Parametric inference of hidden discrete-time diffusion processes by deconvolution

Abstract.

We study a parametric approach for hidden discrete-time diffusion models based on contrast minimization and deconvolution. This approach leads to estimate a large class of stochastic models with nonlinear drift and nonlinear diffusion. It can be applied, for example, for ecological and financial state space models.

After proving consistency and asymptotic normality of the estimator, leading to asymptotic confidence intervals, we provide a thorough numerical study, which compares many classical methods used in practice (Monte Carlo Expectation Maximization Likelihood estimator and Bayesian estimators) to estimate stochastic volatility models. We prove that our estimator clearly outperforms the Maximum Likelihood Estimator in term of computing time, but also most of the other methods. We also show that this contrast method is the most stable and also does not need any tuning parameter.

1 Introduction

This paper is motivated by the parametric estimation of hidden stochastic models of the form:

| (1) |

where one observes ,,, and where the random variables , and are unobserved. Notably is a strictly stationary, ergodic process that depends on two measurable functions and and its stationary density is , where belongs to . The functions , and are known up to a finite dimensional parameter, , and the dependence with respect to is not required to be the same in and . Finally, the innovations and the errors are independent and identically distributed (i.i.d.) random variables, the distribution of the innovations being known for identifiability of the model.

In this work, we propose to estimate the parameters of the two functions and driving the dynamics of the hidden variables . The principle of the estimation method goes as follows. Taking that the stationary density, , is known up to the finite dimensional parameter , our M-estimator consists in optimizing a contrast function that exploits a Fourier deconvolution strategy in a parametric framework. In so doing, we exploit a ”Nadaraya-Watson approach” in the sense that we estimate (respectively, ) as ratio of an estimator of (respectively, ) and an estimator of . Notably we provide an analytical expression of the contrast function for a well-known example and characterize their main properties. Moreover we show that this deconvolution-based estimator is consistent and asymptotically normally distributed for -mixing processes which leads to obtain confidence intervals in practice for many processes. Finally, our Monte Carlo simulations show that our approach gives good results and is fast computing. All the results are illustrated on the famous stochastic volatility model with discrete time version of CIR (Cox Ingersoll Ross, see [Cox et al., 1985]) process for the volatility and are compared with many others methods used in the literature to estimate this model (Monte Carlo Expectation Maximisation, Sequential Monte Carlo).

Our approach extends the previous work [El Kolei, 2013] where parametric estimation of models of type of (1) is handled for constant volatility function () and where the estimator proposed by the author is not adapted for stochastic process with nonlinear diffusion. As in the previous work [El Kolei, 2013], this approach is the extension to the parametric framework of the work [Comte et al., 2010] where the authors propose a non-parametric estimation procedure in the case of discrete time stochastic models of the form of (1).111See also Comte et Taupin in [Comte and Taupin, 2007]. Our aim consists in showing how their procedure can be extended to a parametric framework and further by obtaining confidence intervals which are useful in practice.

Applications. This class of parametric models includes, among others, the autoregressive model with measurement errors, the autoregressive stochastic volatility model ([Taylor, 2005]), the discrete time versions of well-known diffusion processes in finance ([Hull and White, 1990], [Heston, 1993]) and some families of stochastic processes: Vasicek, CIR, modified CIR and hyperbolic processes (see [Cox et al., 1985] and [Genon-Catalot et al., 1999]).

Here, we focus on a stochastic volatility model of the form:

| (4) |

where and are centered gaussian random variables and the sampling interval. Hence, the unobserved variance process is driven by a mean reverting stochastic process which was introduced in [Cox et al., 1985] to model the short term interest rates.

By applying a log-transformation and , the SV model is a particular version of (1) since it can be written as

| (7) |

where follows a log chi-squared distribution.

From a practical point of view, the observed component stands for the log-return of an asset price while the unobserved component stands for the volatility of this asset. The parameter is the positive mean reverting parameter, is the positive long run parameter and the positive volatility of the stochastic volatility process .

Organization of this paper. The paper is organized as follows. Section 2 presents the notations and the model assumptions. Section 3 defines the deconvolution-based M-estimator and states all of the theoretical properties. Some Monte Carlo simulations are discussed in Section 4 and some concluding remarks are provided in the last section. All the proofs can be found in Appendix 5.

2 General setting and assumptions

In this section, we introduce some preliminary main notations and provide the assumptions of the model (1).

2.1 Notations

Subsequently, for any function , we denote by the Fourier transform of the function : , by its -norm, its supremum norm, stands for the scalar product in and “” for the usual convolution product. Moreover, for any integrable and square-integrable functions , , and : we have and . Finally, denotes the Euclidean norm of a matrix , and , (respectively, ) the empirical (respectively, theoretical) expectation, that is, for any stochastic variable: (respectively, ). Regarding the partial derivatives, for any function , is the vector of the partial derivatives of with respect to (w.r.t) and is the Hessian matrix of w.r.t .

2.2 Assumptions

We consider the hidden discrete-time diffusion model (1). The assumptions are the following.

