Monte Carlo versus multilevel Monte Carlo in weak error simulations of SPDE approximations

Abstract.

The simulation of the expectation of a stochastic quantity by Monte Carlo methods is known to be computationally expensive especially if the stochastic quantity or its approximation is expensive to simulate, e.g., the solution of a stochastic partial differential equation. If the convergence of to in terms of the error is to be simulated, this will typically be done by a Monte Carlo method, i.e., is computed. In this article upper and lower bounds for the additional error caused by this are determined and compared to those of , which are found to be smaller. Furthermore, the corresponding results for multilevel Monte Carlo estimators, for which the additional sampling error converges with the same rate as , are presented. Simulations of a stochastic heat equation driven by multiplicative Wiener noise and a geometric Brownian motion are performed which confirm the theoretical results and show the consequences of the presented theory for weak error simulations.

Key words and phrases:

(multilevel) Monte Carlo methods, variance reduction techniques, error simulation, stochastic partial differential equations, weak convergence, upper and lower error bounds1991 Mathematics Subject Classification:

65C05, 60H15, 41A25, 65C30, 65N301. Introduction

Weak error analysis for approximations of solutions of stochastic partial differential equations (SPDEs for short) is one of the topics that is currently under investigation within the community of numerical analysis of SPDEs. The goal of weak error analysis is to quantify how well we can approximate a quantity of interest that depends on the solution of an SPDE. While weak convergence rates for equations driven by additive noise are already available (see, e.g., [9, 1, 16, 6] and references therein), convergence rates for fully discrete approximations of SPDEs driven by multiplicative noise are still under consideration. First results for semi-discrete approximations in space or time are available (cf., e.g., [8, 2, 7, 12]) that suggest that one can, as in the case of additive noise, expect a weak convergence rate of twice the order of the strong one, i.e., of mean square convergence. Nevertheless, the simulation of weak error rates has caused problems so far and results are rarely available. First attempts can be found in [17, 18].

There are several factors that cause problems in the simulation of weak error rates of SPDE approximations but one of the main reasons is the computational complexity of simulating the solution on a fine grid. To give estimates on quantities of interest, which include the approximation of an expectation, the computational complexity is multiplied by the number of samples in Monte Carlo type methods that are necessary to obtain a reasonable result. We observed in practice that the simulated weak errors in our model problem are very small which in turn requires a far from realistic number of samples in Monte Carlo simulations to get acceptable results.

Motivated by this model problem, we look into the properties of the used estimators. While we are interested in simulating the error for a sequence of approximations converging to the real-valued random variable , the quantity is analytically not available. The standard approach is to approximate the expectation by a Monte Carlo estimator . We show in this manuscript that the additional error when using the estimator instead of the original error is for small errors essentially bounded from above and below by in mean square, where denotes the number of Monte Carlo samples. Furthermore, we consider the estimator instead and show that the bounds improve to , i.e., the number of samples is multiplied by the variance of the error, which can be seen as the strong error in the context of SPDE approximations. Finally, we substitute the Monte Carlo estimators by the corresponding multilevel Monte Carlo estimators and show that the additional error decreases to , i.e., to the error that we are interested in. We confirm the theoretical results in simulations of weak errors of the stochastic heat equation driven by multiplicative noise and a geometric Brownian motion. With the new estimators, we are to the best of our knowledge the first to be able to show weak convergence rates for an SPDE driven by multiplicative noise in simulations.

This manuscript is organized as follows. In Section 2 we recall Monte Carlo (MC for short) and multilevel Monte Carlo (MLMC) estimators for real-valued random variables. Upper and lower bounds for the approximation of by different Monte Carlo type estimators are shown. A short review on SPDEs and their approximation in space, time, and noise is given in Section 3 and available convergence results are recalled. Finally, simulation results of strong and weak errors using the estimators introduced in Section 2 for the stochastic heat equation driven by multiplicative noise and a geometric Brownian motion are shown in Section 4. These confirm the theoretical results of Section 2.

2. Monte Carlo versus multilevel Monte Carlo in error analysis

In this section we consider upper and lower bounds for the sampling errors that arise when performing weak error simulations in practice. It turns out that it is not surprising that it has not been possible so far to numerically implement weak error analysis for approximations of SPDEs driven by multiplicative noise. Nevertheless, this section is not SPDE specific but formulated more generally for real-valued, square integrable random variables. Quantities of interest in SPDE applications are examples of the framework considered in this section.

