The Sorted Effects Method: Discovering Heterogeneous Effects Beyond Their Averages

Abstract.

The partial (ceteris paribus) effects of interest in nonlinear and interactive linear models are heterogeneous as they can vary dramatically with the underlying observed or unobserved covariates. Despite the apparent importance of heterogeneity, a common practice in modern empirical work is to largely ignore it by reporting average partial effects (or, at best, average effects for some groups).

While average effects provide very convenient scalar summaries of typical effects, by definition they fail to reflect the entire variety of the heterogeneous effects. In order to discover these effects much more fully, we propose to estimate and report sorted effects – a collection of estimated partial effects sorted in increasing order and indexed by percentiles. By construction the sorted effect curves completely represent and help visualize the range of the heterogeneous effects in one plot. They are as convenient and easy to report in practice as the conventional average partial effects. They also serve as a basis for classification analysis, where we divide the observational units into most or least affected groups and summarize their characteristics. We provide a quantification of uncertainty (standard errors and confidence bands) for the estimated sorted effects and related classification analysis, and provide confidence sets for the most and least affected groups.

The derived statistical results rely on establishing key, new mathematical results on Hadamard differentiability of a multivariate sorting operator and a related classification operator, which are of independent interest.

We apply the sorted effects method and classification analysis to demonstrate several striking patterns in the gender wage gap. We find that this gap is particularly

strong for married women, ranging from to between the and percentiles, as a function

of observed and unobserved characteristics; while the gap for never married women ranges

from to . The most adversely affected women tend to be married, do not have college degrees,

work in sales, and have high levels of potential experience.

Keywords: Sorting, Partial Effect, Marginal Effect, Sorted Effect, Classification Analysis, Nonlinear Model, Functional Analysis, Differential Geometry, Gender Wage Gap

Abstract.

The supplementary material contains 7 appendices with additional results and some omitted proofs. Appendix C introduces some notation. Appendix D includes a brief review of differential geometry. Appendix E gathers the proofs of the key mathematical results in Appendix A. Appendix F provides sufficient conditions for the -Donsker properties in Section 4. Appendix G extends the theoretical analysis to include discrete covariates. Appendices H and I report the results of 3 numerical simulations and an empirical application to the effect of race on mortgage denials, respectively.

1. introduction

In nonlinear and interactive linear models the partial (ceteris paribus) effects of interest often vary with respect to the underlying covariates. For example, consider a binary response model with conditional choice probability , where is a binary response variable, is a vector of covariates, is a distribution function such as the standard normal or logistic, and is a vector of coefficients. The partial or predictive effect (PE) of a marginal change in a continuous covariate with coefficient on the conditional choice probability is

which generally varies in the population of interest with the covariate vector , as varies according to some distribution, say . A common empirical practice is to report the average partial effect (APE),

as a single summary measure of the PE (e.g., \citeasnoun[Chap. 2]wooldridge:text), or to report effects for some groups (e.g., \citeasnounangrist2008mostly). However, the APE completely disregards the heterogeneity of the PE and may give a very incomplete picture of the impact of the covariates.

In this paper we propose complementing the APE by reporting the entire set of PEs sorted in increasing order and indexed by a ranking with respect to the distribution of the covariates in the population of interest. These sorted effects correspond to percentiles of the PE,

and provide a more complete representation of the heterogeneity of . We shall call these effects as sorted predictive or partial effects (SPE) by default, as most models are predictive.111When the underlying model has a structural or causal interpretation, we may use the name sorted structural effects or sorted treatment effects. We also show how to use the SPEs to carry out classifications analysis (CA). This analysis consists of classifying the observational units into most or least affected depending on whether their PEs are above or below some tail SPE, and then comparing the moments or distribution of the covariates of the most and least affected groups.

Heterogeneous effects also arise in the most basic linear models with interactions [oaxaca73, cox84]. Consider a conditional mean model for the Mincer earnings function:

where is log wage, is an indicator of gender (or race, treatment, or program participation), and is a vector of labor market characteristics. The vector is a collection of transformations of and , involving some interaction between and . For example, \citeasnounoaxaca73 used the specification . Then, the PE of changing to is

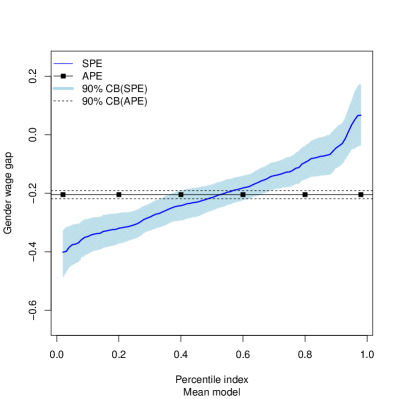

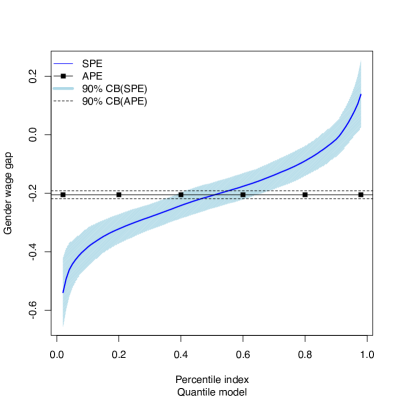

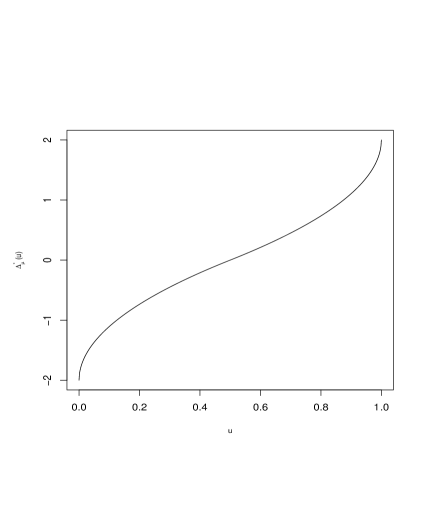

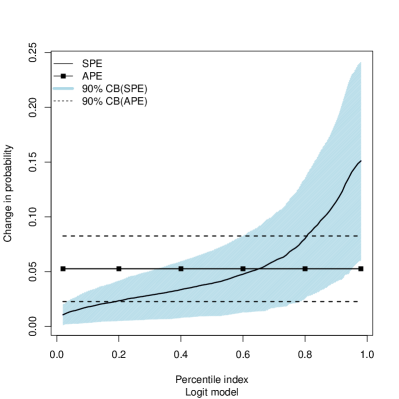

which is a measure of the gender wage gap conditional on worker characteristics. The function provides again a complete summary of the entire range of PEs. The left panel of Figure 1 illustrates the SPE of the conditional gender wage gap for women.

The SPE varies sharply from around to , and does not coincide with the average PE of . The PE is especially (negatively) large for women who have any of the following characteristics: married, low educated, high experience, and working on sales occupations – this follows from the classification analysis, where we compare the average characteristics of the subpopulations of women with covariate values such that is above the 90% percentile and below the 10% percentile. We refer the reader to Section 3 for a detailed discussion of this example.

The general settings that we deal with in this paper as well as the specific results we obtain are as follows: Let denote a covariate vector, denote a generic PE of interest, denote the distribution of in the population of interest, and denote the interior of the support of in this population. The SPE is obtained by sorting the multivariate function in increasing order with respect to . Using tools from differential geometry, we prove that this multivariate sorting operator is Hadamard differentiable with respect to the PE function and the distribution at the regular values of on . This key and new mathematical result allows us to derive the large sample properties of the empirical SPE, which replace and by sample analogs, obtained from parametric or semi-parametric estimators, using the functional delta method. In particular, we derive a functional central limit theorem and a bootstrap functional central limit theorem for the empirical SPE. The main requirement of these theorems is that the empirical and also satisfy functional central limit theorems, which hold for many estimators used in empirical economics under general sampling conditions. We use the properties of the empirical SPE to construct confidence sets for the SPE that hold uniformly over quantile indices. We also show under the same conditions that the empirical version of the objects in the classification analysis follow functional central limit theorems and bootstrap functional central limit theorems. We derive these result by establishing the Hadamard differentiability of a classification operator related to the multivariate sorting operator.

Related technical literature:

Previously, \citeasnounCFG-10 derived the properties of the rearrangement (sorting) operator in the univariate case with known (standard uniform distribution). Those results were motivated by a completely different problem – namely, restoration of monotonicity in conditional quantile estimation – rather than the problem of summarizing heterogeneous effects by the SPEs. These prior technical results are not applicable to our case as soon as the dimension of is greater than one, which is the case in all modern applications where effects are of interest. Moreover, the previous results are not applicable even in the univariate case since the measure is not known in all envisioned applications. The properties of the sorting operator are different in the multivariate case and require tools from differential geometry: computation of functional (Hadamard) derivatives of the sorting operator with respect to perturbations of require us to work with integration on -dimensional manifolds of the type , where . Moreover, we also need to compute functional derivatives with respect to suitable perturbations of the measure . In econometrics or statistics, \citeasnounsasaki-15 also used differential geometry to characterize the structural properties of derivatives of conditional quantile functions in nonseparable models; and \citeasnounkim:pollard used tools from differential geometry to derive the large sample properties of the maximum score and other cube root consistent estimators. Relative to these papers, we share the use of differential geometry tools as a general proof strategy, but we apply these tools to establish the analytical properties of different functionals – namely, the SPEs. Moreover, our results on the functional differentiability of the sorting and classification operators in the multivariate case constitute new mathematical results, which are of interest in their own right.

