Penalized Maximum Likelihood Estimation of

Multi-layered Gaussian Graphical Models

Abstract

Analyzing multi-layered graphical models provides insight into understanding the conditional relationships among nodes within layers after adjusting for and quantifying the effects of nodes from other layers. We obtain the penalized maximum likelihood estimator for Gaussian multi-layered graphical models, based on a computational approach involving screening of variables, iterative estimation of the directed edges between layers and undirected edges within layers and a final refitting and stability selection step that provides improved performance in finite sample settings. We establish the consistency of the estimator in a high-dimensional setting. To obtain this result, we develop a strategy that leverages the biconvexity of the likelihood function to ensure convergence of the developed iterative algorithm to a stationary point, as well as careful uniform error control of the estimates over iterations. The performance of the maximum likelihood estimator is illustrated on synthetic data.

Key Words: graphical models; penalized likelihood; block coordinate descent; convergence; consistency

1 Introduction

The estimation of directed and undirected graphs from high-dimensional data has received a lot of attention in the machine learning and statistics literature (e.g., see Bühlmann and Van De Geer, 2011, and references therein), due to their importance in diverse applications including understanding of biological processes and disease mechanisms, financial systems stability and social interactions, just to name a few (Sachs et al., 2005; Wang et al., 2007; Sobel, 2000). In the case of undirected graphs, the edges capture conditional dependence relationships between the nodes, while for directed graphs they are used to model causal relationships (Bühlmann and Van De Geer, 2011).

However, in a number of applications the nodes can be naturally partitioned into sets that exhibit interactions both between them and amongst them. As an example, consider an experiment where one has collected data for both genes and metabolites for the same set of patient specimens. In this case, we have three types of interactions between genes and metabolites: regulatory interactions between the two of them and co-regulation within the gene and within the metabolic compartments. The latter two types of relationships can be expressed through undirected graphs within the sets of genes and metabolites, respectively, while the regulation of metabolites by genes corresponds to directed edges. Note that in principle there are feedback mechanisms from the metabolic compartment to the gene one, but these are difficult to detect and adequately estimate in the absence of carefully collected time course data. Another example comes from the area of financial economics, where one collects data on returns of financial assets (e.g. stocks, bonds) and also on key macroeconomic indicators (e.g. interest rate, prices indices, various measures of money supply and various unemployment indices). Once again, over short time periods there is influence from the economic variables to the returns (directed edges), while there are co-dependence relationships between the asset returns and the macroeconomic variables, respectively, that can be modeled as undirected edges.

Technically, such layered network structures correspond to multipartite graphs that possess undirected edges and exhibit a directed acyclic graph structure between the layers, as depicted in Figure 1, where we use directed solid edges to denote the dependencies across layers and dashed undirected edges to denote within-layer conditional depedencies.

Selected properties of such so-called chain graphs have been studied in the work of Drton and Perlman (2008), with an emphasis on two alternative Markov properties including the LWF Markov property (Lauritzen and Wermuth, 1989; Frydenberg, 1990) and the AMP Markov property (Andersson et al., 2001).

While layered networks being interesting from a theoretical perspective and having significant scope for applications, their estimation has received little attention in the literature. Note that for a 2-layered structure, the directed edges can be obtained through a multivariate regression procedure, while the undirected edges in both layers through existing procedures for graphical models (for more technical details see Section 2.2). This is the strategy leveraged in the work of Rothman et al. (2010), where for a 2-layered network structure proposed a multivariate regression with covariance estimation (MRCE) method for estimating the undirected edges in the second layer and the directed edges between them. A coordinate descent algorithm was introduced to estimate the directed edges, while the popular glasso estimator (Friedman et al., 2008) was used for the undirected edges. However, this method does not scale well according to the simulation results presented and no theoretical properties of the estimates were provided. In follow-up work, Lee and Liu (2012) proposed the Plug-in Joint Weighted Lasso (PWL) and the Plug-in Joint Graphical Weighted Lasso (PWGL) estimator for estimating the same 2-layered structure, where they use a weighted version of the algorithm in Rothman et al. (2010) and also provide theoretical results for the low dimensional setting, where the number of samples exceeds the number of potential directed and undirected edges to be estimated. Finally, Cai et al. (2012) proposed a method for estimating the same 2-layered structure and provided corresponding theoretical results in the high dimensional setting. The Dantzig-type estimator (Candes and Tao, 2007) was used for the regression coefficients and the corresponding residuals were used as surrogates, for obtaining the precision matrix through the CLIME estimator (Cai et al., 2011). While the above work assumed a Gaussian distribution for the data, in more recent work by Yang et al. (2014), the authors constructed the model under a general mixed graphical model framework, which allows each node-conditional distribution to belong to a potentially different univariate exponential family. In particular, with an underlying mixed MRF graph structure, instead of maximizing the joint likelihood, the authors proposed to estimate the homogeneous and heterogenous neighborhood for each node (which corresponds to undirected and directed edges respectively, if put in the layered-network setting) by obtaining the regularized -estimator of the node-conditional distribution parameters, using traditional approaches (e.g. Meinshausen and Bühlmann, 2006) for neighborhood estimation. However, if we consider the overall error incurred by the neighborhood selection procedure of each individual node, the error bound becomes not tight due to the union bound operation used to obtain it.

In this work, we obtain the regularized maximum likelihood estimator under a sparsity assumption on both directed and undirected parameters for multi-layered Gaussian graphical models and establish its consistency properties in a high-dimensional setting. As discussed in Section 3, the problem is not jointly convex on the parameters, but convex on selected subsets of them. Further, it turns out that the problem is biconvex if we consider a recursive multi-stage estimation approach that at each stage involves only regression parameters (directed edges) from preceeding layers and precision matrix parameters (undirected edges) for the last layer considered in that stage. Hence, we decompose the multi-layer network structure estimation into a sequence of 2-layer problems that allows us to establish the desired results. Leveraging the biconvexity of the 2-layer problem, we establish the convergence of the iterates to the maximum-likelihood estimator, which under certain regularity conditions is arbitrarily close to the true parameters. The theoretical guarantees provided require a uniform control of the precision of the regression and precision matrix parameters, which poses a number of theoretical challenges resolved in Section 3.

In summary, despite the lack of overall convexity, we are able to provide theoretical guarantees for the MLE in a high dimensional setting. We believe that the proposed strategy is generally applicable to other non-convex statistical estimation problems that can be decomposed to two biconvex problems. Further, to enhance the numerical performance of the MLE in finite (and small) sample settings, we introduce a screening step that selects active nodes for the iterative algorithm used and that leverages recent developments in the high-dimensional regression literature (e.g., Van de Geer et al., 2014; Javanmard and Montanari, 2014; Zhang and Zhang, 2014). We also post-process the final MLE estimate through a stability selection procedure. As mentioned above, the screening and stability selection steps are beneficial to the performance of the MLE in finite samples and hence recommended for similarly structured problems.

The remainder of the paper is organized as follows. In Section 2, we introduce the proposed methodology, with an emphasis on how the multi-layered network estimation problem is decomposed into a sequence of two-layered network estimation problem(s). In Section 3, we provide theoretical guarantees for the estimation procedure posited. In particular, we show consistency of the estimates and convergence of the algorithm, under a number of common assumptions in high-dimensional settings. In Section 4, we show the performance of the proposed algorithm with simulation results under different simulation settings, and introduce serveral accerleration techniques which speed up the convergence of the algorithm and reduce the computing time in practical settings.

2 Problem Formulation.

Consider an -layered Gaussian graphical model. Suppose there are nodes in Layer , denoted by

The structure of the model is given as follows:

-

–

Layer 1. .

-

–

Layer 2. For : , with , and .

-

-

–

Layer . For :

and .

The parameters of interest are all directed edges that encode the dependencies across layers, that is:

and all undirected edges that encode the conditional dependencies within layers after adjusting for the effects from directed edges, that is:

It is assumed that and are sparse for all and .

Given centered data for all layers, denoted by for all , we aim to obtain the MLE for all and all parameters. Henceforth, we use to denote random vectors, and to denote the th column in the data matrix whenever there is no ambiguity.

