High-order ADI scheme for option pricing in stochastic volatility models

Abstract

We propose a new high-order alternating direction implicit (ADI) finite difference scheme for the solution of initial-boundary value problems of convection-diffusion type with mixed derivatives and non-constant coefficients, as they arise from stochastic volatility models in option pricing. Our approach combines different high-order spatial discretisations with Hundsdorfer and Verwer’s ADI time-stepping method, to obtain an efficient method which is fourth-order accurate in space and second-order accurate in time. Numerical experiments for the European put option pricing problem using Heston’s stochastic volatility model confirm the high-order convergence.

keywords:

Option pricing , stochastic volatility models , mixed derivatives , high-order ADI schemeMSC:

65M06 , 91B281 Introduction

In financial option pricing, stochastic volatility models as the Heston model [20] have become one of the standard approaches. Unlike the classical Black & Scholes model [3] the volatility (or standard deviation) of the option’s underlying asset is not assumed to be constant, but is modelled as a second, correlated stochastic diffusion process. This additional source of randomness allows to model option prices more accurately and to fit higher moments of the asset return distribution. Using Ito’s lemma and standard arbitrage arguments, partial differential equations of convection-diffusion type with mixed second-order derivatives are derived for pricing options.

For some stochastic volatility models and under additional restrictions, closed-form solutions can be obtained by Fourier methods (e.g. [20, 15]). Another approach is to derive approximate analytic expressions, see e.g. [2] and the literature cited therein. In general, however, —even in the Heston model [20] when the parameters in it are non constant— the partial differential equations arising from stochastic volatility models have to be solved numerically. Moreover, many (so-called American) options feature an additional early exercise right. Then one has to solve a free boundary problem which consists of the partial differential equation and an early exercise constraint for the option price. Also for this problem one typically has to resort to numerical approximations.

In the mathematical literature, there are many papers on numerical methods for option pricing, mostly addressing the one-dimensional case of a single risk factor and using standard, second order finite difference methods (see, e.g., [34] and the references therein). More recently, high-order finite difference schemes (fourth order in space) were proposed [17, 32, 33] that use a compact stencil (three points in space). In the option pricing context, see e.g. [11, 12, 27].

There are less works considering numerical methods for option pricing in stochastic volatility models, i.e. for two spatial dimensions. Finite difference approaches that are used are often standard, second-order methods, e.g. in [26] where different efficient methods for solving the American option pricing problem for the Heston model are proposed. Other approaches include finite element-finite volume [36], multigrid [5], sparse wavelet [25], or spectral methods [35].

The classical alternating direction implicit (ADI) method, introduced by Peaceman and Rachford [31], Douglas [6, 7], Fairweather and Mitchell [30], is a very powerful method that is especially useful for solving parabolic equations (without mixed derivative terms) on rectangular domains. Beam and Warming [1], however, have shown that no simple ADI scheme involving only discrete solutions at time levels and can be second-order accurate in time in the presence of mixed derivatives. To overcome this limitation and construct an unconditionally stable ADI scheme of second order in time, a number of results have been given by Hundsdorfer and Verwer [24, 23] and more recently by in’t Hout and Welfert [22]. These schemes are second-order accurate in time and space. In [21] different second-order ADI schemes of this type are applied to the Heston model. In [13] this approach was combined with different high-order discretisations in space, using high-order compact schemes for two-dimensional convection-diffusion problems with mixed derivatives and constant coefficients. In [19] this approach was combined with sparse grids and applied to a multi-dimensional Black-Scholes equation, again with constant coefficients.

In the present paper we present a high-order ADI method for option pricing in a rather general class of stochastic volatility models, extending the approach in [13]. This involves two-dimensional convection-diffusion equations with mixed derivative terms and space-dependent coefficients which adds substantial algebraic complexity in the derivation of the scheme. The new scheme is second-order accurate in time and fourth-order accurate in space.

This paper is organised as follows. In the next section we discuss stochastic volatility models for option pricing and the related pricing partial differential equation. In Section 3 we recall the Hundsdorfer-Verwer ADI splitting in time. For the spatial discretisation we introduce different high-order methods, in Section 4 for the implicit steps, and in Section 5 for the explicit steps. The solution of the resulting scheme and numerical boundary conditions are discussed in Sections 6 and 7. We present numerical convergence and stability results in Section 8. Section 9 concludes.