-

A0

belongs to the interior of a compact set , .

-

A1

The errors are independent and identically distributed centered random variables with finit variance, . The density of , , belongs to , and for all , .

-

A2

The innovations are independent and identically distributed centered random variables with unit variance and .

-

A3

The ’s are strictly stationary and ergodic with invariant density .

-

A4

The sequences and are independent. The sequence and are independent.

-

A5

On , the functions and admit continuous derivatives with respect to up to order 2.

-

A6

The function to estimate belongs to , is twice continuously differentiable w.r.t for any and measurable w.r.t for all in . Each element of and belongs to .

-

A7

The application admits a unique minimum and its Hessian matrix, denoted by , is non-singular in .

The compactness assumption A0 might be relaxed by assuming that is an element of the interior of a convex parameter space . In this case, the statistical properties of the M-estimator can be proved in the light of convex optimization arguments. Assumptions A1-A3 are quite standard when considering estimation for convolution models. On the other hand, Assumption A3 implies that if is an ergodic process then is stationary and ergodic since it is the sum of an ergodic process and an i.i.d. noise process ([Dedecker et al., 2007]). Consequently inherits the ergodicity property. According to Assumption A4 the unknown density of the ’s is defined to be . It turns out that and thus . Assumption A5 ensures some smoothness for the drift and diffusion functions. Assumption A6 is also quite usual in the literature and serves for the construction and for asymptotic properties of our estimator.

3 Parametric deconvolution estimator

3.1 The contrast function

Definition 1 (Theoretical and empirical contrast functions).

For any square integrable real function , we set

where we recall that is the Fourier transform of the density of the observation noise. Let be given by

-

(1)

, if is a constant function of the hidden variable

-

(2)

, if is not a constant function of the hidden variable

where , and let us define the mapping as

Then, under Assumptions A1 up to A7, the contrast function is defined by:

| (8) |

and its empirical couterparts is given by

| (9) |

Remark 1.

As said in the introduction, the case where the diffusion function is a constant function of the hidden variable has already been studied in [El Kolei, 2013]. Therefore, from now on, we focus on the case 2 in Definition 1 and we refer to the aforementioned paper for the case 1 in Definition 1.

Definition 2 (Minimal contrast estimator).

Suppose that Assumptions A0-A7 hold true then, the minimum-contrast estimator is defined as any solution of

| (10) |

The existence of our estimator can be deduce from regularity properties of the function and compactness argument of the parameter space. See Appendix 5.2.1.

Remark 2.

In this paper we consider the situation in which the observation noise variance is known. This assumption, which is often not satisfied in practice, is necessary for the identifiability of the model and so is a standard assumption for state-space models given in (1).

There is some restrictions on the distribution of the innovations in the Nadaraya-Watson approach. It is known that the rate of convergence for estimating the function is related to the rate of decreasing of . In particular, the smoother is, the slower the rate of convergence for estimating is. This rate of convergence can be improved by assuming some additional regularity conditions on (see [Comte et al., 2010] and [Comte et al., 2006]).

Remark 3.

Let us explain the choice of the contrast function and how the strategy of deconvolution works. The convergence of to as tends to the infinity is provided by the Ergodicity Theorem. Moreover, the limit of the contrast function can be explicitly computed. Using (1) and Assumptions A1-A3, standard computations (see Appendix 5.1) lead to

which is, obviously, minimal at point .

3.2 Asymptotic properties

In this section we first show that our estimator is weakly consistent and asymptotically normally distributed for mixing processes. To this aim, we further assume that for defined in (2) of Definition 1 the following assumptions hold true:

-

A8

(Local dominance): .

-

A9

(Moment condition): For some , .

-

A10

(Hessian Local dominance): For some neighbourhood of :

.

3.2.1 Asymptotic properties of the estimator: consistency and normality

The first result regards the (weak) consistency of our estimator.

Theorem 1.

Sketch of proof..

The main idea for proving the consistency of a M-estimator comes from the following observation: if converges to in probability, and if the true parameter solves the limit minimization problem, then, the limit of the argminimum is . By using an argument of uniform convergence in probability and by compactness of the parameter space, we show that the argminimum of the limit is the limit of the argminimum. A standard method to prove the uniform convergence is to use the Uniform Law of Large Numbers (see Lemma 1 in Appendix 5.2.2). Combining these arguments with the dominance argument (A8) give the consistency of our estimator, and then, the Theorem 1. For further details see Appendix 5.2.2. ∎

The second result states our estimator is -consistent and asymptotically normally distributed. Besides, we give in Corollary 1 the different terms of the asymptotic variance-covariance matrix. For the CLT, we need some mixing properties (we refer the reader to [Dedecker et al., 2007] for a complete review of mixing processes). Hence, in the following, we further assume that:

-

A11

The stochastic process is -mixing.

Theorem 2.

Sketch of proof..

