Ergodicity of an SPDE Associated with a Many-Server Queue

Abstract

We consider the so-called GI/GI/N queueing network in which a stream of jobs with independent and identically distributed service times arrive according to a renewal process to a common queue served by identical servers in a First-Come-First-Serve manner. We introduce a two-component infinite-dimensional Markov process that serves as a diffusion model for this network, in the regime where the number of servers goes to infinity and the load on the network scales as for some . Under suitable assumptions, we characterize this process as the unique solution to a pair of stochastic evolution equations comprised of a real-valued Itô equation and a stochastic partial differential equation on the positive half line, which are coupled together by a nonlinear boundary condition. We construct an asymptotic (equivalent) coupling to show that this Markov process has a unique invariant distribution. This invariant distribution is shown in a companion paper [1] to be the limit of the sequence of suitably scaled and centered stationary distributions of the GI/GI/N network, thus resolving (for a large class service distributions) an open problem raised by Halfin and Whitt in [19]. The methods introduced here are more generally applicable for the analysis of a broader class of networks.

and

t1The first author was supported by NSF grants CMMI-1234100 and DMS-1407504. t2The second author was supported by AFOSR grant FA9550-12-1-0399.

1 Introduction

1.1 Overview

Most stochastic networks are typically too complex to be amenable to exact analysis. Instead, a common approach is to develop approximations that can be rigorously justified via limit theorems in a suitable asymptotic regime. Diffusion models, which capture fluctuations of the state of the network around its mean behavior, and their invariant distributions have been well studied for networks of single server queues in heavy traffic (i.e., queues near instability). Most diffusion models for which rigorous limit theorems have been established thus far have been finite-dimensional processes (e.g., reflected Brownian motions) or (in the case of certain non-head-of-the-line policies) deterministic mappings of a finite-dimensional process (see, e.g., [11, 27, 28]). In contrast, functional central limit theorems for many-server networks with general service distributions lead naturally to diffusion models that are truly infinite-dimensional, and therefore require new techniques for their analysis. Whereas several limit theorems for many-server queues have been established (see Section 1.3 for a review), not much work has been devoted to the analysis of the associated diffusion limit.

The goal of this work is to introduce useful representations of diffusion models of many-server queues with general service distributions, and to develop techniques for the analysis of the associated processes and their invariant distributions. In particular, we seek to resolve an open question related to the GI/GI/N queue, which is a network of parallel servers to which a common stream of jobs with independent and identically distributed (i.i.d.) service requirements arrive according to a renewal process, wait in a common queue if all servers are busy, and are processed in a First-Come-First-Serve manner by servers when they become free. When the system is stable, an important performance measure is the steady state distribution of , the total number of jobs in the network, which includes those waiting in queue and those in service. A quantity of particular interest is the steady state probability that the queue is non-empty. An exact computation of this quantity is in general not feasible for large systems. However, when the service distribution is exponential and the traffic intensity (i.e., the ratio of the mean arrival rate to the mean service rate) of the system has the form for some , and the interarrival distribution satisfies some minor technical conditions, Halfin and Whitt [19, Theorem 2] showed that the sequence of centered and renormalized processes converges weakly on finite time intervals to a positive recurrent diffusion with a constant negative drift when and an Ornstein-Uhlenbeck type restoring drift when . Moreover, they also showed that, as the number of servers goes to infinity, the invariant distribution of converges to the (unique) invariant distribution of the diffusion [19, Proposition 1 and Corollary 2], which provides an explicit approximation for the steady state probability of an -server queue being strictly positive for large . Indeed, the asymptotic scaling for the traffic intensity mentioned above, which is commonly referred to as the Halfin-Whitt asymptotic regime, was shown in [19] to be the only scaling that ensures that, in the limit, the probability of a positive queue is non-trivial (i.e., lies strictly between zero and one).

However, statistical analysis has shown that service distributions are typically non-exponential [7], and the problem of obtaining an analogous result for general, non-exponential service distributions was posed as an open problem in [19, Section 4]. This problem has remained unsolved except for a few specific distributions [15, 21, 41], even though tightness of the sequence of scaled queue-length processes was recently established under general assumptions by Gamarnik and Goldberg [14, 16]. The missing element in converting the tightness result of [14] to a convergence result was the identification and unique characterization of a candidate limit distribution. In analogy with the exponential case, a natural conjecture would be that the limit distribution is equal to the unique stationary distribution (assuming one can be shown to exist) of the process obtained as the limit (on every finite interval) of . However, whereas for exponential service distributions both the process and its limit are Markov processes, this is no longer true for more general service distributions. Specifically, although convergence (over finite time intervals) of the sequence of scaled processes has been established for various classes of service distributions (see, e.g., [34, 30, 15, 35, 33, 24]), the obtained limit is not Markovian, with the exception of the work in [24], which is discussed further in Section 1.3. This makes characterization of the stationary distribution of challenging. It is easy to see that, except for special classes of distributions (e.g., phase-type distributions, as considered in [34]), any Markovian diffusion limit process will be infinite-dimensional. The key challenge is then to identify a suitable diffusion model, whose invariant distribution can be analyzed and shown to be the limit of the stationary distributions of the GI/GI/N queue.

1.2 Discussion of Results

The first contribution of this article is to introduce a two-component Markov process that serves as a diffusion model in the Halfin-Whitt asymptotic regime (see Definition 4.12). The first component is real-valued and is the limit of the sequence . The second component , which takes values in the Hilbert space of square integrable functions on that have a square integrable weak derivative, keeps track of just enough additional information so that is a Markov process. Under suitable conditions on the service distribution, we characterize the components and to be the unique solution to a coupled pair of stochastic equations driven by a Brownian motion and an independent space-time white noise (see Theorem 3.7). Specifically, satisfies an Itô equation with a constant diffusion coefficient and a -dependent drift, and is an -valued process driven by a space-time white noise that satisfies a (non-standard) stochastic partial differential equation (SPDE) on the domain . The two components are further linked by a nonlinear boundary condition: at each time , is a (deterministic) nonlinear function of . A precise formulation of these equations is given in Definition 3.6. The SPDE characterization of facilitates the use of tools from stochastic calculus to compute performance measures of interest and natural generalizations would potentially also be useful for studying diffusion control problems for many-server networks, in a manner analogous to Brownian control problems that have been studied in the context of single-server networks [20].

The second contribution of this article (see Theorem 3.8) is to establish uniqueness of the invariant distribution of the Markov process . Standard methods for establishing ergodicity of finite-dimensional Markov processes such as positive Harris recurrence are not well suited to this setting due to the infinite-dimensional nature of the state space. Other techniques such as the dissipativity method used for studying ergodicity of nonlinear SPDEs (see, e.g. [9, 31]) also appear not immediately applicable due to the non-standard form of the equations, in particular, the presence of the non-linear boundary condition. Instead, we adopt the asymptotic (equivalent) coupling approach developed in a series of papers by Hairer, Mattingly, Scheutzow and co-authors (see, e.g., [12, 17, 3, 18] and references therein) to show that has a unique invariant distribution. The asymptotic equivalent coupling that we construct has a different flavor from that used in previous works, and entails the analysis of a certain renewal equation. We believe that SPDEs with this kind of boundary condition are likely to arise in the study of scaling limits and control of other parallel server networks, and so our constructions could be useful in a broader context.

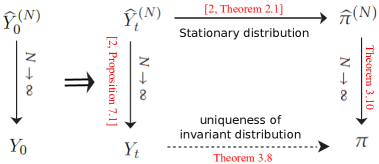

In a companion paper [1] we introduce an -valued process that, together with , serves as a state descriptor of the GI/GI/N queue (see Section 2.2). As depicted in Figure 1, we show in [1, Theorem 2.1] that each has a stationary distribution and, in [1, Proposition 5.1] that the sequence is tight, building on earlier results in [14]. Furthermore, under convergence assumptions on the initial conditions, it follows from [1, Proposition 7.1] that for every , the marginal converges weakly to the corresponding marginal of the diffusion model with the limiting initial condition. In particular, initializing the -server system such that has law , and considering a subsequence that converges to some limit , whose law denoted by , this implies that along that subsequence, converges to , where is the diffusion model with initial condition . Since has law by stationarity, the law of is for each . Theorems 3.7 and 3.8 then imply that is the unique invariant distribution of the diffusion model. When combined, these results show that it is also the limit of the sequence (see Theorem 3.10), thus resolving in the affirmative (for a large class of service distributions) the open question posed in [19] and reiterated in [14].