Through Markov factorization (Lauritzen, 1996), the full log-likelihood function can be decomposed as:

Note that the summands share no common parameters, which enables us to maximize the likelihood with respect to individual parameters in the terms separately. More importantly, by conditioning Layer nodes on nodes in its previous layers, we can treat Layer nodes as the“response” layer, and all nodes in the previous layer combined as a super “parent” layer. If we ignore the structure within the bottom layer () for the moment, the -layered network can be viewed as two-layered networks, each comprising a response layer and a parent layer. Thus, the network structure in Figure 1 can be viewed as a 2 two-layered network: for the first network, Layer 3 is the response layer, while Layers 1 and 2 combined form the “parent” layer; for the second network, Layer 2 is the response layer, and Layer 1 is the “parent” layer. Therefore, the problem for estimating all coefficient matrices and precision matrices can be translated into estimating two-layered network structures with directed edges from the parent layer to the response layer, and undirected edges within the response layer, and finally estimating the undirected edges within the bottom layer separately.

Since all estimation problems boil down to estimating the structure of a 2-layered network, we focus the technical discussion on introducing our proposed methodology for a 2-layered network setting111In Appendix 5.2, we give a detail example on how our proposed method works under a 3-layered network setting.. The theoretical results obtained extend in a straightforward manner to an -layered Gaussian graphical model.

Remark 1.

For the -layer network structure, we impose certain identifiability-type condition on the largest “parent” layer (encompassing layers), so that the directed edges of the entire network are estimable. The imposed condition translates into a minimum eigenvalue-type condition on the population precision matrix within layers, and conditions on the magnitude of dependencies across layers. Intuitively, consider a three-layered network: if and are highly correlated, then the proposed (as well as any other) method will exhibit difficulties in distinguishing the effect of on from that of on . The (group) identifiability-type condition is thus imposed to obviate such circumstances. An in-depth discussion on this issue is provided in Section 3.4.

2.1 A Two-layered Network Set-up.

Consider a two-layered Gaussian graphical model with nodes in the first layer, denoted by , and nodes in the second layers, denoted by . The model is defined as follows:

-

–

.

-

–

For : , and .

The parameters of interest are: and . As with most estimation problems in the high dimensional setting, we assume these parameters to be sparse.

Now given data and , both centered, we would like to use the penalized maximum likelihood approach to obtain estimates for , and . Throughout this paper, we use , and to denote the size- realizations of the random vectors , and , respectively. Also, with a slight abuse of notation, we use and to denote the columns of the data matrix and , respectively, whenever there is no ambiguity.

The full log-likelihood can be written as

| (1) |

Note that the first term only involves and , and the second term only involves . Hence, (1) can be maximized by maximizing w.r.t. , and maximizing w.r.t. , respectively. can be obtained using traditional methods for estimating undirected graphs, e.g., the Graphical Lasso (Friedman et al., 2008) or the Nodewise Regression prcoedure (Meinshausen and Bühlmann, 2006). Therefore, the rest of this paper will mainly focus on obtaining estimates for and . In the next subsection, we introduce our estimation procedure for obtaining the MLE for and .

Remark 2.

Our proposed method is targeted towards maximizing (with proper penalization) in (1) only, which gives the estimates for across-layers dependencies between the response layer and the parent layer, as well as estimates for the conditional dependencies within the response layer each time we solve a 2-layered network estimation problem. For an -layered estimation problem, the maximization regarding occurs only when we are estimating the within-layer conditional dependencies for the bottom layer.

2.2 Estimation Algorithm.

The conditional likelihood for response given can be written as:

where , and . After writing out the Kronecker product, the log-likelihood can be written as:

Here, denotes the -th entry of . With penalization which induces sparsity, the optimization problem can be formulated as:

| (2) |

and the first term in (2) can be equivalently written as:

where is defined as the sample covariance matrix of . This gives rise to the following optimization problem:

| (3) |

where is the absulote sum of the off-diagonal entries in , and are both positive tuning parameters. This penalized log-likelihood corresponds to the objective function initially proposed in Rothman et al. (2010), and has also been examined in Lee and Liu (2012).

Note that the objective function (3) is not jointly convex in , but only convex in for fixed and in for fixed ; hence, it is bi-convex, which in turn implies that the proposed algorithm may fail to converge to the global optimum, especially in settings where , as pointed out by Lee and Liu (2012). As is the case with most non-convex problems, good initial parameters are beneficial for fast convergence of the algorithm, a fact supported by our numerical work on the present problem. Further, a good initialization is critical in establishing convergence of the algorithm for this problem (see Section 3.1). To that end, we introduce a screening step for obtaining a good initial estimate for . The theoretical justification for employing the screening step is provided in Section 3.3.

An outline of the computational procedure is presented in Algorithm 1, while the details of each step involved are discussed next.

Screening. For each variable in the response layer, regress on via the de-biased Lasso procedure proposed by Javanmard and Montanari (2014). The output consists of the -value(s) for each predictor in each regression, denoted by , with . To control the family-wise error rate of the estimates, we do a Bonferroni correction at level : define and set if the -value obtained for the ’th predictor in the ’th regression exceeds . Further, let

| (4) |

where is the collection of indices for those predictors deemed “active” for response :

Therefore, subsequent estimation of the elements of will be restricted to .

Alternating Search. In this step, we utilize the bi-convexity of the problem and estimate and by minimizing in an iterative fashion the objective function with respect to (w.r.t.) one set of parameters, while holding the other set fixed within each iteration.

As with most iterative algorithms, we need an initializer; for it corresponds to a Lasso/Ridge regression estimate with a small penalty, while for we use the Graphical Lasso procedure applied to the residuals obtained from the first stage regression. That is, for each ,

| (5) |

where is some small tuning parameter for initialization, and set . An initial estimate for is then given by solving for the following optimization problem with the graphical lasso (Friedman et al., 2008) procedure:

where is the sample covariance matrix based on .

Next we use an alternating block coordinate descent algorithm with penalization to reach a stationary point of the objective function (3):

-

–

Update as:

(6) which can be obtained by cyclic coordinate descent w.r.t each column of , that is, update each column by:

(7) where

and iterate over all columns until convergence. Here, we use to index the outer iteration while minimizing w.r.t. or , and use to index the inner iteration while cyclically minimizing w.r.t. each column of .

-

–

Update as:

(8) where is the sample covariance matrix based on .

Refitting and Stabilizing. As noted in the introduction, this step is beneficial in applications, especially when one deals with large scale multi-layer networks and relatively smaller sample sizes. Denote the solution obtained by the above iterative procedure by and . For each , set and the final estimate for is given by ordinary least squares:

| (9) |

For , we obtain the final estimate by a combination of stability selection (Meinshausen and Bühlmann, 2010) and graphical lasso (Friedman et al., 2008). That is, after obtaining the refitted residuals , based on the stability selection procedure with the graphical lasso, we obtain the stability path, or probability matrix for each edge, which records the proportion of each edge being selected based on bootstrapped samples of ’s. Then, using this probability matrix as a weight matrix, we obtain the final estimate of as follow:

| (10) |

where we use to denote the element-wise product of two matrices, and is the sample covariance matrix based on the refitted residuals . Again, (10) can be solved by the graphical lasso procedure (Friedman et al., 2008), with properly chosen.

2.3 Tuning Parameter Selection.

To select the tuning parameters , we use the Bayesian Information Criterion(BIC), which is the summation of a goodness-of-fit term (log-likelihood) and a penalty term. The explicit form of BIC (as a function of and ) in our setting is given by

where

and is the total number of nonzero entries in . Here we penalize the non-zero elements in the upper-triangular part of and the non-zero ones in

. We choose the combination over a grid of values, and should minimize the BIC evaluated at .

3 Theoretical Results

In this section, we establish a number of theoretical results for the proposed iterative algorithm. We focus the presentation on the two-layer structure, since as explained in the previous section the multi-layer estimation problem decomposes to a series of two-layer ones. As mentioned in the introduction, one key challenge for estabilishing the theoretical results comes from the fact that the objective function (3) is not jointly convex in and . Consequently, if we simply used properties of block-coordinate descent algorithms, we would not be able to provide the necessary theoretical guarantees for the estimates we obtain. On the other hand, the biconvex nature of the objective function allows us to establish convergence of the alternating algorithm to a stationary point, provided it is initialized from a point close enough to the true parameters. This can be accomplished using a Lasso-based initializer for and as previously discussed. The details of algorithmic convergence are presented in Section 3.1.

