On Optimal Pricing Model for Multiple Dealers in a Competitive Market

Abstract

In this paper, the optimal pricing strategy in Avellande-Stoikov’s [1] for a monopolistic dealer is extended to a general situation where multiple dealers are present in a competitive market. The dealers’ trading intensities, their optimal bid and ask prices and therefore their spreads are derived when the dealers are informed the severity of the competition. The effects of various parameters on the bid-ask quotes and profits of the dealers in a competitive market are also discussed. This study gives some insights on the average spread, profit of the dealers in a competitive trading environment.

1 Introduction

The role of a dealer in securities markets is to stand ready immediately to trade fixed amounts of securities at stated bid and ask prices. An investor who would like to trade immediately (a demander of immediacy) can do so by placing a market order to trade at the best available price: the bid price if selling or the ask price if buying. Liquidity provision was once performed only by dedicated broker-dealers, known as market makers. Market makers kept enough liquidity in their hands so as to satisfy both supply and demand of any arriving traders. In recent years, with the growth of electronic exchanges such as Nasdaq’s Inet, anyone wishing to submit limit orders in the system can easily play the role of a dealer. Agents who can post limit orders based on the availability of high frequency data, form a competitive trading environment. In this paper, we focus on studying the optimal pricing strategies under multiple dealers’ competition.

The pricing strategies of dealers have been studied extensively in the micro-structure literature. The two most often addressed sources of risk faced by dealers are: (1) the inventory risk arising from uncertainty in the asset’s value; and (2) the asymmetric information risk arising from informed trades. As noted by Demsetz (1968) [6], while the limit orders are in a queue, the dealer who places limit orders incurs both inventory and waiting costs. Inventory costs arise from uncertainty about market prices of the securities that the dealer may hold in his portfolio while his limit orders are pending. The waiting costs are the opportunity costs associated with the time between placing an order and its execution. The concept of transaction costs was first proposed by Demsetz [6]. Copeland and Galai (1983) [4] pointed out in their paper that limit orders also suffer from an informational disadvantage, whereby they are picked off by better-informed investors.

Generally speaking, the probability of limit orders being executed depends on the limit order price proximity to the current market price. Cohen et al. (1981) [5], called this phenomenon a “gravitational pull” of existing quotes. Limit orders placed at current market quotes are likely to be executed, whereas the probability of execution for aggressive limit orders is close to zero. They also pointed out that the probability of executing a limit order decreases as a security’s order arrival rate decreases.

Stoll (1978) [21] developed an explicit and rigorous model for an individual dealer limited to the behavior of a single dealer making a market in a single stock. They also discussed the implications of trading cost in different market organizations of dealers. Ho and Stoll (1981) [13] extended Stoll’s (1978) work in the aspect of uncertainty (introduction of transactions uncertainty), explicit treatment of a multi-period strategy for the dealer, and also the introduction of the demand side. For the supply side, the research work was pioneered by Demsetz (1968) [6], and additional theoretical contributions were made by Tinic (1972) [22] and Stoll (1978) [21].

Garman (1976) [8] was the first to investigate the optimal market-making conditions through modeling temporary imbalances between buy and sell orders. Ho and Stoll (1981) [13] adopted Garman’s concept of stochastic supply and demand for securities, viewing both the demand to sell and buy securities as demand for dealer services and assuming a linear demand relation for dealer sales and purchases. They took the “true” price of the stock to be exogenously determined by an information set, and assumed that the dealer’ prices were relative to the “true” price. The key concern of Ho and Stoll is about the risk that the dealer faces, and how this affected dealer’s willingness to provide his services. In another paper by Ho and Stoll (1980) [12], the problem of dealers under competition was analyzed and the bid and ask prices were shown to be related to the reservation (or indifference) prices of the agents.

Based on the idea and work of Ho and Stoll (1981) [13], Avellaneda and Stoikov (2008) [1] enhanced Garman’s model to a quantitative market-making limit order book strategy that generates persistent positive returns; indeed the economic setting of the problem is similar. The main differences are the nature of “true” price of the asset, the explicit utility function of the agent and the trading intensity under the laws governing the micro-structure of financial markets. In [1], the “true” price was given by the market mid-price. In order to model the arrival rate of buy and sell orders that will reach the agent, they drew on recent results in econophysics 111Econophysics is an inter-disciplinary research area, which applies theories and methods in Physics to study Economics problems., Potters and Bouchaud (2003) [20], and gave an exponential arrival rate of the market orders. The approach adopted is to combine the utility framework of the Ho and Stoll (1981) [13] approach with the micro-structure of actual limit order book as described in the econophysics literature. The strategy, focusing on the effects of inventory risk, outperforms the “best-bid-best-ask” market-making strategy where the trader posts limit orders at the best bid and ask available on the market.

More recently, Cartea and Jaimungal [3] used a similar model to introduce risk measures for high-frequency trading. They used a model inspired by Avellaneda-Stoikov [1] in which the mid-price is modeled by a Hidden Markov Model (HMM). Guilbaud and Pham [11] also used a model inspired by the Avellaneda-Stoikov framework but including market orders and limit orders the best (and next to the best) bid and ask together with stochastic spreads. Guéant et al. [10] provided some simple and easy-to-compute expressions for the optimal quotes when the trader is willing to liquidate a portfolio. Some other recent works include Alavi Fard (2014) [23] and Song et al. (2012) [24] for example. It seems that in the literature more attention has been given to trading strategies in a single dealer’s framework while relatively little attention has been paid to a multiple-dealer case. We are dedicated to the latter case.