Let be a probability space and let us for denote by the space of all real-valued random variables such that . We recall that the Monte Carlo estimator of a real-valued random variable is given by

| (1) |

where is a sequence of independent, identically distributed random variables that have the same law as . Furthermore, the multilevel Monte Carlo estimator of a sequence of random variables is defined by

| (2) |

for , where consists of level specific numbers of samples in the Monte Carlo estimators. For more details on multilevel Monte Carlo methods the reader is referred to the large literature starting with [11, 10].

For later estimates we present the following well-known property of a Monte Carlo estimator, which is a specific form of the law of large numbers and can for example be found in [5, Lemma 4.1].

Lemma 2.1.

For and for it holds that

From now on let us consider a square integrable random variable , i.e., , and a sequence of approximations of . We assume that it is known that converges to in the sense that

In order to estimate convergence rates, one is interested in the simulation of , which usually cannot be done exactly but has to be approximated. If one were interested in estimating , the method of common random numbers would tell us that when and are positively correlated, it is better to use an estimator of the form rather than , since the latter has higher variance and both are unbiased. Now, when estimating , the estimators become and instead, neither of which is in general unbiased. In the following lemmas, we therefore show upper and lower bounds on the sampling errors

and

in mean square sense.

Proposition 2.2.

The sampling error of approximating by is bounded from below by

and from above by

Proof.

To prove the proposition let us first observe that

which implies with Lemma 2.1 and since is an unbiased estimator of that

Using this observation we obtain for the squared sampling error that

To find the lower bound, we observe that

by the properties of the expectation and Hölder’s inequality. Setting

which is a positive quantity, we therefore obtain the inequality

This is solved using the non-negativity of by

which finishes the proof of the lower bound.

For the upper bound we apply the reverse triangle inequality to obtain that

where the last step follows from Lemma 2.1. ∎

Having shown that for the sampling error is essentially bounded from below and above by in terms of the number of Monte Carlo samples when simulating , we continue with the sampling error for . It turns out that this decays for a fixed number of Monte Carlo samples with the square root of the variance of .

Proposition 2.3.

The sampling error of approximating by is bounded from below by

and from above by

Proof.

The proof of the lower bound is performed in the same way as that of Proposition 2.2. The only difference is that we have to simplify instead of , which we do in what follows. Therefore, let us observe that due to the properties of the variance and the unbiasedness of the Monte Carlo estimator

The independence of the random variables in the Monte Carlo estimator and the Bienaymé formula imply that

which overall leads to

The proof of the lower bound is finished by applying this formula in the proof of Proposition 2.2 and calculating accordingly.

For the upper bound we observe that

again by the reverse triangle inequality and Lemma 2.1, which finishes the proof. ∎

We first remark that the upper bounds in Proposition 2.2 and Proposition 2.3 were already obtained in the context of weak errors for SPDE approximations in [19, Proposition 5.4].

From the upper bound in Proposition 2.2 we learn that the sampling error will not be worse than the Monte Carlo error. At the same time, under the assumption that the quantity of interest is very small, we also see that the lower bound implies that we are not able to do better. Therefore, the sampling error is essentially bounded from below and above by the Monte Carlo error. This is not surprising but proves how heavily the simulation relies on the number of Monte Carlo samples for small errors . For relatively cheap computations of samples of for arbitrarily large , this is no problem. Nevertheless, in our context, where and are functionals of the solution to an SPDE and its approximation, respectively, the computation is very expensive and the errors are usually very small compared to their variance. Therefore, it is of no surprise that weak error simulations for SPDEs are still missing in the literature or that many people have failed to simulate them by Monte Carlo methods. One example of a failure with the standard estimator is shown in Section 4.

Looking into Proposition 2.3, we see that we obtain similar upper and lower bounds but instead of , the Monte Carlo error is multiplied by , which is usually smaller than and also decrease in if is a sequence of approximations that converges in to . Therefore we expect faster convergence for the estimator in Proposition 2.3 than in Proposition 2.2. This is tested and confirmed in Section 4 for a stochastic heat equation driven by multiplicative noise and a geometric Brownian motion.