More generally, this work also serves to illustrate the usefulness of the technique of asymptotic (equivalent) coupling for the study of stability properties of many-server stochastic networks with general service distributions. Our framework would also allow one to use the general theory of Markov processes, although in an infinite-dimensional setting, to try to obtain a convenient characterization or numerical approximation of the limiting distribution. Such questions are relegated to future work.

1.3 Relevant Prior Work on Infinite-dimensional Representations of the GI/GI/N queue

A Markovian state descriptor for the GI/GI/N queue was proposed by Kaspi and Ramanan in [23, 24] in terms of a pair , where is a finite measure on ; see Section 2.1. A functional strong law of large numbers (or fluid) limit was established in [23] and the sequence of suitably renormalized fluctuations of the state around the fluid limit (in the subcritical, critical and supercritical regimes) was shown to converge in the Halfin-Whitt regime to a limit process in [24]. However, lies in a somewhat complicated space (the component is distribution-valued) and turns out not to be a Markov process on its own (i.e., the Markov property of the state is lost in the limit) unless one imposes very stringent assumptions on the service distribution, or one adds a third component to Markovianize the state. A key insight that led to our simpler representation is the observation that the first and third components (when the latter is chosen to be on a suitable space) on their own form a nice Markov process . It is worth pointing out that the choice of the state space of is somewhat subtle (see Remark 3.9 for an elaboration of this point).

For the simpler case of infinite-server queues, the process in our representation can be shown to be Markovian on its own, there is no nonlinear coupling with to deal with, and the dynamics are simpler to describe (via a linear SPDE). In this case, it is more straightforward to establish uniqueness and identify the form of the invariant distribution without resorting to any asymptotic coupling argument. Other works that consider infinite-server queues include [10] and [36]. Specifically, in [36] a different representation of the state in the space of tempered distributions is used, and a diffusion limit is characterized as a tempered-distribution-valued Ornstein Uhlenbeck process. While this choice of state space facilitates the analysis of the invariant distribution, it requires stronger conditions on the service distribution, such as infinite differentiability of the hazard rate function and boundedness of all its derivatives (see [36, Assumption 1.2]).

1.4 Outline of the Rest of the Paper

In Section 3, we introduce the assumptions on the service distribution and the diffusion model SPDE, and state our main results, Theorems 3.7 and 3.8. In Section 4, we provide an explicit construction of the diffusion model and show that it is the unique solution to the diffusion model SPDE, and is also a time-homogeneous Feller Markov process. The proof of Theorem 3.7 is given at the end of Section 4.5. In Section 5, which is devoted to the proof of Theorem 3.8, we construct a suitable asymptotic equivalent coupling to show that the diffusion model has at most one invariant distribution. Proofs of a few additional results are relegated to Appendices A and B.

1.5 Notation

The following notation will be used throughout the paper. , and are the sets of integers, nonnegative integers and positive integers, respectively. Also, is the set of real numbers and the subset of nonnegative real numbers. For , and denote the minimum and maximum of and , respectively. Also, and . For a set , is the indicator function of the set B (i.e., if and otherwise). Moreover, with a slight abuse of notation, denotes the constant function equal to on any domain .

For every and subset , , and are respectively, the spaces of continuous functions on , bounded continuous functions on and continuous functions with compact support on . For and , denotes the supremum of over , and denotes the supremum of over . A function for which for every is said to be locally bounded. Also, denotes the subspace of functions with , denotes the set of functions for which the derivative, denoted by , exists and is continuous on (with denoting the right derivative at ), and represents the subset of functions in that are bounded and have a uniformly bounded derivative. Moreover, for every Polish space , denotes the set of continuous -valued functions on . Recall that when , a function is uniformly continuous on an interval if for every , there exists a such that for every with . A function is called locally uniformly continuous if, for every , it is uniformly continuous on the interval . Note that for a locally uniformly continuous function , the limit exists and can be continuously extended to by setting

Let and denote, respectively, the spaces of integrable, square-integrable and essentially bounded measurable functions on , equipped with their corresponding standard norms. Also, let denote the space of locally integrable functions on For any and a function that is bounded on finite intervals, denotes the (one-sided) convolution of two functions, defined as , Note that is locally integrable and locally bounded. Let denote the space of square integrable functions on whose weak derivative exists and is also square integrable, equipped with the norm

The space is a separable Banach space, and hence, a Polish space (see e.g. [6, Proposition 8.1 on p. 203]). Also, for a function , denotes the weak derivative of for every Finally, recall that every function is almost everywhere equal to an absolutely continuous function whose derivative coincides with the weak derivative of , almost everywhere [13, Problem 5 on p. 290].

Finally, for two measures on a measurable space , is said to be absolutely continuous with respect to , denoted , if for every subset , implies When and , and are said to be equivalent, and this is denoted by

2 State representations of the -server queue

To motivate the form of the SPDE description of the diffusion model, we recall dynamical equations for the -server model, first for the measure-valued state descriptor of the GI/GI/N queue introduced in [23, 24] in Section 2.1, and then for the reduced state representation in Section 2.2.

2.1 A Measure-Valued Representation for the GI/GI/N Queue

Recall that the total number of jobs in system at time is denoted by . Also, let denote the age of job , which is the amount of service that the job has received by time . In [23], the GI/GI/N queue was described by the state , where is the finite measure

which is the sum, over jobs in service at time , of unit Dirac masses at the ages of the jobs. In particular, is the number of jobs in service (recall that is the integral of the constant function with respect to ), and the non-idling property implies

| (2.1) |

Let and be the cumulative number of jobs that, respectively, arrived into and departed from the system during . Then, the following equation reflects a simple mass balance for the number of jobs in system:

| (2.2) |

Moreover, defining to be the number of jobs that have entered service during , a mass balance equation for the number of jobs in service implies

| (2.3) |

Now, consider the Halfin-Whitt regime where the service distribution has unit mean and the arrival rate satisfies as . In [23], a fluid (or functional law of large numbers) limit was obtained and shown to have as an invariant state. The dynamics of the “diffusion-scaled” processes

and for were studied in detail in [24]. It was shown in [24, Corollary 5.5] that

| (2.4) |

where is the hazard rate function of the service time distribution, and is a càdlàg orthogonal martingale measure with covariance functional

| (2.5) |

for any Borel subset of , and for any bounded continuous function on , represents the stochastic integral of with respect to (see [24, Section 4.1] and [40, Chapters 1 and 2] for more details on martingale measures). Therefore, (2.2) implies that

| (2.6) |

It was also shown, in [24, Proposition 6.2], that for satisfies

| (2.7) |

with

| (2.8) |

and and further coupled through the following diffusion-scaled version of the non-idling condition in (2.1):

| (2.9) |

Furthermore, it was shown in [24, Theorem 3] that converges to a limit process that is characterized by a coupled pair of stochastic evolution equations. However, this process is not very amenable to analysis: it takes values in the somewhat complicated state space (where is a certain distribution space), and is not Markov on its own (i.e., the Markov property of the state representation is not preserved in the limit), although it could be Markovianized by the addition of a third component, thereby making the state space even more complicated.

2.2 A Reduced Representation

We now consider a more tractable representation for the GI/GI/N model, used in [1], in which we append to , the number of jobs in system, a function-valued random element defined as follows: for every ,

| (2.10) |

where the summation is over the indices of jobs in service at time . Roughly speaking, is the conditional expected number of jobs receiving service at time that will still be in the network at time , given the network state at time . The key advantage of this representation is that the process lies in a simpler Hilbert space, but at the same time contains enough information so as to lead to a diffusion model that is Markov.