2 Stochastic volatility models

We consider the following class of stochastic volatility models: asume that asset spot price and variance follow two stochastic diffusive processes for ,

| (1a) | ||||

| (1b) | ||||

which are characterised by two Brownian motions, and , with constant correlation parameter . The drift coefficient for stochastic asset returns is given by the mean return of the asset where and the diffusion coefficient is given by .

The drift coefficient of the asset variance is given by , where constants and are the mean reversion speed of and the long run mean of , respectively. The diffusion coefficient is given by where constant is the volatility of volatility. The constant riskless interest rate is denoted by The constants determine the stochastic volatility model used.

The class of stochastic volatility models (1) includes a number of known stochastic volatility models: The most prominent stochastic volatility model, the Heston model [20] (also called square root (SQR) model) specifies the variance by

Other known stochastic volatility models include the GARCH (or VAR model) model, see [8], where the stochastic variance is modelled by

and the 3/2 model [29] in which the variance follows the process

All of the three stochastic volatility models mentioned above use a linear mean-reverting drift for the stochastic process of the variance , but there are also models, in which the drift is mean reverting in a non-linear fashion. Following [4], we denote these models with an additional “N”: in the SQRN model the stochastic variance follows

in the VARN model

and in the -N model

see [4].

Applying standards arbitrage arguments and Ito’s lemma to the class of stochastic volatility models (1), we can derive the following second order partial differential equation for any financial derivative , to be solved backwards in time with , , :

| (2) |

Here, is the market price of volatility risk which is usually assumed to be proportional to the variance: , where . The boundary conditions and final condition are determined by the type of financial derivative we are solving for. For example, in the case of the European Put Option:

The remaining boundary condition at can be obtained by looking at the formal limit in (2), i.e.,

| (3) |

This boundary condition is used frequently, e.g. in [26, 36]. Alternatively, one can use a homogeneous Neumann condition [5], i.e.,

| (4) |

By using a change of variables:

we transform the partial differential equation to an convection-diffusion equation in two spatial dimensions with a mixed derivative term. The transformed partial differential equation and boundary/initial conditions are now satisfied by , where , , :

| (5) |

| (6a) | ||||||

| (6b) | ||||||

| (6c) | ||||||

| (6d) | ||||||

| (6e) | ||||||

In order to discretise the problem and solve numerically, we truncate our spatial boundaries to finite values. Take , where , and , where , so that the spatial domain forms a closed rectangle in of points with uniform spacing of in the -direction and in the -direction:

The lower -boundary is truncated to to ensure non-degeneracy of the partial differential equation for all values of . We also take a uniform partition of into points such that , where . We denote the discrete approximation of by and .

3 Hundsdorfer-Verwer ADI splitting scheme

We consider the Alternating Direction Implicit (ADI) time-stepping numerical method proposed by Hundsdorfer and Verwer [24, 23]. Our partial differential equation (5) takes the form . We employ the splitting where unidirectional and mixed derivative differential operators are given by:

| (7) |

We consider (5) with the splitting (7) and look for a semi-discrete approximation at time . Given an approximation we can calculate an approximation for at time using the differential operators from (7):

| (8a) | ||||

| (8b) | ||||

| (8c) | ||||

| (8d) | ||||

| (8e) | ||||

| (8f) | ||||

| (8g) | ||||

The parameter is taken to be to ensure second-order accuracy in time. The choice of is discussed in [24]. Typically it is fixed to . Larger values give stronger damping of the implicit terms while lower values return better accuracy.

The first and fourth step in (8) can be solved explicitly, while the remaining steps are solved implicitly. Our aim is to derive high-order spatial discretisations of the differential operators. Following [13] we combine high-order compact finite difference methods for the implicit steps with a (classical, non-compact) high-order stencil for the explicit steps.

