We take the first and second derivatives of ,

| (A.14) | ||||

| (A.15) |

Notice and , then for all . This means is a decreasing function with respect to . By inspection, we have

| (A.16) |

The derivative means that is unimodal and maximized at . Moreover, we have . Note that is a decreasing function of . When , . Therefore, we see that for all .

There exists a unique such that and if and only if . To see this, if there is an such that , then , because is a decreasing function when and . On the other hand, if , the existence and uniqueness of comes from the fact that is continuous and decreasing for , along with .

Now is given by

| (A.17) |

It’s easy to see that is increasing in , holding other parameters fixed. When , , which means for all .

If , then , and there is not an such that .

If , then

| (A.18) |

From cases and above, we conclude that and iff iff there exists a unique such that and . Moreover, iff and , due to the uniqueness of . ∎

Lemma A.2.

Let such that

| (A.19) |

then there exists unique , such that , if and only if , or and .

Proof.

We take the first derivative of ,

| (A.20) |

Conditions , and indicate for all and thus is a decreasing function in . and imply that there exists unique such that .

Now we need to check whether or not. Note if and only if .

| (A.21) |

Now let’s focus on the proof of Proposition 3.4.

Proof.

We consider a candidate stopping time , where . We split the problem into two cases: and .

(I) We first assume . In the stopping region , from the definition and (2.3). In the continuation region , satisfies the following ODE:

| (A.22) |

with boundary conditions:

| (A.23) |

The ODE and last condition in (A.23) indicate that the general solution is given by , where is a constant, is the negative root of the associated quadratic equation, and is a particular solution of (A.22):

| (A.24) |

To determine and , we utilize boundary conditions (A.23) to get the following system of equations:

| (A.25) | ||||

| (A.26) |

The above equations yield (3.7). From Lemma A.1, if and , then there exists unique , satisfying (3.7). We solve numerically and plug it in (A.25) and (A.26), then we can get (3.12) and thus (3.8).

(II) Next we assume . Also from the definition and (2.3), in the stopping region . In the continuation region , satisfies the following ODE:

| (A.27) |

with continuous fit and smooth-pasting conditions:

| (A.28) | ||||

| (A.29) |

Since is a piecewise function, the general solution is also a piecewise function,

| (A.30) |

where

| (A.31) | ||||

| (A.32) |

The constants to are determined by (A.29), and and are the two roots of the quadratic equation: . In (A.31) and (A.32), the particular solution is given by (A.24), and

| (A.33) |

To determine , , , and , we refer to (A.29) to get the following system of equations:

| (A.34) | ||||

| (A.35) | ||||

| (A.36) | ||||

| (A.37) |

A.6 Proof of Corollary 3.5

Proof.

First, recall that and , which after some algebra implies that (see (3.6)). We rewrite in the following form

| (A.38) | ||||

| (A.39) |

where

| (A.40) |

and under the condition . Since depends on , we differentiate to get

| (A.41) |

where

| (A.42) |

A.7 Proof of Proposition 4.1

Proof.

We consider two candidate stopping times and , where . In the entry region , the firm enters the market and thus . In the cancellation region , we have . In the continuation region, , where the firm waits for entry or cancellation, the firm’s value function satisfies the ODE:

| (A.49) |

with the boundary conditions:

| (A.50) |

The general solution of the above ODE is given by , where and are roots of the quadratic equation: , and is a linear particular solution of (A.49):

| (A.51) |

To determine and , along with the constants and , we apply the conditions in (A.50) to obtain the system of equations (4.3)-(4.6). ∎

References

- Chi et al. (1997) Chi, T., Liu, J., and Chen, H. (1997). Optimal stopping rule for a project with uncertain completion time and partial salvageability. IEEE Transactions on Engineering Management, 44(1):54–66.

- Ciurlia and Caperdoni (2009) Ciurlia, P. and Caperdoni, C. (2009). A note on the pricing of perpetual continuous-installment options. Mathematical Methods in Economics and Finance, 4:11–26.

- Dahlgren and Leung (2015) Dahlgren, E. and Leung, T. (2015). An optimal multiple stopping approach to infrastructure investment decisions. Journal of Economic Dynamics and Control, 53:251–267.

- Davis et al. (2004) Davis, M., Schachermayer, W., and Tompkins, R. G. (2004). The evaluation of venture capital as an installment option: Valuing real options using real options. In Dangl, T., Kopel, M., and Kürsten, W., editors, Real Options, pages 77–96. Gabler Verlag.

- Huisman and Thijssen (2013) Huisman, K. and Thijssen, J. J. (2013). To have and to hold: A dynamic cost-benefit analysis of temporary unemployment measures. Working paper, Department of Economics, University of York.

- Kimura (2009) Kimura, T. (2009). American continuous-installment options: Valuation and premium decomposition. SIAM Journal on Applied Mathematics, 70(3):803–824.

- Kort and Wrzaczek (2015) Kort, P. M. and Wrzaczek, S. (2015). Optimal firm growth under the threat of entry. European Journal of Operational Research, 246(1):281–292.

- Kwon (2010) Kwon, H. D. (2010). Invest or exit? Optimal decisions in the face of a declining profit stream. Operations Research, 58(3):638–649.

- Leung and Li (2015a) Leung, T. and Li, X. (2015a). Optimal Mean Reversion Trading: Mathematical Analysis and Practical Applications. World Scientific, Singapore.

- Leung and Li (2015b) Leung, T. and Li, X. (2015b). Optimal mean reversion trading with transaction costs and stop-loss exit. International Journal of Theoretical & Applied Finance, 18(3):1550020.

- Leung et al. (2014) Leung, T., Li, X., and Wang, Z. (2014). Optimal starting–stopping and switching of a CIR process with fixed costs. Risk and Decision Analysis, 5(2):149–161.

- Leung et al. (2015) Leung, T., Li, X., and Wang, Z. (2015). Optimal multiple trading times under the exponential OU model with transaction costs. Stochastic Models, 31(4):554–587.

- Lukas et al. (2016) Lukas, E., Mölls, S., and Welling, A. (2016). Venture capital, staged financing and optimal funding policies under uncertainty. European Journal of Operational Research, 250(1):305–313.

- McDonald and Siegel (1986) McDonald, R. and Siegel, D. R. (1986). The value of waiting to invest. The Quarterly Journal of Economics, 101(4):707–727.

- Pennings and Lint (1997) Pennings, E. and Lint, O. (1997). The option value of advanced R&D. European Journal of Operational Research, 103:83–94.

- Petersen and Bason (2001) Petersen, S. B. and Bason, P. C. (2001). Literature on real options in venture capital and R&D. Essay number 8 in series: Real options approaches in venture capital finance.

- Restrepo et al. (2015) Restrepo, D. C., Correia, R., Peña, I., and Población, J. (2015). Expropriation risk, investment decisions and economic sectors. Economic Modelling, 48:326–342.

- Tian (2011) Tian, Y. (2011). Financing and investment under different debt structures. Financial Modeling and Analysis, 1736:200–215.

- Zhao and Chen (2009) Zhao, G. and Chen, W. (2009). Enhancing R&D in science-based industry: An optimal stopping model for drug discovery. International Journal of Project Management, 27(8):754 – 764.