Defining a one-parameter family of functions by

| (2.11) |

the random element can be written in terms of as

| (2.12) |

Note , and hence, is the number of jobs in service at time . Further, define and set . Then, substituting in the equation (2.7), noting that and , and invoking the relation

| (2.13) |

we observe that satisfies

| (2.14) |

where, substituting and in (2.8) and (2.9), we have

| (2.15) |

and

| (2.16) |

The diffusion model SPDE introduced in Section 3.2 is a limit analog of the equations in the last three displays.

3 Assumptions and Main Results

3.1 Assumptions

Throughout, the function represents the cumulative distribution function (cdf) of the service distribution in the GI/GI/N model, and denotes the complementary cdf.

Assumption I.

The function satisfies the following properties:

-

a.

is continuously differentiable with derivative and .

-

b.

The function defined by

(3.1) is uniformly bounded, that is,

-

c.

The derivative is continuously differentiable with derivative , and the function

is uniformly bounded, that is,

Remark 3.1.

Assumption I.a implies that the service distribution has a continuous probability density function (p.d.f.) and finite mean that is set (by changing units if necessary) to be 1. Note that represents the hazard rate function of the service time distribution, and the boundedness of implies that the support of the service time distribution is all of .

Assumption II.

For some , there exists a finite positive constant such that for all sufficiently large . In other words, the service time distribution has a finite moment.

Remark 3.2.

It is easily verified (see Appendix F) that Assumptions I and II are satisfied by a large class of distributions of interest, including phase-type distributions, Gamma distributions with shape parameter , Lomax distributions (i.e., generalized Pareto distributions with location parameter ) with shape parameter , and the log-normal distribution, which has been empirically observed to be a good fit for service distributions arising in applications [7, Section 4.3].

3.2 An SPDE

In this section, we introduce an SPDE that is shown in Theorem 3.7 to characterize the diffusion model .

3.2.1 Driving Processes

The SPDE is driven by a Brownian motion and an independent space-time white noise on based on the measure , defined on a common probability space , i.e., is a continuous martingale measure with covariance given by

| (3.2) |

For definitions and properties of martingale measures and space-time white noise, we refer the reader to [40, Chapters 1 and 2]. For every bounded measurable function on ,

the stochastic integral of on with respect to the martingale measure is denoted by

| (3.3) |

Note that is a continuous Gaussian process with independent increments. Also, let and let the filtration denote the augmentation (see [22, Definition 7.2 of Chapter 2]) of with respect to . Recall that the stochastic integral is an -martingale with (predictable) quadratic variation

| (3.4) |

The processes and arise as limits of suitably scaled fluctuations of the arrival and departure processes, respectively, in the GI/GI/N model. Specifically, the fluctuations of the scaled renewal arrival processes converge weakly to the process , , where is the constant in the Halfin-Whitt scaling, and is a constant that depends on the mean and variance of the interarrival times (see [24, Remark 5.1]). Moreover, it follows from [23, Lemma 5.9] and [24, Corollary 8.3] that when the fluid limit is invariant, with (referred to as the critical case in [24]), for suitable test functions , the sequence of scaled local martingales converges to ; indeed, the covariance functional (3.2) is the limit of the covariance functional of , obtained by replacing by its limit in the expression (2.5). Furthermore, the independence of and follows from the asymptotic independence result of [24, Proposition 8.4].

3.2.2 The Diffusion Model SPDE

To introduce the state space of the diffusion model, we first list relevant properties of the space .

Lemma 3.3.

The space satisfies the following properties:

-

a.

For every function , there exists a (unique) function such that a.e. on

-

b.

The embedding that takes to is continuous.

-

c.

For every , the mapping is a continuous mapping from into itself. Also, for every the translation mapping from to is continuous. Moreover,

(3.5)

Proof.

Using to denote the embedding from to as defined above, we define the space

which will serve as the state space of the diffusion model.

Corollary 3.4.

is a closed subspace of and hence, is a Polish space.

Proof.

Remark 3.5.

Lemma 3.3 asserts that for every function , there exists a unique continuous function on whose restriction to belongs to the equivalence class of . This continuous representative is used to define the evaluation of on ; in particular, we use to denote the evaluation of at . For ease of notation (and as is customary in the literature, see, e.g., [6, Remark 5, Section 8]), we denote the continuous representative of again by .

Using the notation of Remark 3.5, we can rewrite the state space as

| (3.6) |

Let be equipped with its Borel -algebra . We now introduce the diffusion model SPDE. Note that the diffusion model equations (3.8), (3.9) and (3.10) for in Definition 3.6 below are simply limit analogs of the equations (2.14)-(2.15), (2.9) and (2.6), respectively, of the GI/GI/N model.

Definition 3.6 (Diffusion Model SPDE).

Let be a -valued random element defined on , independent of and . A continuous -valued stochastic process is said to be a solution to the diffusion model SPDE with initial condition if

-

1.

is -adapted, where

-

2.

, -almost surely;

-

3.

-almost surely, is locally integrable and for every , there exists (a unique) such that the function

(3.7) is equal to a.e. on . Again, with a slight abuse of notation, for (and in particular, we denote by the evaluation of the continuous representative at .

-

4.

-almost surely, satisfies

(3.8) subject to the boundary condition

(3.9) and satisfies the stochastic equation

(3.10)

Given , as above, we say the diffusion model SPDE has a unique solution if for every initial condition and every two solutions and with initial condition ,

3.3 Main Results

We first state our results and then describe how they are useful for showing convergence of stationary distributions of the centered and scaled number of jobs in system in the Halfin-Whitt regime, thus resolving the open problem posed in [19]. To state our first result, recall that a Markov family with corresponding transition semigroup is called Feller if for every continuous and bounded function on , is a continuous function.

Theorem 3.7.

The proof of Theorem 3.7 is given at the end of Section 4.5. Let be the transition semigroup associated with the Markov family of Theorem 3.7, and recall that a probability measure on is said to be an invariant or stationary distribution for If

| (3.11) |

Theorem 3.8.

Remark 3.9.

A key contribution of our work is the identification of a suitable augmentation of the state , with a function-valued process such as , that facilitates the analysis of both the process and its invariant distribution. It is worth emphasizing that the most convenient choice of function space for is not completely obvious. For example, could also be viewed as a continuous process taking values in the spaces , , , or , the Sobolev space of integrable functions with integrable weak derivatives on . However, in the case of or , does not seem to admit a representation as a nice Itô process, and it is not clear if is a Feller process. On the other hand, although the choice of leads to a Feller process, it seems difficult to show uniqueness of the invariant distribution in this space. Lastly, when the state space of is chosen to be , it is possible to show that is both a continuous homogeneous Feller process and has a unique invariant distribution (albeit the latter only under more restrictive assumptions on ). However, in this case, it does not seem easy to establish convergence of the centered scaled marginals to , which is a key step in [1] that is used to identify the limit of the sequence of scaled -server stationary distributions. The choice of the space for allows us to establish all three properties at once; in particular, the Hilbert structure of is exploited in [1, Lemma 7.3 and Proposition 7.1] to establish finite-dimensional convergence of to (when the initial conditions converge in a suitable sense).

The assumption is not necessary for the results of this paper; however, we impose it since it is needed to prove existence of the stationary distribution . As explained in Section 1.2, the motivation for our results above is that, when combined with those of [1], they yield the following result, which in particular establishes existence of a stationary distribution for .

Theorem 3.10.

([1, Theorem 2.2]) Suppose Assumptions I-II hold. In addition, suppose has a finite moment for some , and has a bounded weak derivative which satisfies as . Then the transition semigroup associated with the diffusion model SPDE has a unique stationary distribution . Moreover, converges weakly to as .

Remark 3.11.

It is possible to establish existence of the invariant distribution of under a finite moment assumption via a different argument, namely by an application of the Krylov-Bogoliubov theorem together with certain bounds on that are obtained from uniform bounds on the fluctuations of the number of jobs in the server queue obtained in [1, Corollary 5.1].

4 An Explicit Solution to the SPDE

The goal of this section is to prove Theorem 3.7. We start by establishing existence and uniqueness of a solution to the diffusion model SPDE. First, in Section 4.1, we state a number of basic results that are required to define a candidate solution, which we call the diffusion model. In Section 4.2, we provide an explicit construction of this -valued stochastic process. In Section 4.3, we verify that is indeed a solution to the diffusion model SPDE and in Section 4.4, prove that it is the unique solution. Finally, in Section 4.5 we show that the diffusion model is a time-homogeneous Feller Markov process.