Another technical challenge is that each update in the alternating search step relies on estimated quantities –namely the regression and precision matrix parameters –rather than the raw data, whose estimation precision needs to be controlled uniformly across all iterations. The details of establishing consistency of the estimates for both fixed and random realizations are given in Section 3.2.

Next, we outline the structure of this section. In Section 3.1 Theorem 1, we show that for any fixed set of realization of and 222We actually observe and , which is given by a corresponding set of realization in and based on the model., the iterative algorithm is guaranteed to converge to a stationary point if estimates for all iterations lie in a compact ball around the true value of the parameters. In Section 3.2, we show in Theorem 4 that for any random and , with high probability, the estimates for all iterations lie in a compact ball around the true value of the parameters. Then in Section 3.3, we show that asymptotically with , while keeping the family-wise type I error under some pre-specified level, the screening step correctly identifies the true support set for each of the regressions, based upon which the iterative algorithm is provided with an initializer that is close to the true value of the parameters. Finally in Section 3.4, we provide sufficient conditions for both directed and undirected edges to be identifiable (estimable) for multi-layered network.

Throughout this section, to distinguish the estimates from the true values, we use and to denote the true values.

3.1 Convergence of the Iterative Algorithm

In this subsection, we prove that the proposed block relaxation algorithm converges to a stationary point for any fixed set of data, provided that the estimates for all iterations lie in a compact ball around the true value of the parameters. This requirement is shown to be satisfied with high probability in the next subsection 3.2.

Decompose the optimization problem in (3) as follows:

where

and is the collection of symmetric positive definite matrices. Further, denote the limit point (if there is any) of and by and , respectively.

Definition 1 (stationary point(Tseng, 2001) pp.479).

Define to be a stationary point of if and where is the coordinate block.

Definition 2 (Regularity (Tseng, 2001) pp.479).

is regular at if for all such that

Definition 3 (Coordinate-wise minimum).

Define to be a coordinate-wise minimum if

Note for our iterative algorithm, we only have two blocks, hence with the above notation, .

Remark 3.

Tseng (2001) proved that if satisfies certain conditions (Tseng, 2001, see Theorem 4.1 (a), (b) and (c) for details), the limit point given by the general block-coordinate descent algorithm (with blocks) is a stationary point of . However, in the high dimensional setting, the posited objective function does not satisfy any of the assumptions in that Theorem. Hence, for this problem, we need to employ a different strategy to prove convergence to a stationary point, and the resulting statements hold true for all problems that use a -block coordinate descent algorithm.

Since is open and is Gâteaux-differentiable on the , by Tseng (2001) Lemma 3.1, is regular in the . From the discussion on Page 479 of (Tseng, 2001), we then have:

Fact 1:

Every coordinate-wise minimum is a stationary point of .

The following theorem shows that any limit point of the iterative algorithm described in Section 2.2 is a stationary point of , as long as all the iterates are within a closed ball around the truth.

Theorem 1 (Convergence for fixed design).

Suppose for any fixed realization of and , the estimates obtained by implemeting the alternating search step satisfy the following bound:

Then any limit point of the iterative algorithm is a stationary point of .

Proof. We initialize the algorithm at . Then for all :

| (11) | |||||

| (12) |

Now, consider a limit point of the sequence . Note that such limit point exists by Bolzano-Weierstrass theorem since the sequence is bounded. Consider a subsequence such that converges to . Now for the bounded sequence , without loss of generality333switching to some further subsequence of if necessary., we can say that

By (11) it follows immediately that . Also, the following inequality holds:

Thus, by letting over , we have

since is continuous. This implies that

| (13) |

Next, since , for all , let grow along , and we obtain the following:

It then follows from (13) that

| (14) |

Finally, note that , for all . As before, let grow along and with the continuity of , we obtain:

| (15) |

Now, (14) and (15) together imply that is a coordinate-wise minimum of and by Fact 1,

also a stationary point of .

Remark 4.

Recall that in classical parametric statistics, MLE-type asymptotics are derived after establishing that with probability tending to as the sample size goes to infinity, the likelihood equation has a sequence of roots (hence stationary points of the likelihood function) that converges in probability to the true value. Any such sequence of roots is shown to be asymptotically normal and efficient. Note that such (a sequence of) roots may not be global maximizers since parametric likelihoods are not globally log-concave (see Chapter 6 Lehmann and Casella, 1998). Here we show that the obtained by the iterative algorithm is a stationary point which satisfies the first-order condition for being a maximizer of the penalized log–likelihood function (which is just the negative of the penalized least–squares function). Moreover, if we let go to infinity, converges to the true value in probability (shown in Theorem 4), and therefore behaves the same as the sequence of roots in the classical parametric problem alluded to above. Thus, while may not be the global maximizer, it can, nevertheless, to all intents and purposes, be deemed as the MLE.

Remark 5.

The above convergence result is based upon solving the optimization problem on the “entire” space, that is, we don’t restrict to live in any subspace. However, when actually implementing the proposed computational procedure, the optimization of the coordinate is restricted to (as defined in eqn.4). It should be noted that the same convergence property still holds, since for all , the following bound holds, for some :

| (16) |

Consequently, the rest of the derivation in Theorem 1 follows, leading to the convergence property. The bound in eqn (16) will be shown at the end of Section 3.2.

3.2 Estimation consistency

In this subsection, we show that given a random realization of and , with high probability, the sequence lies in a non-expanding ball around , thus satisfying the condition of Theorem 1 for convergence of the alternating algorithm.

It should be noted that for the alternating search procedure, we restrict our estimation on a subspace identified by the screening step. However, for the remaining of this subsection, the main propositions and theorems are based on the procedure without such restriction, i.e., we consider “generic” regressions on the entire space of dimension . Notwithstanding, it can be easily shown that the theoretical results for the regression parameters on a restricted domain follow easily from the generic case, as explained in Remark 9.

Before providing the details of the main theorem statements and proofs, we first introduce additional notations. Let be the vectorized version of the regression coefficient matrix. Correspondingly, we have and . Moreover, we drop the superscripts and use and to denote the generic estimators given by (17) and (18), as opposed to those obtained in any specific iteration:

| (17) | |||||

| (18) |

where

Remark 6.

As opposed to (17) and (18), if and are replaced by plugging in the true values of the parameters, the two problems in (17) and (18) become:

| (19) | |||||

| (20) |

where

In (19), we obtain using a penalized maximum likelihood regression estimate, and (20) corresponds to the generic setting for using the graphical Lasso. A key difference between the estimation problems in (17) and (18) versus those in (19) and (20) is that to obtain and we use estimated quantities rather than the raw data. This is exactly how we implement our iterative algorithm, namely, we obtain using as a surrogate for the sample covariance of the true error (which is unavailable), then estimate using the information in . This adds complication for establishing the consistency results. Original consistency results for the estimation problem in (19) and (20) are available in Basu and Michailidis (2015) and Ravikumar et al. (2011), respectively. Here we borrow ideas from corresponding theorems in those two papers, but need to tackle concentration bounds of relevant quantities with additional care. This part of the result and its proof are shown in Theorem 4.

As a road map toward our desired result established in Theorem 4, we first show in Theorem 2 that for any fixed realization of and , under a number of conditions on (or related to) and , when is small (up to a certain order), the error of is well-bounded. We then verify in Proposition 1 and 2 that for random and , the above-mentioned conditions hold with high probability. Similarly in Theorem 3, we show that for fixed realizations in and , under certain conditions (verified for random and in Proposition 3), the error of is also well-bounded, given being small. Finally in Theorem 4, we show that for random and , with high probability, the iterative algorithm gives that lies in a small ball centered at , whose radius depends on , , and the sparsity levels.

Next, for establishing the main propositions and theorems, we introduce some additional notations:

-

–

Sparsity level of : . As a reminder of the previous notation, we have .

-

–

True edge set of : , and let be its cardinality.

-

–

Hessian of the log-determinant barrier evaluated at :

-

–

Matrix infinity norm of the true error covariance matrix :

-

–

Matrix infinity norm of the Hessian restricted to the true edge set:

-

–

Maximum degree of : .

-

–

We write if there exists some absolute constant that is independent of the model parameters such that .

Definition 4 (Incoherence condition (Ravikumar et al., 2011)).

satisfies the incoherence condition if:

Definition 5 (Restricted eigenvalue (RE) condition (Loh and Wainwright, 2012)).

A symmetric matrix satisfies the RE condition with curvature and tolerance , denoted by if

Definition 6 (Diagonal dominance).

