Calibration and simulation of arbitrage effects in

a non-equilibrium quantum Black-Scholes model

by using semiclassical methods

An interacting Black-Scholes model for option pricing, where the usual constant interest rate is replaced by a stochastic time dependent rate of the form ,

accounting for market imperfections and prices non-alignment, was

developed in [1]. The white noise amplitude , called

arbitrage bubble, generates a time dependent potential which

changes the usual equilibrium dynamics of the traditional Black-Scholes

model. The purpose of this article is to tackle the inverse problem, that is, is it possible to extract the time dependent potential and its associated bubble shape from the real empirical financial data? In order to give an answer to this question, the interacting

Black-Scholes equation must be interpreted as a quantum Schrödinger

equation with hamiltonian operator , where

is the equilibrium Black-Scholes hamiltonian and

is the interaction term. If the term is small enough, the

interaction potential can be thought as a perturbation, so one can compute the solution of the interacting Black-Scholes equation

in an approximate form by perturbation theory. In [2]

by applying the semi-classical considerations, an approximate solution

of the non equilibrium Black-Scholes equation for an arbitrary bubble

shape was developed. Using this semi-classical solution and

the knowledge about the mispricing of the financial data, one can

determinate an equation, which solutions permit obtain the functional form

of the potential term and its associated bubble .

In all the studied cases, the non equilibrium model performs a better

estimation of the real data than the usual equilibrium model. It is

expected that this new and simple methodology for calibrating and

simulating option pricing solutions in the presence of market imperfections,

could help to improve option pricing estimations.

1 Introduction

For almost 35 years, since the seminal articles by Black and Scholes (1973, [3]) and Merton (1973, [4]), the Black-Scholes (B-S) model has been widely used in financial engineering to model the price of a derivative on equity. In analytic terms, if and are the risk-free asset and underlying stock prices, the price dynamics of the bond and the stock in this model are given by the following equations:

| (1) |

where , and are constants and is a Wiener process. In order to price the financial derivative, it is assumed that it can be traded, so one can form a portfolio based on the derivative and the underlying stock (no bonds are included). Considering only non dividend paying assets and no consumption portfolios, the purchase of a new portfolio must be financed only by selling from the current portfolio. Here, denote the option price, the portfolio and the price vector of shares. Calling the value of the portfolio at time ; the dynamic of a self-financing portfolio with no consumption is given by

| (2) |

In other words, in a model without exogenous incomes or withdrawals,

any change of value is due to changes in asset prices.

Another important assumption for deriving B-S equation is that the market is efficient in the sense that is free from arbitrage possibilities. This is equivalent with the fact that there exists a self-financed portfolio with value process satisfying the dynamic:

| (3) |

which means that any locally riskless portfolio has the same rate of return than the bond.

For the classical model presented above, there exists a

well known solution for the price process of the derivative

(see, for example [5]). Given its simplicity, this formulation

can be described as one of the most popular standards in the profession.

Today however, it is possible to find models that have relaxed almost

all of the initial assumptions of the Black-Scholes model, such as

models with transaction costs, different probability distribution

functions, stochastic volatility, imperfect information, etc; all

of which have improved the prediction capabilities of the original

B-S model. See [5]-[8] for some complete reviews

of these extensions.

Some attempts to improve the predictions of the Black-Scholes models, that take into account deviations of the equilibrium in the form of arbitrage situations, have been developed in [1], [9], [10], [11]. In this case, some of these models assume that the return from the B-S portfolio is not equal to the constant risk-free interest rate, but instead, the no arbitrage principle (3) is modified according to the equation

| (4) |

where is a random arbitrage return. This formulation

gives great flexibility to the model, since can be seen

as any deviations of the traditional assumed equilibrium, and not

just as an arbitrage return. For instance, Ilinski (1999, [12])

and Ilinski and Stepanenko (1999, [13]) assume

that follows an Ornstein-Uhlenbeck process. Deviation

from the non arbitrage assumption implies that investors can make

profit in excess from the risk-free interest rate. For example, if

is greater than zero, then what one can do is: borrow from the bank,

paying interest rate , invest in the risk-free rate stock portfolio

and make a profit. Alternatively, one could go short the option, delta

hedging it.

The object of this paper, is to study the arbitrage effects on the option prices.