4.1 Preliminaries

In this section we establish regularity properties of various objects that arise in the analysis of the SPDE.

4.1.1 Properties of the Martingale Measure

Recall the definition given in Section 3.2 of the continuous martingale measure and stochastic integral . We now define two families of operators that allow us to represent some relevant quantities in a more succinct manner. Consider the family of operators that map functions on to functions on , and are defined as follows: for every ,

| (4.1) |

In particular, for any bounded function on , , and hence, maps the space of continuous bounded functions on to the space of continuous bounded functions on . Next, consider the family of operators which are defined as follows: for every , let

| (4.2) |

for any function on . The operator clearly maps the space into itself.

Observe that the family of functions defined in (2.11) admits the representation

| (4.3) |

Also, and the family of operators satisfies the semigroup property:

Furthermore, for every function defined on and ,

| (4.4) |

Next, we define a family of stochastic convolution integrals: for and ,

| (4.5) |

Recall that a stochastic process or random field with index set is called a modification of another stochastic process or random field defined on a common probability space, if for every , almost surely. In contrast, and are said to be indistinguishable if Lemma 4.1 and Proposition 4.3 below show that we can choose suitably regular modifications of certain stochastic integrals.

Lemma 4.1.

Suppose Assumption I holds. Then, , and have modifications that are jointly continuous on .

Proof.

Fix , and . Recalling from (3.2) the quadratic variation process of integrals with respect to , and using the Burkholder-Davis-Gundy inequality for martingales (see e.g [40, Theorem 7.11]), there exists a constant such that for every bounded measurable function on ,

| (4.6) |

Let be such that , and set . Then, by (4.2) and the bound (4.6), is bounded by

where . Then, by Assumption I.b and the mean value theorem, there exists such that

Note that the inequality is used in the second line, which holds because . Therefore, by the Kolmogorov-Centsov theorem (see, e.g., [37, Theorem I.25.2], with , and ), the random field has a continuous modification.

In a similar fashion, by definition (4.1) and another application of the bound (4.6), there exists such that

for some . Again, by the Kolmogorov-Čentsov theorem, the process has a continuous modification. Similarly, using Assumption I.c and (4.1), we obtain

for some . Thus, has a continuous modification. ∎

Remark 4.2.

By , and , we always denote the jointly continuous modification. Note that, by substituting in Lemma 4.1, this also implies the continuity of the stochastic processes and .

Proposition 4.3.

To prove Proposition 4.3 we need the following intermediate result on properties of the random element for fixed

Lemma 4.4.

Proof.

We start by proving property a, which is similar in spirit to, but not a direct consequence of, Lemma E.1 of [24]. For fixed , by Assumption I.b, the function

is measurable in , bounded and satisfies

Since is an orthogonal, and therefore a worthy, martingale measure, by the stochastic Fubini theorem for martingale measures (see e.g. [40, Theorem 2.6]) we have

Since , equation (4.7) follows from the last display.

Now we turn to the proof of property b. For every , (3.4), (4.1) and Assumption I.b imply that

Similarly, we have

Therefore, Fubini’s theorem and the last two inequalities together show that

which is finite by Assumption II (see Remark 3.2). Therefore, the norms of both and are finite in expectation, and hence finite almost surely. ∎

Corollary 4.5.

Proof.

Corollary 4.5 shows that is an -valued stochastic process. Next, we show that this process has a continuous modification.

Proof.

Choose and , and define

| (4.8) |

Then for every ,

Since and are deterministic functions and has independent increments, this shows that is the sum of two independent Gaussian processes. Therefore, is a Gaussian process with covariance function where for ,

Using the fact that for and ,

by the mean value theorem for , (3.4), Assumption I.b, and the monotonicity of , we have for some ,

and an analogous calculation shows that

Setting , this implies that for every ,

| (4.9) |

Recall that given a pair of jointly Gaussian random variables with covariance matrix , . Applying this identity with and , and using (4.9) and the Cauchy-Schwarz inequality, we obtain

| (4.10) |

Then, by Tonelli’s theorem,

The bound (4.1.1) then implies that

for which is finite by Assumption II (see Remark 3.2). Substituting the definition (4.8) of into the last inequality, it follows that

| (4.11) |

Now, note that by (4.8) and Corollary 4.5, almost surely, has weak derivative

Using estimates analogous to those used above, one can show that

| (4.12) |

where now

which is finite by Assumptions I and II. Combining (4.11) and (4.12), for every , we have

for a finite that depends only on . The existence of an -continuous modification of then follows from a version of Kolmogorov’s continuity criterion for stochastic processes taking values in general Polish spaces (see, e.g., Lemma 2.1 in [39]). ∎

Remark 4.7.

By the continuous embedding result of Lemma 3.3.b, given a real-valued function on such that is continuous from to , the mapping has a representative that is a jointly continuously function on . Therefore, the continuous modification of in Proposition 4.3 is indistinguishable from the jointly continuous modification of in Remark 4.2.

Next, we establish a simple relation used in the proof of Theorem 3.7.

Lemma 4.8.

Suppose Assumption I holds. Then, almost surely, for all ,

| (4.13) |

Proof.

Since, from (4.1) and (4.2) it is clear that , the stochastic Fubini theorem for martingale measures ([40, Theorem 2.6]) shows that for every , almost surely,

| (4.14) |

However, Lemma 4.1 and Remark 4.2 show that both sides of (4.14) are jointly continuous in . This implies the stronger statement that almost surely, the equality in (4.14) is satisfied for every . ∎

Setting in (4.13), we see that, almost surely,

| (4.15) |

4.1.2 An Auxiliary Mapping

Next, we introduce an auxiliary mapping that appears in the explicit construction of the diffusion model (see Definition 4.12). For every , define

| (4.16) |

for . The following lemma establishes useful properties of the mapping .

Lemma 4.9.

Proof.

The proof is postponed to Appendix B. ∎

4.2 The Diffusion Model

Here, we explicitly construct our proposed diffusion model . In the next two subsections we show that is indeed the unique solution to the diffusion model SPDE. The -component of this process is defined in terms of the (deterministic) centered many-server (CMS) mapping introduced in [24], and recalled below as Definition 4.11.

The first assertion of Lemma 4.10 below, which characterizes the CMS mapping, and shows it is continuous, can be deduced from a more general result established in [24] (see Proposition 7.3 and the proof of Lemma 7.4 therein). Since the proof of this characterization is simpler in our context (because we only consider the so-called critical regime) for completeness, we include a direct proof below. Recall that denotes the set of functions with .

Lemma 4.10.

Given with , there exists a unique pair that satisfies the following equations: for every ,

| (4.18) | ||||

| (4.19) |

Furthermore, the mapping that takes to is continuous and non-anticipative, that is, for every and , if and are equal on , then coincides with on .

Proof.

Fix with and set

| (4.20) |

Then, substituting from (4.19) into (4.18), it is straightforward to see that satisfy (4.18) and (4.19) if and only if satisfies the Volterra equation

| (4.21) |

and satisfies (4.19). However, since is Lipschitz and the assumptions on imply that is continuous and , there exists a unique solution to (4.21) (Theorem 3.2.1 of [8] shows that a unique solution exists on a finite interval, while Theorem 3.3.6 of [8] ensures that the solution can be extended to the whole interval ). Defining as in (4.19), with replaced by , it follows that is the unique solution to the equations (4.18)-(4.19) associated with . Let denote the map that takes to this unique solution.

The continuity of follows from Proposition 7.3 in [24]. To prove the non-anticipative property, for define by (4.20) with and replaced by and . We need to show that for every , if and agree on , we have . Subtracting equation (4.21) with and replaced by and , respectively, and defining , we have

Using the fact that the map is Lipschitz with constant , we have

Since , Gronwall’s inequality implies for . Then, because satisfies (4.19) with and replaced by and , respectively, we also have for . ∎

Definition 4.11 (Centered Many-Server Mapping).

