Model-Free Approaches to Discern Non-Stationary Microstructure Noise and Time-Varying Liquidity in High-Frequency Data111The authors thank the referees for valuable suggestions and insights which make significant improvements. The authors also benefited much from discussions with Yingying Li, Xinhua Zheng, Yoann Potiron, Markus Bibinger. This research was funded by National Science Foundation Grant DMS 14-07812. All comments are gratefully welcomed.

Abstract

In this paper, we provide non-parametric statistical tools to test stationarity of microstructure noise in general hidden Itô semimartingales, and discuss how to measure liquidity risk using high-frequency financial data. In particular, we investigate the impact of non-stationary microstructure noise on some volatility estimators, and design three complementary tests by exploiting edge effects, information aggregation of local estimates and high-frequency asymptotic approximation. The asymptotic distributions of these tests are available under both stationary and non-stationary assumptions, thereby enable us to conservatively control type-I errors and meanwhile ensure the proposed tests enjoy the asymptotically optimal statistical power. Besides, it also enables us to empirically measure aggregate liquidity risks by these test statistics. As byproducts, functional dependence and endogenous microstructure noise are briefly discussed. Simulation with a realistic configuration corroborates our theoretical results, and our empirical study indicates the prevalence of non-stationary microstructure noise in New York Stock Exchange.

Keywords: Microstructure, High-Frequency Tests, Statistical Powers, Stable Central Limit Theorems, Non-Stationarity, Volatility, Liquidity

JEL classification: C12, C13, C14, C58

1 Introduction

The introduction of high-tech trading mechanisms into markets, for example, electronic communication networks (ECNs) and other electronic trading platforms, provides an opportunity for speculators and market makers to take advantage of speed in trading and market making, and this technological innovation also brings new regulatory challenges. The subsequent high-frequency trading results in a huge amount of high-frequency transaction and quotation data, which in particular opens two potential gates for research in theoretical and empirical asset pricing: one is estimation methodology using high-frequency data, since practitioners and researchers can get access to the big data and estimate variables of interest with greater accuracy; the other is a “frog eyes’ view” on market microstructure, since low-latency data offers a valuable chance to investigate trading behaviors with a higher resolution than ever before.

Correspondingly, this paper’s contributions to the literature are twofold: i) one is stationarity test of microstructure noise, we study the estimation problem when using high-frequency data with non-stationary noises, and then test non-stationarity in microstructure noise via several complementary model-free approaches; ii) the other one is on empirical market microstructure, since the microstructure noise can capture some information about market quality and liquidity, we estimate noise levels as measures of time-varying bid-ask spreads, risk aversions of market participants, etc., and detect short-term liquidity variations.

1.1 Literature review

The high-frequency finance practice motivates two clearly distinct and closely related researches:

One is more accurate estimation in financial econometrics, to name a few but not all, the estimation of integrated volatilities, quadratic covariances, the activities of jumps, the leverage effects, the volatility of volatility, the lead-lag effect. This stream of research started from j94, jp98 from the perspective of stochastic calculus, and fn96, e00, z01, abdl01, bs02 in the context of econometrics. Now, the high-frequency financial econometrics has already developed into a considerably influential research field with numerous prominent scholars and there are already monographs on this area: js03, jp12 developed probabilistic tools for high-frequency financial data analysis, aj14 provided an excellent overview in econometric literature, h12 is a good account from a financial standpoint. There are also academic chapters concisely reviewing high-frequency financial econometrics: re10, mz12, j12.

The other one is the study of market microstructure. Low-latency data allows financial practitioners and researchers to look at the financial markets at a higher resolution level, for example, one can know the bid/ask dynamics within each second, one can also know the order flow through the limit order book. The market microstructure theory studies how the latent demand and latent supply of market participants are ultimately translated into prices by studying the specific market structure in detail. The cornerstone papers include gm85, k85, both of them are using (pesudo)444To say it “pseudo” because in the model considered in k85, the market maker does not aim to maximize their utility, instead his or her objective is only to guarantee market clearing. game-theoretical argument in information economics. More comprehensive books include o95, h07. However, when looking closely at the transaction or quotation prices, one can find that the price is no longer an Itô semimartingale, not even random walk. For this reason, according to market microstructure theory [o03], the semimartingale model in classical asset pricing theory [hp81, ds94] is not a photographic depiction of the real prices of financial assets, yet it is still a fairly good approximation to asset prices when the sampling frequency is relatively low, and that is the reason the literature suggests using at most 5-minute subsampling.

Some estimation methods for integrated volatility using noisy high-frequency financial data have already been well established: i) zma05 found the first consistent estimator (two-time scale realized volatility) using subsampling and averaging in the presence of i.i.d. market microstructure noise and z06 gave a multi-scale version with the optimal rate of convergence , lm07 discussed the robustness of TSRV to noise assumptions in general, kl08 generalized the TSRV to the model with endogenous and diurnal noise and put forward a modified version of TSRV which we shall use in this paper. Later, amz11 generalized the model to allowing correlated noises under stationary and strong-mixing conditions; ii) b08 provided a kernel-based estimator under the model in which the noise process is temporarily dependent and stationary and possibly linearly correlated with the latent Itô process, their inference is also robust to endogenous spacing; iii) j09 designed a generalized version of the pre-averaging approach [pv09], under a Markovian noise model which allows arbitrary fashion of noise but without correlation between noise and the latent process; iv) Motivated by the likelihood method from amz05, x10 established quasi-maximum likelihood method (QMLE) in the estimation of integrated volatility; v) bhmr14 developed the local generalized method of moments to estimate quadratic covariation using noisy high-frequency data.