Organization of the paper:

In Section 2 we discuss the quantities of interest in nonlinear and interactive linear models with examples; introduce the SPE and related CA, along with their empirical counterparts; and outline the main inferential results. In Section 3 we provide an empirical application to the gender wage gap in the U.S. in 2015. We derive the properties of the empirical SPE and CA in large samples and show how to use these properties to make inference in Section 4. Appendix A provides some key mathematical results on the differentiability of the multivariate sorting and classification operators and Appendix B contains the proof of the main results. All other proofs are given in the online appendix with supplementary material (SM), which also contains additional technical material, and results from Monte Carlo simulations and an empirical application to mortgage denials using binary response models [cfy17sup].

2. Sorted Effects and Classification Analysis

We start by discussing the objects of interest in nonlinear and interactive linear models.

2.1. Effects of Interest

We consider a general model characterized by a predictive function , where is a -vector of covariates that may contain unobserved components, as in quantile regression models. The function usually arises from a model for a response variable , which can be discrete or continuous. We call the function predictive because the underlying model can be either predictive or causal under additional assumptions, but we do not insist on estimands having a causal interpretation. For example, in a mean regression model, corresponds to the expectation function of conditional on ; in a binary response model, corresponds to the choice probability of conditional on ; in a quantile regression model, , where the covariate consists of the unobservable rank variable with a uniform distribution, , and the observed covariate vector , and where is the conditional -quantile of given .

Let , where is the key covariate or treatment of interest, and is a vector of control variables. We are interested in the effects of changes in on the function holding constant. These effects are usually called partial effects, marginal effects, or treatment effects. We call them predictive effects (PE) throughout the paper, as such a name most accurately describes the meaning of the estimand (especially when a causal interpretation is not available). If is discrete, the PE is

| (2.1) |

where and are two values of that might depend on (e.g., and , or and ). This PE measures the effect of changing from to holding constant at . If is continuous and is differentiable, the PE is

| (2.2) |

where denotes , the partial derivative with respect to . This PE measures the effect of a marginal change of from the level holding constant at .222We can also consider high-order and crossed effects. For example, gives the second-order PE of the continuous treatment if is twice differentiable; and, letting where and are discrete, gives the crossed effect or interaction of and .

We consider the following examples in the empirical applications of Section 3 and SM.

Example 1 (Binary response model).

Let be a binary response variable such as an indicator for mortgage denial, and be a vector of covariates related to . The predictive function of the probit or logit model takes the form:

where is a vector of known transformations of , is a parameter vector, and is a known distribution function (the standard normal distribution function in the probit model or standard logistic distribution function in the logit model). If is a binary variable such as an indicator for black applicant and is a vector of controls such as the applicant characteristics relevant for the bank decision, the PE,

describes the difference in predicted probability of mortgage denial for a black applicant and a white applicant, conditional on a specific value of the observable characteristics . ∎

Example 2 (Interactive linear model with additive error).

Let be the logarithm of the wage. Suppose , where is an indicator for female worker and are other worker characteristics. We can model the conditional expectation function of log wage using the linear interactive model:

where is a collection of transformations of and , involving some interaction between and . For example, . Then the PE

is the (average) gender wage gap or difference between the expected log wage of a woman and a man, conditional on a specific value of the characteristics . ∎

Example 3 (Linear model with non-additive error, or QR model).

Let be log wage, be an indicator for female worker, and be a vector of worker characteristics as in the previous example. Suppose we model the conditional quantile function of log wage using the linear interactive model:

where is the conditional -quantile of given and . Thus the covariate vector includes the observed covariates as well as the rank variable , which is an unobserved factor (e.g., “ability rank”). Here is a collection of transformations of and , e.g., . Then the PE

is the (-quantile) gender wage gap or difference between the conditional -quantile of log-wage of a woman and a man, conditional on a specific value of the characteristics .

Note that in this case,

where is the distribution function of the standard uniform random variable, and is the distribution of . For estimation purposes, we will have to exclude the tail quantile indices, so will be redefined to have support on a set of the form , where is a small positive number. ∎

The set of examples listed above are the most basic, leading cases, arising mostly in predictive analysis and program evaluation. Our theoretical results are rather general and are not limited to these cases. Thus, they allow for both and to originate from causal or structural models and to be estimated by structural methods. For example, in treatment effects models with selection on observables [rr83], the PE is the conditional average treatment effect where and are potential outcomes in the treated and non-treated statuses and is a vector of covariates. The standard approach is to aggregate the conditional average treatment effects by integration with respect to the distribution of the covariates in the population of interest . This yields the average treatment effect if is the distribution in the entire population or the average treatment effect on the treated if is the distribution in the treated subpopulation. The SPE can be used to complement the analysis by reporting the entire range of conditional average treatment effects, and also to determine the optimal treatment allocation with budget constraints. Thus, \citeasnounbd12 showed that under some conditions this optimal allocation has a cutoff determined by a tail percentile of the conditional average treatment effects, i.e. by a SPE. Another example is the welfare analysis described in \citeasnounhn17, where is the compensating or equivalent variation of a price change conditional on covariates such as income and demographic characteristics, and is the distribution of covariates in the population of interest.

In all the previous examples, the PE is a function of and therefore can be different for each observational unit. To summarize this effect in a single measure, a common practice in empirical economics is to average the PEs. Averaging, however, masks most of the heterogeneity in the PE allowed by nonlinear or interactive linear models. We propose reporting the entire set of values of the PE sorted in increasing order and indexed by a ranking with respect to the population of interest. These sorted effects provide a more complete representation of the heterogeneity in the PE than the average effects.

Definition 2.1 (-SPE).

The -sorted predictive effect with respect to is

where denotes expectation with respect to .

The -SPE is the -quantile of when is distributed according to . As for the average effect, can be chosen to select a target subpopulation from the entire population. For example, when is a treatment indicator:

-

•

If is set to the marginal distribution of in the entire population, then is the population -SPE.

-

•

If is set to the distribution of conditional on , then is the -SPE on the treated or exposed.

By considering at multiple quantile indices, we obtain a one-dimensional representation of the heterogeneity of the PE. Accordingly, our object of interest is the SPE-function

where is the set of quantile indices of interest.

We also show how to use the -SPE for classification analysis. Let with , and be a -dimensional random vector that includes and possibly other variables such as in Examples 1–3. By abuse of notation, we also denote the distribution of over its support as .

Definition 2.2 (-CA).

The -classification analysis consists of 2 steps: (i) Assign all with to the -least affected subpopulation, and all with to the -most affected subpopulation. (ii) Obtain the moments and distribution of in the least and most affected subpopulations. We denote by and generic objects indexed by in the least and most affected subpopulations, respectively. For example, corresponds to the -moment of in the -least affected subpopulation, and to the distribution of at in the -least affected subpopulation.333For a -dimensional random variable and , we denote and . We define the same quantities in the -most affected subpopulation replacing by in the conditioning set.

2.2. Empirical SPE

In practice, we replace the PE and the distribution by sample analogs to construct plug-in estimators of the SPE. Let and be estimators of and obtained from , an independent and identically distributed sample of size from .

Definition 2.3 (Empirical -SPE).

The estimator of is

Then the empirical SPE-function is

where is the set of indices of interest that typically excludes tail indices and satisfies other technical conditions stated in Section 4.

Example 1 (Binary response model, cont.) The estimator of the PE is

where is the maximum likelihood (ML) estimator of ,

∎

Example 2 (Interactive linear model with additive error, cont.) The estimator of the PE is

where is the ordinary least squares (OLS) estimator of ,

∎

Example 3 (Linear model with non-additive error, cont.) The estimator of the PE is

where is the \citeasnounKoenker:1978 quantile regression (QR) estimator of ,

∎

Remark 2.1 (Estimation of ).

Let denote the indicator for an observational unit belonging to the subpopulation of interest. For example, if , then indicates the unit is in the subpopulation of the treated and indicates the unit is in the subpopulation of the untreated. The indicator can also incorporate other restrictions, for example restricts the support of covariate to the region . Finally, if is always , then this means that we work with the entire population. Estimation of can be done using the empirical distribution:

provided that . An alternative would be to use the smoothed empirical distribution.

If can be decomposed into known and unknown parts, then we only need to estimate the unknown parts. Thus, in Example 3, where is known to be the uniform distribution and is unknown, but can be estimated by the empirical distribution of in the part of the population of interest. ∎

2.3. Empirical CA

The empirical version of the -CA classifies the observations in the sample using the empirical PEs and -SPE, and computes the moments and distributions in the resulting most and least affected subsamples.