Recall that is a Brownian motion and for fixed define

| (4.22) |

Definition 4.12 (Diffusion Model).

Deterministic initial conditions will be denoted by lower case: Also, when the initial condition is clear from the context, we will often not mention it explicitly, and also omit the superscript and just use to denote the diffusion model.

Remark 4.13.

Note that and have continuous sample paths and . Also, for every -valued random element , by Lemma 3.3.a and Remark 3.5, has a representative (also denoted by ) which is continuous on and satisfies by the definition of . Therefore, almost surely, lies in the domain of the CMS mapping . Hence, in (4.23) is well defined and (by Lemma 4.10) satisfies a.s.,

| (4.25) | ||||

| (4.26) |

for . Also, almost surely for every , implies lies in (see Lemma 3.3.c), the continuity of and Lemma 4.9.a imply , and Proposition 4.3 implies lies in . Thus, in (4.24) also lies in and furthermore, by Lemma 3.3.a, has a continuous modification, so in (4.24) is well defined for .

4.3 Existence of a Solution

We now show that the diffusion model defined in Section 4.2 is indeed a solution to the diffusion model SPDE. Throughout this section, we fix and let be the diffusion model with initial condition , as specified in Definition 4.12.

Proposition 4.14.

Suppose Assumptions I-II hold. Then the diffusion model with initial condition satisfies the following properties:

-

a.

Almost surely, the sample paths of are -valued and continuous, and for every the weak derivative of satisfies for a.e. ,

(4.27) -

b.

Almost surely, , for all

-

c.

is an almost surely continuous -valued process.

Proof.

For part a, we look at each term in the definition of in (4.24) separately. Since , the translation mapping is continuous in by Lemma 3.3.c and for each , has weak derivative . For the second term, by Proposition 4.3, is a continuous -valued process and almost surely, for every , the function has weak derivative . Finally for the third term, since the range of the CMS map lies in (see Definition 4.11 and Lemma 4.10), almost surely, the process defined in (4.23) is continuous. Therefore, by Lemma 4.9.c, is a continuous -valued process. Also, by (4.17), for every , has weak derivative . This completes the proof of part a.

Lemma 4.15.

Remark 4.16.

Recall again that for (and, in particular, ), , and in the above identity denote the evaluation of their corresponding continuous representative at .

Proof of Lemma 4.15.

By Proposition 4.14.a, almost surely for every , the weak derivative of exists and is given by (4.27). We prove the claims separately for each term on the right-hand side of (4.27). First, since , the mapping is clearly locally integrable on and for every , and almost every ,

| (4.29) |

Moreover, for every , since , also lies in , and therefore by Lemma 3.3.a, there exists a continuous function on , that is equal to almost everywhere on .

Next, Lemma 4.1 implies that almost surely, is jointly continuous and hence, locally integrable on . Also, for every , by (4.13) of Lemma 4.8,

| (4.30) |

By Lemma 4.1, is continuous on .

Finally, it follows from the continuity of and (see Assumption I) that the mapping is jointly continuous and hence, locally integrable on . Also, for every , using Fubini’s theorem,

| (4.31) |

Again, by the continuity of and , the mapping is continuous on . Equation (4.15) then follows from equations (4.27)-(4.3). ∎

Lemma 4.17.

Proof.

Comparing (4.32) and (3.8), and recalling that , it is clear that these two equations are equivalent if and only if for every , the following identity holds:

| (4.33) |

On the other hand, by (3.9) and (3.10) and the definition of given above, for , we have

Equation (3.9) (for ) also implies that . When substituted into the last display, (4.33) follows. ∎

Proposition 4.18.

Proof.

By Proposition 4.14.c, is a continuous -valued process. We show that it satisfies conditions 1-4 of Definition 3.6. Condition 2 holds because by definition, and condition 3 follows from Lemma 4.15. Next, we verify condition 1 of Definition 3.6 by showing that is -adapted. Fix , and note that the stopped processes and agree with and , respectively, on . Hence, by definition (4.23) of and the non-anticipative property of proved in Lemma 4.10, we have

Clearly, and are -measurable, while and are -measurable. Therefore, by the continuity, and hence, measurability of the mapping proved in Lemma 4.10, and are -measurable. Moreover, from the definition of the mapping , for every and , the value of does not depend on the values of outside the interval , and hence, On the other hand, is continuous by Lemma 4.9.c, and hence is also -measurable. Also, is -measurable and is -measurable by definition. Therefore, defined in (4.24) is -measurable. Consequently, is -adapted, and condition 1 follows.

We now turn to the proof of condition 4. By Lemma 4.17 it suffices to show that and satisfy equations (4.32), (3.9) and (3.10). First, substituting from (4.15), and using the definition (4.16) of , the right-hand side of (4.32) is equal to

By (4.24), this is equal to , which proves (4.32). Moreover, Proposition 4.14.b shows that the relation in (3.9) holds. Combining this relation with the expression for from (4.26), we have almost surely, for every ,

Together with the expression for in (4.24) and for in (4.16), both with , this implies

| (4.34) |

whereas substituting in (4.15), we have almost surely, for every ,

| (4.35) |

where we have used the identities and . Equation (3.10) then follows from (4.35), (4.34) and the relation . This completes the proof. ∎

4.4 Uniqueness

Here, we show that the diffusion model SPDE has a unique solution. We first establish uniqueness of the weak solution to a transport equation within a certain class of functions.

Lemma 4.19.

Suppose Assumption I holds, and a function with is given. Let be a function that satisfies the following two properties:

-

1.

The mapping lies in . For each , let denote the weak derivative of .

-

2.

The function is locally integrable.

Then satisfies the equation

| (4.36) |

for every if and only if

| (4.37) |

with as defined in (4.16).

Proof.

This result would be standard if and were continuously differentiable functions. In that case, (4.36) would reduce to the classical inhomogeneous transport equation with initial condition , whose unique solution is [13, Section 2.1.2]:

While there are several related results, there appears to be no readily quotable result for the class of and mentioned above. Thus, for completeness, we include a proof in Appendix D. ∎

Proposition 4.20.

Proof.

For , let be a solution to the diffusion model SPDE with initial condition , and define . We need to show that . Denote for , and note that By Lemma 4.17, for , satisfies the equation (4.32) with replaced by , and hence satisfies the following nonhomogeneous transport equation:

with . By Definition 3.6, both and hence satisfy properties 1 and 2 of Lemma 4.19. Therefore, by (4.37) of Lemma 4.19, with replaced by , we have

| (4.38) |

Since is continuous almost surely, an application of Lemma 4.9.a shows that for every , is continuously differentiable on , with continuous derivative

In particular, the function is well defined on and satisfies

| (4.39) |

Also, recalling the constants and from Assumptions I.b and I.c, and the fact that by Assumption I.a and Remark 3.1, we see that

| (4.40) |

On the other hand, for , satisfies (3.10) with replaced by . Therefore,

| (4.41) |

In turn, this implies

| (4.42) |

which, when combined with (4.39) and the bounds in Assumption I, shows that for every and ,

Since , by Gronwall’s lemma this implies for all . When combined with (4.42), this implies that for all , which in turn implies due to (4.38). Thus, we have shown that for all , which proves the desired uniqueness. ∎

4.5 Markov Property

Finally, we show that the family of laws associated with the diffusion model of Section 4.2 is a time-homogeneous Feller Markov family. For , we define the operator as follows: for every function on , the shifted function is defined by

| (4.43) |

Also, for every , we define the shifted convolution integral as

| (4.44) |

Then, the identity (4.4) shows that

| (4.45) |

Lemma 4.21.

Proof.

| (4.48) |

Also, by definition (4.43) of and (4.16) of , we have

| (4.49) | ||||

| (4.50) |

Substituting from (4.24) (with and replaced by and , respectively) and using equations (4.45) and (4.50), the right-hand side of (4.46) is equal to

To prove (4.47), subtract equation (4.26) with from the same equation with replaced by , and use (4.22), to get

| (4.51) | |||||

Additionally, by Proposition 4.14.b with replaced by , Substituting from (4.46), using definition (4.16) of and the identity , we obtain

| (4.52) |

Equation (4.47) then follows from (4.51), (4.52) and Definition 4.11 of (also see Lemma 4.10). ∎

Lemma 4.22.