In this paper, the dealers’ optimal bid and ask quotes in the multiple dealers case are determined. The optimal pricing strategy accounts for two key factors: the inventory level of the the dealer and the competition severity. Our paper contributes to the high frequency trading literature in various aspects. Firstly, we derive the optimal bid and ask prices for each dealer when the dealers are informed the severity of the competition (for example,how many active dealers are in the market). Each dealer quotes his optimal prices considering the market information and his own inventory level to maximize his final profit at terminal time . Secondly, we compare quoting prices with those obtained in [1] to shed some lights on trading competition in the market. Thirdly, we also conduct comparison of the profit generated by dealers in competitive markets with that in single dealer markets. This comparison may hopefully enhance our understanding on how high frequency trading dealers gain profits by providing stock liquidity.

The remainder of the paper is structured as follows. In Section 2, to give readers the background of research, we review two models, one by Ho and Stoll in [13] and the other by Avellaneda and Stoilov in [1]. In Section 3, we present the extended model and results in [1] for a market consisting of dealers. The limit order book intensities for the dealers are derived. In Section 4, we consider two situations, inactive dealers and active dealers, for the multiple dealer problem. In the case of dealers in markets under competition, we need to make use of an approximation method and the principle of Dynamic Programming (DP), i.e., the solution methods combine backward induction with a forward simulation of states. In Section 5, numerical results are given and compared for one-dealer and multiple-dealer situations. Finally, concluding remarks are given in Section 6 to discuss further research issues.

2 A Review of Two Models

In this section, we describe the background of this research by reviewing two related models, one by Ho and Stoll in [13] and the other by Avellaneda and Stoilov in [1]. The developments below follow those in [1, 13].

2.1 Ho-Stoll Model

The model proposed by Ho and Stoll (1981) [13] imposed the following assumptions.

-

(i)

Transactions are assumed to evolve over time according to Poisson jump processes as in Garman (1976) [8]. Two Poisson processes are used, one for purchases by the dealer and the other for sales by the dealer, as follows:

and

where is the indicator function of the event , is the market order size, and and are the intensities of the transactions. Here and are the increments of the number of market buy orders and the number of market sale orders, respectively.

-

(ii)

The dealer determines a price of immediacy, , should a market sale order arrive and a price, , should a market buy order arrive. The dealer does not directly quote and , instead, he quotes his bid and ask prices, respectively, as follows:

Here is the dealer’s opinion of the true price of the stock at the time he sets the bid-ask quotation and this price is supposed to be a given constant.

-

(iii)

The intensities, and , depend on the dealer’s selling fee and buying fee, respectively.

-

(iv)

In addition to uncertainty about the timing of subsequent transactions, the dealer faces uncertainty about the return on his existing portfolio. Consequently

Here are the balances of the cash account, inventory account, and base wealth, respectively. Here , represent the mean return of inventory account and base wealth per unit time, respectively. And is the constant continuously compounded risk-free rate. Here and are Wiener processes with mean zero and constant variance rates, and , respectively.

The objective of the dealer is to maximize the expected utility of his total wealth, , at the terminal time , where

Notice that is the conditional expectation of given information up to time . Numerous transactions and price changes occur between and .

2.2 Avellaneda-Stoikov Model

-

(i)

Assume that the money market pays no interest, and the mid-market price, or mid-price, of the stock evolves over time according to the following zero-drift diffusion process:

(1) where the initial value , is a standard one-dimensional Brownian motion and is a constant, i.e., a constant volatility model.

-

(ii)

The agent’s objective is to maximize the expected exponential utility of his portfolio at the terminal time . The exponential utility is given by

(2) where is the risk-aversion parameter.

-

(iii)

The Poisson intensity at which the agent’s orders are executed is supposed to be exponential. In the symmetric case, exponential arrival rates are assumed to take the following form:

(3) -

(iv)

The reservation bid and ask prices and , which can be interpreted as the indifference prices for buying and selling, respectively, are introduced and they satisfy

(4) where , is the initial wealth at time and is the initial inventory level at time .

In their model, it is assumed that there is only one monopolistic dealer in the trading system. The dealer buys or sells one stock in the market. The dealer quotes the bid price and the ask price , and is committed to, respectively, buy and sell one share of stock at these prices. The wealth in cash jumps whenever there is a buy order or sell order and it is governed by

| (5) |

Here is the amount of stocks bought by the dealer and is the amount of stocks sold. They are assumed to follow Poisson processes with intensities and , respectively. The number of units of the stock or the inventory level held by the dealer is then governed by

| (6) |

The objective of the dealer who can set limit orders is

| (7) |

where , and the dealer holds stocks at time . Note that and are the prices of immediacy for selling and buying, respectively, from the dealer’s perspective. For the case of an inactive trader, the choice variables and are absent. According to Avellaneda and Stoikov (2008) [1], the value function for the inactive dealer, who holds an inventory of stocks until the terminal time , can be written as follows:

| (8) |

The definition of reservation or indifference price was introduced in [1] and we shall give it in Eq. (11). The dealer’s reservation bid and ask prices and are given, respectively, by

| (9) |

i.e.,

| (10) |

Hence the average of the above two prices, say the reservation price or the indifference price, is given by

| (11) |

To consider the case of active dealers, who will make decisions to buy or sell before the terminal time , in [1], the authors derived the following HJB equation (see for instance [1], Section 3):

| (12) |

To solve the HJB equation, in [1], the authors consider the simplest case by assuming that the Poisson intensities take the following form (c.f. Eq. (3)):

| (13) |

Then the following trial solution was adopted:

| (14) |

where is approximated up to the second-order of a Taylor expansion about the inventory variable :

| (15) |

When the inventory level is , the reservation bid price of the stock and the reservation ask price of the stock are given, respectively, by

| (16) |

Substituting into Eq. (12) yields

| (20) |

Using the first-order optimality condition, the problem can be transformed into the following one:

| (21) |

In [1], the authors consider an asymptotic expansion of about , and higher order terms are assumed to be small enough to be negligible. By considering the coefficients of and , the following results are obtained:

| (22) |

which matches with Eq. (11) and the bid-ask spread is then given by

| (23) |

3 The Limit Order Book Rates

In this section, we consider the situation of multiple dealers in a competitive market. We focus on the discussion of dealers’ trading rates in the market.