The asymptotic normality follows essentially from Central Limit Theorem for mixing processes (see [Jones, 2004]). Thanks to the consistency, the proof is based on a moment condition of the Jacobian vector of the function and on a local dominance condition of its Hessian matrix. For further details, see Appendix 5.2.3. ∎

The following corollary gives an expression of the variance-covariance matrix of Theorem 2 for the practical implementation:

Corollary 1.

Under our assumptions, the variance-covariance matrix is given by:

with

and the gradient is taken at point ; furthermore, the Hessian matrix is given by:

Proof.

See Appendix 5.2.4 for further details. ∎

4 Application: the CIR process

We consider the following stochastic volatility model

| (13) |

where follows a log chi-squared distribution and a gaussian distribution. This can be also seen as a discrete version of the so called Heston model with independent noise between the log-returns and its volatility . Here, we further assume that the variance process is greater than zero. To ensure this condition, we make the following assumption:

which is known as the Feller condition (see [Cox et al., 1985]) and implies that the variance process is ergodic and -mixing. Furthermore, the stationary distribution for this process is the gamma distribution (see [Genon-Catalot et al., 1999]).

4.1 Minimum contrast estimator

In this case, the functions , and are given by:

with . Using the Fourier transform of the Gamma and the log chi-squared density, we have

with the expectation of the logarithm of a chi-squared random variable, i.e. (see [Abramowitz and Stegun, 1992] and Appendix 5.3 for the expression of the Fourier transform). Next, the Fourier transform of is given by

with , . Finally, the -norm of is given by:

where corresponds to the Gamma function given by .

Proof.

See Appendix 5.3. ∎

Hence, the M-estimator solves:

| (14) |

where:

4.2 Others methods

Particle filters : EKF, APFS, APF and KSAPF. For the comparison with our contrast estimator given in (14), we use the following methods: the Extended Kalman Filter (EKF), the Auxiliary Particle filter (APF), the Auxiliary Particle filter with static parameter (APFS) and the Kernel Smoothing Auxiliary Particle filter (KSAPF). We refer the reader to [Reif et al., 1999], [Pitt and Shephard, 1999], [Doucet et al., 2001] and [Liu and West, 2001] for a complete revue of these methods.

In order to estimate the parameters with these methods, for the EKF, APF and KSAPF estimators we use the Kitagawa and al.’s approach (see [Doucet et al., 2001] chapter 10 p.189) in which the parameters are supposed time-varying: where is a centered Gaussian random with a variance matrix supposed to be known. Hence, we consider the augmented state vector where is the hidden state variable and the unknown vector of parameters. Furthermore, for the numerical part we call APFS an Auxiliary Particle filter without time-varying parameters.

The MCEM. From a theoretical point of view, the MLE is asymptotically efficient. However, in practice since the states are unobservable and since the model (13) is non Gaussian, the likelihood is untractable. We have to use numerical methods to approximate it. In this section, we illustrate the MCEM estimator which consists in approximating the likelihood and applying the Expectation-Maximisation algorithm introduced by Dempster [Dempster et al., 1977] to find the parameter .

4.3 Numerical Results

In this section we present some Monte Carlo simulations using the model (13). For the analysis we consider the following “true parameter” which is consistent with empirical applications of daily data (see [Do, 2005]). Thus, we have sampled the trajectory of the , and conditionally to the trajectory, we have sampled the variables with a variance noise 222 For the simulation (see Appendix 5.3) we take with and where .

The numerical illustration goes as follows: we work with a number of observations equal to , we first compare all the methods proposed in term of computing time, then we run estimates for each method and we compare the performance of our estimator with others methods by computing the Mean Square Error (MSE) defined as:

| (15) |

where corresponds to the dimension of the vector of parameters.

Then, we illustrate the statistical properties of our contrast estimator, by computing the confidence intervals for different number of observations. Finally, we study the influence of the signal noise ratio since the performance of our estimator depends on the regularity of and (see Remark 2).

For particles methods, we take a number of particles equal to . Note that for the Bayesian procedure (APF, APFS and KSAPF) we need a prior on , and this only at the first step. The prior for is taken to be the Uniform law and conditionally to the distribution of is its stationary law:

For the KSAPF, we take a bandwidth and for the APF we take a matrix with the identity matrix in (see Section 4.3.1 for the definition of the matrix ).

4.3.1 Computing time

| APF | KSAPF | APFS | EKF | Contrast | MCEM | |

|---|---|---|---|---|---|---|

| CPU (sec) | 105.1695 | 93.8846 | 192.2166 | 0.2 | 20.4074 | 217430 |

This comparison illustrates the numerical complexity of the MCEM. Therefore, in the following, we only compare our contrast estimator with the particles estimators.