Many estimators of integrated volatilities using high-frequency noisy data were developed under the assumption that the microstructure noise is stationary. However, the literature in empirical finance, such as ap88, h93, ab97, gjf99, has already shown in 1990s that markets exhibit systematic intra-day patterns. Therefore, allowing heteroskedasticity and non-stationary in microstructure noise in integrated volatility estimation is of particular importance in application. Particularly, kl08 used a parametric model to describe the diurnal pattern in microstructure noise. ay09 used the estimates of noise variance in high-frequency data to measure the market liquidity from June 1996 to December 2005. There is other related research in the literature, acd09 studied the changes in microstructure noise due to sampling frequency, bry13 derived the optimal sampling frequency in terms of finite-sample forecast mean squared error in linear forecast model with non-stationary microstructure noise.

1.2 Structure of this paper

Section 2 describes our model and assumptions; after showing non-stationarity effect on the two scale estimator, complementary statistical tests are designed to detect microstructure noise stationarity based on high-frequency asymptotics, the asymptotic distributions under both null and alternative hypotheses and their implications for testing are shown in section 3, 4, 5; section 6 introduces an aggregate measure of liquidity risk and studies its estimation problem; relation between volatility and variance of microstructure noise, as well as endogenous microstructure noise are discussed in section 7; section 8 and LABEL:empirical contain our simulation and empirical analysis; section LABEL:conclu concludes. Some proofs are given in the Appendix.

2 The model and assumptions

2.1 Model setup

Firstly, we have a filtered probability space on which a latent Itô semimartingale is adapted, and can be described by

| (1) |

where is the drift, is the spot volatility in financial terminology (for example, its dynamics can be described by Heston model [he93]); is a 1-dimensional Wiener process; is a jump process which is described in subsection 2.3.

Secondly, we have another filtered probability space on which the observable process is adapted. Then, we can define the market microstructure noise process 555Although the noise is immaterial outside the observation times, it does not harm to assume there exist such a noise process in continuous time., as the difference between the latent and observable processes:

| (2) |

besides we define

| (3) |

we call the “estimable latent process” because we can indeed estimate it from the actual observations via, for example, pre-averaging [pv09, j09, jpv10, mz16a]. It is natural to assume the process is an Itô semimartingale, for example, if we assume for some [lm07] then is an Itô semimartingale666The definition (3) suggests the possibility of our inability to recover the latent process from the noisy observations , since does not necessarily equal to . More strikingly, as later discussed, this allows correlation between the microstructure noise and the latent process.. Based upon , we can define a noise process of another form, which is not necessarily the difference between the observable process and the latent process , instead defined theoretically via

| (4) |

we call the “distinguishable noise”, which can be disentangled from the estimable latent process [br06b].

Thirdly, we have a Markov kernel to provide a connection between the processes and , namely , i.e., conditional on the whole latent process , there exists a probability measure on the space .

Thus, all the relevant process, either latent or observable, can be defined on the extended filtered probability space 777This model combines the features of the models in lm07 and jp12 (or j09, jpv10), and is endowed with a additional feature that ’s are not defined as the differences between the observations ’s and the latent values ’s but the differences between the observations ’s and the values we can actually recover which are ’s. where

| (5) |

Moreover, define

i.e., . By this definition, is also a stochastic process. Note that could depend on more than one latent random variables, i.e., it is possible that for each . In Section 4 and Section 6 regarding some behaviors in the presence of non-stationary microstructure noise, we pose specific restrictions on the process , and let it be an Itô diffusion, and use asymptotic properties to show asymptotically optimal power and measure liquidity in high-frequency data.

2.2 Observational notation

This subsection can be skipped at the first reading. Please be advised to go back to this subsection when encounter the observational notation in later sections.

Suppose we focus on a finite interval on which ultra-high frequency data is recorded. Define to be the finest time grid whence all the observations were obtained. Suppose we have observations after the reference starting point 0, then can be written as

| (6) |

We sometimes do sparse sampling, typically start from the -th observation and take one sample from every observations. Formally, we define sub-grids ’s indexed by for each :

| (7) |

To analyze the edge effect888The edge effect is a pervasive phenomenon in non-parametric high-frequency econometrics. Verbally stated, edge effect is “information phasing in and phasing out at the edges of time intervals”, which is caused by inhomogeneous usage of data. Although undesirable, this feature is inevitable in estimation. and the modified TSRV, we need more observational notation:

| (8) |

thus, we have and the following relationships

sometimes, we will also denote by the -th time point in a given grid , for example, , .999The time grids defined in (7) and (8) depend on the tuning parameter which should be more properly written as , however, the dependence on will be suppressed in the observational notation, for the sake of readability and notational ease. Nonetheless, it is important to keep this implicit dependence on in mind.