Definition 2.4 (Empirical -CA).

The empirical -classification analysis consists of 2 steps: (1) Assign all with to the -least affected subsample, and all with to the -most affected subsample. (2) Estimate the moments and distribution of in the least and most affected subpopulations by the empirical analogs in the least and most affected subsamples, i.e. and . For example, estimates the -moment of in the -least affected subpopulation and the distribution of at in the -least affected subpopulation. The corresponding estimators in the -most affected subpopulation are constructed replacing by in the conditioning set. Here we use the same notation as in Definition 2.2.

2.4. Inference on SPE

The main inferential result for the SPE can be previewed as follows. Assume that the PE function is not locally flat in the sense that the norm of its gradient does not vanish anywhere over the support, and other regularity conditions stated in Section 4. Then, the empirical SPE-process is -consistent and converges in distribution to a centered Gaussian process, namely

the metric space of bounded functions on , as a stochastic process indexed by , where is a compact subset of . Moreover, the exchangeable bootstrap algorithm specified in Algorithm 2.1 estimates consistently the law of .

The next corollary to Theorem 4.1 in Section 4 provides uniform bands that cover the SPE-function simultaneously over a region of values of with prespecified probability in large samples. It does cover pointwise confidence bands for the SPE-function at a specific quantile index as a special case by simply taking to be the singleton set .

Corollary 2.1 (Inference on SPE-function using Limit Theory and Bootstrap).

We now describe a practical bootstrap algorithm to estimate the quantiles of . Let denote the bootstrap weights, which are nonnegative random variables independent of the data obeying the conditions stated in \citeasnounvdV-W. For example, is a multinomial vector with dimension and probabilities in the empirical bootstrap. In what follows is the number of bootstrap draws, such that . In our experience, setting suffices for good accuracy.

Algorithm 2.1 (Bootstrap law of and its quantiles).

1) Draw a realization of the bootstrap weights . 2) For each , compute , a bootstrap draw of , where and are the bootstrap versions of and that use as sampling weights in the computation of the estimators. Construct a bootstrap draw of as . 3) Repeat steps (1)-(2) times. 4) For each , compute a bootstrap estimator of such as the bootstrap interquartile range rescaled with the normal distribution, where is the th sample quantile of in the draws and is the th quantile of . 5) Use the empirical distribution of across the draws to approximate the distribution of . In particular, construct , an estimator of , as the -quantile of the draws of .

Remark 2.2 (Monotonization of the bands).

While the SPE-function is increasing by definition, the end functions of the confidence band might not be increasing. \citeasnouncfg-09 showed that monotonizing the end functions via rearrangement reduces the width of the band in uniform norm, while increases coverage in finite-samples. We use this refinement in the empirical examples.444In practice, the rearrangement simply consists in sorting the two vectors containing the discretized version of the end-functions in increasing order; see \citeasnouncfg-09 for more details. ∎

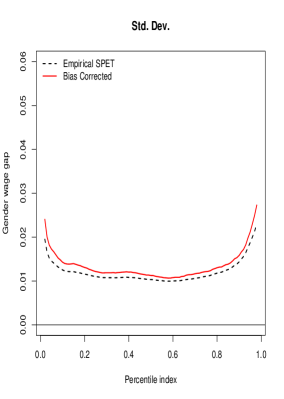

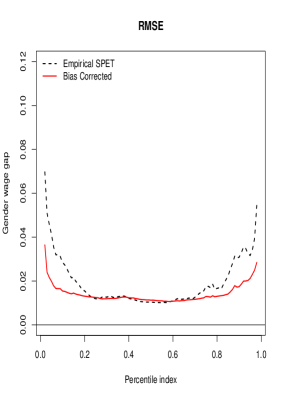

Remark 2.3 (Finite-Sample Bias Corrections).

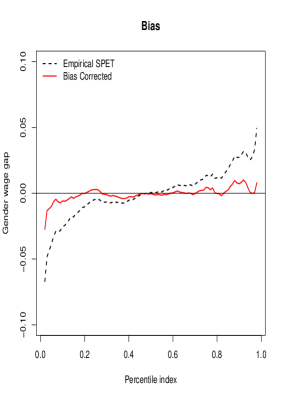

The empirical -SPE might be biased in small samples, specially at the the tails. Bootstrap is also useful to improve the estimator and confidence bands. Thus, a corrected estimator can be formed as and a corrected -confidence band as , where is the mean of the bootstrap draw of the estimator. In Appendix H of the SM, we show that this correction reduces the bias of the estimator and increases the coverage of the confidence bands in a simulation calibrated to the gender wage gap application. ∎

2.5. Inference on CA

Let and . The main inferential result for CA can be previewed as follows: the empirical CA-process converges in distribution to a centered bivariate Gaussian process, namely

| (2.3) |

as a stochastic process indexed by . Moreover, exchangeable bootstrap estimates consistently the law of .

The next corollary to Theorem 4.2 in Section 4 provides uniform bands that cover linear combinations of the -dimensional vector with coefficients simultaneously over with prespecified probability in large samples. It covers pointwise confidence intervals for the mean of the component of for least affected as a special case with linear combination, , and , where is a unit vector with a one in the position. Joint confidence intervals for differences of means of the , , components of between most and least affected are a special case with linear combination, , and . Joint uniform bands for the distribution of the component of for most and least affected are also a special case with linear combinations, , , and , where is an arbitrarily large number. By appropriate choice of the linear combinations and the index set , we can therefore conduct multiple tests while preserving the significance level from simultaneous inference problems [rsw10b, rsw10, lsx16]. We show examples in the empirical application of Section 3.

Corollary 2.2 (Inference on CA-function using Limit Theory and Bootstrap).

Under the assumptions of Theorem 4.2, for any ,

where is any consistent estimator of , the -quantile of

and is a uniformly consistent estimator of , the variance function of . A p-value of the null hypothesis for all and of the realization of the statistic is

We provide consistent estimators of , and in Algorithm 2.2.

Algorithm 2.2 (Bootstrap law of , quantiles and p-values).

1) Draw a realization of the bootstrap weights . 2) For each , compute and , a bootstrap draw of and , where and are the bootstrap versions of and that use as sampling weights in the computation of the estimators. Construct a bootstrap draw of as , where . 3) Repeat steps (1)-(2) times. 4) For each and , compute a bootstrap estimator of such as the bootstrap interquartile range rescaled with the normal distribution where is the th sample quantile of in the draws and is the th quantile of . 5) Use the empirical distribution of across the draws to approximate the distribution of . In particular, construct , an estimator of , as the -quantile of the draws of , and an estimation of the p-value as the proportion of the draws of that are greater than .

2.6. Inference on Most and Least Affected Subpopulations

In addition to moments and distributions, we can conduct inference on the subpopulations of most and least affected.555Here we follow the set inference approach described in \citeasnounckm15, which builds on \citeasnouncht:bounds. In addition our results justify the use of subsapling-based methods as in \citeasnouncht:bounds and \citeasnounRSset. Let

be the sets representing the -least and -most affected subpopulation, respectively. Here we assume that is compact or that the support of has been intersected with a compact set to form . We can construct an outer -confidence set for as666Note that we can also similarly construct an inner confidence region, which is the complement of the outer confidence region of , see \citeasnounckm15 for relevant discussion.

where is a consistent estimator of , the -quantile of the random variable

and is a uniformly consistent estimator of , the variance function of the process defined in Section 4. The estimator can be obtained as the -quantile of the bootstrap version of ,

where and are defined as in Algorithm 2.1. A similar -confidence set, can be constructed for . These sets can be visualized by plotting all 2 or 3 dimensional projections of their elements. We provide an example of such plots in Section 3. An immediate consequence of the set inference results in \citeasnounckm15 and the results of this paper is the following corollary:

Corollary 2.3 (Inference on Most and Least Affected Subpopulations).

The sets and cover and with probability approaching , and and are consistent in the sense that they approach to and at a -rate with respect to the Hausdorff distance.

3. Empirical Analysis of the Gender Wage Gap

We report the main results of the application to the gender wage gap using data from the U.S. March Supplement of the Current Population Survey (CPS) in 2015. In Appendix H of the SM, we complement the analysis with supporting results from a simulation calibrated to this application. There, we find that our estimation and inference methods perform well in finite samples that closely mimic the characteristics of the CPS data. This exercise serves to indirectly verify the plausibility of the main regularity conditions mentioned in Section 2 and formally stated in Section 4.

Our sample consists of white, non-hispanic individuals who are aged 25 to 64 years and work more than 35 hours per week during at least 50 weeks of the year. We exclude self-employed workers; individuals living in group quarters; individuals in the military, agricultural or private household sectors; individuals with inconsistent reports on earnings and employment status; individuals with allocated or missing information in any of the variables used in the analysis; and individuals with hourly wage rate below . The resulting sample contains workers including men and of women.