4.3.2 Parameter estimates

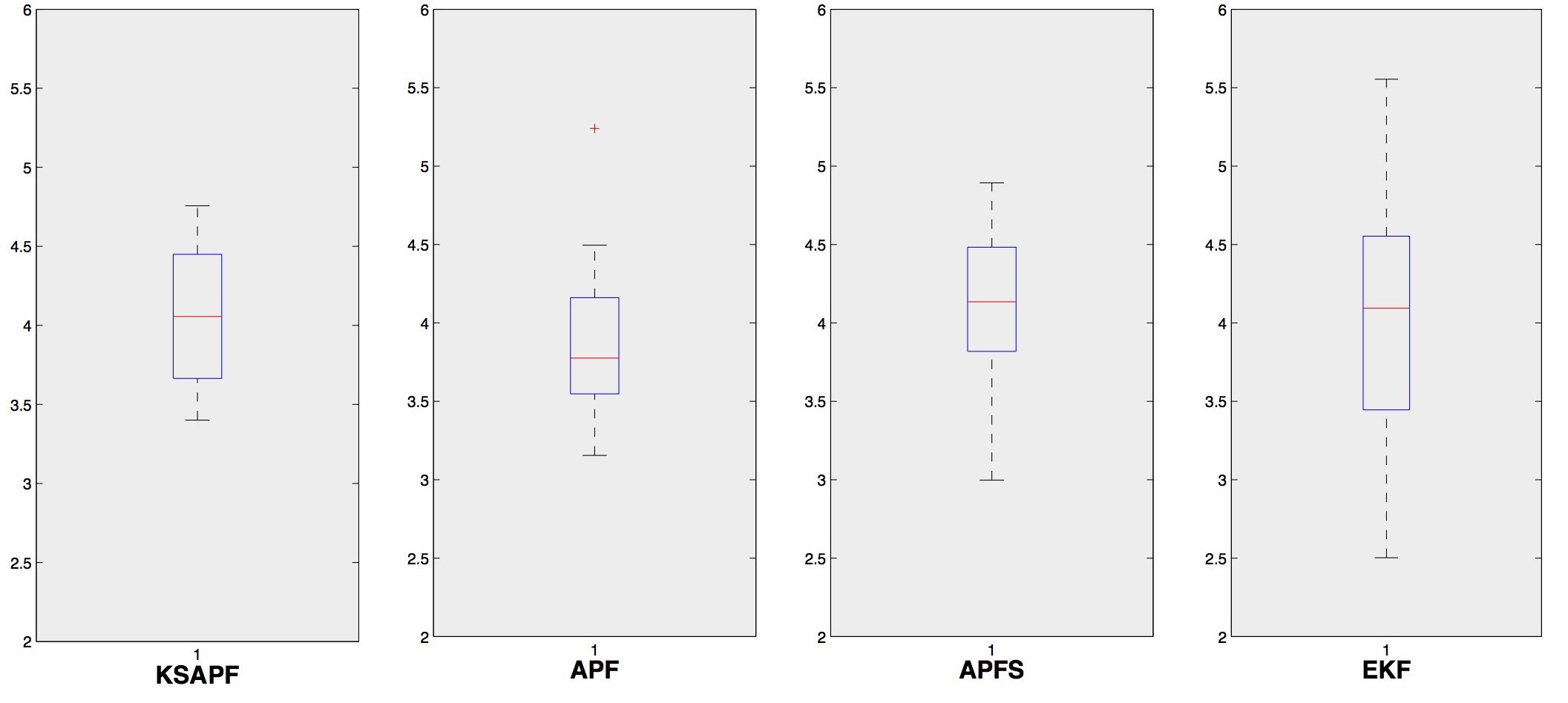

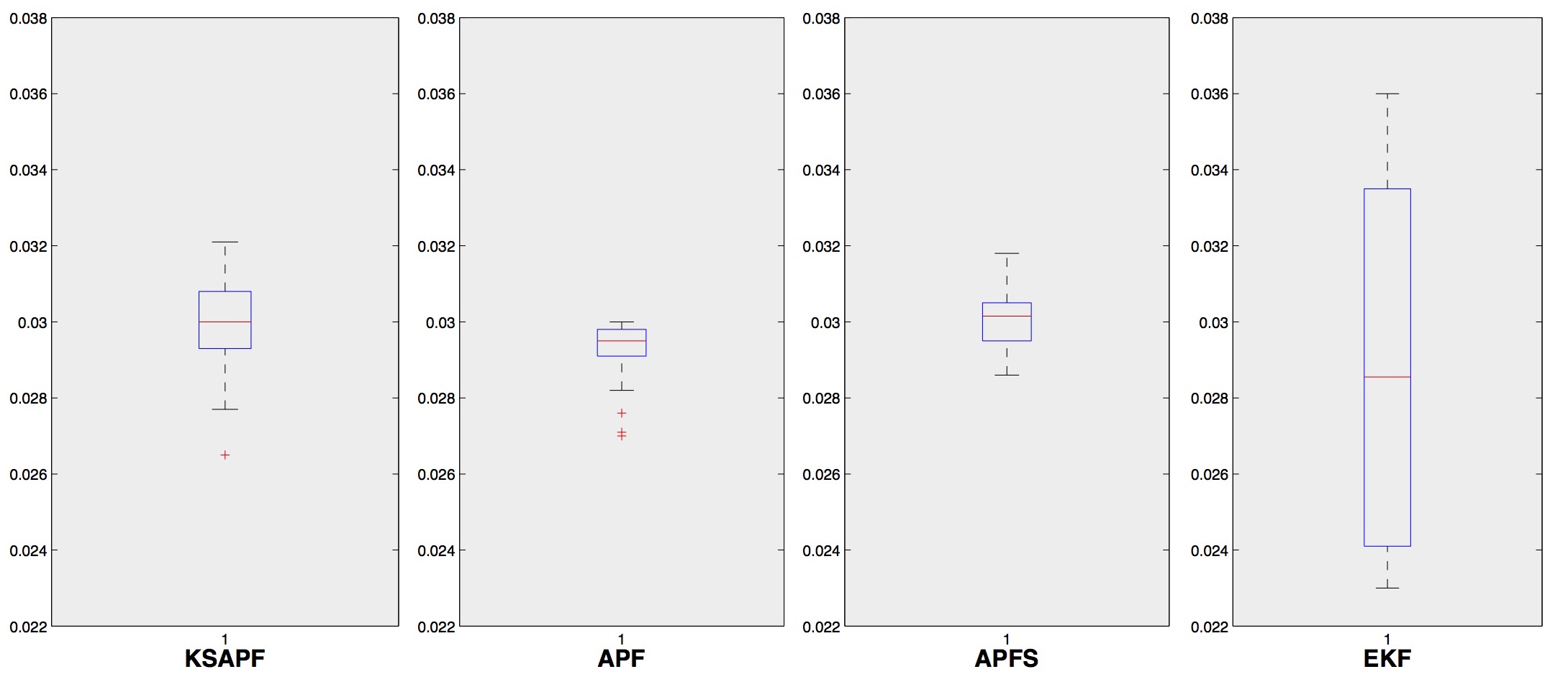

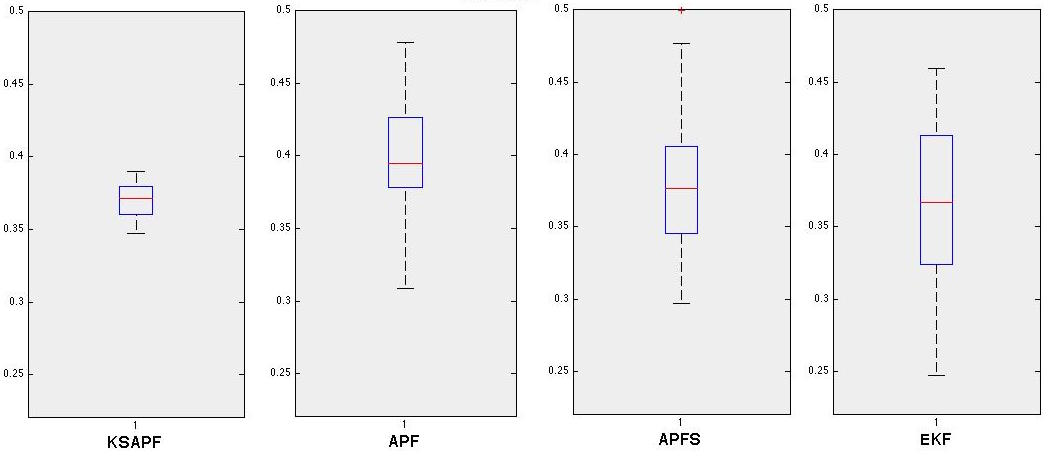

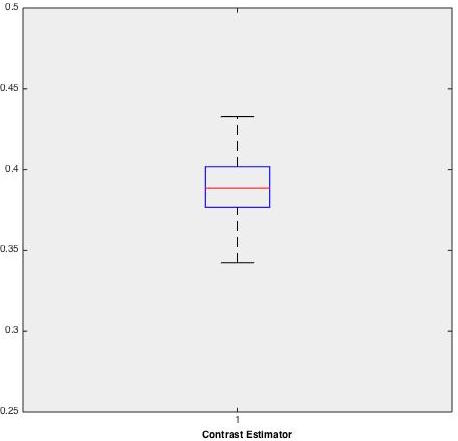

We illustrate by boxplots the different estimates (see Figures [1] up to [3]). In Table [2], we compute the MSE defined in (15) for each method and with a number of MC equal to and the CPU for a number of observations (see Table [1]).

We note that for all parameters, the EKF estimator is very bad since the stochastic volatility model (13) is strongly nonlinear, and its corresponding boxplots have the largest dispersion meaning that this filter is not stable and not appropriated to estimate this model. Among particle filters, the KSAPF and the APF are the best estimators although the dispersion is huge for the mean reversion parameter and the volatility parameter .

Besides, the APFS is less efficient than the others particle filters. Our estimator is stable and performs the others when one compare the MSE. From a computational point of view, all particles filters have an equivalent CPU. Our contrast estimator is fast and its implementation is straightforward and the MSE is the smallest (see Table [1]).