In order to define some of our tests in Section 4, we need to introduce some shrinking moving windows and local sampling grids. Later, we will partition the fixed time interval (in application, could be 5 business days or some longer periods) into (depends on and ) sub-intervals ’s, such that each contains observations, i.e. , and . We also let denote the shrinking sampling grid over , i.e., , , .

2.3 Assumptions

Beyond the model setup in subsection 2.1, we have to make the following identification assumption in order to achieve identifiability and estimability:

| (9) |

otherwise all the estimation methods will break down [j09]. Note that under the identification assumption (9), we have and are identical, and there is no correlation between noise and the latent process.

As a sum-up, the following assumptions will be needed for various results:

Assumption 1.

Diffusion part of Itô semimartingale. The underlying model is (1), , and are adapted, and are càdlàg processes and locally bounded.

Assumption 2.

Jumps of Itô semimartingale. with being a Poisson random measure on and being the predictable compensator of in the sense that is a local martingale for . One could write where is a -finite measure on .

Assumption 3.

Finite jumps of Itô semimartingale. On top of Assumption 2, assume a function on such that where .

Assumption 4.

Assumption 5.

Conditional independence. Conditional on the latent variable(s), the observations ’s at different times are independent, i.e., for . This assumption simplifies the proof substantially101010An interpretation of this assumption is that the market microstructure effects occurred at different times are independent if the market participants know the latent efficient prices..

Assumption 6.

Locally boundedness of microstructure effect. , and , , such that , when , .

Assumption 7.

Possibly irregular observational grid with shrinking mesh. The sampling times can be irregular, but independent of the latent process. The Mesh of the grid goes to zero, more specifically, .

Based on some of these assumptions, we provide results involving various modes of stochastic convergences. It is necessary to clarify our notation for these convergence modes: means convergence in probability, means convergence in law (convergence in distribution, weak convergence), means stable convergence in law111111The concept “ stable convergence in law” may appear unfamiliar for some readers, please refer to mz12 or chapter 2 in jp12 for definition..

3 Testing stationarity/non-stationarity: the first test

In this article, we are considering testing the null hypothesis that the market microstructure noise is stationary:

and we concern the following questions:

-

•

Could we find any non-parametric test to tell the stationarity of microstructure noise?

-

•

Is any stationarity test valid in terms of controlling type-I error?

-

•

Is it asymptotically optimal in that its statistical power is the largest in asymptotics?

3.1 Prelude: non-stationarity and its remedy in estimation

In this subsection, we divert our focus to the estimation of integrated volatility (or continuous quadratic variation in the terminology of stochastic calculus) using high-frequency data contaminated by (possibly non-stationary) market microstructure noise. Our first test statistic was inspired by this.

Two-time scale realized volatility estimator (TSRV) [zma05] is the first consistent estimator of integrated volatility using noisy high frequency financial data. In this article, we define as the realized variance of process computed on a given sampling grid . The TSRV is defined as follows:

| (10) |

where, according to the notation introduced in subsection 2.2,

The optimal choice for the tuning parameter is 121212A caveat in application is to choose such that is sufficiently small, in order to reduce the edge effect., which results in the best possible order of TSRV. In the identical fashion, we can define , and .

The intuition behind the design of is sub-sampling and averaging: each is computed on a sparser grid hence mitigate the microstructure effect, hence their average should be more closer to ; the second term is a good proxy to the noise variance, hence it is to offset the bias due to the noise in .

The TSRV was originally designed under the setting where microstructure noises are stationary; however, under non-stationary microstructure noises, TSRV has a bias term produced by edge effect due to the following lemma:

From Lemma 1, we can see the noise in each time point does not contribute equally to the bias in the averaged realized variance . In the first and last sample points, the conditional second moments of noises are multiplied by the factor , in contrast, the conditional second moments of noises in the middle of the sample points are multiplied by the factor . However, the noise correction term in (10) acts as if ’s all have the same contribution to the noise component in . The modification to the TSRV and the first two tests are motivated by the inhomogeneity of utilization of information at the two edges of the time interval .

To the best of our knowledge, kl08 is the first study which considered the edge effect in TSRV due to the non-stationary microstructure noise, and they redefined the TSRV by where

under a parametric model which incorporates the diurnal and endogenous measurement error.131313The model upon which kl08 was based is where , i.i.d., . In the following, we used this design to attack the non-stationarity problem under the general hidden Itô semimartingale model given in Section 2.

In this paper, we call the new TSRV consisting of the modified version of realized variance in kl08 as “sample-weighted TSRV”, which is defined as

The sample-weighted TSRV enjoys the following asymptotic property under the general model in Section 2:

Theorem 1.

The theorem tells us the sample-weighted TSRV in non-stationary noise setting enjoys the same asymptotic property as those of traditional TSRV in stationary noise setting [zma05, lm07, amz11], in that the asymptotic distribution as well as the convergence rate remains unchanged; in other words, the asymptotic property of the sample-weighted TSRV is invariant with respect to non-stationary market microstructure noise.