In [1], for only one dealer in the market, the arrival rates of buy and sell orders that will reach the dealer follows a Poisson process with a common exponential arrival rate in Eq. (13) which depends on dealer’s quotes. In the case of multiple dealers market under competition, we assume that the overall frequency of market orders will depend on the quotes of all dealers in the market. Suppose that there are dealers in the market and that dealers have impacts on the arrival of market orders. Under certain assumptions, we shall show that the market orders follow a Poisson process with common exponential arrival rate,

Here reflects the influence (e.g. competitiveness) of Dealer on the overall frequency of market orders. In a number of studies [1, 2, 7, 9, 19], it has been shown that the distances , (c.f. Eq. (7)) and the current shape of the limit order book determine the priority of execution when large market orders get executed. For example, when a large market order to buy stocks arrives, the limit orders with the lowest ask prices will be automatically executed. Let be the price of the highest limit order executed in this trade, we define to be the temporary market impact of the trade of size . If the agent’s limit order is within the range of this market order, i.e. , his limit order will be executed. To quantify dealers’ trading intensity, other than the overall frequency of market orders, we need to know the distribution of market orders’ size and the temporary impact of a large market order. We have the following proposition.

Proposition 1

Suppose that dealers’ impacts on the overall frequency of market orders, i.e., and are “separable” and have an “identical functional form”, i.e., (we take as an example), taking the following form:

and . Here describes Dealer ’s impact on market orders’ overall frequency. Then

Furthermore, if the distribution of the size of market orders obeys a “power law”, [7, 9, 19], i.e., and the market impact follows a “ law” [2], i.e., , then we have

The proof of the proposition can be found in Appendix A.

4 The Multiple-Dealer Problem

In this section, we discuss the situation of multiple dealers buying and selling stocks in a competitive market. In particular, we consider two situations: inactive and active dealers. The underlying problem is a state-feedback control problem. Both inactive dealer’s “frozen” strategy and active dealer’s optimal quoting strategy are discussed in this section. For the active dealer’s situation, each dealer follows a multi-period strategy that maximizes his objective function taking into account not only his own possible future actions but also those of his competitors. This is much more complex than the single dealer case. Discrete and continuous models for active dealers are discussed. Furthermore, a comparison between the performances of active dealers and inactive dealers is made.

Our objective is to study the trading strategies of different dealers in a competitive market, where each dealer has his own reservation value of the stock based on his inventory position. The dealers wish to buy or sell stocks in the market, and the mid-price is assumed to be governed by the following stochastic differential equation (c.f. Eq. (1)): with initial value . Here is a standard Brownian motion and is a positive constant. Each dealer , , quotes his bid price and ask price , and is committed to, respectively, buying and selling one share of the stock at these prices at time . Hence, the wealth of Dealer in cash jumps whenever there is a buy or sell order executed.

| (24) |

where is the amount of stocks bought and is the amount of stocks sold by Dealer up to time . They are supposed to follow Poisson processes with intensities, and , respectively. In view of the results in Proposition 1, the Poisson intensities take the form:

| (25) |

The number of stocks is governed by

| (26) |

Let

| (27) |

then we have

| (28) |

4.1 Inactive Dealer

We first consider an inactive trader, Dealer , who does not have any limit orders in the market and simply holds an inventory of stocks until the terminal time , which is a special case of the feedback control problem in which . Following [1], it is not difficult to show that

| (29) |

which is the same as the value function calculated in the monopolistic market, showing us directly its dependence on the market parameters. The reservation bid and ask prices are given implicitly by the relations

| (30) |

which means that the agent is indifferent between keeping inactive and buying one stock at the reservation bid price (or, selling one stock at the reservation ask price ). It is straightforward to calculate that

| (31) |

and the reservation (or difference) price is given by

| (32) |

4.2 The Active Dealers

In general, it may not be easy to determine the optimal quoting strategies for dealers in a competitive market. In the market, each dealer’s action depends not only on his own but also his competitor’s characteristics. They all need to solve a relatively complex Dynamic Programming (DP) problem than the one encountered in the single dealer case. In this section, we develop a feasible quoting policy using a linear approximation method and the principle of DP. We first discuss a discrete model and then give a recursive formula for the bid and ask quotes. We then extend the discrete model to a continuous one. By directly using a linear approximation and the DP principle to solve the optimal control problem, one can obtain an optimal quoting strategy for dealers in the continuous competition model.

4.2.1 The One-period Model

Suppose there are dealers in the market, namely Dealer 1, Dealer 2, , Dealer . In the one period case, we assume that dealers may only trade in the last trading session, and trades happen immediately after time . Dealers choose their bid and ask quotes at the beginning of the trading session, , defined through the controls . These quotes influence the arrival rates of market orders over the time interval . By Eq. (25), the arrival rates take the following forms:

| (33) |

For any dealer in this competitive market, the objective is to determine the optimal bid and ask quotes to maximize his own expected utility function:

| (34) |

which is a stochastic feedback control problem. For any dealer, he can only determines his optimal bid and ask quotes and . However, the stochastic feedback problem is related to optimal bid and ask quotes and of all dealers. Thus it is also a problem of game competition, especially, it is a simultaneous game problem. Suppose all dealers achieve the Nash equilibrium in this game problem, then the results in the proposition below follow.

Proposition 2

The optimal quoting policy in the one period case is

| (35) |

and Dealer ’s utility is given by

| (36) |

where .

The proof can be found in Appendix B.