‘

| APF | KSAPF | APFS | EKF | Contrast | |

|---|---|---|---|---|---|

| MSE | 0.189 | 0.166 | 0.205 | 0.43 | 0.124 |

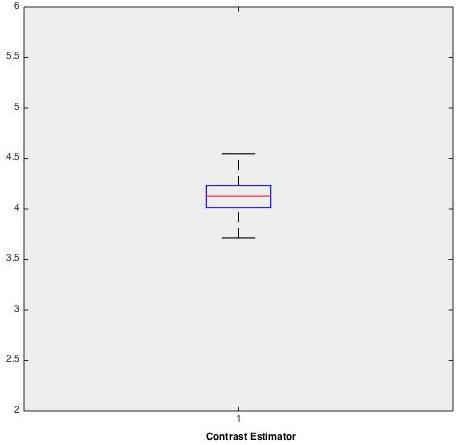

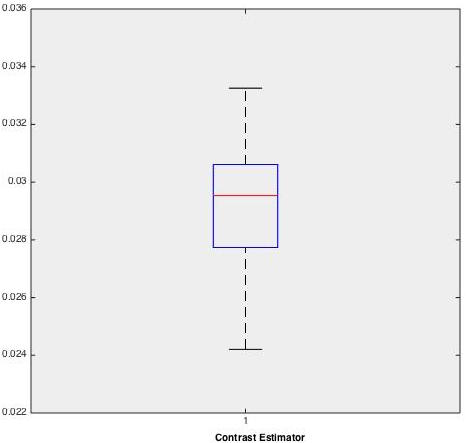

4.3.3 Confidence Interval of the minimum contrast estimator

To illustrate the statistical properties of our contrast estimator, we compute the confidence intervals with the confidence level equal to for estimators. The coverage corresponds to the number of times for which the true parameter belongs to the confidence interval. The results are illustrated in Figure [4]. We note that the coverage converges to for a small number of observations and as expected, the confidence interval decreases with the number of observations. Note that of course a MLE confidence interval would be smaller since the MLE is efficient but the corresponding computing time would be huge (see Table [1]).

4.3.4 Ratio signal-noise for the contrast estimator

We denote by the ratio signal-noise and in Table (3) we compare the MSE for different and different number of observations for the contrast estimator. We note that the MSE decreases with the number of observations and is smaller for small ratio-signal-noise. As explained in Section 3.1 and see [Comte et al., 2010] for more details, the rate of convergence of our approach depends on the regularity of the noise density . And, in particular, the smoother the noises are, the slower the rate of convergence is. For the CIR model, the density of the noises and the function are ordinary smooth, so we are in a favourable case.

| Mean( | Mean( | Mean( | MSE | |

|---|---|---|---|---|

| and | 0.0315 | 3.88 | 0.401 | 0.14 |

| and | 0.0303 | 3.89 | 0.405 | 0.16 |

| and | 0.0312 | 3.76 | 0.401 | 0.11 |

| and | 0.0308 | 3.83 | 0.41 | 0.18 |

4.4 Summary and Conclusions

In this paper we have proposed a new method to estimate hidden nonlinear diffusion process. This method is based on a deconvolution strategy and leads to consistent and asymptotically normal estimator. We have numerically studied the performance of our estimator for the CIR process widely used in many domains and we were able to construct confidence interval (see Figure [4]). As the boxplots [1] up to [3] show, only Contrast, APF, and KSAPF estimators are comparable. Indeed EKF and APFS estimators are biased and their MSE are bad, especially for the EKF method since the CIR process is nonlinear. Furthermore, if one compares the MSE of the particle filters, the KSAPF estimator is the best method. Among particles filters, it is clearly known that the APFS is less efficient than the APF filter since the parameters are not time-varying and so the only randomness is made at the first step by the prior law and not in each propagation step.

Then, the Contrast, APF, and KSAPF methods lead to unbiased and not so much varying estimator. We emphasize that our estimator performs the others in a MSE aspect (see Table [1]). Most importantly, our estimator can be constructed without any arbitrary parameters choice, is straightforward to implement, fast and allows to construct confidence interval.

References

- [Abramowitz and Stegun, 1992] Abramowitz, M. and Stegun, I. A., editors (1992). Handbook of mathematical functions with formulas, graphs, and mathematical tables. Dover Publications Inc., New York. Reprint of the 1972 edition.

- [Comte et al., 2010] Comte, F., Lacour, C., and Rozenholc, Y. (2010). Adaptive estimation of the dynamics of a discrete time stochastic volatility model. J. Econometrics, 154(1):59–73.

- [Comte et al., 2006] Comte, F., Rozenholc, Y., and Taupin, M.-L. (2006). Penalized contrast estimator for adaptive density deconvolution. Canad. J. Statist., 34(3):431–452.

- [Comte and Taupin, 2007] Comte, F. and Taupin, M.-L. (2007). Adaptive estimation in a nonparametric regression model with errors-in-variables. Statist. Sinica, 17(3):1065–1090.