3.2 The first test

Assuming is true, both of the asymptotic distributions of the original TSRV and the sample-weighted TSRV are mixed normals. So, the asymptotic distribution of the difference between two different versions (after proper scaling) is also a mixed normal. Therefore, we can test the null based on the asymptotic behavior of their difference , note that

| (13) |

The first test statistic is designed as follows:

| (14) |

where is the sample quarticity based on the observation ’s.

Our first test statistic has the following asymptotic property:

Theorem 2.

We use this result to test the stationarity of the market microstructure noise in subsection LABEL:empitest (Figure LABEL:EmpriTest1).

The denominator of the test statistic (15), namely is actually an estimator of . This is formally introduced in (17), which is not only used in the first test statistic but also used in the second test statistic in subsection 4.2. It is interesting in its own right, hence we here give the result:

Remark 1.

Based on Lemma 2, if the noise is stationary, , so a natural estimate of is

| (17) |

Remark 2.

We now investigate the behavior of our first test statistic when microstructure noise is non-stationary. Since , hence

| (18) |

Since we assume local boundedness of noise variance, is finite almost surely, regardless of noise stationarity. From the proof in subsection LABEL:prfthm1, we know

| (19) |

where

| (20) |

Since in our setup, explodes when the noise is not stationary. Thus, the type-\@slowromancapii@ error of this test is asymptotically negligible.

Corollary 1.

Assume and are càdlàg processes141414The term “càdlàg” (French acronym of “continue à droite, limite à gauche”) describes the property of a function that is everywhere right-continuous and has left limits everywhere, for example, a Brownian motion (sample path are continuous almost surly), Lévy processes (countably many jump discontinuities). on with , being continuity points almost surly, additional we have the Assumption 1, 2, 5, 6, 7, and let , . When the noise process is non-stationary,

| (21) |

on the event that .

Remark 3.

The test statistic can disclose potential non-stationarity in the market microstructure noise via two edges of the mesh , and the middle of the mesh . We can show there are, in latter subsections, schemes which are able not only to reflect the heterogeneity between two edges and the middle, but also to capture almost all of the information about the non-stationarity in the data, however, inevitably with more computational cost. We will discuss these schemes in Section 4.

4 The second and third tests

4.1 The general idea

The second and third tests are designed as an attempt to effectively utilize all the information relevant to noise stationarity contained in the data, in contrast to the first test (see Remark 3). The basic idea of the second and third tests is to conduct local tests on sub-intervals and then combine evidences from all the local tests.

To straighten the idea, recall the observational notation in subsection 2.2, we partition the fixed time interval into sub-intervals ’s, such that each contains observations. Similar to the definition of the first test statistic, but instead of the whole interval , the second test uses local test statistic defined on a moving window of the form with a suitable window length (in terms of the number of subintervals ’s):

| (22) |

Then, we use the overlapping window to calculate the quantity , which depends on the process , the stage of statistical experiment , tuning parameter and , and a number :

| (23) |

Similarly, we also define a quantity based on non-overlapping windows:

| (24) |

4.2 The second test

We designed our second test statistic by

| (25) |

where

| (26) |

We have the following result in regard to the asymptotic property of :

Theorem 3.

We use this result to test the stationarity of the market microstructure noise in subsection LABEL:empitest (Figure LABEL:EmpriTest2).

We can also define another quantity based on non-overlapping intervals

Following from Theorem 3, the asymptotic property of can be derived.

Corollary 2.

Remark 4.

It is a little bit surprising when we compare Corollary 2 with Theorem 3, since the limiting mixed normals of and have the same asymptotic variance which can be consistently estimated by , though the convergence rate of the former is lower. However, the results only demonstrate the limiting behaviors. required less computation, while is more accurate in terms of asymptotic approximation because of its higher rate of convergence.

4.3 The third test

There is a moderate edge effect in the second test statistic (25) (coming from the first and the last observations). Motivated by Remark 3 regarding the first test statistic (14), we can design a complementary test statistic (defined by (30)) with the same asymptotic property with when the noise is stationary, yet has a smaller edge effect in finite sample. However, we should keep in our toolbox - although offers better approximation when noise is stationary, we will see has more statistical power as indicated in Figure 1.

4.4 Optimal statistical powers

How and behave when the noise is non-stationary determine their statistical powers. If the test statistics tend to be large when the microstructure noise is non-stationary, they can easily detect non-stationarity.

The behaviors of and largely indicate the behaviors of and . We investigate in this subsection the asymptotic behaviors of and when microstructure noise is non-stationary under a slightly strengthened setting, we need 2 more assumptions on top of those assumptions in subsection 2.3:

Assumption 8.

Regular sampling. The sample grid is equi-distant over the interval .

Assumption 9.

Noise variance process is Itô. is an Itô diffusion (in time):

| (32) |

where is locally bounded, optional and càdlàg, is a standard Brownian motion, is a locally bounded Itô diffusion.