A matrix is strictly diagonally dominant if

Based on the model in Section 2.1, since we are assuming and come from zero-mean Gaussian distributions, it follows that and are zero-mean sub-Gaussian random vectors with parameters and , respectively. Moreover, thoughout this section, all results are based on the assumption that is diagnally dominant.

Remark 7.

Before moving on to the main statements of Theorem 2, we would like to point out that with a slight abuse of notation, for Theorem 2 and its related propositions and corollaries, the statements and analyses are based on equation (17) only, with any determinisitic symmetric matrix within a small ball around . Similarly in Theorem 3, Proposition 3 and Corollary 2, the analyses are based on equation ((18) only, for any given determinisitic within a small ball around . The randomness of and during the iterative procedure will be taken into consideration comprehensively in Theorem 4.

Theorem 2 (Error bound for with fixed realizations of and ).

Consider given by (17). For any fixed pair of realizations of and , assume the following:

-

A1. is a deterministic matrix satisfying the bound: where and is some constant depending only on ;

-

A2. , with ;

-

A3. satisfies the deviation bound:

where is some quantity depending on .

Then, for any , the following bound holds:

Proof.

The statement of the theorem is a variation of Proposition 4.1 in Basu and Michailidis (2015), and its proof follows directly from the proof of the

proposition in Basu and Michailidis (2015, Appendix B). We only outline how the statement differs. In the original statement of Proposition 4.1 in Basu and Michailidis (2015), the authors provide the error bound for , obtained as per (19) whose dimension is with denoting the true lag of the vector-autoregressive process, under an RE condition for and a deviation bound for . For our problem, we impose a similar RE condition on and deviation bound on , so as to yield a bound on that lies in a -dimensional space.

The following two propositions verify the RE condition for and deviation bound for hold with high probability for a random pair , given any symmetric, matrix satisfying (A1). The proofs for these two propositions are given in the Appendix.

Proposition 1 (Verification of RE condition for random and ).

Consider any deterministic matrix satisfying (A1). Let the sample size satisfy . With probability at least for some constant , satisfies the following RE condition:

where , , and is defined as:

where ’s denote the entries in hence is the gap between its diagonal entry and the sum of off-diagonal entries for row .

Proposition 2 (Deviation bound for for random and ).

Consider any deterministic matrix satisfying (A1). Let sample size satisfy . With probability at least

the following bound holds:

where

| (21) |

Remark 8.

In Proposition 1, the quantity that shows up in the sample size requirement is a result of , which is the common order of error in a generic graphical Lasso problem. Hence here we explicitly list it for the purpose of showing results for the generic graphical Lasso estimation problem. In our iterative algorithm, the order of depends on the relative order of and , which may potentially make the sample size requirement more stringent. This will be discussed in more detail in the proof of Theorem 4.

Given the results in Theorem 2, Proposition 1 and Proposition 2, next we provide Corollary 1, which gives the error bound for for random realizations of and . Its proof is given in the Appendix.

Corollary 1 (Error Bound for for random and ).

Consider any determinisitic satisfying the following elementwise -bound:

with . Then for sample size and for any regularization parameter with the expression of given in (21), there exists and such that with probability at least:

the following bound holds:

| (22) |

where .

Theorem 3 (Error bound for for fixed realizations of and ).

Consider given by (18). For any fixed pair of realization , assume the following:

-

B1. is a deterministic vector satisfying , where , with being some constant depending only on ;

-

B2. where

and is some quantity depending on ;

-

B3. Incoherence condition holds for .

Then, for and sample size satisfying , the following error bound for holds:

| (23) |

where is the incoherence parameter as defiend in Definition 4.

Proof. The statement of this theorem is a variation of Theorem 1 in Ravikumar et al. (2011), so here, instead of providing a complete proof of the theorem, we only outline how the estimation problem differs in our setting, as well as the required changes in its proof.

In Ravikumar et al. (2011), the authors consider the optimization problem in (20), and show that for a random realization, with certain sample size requirement and choice of the regularization parameter, the following bound for holds with probability at least for some :

| (24) |

where is defined as:

| (25) |

The quantity that shows up in expression (24) is the bound for . In particular, in Lemma 8 (Ravikumar et al., 2011), they show that with probability at least , , the following bound holds:

In our optimization problem (18), we are using instead of , hence a bound for is necessary, and the remaining argument in the proof of Theorem 1 (Ravikumar et al., 2011) will follow through.

Therefore in our theorem statement, we use as a bound for then yield the bound for , since we are using the surrogate error in the estimation, instead of the true error .

Proposition 3 gives an explicit expression for under condition (B1). Specifically, it shows how well concentrates around for random and , given some small-errored (or , equivalently), and its proof is given in the appendix.

Proposition 3.

Given Theorem 3 and Proposition 3, we provide Corollary 2, which gives the error bound for for random realizations of and :

Corollary 2 (Error bound for for random and ).

Consider any deterministic satisfying the following bound:

with . Also suppose the incoherence condition (B3) is satisfied. Then, for sample size and regularization parameter with given in (27), with probability at least

the following bound holds:

After providing the error bound for (17) and (18), in Theorem 4 we establish that with high probability, the error of the sequence of estimates obtained in the alternating search step of the algorithm described in Section 2.2 is uniformly bounded; that is, the sequence of estimates lie in a non-expanding ball around the true value of the parameters uniformly with a radius that doesn’t depend on , the iteration number.

Theorem 4 (Error bound for and ).

Consider the iterative algorithm given in Section 2.2 that gives rise to sequences of and alternately. For random realization of and , we assume the following:

-

C1. The incoherence condition holds for .

-

C2. is diagonally dominant.

-

C3. The maximum sparsity level for all regression satisfies .

(I) For sample size satisfying , there exist constants such that for any

with probability at least , the initial estimate satisfies the following bound:

| (28) |

where . Moreover, by choosing where the expression for is given in (27), with probability at least

the following bound holds:

| (29) |

(II) For sample size satisfying , for any iteration , with probability at least

the following bounds hold for all and :

where is the sparsity of , and are constants depending only on and , respectively.

Proof. We first consider part (I) of the theorem. Note that by (5), can be equivalently written as:

| (30) |

where

Consider the following events:

-

E1.

,

-

E2.

.

Note that E1 E2 implies the following events:

and

| (31) |

Hence, by Proposition 4.1 of Basu and Michailidis (2015), the bound (28) holds on E1 E2.

By Lemmas 1 and 2, is at least , for some . By Lemma 3, is at least for some , . Hence, with probability at least

the bound in (28) holds, which proves the first part of (I). In particular, we have on .

To prove the second part of (I), note that by Theorem 3 the bound in (29) holds when B1-B3 are satisfied. Now, from the argument above, B1 holds on the event E1 E2. Also, from the proof of Proposition 3, B2 is satisfied, i.e.,

| (32) |

on E1 E2 E3 E4, where the events E3 and E4 are given by:

-

E3.

for some and that depends on ,

-

E4.

for some and that depends on .

Therefore, the probability of the bound for in (29) to hold is at least

| (33) |

By Lemma 2, Lemma 3 and the proof of Proposition 3, the probability in (33) is lower bounded by:

Consider the following two cases where the relative order of and differ. Case 1: , then ; case 2: , then . In either case, since we are assuming to be a small quantity and it follows that , the following bound always holds:

where is some large fixed constant that bounds the constant terms in front of .

Now we consider part (II) of the theorem. Note that for each , and are obtained via solving the following two optimizations:

| (34) | |||||

| (35) |

where

Consider the bound on for . The argument is similar to that of , with appropriate modifications to account for the fact that the objective function now involves log likelihood instead of least squares. Formally, we consider the event E1 E2 E3 E4 E5, where

-

E5.

.

Note that holds on this event. By Lemma 3, . Combining this with the lower bound on (33) and the sample size requirement (note this sample size requirement can be relaxed to if ), we obtain that with probability at least

the following three events hold simultaneously:

-

A1’ ;

-

A2’ where

-

A3’ with the expression for given in (21).

By Theorem 2, by choosing , the following bound holds:

| (36) |

The error bound for can now be established using the same argument for , with the only difference that now we consider the event instead of and use (36) instead of (28).