We estimate interactive linear models with additive and non-additive errors, using mean and quantile regressions, respectively. The outcome variable is the logarithm of the hourly wage rate constructed as the ratio of the annual earnings to the total number of hours worked, which is constructed in turn as the product of number of weeks worked and the usual number of hours worked per week. The key covariate is an indicator for female worker, and the control variables include 5 marital status indicators (widowed, divorced, separated, never married, and married); 5 educational attainment indicators (less than high school graduate, high school graduate, some college, college graduate, and advanced degree); 4 region indicators (midwest, south, west, and northeast); a quartic in potential experience constructed as the maximum of age minus years of schooling minus 7 and zero, i.e., ; 5 occupation indicators (management, professional and related; service; sales and office; natural resources, construction and maintenance; and production, transportation and material moving); 12 industry indicators (mining, quarrying, and oil and gas extraction; construction; manufacturing; wholesale and retail trade; transportation and utilities; information; financial services; professional and business services; education and health services; leisure and hospitality; other services; and public administration); and all the two-way interactions between the education, experience, occupation and industry variables except for the occupation-industry interactions.777The sample selection criteria and the variable construction follow \citeasnounMulligan-Rubinstein-08. The occupation and industry categories follow the 2010 Census Occupational Classification and 2012 Census Industry Classification, respectively. All calculations use the CPS sampling weights to account for nonrandom sampling in the March CPS.

| All | Women | Men | All | Women | Men | ||

| Log wage | 3.15 | 3.02 | 3.25 | O.manager | 0.48 | 0.55 | 0.43 |

| Female | 0.44 | 1.00 | 0.00 | O.service | 0.10 | 0.10 | 0.09 |

| MS.married | 0.65 | 0.61 | 0.68 | O.sales | 0.23 | 0.31 | 0.16 |

| MS.widowed | 0.01 | 0.02 | 0.01 | O.construction | 0.09 | 0.01 | 0.15 |

| MS.separated | 0.02 | 0.02 | 0.02 | O.production | 0.11 | 0.04 | 0.17 |

| MS.divorced | 0.13 | 0.16 | 0.10 | I.minery | 0.03 | 0.01 | 0.04 |

| MS.Nevermarried | 0.19 | 0.18 | 0.20 | I.construction | 0.06 | 0.01 | 0.09 |

| E.lhs | 0.02 | 0.02 | 0.03 | I.manufacture | 0.14 | 0.08 | 0.18 |

| E.hsg | 0.25 | 0.21 | 0.28 | I.retail | 0.13 | 0.11 | 0.14 |

| E.sc | 0.28 | 0.29 | 0.27 | I.transport | 0.04 | 0.02 | 0.06 |

| E.cg | 0.28 | 0.30 | 0.27 | I.information | 0.02 | 0.02 | 0.03 |

| E.ad | 0.16 | 0.18 | 0.15 | I.finance | 0.08 | 0.10 | 0.07 |

| R.northeast | 0.19 | 0.19 | 0.19 | I.professional | 0.11 | 0.10 | 0.13 |

| R.midwest | 0.27 | 0.28 | 0.27 | I.education | 0.24 | 0.40 | 0.11 |

| R.south | 0.35 | 0.35 | 0.35 | I.leisure | 0.05 | 0.05 | 0.04 |

| R.west | 0.18 | 0.18 | 0.19 | I.services | 0.03 | 0.03 | 0.04 |

| Experience | 21.68 | 21.72 | 21.65 | I.public | 0.07 | 0.06 | 0.07 |

| Source: March Supplement CPS 2015. | |||||||

Table 1 reports sample means of the variables used in the analysis. Working women are more highly educated than working men, have about the same potential experience, and are less likely to be married and more likely to be divorced. They work relatively more often in managerial and sales occupations and in the industries providing education and health services. Working men are relatively more likely to work in construction and production occupations within non-service industries. The unconditional gender wage gap is 23%.

Figure 1 of Section 1 plots estimates and 90% confidence bands for the APE and SPE-function on the treated (women) of the conditional gender wage gap using additive and non-additive error models. The PEs are obtained as described in Examples 2 and 3 with . In this case , which makes it very difficult to identify any pattern about the gender wage gap just by looking at the regression coefficients. The distribution is estimated by the empirical distribution of for women, and is approximated by a uniform distribution over the grid . The confidence bands are constructed using Algorithm 2.1 with standard exponential weights (weighted bootstrap) and , and are uniform for the SPE-function over the grid . We monotonize the bands using the rearrangement method described in Remark 2.2, and implement the finite sample corrections described in Remark 2.3. After controlling for worker characteristics, the gender wage gap for women remains on average around 20%. More importantly, we uncover a striking amount of heterogeneity, with the PE ranging between -6.5 and 40% in the additive error model and between -14 and 54% in the non-additive error model.888In the 2016 version of the paper we found similar patterns of heterogeneity using CPS 2012 data with a specification that did not include occupation and industry indicators.

| 10% Least | 10% Most | 10% Least | 10% Most | ||||||

| Est. | S.E. | Est. | S.E. | Est. | S.E. | Est. | S.E | ||

| Log wage | 3.08 | 0.03 | 2.97 | 0.03 | O.manager | 0.67 | 0.04 | 0.38 | 0.04 |

| M.married | 0.28 | 0.03 | 0.87 | 0.02 | O.service | 0.08 | 0.02 | 0.10 | 0.02 |

| M.widowed | 0.02 | 0.01 | 0.01 | 0.01 | O.sales | 0.19 | 0.03 | 0.42 | 0.04 |

| M.separated | 0.02 | 0.01 | 0.01 | 0.00 | O.construction | 0.02 | 0.01 | 0.01 | 0.00 |

| M.divorced | 0.15 | 0.02 | 0.07 | 0.02 | O.production | 0.03 | 0.01 | 0.09 | 0.02 |

| M.nevermarried | 0.52 | 0.03 | 0.04 | 0.01 | I.minery | 0.01 | 0.01 | 0.02 | 0.01 |

| E.lhs | 0.01 | 0.01 | 0.06 | 0.01 | I.construction | 0.02 | 0.01 | 0.02 | 0.01 |

| E.hsg | 0.08 | 0.02 | 0.30 | 0.04 | I.manufacture | 0.02 | 0.01 | 0.11 | 0.02 |

| E.sc | 0.15 | 0.03 | 0.23 | 0.04 | I.retail | 0.06 | 0.02 | 0.19 | 0.03 |

| E.cg | 0.37 | 0.04 | 0.17 | 0.03 | I.transport | 0.01 | 0.01 | 0.04 | 0.01 |

| E.ad | 0.39 | 0.04 | 0.24 | 0.03 | I.information | 0.04 | 0.01 | 0.05 | 0.01 |

| R.ne | 0.24 | 0.02 | 0.18 | 0.02 | I.finance | 0.03 | 0.02 | 0.09 | 0.03 |

| R.mw | 0.26 | 0.02 | 0.28 | 0.02 | I.professional | 0.06 | 0.02 | 0.04 | 0.02 |

| R.so | 0.31 | 0.02 | 0.39 | 0.03 | I.education | 0.46 | 0.04 | 0.33 | 0.04 |

| R.we | 0.19 | 0.02 | 0.15 | 0.02 | I.leisure | 0.10 | 0.03 | 0.01 | 0.01 |

| Experience | 13.05 | 1.03 | 26.32 | 0.75 | I.services | 0.09 | 0.02 | 0.01 | 0.01 |

| I.public | 0.09 | 0.02 | 0.08 | 0.02 | |||||

| PE estimated from a linear conditional quantile model with interactions. | |||||||||

| Standard Errors obtained by weighted bootstrap with 500 repetitions. | |||||||||

Table 8 shows the results of a classification analysis, exhibiting characteristics of women that are most and least affected by the gender wage gap together with standard errors obtained by weighted bootstrap. We focus here on the non-additive model, but the results from the additive model are similar. Since the PE are predominantly negative, we define the most affected as and the lest affected as to facilitate the interpretation. According to this model the 10% of the women most affected by the gender wage gap on average earn lower wages, are much more likely to be married, much less likely to be never married, have lower education, live in the South, possess much more potential experience, are more likely to have sales and non managerial occupations, and work more often in manufacture and retail and less often in education industries than the 10% least affected women.