We remark that

- (i)

-

Only in the one-period case, a dealer’s bid and ask quotes are independent of his competitors. However, even in the one-period case, the value function of each dealer is not independent of the inventory position and other parameters, such as risk aversion of the competing dealers.

- (ii)

-

Dealer ’s bid-ask spread is given by

(37) which is independent of the inventory. After taking a first-order approximation of the order arrival term, we have

(38) where the linear term does not depend on the inventory variables. Therefore, if we substitute Eq. (38) into Eq. (36), we arrive at the conclusion that Dealer ’s utility depends only on his own inventory . We define this approximation as

which equals

(39) where

(40) - (iii)

-

Set

where

is independent of stock price and cash wealth .

- (iv)

-

We define the market bid and ask quotes,

and the market bid-ask spread,

which depends on dealers’ inventories. We remark that Dealer ’s bid-ask spread is always positive, however, the market bid-ask spread can be negative.

- (v)

-

Notice that

which means that active dealers will always have advantage over the inactive dealers.

In the next section, we shall employ this linear approximation technique to analyze the dynamics of dealer markets in the multi-period case.

4.2.2 The Two-period Model

Assume that Dealer may only trade in the intervals and . The dealer chooses bid and ask quotes at time and with the controls and , and trades happen immediately after time and . Adopting the above linear approximation, one can establish the following proposition.

Proposition 3

In two period model, dealers’ optimal bid and ask quotes are given by

| (41) |

and Dealer ’s utility is given by

| (42) |

where .

The proof can be found in Appendix C.

We remark that

- (i)

-

The spread (compare to Eq. (37))

is independent of the inventory. By taking a first-order approximation of the order arrival term, we have (compare to Eq. (38))

(43) We notice that the linear term does not depend on the inventory. Similar to the one-period case, substituting the linear approximation of into Eq. (41), one can get an approximation of Dealer ’s utility , which equals to

(44) and it only depends on his own inventory.

- (ii)

-

Set

where

is independent of stock price and cash wealth .

By repeating the argument of this analysis, one can get the following result for the multi-period model.

4.2.3 The Multi-period Model

Suppose that there are at most trades occur in . Divide the time period into small subintervals, . Assume that each trade may only occur immediately after the beginning of those subintervals and there is no trade occurring in . All dealers choose their bid and ask quotes at time , defined by the controls and . Adopting the approximation of dealers’ utility functions and using the back-forward analysis method, it is straightforward to obtain the following proposition and we skip the proof.

Proposition 4

In the -period model, dealers’ optimal bid and ask quotes are given by

| (45) |

and Dealer ’s utility is given by

| (46) |

where .

4.2.4 The Continuous Model

In every step of the back-forward model, we adopt the first-order approximation of the arrival terms appearing in the utility function. Then we find that an approximate dealer’s utility functions depend only on their own inventories. We then consider the case of continuous model. Define the approximate utility as . The following theorem results from applying the principle of Dynamic Programming (DP).

Theorem 1

The optimal bid and ask quotes in dealer markets under competition are given by

| (47) |

and dealers’ approximate utility functions under the quoting strategy are greater than those for the inactive case; that is,

| (48) |

Proof: We note that

which is derived when the dealer follows the optimal strategy for setting and at each point in time period . To simplify our discussion, we suppose that other dealers are in equilibrium under the Cournot competitive environment [15]. The Cournot competition model is an economic setting for describing a market where firms compete on their amount of output and make decisions independently of each other.

Using the principle of Dynamic Programming (DP) and under certain smoothness conditions of the value function ,the following HJB equation is obtained.

| (49) |

As in [1], the following ansatz is considered

where is an approximate quadratic polynomial in the inventory variable . Then the HJB equation can be written as follows:

| (50) |

From the first-order optimality condition in Eq. (50), we can obtain the optimal distance and of Dealer given the equilibrium values of all dealers, which satisfy

| (51) |

where

| (52) |

The above is the best response function of Dealer given the values of other dealers’ quotes. In Nash equilibrium, all dealers will play the best responses. Thus we can solve the above equations simultaneously to obtain the optimal feedback controls and . We recall that

Thus we have

| (53) |

and similarly,

| (54) |

Substituting the optimal values given by Eq. (51) into Eq. (50) and using the rate of limit order book in Proposition , we obtain

| (55) |

We consider an asymptotic expansion of in the inventory variable

| (56) |

From the exact relations of the indifference bid and ask prices, and , we obtain

| (57) |

Recall the first-order optimality conditions

| (58) |

and we have

| (59) |

which does not depend on the inventory . Taking a first-order approximation of the order arrival term

| (60) |

we notice that the linear term does not depend on . Since

then . Therefore, by grouping the terms of order , we obtain

| (61) |

whose solution is . Grouping terms of order yields

| (62) |

whose solution is

| (63) |

We obtain almost the same value function for an active agent as for an inactive agent,

and the same indifference price

Now we analyze the difference between our approximation and the exact solution of our HJB equation. Suppose that

| (64) |

where is a family of continuous functions. Substituting the above expression directly into the HJB equation, we obtain

| (65) |

where is a family of positive functions. Consequently,

which is always greater than zero for . Thus we have

i.e.,

| (66) |

Now we set the bid-ask spread as

| (67) |

and a price adjustment as

| (68) |

We remark that

- (i)

-

For the “frozen inventory” problem, we have

For the active dealer, we have

This means that active dealers using our strategy to quoting always have an advantage over inactive dealers.