Note that an upper bound for the leading term of the right hand side of (36) is at most of the order , and can be written as:

with being some potentially large number that bounds the constant term. Notice that is of the same order as ; thus, for , we can also achieve the following bound:

with high probability since we are assuming to be some potentially large number.

Note that the events rely only on the parameters and not on the estimated quantities, and on their intersection we have uniform upper bounds on the errors of and for . Hence the error bounds for can be used to invoke Theorems 2 and 3 inductively on realizations and from the set to provide high probability error bounds for all subsequent iterates as well. This leads to the uniform error bounds of part (II) with the desired probability.

As a direct result of Proposition 1 in Basu and Michailidis (2015) and Corollary 3 in Ravikumar et al. (2011), the following bound also holds:

Corollary 3.

Under the same set of conditions C1, C2 and C3 in Theorem 4, there exists , and constants and such that for all iterations , the following bound holds:

with probability at least

where and are the sparsity for and , respectively.

Remark 9.

As mentioned earlier in this subsection, the actual implementation of the alternating search step is restricted to a subspace of . Next, we outline the corresponding theoretical results for this specific scenario in which for each regression , some fixed superset of the indices of true covariates is given, and the regressions are restricted to these supersets, respectively. Note that we need to make sure that the restricted subspace contains all the true covariates for the results below to be valid.

Let denote the given fixed superset for each regression , and we consider regressing the response on . We use to denote the corresponding vectorized estimator of iteration , that is,

where is obtained by doing the regression in (7), however with the indices of covariates restricted to . Also, we let be the corresponding true value of . Note that always holds that

Now let

and let be its cardinality. It can be shown that the best achievable error bound for is identical to , where is obtained by considering covariates for all regressions, instead of the entire . For this specific reason, formally, we state the theoretical results for the case where we consider regressing on , which is almost identical to the generic case.

Suppose conditions C1, C2 and C3 in Theorem 4 hold, then there exists constants such that: (I) for sample size satisfying , w.p. at least , for any

the initial estimate satisfies the following bound:

where . Moreover, by choosing where the expression for is given in (27), with probability at least

the following bound holds:

(II) For sample size satisfying , for any iteration , with probability at least

the following bound hold for all and :

where is the sparsity of , , , and are all constants that do not depend on .

3.3 Family-Wise Error Rate control of the Screening Step

As mentioned in the Introduction, for the iterative algorithm to work effectively, it is crucial to initialize from points that are close to the true parameters. Our screening step provides such guarantees asymptotically. Based on the screening step described in Section 2.2, initial esimates for each column of the regression matrix are obtained by Lasso or Ridge regression with the support set restricted to the one identified by the screening step. It is desirable for the screening step to correctly identify the true support set. In particular, we would like to retain as many true positive predictor variables as possible without discovering too many false positive ones. The following theorem states that as long as and the sparsity is not beyond a specified level, the screening step will be able to recover all true positive predictors, while keeping the family-wise type I error under control.

Theorem 5.

Let denote the true support set of the th regression and be its cardinality. Suppose that and the following condition for sparsity holds:

Then, the screening step described in Section 2.2 will correctly recover for all with probability approaching to 1, while keeping the family-wise type I error rate under the prespecified level .

Proof. First, we note that with a Bonferroni correction, the family-wise type I error will be automatically controlled at level . Hence, we will focus on the power of the screening step. Also, from Theorem 7 of Javanmard and Montanari (2014), it is easy to see that all the arguments below hold for a large set of random realizations of , whose probability approaches 1 under the specified asymptotic regime when the eigenvalues of are bounded away from and infinity.

Let denote the true value of the regression coefficients and denote the estimates given by the de-biased Lasso procedure in Javanmard and Montanari (2014). With the given level for sparsity, by Theorem 8 in Javanmard and Montanari (2014), each satisfies the following:

where is the sample covariance matrix of the predictors , is the population noise level of the error term , and is the matrix corresponding to the th regression, produced by the procedure described in Javanmard and Montanari (2014)444Details of the procedure is described in p.2871 in Javanmard and Montanari (2014), with being an intermediate quantity obtained by solving an optimization problem.. Let denote the th coordinate of the th regression coefficient vector and be the covariance matrix of the estimator , then

and in particular, the variance of is . Using these notations, for a prespecified level , the test statistics for testing vs. , for all can be equivalently written as:

where denotes the upper quantiles of .

Define the “family-wise” power as follows:

Correspondingly, the family-wise type II error can be written as:

| (37) |

By Theorem 16 in Javanmard and Montanari (2014), asymptotically, :

| (38) |

Here

where we use to denote the random variable following a standard Gaussian distribution. Hence, (38) can be re-written as:

| (39) |

where we use to denote the random variable following a standard Gaussian distribution.

Note that the following inequality holds for standard Normal percentiles:

and by taking the inverse function, the following inequality holds:

Letting , it follows that:

hence

Now given

the following expression follows:

indicating that asymptotically, . On the other hand, using the fact that , the last expression in (39) can be bounded by:

Now with and the given sparsity level, that is, , it follows that:

i.e.,

Combining with (37), we have:

This is equivalent to establishing that, given , the screening step recovers the true support sets for all with high probability, while keeping the family-wise type I error rate under control.

Remark 10.

The specified level for sparsity is necessary for the de-biased Lasso procedure in Javanmard and Montanari (2014) to produce unbiased estimates for the regression coefficients. In terms of support recovery for the screening step, with , we only require , which is much weaker and easily satisfied.

The following corollary connects the screening step with the alternating search step, under the discussed asymptotic regime :

Corollary 4.

Consider the model set-up given in Section 2.1. Let denote the maximum sparsity for all , and denote the maximum degree of . Also, let denote the sparsity for and denote the sparsity for . Assume there exist positive constants satisfying:

such that

As ,

and for all iterations :

The proof of this corollary follows along the same lines as Theorem 4, and we leave the details to the reader.

3.4 Estimation Error and Identifiability

In this subsection, we discuss in detail the conditions needed for the parameters in our multi-layered network to be identifiable (estimable). We focus the presentation for ease of exposition on a three-layer network and then discuss the general -layer case.

Consider a -layer graphical model. Let be the dimensional random variable, which represents the “super”-layer on which we regress to estimate , and . As shown in Theorem 2, the estimation error for takes the following form:

where is the curvature parameter for RE condition that scales with (see Proposition 1). Therefore, the error of estimating these regression parameters is higher when is smaller. In this section, we derive a lower bound on this quantity to demonstrate how the estimation error depends on the underlying structure of the graph.

For the undirected subgraph within a layer , we denote its maximum node capacity by . For the directed bipartite subgraph consisting of Layer edges (), we similarly define the maximum incoming and outgoing node capacities by and . The following proposition establishes the lower bound in terms of these node capacities

Proposition 4.

Proof. From the structural equations of a multi-layered graph introduced in Section 2.1, and setting , we can write

| (40) |

Define . Then, is a centered Gaussian random vector with a block diagonal variance-covariance matrix . Hence, the concentration matrix of takes the form

This leads to an upper bound

The result then follows by using the matrix norm inequality (Golub and Van Loan, 2012), where and denote the maximum absolute row and column sums of , and the fact that .

The three components in the lower bound demonstrate how the structure of Layers 1 and 2 impact the accurate estimation of directed edges to Layer 3. Essentially, the bound suggests that accurate estimation is possible when the total effect (incoming and outgoing edges) at every node of each of the three subgraphs is not very large.

This is inherently related to the identifiability of the multi-layered graphical models and our ability to distinguish between the parents from different layers. For instance, if a node in Layer has high partial correlation with nodes of Layer , i.e., a node in Layer 2 has parents from many nodes in Layer 1 and yields a large ; or similarly, a node in Layer is the parent of many nodes in Layer , yielding a large . In either case, we end up with some large lower bound for and it can be hard to distinguish Layer edges from Layer edges.

For a general -layer network, the argument in the proof of Proposition 4 can be genaralized in a straightforward manner, with a modified of the form

and combining node capacities for different layers. The conclusion is qualitatively similar, i.e., the estimation error of a -layer graphical model is small as long as the maximum node capacities of different inter-layer and intra-layer subgraphs are not too large.

4 Performance Evaluation and Implementation Issues

In this section, we present selected simulation results for our proposed method, in two-layer and three-layer network settings. Further, we introduce some acceleration techniques that can speed up the algorithm and reduce computing time.