| Est. | S.E. | P-val.1 | JP-val.2 | Est. | S.E. | P-val.1 | JP-val.2 | ||

| Log wage | -0.10 | 0.04 | 0.03 | 0.70 | O.manager | -0.29 | 0.06 | 0.00 | 0.00 |

| M.married | 0.59 | 0.04 | 0.00 | 0.00 | O.service | 0.02 | 0.03 | 0.99 | 1.00 |

| M.widowed | -0.02 | 0.02 | 0.93 | 1.00 | O.sales | 0.22 | 0.06 | 0.00 | 0.03 |

| M.separated | -0.01 | 0.01 | 0.89 | 1.00 | O.construction | -0.01 | 0.01 | 0.67 | 1.00 |

| M.divorced | -0.08 | 0.04 | 0.46 | 0.86 | O.production | 0.06 | 0.02 | 0.08 | 0.42 |

| M.nevermarried | -0.48 | 0.04 | 0.00 | 0.00 | I.minery | 0.01 | 0.01 | 0.97 | 1.00 |

| E.lhs | 0.05 | 0.01 | 0.01 | 0.17 | I.construction | -0.00 | 0.01 | 1.00 | 1.00 |

| E.hsg | 0.22 | 0.05 | 0.00 | 0.00 | I.manufacture | 0.08 | 0.02 | 0.02 | 0.15 |

| E.sc | 0.08 | 0.06 | 0.70 | 1.00 | I.retail | 0.12 | 0.04 | 0.06 | 0.32 |

| E.cg | -0.19 | 0.06 | 0.01 | 0.16 | I.transport | 0.04 | 0.01 | 0.08 | 0.39 |

| E.ad | -0.15 | 0.06 | 0.07 | 0.46 | I.information | 0.01 | 0.02 | 1.00 | 1.00 |

| R.ne | -0.06 | 0.04 | 0.35 | 0.99 | I.finance | 0.06 | 0.04 | 0.78 | 0.99 |

| R.mw | 0.02 | 0.04 | 0.95 | 1.00 | I.professional | -0.01 | 0.03 | 1.00 | 1.00 |

| R.so | 0.08 | 0.04 | 0.23 | 0.97 | I.education | -0.13 | 0.06 | 0.29 | 0.74 |

| R.we | -0.04 | 0.03 | 0.69 | 1.00 | I.leisure | -0.09 | 0.03 | 0.04 | 0.22 |

| Experience | 13.27 | 1.54 | 0.00 | 0.00 | I.services | -0.07 | 0.02 | 0.02 | 0.15 |

| I.public | -0.01 | 0.03 | 1.00 | 1.00 | |||||

| PE estimated from a linear conditional quantile model with interactions. | |||||||||

| Standard Errors and p-values obtained by weighted bootstrap with 500 repetitions. | |||||||||

| 1 These p-values are adjusted for multiplicity to account for joint testing of zero coefficients | |||||||||

| on for all variables within a category: M E, R, O, or I. | |||||||||

| 2 These p-values are adjusted for multiplicity to account for joint testing of zero coefficients | |||||||||

| on all the variables in the table. | |||||||||

Table 3 tests if the differences found in table 8 are statistically significant. It reports p-values for the test of equality of means for most and least affected women. The first p-value accounts for simultaneous inference on all variables within a given category. For example, it accounts that we are conducting five tests corresponding to the five categories of marital status. For the non categorical variables log wage and experience the p-values are for one test. The second p-value accounts for simultaneous inference of all the differences displayed in the table.999We employ the so called ”single-step” methods for controlling the family-wise error rate. To generate a (somewhat) higher power, we recommend to employ the p-values generated via ”step-down” methods, such as those reported in \citeasnounRWpvals and \citeasnounlsx16. These p-values are obtained by Algorithm 2.2 with the appropriate choice of vectors of linear combinations and set , and 500 weighted bootstrap repetitions. The p-values show that most of the differences from table 8 are statistically significant at conventional significant levels after controlling for simultaneous inference. In particular, the most affected women are significantly more likely to be married, high-school graduates, more experienced, and in sales occupations, and less likely to be never married and in managerial occupations under the most strict simultaneous inference correction. \citeasnounbk17 have recently documented the importance of differences in occupation and industry to explain the gender wage gap using data from the Panel Study of Income Dynamics (PSID) 1980-2010 and a different methodology based on wage decompositions. Consistent with our findings, they argue that this importance might be due to compensating differentials. Unlike \citeasnounbk17 and previous studies in the literature, our analysis uncovers significant heterogeneity in the extent of the gender wage gap and relates this heterogeneity to human capital, occupation, industry and other characteristics.

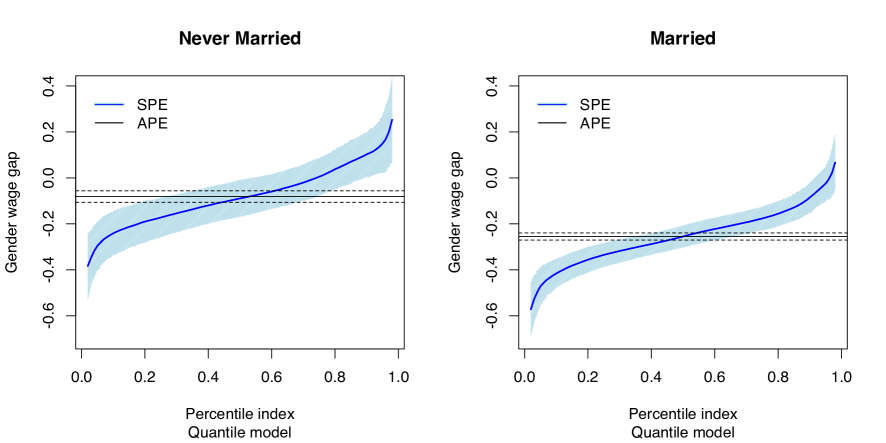

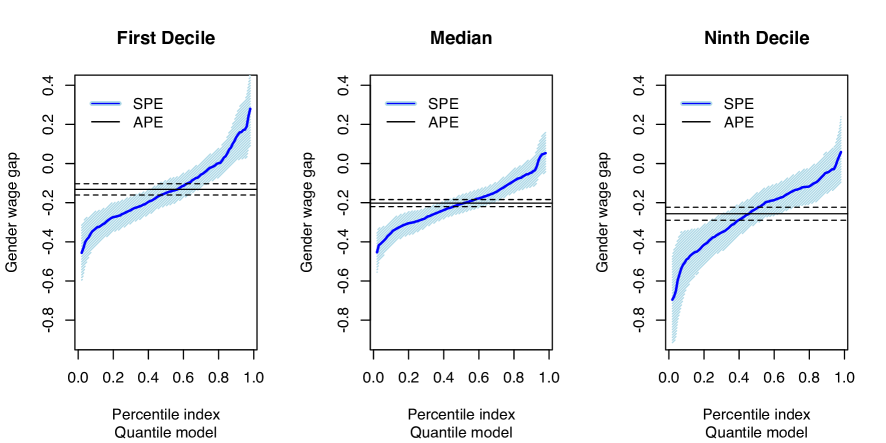

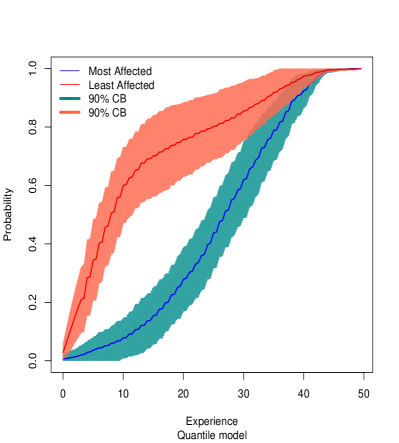

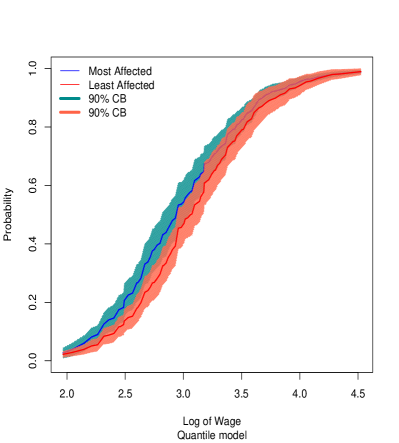

We further explore these findings by analyzing the APE and SPE on the treated conditional on marital status and unobserved rank in the non-additive error model. Figures 2 and 3 show estimates and 90% confidence bands of the APE and SPE-function of the gender wage gap for 2 subpopulations defined by marital status (married and never married) and 3 subpopulations defined by unobserved rank (first decile, median and ninth decile, where the unobserved rank is .1, .5 and .9, respectively). The confidence bands are constructed as in fig. 1. We find significant heterogeneity in the gender gap within each subpopulation, and also between subpopulations defined by marital status and unobserved rank. The SPE-function is more negative for married women and at the tails of the conditional distribution. Married women at the top decile suffer from the highest gender wage gaps. This pattern is consistent with “glass-ceiling” effects behind the gender wage gap [abv03].

Figure 4 plots simultaneous 90% confidence bands for the distribution of experience and log wage for the most and least affected women. They are obtained by Algorithm 2.2 with 500 weighted bootstrap replications. The estimated distribution of experience for the most affected first-order stochastically dominates the same estimated distribution for the least affected women. Moreover, the uniform bands confirm that this dominance is statistically significant at the 90% confidence level for the underlying distributions. The estimated (marginal) distribution of log wage for the least affected first-order dominates the same estimated distribution for most affected, but we cannot reject that the underlying distributions are equal at the 10% significance level. The results of the classification analysis are consistent with preferences that make never married highly educated young women working on managerial occupations be more career-oriented.101010We find similar results using the additive error model. We do not report these results for the sake of brevity.