- (ii)

- (iii)

-

The price adjustment , depends on the dealer’s inventory. It is an inventory response equation that specifies the price adjustments variable be negative (positive) when inventory is positive (negative). When , both bid price and ask price are “low”, in this situation, the dealer prefers to sell than to purchase, and this will therefore reduce the dealer’s inventory. On the other hand, if , then the dealer prefer to purchase than to sell. The degree of price response to an inventory change depends on the same factors determining the size of the bid and ask spread-time remained (), Dealer ’s risk aversion (determined by ) and variance (determined by );

- (iv)

-

Compared with the “frozen inventory strategy”, our strategy can eventually improve dealer’s final profit which is no less than the original indifference curve (in the “frozen inventory” problem, can be seen as ).

5 Numerical Experiments

In this section, we present and discuss numerical results on both single monopolistic dealer and multiple dealers in a competitive market.

5.1 Bid-ask Quotes

Avellaneda and Stoikov (2008) tested the performance of their “inventory” strategy, focusing primarily on the shape of the profile and the final inventory . They compared it with a benchmark strategy that is symmetric around the mid-price, regardless of the inventory under the assumption of a monopolistic dealer. In this section, we test the performance of our strategy for multiple dealers in a competitive stock market.

Suppose that there are dealers in a market. In the numerical experiments, we assume ’s to be identical, i.e., . As far as our simulation is concerned, we chose the following parameters: , , , , , , , and , where (the values of the parameters are chosen to be the same as those in [1]). The simulation results are obtained through the following procedures:

-

(i)

At time , the agents’ quotes, and for Dealer , are computed, given the state variables;

-

(ii)

At time , the state variables are updated: with probability , Dealer ’s inventory decreases by one and his wealth increases by ; with probability , Dealer ’s inventory variable increases by one and the wealth decreases by , where . The mid-price is updated by a random increment .