This study will have two principal components:

1) Calibration: one hopes to obtain a measure of the arbitrage effects

from the empirical financial data, and

2) Simulation: the above measure can be used to obtain the “improve”

option price and compare it with the usual Black-Scholes model and

the real option prices.

For this, it is assumed that arbitrage can be modelled using equation

(4), so one will consider the B-S model in

(1) and self-financing portfolio condition in (2)

and in what follows the following arbitrage condition is assumed:

| (5) |

where is a given deterministic function called “arbitrage bubble” [1] and is the same Wiener process in the dynamic of the underlying stock . Equation (5) will generate a non equilibrium Black-Scholes model. Note that condition (5) can be rewritten as

| (6) |

where is a white noise. This can be interpreted as a stochastic

perturbation in the rate of return of the portfolio with amplitude

: .

As it is well known, in a perfectly competitive market, assumed by

the original B-S model, the action of buyers and sellers

exploiting the arbitrage opportunity will cause the elimination of

the arbitrage in the very short run, so in our setting one will considered

implicitly the speed of market’s adjustment by modelling an “arbitrage

bubble”, which can be defined in duration and size, taking this

way into account the market clearance power. All this information

is contained in the function . In fact, in [1]

was showed that, for an infinite arbitrage bubble the non equilibrium

Black-Scholes model goes to the usual Black-Scholes model, so (5)

accounts implicitly for the market power clearance.

In [9]-[13] different generalizations of the Black-Scholes model are proposed. These models include a stochastic rate model whose dynamic is generated by a second Brownian motion independent of the asset Brownian motion. In a sense, these models are inspired by “stochastic volatility ideas”.

What we are trying to do here, is to incorporate arbitrage effects, but as close as possible to the original Black-Scholes model, which has only one source of randomness (associated with the asset price S) and where the B bonus dynamics is completely deterministic.

The central idea is that arbitrage effect can change the portfolio returns in a random fashion, and the source of randomness must be generated by the same asset Brownian motion. It is in that sense that the term “endogenous stochastic arbitrage” appears in the title of paper [1]. In that setting, the only remaining degree of freedom necessary is the amplitude of such a Brownian motion that is expressed in equation (5).

Although, equation (5) can be rewritten as a stochastic rate model as in equation (6), it is not clear if such interpretation is well defined in mathematical terms, or if even it is integrable. So, our point of view is not seeing our model as a stochastic rate model, but instead as a “perturbed portfolio return model”, defined by equation (5).

Thus, one is assuming a model-dependent arbitrage, where the arbitrage

possibilities are modelled with the same stochastic process that govern

the underlying stock. This assumption allows us to link the arbitrage

equation to the B-S original model111Otherwise, the arbitrage should be modelled exogenously to the B-S

model. This assumption is reasonable from a theoretical perspective for

some kinds of arbitrages, which are inherent to the underlying asset,

and endogenous in nature to the asset in analysis. The validity of

this maintained hypothesis has been tested empirically bellow, see

for instance [14].

In [1] analytical solutions of the non equilibrium Black-Scholes model were found for a time dependent “step function” arbitrage bubble for an option with maturity :

| (7) |

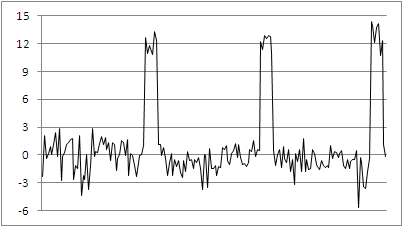

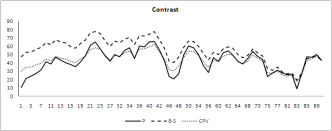

This particular shape of the bubble was motivated by an empirical study of futures on the index between September 1997 and June 2009. There, through the empirical analysis of the future mispricing, one can get the shape of the arbitrage bubble, which in that case corresponds roughly to a step function shape, as is showed in the figure below:

So in the option pricing context, one can naturally ask:

Can the shape of the arbitrage bubble be obtained from an empirical

analysis of the option mispricing, using the same approach for futures

on the index given in [1]?

The object of this paper is to show that the answer is positive and to

develop a methodology for extracting the arbitrage bubble from the

empirical financial data through the analysis of the option mispricing.

In order to do that, one will need to use some result of semi-classical

approximations applied to option pricing as develop in [2].