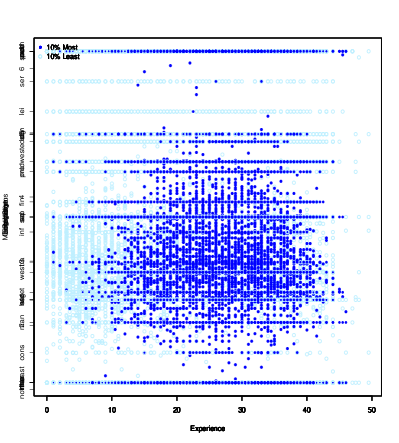

Finally, Figure 5 plots two dimensional projections of experience-log wage and experience-marital status of the confidence sets for the 10% most and least affected subpopulations. We show the results from the additive error model for the conditional expectation. Here we use a simplified specification that excludes the two-way interactions from to get more precise estimates of all the PEs. We obtain 90% confidence sets for the most and least affected subpopulations by weighted bootstrap with standard exponential weights and 500 repetitions. The sets and include and of the women in the sample, respectively.111111Recall that in this application the set corresponds to most affected women and to least affected women. We drop one woman that is included in both sets. The projections show that there are relatively more least affected women with low experience at all wage levels, more high affected women with high wages with between 15 and 25 years of experience, and more least affected women which are not married at all experience levels.

4. Detailed Large Sample Theory

4.1. Detailed Large Sample Theory for SPE

For an open set , let the class on denote the set of continuously differentiable real valued functions on . We make the following technical assumptions about the PE function and the distribution of the covariates:

. The part of the domain of the PE function of interest, , is open and its closure is compact. The distribution is absolutely continuous with respect to the Lebesgue measure with density . There exists an open set containing such that is on , and is continuous on and is zero outside the domain of interest, i.e. for any .

. Let . For any regular value of on , we assume that the closure of has a finite number of connected branches.

The following property of the set is a useful implication of Assumptions and that we will exploit in the analysis.

Remark 4.1 (Properties of ).

By Theorem 5-1 in \citeasnoun[p. 111]spivak-65, and imply that is a -manifold without boundary in of class for any that is a regular value of on .

Assumption imposes mild smoothness conditions on the PE function . It also requires that all the components of the covariate are continuous random variables. We defer the treatment of the case where has both continuous and discrete components to the SM. As a matter of generalization, our theoretical analysis allows us to replace that vanishes on , by the weaker condition that the intersection of and the boundary of have zero volume with respect to , namely

| (4.4) |

where denotes the boundary of , is the gradient of , and denotes the integral of the function on the manifold with respect to volume; see Appendix D in the SM for a brief review on Differential Geometry. This relaxation is relevant to cover the case where includes an uniformly distributed component such as the unobserved rank in Example 3.121212 In the numerical examples of Section H in the SM, the first two designs only satisfy this relaxed condition.

Assumption imposes shape restrictions on that rule out cases such as infinite cyclical oscillations or flat areas. A simple sufficient condition for is that the map does not have critical points on . This means that is not locally flat anywhere on , which we define to mean that the norm of the gradient, , does not vanish on . In this case, any in the image of under is regular. This condition is probably the most relevant for practice and can be verified in applications, at least informally.

Remark 4.2 (Verification of Regularity Conditions in Practice).

The main regularity condition is that PE function be smooth and not locally flat, namely does not vanish. Our inferential results are developed under this assumption, and they do not apply otherwise. To verify if these results apply in practice, we strongly recommend to conduct a Monte Carlo experiment using a data generating process that mimics the application at hand.131313In fact, we recommend doing this for every econometric method. Indeed, failure of the inference method in the simulation experiment implies failure of the regularity conditions. We provide an application of this supporting analysis to the gender wage gap example in Appendix H. Looking forward, it would be useful to develop further an inference method with good robustness properties with respect to the regularity conditions, i.e. that remains uniformly valid when the PE function is (close to being) locally flat. We delegate this line of research to future work.141414For instance, it is of interest to determine whether the use of subsampling instead of bootstrap can deliver a more robust inference method when the PE function is close to being flat; see, e.g. \citeasnounRomano:Shaikh:AoS.

We make the following assumptions about the estimator of the PE. Let denote the set of bounded and measurable functions and a fixed subset of continuous functions on . Let be the set of bounded and measurable functions on and denote weak convergence (convergence in distribution).

. , the estimator of , belongs to with probability approaching and obeys a functional central limit theorem, namely,

where is a sequence such that as , and is a tight process that has almost surely uniformly continuous sample paths on .

In the parametric and semiparametric models of Examples 1–3, holds under weak conditions that guarantee asymptotic normality of the ML, OLS and QR estimators. For the QR estimator in Example 3 where the unobserved rank is one of the covariates, these conditions include that the density of conditional on be bounded away from zero [koenker:book], which is facilitated by excluding tail quantile indexes.

Let be the estimator of the distribution . It is convenient to identify and with the operators:

mapping from the set to , where is the fixed subset of continuous functions on containing , and is any compact set of . We require to be totally bounded under the norm. Define as the set of all bounded linear operators on of the form

which are uniformly continuous on under the norm. We define the boundedness of these operators with respect to the norm:

and define the corresponding distance between two operators and in as . Clearly, .

We make the following assumption about .

. The function is a distribution over obeying in ,

| (4.5) |

where is a.s. an element of (i.e. it has almost surely uniformly continuous sample paths on with respect to the metric) and is a sequence such that as .

When is the empirical distribution based on a random sample from the population with distribution , then and , where is a -Brownian Bridge, i.e. a Gaussian process with zero mean and covariance function . In this case condition imposes that the function class

is -Donsker. Note that is the parameter space that contains as well as in . In parametric models for the PE where , is known, with , and is on for all , the class is -Donsker under mild conditions specified for example in \citeasnoun[Chap. 19]vdV. Examples 1 and 2 specify the PE parametrically. Lemma F.1 in the SM gives other sufficient conditions for the Donsker property.

The following result is derived as a consequence of the new mathematical results on the Hadamard differentiability of the sorting operator, stated in Lemma A.2 in the Appendix (proof given in SM due to space constraints), in conjunction with the functional delta method. It shows that the empirical SPE-function follows a FCLT over sets of quantiles corresponding to pre-images of compact sets of .

Define as a compact set consisting of regular values of on , and for a fixed , where is the density of defined in Lemma A.1(a). Let , the slowest of the rates of convergence of and . Assume and , where when and when . For example, if is treated as known.

Theorem 4.1 (FCLT for and ).

Suppose that - hold, and the convergence in and holds jointly. Then, as ,

(a) The estimator of the distribution of PE obeys a functional central limit theorem, namely, in ,

as a stochastic process indexed by , where

(b) The empirical SPE-process obeys a functional central limit theorem, namely in ,

| (4.6) |

as a stochastic process indexed by .

Remark 4.3 (Critical values).

(a) Theorem 4.1 shows that () follows a FCLT over any compact set (the pre-image of ), where excludes the critical values of on . Thus, we can set when the map does not have critical points on . This case is nice because it allows us not to worry about critical values when performing inference, and practically relevant as it occurs very naturally in many applications. For instance, it arises whenever is strictly locally monotonic in some direction. (b) In numerical examples reported in the SM, we find that the bootstrap inference method proposed performs well even in models where has critical points, without excluding the corresponding critical values from . This evidence suggests that the exclusion of critical values might not be necessary for inference. ∎

4.2. Detailed Large Sample Theory for CA

It is convenient to modify the notation for the -CA separating the dependence on from and and specifying the characteristic of interest as . Moreover, when we remove the dependence on by taking expectations conditional on . Let and , where , , , , is some fixed integer, is the distribution of at conditional on , and . For example, or for . To derive the properties of , we use that the class of functions is -Donsker. When is continuous, this property holds by assumption when is the empirical distribution.151515Lemma F.2 in the SM gives other sufficient conditions for the Donsker property.

The following result is derived as a consequence of the new mathematical results on the Hadamard differentiability of the classification operator, stated in Lemma A.3 in the Appendix (proof given in SM due to space constraints), in conjunction with the functional delta method.

Theorem 4.2 (FCLT for ).

Suppose that - hold, the convergence in and holds jointly, and . If , then assume that is compact and is continuous on for all . Then, as , (a) obeys a FCLT with respect to , namely, in ,

as a stochastic process indexed by , where , , and is the limit process of Theorem 4.1; and (b) if in addition Assumption holds, then obeys the same FCLT with respect to .

Assumption is a technical condition stated in Appendix E of the SM to deal with the discontinuity of the indicator functions when . A sufficient condition for is that

holds uniformly over all , and . In other words, the manifold and the set of points can not have an intersection with positive volume of -dimension.

4.3. Bootstrap Inference for SPE and CA

Corollaries 2.1 and 2.2 use critical values of statistics related to the limit processes and to construct confidence bands and p-values. These critical values can be hard to obtain in practice. In principle one can use simulation, but it might be difficult to numerically locate and parametrize the manifold , and to evaluate the integrals on needed to compute the realizations of and . This creates a real challenge to implement our inference methods. To deal with this challenge we employ (exchangeable) bootstrap to compute critical values [praestgaard-wellner-93, vdV-W] instead of simulation. We show that the bootstrap law is consistent to approximate the distribution of the limit processes of Theorems 4.1 and 4.2.