4.1 Simulation Results

For the 2-layer network, as mentioned in Section 2.1, since the main target of our proposed algorithm is to provide estimates for and (since can be estimated separately), we only present evaluation results for and estimates. Similarly, for the three-layer network, we only present evaluation results involving Layer 3, using the notation in Section 3.4, that is, and estimates, which is sufficient to show how our proposed algorithm works in the presence of a “super” - layer, taking advantange of the separability of the log-likelihood.

2-layered Network. To compare the proposed method with the most recent methodology that also provides estimates for the regression parameters and the preccision matrix (CAPME, Cai et al. (2012)), we use the exact same model settings that have been used in that paper. Specifically, we consider the following two models:

-

•

Model A: Each entry in is nonzero with probability , and off-diagonal entries for are nonzero with probability .

-

•

Model B: Each entry in is nonzero with probability , and off-diagonal entries for are nonzero with probability .

As in Cai et al. (2012), for both models, nonzero entries of and are generated from , and diagonals of are set identical such that the condition number of is .

| Model A | |

|---|---|

| Model B | |

To evaluate the selection performance of the algorithm, we use sensitivity (SEN), specificity (SPE) and Mathews Correlation Coefficient (MCC) as criteria:

Further, to evaluate the accuracy of the magnitude of the estimates, we use the relative error in Frobenius norm:

Tables 3 and 3 show the results for both the regression matrix and the precision matrix. For the precision matrix estimation, we compare our result with those available in Cai et al. (2012), denoted as CAPME.

| SEN | SPE | MCC | rel-Fnorm | ||

| Model A | (30,60,100) | 0.96(0.018) | 0.99(0.004) | 0.93(0.014) | 0.22(0.029) |

| (60,30,100) | 0.99(0.009) | 0.99(0.003) | 0.93(0.017) | 0.18(0.021) | |

| (200,200,150) | 0.99(0.001) | 0.99(0.001) | 0.88(0.009) | 0.18(.007) | |

| (300,300,150) | 1.00(0.001) | 0.99(0.001) | 0.84(0.010) | 0.21(0.007) | |

| Model B | (200,200,200) | 0.970(0.004) | 0.982(0.001) | 0.927(0.002) | 0.194 (0.009) |

| (200,200,100) | 0.32(0.010) | 0.99(0.001) | 0.49(0.009) | 0.85(0.006) |

| SEN | SPE | MCC | rel-Fnorm | |||

|---|---|---|---|---|---|---|

| Model A | (30,60,100) | 0.77(0.031) | 0.92(0.007) | 0.56(0.030) | 0.51(0.017) | |

| CAPME | 0.58(0.03) | 0.89(0.01) | 0.45(0.03) | |||

| (60,30,100) | 0.76(0.041) | 0.89(0.015) | 0.59(0.039) | 0.49(0.014) | ||

| (200,200,150) | 0.78(0.019) | 0.97(0.001) | 0.55(0.012) | 0.60(0.007) | ||

| (300,300,150) | 0.71(0.017) | 0.98(0.001) | 0.51(0.011) | 0.59(0.005) | ||

| Model B | (200,200,200) | 0.73(0.023) | 0.94(0.003) | 0.39(0.017) | 0.62(0.011) | |

| CAPME | 0.36(0.02) | 0.97(0.00) | 0.35(0.01) | |||

| (200,200,100) | 0.57(0.027) | 0.44(0.007) | 0.04(0.008) | 0.84(0.002) | ||

| CAPME | 0.19(0.01) | 0.87(0.00) | 0.04(0.01) |

As it can be seen from Tables 3 and 3, the sample size is a key factor that affects the performance. Our proposed algorithm performs extremely well in its selection properties on and strikes a good balance between sensitivity and specificity in estimating 555We suggest using as the FWER thresholding level. For tuning parameter selection, we suggest doing a grid search for on with BIC.. For most settings, it provides substantial improvements over the CAPME estimator.

3-layer Network. For a 3-layer network, we consider the following data generation mechanism: for all three models A, B and C, each entry in is nonzero with probability , each entry in and is nonzero with probability , and off-diagonal entries in are nonzero with probability . Similar to the 2-layered set-up, the nonzero entries in are generated from with its diagnals set identical such that its condition number is . For the regression matrices in the three models, nonzeros in are generated from , and nonzeros in and are generated from , where the signal strength in the three models are given by 1, 1.5 and 2, respectively. More specifically, for Model A, B and C, nonzeros in or are generated from , and , respectively.

| Layer 3 Signal.Strength | ||

|---|---|---|

| Model A | (50,50,50,200) | |

| Model B | (50,50,50,200) | |

| Model C | (50,50,50,200) | |

| (20,80,50,200) | ||

| (80,20,50,200) | ||

| (100,100,100,200) |

As mentioned in the beginning of this subsection, we only evaluate the algorithm’s performance on and .

| SEN | SPE | MCC | rel-Fnorm | ||

|---|---|---|---|---|---|

| Model A | (50,50,50,200) | 0.51(0.065) | 0.99(0.001) | 0.69(0.049) | 0.68(0.050) |

| Model B | (50,50,50,200) | 0.85(0.043) | 0.99(0.001) | 0.898(0.025) | 0.36(0.056) |

| Model C | (50,50,50,200) | 0.97(0.018) | 0.99(0.002) | 0.96(0.016) | 0.16(0.040) |

| (20,80,50,200) | 0.55(0.078) | 0.99(0.001) | 0.72(0.059) | 0.63(0.066) | |

| (80,20,50,200) | 0.99(0.006) | 0.99(0.002) | 0.94(0.017) | 0.076(0.032) | |

| (100,100,100,200) | 1.00(0.001) | 0.99(0.001) | 0.87(0.016) | 0.07(0.007) |

| SEN | SPE | MCC | rel-Fnorm | ||

|---|---|---|---|---|---|

| Model A | (50,50,50,200) | 0.53(0.051) | 1.00(0.000) | 0.72(0.036) | 0.65(0.041) |

| Model B | (50,50,50,200) | 0.90(0.033) | 1.00(0.000) | 0.95(0.019) | 0.25(0.049) |

| Model C | (50,50,50,200) | 0.98(0.013) | 1.00(0.000) | 0.99(0.007) | 0.12(0.042) |

| (20,80,50,200) | 0.95(0.013) | 1.00(0.000) | 0.98(0.007) | 0.19(0.030) | |

| (80,20,50,200) | 0.96(0.027) | 0.99(0.001) | 0.97(0.022) | 0.14(0.063) | |

| (100,100,100,200) | 1.00(0.000) | 1.00(0.000) | 0.99(0.002) | 0.025(0.002) |

| SEN | SPE | MCC | rel-Fnorm | ||

|---|---|---|---|---|---|

| Model A | (50,50,50,200) | 0.69(0.044) | 0.638(0.032) | 0.20(0.036) | 0.82(0.017) |

| Model B | (50,50,50,200) | 0.77(0.050) | 0.82(0.036) | 0.42(0.071) | 0.68(0.040) |

| Model C | (50,50,50,200) | 0.88(0.041) | 0.91(0.019) | 0.63(0.059) | 0.56(0.034) |

| (20,80,50,200) | 0.72(0.041) | 0.80(0.028) | 0.36(0.050) | 0.72(0.021) | |

| (80,20,50,200) | 0.90(0.028) | 0.92(0.011) | 0.68(0.039) | 0.58(0.018) | |

| (100,100,100,200) | 0.96(0.014) | 0.96(0.003) | 0.68(0.016) | 0.049(0.010) |

Based on the results shown in Tables 7, 7 and 7, the signal strength across layers affects the accuracy of the estimation, which is in accordance with what has been discussed regarding identifiability. Overall, the MLE estimator performs satisfactorily across a fairly wide range of settings and in many cases achieving very high values for the MCC criterion.