4 High-order compact scheme for implicit steps

For , consider

| (9) |

with arbitrary right hand side . We wish to derive a fourth-order accurate in space approximation for (9) which can be used to solve the implicit second and fifth step in (8). Using standard second-order central difference operators and Taylor’s expansion, we have:

| (10) | ||||

| (11) |

where

If we can find second-order accurate expressions for and using only information on the compact stencil, then it will be possible to approximate and with fourth order accuracy on the compact stencil. By differentiating (9) once and twice with respect to , respectively, it is possible to express and in terms of first- and second-order derivatives of and with respect to :

| (12) | ||||

| (13) |

By substituting standard second-order central difference operators into and we obtain second-order accurate in space approximations for and :

| (14) | ||||

| (15) |

Substituting (14) and (15) into (10) and (11), respectively, yields:

| (16) | ||||

| (17) |

Substituting these fourth-order approximations for and into (9) and rearranging the equation such that all derivatives of with respect to are on the left hand side and all derivatives of with respect to are on the right hand side we obtain a fourth-order compact scheme for (9):

| (18) |

Finally, substituting the expressions for the difference operators , into (18) and separating the terms into values of and at the three horizontally adjacent nodal points in space, we get:

| (19) |

Equation (19) defines a fourth-order compact approximation for (19). In other words, we have a system of equations which defines a fourth-order accurate approximation for (19) at any point on the inner grid of the spatial domain (all points of the spatial domain except those that lie on the and boundaries). To approximate (19) at points along the boundaries of the inner grid of the spatial domain, we will require a contribution from the Dirichlet values at the -boundaries of the spatial domain. We collect these separately in a vector . Details on the boundary conditions are given in Section 7. The linear system to be solved can be written in matrix form:

where , . The coefficient matrices and are block diagonal matrices, with the following structure:

where each and are tri-diagonal matrices.

Let us consider now the case of :

| (20) |

Due to the appearance of terms in the coefficients of , the algebraic complexity in deriving a fourth-order accurate scheme in space is much greater. By Taylor’s expansions we obtain:

| (21) | |||

| (22) |

We wish to find second order accurate approximations for and on the compact stencil in order to find fourth-order accurate expressions for and . Re-arranging (20), we get:

Via repeated applications of the chain rule, second-order accurate approximations for and are given by:

| (23) |

| (24) |

where and denote the standard second-order central difference operators.

Substituting (23) and (24) into (21) and (22), respectively, yields fourth-order accurate approximations (not given here) for and on the compact stencil. By substituting these fourth-order accurate approximations into (20) and separating the and terms onto the left and right hand sides, respectively, we obtain a linear system which can be represented in matrix form:

where , . We do not impose any boundary conditions in -direction, but discretise the boundary grid points with the same scheme, and handle resulting ghost points via extrapolation; details on the boundary conditions are given in Section 7. The coefficient matrices and are block tri-diagonal matrices with the following structures:

where each and are diagonal matrices, with values on these diagonals given as follows:

| (27) |

| (28) |

| (29) |

5 High-order scheme for explicit steps

The first and fourth steps of the ADI scheme (8) operate only on previous approximations to explicitly calculate an updated approximation. The differential operator in these steps takes the form of the right hand side of (5). For the mixed derivative term it seems not to be possible to exploit the structure of the differential operator to obtain a fourth-order approximation on a compact computational stencil. Hence, in order to maintain fourth-order accuracy of the scheme in the explicit steps of (8), the derivatives in each differential operator , and are approximated using classical, fourth-order central difference operators which operate on a larger -stencil in the spatial domain.

For , we have the following scheme:

For , we have:

Finally, for the mixed derivative term , the following computational stencil is used:

Using these fourth-order approximations, the first and fourth step in (8) can be computed directly. The values at the spatial boundaries for each solution of the ADI scheme are determined by the boundary conditions, the computational stencil is required for all remaining points in the spatial domain. For the explicit steps, the -point computational stencil exceeds the spatial boundary when we wish to approximate differential operator at any point along the boundary of the spatial domain’s inner grid. For example if we wish to evaluate , we will require contributions from ghost points which fall outside the spatial domain, as marked by bullet points in Figure 1.

We extrapolate information from grid points , where to establish values at these ghost points for the purpose of evaluating the differential operator at any point along the boundary of the inner grid of the spatial domain. To calculate the values at these ghost points, we use the following five-point extrapolation formulae for three cases:

The extrapolation at the and boundaries and the remaining three corners is handled analogously.