Proof.

Fix . By definition (4.22) of and (4.43) of , we have

Since has independent stationary increments and is independent of , is independent of for all , and is itself a Brownian motion. Hence, the claim for follows.

Next, define the martingale measure as follows: for , . Since is a white noise independent of , is again a white noise with the same distribution as , and independent of Also, for any continuous , using (4.44) we have

Substituting and , we conclude that the processes and are independent of , and have the same distribution as and , respectively. ∎

Proposition 4.23.

Proof.

The Feller property can be deduced from the proof of Theorem 5(2) in Section 9.5 of [24], but since in our case the Markov process is homogeneous, the proof is simpler and so we include it here. Let be the diffusion model with initial condition . Recall from Proposition 4.3 that for any , and both lie in almost surely, and hence, so does , using equation (4.45). First, we claim that for every , there exists a continuous mapping such that for ,

| (4.53) |

Recall that is the space of continuous functions with , and for notational convenience, set . To see why the claim is true, first recall that the embedding from to and the evaluation map from to are continuous (see Lemma 3.3.b for the former). Then, by the representation of in (4.47) and the continuity of the CMS mapping from Lemma 4.10, it follows that there exists a continuous mapping such that for every ,

Moreover, it follows from the representation of in (4.46), the continuity of established in Lemma 4.9.b, and the continuity of the shift mapping on , that there exists a continuous function such that for every ,

The claim follows from the last two displays.

Next, we prove the Markov property of the family . For every , , and hence by condition 1. of Definition 3.6 and Proposition 4.18, is -measurable. Also, , and are independent of by Lemma 4.22. Hence, for every bounded and measurable functional , using the claim (4.5) we have

Moreover, using the simple observation that for any two independent random variables and , and any bounded measurable function , one has where (this is immediate to see for separable functions of the form , and can be extended to general bounded measurable functions using the linearity of conditional expectation and the monotone convergence theorem), and applying Lemma 4.22, for every we have

| (4.54) |

The last two displays show that the family is a time-homogeneous Markov family.

Finally, we prove the Feller property. Recall that denotes the transition semigroup corresponding to the Markov family , and note that for every and bounded continuous function , by another use of (4.54),

By the continuity of the mapping and (4.54) and an application of the bounded convergence theorem, the mapping is continuous, and hence the Markov family is Feller. ∎

5 Uniqueness of the Invariant Distribution

This section is devoted to the proof of Theorem 3.8. As mentioned in the introduction, to prove uniqueness of the invariant distribution, we will adopt the so-called asymptotic (equivalent) coupling method, which is particularly well suited to infinite-dimensional Markov processes. In Section 5.1, we first describe this method in the generality required for our problem, following the exposition in [18]. At the end of Section 5.1, we discuss the main steps involved in applying this framework to our problem, which are carried out in Sections 5.2–5.6.

5.1 Asymptotic Coupling: The General Framework

Let be a Polish space with a compatible metric , equipped with the Borel -algebra . As usual, let denote the space of -valued functions on . We endow with the Kolmogorov -algebra , which is the -algebra generated by all cylinder sets. Let and denote the spaces of probability measures on and . For every , recall that a coupling of and is a probability measure whose first and second marginals, respectively, are and , that is, for , where, is the th coordinate projection map, and is the push-forward of the measure under . Define to be the set of couplings of and . One can relax the definition of a coupling to define the space of absolutely continuous couplings as follows:

| (5.1) |

If in satisfies , , will be referred to as an equivalent coupling of and . In contrast to a coupling, the corresponding marginals of an absolutely continuous (or equivalent) coupling need only be absolutely continuous with respect to (resp., equivalent to), and not necessarily equal to, and , respectively.

Let be the transition semigroup of a Markov kernel on . For every , let denote the distribution of the Markov process with initial value and transition semigroup on the path space ( is denoted in [18] by ). Recall that a probability measure on is called an invariant distribution for the semigroup if (3.11) holds for every . Finally, let be the set of pairs of paths that meet at infinity:

| (5.2) |

and note that

Recall that a probability measure on is called an invariant distribution for the semigroup if (3.11) holds for every .

Proposition 5.1.

Assume there exists a measurable set and a mapping with the following properties:

-

(I)

for any invariant probability measure of .

-

(II)

For every measurable set , is measurable.

-

(III)

For every , .

Then has at most one invariant probability measure.

Proof.

Remark 5.2.

As observed in Remark 1.2 of [18], for the purpose of Proposition 5.1, in the definition (5.1) of , one can without loss of generality replace absolute continuity by (the apparently stronger condition of) equivalence. This is because if there is an absolutely continuous coupling that satisfies conditions (II) and (III) of Proposition 5.1, then the measure is an equivalent coupling that also satisfies the same conditions. Thus, we refer to the approach to establishing uniqueness of the invariant distribution by invoking Proposition 5.1 as the asymptotic equivalent coupling approach.

In Sections 5.2-5.6, we apply the asymptotic equivalent coupling framework of Proposition 5.1, with , in order to establish uniqueness of the invariant distribution of the transition semigroup associated to the Markov family of the diffusion model defined in Section 4.2. Let be the measurable subset of defined as

| (5.3) |

First, in Section 5.2, for each pair , we construct a pair of stochastic processes on a common probability space and define the mapping

| (5.4) |

where denotes the joint distribution of . The required measurability properties are proved in Section 5.3. Next, in Section 5.4, we show that , and in Section 5.5 we show that the law of is , and that the law of is equivalent to , thus establishing that defines an asymptotic equivalent coupling. Finally, we combine these results in Section 5.6 to complete the proof of Theorem 3.8.

Remark 5.3.

It is worthwhile to clarify why, in Proposition 5.1, we formulate a continuous-time version of the asymptotic coupling theorem, rather than deduce the result by simply applying the original discrete-time version established in [18, Corollary 2.2] to the discrete skeleton of the continuous-time process (i.e., the Markov chain obtained by sampling at integer times). To show uniqueness of the invariant measure of the continuous-time Markov process, is clearly suffices to show uniqueness of the invariant measure of its discrete skeleton (that is, the Markov chain obtained by sampling the continuous process at integer times). In turn, by Corollary 2.2 of [18], for uniqueness of the invariant measure of the discrete skeleton, it suffices to verify the three conditions of that corollary, which are the natural discrete analogs of properties (I), (II) and (III) of Proposition 5.1. Now, the continuous version of properties (II) and (III) immediately imply the discrete version because any asymptotic equivalent coupling of the continuous-time process on some set induces a corresponding asymptotic equivalent coupling of the discrete skeleton. Thus, if then the discrete-time version can be directly invoked because in this case the first condition of Corollary 2.2 of [18], which states that for every invariant measure of the discrete skeleton, is trivially satisfied. However, when is a strict subset of then the property that for all invariant measures of the continuous-time process need not imply that for all invariant measures of the discrete skeleton, since the latter could in general be strictly larger. Moreover, in some situations (as turns out to be the case in our application), it may be relatively easy to show the former, but non-trivial to show the latter. In such cases, it is more convenient to directly apply the continuous-time version of the result, as formulated in Proposition 5.1.

5.2 Construction of a Candidate Coupling

Fix two initial conditions and in the set defined in (5.3), and let be the diffusion model with initial condition . Then, by Definition 4.12, and the associated process satisfy (4.23) and (4.24) with in place of . In particular, . Now, define the (random) locally integrable function

| (5.5) |

Combining (4.15) and (4.15), the latter with , we have

| (5.6) |

We now construct another process , which starts from , on the same probability space. Fix . Given defined above, it is easy to see that -almost surely, the linear integral equation

| (5.7) |

has a unique continuous solution , which has the from

| (5.8) |

where . Since satisfies the diffusion model SPDE, by Proposition 4.18, satisfies (3.10), which when combined with (5.6) and (5.7), shows that for ,

| (5.9) |

Also, for , define

| (5.10) |

Clearly, is also continuous, almost surely. We now introduce a process that, as shown in Corollary 5.5 below, can be characterized as the unique (almost surely locally integrable) solution to the following renewal equation:

| (5.11) |

In Proposition 5.4, we first collect some general results on solutions of the renewal equation. Part a of the proposition is used below in the proof of Corollary 5.5, part b is used in Section 5.4 to establish an asymptotic convergence property of the diffusion model, and part c is used in Section 5.3 to establish measurability properties of the candidate asymptotic coupling. Recall the definition of the convolution operator from Section 1.5.