There, an approximate solution for the non equilibrium Black-Scholes

equation in the presence of an arbitrary arbitrage bubble was constructed.

This semi-classical solution plus the option mispricing data, permit

to obtain a non linear equation for the arbitrage bubble.

By solving this equation by means of numerical methods

the approximate shape of the arbitrage bubble can be obtained.

Then, taking this arbitrage bubble back to the non equilibrium Black-Scholes

equation, one can determinate the “exact” interacting option price

solution by means of a Crank-Nicolson method and compare it with the

usual equilibrium Black-Scholes solution. In all studied cases, the

non equilibrium solution performs a better numerical estimation for

the empirical data than the usual Black-Scholes solution.

To proceed and to make the paper self contained, section 2 review the interacting Black-Scholes model according to [1] and section 3 gives it interpretation as a quantum model. The section 4, quickly review the principal results of applying semi-classical quantum ideas to the interacting Black-Scholes model as developed in [2]. In section 5, the calibration problem is analysed, that is, how to estimate the interaction potential in the non equilibrium Black-Scholes framework, and the deduction of an equation which permits to found arbitrage bubble from the real financial data. In section 6, the simulation problem is developed to obtain the exact option price solution of the non equilibrium model, for several different data set. Finally, in section 7, final conclusion and future prospects are given.

2 The non equilibrium Black-Scholes model

Following [1] we will find the price dynamics of the financial derivative under the endogenous arbitrage condition (5). We are going to derive the price dynamic as the solution of certain boundary value problem. In what follows we consider the price process depending on , , but we omit this dependence for the sake of simplicity.

Using Itô calculus we get:

Given the dynamic for in (1) we have:

Self-financing portfolio condition in (2) can be understood as . Considering this and (5) together and replacing dynamics for and we get:

Collecting - and - terms we have:

| (8) |

The condition for existence of non-trivial portfolios satisfying (8) give us the following:

Given the B-S model for a financial market in (1), self-financing portfolio condition (2) and stochastic arbitrage condition in (5) the price process of the derivative is the solution of the following boundary value problem in the domain .

| (9) |

for constant , , , any function

and a simple contingent claim .

Thus, equation (9) shows a particular type of arbitrage,

that occurs when the underlying asset and its arbitrage possibilities

are generated by a common and endogenous stochastic process. This

formulation is fairly general, in the sense that could take

any functional form. This function will be called the arbitrage

bubble. Note that when , the standard equilibrium B-S

model is recovered.

It is important to stress here that the model generated by equation (9) is an out-of- equilibrium model, in the sense that, it does not satisfy the martingale hypothesis for .

3 The interacting Black-Scholes model as a Schrödinger

quantum equation.

Black-Scholes equation in the presence of an arbitrage bubble (9) can be written as

| (10) |

where

is the usual arbitrage free Black-Scholes operator. The factor

| (11) |

can be interpreted as an effective potential induced by the arbitrage bubble . In this way, the presence of arbitrage generates an external time dependent force, which have an associated potential . Then the interacting Black-Scholes model developed in [1] corresponds, from a physics point of view, to an interacting particle with an external field force. Obviously, when arbitrage disappear, the external potential is zero and we recover the usual Black-Scholes dynamics. One can also see, that the option price dynamics depends explicitly on the arbitrage bubble form . From a financial optics, the arbitrage bubbles should be time-finite lapse and they should have a characteristic amplitude. So, in general, arbitrage bubbles can be defined by three parameters: the born-time, dead-time and the maximum amplitude between these two times. In [2] an approximate analytical solution for the non equilibrium Black-Scholes equation, for an arbitrary arbitrage bubble form was found.

3.1 The quantum hamiltonian.

Following [2], where a Black-Scholes-Schrödinger model based on the endogenous arbitrage option pricing formulation introduced by [1] was developed, consider again the interacting Black-Scholes equation (9) and take the variable change , to obtain

and if we make a second (time dependent) change of variables we arrive to

where

Now we can state: Given the non equilibrium Black-Scholes model in (9) for the price of an option with arbitrage, if we define

the dynamics is given by

where

| (12) |

is the interaction potential in the space.