As described in subsection 2.2, we partition the whole time interval into disjoint sub-intervals for such that in each sub-interval we have observations, particularly we have and , . Since Assumption 8 is assumed, we let .

Theorem 5.

Theorem 6.

Theorem 3 and 4 provide us the asymptotic distributions of and under the stationarity hypothesis, which aid us to control the type-\@slowromancapi@ error. On the other hand, Theorem 5 and 6 reveal asymptotic behaviors of and under the alternative hypothesis by respectively analyzing and . Since the moments of noise are locally bounded, and are always finite. Following Theorem 5, 6, we have the following corollary:

Corollary 3.

Recall the choices of tuning parameter, for , for and , their asymptotic powers attain the optimal. As in finite samples, has more statistical power than by a factor of magnitude ; is more powerful than by a factor of magnitude .

5 A user’s guide of stationarity tests

We currently have 3 complementary tests, namely , and , each test has its own advantages as well as disadvantages. In this subsection, we are going to discuss their strength and weakness, and how to choose the optimal test for different circumstances.

-

(1)

The first test divides the sample into 3 periods and compares the noise level in the middle with those on the edges. If we are interested in possible daily diurnal noise patterns, for example, let us test whether the noise level is higher in opening and closing trading hours, the best choice is to apply on 1-day high-frequency data. However, is not sensitive to local changes, for example, in case of a periodic change and the data sample covers several cycles, will likely misjudge the non-stationarity fact;

-

(2)

The second test uses moving local windows each containing observation, and compares noise levels in the edges and the middle of each local window; the third test also uses local windows but compares the noise level in one local widow with those in neighboring windows. Because they conduct test locally and aggregate local evidences, and are more powerful in detecting local noise changes which could probably ignore. However, if the noise transition goes very smoothly but there is a systematic paradigm shift on a global scale, and might lead to false stationarity conclusion;

-

(3)

As said in subsection 4.3, has a smaller edge effect than hence is more a accurate test under the null hypothesis; whereas enjoys larger statistical power (the lower right panel in Figure 1). The intuition is that by construction the focus of is too local although it results in the smaller edge effect, which turns into its disadvantage when the noise is non-stationary.

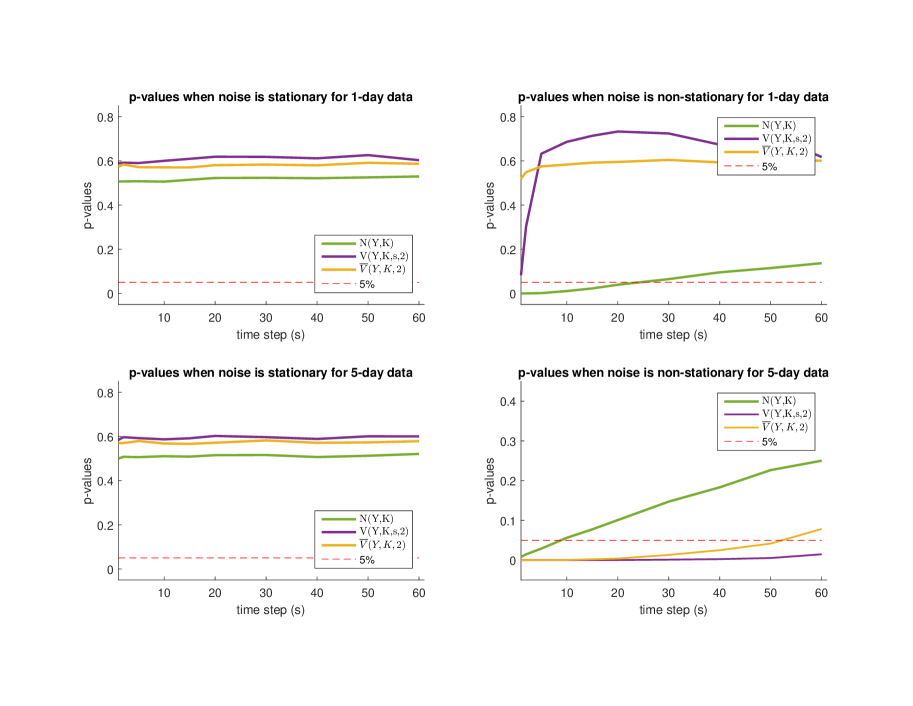

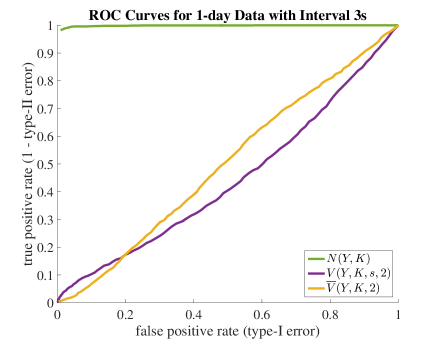

As a simulation comparison, Figure 1 shows averaged p-values computed from simulated 1-day/multi-day data with stationary/non-stationary noises. Figure 2 shows their ROC curves. The simulation configuration is described in subsection 8.1, and each p-values shown is the average of 3000 Monte Carlo samples.