To state the bootstrap validity result formally, we follow the notation and definitions in \citeasnounvdV-W. Let denote the data vector and let be the vector of bootstrap weights. Consider a random element in a normed space . We say that the bootstrap law of consistently estimates the law of some tight random element and write if

where denotes the space of functions with Lipschitz norm at most 1; denotes the conditional expectation with respect to given the data ; denotes the expectation with respect to , the distribution of the data ; and denotes convergence in (outer) probability.

The next result is a consequence of the functional delta method for the exchangeable bootstrap. Let , the bootstrap draw of defined in Algorithm 2.2.

Theorem 4.3 (Bootstrap FCLT for and ).

Suppose that the bootstrap is consistent for the law of the estimator of the PE, namely in , and for the law of the estimated measure, namely in . Then, (1) under the assumptions of Theorem 4.1, the bootstrap is consistent for the law of the empirical SPE-process, namely

and (2) under the assumptions of Theorem 4.2, the bootstrap is consistent for the law of the empirical CA-process, namely

Theorem 4.3 employs the high-level condition that the bootstrap can approximate consistently the laws of and , after suitable rescaling. In Examples 1-3 when is the empirical measure based on the random sample of size , the exchangeable bootstrap method entails randomly reweighing the sample using the weights , which include empirical boostrap and i.i.d. exponential weights, for example. In this case the high level condition holds if the weights satisfy the conditions stated in equation (3.6.8) of \citeasnounvdV-W. We refer to \citeasnounvdV-W and \citeasnounCFM for bootstrap FCLT for parametric and semi parametric estimators of including least squares, quantile regression, and distribution regression, as well as nonparametric estimators of including the empirical distribution function.

Appendix A Key New Mathematical Results: Hadamard Differentiability of Sorting and Classification Operators

A.1. Notation

We denote the PE as , the empirical PE as , and , the gradient of . For a vector , denotes the Euclidian norm of , that is , where the superscript T denotes transpose.

A.2. Basic Analytical Properties of Sorted Functions

The following lemma establishes the properties of the distribution function and the SPE-function .

Define as a compact set consisting of regular values of on .

Lemma A.1 (Basic Properties of and ).

Under conditions and :

1. For any , the derivative of with respect to is:

| (A.7) |

This integral is well-defined because the gradient is finite, continuous, and bounded away from on . The map is uniformly continuous on .

2. Fix , then for any the derivative of respect to is:

| (A.8) |

Moreover, the derivative map is uniformly continuous on .

A.3. Functional Derivatives of Sorting-Related Operators

We consider the properties of the distribution function and the SPE-function as functional operators and . We show that these operators are Hadamard differentiable with respect to . These results are critical ingredients to deriving the large sample distributions of the empirical versions of and in Section 4.

We now recall the definition of uniform Hadamard differentiability from \citeasnounvdV-W.

Definition A.1 (Hadamard Derivative Uniformly in an Index).

Suppose the linear spaces and are equipped with the norms and , and is a compact subset of a metric space. A map is called Hadamard-differentiable uniformly in at tangentially to a subspace if there is a continuous linear map such that uniformly in :

| (A.9) |

for all converging real sequences and such that for every , and ; moreover, the map is continuous on .

In what follows, we let denote the space of continuous functions on equipped with the sup-norm, and denote a subset of that contains uniformly continuous functions.

Lemma A.2 (Hadamard differentiability of and ).

Let and . Assume that - hold. Then,

(a) The map , mapping , is Hadamard differentiable uniformly in at tangentially to with the derivative map defined by

(b) The map , mapping is Hadamard differentiable uniformly in at tangentially to with the derivative map, , defined by

A.4. Functional Derivatives of Classification Operators

Let and , where and are defined as before; is the set of bounded linear operators mapping from the set to , with norm

where the map is uniformly continuous on under the norm. We derive the properties of the least affected classification operator defined by

where for moments and for distributions of the components of , and for some . The properties of the most affected operator can be derived using similar arguments, which are omitted for brevity.

Lemma A.3 (Hadamard differentiability of ).

Assume that Assumptions S.1 and S.2 hold, , and . Then,

(a) The map is Hadamard-differentiable uniformly in at tangentially to .

(b) If in addition Assumption stated in Appendix E of the SM holds, the map is Hadamard-differentiable uniformly in at tangentially to .

(c) The derivative map is defined by:

where and .

Appendix B Proofs of Section 4

We first recall Theorem 3.9.4 of \citeasnounvdV-W.

Lemma B.1 (Delta-method).

Let and be metrizable topological vector spaces, and is a compact subset of a metric space. Let be a Hadamard differentiable mapping uniformly in at tangentially to , with derivative . Let be stochastic maps taking values in such that for some sequence of constants , where is separable and takes values in . Then , as a stochastic process indexed by .

Proof of Theorem 4.1.

Proof of Theorem 4.2.

To prove Theorem 4.3, we recall Theorem 3.9.11 of \citeasnounvdV. Here we use the notation for bootstrap convergence defined in Section 4.3.

Lemma B.2 (Delta-method for bootstrap in probability).

Let and be metrizable topological vector spaces, and is a compact subset of a metric space. Let be a Hadamard-differentiable mapping uniformly in at tangentially to with derivative . Let be a random element such that . Let be a stochastic map in , produced by a bootstrap method, such that . Then, , as a stochastic process indexed by .

Proof of Theorem 4.3.

The statement (1) follows directly from Lemma A.2, and Lemma B.2, by setting , , , , , , , and . The expression of is the Hadamard derivative in statement (b) of Lemma A.2. The statement (2) follows directly from Lemma A.3, and Lemma B.2, by setting , , , , , , , and . The expression of is the Hadamard derivative in statement (c) of Lemma A.3. ∎

Supplement to “The Sorted Effects Method: Discovering Heterogeneous Effects Beyond Their Averages”

Victor Chernozhukov, Iván Fernández-Val, Ye Yuo

Appendix C Notation

For a possibly multivariate random variable , denotes the interior of the support of in the part of the population of interest, denotes the distribution of over , and denotes an estimator of . We denote the expectation with respect to the distribution by . We denote the PE as , the empirical PE as , and , the gradient of . We also use to denote the minimum of and . For a vector , denotes the Euclidian norm of , that is , where the superscript T denotes transpose. For a non-negative integer and an open set , the class on includes the set of times continuously differentiable real valued functions on . The symbol denotes weak convergence (convergence in distribution), and denotes convergence in (outer) probability.

Appendix D Background on Differential Geometry

We recall some definitions from differential geometry that are used in the analysis. For a continuously differentiable function defined on an open set containing the set , is a critical point of on , if

| (D.10) |

where is the gradient of ; otherwise is a regular point of on . A value is a critical value of on if the set contains at least one critical point; otherwise is a regular value of on .

In the multi-dimensional space, a function can have continuums of critical points. For example, the function has continuums of critical points on the circles for each positive integer .

We recall now several core concepts related to manifolds from \citeasnounspivak-65 and \citeasnounmunkres-91.

Definition D.1 (Manifold).

Let , and be positive integers such that . Suppose that is a subspace of that satisfies the following property: for each point , there is a set containing that is open in , a set that is open in , and a continuous map carrying onto in a one-to-one fashion, such that: (1) is of class on , (2) is continuous, and (3) the Jacobian matrix of , , has rank for each . Then is called a -manifold without boundary in of class . The map is called a coordinate patch on about . A set of coordinate patches that covers is called an atlas.

Definition D.2 (Connected Branch).

For any subset of a topological space, if any two points and cannot be connected via path in , then we say that and are not connected. Otherwise, we say that and are connected. We say that is a connected branch of if all points of are connected to each other and do not connect to any points in .

Definition D.3 (Volume).

For a matrix with , , let , which is the volume of the parallelepiped with edges given by the columns of , .

The volume measures the amount of mass in of a -dimensional parallelepiped in , . This concept is essential for integration on manifolds, which we will discuss shortly. First we recall the concept of integration on parameterized manifolds:

Definition D.4 (Integration on a parametrized manifold).

Let be open in , and let be of class on , . The set together with the map constitute a parametrized -manifold in of class . Let be a real-valued continuous function defined at each point of . The integral of over with respect to volume is defined by

| (D.11) |

provided that the right side integral exists. Here is the Jacobian matrix of the mapping , and is the volume of matrix as defined in Definition D.3.

The above definition coincides with the usual interpretation of integration. The integral can be extended to manifolds that do not admit a global parametrization using the notion of partition of unity. This partition is a set of smooth local functions defined in a neighborhood of the manifold. The following Lemma shows the existence of the partition of unity and is proven in Lemma 25.2 in \citeasnounmunkres-91.

Lemma D.1 (Partition of Unity on of class ).

Let be a -manifold without boundary in of class , , and let be an open cover of . Then, there is a collection , where is defined on an open set containing for all , with the following properties: (1) For each and , , (2) for each there is an open set containing such that all but finitely many are on , (3) for each , , and (4) for each there is an open set , such that .

Now we are ready to recall the definition of integration on a manifold.

Definition D.5 (Integration on a manifold with partition of unity).