- [Cox et al., 1985] Cox, J. C., Ingersoll, Jr., J. E., and Ross, S. A. (1985). A theory of the term structure of interest rates. Econometrica, 53(2):385–407.

- [Dedecker et al., 2007] Dedecker, J., Doukhan, P., Lang, G., León R., J. R., Louhichi, S., and Prieur, C. (2007). Weak dependence: with examples and applications, volume 190 of Lecture Notes in Statistics. Springer, New York.

- [Dempster et al., 1977] Dempster, A. P., Laird, N. M., and Rubin, D. B. (1977). Maximum likelihood from incomplete data via the EM algorithm. J. Roy. Statist. Soc. Ser. B, 39(1):1–38. With discussion.

- [Do, 2005] Do, B. (2005). Estimating the Heston stochastic volatility model from option prices by filtering. A simulation exercise.

- [Doucet et al., 2001] Doucet, A., de Freitas, N., and Gordon, N., editors (2001). Sequential Monte Carlo methods in practice. Statistics for Engineering and Information Science. Springer-Verlag, New York.

- [El Kolei, 2013] El Kolei, S. (2013). Parametric estimation of hidden stochastic model by contrast minimization and deconvolution. Metrika, 76(8):1031–1081.

- [Fan et al., 1990] Fan, J., Truong, Y. K., and Wang, Y. (1990). Nonparametric function estimation involving errors-in-variables.

- [Genon-Catalot et al., 1999] Genon-Catalot, V., Jeantheau, T., and Laredo, C. (1999). Parameter estimation for discretely observed stochastic volatility models. Bernoulli, 5(5):855–872.

- [Hansen and Horowitz, 1997] Hansen, B. E. and Horowitz, J. L. (1997). Handbook of econometrics, vol. 4 robert f. engle and daniel l. mcfadden, editors elsevier science b. v., 1994. Econometric Theory, 13(01):119–132.

- [Hayashi, 2000] Hayashi, F., editor (2000). Econometrics. Princeton University Press, Princeton NJ.

- [Heston, 1993] Heston, S. L. (1993). A Closed-Form Solution for Options with Stochastic Volatility with Applications to Bond and Currency Options. Review of Financial Studies, 6(2):327–43.

- [Hull and White, 1990] Hull, J. and White, A. (1990). Pricing interest-rate-derivative securities. Review of Financial Studies, 3(4):573–92.

- [Jones, 2004] Jones, G. L. (2004). On the Markov chain central limit theorem. Probab. Surv., 1:299–320.

- [Liu and West, 2001] Liu, J. and West, M. (2001). Combined parameter and state estimation in simulation-based filtering. in arnaud doucet, nando de freitas, and neil gordon, editors. Sequential Monte Carlo Methods in Practice.

- [Newey and McFadden, 1994] Newey, W. K. and McFadden, D. (1994). Large sample estimation and hypothesis testing. In Handbook of econometrics, Vol. IV, volume 2 of Handbooks in Econom., pages 2111–2245. North-Holland, Amsterdam.

- [Pitt and Shephard, 1999] Pitt, M. K. and Shephard, N. (1999). Filtering via simulation: auxiliary particle filters. J. Amer. Statist. Assoc., 94(446):590–599.

- [Reif et al., 1999] Reif, K., Günther, S., Yaz, E., and Unbehauen, R. (1999). Stochastic stability of the discrete-time extended Kalman filter. IEEE Trans. Automat. Control, 44(4):714–728.

- [Taylor, 2005] Taylor, S. (2005). Financial returns modelled by the product of two stochastic processes, a study of daily sugar prices., volume 1, pages 203–226. Oxford University Press.

5 Appendix

5.1 The contrast function

5.2 Proofs

For the reader convenience we split the proof of Theorems 1 and 2 into three parts: in Subsection 5.2.1, we give the proof of the existence of our contrast estimator defined in (10). In Subsection 5.2.2, we prove the consistency, that is, the Theorem 1. Then, we prove the asymptotic normality of our estimator in Subsection 5.2.3, that is, the Theorem 2. The Subsection 5.2.4 is devoted to Corollary 1.

Recall from Remark 1 that we only made the proof for the function defined by (2) in Definition 1 and we refer to [El Kolei, 2013] for the proof in the case (1) of Definition 1.

5.2.1 Proof of the existence and measurability of the M-Estimator

By assumption, the function is continuous. Moreover, and then are continuous w.r.t . In particular, the function is continuous w.r.t , for . Hence, the function is continuous w.r.t. belonging to the compact subset . So, there exists that belongs to such that:

5.2.2 Proof of the Consistency

For the consistency of our estimator, we need to use the uniform convergence given in the following Lemma. Let us consider the following quantities:

where is real function from with value in .

Lemma 1.

Uniform Law of Large Numbers (ULLN)(see [Newey and McFadden, 1994] for the proof.)

Let be an ergodic stationary process and suppose that:

-

(1)

For all , is continuous and for all , is measurable.