Proposition 5.4.

-

a.

If , the renewal equation

(5.12) has a unique locally integrable solution .

-

b.

If has a finite second moment, the function lies in and its integral lies in , then the solution of the renewal equation (5.12) also lies in . Moreover, there exist constants such that

(5.13) -

c.

If , then the solution of the renewal equation (5.12) also lies in and the mapping that takes to is continuous.

Proof.

Corollary 5.5.

There exists a unique locally integrable process that satisfies equation (5.11).

Proof.

Next, for , define

| (5.14) |

Substituting from above into (5.11) and simplifying terms, we obtain

| (5.15) |

which we observe is analogous to (5.5). Moreover, recall the definition (4.16) of the family of mappings , and in a fashion analogous to the definition of in (4.24), define

| (5.16) |

Since is almost surely continuous, it follows from (the proof of) Proposition 4.14.a that is also a continuous -valued process. Finally, set , and define to be the joint distribution of .

5.3 Proof of the Measurability Property

In this section we prove the measurability condition (II) of Proposition 5.1 for the family of candidate equivalent couplings that we constructed in the last section. Let be the associated processes defined therein.

Lemma 5.6.

Proof.

We claim that for every , almost surely, the mapping is continuous from to . We first show that assuming the claim, the assertion of the lemma holds, and then we prove the claim.

Assuming that the claim holds, for every , and functions , by invoking the bounded convergence theorem we conclude that the mapping

is continuous, and hence, measurable. The assertion in the lemma then follows from the definition of the Kolmogorov -algebra and a standard monotone class argument.

We now turn to the proof of the claim. Fix . We start by showing that the mapping from to is continuous, almost surely. Fix , where is a subset of with , on which Proposition 4.14 holds and the Brownian motion has continuous paths. Recall again that denotes the space of continuous functions on with . The map from to is continuous due to Lemma 3.3.b. Since by definition (4.23), and the CMS mapping is continuous by Lemma 4.10, it follows that the mapping is continuous. In particular, for fixed , the mapping is continuous and, by the definition (4.24) of , continuity of the translation map (Lemma 3.3.c) and continuity of the mapping (Lemma 4.9.b), the mapping is also continuous. Thus, we have shown that the mapping is continuous for every and .

Next, we prove continuity of the mapping . It is clear from the equation (5.8) and the form of the function specified below (5.8) that the map is continuous. Together with the continuity of proved above, this implies that the map is continuous. Next, recall that by the definition of , if then . Using this identity, equation (5.6) and equation (4.15) with , we have

When combined with the continuity of the mappings (which holds by Lemma 3.3.b) and (established above), this implies that the mapping is continuous. In turn, due to the continuity of the mappings that take to and established above, this implies that the map from to defined in (5.10) is also continuous. Next, observe from (5.11) that satisfies the renewal equation where

Therefore, defined as , , satisfies the renewal equation where, using the identity (which holds because ), we obtain

Therefore, lies in and the map from to is continuous. An application of Proposition 5.4.c then shows that also lies in , and that the map from to and hence, from to , is continuous. Consequently, defined in (5.14) is also obtained as a continuous map of . Finally, by definition (5.16) of , continuity of the translation map (Lemma 3.3.c) and the continuity of the mapping (Lemma 4.9.b), can also be expressed as a continuous mapping of . Therefore, the mapping is also continuous for every . This completes the proof of the claim, and hence, the proof of the lemma. ∎

5.4 Asymptotic Convergence

In this section, we prove condition (III) of Proposition 5.1, that is, the asymptotic convergence of the processes and whenever their respective initial conditions and lie in the set . Specifically, given the processes defined in Section 5.2, define for , , , , , , , , , and . Our goal is to show that almost surely,

| (5.17) |

Subtracting from both sides of equation (5.7), we see that satisfies the integral equation

| (5.18) |

whose solution is given by

| (5.19) |

Clearly, converges to zero with probability one as .

We now turn to the proof of the asymptotic convergence of , which consists of two main steps. In the first step (see Lemma 5.7) we use the fact that satisfies a certain renewal equation to show that it is square integrable. In the second step (Lemma 5.9) we combine the square integrability of with other estimates to show that converges to zero in . First, note that on substituting the expression for from (5.10) into the definition of in (5.14), subtracting this from the equation for in (4.26), and recalling the definition of from (4.22), we obtain

| (5.20) |

When combined with (5.18) and the fact that , (5.20) further simplifies to

| (5.21) |

Lemma 5.7.

Proof.

Subtracting (5.15) from (5.5), we obtain

| (5.23) |

Substituting from (5.21) into (5.23) and using Fubini’s theorem, we see that satisfies the renewal equation

| (5.24) |

with

| (5.25) |

We now claim that there exists such that

| (5.26) |

where . We first show how the proof of the lemma follows from the claim. Indeed, since satisfies the renewal equation (5.24), has a finite second moment by Assumption II, and and lie in by (5.26), Proposition 5.4.b implies that there exist deterministic constants such that

When combined with (5.26), this implies that lies in and satisfies (5.22) with and . It only remains to prove the claim (5.26).

First, note that for every , using the fact that because implies , we have

| (5.27) |

Moreover, by Young’s inequality (see, e.g., [4, Theorem 3.9.4]), Assumption I.c, the finite mean assumption on and (5.19), we have

| (5.28) |

Together with (5.25), (5.27) and Minkowski’s integral inequality, this implies that

Since due to (5.19), we conclude that (5.26) holds with . This completes the proof of the lemma. ∎

In Lemma 5.9 below, we use (5.22) to prove the asymptotic convergence of . The proof of Lemma 5.9 makes use of the following elementary result on the convolution operator.

Lemma 5.8.

Let , and suppose is bounded and as . Then satisfies

Proof.

Fix and choose such that , where is the essential supremum of a function . Then for ,

which implies that

Sending in the last display, and noting that because , it follows that . Since is arbitrary, the lemma follows on sending . ∎

Proof.

Subtracting (5.16) from (4.24), we see that

Using (4.16) and (5.21) to expand the right-hand side above, we have

| (5.29) |

where and To prove the lemma, it suffices to show that almost surely, the norm (as a function of ) of each of the terms on the right-hand side of (5.29) goes to zero as . For the first term, as by (3.5) of Lemma 3.3. For the second term, by (5.19) we have

which converges to zero because is finite by Assumption I.b.

Next, since is continuous and is bounded and continuous by Assumption I.c, by the bounded convergence theorem, for each , has a weak derivative

Therefore, applying Hölder’s inequality and Tonelli’s theorem, we see that

and, likewise, we have

Now, is integrable by (5.19) and both and are continuous, bounded by , lie in and vanish at infinity. Thus, it follows from Lemma 5.8 that as , and , and consequently, . Similarly, since is continuous and has a continuous and bounded density due to Assumption I.b, by the bounded convergence theorem, for each , has weak derivative

An exactly analogous analysis then shows that

and

Again, since is integrable by Lemma 5.7 and both and are integrable, bounded by and vanish at infinity, another application of Lemma 5.8 shows that as , and , and consequently, . This completes the proof. ∎

5.5 Marginal Distributions

In this section, we continue to use the notation introduced in Section 5.4. The main result of this section is as follows:

Proposition 5.10.