The last two equations can be interpreted as a

Schrödinger equation in imaginary time for a particle of mass

with wave function in an external time dependent field

force generated by . If we write the Schrödinger as

| (13) |

Following the arguments developed by Baaquie in [15] we can read the hamiltonian operator as

Since momentum operator in imaginary time is

we finally arrive to the quantum hamiltonian for the interactive Black-Scholes model as a function of the momentum operator.

3.2 The underlying classical mechanics.

In order to obtain a semi-classical approximation for the solution of the non equilibrium Black-Scholes model, we need develop the classical equation of motion, that is, the Newton equations associated to the quantum model. So, if we take the classical limit "" the quantum hamiltonian becomes the classical hamiltonian function

The classical hamiltonian equations

reduce in this case to

The corresponding lagrangian

becomes

| (14) |

The Euler-Lagrange equation

gives for this system, the following Newton equation

We can consider here some special cases in detail.

The time-independent arbitrage model

First, if the bubble depends only on S, that is , this imply that

and we have in this case the identity

so the Newton equation reads

or

where

The time-dependent arbitrage model

In the second case, the arbitrage bubble depends only on time coordinate so

and

so

The Euler -Lagrange equation reads now

that is

which can be easily integrated as

| (15) |

where and are arbitrary constants.

In that follows we consider arbitrage bubbles that are time dependent

only, that is,

The reasons to do that are:

(i) the model is more “simple” in mathematical terms and

(ii) the financial data available to us are time dependent but no

dependent.

In a further study we will analyse the behaviour of the interacting

Black-Scholes model for arbitrage bubbles that depends explicitly

on the underlying asset price .

Note that for the time dependent arbitrage bubble , the

potential in (11) and the potential in (12) are completely equivalent:

.

4 The semi-classical approximation

Semi-classical methods have been used to find approximate solutions

of the Schrödinger equation in different areas of theoretical physics,

such as nuclear physics [16], quantum gravity [17],

chemical reactions [18], quantum field theory [19],

path integrals [20]. When the system has interactions,

the semi-classical approach gives an approximate solution for the wave

function of the system, while for free interaction case, semi-classical

approximation can give exact results [21]. In this section,

following [2] we develop a financial application, based

on the quantum arbitrage model of the previous section.

In a general setting, the solution of the Schrödinger equation (13) can be written as

where is a specific contract (Call, Put, Binary Call…) in the space, and is the propagator which admits the path integral representation

where is the classical action evaluated over the path () and the integral is done over all paths that connect the points and . If one writes as and expands the action around the classical path, one has

(where all functional derivatives are evaluated on the classical path ) and integrate over all trajectories , the propagator becomes

If one consider contributions up to second order terms (see for example [20]), the semi-classical approximation for the propagator is given by

On the other hand, the solution for the option price in the space is then

so the propagator for the option price is, in the semi-classical approximation

| (16) |

In order to found the semi-classical approximation for the option price, in presence of a time dependent arbitrage bubble , we must obtain first the classical solution (15) for a time variable (), with the initial condition and final condition . This implies that the constant in (15) is given by

so the Lagrangian (14) evaluated over the classical path is

and the action evaluated over the classical path becomes finally

where

| (17) |

is the accumulative potential between and .

The semi-classical propagator in the space is then according to (16)

By using the transformation

and the fact that , one can now write the semi-classical propagator in the space as

| (18) |

so the semi-classical solution for the option price is then given by

| (19) |

Now, note that the Black-Scholes propagator is just the semi-classical propagator (18) evaluated at

| (20) |

so the pure Black-Scholes solution is

| (21) |

From (18) and (20) one can see that both propagators are related by

and from (19)

which due to (21), is equivalent to say

| (22) |

The last equation therefore, is the semi-classical approximation for the non equilibrium Black-Scholes

solution for the option price, in presence of an arbitrary time dependent arbitrage bubble .

Here is the arbitrage-free Black-Scholes solution for the specific option with contract and

is the accumulative potential given by (17).

In this way, the function renormalizes the bare arbitrage-free

Black-Scholes solution. One important fact of this last equation is

that it permits to obtain an approximation of our Black-Scholes-Schrödinger interacting

model from the classical Black-Scholes model, by means of a rescaling of the price variable, so usual computational codes can be easily

modified to obtain an approximation for the interacting model.

5 Interaction potential and arbitrage bubble calibration

Now finally, after a long trip on the interacting model and its semi-classical

approximation, we can tackle the main two point of this paper, that

is, the calibration and simulation problem for the arbitrage bubble

and for the option price solution of the non equilibrium Black-Scholes

model respectively.