As a second step in the error analysis, we now consider upper and lower bounds for the sampling error if multilevel Monte Carlo estimators are used instead of the corresponding singlelevel ones, which we discussed above. The results are obtained in a similar way as before.

Proposition 2.4.

The sampling error of approximating by is bounded from below by

and from above by

Proof.

The lower bound is again proven in the same way as in Proposition 2.2, where the only difference is in the computation of , which we include for completeness. We obtain by the independence of the Monte Carlo estimators on different levels, its unbiasedness, and by Lemma 2.1 that

For the upper bound we apply after the reverse triangle inequality the same arguments as in the previous computation which yield

This finishes the proof of the proposition. ∎

Here the performance of the upper and lower bound depends on the choice of the sample sizes for the different levels of the multilevel Monte Carlo estimator. In Theorem 1 in [18] it is assumed that there are upper bounds for and . If we assume that we know the errors exactly, we can set and in the notation of that theorem in [18] and choose the sample sizes accordingly. This is made precise in the following corollary that states that the correct choice of samples leads to a sampling error of the same size up to a constant as which we would like to observe.

Corollary 2.5.

Choosing for a fixed level the sample sizes in the multilevel Monte Carlo estimator and for and some it holds that

and

where denotes the Riemann zeta function. Therefore,

i.e., the sampling error converges with the same rate as .

Proof.

Let us first observe that for we have that . This implies with the given choices of , , that

as well as

We observe next that

for all and plug the obtained inequalities into the equations in Proposition 2.4 to finish the proof of the corollary. ∎

For completeness we include the equivalent statement to Proposition 2.3 for the multilevel Monte Carlo estimator, but we remark that it is of no practical interest. This is due to the fact that in particular has to be computed, i.e., many samples of the exact solution must be generated, which is computationally too expensive and destroys the idea of multilevel Monte Carlo methods.

Proposition 2.6.

The sampling error of approximating by is bounded from below by

and from above by

Proof.

The proof is again performed in the same way as that of Proposition 2.2, where it is essential to derive

Due to the repetition in techniques and the rather theoretical nature of the claim we leave further details of the proof to the interested reader. ∎

3. Approximation of mild SPDE solutions

In this section we employ the framework of [17] in a simplified setting and recall some of the results of that monograph. We provide a noise approximation result for a stochastic evolution equation with multiplicative noise in the very end of this section. Let be the space of square integrable functions on the unit interval with inner product given by , which is a real separable Hilbert space with orthonormal basis , where . Let , where is the space of all bounded linear operators from to , be a self-adjoint, positive definite operator of trace class. We denote by the Hilbert space with inner product , where denotes the pseudo-inverse of . Furthermore, we let be the extension of the probability space in Section 2 with a normal filtration. We assume that is an - adapted -Wiener process. In this framework we consider for the stochastic partial differential equation

| (3) |

with initial condition , which we refer to as the one-dimensional heat equation driven by multiplicative Wiener noise. Here we denote by the Laplace operator with zero boundary conditions. It holds that has eigenbasis with eigenvalues and generates a -semigroup of contractions denoted by on . The fractional operator has domain for . It holds that is a separable Hilbert space when equipped with the inner product

We impose further assumptions on the parameters of (3) in what follows, which are stronger than Assumptions 2.13 and 2.17 in [17, Chapter 2] and hence guarantee the existence and uniqueness of a mild solution

| (4) |

Assumption 3.1.

Assume that the parameters of (3) satisfy:

-

(i)

The trace class operator is defined through the relation where for two constants and .

-

(ii)

Fix a parameter . The mapping satisfies for a constant

-

(a)

for all ,

-

(b)

for all ,

-

(c)

for all , and

-

(d)

for all basis vectors and ,

where denotes the space of Hilbert–Schmidt operators from to .

-

(a)

-

(iii)

Assume that is a deterministic initial value.

We remark that in the notation of Assumption 3.1(i), we may write in terms of its Karhunen–Loève expansion

| (5) |

where is a sequence of independent, real-valued Wiener processes.