Proof.

has distribution by definition. For fixed , to show that the distribution of is equivalent to , we first show that satisfies the same equations as , but with replaced by some process , and then invoke Girsanov’s theorem to prove that is a Brownian motion on the entire time interval under another probability measure that is equivalent to . Let , where is defined by

| (5.30) |

and set . We will first show that

| (5.31) |

where is the CMS mapping introduced in Definition 4.11. To prove (5.31), first note that the expression (5.9) for can be rewritten as

| (5.32) |

By equation (5.15) for , relation (4.15), and Fubini’s theorem, we have

Together with (5.32), this implies

| (5.33) |

where

| (5.34) |

Also, by definitions (5.10) and (5.14) of and and equation (5.30), we have

| (5.35) |

Substituting from (5.35) in (5.33) and noting from (5.34) and the fact that , , we conclude that

| (5.36) |

Comparing the equation obtained on substituting from (5.36) into (5.35) with the CMS equation (4.25), and comparing (5.35) with the CMS equation (4.26), it follows that (5.31) holds. Furthermore, defined in (5.16) has the same form as the expression (4.24) for , but with replaced by . In summary, we have shown that is defined in the same way as the process in Definition 4.12, except that is replaced by . Therefore, to complete the proof, it suffices to show that there exists a new probability measure on that is equivalent to and under , is a Brownian motion independent of .

Define the process as

| (5.37) |

where is as above. Consider the local martingale , with quadratic variation , . Note that and by (5.30), (5.22) and (5.19), there exist constants , such that

Therefore, , which implies that is a uniformly integrable exponential martingale (see, e.g., [25, Section 3]). Then, by Doob’s convergence theorem, converges almost surely as to an integrable random variable . The inequality also implies that is itself a uniformly integrable martingale. Therefore, by another application of Doob’s convergence theorem, almost surely, has a finite limit as , which ensures that is almost surely positive. Define a probability measure on by:

| (5.38) |

where denotes expectation with respect to . Since is almost surely positive, is equivalent to Also, by Girsanov’s theorem (see, e.g., [38, Theorem (38.5), Chapter IV]), is a Brownian motion under . Moreover, recall that under , for every , , is a martingale independent of , . Thus, by [22, Proposition 5.4, Chapter 3] (note that since is a martingale, for every and , , and hence, our definition of is compatible with its definition (5.4) in [22, Chapter 3]) under , is a martingale, and for Therefore, under , is a martingale measure with covariance function given in (3.2) and is independent of . This completes the proof. ∎

5.6 Proof of Theorem 3.8

Proof of Theorem 3.8.

Proposition 4.23 shows that the diffusion model is a time-homogeneous Feller Markov process on the Polish space . Let be the transition semigroup associated to . In order to show that has at most one invariant distribution, it suffices to show that the candidate coupling constructed in Section 5.2 satisfies the conditions of Proposition 5.1. Recall that . For every , it follows from Lemma 5.6 that the mapping is measurable for every and from Proposition 5.10 that . Moreover, (5.17) follows from (5.19) and Lemma 5.9, and hence, So, to complete the proof of the theorem, it suffices to show that the subset satisfies the first condition of Proposition 5.1.

Let be an invariant distribution of . Assume to the contrary that . Let be a -valued random element distributed as , and let be the diffusion model with initial condition . Since is invariant for , for every , is also distributed as , and therefore, . Equivalently, we have for all Since has continuous sample paths almost surely, this implies that

| (5.39) |

By (4.25), (4.26) and (5.39), almost surely, for every we have and

For every , and are two independent finite variance Gaussian random variables that are independent of . Therefore, is the sum of the random variable , an independent zero-mean Gaussian random variable with finite covariance, and a finite constant , which therefore satisfies . This contradicts (5.39), and hence, , and the proof is complete. ∎

Acknowledgements. The authors would like to thank anonymous reviewers for feedback that improved the presentation of the paper.

Appendix A Properties of the Renewal Equation

Proof of Proposition 5.4..

For part a, let be the renewal function associated with the distribution function , where denotes the -fold convolution of . Since the service distribution with cdf has probability density function , by [2, Proposition 2.7, Section V], has density , which satisfies the equation Moreover, since is continuous (and hence locally bounded), is also locally bounded. Define the function . Then the local integrability of and local boundedness of imply the local integrability of , and, using the distributive and associative properties of the convolution operation, we have

Therefore, is a solution to the equation given in (5.12).

To show that is the unique solution to (5.12) that lies in , let , be two solutions to (5.12). Then is a solution to the equation . For , let , and note that the function satisfies

Also, for every ,

where the finiteness holds since . Hence, is locally bounded and satisfies the renewal equation (i.e., with “input function” identically equal to zero). However, by [2, Theorem 2.4, p. 146], this implies . Since this holds for every , this implies .

To see why part b holds, first note that implies . Therefore, is a solution to (5.12) from part a, and, moreover, it satisfies

and hence, recalling the notation ,

| (A.1) |

With some abuse of notation, we also let denote the renewal measure associated with the distribution , and let denote Lebesgue measure on . Then, since is the density of the signed measure with respect to on , we have where is the total variation norm. Since has a finite second moment (and has mean ), it follows from [29, eqn. (6.10), p. 86] (with ) that is finite and hence, . By Young’s inequality, we then have Substituting this inequality into (A.1), we obtain the bound (5.13) with and

Finally, to see why c holds, note that since and is bounded on finite intervals, also lies in , and hence, so does . Moreover, for every and corresponding solutions , we have

and the continuity claim follows. ∎

Appendix B Properties of the Auxiliary Mapping

Proof of Lemma 4.9.

We first prove property a. Fix By Assumption I.a, the mapping is continuously differentiable with derivative . Also, by Assumption I.c, is continuously differentiable with derivative , and since is continuous, the mapping is continuously differentiable with derivative . Therefore,

Furthermore, from (4.16), we have

| (B.1) |

Since the right-hand side of (B.1) is a uniformly bounded and integrable function of , it follows that for each , . Furthermore, using Assumption I.c and (4.17), we have

| (B.2) |

Again, and are bounded and integrable by Assumption II, and therefore, also lies in . Thus, . This completes the proof of part a.

For part b, let and be functions in . By linearity of the mapping and the bounds (B.1) and (B), we have

| (B.3) |

and

| (B.4) |

with , which is finite by Assumption I.c and Assumption II. The assertion in part b. then follows from (B.3) and (B.4).

For part c, fix . For every , by definition (4.16) of , Minkowski’s integral inequality, Assumption I.b and Fubini’s theorem, we have

| (B.5) | ||||

The first two terms in (B.5) converge to zero as by the continuity of . Also, since Assumption I implies that is square integrable, for every , the term is bounded by and hence, the third term converges to zero as by an application of the bounded convergence theorem and continuity of the translation map in the norm.

Similarly, for every , by definition (4.17) of and Assumption I.c,

| (B.6) | ||||

Again, the first two terms on the right-hand side above converge to zero as by the continuity of , and the third term converges to zero as by continuity of the translation map in the norm, boundedness of (see Assumption I.c and Remark 3.2) and the bounded convergence theorem. The -continuity of follows from (B.5) and (B.6). ∎

Appendix C Properties of

Proof of Lemma 3.3.c.

The first claim follows from the following elementary inequality: for every

For the second claim, fix and . Since is dense in , there exists a function that is uniformly continuous on such that . Therefore, for every ,

Taking the limit as on both sides of the last inequality, by the uniform continuity of and the dominated convergence theorem, we have

Since is arbitrary, this shows that the translation map is continuous in . If , then and so the above argument also shows that the map is continuous in , which proves the continuity of in . Finally, by definition,

Since the right-hand side above converges to zero as Similarly, since and (3.5) follows. ∎

Appendix D Solution to the Transport Equation

We now provide a full justification of Lemma 4.19. Define , for . First, we show that is indeed a solution to (4.36). Since , by Lemma 4.9, and for every , has weak derivative .

Because , and are continuous (see Assumption I), the mapping is continuous, and hence, locally integrable. Moreover, for ,

which is equal to . Here, the application of Fubini’s theorem in the second equality above is justified because and are continuous and hence locally integrable. This shows that satisfies (4.36).

Next, let be any function that satisfies properties 1 and 2 of Lemma 4.9 and equation (4.36). Then also satisfies properties 1 and 2, and

| (D.1) |

Fix and , and for , let be a regularizing kernel:

for a positive function with and . For define and note that for every , is continuously differentiable on (in particular, ), with . Hence, , and since

In turn, this yields

| (D.2) |