In order to solve the calibration problem, consider the empirical

time-series of the underlying asset and the real price

of the option in the interval . One can

ask for the interaction potential function

associated to a time dependent arbitrage bubble that allows

the solution of equation (10) when

evaluated over to fit all the time-serie of .

One way to proceed is to take a definite functional form for the function with parameters . In this case the solution of (6) becomes a function of the vector and then, the set of coefficients can be determined minimizing the quantity

| (23) |

over all sets of coefficients . But it is not clear if

such a minimum exists or there exist several local minima and the

problem reduces to find the true one. Numerically this problem can

turn to be impossible to achieve. Moreover, our initial guess for

is a matter of taste, and it is not clear what the correct

initial functional form is and from which the minimization can start.

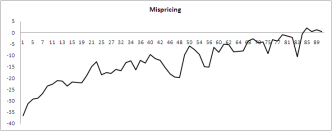

In order to determine a guess function for the potential we will follow a different path, based on the semi-classical approximation and the notion of mispricing. The mispricing, denoted by , is defined in [22] as the difference between the empirical option price and the value of Black-Scholes solution evaluated over the empirical underlying asset price

| (24) |

Naturally, the function above is known only over a discrete time set of points. Let be the exact potential originated by the exact arbitrage bubble which gives the correct empirical option price when the solution of the interacting Black-Scholes model (10) is evaluated over the empirical underlying asset price

| (25) |

the solution makes the value of the equation (23) be exactly zero. Now suppose that potential is weak ( ), in such a way that the semi-classical approximation for the option price is valid, so we can replace the option price by its semi-classical approximation (22)

| (26) |

where

| (27) |

so the mispricing equation (24) becomes an equation for the arbitrage bubble

| (28) |

Equation (28) is the most important equation of this paper, because it allows us, from the knowledge

about the empirical mispricing , to obtain an estimation of the interaction potential and the arbitrage bubble by doing the following steps:

1) Given the empirical mispricing in (24), the equation (28) can be solved for the function by the Newton-Raphson method for each time instant. In this way, is determinated in a discrete set of points.

2) Then, by a nonlinear regression one can

estimate a continuous curve that fits approximately this discrete set of points.

3) From the definition of in equation

(27) we get

| (29) |

and hence a time-dependent potential can be determined in the weak limit from the time variation of the nonlinear regression for .

4) From (27) one can obtain the arbitrage bubble according to

| (30) |

This procedure solves the calibration problem mentioned above at least in the weak limit. For the strong regime () the semi-classical approximation could not longer be valid, but the functional form of the potential given by (29) can still be a good starting point for obtaining an approximate value for the potential.

6 Numerical results and option price simulation

In order to test our method and solve the simulation problem for the option price solution of the non equilibrium Black-Scholes model, we simulate the behaviour of an European call option using the 90-days futures of the e-mini S&P 500 from September 1998 to June 2007. We set the contract having the same underlying asset, opening and expiring dates than the S&P 500 futures. We establish the option strike price as the underlying price at the opening date of the contract, assuming the market is going to be flat, in such a way that the option price is

| (31) |

where will be the empirical simulated option market price at -day, is the e-mini S&P 500 future price and is the option strike price. As it is well known E-mini S&P 500 options are priced in index points up to two decimals. One E-mini S&P 500 option can be exercised into one E-mini S&P 500 futures contract and since each contract has a multiplier of $50, the option price must also be multiplied by $50 to get a corresponding dollar value and every one point change in the price of the option or the underlying futures for that matter is worth $50 per contract.