6 Solving the high-order ADI scheme

Starting from a given , the ADI scheme (8) involves six approximation steps to obtain , the solution at the next time level. The first approximation can be solved for explicitly using the -point computational stencil derived in Section 5. The second approximation for our solution, denoted by , has to be solved for implicitly:

| (30) |

We apply the fourth-order compact scheme established in Section 4 to solve (30). In matrix form we obtain

Collecting unknown terms on the left hand side and known terms , and on the right hand side we get

To solve, we invert the tri-diagonal matrix . For the third step of the ADI scheme, we proceed analogously, and use the the high-order compact scheme presented in Section 4 to solve for implicitly. The fourth, fifth and sixth step of the ADI scheme are performed analogously as the first, second and third steps, respectively.

Note that the matrix appears twice in the scheme (8), in the second and fifth step. Similarly, appears in the third and the sixth step. Hence, using LU-factorisation, only two matrix inversions are necessary in each time step of scheme (8). Moreover, since the coefficients in the partial differential equation (5) do not depend on time, and the matrices are therefore constant, they can be LU-factorised before iterating in time to obtain a highly efficient algorithm.

7 Boundary conditions

For the case of the Dirichlet conditions at and we impose

Using the homogeneous Neumann conditions (6d) and (6e) which are correct in the limit and , respectively, at the (finite) boundaries and would result in a dominant error along these boundaries. Hence, we do not impose any boundary condition at these two boundaries but discretise the partial derivative using the computational stencil from the interior. The values of the unknown on the boundaries are set by extrapolation from values in the interior. This introduces a numerical error, and it needs to be considered that the order of extrapolation should be high enough not to affect the overall order of accuracy. We refer to Gustafsson [18] to discuss the influence of the order of the approximation on the global convergence rate. We use the following extrapolation formulae:

8 Numerical experiments

In this section we report the results of our numerical experiments. We estimate the numerical convergence order of the high-order ADI scheme and then perform additional experiments to validate its stability.

8.1 Numerical convergence

We perform a numerical study to compute the order of convergence of the high-order ADI scheme. Since the initial condition for the option pricing problem, the payoff function , is non-smooth at , we cannot in general expect to observe high-order convergence [28]. A straightforward way to smooth the initial condition is to choose the mesh in such a way that the non-smooth point of the initial condition is not a point of the mesh. The construction of such a mesh is always possible in a simple manner. Following this approach, the non-smooth payoff can be directly considered in our scheme and, indeed, we observe high-order numerical convergence. Alternatively, suitable smoothing operators can be employed to achieve a similar effect, see [28, 14].

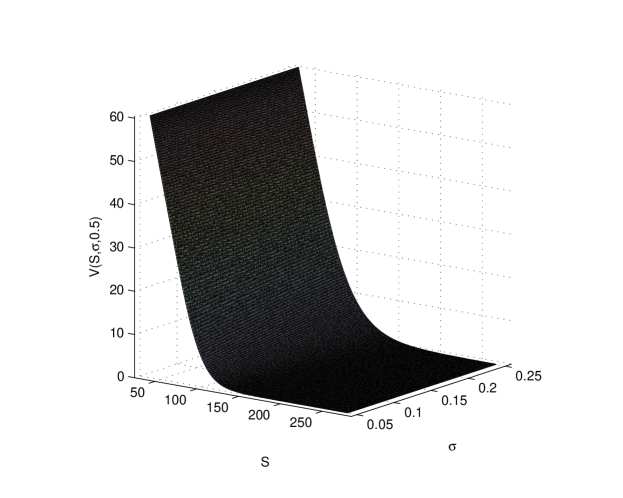

For convenience, we choose an equally sized space step creating an evenly-spaced mesh both horizontally and vertically. We set the parameter in (8) in all numerical experiments. Figure 2 shows the numerical solution for the European option price at time using the parameters from Table 1.