In order to be able to simulate realizations of the mild solution (4), we approximate it by a Galerkin finite element method in space and an implicit Euler–Maruyama scheme in time. For this, let be the nested sequence of finite-dimensional subspaces, where is given for each by the family of continuous functions that are piecewise linear on the intervals of an equidistant partition of defined by for and zero on the boundary, where is assumed to be an integer.

We define the discrete operator on each by letting be the unique element of such that

for all .

For the discretization in time we define a uniform time grid with time step size by for , where is again assumed to be an integer. To be able to implement this approximation scheme on a computer, one must also consider a noise approximation, i.e., an approximation of the -Wiener process . One way of doing this is to truncate the Karhunen–Loève expansion (5), which has earlier been considered for example in [15, 14, 4, 3, 13]. This leads to the Wiener process

The fully discrete implicit Euler-Maruyama approximation of is then given in recursive form by

| (6) |

for with initial condition , where denotes the orthogonal projection onto . This scheme converges strongly with to the mild solution, which is stated in the following theorem that combines [17, Theorem 3.14] with an additional noise approximation.

Theorem 3.2.

Under Assumption 3.1 for fixed and the couplings , with , it holds that for all there exists a constant such that for all and

Proof.

The proof is the same as that of [19, Theorem 4.3] except that

is used in the estimate of in that proof, which does not change the final bound on . ∎

While strong approximations are well understood and proven for the considered framework, weak convergence rates in the sense of bounds of the error

where is a smooth functional, are still missing. Nevertheless, results on the convergence of approximations of SPDEs driven by additive noise (cf., e.g., [1, 16]) as well as semi-discrete approximations of either space (cf., e.g., [8, 2, 7]) or time (cf., e.g., [12]) suggest that the weak convergence rate is twice the strong one. This is in accordance with the results obtained in our simulations in Section 4, where we consider the case . Our choice of the test function ensures that the weak error is bounded by the strong error (cf., [17, Chapter 6] and [19, Chapter 5]).

4. Simulation

In this section simulation results that combine the theory of Section 2 and Section 3 are presented, i.e., weak errors of an SPDE approximation are computed with Monte Carlo and multilevel Monte Carlo methods and compared. In the setting of Assumption 3.1, we now fix the parameters , and and consider two choices of the operator .

The first operator is defined for and by

while the so called Nemytskii type operator is defined for by

These operators satisfy Assumption 3.1(ii) for and respectively, shown in [17, Section 6.4] and [17, Example 2.23].

The choice admits an analytical solution of (3) and for this the identities

| (7) | ||||

| (8) | ||||

| (9) |

hold for all . The numerical approximations of are now computed by first setting and then recursively solving the numerical equation

where the interpolation operator is defined by

and for , , we set

as well as

The replacement of the operator with mirrors to a large extent the setting of [17, Chapter 6], where the author notes that this is quite common in practice, and we note that the simulation results below indicate that the order of convergence is not affected. For refinement levels we set and, as a shorthand notation, we write for the end time evaluation of (6) with and . With these choices, by Theorem 3.2, we expect a strong convergence rate of order in time and by the usual rule of thumb that the weak rate of convergence is twice the strong one, we expect a weak rate of order .

The following simulations were performed on the Glenn cluster at Chalmers Centre for Computational Science and Engineering (C3SE) using the MATLAB Distributed Computing Server™. In all of them, we approximate for by .

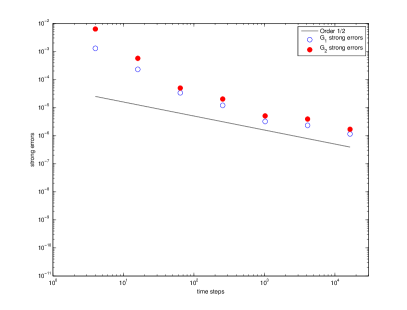

In Figure 1(a) an approximation of the strong error , i.e.,

is calculated for levels , where we replace the exact solution with a reference solution . For the reference solution is given by (7) truncated at , while for we let , since we do not have access to an analytic solution. We let and take samples. It should be noted that the same realizations of the -Wiener processes are used for the error computations on all levels. The observed error rate is asymptotically and therefore consistent with Theorem 3.2.