Here, we specify the e-mini S&P 500 futures contracts used to simulate the option:

| Table 1: e-mini contracts |

|---|

| 1) e-mini S&P 500 12/03/1998 - 10/06/1998 |

| 2) e-mini S&P 500 10/09/1998 - 09/12/1998 |

| 3) e-mini S&P 500 10/12/1998 - 09/03/1999 |

| 4) e-mini S&P 500 09/06/2005 - 07/09/2005 |

| 5) e-mini S&P 500 07/09/2006 - 06/12/2006 |

| 6) e-mini S&P 500 07/12/2006 - 07/03/2007 |

| 7) e-mini S&P 500 08/03/2007 - 06/06/2007 |

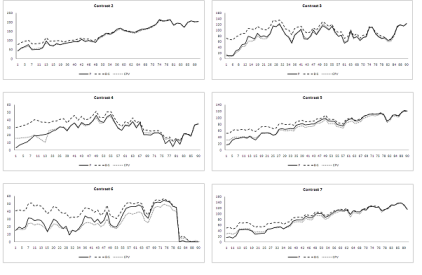

We will show our results in the case of the first contract (e-mini S&P 500 from 12/03/1998 to 10/06/1998). Firstly, we compute the mispricing in (24) between the simulated option price and the Black-Scholes price (see figure 2). For this last calculation, we estimate the standard deviation of the underlying returns from the previous 90 days and we take the three-months USA Treasury rate at the initial day of the contract as the risk-free rate. The estimated numerical values in fact are and .

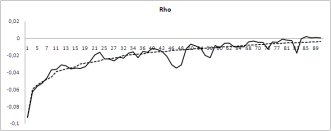

Now we can solve equation (28) via Newton-Raphson to obtain the empirical function daily for this contract as we can see in Figure 3. We propose then a continuous potential model for this function of the form and perform a non-linear Levenberg-Marquardt regression in order to fit parameters , and . The estimated parameter values are , and and figure 3 shows the results.

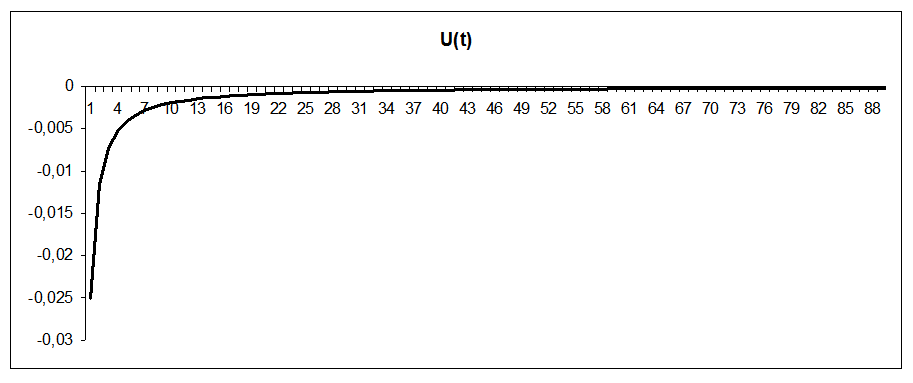

At this point, we can obtain the time-dependent potential by using equation (29)

| (32) |

as shown in figure 4.

Now by replacing the continuous potential in the interacting Black-Scholes equation (10) and integrating it by means of the Crank-Nicholson method, we obtain the interacting solution for the option price of a call option (figure 5).

Clearly, the calibration of the potential allows us to fit a more exact

price than that of the traditional Black-Scholes model without considering

arbitrage. One can test the behavior of the interacting versus

the usual Black-Scholes models for option pricing in terms of

the performance measure discussed before. The computed

values of the are: for the Black-Scholes model

and for the interacting Black-Scholes model, which difference is clearly visible in figure 5.

When we use our calibrated model with its respective potential for simulating the rest of the contracts considered in our series (table 1), we find similar results, that in all the cases defeat Black-Scholes predictions as showed in figure 6:

7 Conclusions

In this work, we have calibrated the arbitrage effects for a non equilibrium

quantum Black-Scholes model of option pricing. This calibration procedure

rests heavily on the semi-classical approximation of the interacting

Black-Scholes model, which permits to construct an equation for

the interaction potential, from which the arbitrage bubble and the interaction potential can be

estimated. By using this estimated potential, we can simulate

the price trajectory of a real call option for several contracts of

the S&P index, which allow to take into account any market imperfection

and prices desaligment. Even though we use a semi-classical approximation

for the solution of the interacting Schrödinger equation, the results

are extremely good in predicting the real option price and its trajectory

for every contract simulated.

Since in real life, market imperfections always happen, almost on

a regular basis, and hence arbitrage processes form part of the normal

operation of the stock exchange, logically mispricing are always going

to exist. If we could calibrate this mispricing using the potential

of our interacting Black-Scholes, even in a small part, it is expected

that our results are always going to outperform the traditional Black-Scholes

formulation. In this context, we think this model and its calibration

procedure could be used very easily to simulate in a more exact fashion

option pricing of any underlying asset.