These plots show some properties of the tests we proposed:

1. For type-I error, all the tests can control their type-I errors pretty well regardless of the time span of the data, in that can very accurately control its type-I error in finite samples, and are more conservative in the sense that their effective type-I error is smaller than specified;

2. For type-II error or statistical power, only performs satisfactorily on 1-day data, meanwhile, and are much better when applied to multi-day data in terms of their larger statistical powers and faster convergence rates. Consistent with Corollary 3, has a better statistical power in finite sample.

\floatfoot

\floatfoot

ROC curves show how type-II changes as type-I error varies. Once again, the ROC curves indicates that when microstructure noise exhibits a daily diurnal pattern, is optimal for 1-day data, is optimal for multi-day data.

As a summary, we list different considerations about the optimal choice of these tests in Table 1. We suggest some choices of the tuning parameters (, ) to balance various errors in the high-frequency approximation. Table 2 shows the convergence rates and statistical powers of our tests under the suggested tuning parameters.

| Test Statistics | |||

|---|---|---|---|

| type-\@slowromancapi@ error control | most accurate | least accurate | moderately accurate |

| Strength in detection151515Evaluated in terms of statistical power. | global change | local change | local change (suboptimal) |

| Length requirement | 1/multi-day data | multi-day data | multi-day data |

| Frequency requirement161616The minimal thresholds are expressed in terms of averaged time gap between consecutive observations. They are estimated from our simulation whose configuration is fairly realistic (subsection 8.1). | 20s/10s | 60s | 50s |

| Computational cost | relative small | relative large | relative large |

| — | — | ||

| rates under | |||

| magnitudes under |

6 Measuring aggregate liquidity risks

6.1 A notion of “aggregate liquidity risk”

On one hand, as the quadratic variation of over is a reasonable measure of the “aggregate” variation of the process . On the other hand, microstructure noise variance is a measure of market quality [h93], or more specifically, market liquidity [ay09]. Hence, it should not be utterly unreasonable to interpret as “aggregate liquidity risks”. In this section, we are going to define a notion of “aggregate liquidity risks” and provide an estimator with an associated CLT.

6.2 Estimating aggregated liquidity risk

Recall Theorem 6 and note that , is a consistent estimator of , i.e.

| (35) |

However, We can rewrite (34) as

depending the relation between the number of blocks and the number of observations within each block, we have different second-order properties. If we let , we have an unbiased central limit theorem for estimating . Otherwise, in case (or ), we have a CLT with a finite (or diverging) bias.

Corollary 4.

171717Corollary 4 in some sense is an extension of the “integral-to-spot device” in mz16a: for a semimartingale {} on , let , and , then under some regularity conditions (to guarantee standard stable convergence plus additional restriction on edge effects), as and , Define and . Under some regularity conditions, according to the “integral-to-spot device” in mz16a However, we do not know the true values of ’s in application, after swapping for , (36) Note that , Corollary 4 reveals the possible additional terms and provides the central limit theorem associated with (36). Upon choosing appropriately, the additional terms on the right side of (36) is zero and we have an unbiased central limit theorem.Remark 5.

Toward a better finite-sample performance, for example, to get a more accurate confidence interval for the aggregate liquidity risk, we suggest to use the estimate of

as the approximation to the finite-sample variance, in order to avoid the situation in which we underestimate the finite-sample variance and become overoptimistic about the accuracy of our estimate. The 95% confidence interval for our measure “aggregated liquidity risk” is

| (38) |

where

and .

7 Noise functional dependency and model extension

The law of microstructure noise is represented via a Markov kernel for each time , through which the second moment of the noise evolves according to a random function in time on the probability space . The random function could depend on various latent variables, and more generally the form of allows a wide range of correlation structures between the efficient price process and the microstructure noise. In this section, we discuss an elementary empirical evidence about the dependence of on and the implication of the violation of our identification assumption i.e. Assumption 4.

7.1 Regression: market microstructure noises and spot volatilities

In this subsection, we go beyond the recognition that the second moment of microstructure noise is evolving over time, document the dependence of on volatility . In doing so, we conduct time series linear regression of ’s on the latent variables ’s181818as16 provide a theoretical underpinning for the negative correlation between volatility and liquidity, equivalently, positive correlation between and : a higher volatility indicates a higher risk that arbitrageurs might take advantage of market makers’ previous orders to act against market makers; hence, it reduces the activities of liquidity provision.. We assume that the latent market microstructure noise variance and the latent volatility are correlated:

Assumption 10.

With probability 1, we have ,

| (39) |

where .

Since both and are unobservable, we need some preliminary estimates for both variables. Here, we use scaled sample-weighted TSRV and realized variance calculated from local samples to estimate spot volatilities ’s and local noise levels, respectively, i.e., and , where , , is the cardinality of . Then, we can conduct linear regression on these pairs of volatility-noise estimates ’s by ordinary least squares:

| (40) |

where is the number of observation in the small time interval , and denotes a component in the noise variance not captured by the volatility estimator . Besides, we use in the subscripts of estimators and to emphasize that the values of the estimators in (40) depend on the sample size , and the distribution of also depends on .