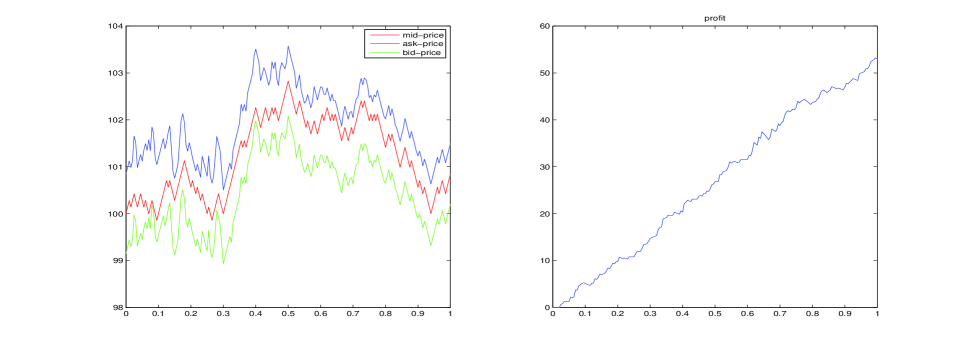

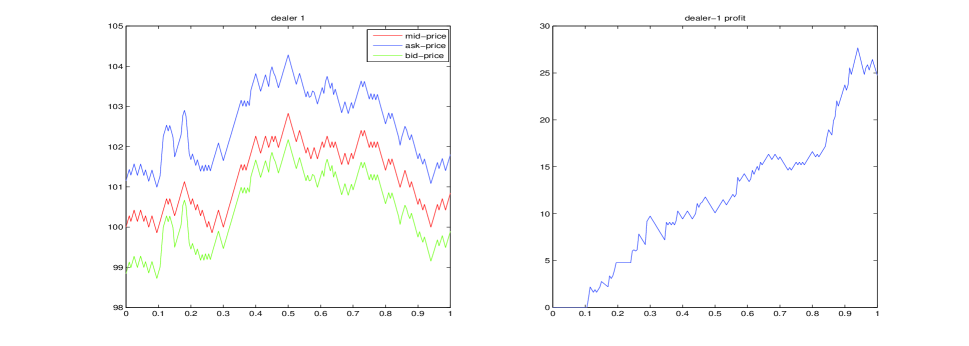

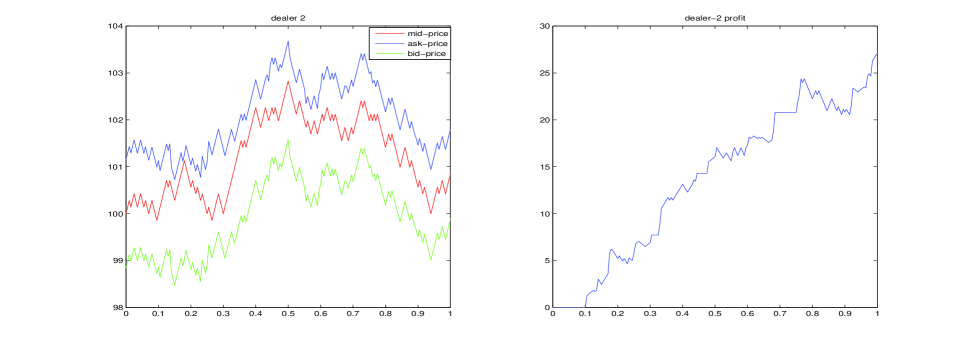

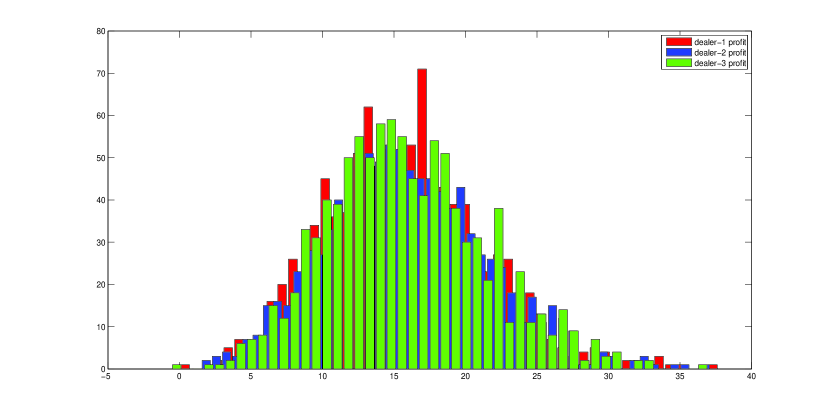

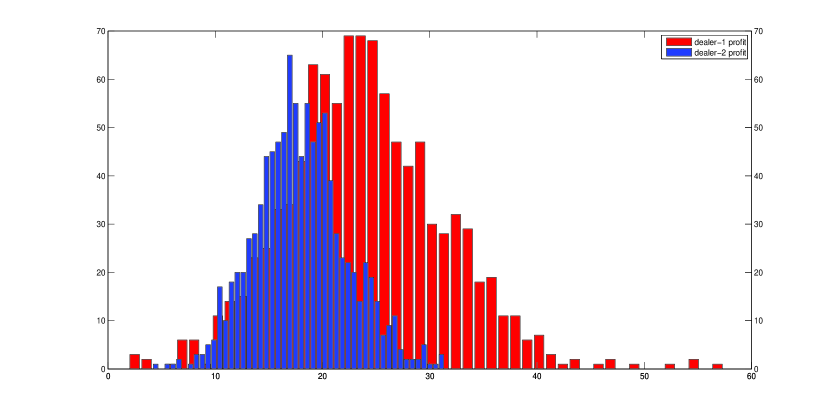

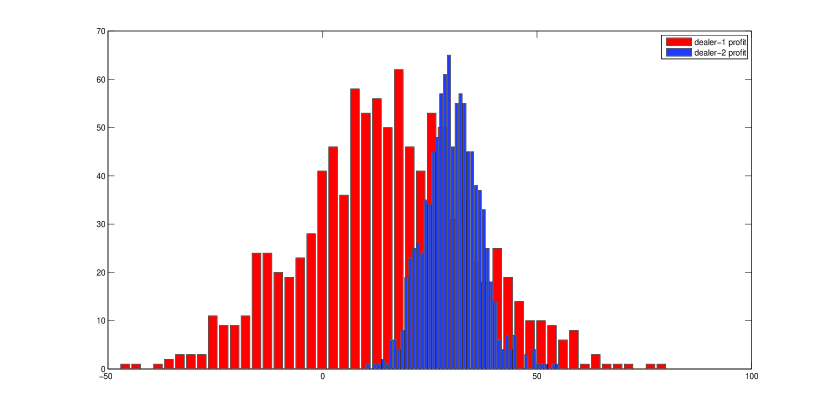

Figure 1 and Figure 2, respectively, present the optimal bid-ask quotes and their profits of the monopolistic dealer and competitive dealers (two dealers). The profit of each dealer in the two-dealer case is approximately half of that in the monopolistic case. This seems consistent with the assumption that , (), equal sharing of the profits. Avellaneda-Stoikov’s inventory strategy generates persistent positive returns while our extended strategy preserves this good property in a competitive market.

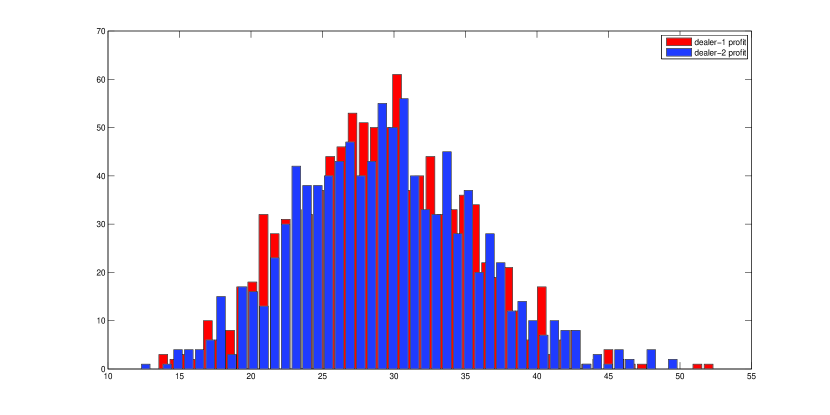

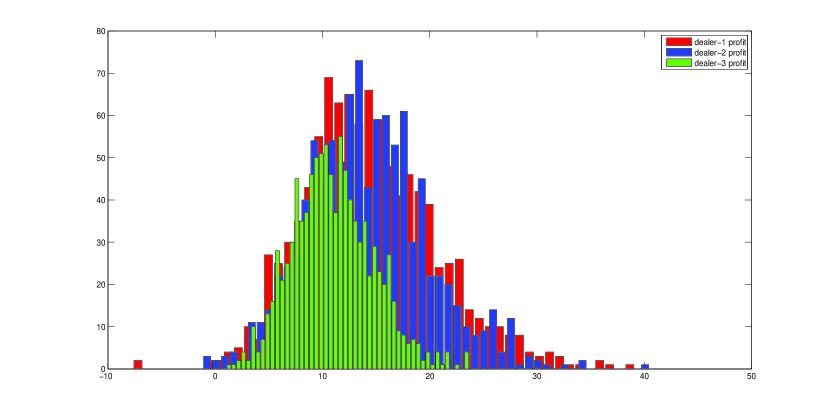

5.2 Competitive Dealers and Their Profits

We consider the effects of changing from one monopolistic dealer to multiple dealers in a competitive market where the number of dealers varies. The numerical results are presented in Tables 1-4 and also Figures 3 and 4.