-

(2)

There exists a function (called the dominating function) such that for all and . Then:

Moreover, is a continuous function of .

By assumption for all , is continuous and for all , is measurable which implies the continuity and the measurability of the function on the compact subset . Furthermore, the local dominance assumption (A8) implies that is finite. Indeed,

with the function defined in (2) in Definition 1.

As is continuous on the compact subset , is finite. Therefore, is finite if is finite. Lemma 1 gives us the uniform convergence in probability of the contrast function: for any ,

Combining the uniform convergence with Theorem 2.1 p. 2121 chapter 36 in [Hansen and Horowitz, 1997] yields the weak (convergence in probability) consistency of the estimator.∎

5.2.3 Proof of the asymptotic normality

Consider the model (1) under the assumptions

A0-A7. The proof of the asymptotic normality

results from assumptions A8-A11 is a

straighforward application of [Hayashi, 2000] (Propostion 7.8. p.

472 and [Jones, 2004]). Furthermore, for the CLT, we need to recall some mixing properties (we refer the reader to [Dedecker et al., 2007] for a complete revue of mixing processes).

Let be a Markov transition kernel on a general space and let denotes the step Markov transition corresponding to . Then, for and a measurable set :

Let be a nonnegative function and be a nonnegative decreasing function such that:

where denotes the total variation norm.

Remark 4.

is geometrically ergodic if holds with for some . is uniform ergodic if holds with bounded and for some . is polynomial ergodic of order where if holds with .

The proof of the asymptotic normality is based on the following Lemma:

Lemma 2.

[see [Hayashi, 2000] and [Jones, 2004] for the proof.]

Suppose that the conditions of the consistency hold. Suppose further that:

-

(1)

is -mixing.

-

(2)

(Moment condition): for some and for each

.

-

(3)

Assumption holds such that and satisfies with defined in (2).

-

(4)

(Hessian Local condition): for some neighbourhood of and for

Proof.

It just remains to check that the conditions (2) and (4) of Lemma 2 hold under our assumptions.

Moment condition:

as the function is twice continuously differentiable w.r.t , for all , the application is twice continuously differentiable for all and its first derivatives are given by:

By assumption, for each , , therefore one can apply the Lebesgue differentiation Theorem and Fubini’s Theorem to obtain :

| (16) |

Then, for some :

| (17) | |||||

where and are two positive constants. By assumption, the function is twice continuously differentiable w.r.t . Hence, is continuous on the compact subset and the first term of equation (17) is finite. The second term is finite by the moment assumption (A9).

Hessian Local dominance:

for , , the Lebesgue differentiation Theorem gives:

and, for some neighbourhood of :

The first term of the above equation is finite by continuity and compactness argument and the second term is finite by the Hessian local dominance assumption (A10).

∎

5.2.4 Proof of Corollary 1

By replacing by its expression (16), we have:

Furthermore, by Eq.(1) and by independence of the centered noise and , we have:

Using Fubini’s Theorem and Eq.(1) we obtain:

so that

| (18) | |||||

Hence,

where

By using Eq.(18) and the stationary property of the , one can replace the second term of the above equation by:

Furthermore, by using Eq.(1) we obtain:

| (19) | |||||

| (20) | |||||

| (21) |

By independence of the centered noise, the term (19), (20) and (21) are equal to zero. Now, if we use Fubini’s Theorem we have:

| (22) |

Hence, the covariance matrix is given by:

Finally, we obtain: with and .

Expression of the Hessian matrix : We have:

| (23) |

For all in , the application is twice differentiable w.r.t on the compact subset . And for :

and for :

5.3 M-estimator using the example in Section 4

Expression of :

consider the random variable with where is standard Gaussian random variable, and . The Fourier transform of is given by:

Using a change of variable , we get:

Then

The CIR process:

taking that and has a (log-) Chi-squared probability density function, if the Feller’s condition holds true () and , then the volatility process is stationary ergodic and . The stationary distribution is the gamma distribution (see [Genon-Catalot et al., 1999]). On the other hand, the functions , and are given by:

where and , .

Therefore

After replacing by , we obtain:

It follows that for all , the squared norme of is given by:

where . Finally, using the non-centered moments of a Gamma-distributed random variable, , we get:

and

and the expression of the contrast function (14) is obtained. It is worth noting that the function defined in Definition 1 must be approximated numerically by using standard quadrature methods or Fast Fourier Transform.

5.3.1 Proof of Theorems 1 and 2 for the CIR process

Mixing property: under the Feller’s condition, the volatility process is -mixing and so -mixing by using the strong Markov property.

Regularity conditions: for the CIR process, the function is given by the following polynomial function with , and for all this function is smooth w.r.t. . Hence, it remains to prove the moment condition and the local dominance to apply Theorem 2.

Since the function is polynomial w.r.t belonging to the compact subset , all the derivatives exist and in particular and are finite. Furthermore, by combining the compactness argument and as the Fourier transform satisfies (see [Fan et al., 1990]):

which means that is ordinary-smooth in its terminology, we obtain:

.