Let be an open cover of a -manifold without boundary in of class , . Suppose there is an coordinate patch , that is one-to-one and of class on for each . Denote . Then for a real-valued continuous function defined on an open set that contains , the integral of over with respect to volume is defined by:

| (D.12) |

provided that the right side integrals exist, where is a partition of unity on of class that satisfies the conditions of Lemma D.1. \citeasnoun[p. 212]munkres-91 shows that the integral does not depend on the choice of cover and partition of unity.

Appendix E Proofs of Appendix A

To analyze the analytical properties of the SPE-function, it is convenient to treat the PE as a multivariate real-valued function

where contains the set . Let be a distribution function. The distribution of with respect to is the function with

| (E.13) |

The SPE-function is the map

defined at each point as the left-inverse function of , i.e.,

| (E.14) |

From this functional perspective, the map is the result of applying a sorting operator to the map that sorts the values of in increasing order weighted by . The next subsections provide the proofs of 3 results:

-

1)

Lemma A.1, which characterizes some analytical properties of the distribution function and the sorted function ,

-

2)

Lemma A.2, which derives the functional derivatives of and with respect to and , and

-

3)

Lemma A.3, which derives the functional derivatives of the related classification operator with respect to , and .

E.1. Proof of Lemma A.1

We use the following results in the proof of Lemma A.1.

Lemma E.1.

If is on an open set , then for any compact subset of , the sets of critical points and critical values of on are closed.

Proof.

(1) Critical points: since is continuous on and is compact, the set of points such that is closed.

(2) Critical values: since is continuous and is compact, the image set is a compact set in . For any sequence of critical values in , there is a corresponding sequence in such that . Suppose converges to . By compactness of , we can find a converging subsequence of with limit such that . Then by continuity of , . By continuity of , , and therefore is a critical value of . Hence the set of critical values is closed. ∎

Lemma E.2.

For a compact set in a metric space , suppose there is an open cover of . Then there exists a finite open sub-cover of and , such that for every point , the -ball around is contained in the finite sub-cover.

Proof of Lemma E.2.

Since is a compact set in the metric space (with metric ), then any open cover of has a finite open subcover which covers .

Let . We prove the statement of the lemma by contradiction. Suppose for any , there exists some point such that and . Then, by compactness of there exists such that . Let be the limit of . By compactness of , . Since as and is an open cover of , there must be a open ball around such that , which contradicts with , for large enough. Therefore there must be an such that the -ball around any is covered by . ∎

Proof of Lemma A.1.

The proof of statement (2) follows directly from the inverse function theorem.

The proof of statement (1) is divided in two steps. Step 1 constructs a finite set of open rectangles that covers the set and has certain properties that allow us to apply a change of variable to the derivative of . Step 2 expresses the derivative as an integral on a manifold.

For a subset and , define . Similarly, for any and , define . Without loss of generality, we assume that only has one connected branch. We will discuss the case where has multiple connected branches at the end of the proof of this lemma.

Step 1.

For any regular value , the set is a -manifold in of class by Theorem 5-1 in \citeasnoun[p. 111]spivak-65. Denote and for . These enlargements of the set are used to apply a change of variable technique to integrals on .

By assumptions -, there exists small enough and such that:

(1) and contains no critical values of on , and .

(2) .

(3) .

(4) For any , is a -manifold in of class .

Indeed, by Lemma E.1, the set of regular values is open. Therefore, there exists a small neighborhood with such that there exists no critical value of on in . Then any satisfies statement (1). Statements (2) and (3) follow by the compactness of , the continuity of mapping , and assumptions and . Statement (4) is implied by Theorem 5-1 in \citeasnoun[p. 111]spivak-65.

Next, we establish a finite cover of with certain good properties, for some .

For any , satisfies the properties (2)–(4) stated above. Consider the rectangles centered at where , with , . Let be such that:

which can be fulfilled by using small enough .

By continuity of , for small enough and any , there always exists an index such that since for all by the property (2) above, where . Also we can find a finite set of ’s, denoted as , such that forms a finite open cover of . We rename these open rectangles as , , where and , .

For a given , consider the center of , denoted as . Without loss of generality, we can assume that . Then, for all , . This means that is partially monotonic in on . By the implicit function theorem, there exists such that , for any and . Also by the implicit function theorem,

So because and . Therefore,

since , with and .

We can choose and , using small enough in order to fulfill the following property of : with small enough,

or geometrically, the tube does not intersect ’s faces except at the ones which are parallel to the vector . In such a case, we say that intersects at the axis . More generally, for all , intersects at axis , where is the center of . This property implies that is a well-defined injection from to , for , which will allow us to perform a change of variable in the equation (E.16). Such a property holds for any .

Step 2.

Let be such that . We first apply partition of unity to the open cover of of Step 1.

By Lemma D.1, for the finite open cover of the manifold , we can find a set of partition of unity , on with the properties given in the lemma.

Our main goal is to compute

Denote , for any and . Denote , and .

For any , . Therefore, the properties (1) to (4) stated in Step 1 are satisfied when we replace by . Note that,

| (E.15) |

This third and fourth equalities hold because for any and , respectively.

For any , without loss of generality, suppose that intersects at the axis. Then, on , and we can apply the implicit function theorem to show existence of the implicit function such that for all . Define the injective mapping as:

In equation (E.15), we apply a change of variable defined by the map to the -th element of the sum:

| (E.16) |

The second equality follows because

where .

The last equality follows as , because by the uniform continuity of

over . In (E.16), the last component of is fixed to be without being specified for simplicity. We will maintain this convention in the rest of the proof whenever the variable of integration is (excluding ).

Next, we write the first term of (E.16) as an integral on a manifold, which is

| (E.17) |

Summing up over and in (E.16) and using Definition 5.5,

| (E.18) |

Let us explain(E.17). Equation (E.17) is calculated using the following fact: The mapping such that has Jacobian matrix

where . The volume of is , where . By the Matrix Determinant Lemma,

Hence, the left hand side of equation (E.17) is:

and it can be further re-expressed as the right side of (E.17) using Definition 5.4.

Finally, if has multiple branches but a finite number of them, we can repeat Step 1 and 2 in the proof above for each individual branch. Since the number of connected branches is finite, the remainders in equation (E.19) converge to uniformly. Thus, adding up the results for all connected branches in equation (E.19), the statements of Lemma A.1 hold. ∎

E.2. Proof of Lemma A.2

We use the following results in the proof of Lemma A.2.

Lemma E.3 (Continuity).

Let be a measurable function defined on which vanishes outside , where is a constant. Let be a regular value of on . Suppose is continuous on for any and some small such that . Then, is continuous on .

Proof.

First, we follow Step 1 in the Proof of Lemma A.1. Suppose we have a set of open rectangles such that for any , where is a small enough positive number, . Moreover, let be small enough such that all are regular values. By compactness of , is bounded and uniformly continuous on .

By construction, , , satisfies that intersects at axis , for any .

Then, following Step 2 in the Proof of Lemma A.1, there exists a set of partition of unity functions of , .

Then, for any , by the definition of partition of unity,

| (E.20) |

The equation (E.20) holds since for all .

To show that converges to as converges to , it suffices to show that converges to as converges to , for all and .

Without loss of generality, assume that intersects at axis . Then, there exists constants and such that and for all , .

We can apply the implicit function theorem to establish existence of the function such that for all . Define the one-to-one mapping as:

where for . Note that and are both functions.

For any such that , by the change of variables we have:

| (E.21) |

Since for all and and , , and are uniformly continuous functions on , conclude that the map

is uniformly continous on .

Since and is bounded, it immediately follows that is continuous at , and hence

is continuous at .

This argument applies to every , and by compactness of the continuity claim extends to the entire . ∎

Lemma E.4 (Hadamard differentiability of and ).

Suppose that - hold. Then:

(a) The map is Hadamard-differentiable uniformly in at tangentially to , with the derivative map defined by

(b) The map is Hadamard-differentiable uniformly in at tangentially to , with the derivative map defined by:

Proof of Lemma E.4.

To shows statement (a), for any under sup-norm such that , and , we consider

By assumption, any function is bounded and uniformly continuous on . Hence, is uniformly bounded for , since in sup-norm.

For any we consider a procedure similar to Lemma A.1. We use the same notation as in Step 1 of the proof of Lemma A.1. Suppose for small enough, we have a rectangle cover of such that for all , intersects each at some axis , . As before, there is a partition of unity on the cover sets . As in the proof of Lemma A.1, we can rewrite

Then, for any fixed positive number , there exist large enough such that . Moreover, for any , and large enough ,

As in Step 2 of the proof of Lemma A.1, suppose intersects at . Define the parametrization

where is the implicit function derived from equation , for any . Therefore, for large enough ,

Next, by a change of variables from to ,

where the inequality in the above equation holds by continuity of . More specifically, fixing and , for ,

and

as . The last equality above holds because for all .

Since and are fixed for any , and is bounded by some absolute constant, and , we can let to conclude that:

The right side is given by:

On the other hand,

for some . So,

And, by a change of variables from to ,

Let and , it follows that