| Agent | Average Spread | Profit | Std (Profit) | Std () | |

|---|---|---|---|---|---|

| Dealer | 1.49 | 64.26 | 5.68 | 0.20 | 3.40 |

| Agent | Average Spread | Profit | Std (Profit) | Std () | |

|---|---|---|---|---|---|

| Dealer 1 | 2.11 | 29.15 | 6.09 | -0.02 | 2.88 |

| Dealer 2 | 2.11 | 29.40 | 6.22 | 0.08 | 2.79 |

| Agent | Average Spread | Profit | Std (Profit) | Std () | |

|---|---|---|---|---|---|

| Dealer 1 | 2.79 | 15.69 | 5.65 | 0.14 | 2.51 |

| Dealer 2 | 2.79 | 15.85 | 5.69 | -0.11 | 2.58 |

| Dealer 3 | 2.79 | 15.88 | 5.53 | -0.01 | 2.44 |

| Agent | Average Spread | Profit | Std (Profit) | Std () | |

|---|---|---|---|---|---|

| Dealer 1 | 5.40 | 1.76 | 2.34 | 0.028 | 0.79 |

| Dealer 2 | 5.40 | 1.93 | 2.52 | -0.045 | 0.84 |

| Dealer 3 | 5.40 | 1.95 | 2.57 | 0.003 | 0.82 |

| Dealer 4 | 5.40 | 1.79 | 2.46 | -0.03 | 0.80 |

| Dealer 5 | 5.40 | 1.83 | 2.49 | 0.003 | 0.79 |

| Dealer 6 | 5.40 | 1.86 | 2.50 | -0.001 | 0.83 |

| Dealer 7 | 5.40 | 1.86 | 2.60 | -0.019 | 0.86 |

We observe that the standard deviations of are relatively larger when compared with the corresponding values of in most of the cases. And in the case of seven dealers, the standard deviations of the profits are relatively large compared with the corresponding profits as well. When the number dealers increases, we observe that profit decreases but the average spread increases. Continuous markets are characterized by the bid and ask prices at which trades can take place. The bid-ask spread reflects the difference between what active buyers must pay and what active sellers receive. It is an indicator of the cost of trading and the illiquidity of a market. We can see from the results that, when more and more agents enter into a competitive market, on one hand, competition becomes intense, which reduces the profit that each agent can obtain from the stock market. On the other hand, the liquidity of the stock enhances which provides good supplies to the traders.

5.3 Sensitivity Study of

We now consider the effects of varying the parameter, . Suppose the number of dealers in the competitive market is fixed and that all dealers’ initial states are the same, except the risk aversion parameter. We can see from Tables 5 & 6 and Figures 5 & 6 that risky dealers take larger positions than risk-averse ones. They have smaller values of average spreads and larger profits, but also suffer from larger variances of profits and final inventories , which lead to higher levels of uncertainty.

| Agent | Average Spread | Profit | Std (Profit) | Std () | |

|---|---|---|---|---|---|

| Dealer 1 | 2.01 | 23.97 | 7.44 | 0.07 | 4.30 |

| Dealer 2 | 3.39 | 17.98 | 4.25 | -0.074 | 1.61 |

| Agent | Average Spread | Profit | Std (Profit) | Std (). | |

|---|---|---|---|---|---|

| Dealer 1 | 2.77 | 14.36 | 6.26 | -0.09 | 3.43 |

| Dealer 2 | 2.79 | 14.21 | 5.68 | -0.01 | 2.70 |

| Dealer 3 | 3.74 | 10.99 | 3.74 | 0.08 | 1.47 |

5.4 Sensitivity Study of Initial Inventory Positions

We also consider the effects of varying inventories on the performance of the dealers. For simplicity, we consider the two-dealer case.

| Agent | Average Spread | Profit | Std (Profit) | Std () | |

|---|---|---|---|---|---|

| Dealer 1 | 2.11 | 14.85 | 19.59 | 0.19 | 2.94 |

| Dealer 2 | 2.11 | 30.24 | 6.34 | -0.13 | 3.00 |

| Agent | Average Spread | Profit | Std (Profit) | Std () | |

|---|---|---|---|---|---|

| Dealer 1 | 2.11 | -391.98 | 84.14 | 2.09 | 2.99 |

| Dealer 2 | 2.11 | 37.55 | 12.45 | -1.98 | 2.91 |

| Agent | Average Spread | Profit | Std (Profit) | Std () | |

|---|---|---|---|---|---|

| Dealer 1 | 2.01 | 13.11 | 40.42 | 25.31 | 4.74 |

| Dealer 2 | 2.01 | 32.69 | 16.18 | -7.12 | 4.57 |

Setting all the parameters identical, and we assume that dealers differ only in their initial inventory positions. From Tables 7 & 8 and Figure 7, one can see that with a larger initial position, Dealer 1 in both examples gain smaller amounts of profits. When the initial position is significantly large (Table 8), Dealer 1 obtains a negative profit as one may prefer a less risky position with a negative profit than a risky position with a positive cash flow. From Table 9, one can see that when lowering the risk aversion of Dealer 1, his final profit will increase accordingly. We refer interested readers on the analysis of the effects of initial inventories to the paper by Ho and Stoll (1980) [12].

6 Conclusions

The field of market micro-structure encompasses two general types of models, i.e., inventory models and information models. In this paper, we focus on the effect of inventory and extend Avellanede-Stoikov’s optimal price strategy for a monopolistic dealer to that for multiple dealers in a competitive market. We derive the approximate optimal bid and ask prices for each dealer when the dealers are informed the severity of the competition. We also analyze the effect of various parameters in our model on the bid-ask quotes and profits of the dealers in a competitive market. For future research, one may take into account the presence of additional market factors such as order handling costs, asymmetric information and inter-dealer trading in the model.

In this paper, the mid-price of the stock is assumed to follow Eq. (1). In our future study, we shall consider a more general volatility model, for example, the Heston stochastic volatility model [16, 17, 18]. We shall assume the mid-price follows the following stochastic differential equations:

| (69) |

where , and are positive constants and the volatility, , is related to the level of stock price via the third equation in Eq. (69) and .