4.1.1 Simulation Results for non-Gaussian data

In many applications, the data may not be exactly Gaussian, but approximately Gaussian. Next, we present selected simulation results when the data comes from some distribution that deviates from Gaussian. Specifically, we consider two types of deviations based on the following transformations: (i) a truncated empirical cumulative distribution function and (ii) a shrunken empirical cumulative distribution functions as discussed in Zhao et al. (2015). In both simulation settings, we consider Model A with under the two-layer setting, and the transformation is applied to errors in Layer 2. Table 8 shows the simulation results for these two scenarios over 50 replications.

| Setting | Parameter | SEN | SPE | MCC | rel-Fnorm |

|---|---|---|---|---|---|

| Model A | 0.96(0.017) | 0.99(0.003) | 0.94(0.012) | 0.20(0.028) | |

| shrunken | 0.76(0.031) | 0.91(0.008) | 0.55(0.030) | 0.51(0.019) | |

| Model A | 0.96(0.021) | 0.98(0.004) | 0.93(0.015) | 0.21(0.034) | |

| truncation | 0.76(0.033) | 0.92(0.008) | 0.56(0.035) | 0.52(0.023) |

Based on the results in Table 8, relatively small deviatiosn from the Gaussian distribution does not affect the performace of the MLE estimates under the examined settings that are comparable to those obtained with Gaussian distributed data.

4.2 A comparison with the two-step estimator in Cai et al. (2012)

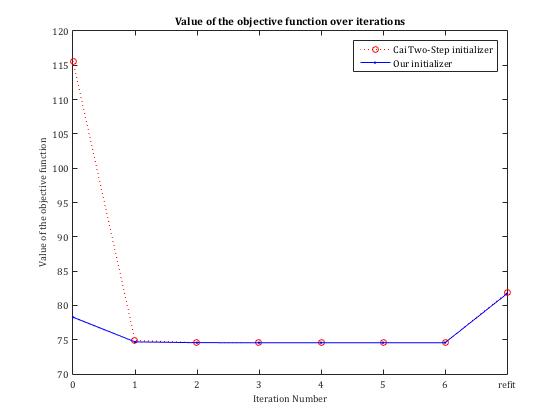

Next, we present a comparison between the MLE estimator and the two-step estimator of Cai et al. (2012). Specifically, we use the CAPME estimate as an initializer for the MLE procedure and examine its evolution over successive iterations. We evaluate the value of the objective function at each iteration, and also compare it to the value of the objective function evaluated at our initializer (screening Lasso/Ridge) and the estimates afterwards. For illustration purposes, we only show the results for a single relaization under Model A with , although similar results were obtained in other simulation settings. Figure 2 shows the value of the objective function as a function of the iteration under both initialization procedures, while Table 9 shows how the cardinality of the estimates changes over iterations for both initializers. It can be seen that the iterative MLE algorithm significantly improves the value of the objective function over the CAPME initialization and also that the set of directed and undirected edges stabilizes after a couple iterations.

| 0 | 1 | 2 | 3 | 4 | 5 | 6 | refit | ||

|---|---|---|---|---|---|---|---|---|---|

| Our initializer | 275 | 275 | 275 | 275 | 275 | 275 | 275 | 275 | |

| 282 | 255 | 247 | 247 | 248 | 248 | 248 | 260 | ||

| CAPME initializer | 433 | 275 | 275 | 275 | 275 | 275 | 275 | 275 | |

| 979 | 267 | 250 | 249 | 249 | 248 | 248 | 260 |

Based on Figure 2 and Table 9, we notice that Cai et. al’s two-step estimator yields larger value of the objective function compared with our initializer that is obtained through screening followed by Lasso. However, over subsequent iterations, both initializers yield the same value in the objective function, which keeps decreasing according to the nature of block-coordinate descent.

4.3 Implementation issues

Next, we introduce some acceleration techniques for the MLE algorithm aiming to reduce computing time, yet maintaining estimation accuracy over iterations.

-block update. In Section 2, we update and by (6) and (8), respectively, and within each iteration, the updated is obtained by an application of cyclic -block coordinate descent with respect to each of its columns until convergence. As shown in Section 3.1, the outer 2-block update guarantees the MLE iterative algorithm to converge to a stationary point. However in practice, we can speed up the algorithm by updating without waiting for it to reach the minimizer for every iteration other than the first one. More precisely, for the alternating search step, we take the following steps when actually implementing the proposed algorithm with initializer and :

-

–

Iteration 1: update and as follows, respectively:

and

where is the sample covariance matrix of .

-

–

For iteration , while not converged:

-

For , update once by:

where

(41) -

Update by:

where is defined similarly.

-

Intuitively, for the first iteration, we wait for the algorithm to complete the whole cyclic block-coordinate descent step, as the first iteration usually achieves a big improvement in the value of the objective function compared to the initialization values, as depicted in Figure 2.

However, in subsequent iterations, the changes in the objective function become relatively small, so we do successive block-updates in every iteration, and start to update once a full block update in is completed, instead of waiting for the update in proceeds cyclically until convergence. In practice, this way of updating and leads to faster convergence in terms of total computing time, yet yields the same estimates compared with the exact -block update shown in Section 2.

Parallelization. A number of steps of the MLE algorithm is parallelizable. In the screening step, when applying the de-biased Lasso procedure (Javanmard and Montanari, 2014) to obtain the -values, we need to implement separate regressions, which can be distributed to different compute nodes and carried out in parallel. So does the refitting step, in which we refit each column in in parallel.

Moreover, according to Bradley et al. (2011); Richtárik and Takáč (2012); Scherrer et al. (2012) and a series of similar studies, though the block update in the alternating search step is supposed to be carried out sequentially, we can implement the update in parallel to speed up convergence, yet empirically yield identical estimates. This parallelization can be applied to either the minimization with respect to within the 2-block update method, or the minimization with respect to each column of for the -block update method. Either way, in (41) is substituted by

which is not updated until we have updated ’s once for all in parallel.

The table below shows the elapsed time for carrying out our proposed algorithm using 2-block/ -block update with/without parallelization, under the simulation setting where we have . The screening step and refitting step are both carried out in parallel for all four different implementations666For parallelization, we distribute the computation on 8 cores..

| 2-block | -block | 2-block in parallel | -block in parallel | |

|---|---|---|---|---|

| elasped time (sec) | 5074 | 2556 | 848 | 763 |

As shown in the table, using -block update and parallelization both can speed up convergence and reduce computing time, which takes only 1/7 of the computing time compared with using 2-block update without parallelization.

Remark 11.

The total computing time depends largely on the number of bootstrapped samples we choose for the stability selection step. For the above displayed results, we used 50 bootstrapped samples to obtain the weight matrix. Nevertheless, one can select the number of bootstrap samples judiciously and reduce them if performance would not be seriously impacted.

References

- Andersson et al. (2001) Steen A Andersson, David Madigan, and Michael D Perlman. Alternative markov properties for chain graphs. Scandinavian journal of statistics, 28(1):33–85, 2001.

- Basu and Michailidis (2015) Sumanta Basu and George Michailidis. Regularized estimation in sparse high-dimensional time series models. Annals of Statistics, 43(4):1535––1567, 2015.

- Bradley et al. (2011) Joseph K Bradley, Aapo Kyrola, Danny Bickson, and Carlos Guestrin. Parallel coordinate descent for l1-regularized loss minimization. arXiv preprint arXiv:1105.5379, 2011.

- Bühlmann and Van De Geer (2011) Peter Bühlmann and Sara Van De Geer. Statistics for high-dimensional data: methods, theory and applications. Springer Science & Business Media, 2011.

- Cai et al. (2012) T Tony Cai, Hongzhe Li, Weidong Liu, and Jichun Xie. Covariate-adjusted precision matrix estimation with an application in genetical genomics. Biometrika, page ass058, 2012.

- Cai et al. (2011) Tony Cai, Weidong Liu, and Xi Luo. A constrained minimization approach to sparse precision matrix estimation. Journal of the American Statistical Association, 106(494):594–607, 2011.

- Candes and Tao (2007) Emmanuel Candes and Terence Tao. The dantzig selector: statistical estimation when p is much larger than n. Annals of Statistics, pages 2313–2351, 2007.

- Drton and Perlman (2008) Mathias Drton and Michael D Perlman. A sinful approach to gaussian graphical model selection. Journal of Statistical Planning and Inference, 138(4):1179–1200, 2008.

- Friedman et al. (2008) Jerome Friedman, Trevor Hastie, and Robert Tibshirani. Sparse inverse covariance estimation with the graphical lasso. Biostatistics, 9(3):432–441, 2008.

- Frydenberg (1990) Morten Frydenberg. The chain graph markov property. Scandinavian Journal of Statistics, pages 333–353, 1990.

- Golub and Van Loan (2012) Gene H Golub and Charles F Van Loan. Matrix computations, volume 3. JHU Press, 2012.