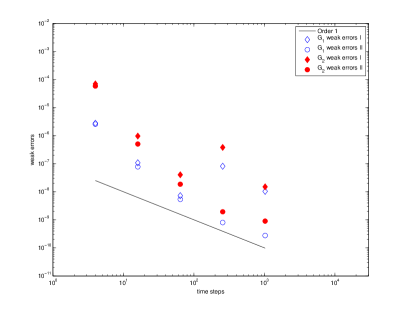

Next, we estimate the weak error and compare the performance of the singlelevel Monte Carlo estimators of Propositions 2.2 and 2.3. In Figure 1(b) the weak error is approximated with samples and . For the weak error approximation according to Proposition 2.2 with and we set

which we refer to as error of type I in what follows. Here we calculate , , using separate sets of realizations of -Wiener processes for each level . Furthermore, we replace by (9) evaluated at and truncated at in the case of . In the case of , we replace it instead by a reference solution with and , which is calculated on an independent set of -Wiener processes. For the weak error approximation according to Proposition 2.3

called error of type II in what follows, the samples of , , are computed on the same set of -Wiener processes. In the case of , we replace the exact solution with (8) evaluated at and truncated at . For we use again a reference solution . In said figure, i.e., Figure 1(b), we show the average of these estimators

for , where is a sequence of independent copies of and , to see how they perform in general. While the errors of type II supersede and then approach twice the strong order of convergence, the errors of type I do not. This is due to the limitation of the convergence by the number of Monte Carlo samples from below as shown in Proposition 2.2, that is to say, with a constant sample size we get a sampling error proportional to . This indicates that the observation of weak convergence results with a naive Monte Carlo estimator cannot be computed satisfactory in an acceptable time even for such a relatively easy example, where details on the computational times are collected for all estimators at the end of the example.

For the errors of type II the rate of convergence seems to decrease for the last level. This is explained by Proposition 2.3—in contrast to the the type I errors the sampling error is proportional to which is bounded by the strong error (measured in ) and therefore the rate of convergence starts to resemble .

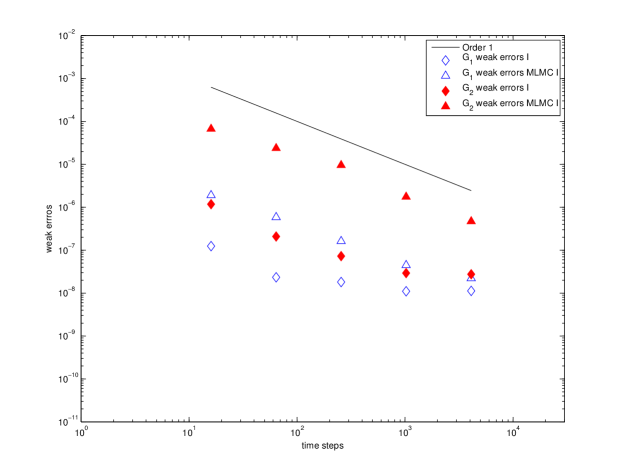

For the last set of simulations in Figure 2 we compare singlelevel type I errors to type I weak errors obtained using the multilevel Monte Carlo estimator (2) instead of the naive Monte Carlo approximation (1). For we set to obtain a series of fully discrete approximations , where for computational reasons we let . In the errors

we replace by the same quantities as for the type I errors in Figure 1(b). We note that each multilevel estimate is generated independently of one another so that the type I errors become a natural comparison. Figure 2 shows the multilevel error approximations for and the corresponding singlelevel errors of type I with sample sizes . We again show an average of these and let . From the figure we observe that the multilevel Monte Carlo estimators show the weak convergence rate, while the errors of type I fail. The latter errors are dominated by the sampling error as before, but for the multilevel estimator we know from Corollary 2.5 that the sampling error is bounded from above and below by the weak error. This explains why this approach succeeds in showing the expected weak convergence rates. The fact that the errors of type I are in total smaller than those obtained by the multilevel Monte Carlo simulation is due to the larger constant in the error estimates of Corollary 2.5 which can be reduced by enlarging the overall number of samples in the multilevel Monte Carlo method.