7 Appendix

7.1 Appendix A.

Proof: Consider first the arrival rate of market order. When ,

By condition (i), when

where ; when , this is equivalent to the case when , that is

Consequently

By Condition (i), for any ,

where . When then this situation is equivalent to the case when , i.e.,

and . Consequently, we gave

To calculate the arrival rate of buy and sell orders that will reach the dealer, we need the following information:

(i) the overall frequency of market orders;

(ii) the distribution of market orders’ size;

(iii) the temporary impact of a large market order.

From above, we are given one of the estimation of market orders’ frequency.

For the other conditions, from a lot of studies, see for instance

[7, 9, 19],

we have some statistical properties of the limit order book, such as,

the distribution of the size of market orders obeys a power law:

and the market impact follows a “ law” [2], i.e., or

Here we recall that where is the price of the highest limit order executed in the trade and is stock mid-price. Aggregating the information of limit order book’s statistical properties, we have

and

We have, for some constant ,

7.2 Appendix B

Proof: We note that there is no trading in the period ,

Thus the expected exponential utility of Dealer ’s ultimate wealth equals

By considering the first-order optimality conditions, we can obtain the optimal bid and ask quotes as follows:

| (70) |

Substituting the optimal bid and ask quotes into the expected utility function, one can get the utility for Dealer .

7.3 Appendix C

Proof: We apply the principle of Dynamic Programming (DP) to Dealer ’s utility function, and obtain

| (71) |

By considering the first order optimality conditions, we obtain Dealer ’s optimal ask quote as follows:

| (72) |

Similarly, we can give his bid quote

| (73) |

Substituting the optimal bid and ask quotes into the utility function, one can obtain Dealer ’s utility function:

| (74) |

Acknowledgements

The authors would like to thank the referees and the editor for their helpful comments and suggestions. This research work was supported by Research Grants Council of Hong Kong under Grant Number 17301214 and HKU CERG Grants and Hung Hing Ying Physical Research Grant.

References

- [1] M. Avellaneda and S. Stoikov (2008), High-frequency trading in a limit order book, Quantitative Finance, 8, 217–224.

- [2] J. Bouchaud, M. Mezard and M. Potters (2002), Statistical properties of stock order books: empirical results and models, Quantitative Finance, 2, 251–256.

- [3] Á. Cartea and S. Jaimungal (2015), Risk measures and fine tuning of high frequency trading strategies, Mathematical Finance, 25 576–611.

- [4] T. Copeland and D. Galai (1983), Information effects on the bid-ask spread, Journal of Finance, 38, 1457–1469.

- [5] K. Cohen, S. Maier, R. Schwartz and D. Whitcomb (1981), Transaction costs, order placement strategy, and existence of the bid-ask spread, Journal of Political Economy, 89, 287–305.

- [6] H. Demsetz (1968), The cost of transacting, Quarterly Journal of Economics, 82, 33–53.

- [7] X. Gabaix, P. Gopikrishnan, V. Plerou and H. Stanley (2006), Institutional investors and stock market volatility, Quarterly Journal of Economics, 121, 461–504.

- [8] M. Garman (1976), Market Microstructure, Journal of Financial Economics, 3, 257–275.

- [9] P. Gopikrishnan, V. Plerou, X. Gabaix, and H. Stanley (2000), Statistical properties of share volume traded in financial markets, Physical Review E, 62, 4493–4469.

- [10] O. Guéant, C. Lehalle, and J. Fernandez-Tapia (2012), Optimal portfolio liquidation with limit orders, SIAM Journal on Financial Mathematics, 3, 740–764.

- [11] F. Guilbaud and H. Pham (2011), Optimal high frequency trading with limit and market orders, working paper.

- [12] T. Ho and H. Stoll (1980), On dealer markets under competition, Journal of Finance, 35, 259–267.

- [13] T. Ho and H. Stoll (1981), Optimal dealer pricing under transactions and return uncertainty, Journal of Financial Economics, 9, 47–73.

- [14] T. Ho and R. Macris (1984), Dealer bid-ask quotes and transaction prices an empirical study of some AMEX options, Journal of Finance, 39, 23–45.

- [15] C. Holt, Markets, games and strategic behavior, Pearson Education, USA, 2006.

- [16] J. Hull and A. White (1990), Pricing interest-rate derivative securities, The Review of Financial Studies, 3, 573–592.

- [17] J. Hull (2006), Options, futures, and other derivatives, N.J: Prentice Hall. Upper Saddle River, (6th ed.).

- [18] Heston, S.L.(1993), A Closed-Form Solution for Options with Stochastic Volatility with Applications to Bond and Currency Options, The Review of Financial Studies 6(2), 327–343.

- [19] S. Maslow and M. Mills (2001), Price fluctuations from the order book perspective: empirical facts and a simple model, Physica A, 299, 234–246.

- [20] M. Potters and J. Bouchaud (2003), More statistical properties of order books and price impact, Physica A, 324, 133–140.

- [21] H. Stoll (1978) The supply of dealer services in securities markets, Journal of Finance, 33, 1133–1151.

- [22] S. Tinic (1972) The economics of liquidity services, Quarterly Journal of Economics, 86, 79–93.

- [23] F. Alavi Fard (2014) Optimal bid-ask spread in limit-order books under regime switching framework, Review of Economics and Finance, Volume 4, Issue 4, Article ID: 1923-7529-2014-04-33-16.

- [24] N. Song, W. Ching, T. Siu and C. Yiu (2012) Optimal submission problem in a limit order book with VaR constraint, The Fifth International Joint Conference on Computational Sciences and Optimization (CSO2012), IEEE Computer Society Proceedings, 266–270.