- Javanmard and Montanari (2014) Adel Javanmard and Andrea Montanari. Confidence intervals and hypothesis testing for high-dimensional regression. Journal of Machine Learning Research, 15(1):2869–2909, 2014.

- Lauritzen (1996) Steffen L Lauritzen. Graphical models. Oxford University Press, 1996.

- Lauritzen and Wermuth (1989) Steffen L Lauritzen and Nanny Wermuth. Graphical models for associations between variables, some of which are qualitative and some quantitative. The Annals of Statistics, pages 31–57, 1989.

- Lee and Liu (2012) Wonyul Lee and Yufeng Liu. Simultaneous multiple response regression and inverse covariance matrix estimation via penalized gaussian maximum likelihood. Journal of multivariate analysis, 111:241–255, 2012.

- Lehmann and Casella (1998) Erich Leo Lehmann and George Casella. Theory of point estimation, volume 31. Springer Science & Business Media, 1998.

- Loh and Wainwright (2012) Po-Ling Loh and Martin J Wainwright. High-dimensional regression with noisy and missing data: provable guarantees with nonconvexity. Annals of Statistics, 40(3):1637–1664, 2012.

- Meinshausen and Bühlmann (2006) Nicolai Meinshausen and Peter Bühlmann. High-dimensional graphs and variable selection with the lasso. Annals of Statistics, pages 1436–1462, 2006.

- Meinshausen and Bühlmann (2010) Nicolai Meinshausen and Peter Bühlmann. Stability selection. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 72(4):417–473, 2010.

- Ravikumar et al. (2011) Pradeep Ravikumar, Martin J Wainwright, Garvesh Raskutti, Bin Yu, et al. High-dimensional covariance estimation by minimizing ℓ1-penalized log-determinant divergence. Electronic Journal of Statistics, 5:935–980, 2011.

- Richtárik and Takáč (2012) Peter Richtárik and Martin Takáč. Parallel coordinate descent methods for big data optimization. Mathematical Programming, pages 1–52, 2012.

- Rothman et al. (2010) Adam J Rothman, Elizaveta Levina, and Ji Zhu. Sparse multivariate regression with covariance estimation. Journal of Computational and Graphical Statistics, 19(4):947–962, 2010.

- Sachs et al. (2005) Karen Sachs, Omar Perez, Dana Pe’er, Douglas A Lauffenburger, and Garry P Nolan. Causal protein-signaling networks derived from multiparameter single-cell data. Science, 308(5721):523–529, 2005.

- Scherrer et al. (2012) Chad Scherrer, Mahantesh Halappanavar, Ambuj Tewari, and David Haglin. Scaling up coordinate descent algorithms for large l1 regularization problems. arXiv preprint arXiv:1206.6409, 2012.

- Sobel (2000) Michael E Sobel. Causal inference in the social sciences. Journal of the American Statistical Association, 95(450):647–651, 2000.

- Tseng (2001) Paul Tseng. Convergence of a block coordinate descent method for nondifferentiable minimization. Journal of optimization theory and applications, 109(3):475–494, 2001.

- Van de Geer et al. (2014) Sara Van de Geer, Peter Bühlmann, Ya’acov Ritov, Ruben Dezeure, et al. On asymptotically optimal confidence regions and tests for high-dimensional models. Annals of Statistics, 42(3):1166–1202, 2014.

- Wang et al. (2007) Chao Wang, Venu Satuluri, and Srinivasan Parthasarathy. Local probabilistic models for link prediction. In Data Mining, 2007. ICDM 2007. Seventh IEEE International Conference on, pages 322–331. IEEE, 2007.

- Yang et al. (2014) Eunho Yang, Yulia Baker, Pradeep Ravikumar, Genevera Allen, and Zhandong Liu. Mixed graphical models via exponential families. In Proceedings of the Seventeenth International Conference on Artificial Intelligence and Statistics, pages 1042–1050, 2014.

- Zhang and Zhang (2014) Cun-Hui Zhang and Stephanie S Zhang. Confidence intervals for low dimensional parameters in high dimensional linear models. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 76(1):217–242, 2014.

- Zhao et al. (2015) Tuo Zhao, Xingguo Li, Han Liu, Kathryn Roeder, John Lafferty, and Larry Wasserman. huge: High-Dimensional Undirected Graph Estimation, 2015. URL http://CRAN.R-project.org/package=huge. R package version 1.2.7.

5 Appendix

5.1 Proofs for Propositions and Auxillary Lemmas

To prove Proposition 1, we need the following two lemmas. Lemma 1 was originally provided as Lemma B.1 in Basu and Michailidis (2015), which states that if the sample covariance matrix of satisfies the RE condition and is diagonally dominant, then also satisfies the RE condition. Here we omit its proof and only state the main result. Lemma 2 verifies that with high probability, the sample covariance matrix of the design matrix satisfies the RE condition.

Lemma 1.

If , and is diagonally dominant, that is, for all , where is the th entry in , then

Lemma 2.

With probability at least , for a zero-mean sub-Gaussian random design matrix , its sample covariance matrix satisfies the RE condition with parameter and , i.e.,

| (42) |

where , , .

Proof. To prove this lemma, we first use Lemma 15 in Loh and Wainwright (2012), which states that if is zero-mean sub-Gaussian with parameter , then there exists a universal constant such that

| (43) |

where is a set of sparse vectors, defined as:

By taking , with probability at least for some , the following bound holds:

| (44) |

Then applying supplementary Lemma 13 in Loh and Wainwright (2012), for an estimator of satisfying the deviation condition in (44), the following RE condition holds:

Finally, set , then with probability at least , with , .

With the above two lemmas, we are ready to prove Proposition 1.

Proof.[Proof of Proposition 1] We first show that if is diagonally dominant, then is also diagonally dominant provided that the error of is of the given order and is sufficiently large. Define

where is the th entry of , then is the gap between the diagonal entry and the off-diagonal entries of row in matrix . We can decompose into the following:

Recall that we define as . Hence

| (45) |

Now given , with , , and it follows that

Now by Lemma 2, with high probability. Combine with Lemma 1 and inequality (45), with probability at least for some , satisfies the following RE condition:

| (46) |

where , .

Lemma 3.

Let be a zero-mean sub-Gaussian matrix with parameter and be a zero-mean sub-Gaussian matrix with parameters . Moreover, and are independent. Let , then if , the following two expressions hold with probability at least for some , respectively:

| (47) |

and

| (48) |

Proof. The proof of this lemma uses Lemma 14 in Loh and Wainwright (2012), in which they show that if is a zero-mean sub-Gaussian matrix with parameters and is a zero-mean sub-Gaussian matrix with parameters , then if ,

where and are the th row of and , respectively.

Here, we replace by , and since and are independent, . Let , we get:

Note that the sub-Gaussian parameter satisfies . This directly gives the bound in (47).

To obtain the bound in (48), we note that if is sub-Gaussian with parameters , then is sub-Gaussian with parameter , where

Then we replace by and yield the bound in (48).

As a remark, here we note that the event in (47) and (48) may not be independent. However, the two events hold simultaneously with probability at least , with this crude bound for probability hold for sure.

Now we are ready to prove Proposition 2.

Proof.[Proof of Proposition 2] First we note that

which directly gives the following inequality:

| (49) |

Now we would like to bound the two terms separately.

For the second term, first we note that

| (50) |

where we have and , and the inequality comes from the fact that . Note that

since gives the largest element (in absolute value) of the th row of , and taking the maximum over all ’s gives the largest element of over all entries. And for , it holds that

where is the -operator norm, and the last equality follows from the fact that . As a result, (50) can be re-written as:

| (51) |

Now, using (47), w.p. at least , we have

and since , it directly follows that . Therefore, with probability at least ,

| (52) |

Combine the two terms, we obtain the conclusion in Proposition 2.

Proof.[Proof of Corollary 1] Here we examine the probability that events A1-A3 hold in Theorem 2. First we note that (A1) in Theorem 2 holds deterministically. Now by Proposition 1, (A2) is satisfied w.p. at least . By Proposition 2, the deviation bound (A3) holds with probability at least , where is specified in (21). Combine all sample size requirement, the leading term becomes . Therefore, for random pair , with probability at least

for some , the bound in (22) holds, as the result of Theorem 2 and Proposition 1 and 2 combined.

Proof.[Proof of Proposition 3] First we note the following decomposition:

where is the sample covariance matrix of the true errors .