| Parameter | Value |

|---|---|

| Strike price | |

| Time to maturity | |

| Interest rate | |

| Volatility of volatility | |

| Mean reversion speed | |

| Long run mean of volatility | |

| Correlation | |

| Parabolic mesh ratio | |

| Stochastic volatility drift parameter | |

| Stochastic volatility diffusion parameter |

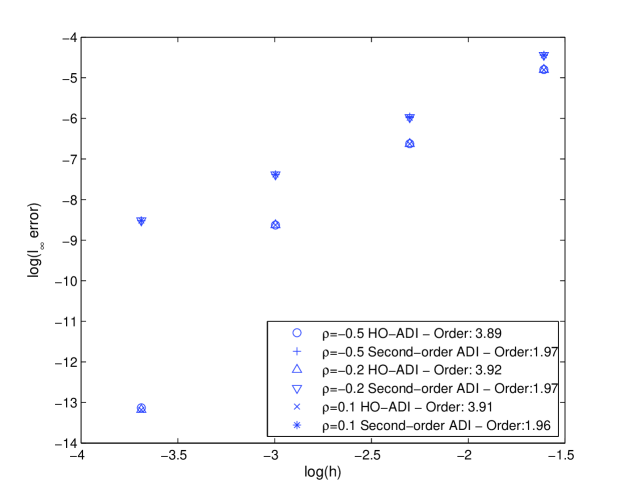

We compute the -norm error and the maximum norm error of the numerical solution with respect to a numerical reference solution on a fine grid. We fix the parabolic mesh ratio to a constant value which is natural for parabolic partial differential equations as (5). Then, asymptotically, we expect these errors to converge as for some and representing constants. This implies Hence, the double-logarithmic plot against should be asymptotic to a straight line with slope . This gives a method for experimentally determining the order of the scheme. We expect to observe a numerical convergence rate of approximately order in space. For comparison, we conduct additional experiments using a standard, second-order ADI scheme based on (8) combined with a second-order central difference discretisation in space. Figure 3 shows the double logarithmic plot of -error versus space step . We observe that the numerical convergence order agrees well with the theoretical order of the schemes.

In all cases, the high-order ADI scheme outperforms the standard second-order ADI scheme for a given mesh width . Or in other words, to realise a chosen level of accuracy we could use a coarser grid for the high-order ADI scheme than the standard second-order scheme which translates into solving smaller linear systems and therefore is more computationally efficient.

8.2 Numerical stability analysis

In this section we investigate whether there are any stability restrictions on the choice of the time-step for the high-order ADI scheme. Unlike for standard second-order schemes, the algebraic complexity of the numerical stability analysis of high-order compact schemes is very high since the established stability notions imply formidable algebraic problems for high-order compact schemes. As a result, there are only few stability results for high-order compact schemes in the literature [14, 9, 16]. This is even more pronounced in higher spatial dimensions, as most of the existing studies with analytical stability results for high-order compact schemes are limited to a one-dimensional setting.

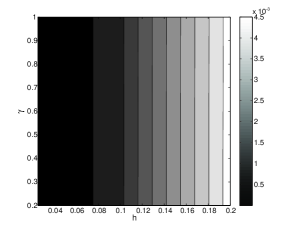

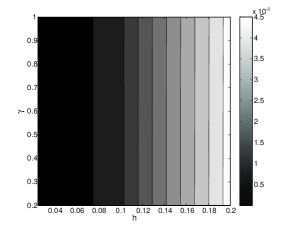

For diffusion equations (without convection) with mixed derivative terms and constant coefficients, a stability analysis of the ADI method (8) with standard second-order discretisation in space [22] revealed it to be unconditionally stable. The analysis in [22] is based on studying the stability for a simplified, linear test equation which implies the assumption that all involved discretisation matrices are normal and commuting. The discretisation matrices of high-order compact schemes generally do not fulfil these assumptions and, hence, in the present case with non-constant coefficients, the situation is much more involved. A thorough stability analysis is therefore beyond the scope of the present paper. Instead, to validate the stability of the scheme, we perform additional numerical stability tests. We remark that in our numerical experiments we observe stable behaviour throughout. We compute numerical solutions for varying values of the parabolic mesh ratio and the mesh width . Plotting the associated -norm errors in the plane should allow us to detect stability restrictions depending on or oscillations that occur for high cell Reynolds numbers (large ). This approach for a numerical stability study was also used in [9, 10].

We give results for the European Put option using the parameter from Table 1. For our stability plots we use with and a descending sequence of spatial grid points. Figure 4 shows the stability plots for the correlation parameter and .

We observe that the influence of the parabolic mesh ratio on the -error is only marginal and the relative error does not exceed as a value for both stability plots. We can infer that there does not seem to be a stability condition on for either situation. For increasing values of , which also result in a higher cell Reynolds number, the error grows gradually, and no oscillations in the numerical solutions occur.