To give the reader an idea of the computational complexity of the shown convergence plots, we include the computing times, rounded off to the nearest hour, for 8 computing nodes with a total of 128 cores on the Glenn cluster of C3SE. The strong error plot Figure 1(a) cost 40 hours, while the weak error simulation of type II in Figure 1(b) took 102 hours. The reference solution used for the weak singlelevel errors of type I and the multilevel Monte Carlo errors for were computed in 13 hours. The costs for the weak errors of type I in Figure 1(b) are negligible (i.e., less than one hour). The computation of the multilevel errors in Figure 2 took 32 hours, while it took just 2 hours for the singlelevel errors. It is important to note that the computation of the type I errors was quite cheap since we could reuse the reference solution for . One should also be aware that we would have needed to increase the number of samples by at least a factor of to see the weak convergence for the type I error of , which would have increased the computational time to more than 8000 hours.

In conclusion we have seen in this section that the simulation of weak errors of SPDE approximations causes severe problems which we already expected out of the theory in Section 2. The use of a multilevel Monte Carlo estimator and a modified Monte Carlo estimator finally led to the expected weak convergence plots due to a faster convergence of the sampling error caused by the approximation of the expectation shown theoretically in Section 2. It is important to point out at this point here that these are to our knowledge the first successful simulations of weak errors for SPDEs driven by multiplicative noise.

Due to the limitations in computational complexity, we further illustrate the theoretical results of Section 2 with the simulation of an ordinary stochastic differential equation. The relative cheapness of such a simulation allows us to make the consequences of Section 2 even clearer than above. Let us therefore consider in what follows the easy example of a geometric Brownian motion in one dimension, i.e., the stochastic differential equation

| (10) |

with initial condition and , where and denotes a one-dimensional Brownian motion. The solution to the geometric Brownian motion is known to be

and the second moment can be computed explicitly to be

For the approximation let us consider an equidistant time discretization with time step size by for , where is assumed to be an integer. The Euler–Maruyama scheme is then given by the recursion

and , where denotes the approximation of . It is known that this scheme converges for the geometric Brownian motion with strong order , i.e.,

and with weak order , i.e., for sufficiently smooth test functions it holds that

where . Here the constant does not depend on .

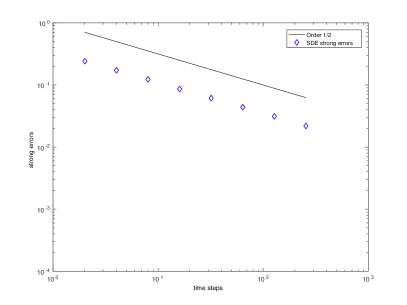

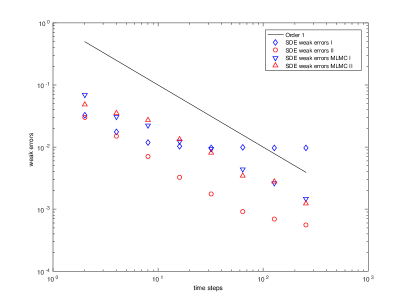

In the simulation of the four estimators from Section 2, let us consider the geometric Brownian motion (10) with , , , and . Furthermore, let be the number of samples in the Monte Carlo estimator and in the notation of the previous example with the same estimators as before . Then we obtain on time grids with grid points for the convergence plots for the simulated strong and weak errors which are presented in Figure 3.

In the weak error simulation, the function is used. We observe that the strong error in Figure 3(a) converges as expected with . In Figure 3(b) one sees that the type I estimator of Proposition 2.2 , which just does a Monte Carlo simulation on the approximate solution, only converges on the first two grid points with the desired order before as in the theory the Monte Carlo error dominates. At the same time, the type II estimator , which was considered in Proposition 2.3, behaves a lot better. It converges with the desired order up to the last two points, where the strong order of convergence dominates as predicted by the theory. Both the multilevel Monte Carlo estimator of type I from Proposition 2.4 and of type II from Proposition 2.6 converge with the desired order of convergence but the absolute errors are larger due to the larger constant in the overall error. This easy example, where all correct values were known and could be used for the computations of the exact solutions, shows clearly the behaviour that we expected from the theoretical upper and lower bounds on weak error estimators in Section 2.

References

- [1] Adam Andersson, Raphael Kruse, and Stig Larsson. Duality in refined Sobolev–Malliavin spaces and weak approximations of SPDE. Stoch. PDE: Anal. Comp., 4(1):113–149, 2016.