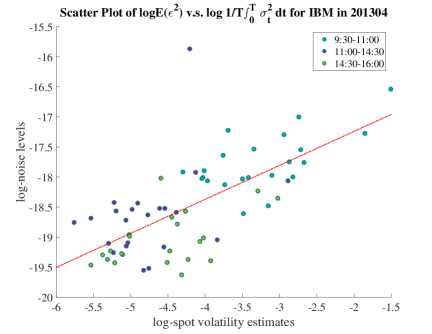

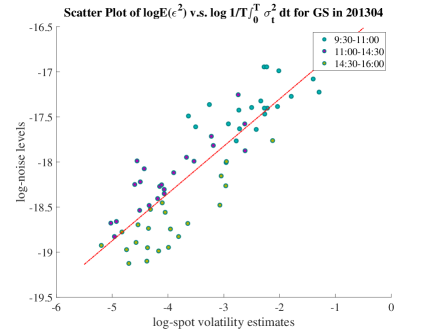

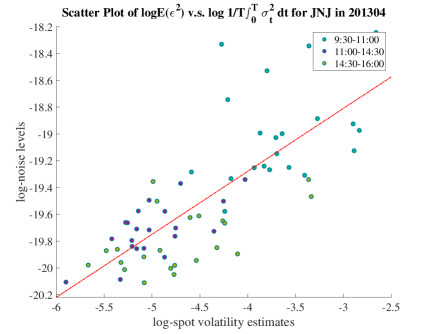

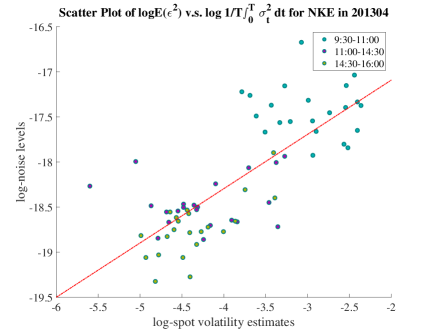

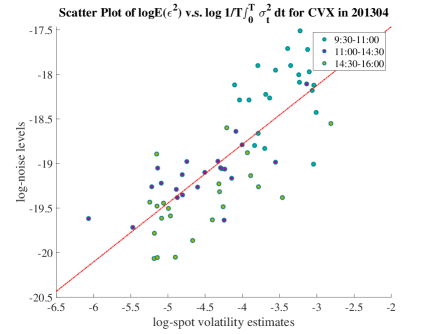

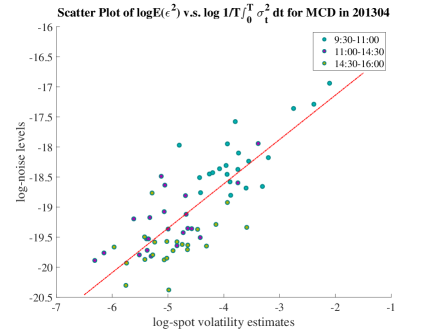

By lemma 3, if there is a linear relationship between the noise variance and the spot volatility, the regression (40) provides consistent estimates of linear coefficients. Figure 3 shows the least square regression plots for high-frequency transaction data in April, 2013 of 6 stocks: International Business Machines (IBM), Goldman Sachs (GS), Johnson & Johnson (JNJ), Nike, Inc. (NKE), Chevron Corporation (CVX), McDonald’s (MCD).

The time series regression and empirical analysis here are preliminary. One can investigate the statistical properties of this type of linear regression in more detail. Perhaps, there are non-linear relations. These issues will be addressed in our future research.

7.2 Model extension: endogenous noise

In our model, we allow arbitrary fashion of the noise process up to the time-varying Markov kernel plus the identification assumption (Assumption 4). As documented in j09, the identification assumption is restrictively strong. If one is interested in the stationarity of , our methods are valid regardless the identification assumption holds or not. However, if one is concerned about our methods will break down when the identification assumption is violated. Nevertheless, this extension is indispensable for empirically compatible modeling and it allows endogenous microstructure noise (noise which is correlated with the efficient price [hl06]).

Note that in subsection 2.1, conditioning on all latent variables, is a mean-zero random variable, i.e., since . However, the conditional mean of is not necessarily 0 since .

This observation enables us to, non-parametrically, introduce endogenous noise into our model. We can allow instantaneous/realized correlation between the latent process and the noise process . Although is not necessarily 0, we assume the unconditional mean is zero, then calculation shows

[j09] assumed , so there is no endogenous noise in their model. However, as long as , there is correlation between the latent process defined by (1) and the noise process defined by (2).

An intuitive interpretation is that encodes some relevant information about the processes defined on the latent probability space if it is correlated with the latent random variables and . In contrast, is a pure noise and conveys no useful information about the latent processes, the correlation between and any latent random variable is zero. For this reason, we call “endogenous microstructure noise”, and call “exogenous microstructure noise”.

Remark 6.