These observations are confirmed by additional numerical convergence tests for varying parabolic mesh ratio . The numerical convergence orders reported in Table 2 show that the numerical convergence order for the high-order scheme, measured both in the -norm and -norm is very close to four, and does not depend on the parabolic mesh ratio .

| 0.2 | 0.4 | 0.6 | 0.8 | 1.0 | |

|---|---|---|---|---|---|

| HO-ADI -error | 3.8871 | 3.8870 | 3.8868 | 3.8866 | 3.8864 |

| Standard ADI -error | 2.4521 | 2.4519 | 2.4517 | 2.4514 | 2.4510 |

| HO-ADI -error | 3.8960 | 3.8961 | 3.8961 | 3.8962 | 3.8964 |

| Standard ADI -error | 1.9744 | 1.9744 | 1.9744 | 1.9743 | 1.9742 |

9 Conclusion

By combining fourth-order (compact and non-compact) finite difference schemes in space with Hundsdorfer and Verwer’s second-order ADI time-stepping scheme, we have constructed a new numerical method for solving option pricing problems for stochastic volatility models. Numerical experiments for approximating the price of a European Put option using Heston’s stochastic volatility model with generic parameters confirm the numerical convergence of the scheme in space and time while the results for a range of parabolic mesh ratios suggest unconditional stability.

Acknowledgement

BD acknowledges partial support by the Leverhulme Trust research project grant ‘Novel discretisations for higher-order nonlinear PDE’ (RPG-2015-69). JM has been supported in part by a studentship under the EPSRC Doctoral Training Partnership (DTP) scheme.

References

- [1] R.M. Beam and R.F. Warming, Alternating Direction Implicit methods for parabolic equations with a mixed derivative, Siam J. Sci. Stat. Comput., 1(1), (1980).

- [2] E. Benhamou, E. Gobet, and M. Miri. Time Dependent Heston Model, SIAM J. Finan. Math. 1, 289–325, 2010.

- [3] F. Black and M. Scholes. The pricing of options and corporate liabilities. J. Polit. Econ. 81, 637–659, 1973.

- [4] P. Christoffersen, K. Jacobs, and K. Mimouni. Models for S&P500 dynamics: Evidence from realized volatility, daily returns, and option prices. Review of Financial Studies, 23:3141–3189, 2010.

- [5] N. Clarke and K. Parrott. Multigrid for American option pricing with stochastic volatility. Appl. Math. Finance 6(3), 177–195, 1999.

- [6] J. Douglas, Alternating direction methods for three space variables, Numer. Math., 4, 41–63, 1962.

- [7] J. Douglas and J. E. Gunn, A general formulation of alternating direction methods. I. Parabolic and hyperbolic problems, Numer. Math., 6, 428–453, 1964.

- [8] J. Duan. The GARCH option pricing model. Math.Finance, 5(1):13–32, 1995.

- [9] B. Düring and M. Fournié. High-order compact finite difference scheme for option pricing in stochastic volatility models. J. Comput. Appl. Math., 236(17):4462–4473, 2012.

- [10] B. Düring, M. Fournié, and C. Heuer. High-order compact finite difference schemes for option pricing in stochastic volatility models on non-uniform grids. J. Comput. Appl. Math., 271(18):247–266, 2014.

- [11] B. Düring, M. Fournié, and A. Jüngel. Convergence of a high-order compact finite difference scheme for a nonlinear Black-Scholes equation. Math. Mod. Num. Anal. 38(2), 359–369, 2004.

- [12] B. Düring, M. Fournié, and A. Jüngel. High-order compact finite difference schemes for a nonlinear Black-Scholes equation. Intern. J. Theor. Appl. Finance 6(7), 767–789, 2003.

- [13] B. Düring, M. Fournié, and A. Rigal. High-order ADI schemes for convection-diffusion equations with mixed derivative terms. In: Spectral and High Order Methods for Partial Differential Equations - ICOSAHOM’12, M. Azaïez et al. (eds.), pp. 217–226, Lecture Notes in Computational Science and Engineering 95, Springer, Berlin, Heidelberg, 2013.