- [2] Adam Andersson and Stig Larsson. Weak convergence for a spatial approximation of the nonlinear stochastic heat equation. Math. Comp., 85(299):1335–1358, 2016.

- [3] Andrea Barth and Annika Lang. Milstein approximation for advection-diffusion equations driven by multiplicative noncontinuous martingale noises. Appl. Math. Opt., 66(3):387–413, 2012.

- [4] Andrea Barth and Annika Lang. Simulation of stochastic partial differential equations using finite element methods. Stochastics, 84(2-3):217–231, 2012.

- [5] Andrea Barth, Annika Lang, and Christoph Schwab. Multilevel Monte Carlo method for parabolic stochastic partial differential equations. BIT, 53(1):3–27, 2013.

- [6] Charles-Edouard Bréhier, Martin Hairer, and Andrew M Stuart. Weak error estimates for trajectories of SPDEs for spectral Galerkin discretization. arXiv:1602.04057 [math.PR], February 2016.

- [7] Daniel Conus, Arnulf Jentzen, and Ryan Kurniawan. Weak convergence rates of spectral Galerkin approximations for SPDEs with nonlinear diffusion coefficients. arXiv:1408.1108 [math.PR], August 2014.

- [8] Arnaud Debussche. Weak approximation of stochastic partial differential equations: the nonlinear case. Math. Comp., 80(273):89–117, 2011.

- [9] Arnaud Debussche and Jacques Printems. Weak order for the discretization of the stochastic heat equation. Math. Comp., 78(266):845–863, 2009.

- [10] Michael B. Giles. Improved multilevel Monte Carlo convergence using the Milstein scheme. In Alexander Keller, Stefan Heinrich, and Harald Niederreiter, editors, Monte Carlo and quasi-Monte Carlo methods 2006. Selected papers based on the presentations at the 7th international conference ‘Monte Carlo and quasi-Monte Carlo methods in scientific computing’, Ulm, Germany, August 14–18, 2006, pages 343–358. Springer, 2008.

- [11] Stefan Heinrich. Multilevel Monte Carlo methods. In Svetozar Margenov, Jerzy Wasniewski, and Plamen Y. Yalamov, editors, Large-Scale Scientific Computing, volume 2179 of Lecture Notes in Computer Science, pages 58–67. Springer, 2001.

- [12] Arnulf Jentzen and Ryan Kurniawan. Weak convergence rates for Euler-type approximations of semilinear stochastic evolution equations with nonlinear diffusion coefficients. arXiv:1501.03539 [math.PR], January 2015.

- [13] Arnulf Jentzen and Michael Röckner. A Milstein scheme for SPDEs. Foundations of Computational Mathematics, 15(2):313–362, 2015.

- [14] Peter E. Kloeden, Gabriel J. Lord, Andreas Neuenkirch, and Tony Shardlow. The exponential integrator scheme for stochastic partial differential equations: Pathwise error bounds. J. Comput. Appl. Math., 235(5):1245–1260, 2011.

- [15] Mihály Kovács, Stig Larsson, and Fredrik Lindgren. Strong convergence of the finite element method with truncated noise for semilinear parabolic stochastic equations with additive noise. Numerical Algorithms, 53(2-3):309–320, 2010.

- [16] Mihály Kovács, Felix Lindner, and René Schilling. Weak convergence of finite element approximations of linear stochastic evolution equations with additive Lévy noise. SIAM/ASA J. on Uncert. Quant., 3(1):1159–1199, 2015.

- [17] Raphael Kruse. Strong and Weak Approximation of Semilinear Stochastic Evolution Equations, volume 2093 of Lecture Notes in Mathematics. Springer, 2014.

- [18] Annika Lang. A note on the importance of weak convergence rates for SPDE approximations in multilevel Monte Carlo schemes. In Ronald Cools and Dirk Nuyens, editors, Monte Carlo and Quasi-Monte Carlo Methods, MCQMC, Leuven, Belgium, April 2014, volume 163 of Springer Proceedings in Mathematics & Statistics, pages 489–505, 2016.

- [19] Andreas Petersson. Stochastic partial differential equations with multiplicative noise: Numerical simulations of strong and weak approximation errors. Master’s thesis, University of Gothenburg, May 2015.