Future research could be directed to capture different potential

patterns for different underlying assets and different market situations.

Even in this case the potential is short-lived and circumstantial,

for example in the case of bubbles, rebounds, crises or critical information

(for example, when Bernanke talks!), it is possible to use our methodology

to capture the potential of the contract in a similar situation and

used to simulate the new contract. Alternatively, if the situation

is normal and no special situations are foreseen, a good practice could

be using the contract immediately before in order to calibrate the

potential and hence our quantum model; considering the reasons given

above, in almost all the cases it is expected our model will defeat

the traditional Black-Scholes model.

References

- [1] M. Contreras, R. Montalva, R. Pellicer and M. Villena, Dynamic Option Pricing with Endogenous stochastic Arbitrage, Physica A: Statistical Mechanics and its Applications Vol. 389, No. 17, (2010) 3552–3564.

- [2] M. Contreras, R. Pellicer, A. Ruiz and M. Villena, A Quantum Model of Option Pricing:When Black-Scholes meets Schrödinger and its semi-classical limit, Physica A: Statistical Mechanics and its Applications, Vol. 389, No. 23, (2010) 5447–5459

- [3] F. Black and M. Scholes, The Pricing of Options and Corporate Liabilities., Journal of Political Economy. 8,31 (1973) 637–654.

- [4] R.C. Merton, Theory of Rational Option Pricing., Bell Journal of Economics and Management Science. 4,1 (1973) 141–183.

- [5] T. Björk, Arbitrage Theory in Continuous Time, Oxford University Press, (1998).

- [6] D. Duffie, Dynamic Asset Pricing Theory. 2nd Edition, Princeton University Press: New Jersey,1996.

- [7] J. C. Hull, Options, futures, and other derivatives, Englewood Cliffs, NJ, Prentice-Hall,1997.

- [8] P. Wilmott, Derivatives: The Theory and Practice of financial engineering., J. Wiley, (1998).

- [9] M. Otto, Stochastic Relaxational Dynamics Applied to Finance: Towards Non-Equilibrium Option Pricing Theory., Internal J. Theoret. and Appl. Fin. 3,3 (2000), 565.

- [10] S. Panayides, Arbitrage opportunities and their implications to derivative hedging., Physica A: Statistical Mechanics and its Applications. Elsevier (2006).

- [11] S. Fedotov and S. Panayides, Stochastic arbitrage return and its implication for option pricing., Physica A: Statistical Mechanics and its Applications. Elsevier (2005).

- [12] K. Ilinski, How to Account for the Virtual Arbitrage in the Standard Derivative Pricing., preprint.cond-mat/9902047 (1999).

- [13] K. Ilinski and A. Stepanenko, Derivative Pricing with Virtual Arbitrage., preprint.cond-mat/9902046 (1999).

- [14] K. Ilinski,Physics of Finance: Gauge Modelling in Non-equilibrium pricing, Wiley (2001).

- [15] Baaquie, B. Quantum Finance, Cambridge University Press, (2004).

- [16] R. Schaeffer, Theoretical Methods in Medium Energy and Heavy Ion Physics, K.W. McVoy, W.A.Friedman Eds, Nato Advanced Studies Institute Series B38 (1978) 109 p189.

- [17] G. W. Gibbons and S. Hawking, Action integrals and partition functions in quantum gravity, Phys. Rev. D vol. 15 n 10 (1977) 2752.

- [18] S. Keshavamurhy, semi-classical methods in chemical reaction dynamics, Ph. D. thesis, Chemistry department University of California, (1994)

- [19] V. Riva, semi-classical methods in 2D QFT: spectra and finite size effects, Ph. D. thesis (2004), arXiv:hep-th/0411083v1.

- [20] M. Chaichian and A. Demichev Path Integrals in Physics Vol. I, Institute of Physics Publishing IOP (2001)

- [21] H. Kleinert Path Integrals in Quantum Mechanics, Statistic, Polymer Physics, and Financial Markets. World Scientific Publishing Company, 4 edition (2006)

- [22] Lo, A. W. and MacKinlay, A. C., A Non-Random Walk Down Wall Street, Princeton University Press, (1999).