- [14] B. Düring and C. Heuer. High-order compact schemes for parabolic problems with mixed derivatives in multiple space dimensions. SIAM J. Numer. Anal., 53(5):2113–2134, 2015.

- [15] B. Düring. Asset pricing under information with stochastic volatility. Rev. Deriv. Res. 12(2), 141–167, 2009.

- [16] M. Fournié and A. Rigal. High Order Compact Schemes in Projection Methods for Incompressible Viscous Flows, Commun. Comput. Phys. 9(4), 994–1019, 2011.

- [17] M.M. Gupta, R.P. Manohar and J.W. Stephenson, A single cell high-order scheme for the convection-diffusion equation with variable coefficients, Int. J. Numer. Methods Fluids, 4, 641–651, 1984.

- [18] B. Gustafsson. The convergence rate for difference approximation to general mixed initial-boundary value problems. SIAM J. Numer. Anal. 18(2), 179–190, 1981.

- [19] C. Hendricks, M. Ehrhardt and M. Günther, High-order-compact ADI schemes for diffusion equations with mixed derivatives in the combination technique, preprint, 2015.

- [20] S.L. Heston. A closed-form solution for options with stochastic volatility with applications to bond and currency options. Review of Financial Studies 6(2), 327–343, 1993.

- [21] K.J. in’t Hout and S. Foulon. ADI finite difference schemes for option pricing in the Heston model with correlation. Int. J. Numer. Anal. Mod. 7, 303–320, 2010.

- [22] K.J. in’t Hout and B.D. Welfert. Stability of ADI schemes applied to convection-diffusion equations with mixed derivative terms. Appl. Num. Math. 57, 19–35, 2007.

- [23] W. Hundsdorfer and J.G Verwer, Numerical solution of time-dependent advection-diffusion-reaction equations, Springer Series in Computational Mathematics, 33, Springer-Verlag, Berlin, (2003).

- [24] W. Hundsdorfer, Accuracy and stability of splitting with stabilizing corrections, Appl. Num. Math., 42, 213–233, (2002).

- [25] N. Hilber, A. Matache, and C. Schwab. Sparse wavelet methods for option pricing under stochastic volatility. J. Comput. Financ. 8(4), 1–42, 2005.

- [26] S. Ikonen and J. Toivanen. Efficient numerical methods for pricing American options under stochastic volatility. Numer. Methods Partial Differential Equations 24(1), 104–126, 2008.

- [27] W. Liao and A.Q.M. Khaliq. High-order compact scheme for solving nonlinear Black-Scholes equation with transaction cost. Int. J. Comput. Math. 86(6), 1009–1023, 2009.

- [28] H.O. Kreiss, V. Thomee, and O. Widlund. Smoothing of initial data and rates of convergence for parabolic difference equations. Comm. Pure Appl. Math. 23, 241–259, 1970.

- [29] A.L. Lewis. Option valuation under stochastic volatility. Finance Press, Newport Beach, CA, 2000.

- [30] A. R. Mitchell and G. Fairweather, Improved forms of the alternating direction methods of Douglas, Peaceman, and Rachford for solving parabolic and elliptic equations, Numer. Math. 6, 285–292, 1964.

- [31] D.W. Peaceman and H.H. Rachford Jr., The numerical solution of parabolic and elliptic differential equations, J. Soc. Ind. Appl. Math. 3, 28–41, 1959.

- [32] A. Rigal, Schémas compacts d’ordre élevé: application aux problèmes bidimensionnels de diffusion-convection instationnaire I, C.R. Acad. Sci. Paris. Sr. I Math., 328, 535–538, 1999.

- [33] W.F. Spotz and C.F. Carey. Extension of high-order compact schemes to time-dependent problems. Numer. Methods Partial Differential Equations 17(6), 657–672, 2001.

- [34] D. Tavella and C. Randall. Pricing Financial Instruments: The Finite Difference Method. John Wiley & Sons, 2000.

- [35] W. Zhu and D.A. Kopriva. A spectral element approximation to price European options with one asset and stochastic volatility. J. Sci. Comput. 42(3), 426–446, 2010.

- [36] R. Zvan, P.A. Forsyth and K.R. Vetzal. Penalty methods for American options with stochastic volatility. J. Comp. Appl. Math. 91(2), 199–218, 1998.