When one tries to estimate the integrated volatility, the quantity which is actually estimated is , not necessarily the usually desired target . This is discussed by [lm07]. In contrast to [j09], we do not assume . In other words, in the case where , the integrated volatility is not identifiable; however, if we are satisfied with estimating , then we are able to introduce some conditional correlation between the efficient price and the microstructure noise.

One conceptual finding from the model extension is the informational content in microstructure noise with respect to the efficient price in financial term (or latent process in statistical term) which is modeled as an Itô semimartingale. The interpretation comes from market microstructure theory [o95, o03]. As in the classical asset pricing theory, we take the price as given and exogenous, and conduct trading and hedging strategies, portfolio allocation and risk management. But, the price discovery and price formation depend on the behaviors of market participants, no price will be produced without investment activities of various market participants. It is the balance between demand and supply from investors, it is the psychology of people in the market, it is the synthesis of microscopic effects of beliefs and behaviors of market participants, that determine the prices. Thus, the efficient price should be an endogenous process in the financial market. It is one of striking difference between asset pricing and market microstructure theory: the classical asset pricing theory assumes frictionless and competitive market in which people do not have to worry about the price impact and liquidity constraint. While, in market microstructure theory, the modelers need to look inside the “black box” of the trading processes, and take market making, price discovery, liquidity formation, inventory control, asymmetric information into account.

Since we consider the price as endogenous, which, for example, affected by transaction costs (like bid-ask spread), inventory control, discrete adjustment of price, lagged incorporation of new information, insider trading and adverse selection brought by asymmetric information, lack of liquidity caused by one or several of the factors mentioned above, the Itô process is merely an approximation to the efficient price observed at high-frequency, at which market microstructure effects manifest itself to such extent that the accumulated noise swamps the integrated volatility of the latent Itô process and the variation in microstructure noise dominates the total variance.

Therefore, it is reasonable (even indispensable) to extend our model to allow endogenous microstructure noise, at least from the viewpoint of microstructure theory, and for sake of realistic modeling at low-latency and millisecond level. This topic is not the focus of this paper; in-depth discussion and treatment on endogenous microstructure noise will be addressed in our future research.

8 Simulation

8.1 Simulation scenario

The configuration of our simulation design is

| (41) | |||||

| (42) | |||||

| (43) |

where , and are Poisson processes with parameters and respectively, the jump sizes satisfy and with . The stationary microstructure noise behaves as , whereas the non-stationary microstructure noises are distributed as

| (44) |

where and is the number of high-frequency observations in 1 business day. In (44), the noise variance of changes according to a U-curve, which means that the noise is of relatively higher levels around opening and closed hours. The U-curve is chosen such that the averaged noise variance within a day is . The noise conforms to the empirical feature that the variance of microstructure noise increases with the level of volatility [br06]. The parameters are chosen so that they are consistent with ay09:

parameters 0.03 -0.6 6 0.0016 0.004 parameters 6 0.16 0.5 12 -5 0.8 noise parameters 10 0.3

Furthermore, is sampled from the stationary distribution of Cox-Ingersoll-Ross process [cir85], i.e., so the unconditional mean of the volatility is . is chosen such that in average. We also adopted a random sampling scheme according to an inhomogeneous Poisson process where is averaged sampling duration and the trading intensity evolves periodically with being the length of 1 business day.

8.2 Simulation results

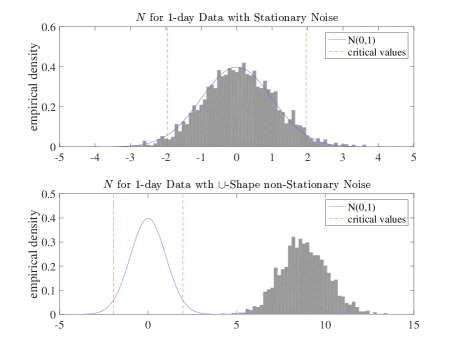

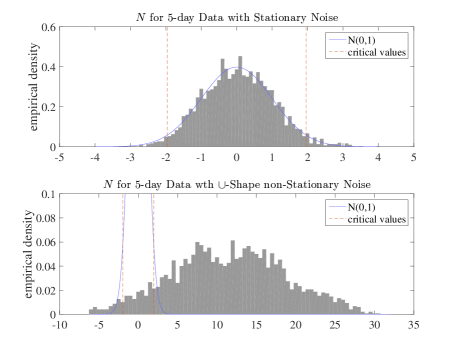

In Figure 4, LABEL:V and LABEL:Vbar, we show the simulation results of , and where is taken to be 1 business day (left panel in each figure) and 5 business days (right panel in each figure). For each test and each time span, the simulation is conducted in 2 different circumstances: stationary noise (upper picture in each column), U-shape noise (44) (lower picture in each column). The plots show various empirical densities function of our proposed tests against the density of . Each group of tests were computed from 3000 sample paths with averaged sampling interval 1 second.

\floatfoot

These plots show the empirical densities of when it applies to 1-day/5-day data with stationary/non-stationary noises. Compared the simulation of other tests, we can see converges faster to when microstructure noise is stationary. On the other hand, if the microstructure noise is non-stationary and exhibits daily diurnal pattern, is the best for 1-day data.