22email: tbel@cemi.rssi.ru 33institutetext: N. Konyukhova, S. Kurochkin 44institutetext: Dorodnicyn Computing Centre of RAS, ul. Vavilova 40, Moscow, Russia

44email: nadja@ccas.ru; kuroch@ccas.ru 55institutetext: S. Pinelas et al. (eds.), Differential and Difference Equations with Applications, Springer

Proceedings in Mathematics & Statistics 47, DOI 10.1007/978-1-4614-7333-6-3

Singular Problems for Integro-Differential Equations in Dynamic Insurance Models

Abstract

A second order linear integro-differential equation with Volterra integral operator and strong singularities at the endpoints (zero and infinity) is considered. Under limit conditions at the singular points, and some natural assumptions, the problem is a singular initial problem with limit normalizing conditions at infinity. An existence and uniqueness theorem is proved and asymptotic representations of the solution are given. A numerical algorithm for evaluating the solution is proposed, calculations and their interpretation are discussed. The main singular problem under study describes the survival (non-ruin) probability of an insurance company on infinite time interval (as a function of initial surplus) in the Cramér-Lundberg dynamic insurance model with an exponential claim size distribution and certain company’s strategy at the financial market assuming investment of a fixed part of the surplus (capital) into risky assets (shares) and the rest of it into a risk free asset (bank deposit). Accompanying ”degenerate” problems are also considered that have an independent meaning in risk theory.

1 Introduction

The important problem concerning the application of financial instruments in order to reduce insurance risks has been extensively studied in recent years (see, e.g., kony_AzMul , kony_BelKonKur1 , kony_BelKonKur2 , and references therein). In particular in kony_BelKonKur1 , kony_BelKonKur2 the optimal investing strategy is studied for risky and risk-free assets in Cramér-Lundberg (C.-L.) model with budget constraint, i.e., without borrowing.

This paper complements and revises some results of kony_BelKonKur2 . The parametric singular initial problem (SIP) for an integro-differential equation (IDE) considered here is a part of the optimization problem stated and analyzed in kony_BelKonKur1 , kony_BelKonKur2 : the solution of this SIP gives the survival probability corresponding to the optimal strategy when the initial surplus values are small enough. The singular problem under study is also interesting both as an independent mathematical problem and for the models in risk theory. We give more complete and rigorous analysis of this problem in comparison with kony_BelKonKur2 and add some new ”degenerate” problems having independent meaning in risk theory. Some new numerical results are also discussed.

The paper is organized as follows. In Sect. 2 we set the main mathematical problem and formulate the main results concerning solvability of this problem and the solution behavior; we describe also two ”degenerate” problems (when some parameters in the IDE are equal to zero) and discuss their exact solutions. In Sect. 3 we give a rather brief description of the mathematical model for which the problem in question arises (for detailed history, models’ description and derivation of the IDE studied here, see kony_BelKonKur1 , kony_BelKonKur2 ). In Sect. 4 we describe our approach to the problem and give brief proofs of main results (for some assertions, we omit the proofs since they are given in kony_BelKonKur2 ). In Sect. 5 we study an accompanying singular problem for capital stock model (the third ”degenerate” problem); the results of this section are completely new. Numerical results and their interpretation are given in Sect. 6.

2 Singular Problems for IDEs and Their Solvability

2.1 Main Problem

The main singular problem under consideration has the form:

| (1) |

| (2) |

| (3) |

| (4) |

Here in general all the parameters , , , , are real positive numbers.

The second limit condition at zero is a corollary of the first one and IDE (1) itself. For this IDE, conditions (2) imply providing a degeneracy of the IDE (1) as : any solution to the singular problem without initial data (1), (2) must satisfy IDE (1) up to the singular point .

The ”truncated” problem (1)-(3) (constrained singular problem) always has the trivial solution . A nontrivial solution is singled out by the additional limit conditions at infinity (4).

In what follows we use notation

| (5) |

where is a Volterra integral operator, , is the linear space of continuous functions defined and bounded on .

For IDE (1), the entire singular problem on was neither posed nor studied before kony_BelKonKur2 and the present paper.

2.2 Formulation of the Main Results

The problem (1)-(4) may be rewritten in the equivalent parametrized form:

| (6) |

| (7) |

| (8) |

| (9) |

Here is an unknown parameter whose value must be defined.

Lemma 1

For IDE (6), let the values , , , , be fixed with , , , , . Then for any fixed the IDE SIP (6), (7) is equivalent to the following singular Cauchy problem (SCP) for ODE:

| (10) |

| (11) |

There exists a unique solution to SCP (10), (11) (therefore also to the equivalent IDE SIP (6), (7)); for small , this solution is represented by the asymptotic power series

| (12) |

where coefficients are independent of and may be found by formal substitution of series (12) into ODE (10), namely from the recurrence relations

| (13) |

| (14) |

| (15) |

Theorem 2.1

For IDE (1), let all the parameters , , , , be fixed positive numbers and let the inequality

| (16) |

be fulfilled. Then the following statements are valid:

- 1.

-

2.

The function can be obtained as the solution of IDE SIP (6), (7), namely by solving the equivalent ODE SCP (10), (11) where the value must be chosen to satisfy conditions at infinity (4) (as the normalizing condition); for defined in this way, the restriction is valid for any finite , i.e., for , inequalities (3) are fulfilled tacitly.

-

3.

If the inequality is fulfilled then the solution is concave on ; in particular this is true when

(17) -

4.

If the inequality is true then is convex on a certain interval where is an inflection point, .

- 5.

-

6.

For large , the asymptotic representation

(18) takes place with where in general the value (as well as the value ) cannot be determined using local analysis methods.

2.3 The ”Degenerate” Problems and Their Exact Solutions

A particular case of IDE (1) is considered ”degenerate” when some of its parameters are equal to zero.

The First ”Degenerate” Case: , , ,

For this case, the ”degenerate” IDE problem

| (19) |

| (20) |

is equivalent to the ODE problem with one parameter:

| (21) |

| (22) |

Then we obtain , , and

| (23) |

If inequality (17) is not valid, i.e., , then there is no solution to problem (19), (20) [resp., to problem (21), (22)].

In what follows, function (23) is well known in classical C.-L. risk theory and has an independent meaning (see further Sect. 3.1).

The Second ”Degenerate” Case: , , , ,

For , the ”degenerate” IDE problem

| (24) |

is equivalent to the parametrized ODE problem:

| (25) |

This implies , ,

| (26) |

where, taking into account the notation , , for incomplete gamma-function (see, e.g., kony_BatErd ), we have

| (27) |

In particular we obtain the asymptotic representation when :

| (28) |

For , the solution to the IDE problem on ,

| (29) |

can be found as a solution to the equivalent ODE problem:

| (30) |

This implies the same formulas (26)-(28) with where is the usual Euler gamma-function. In particular, using the formula

we obtain here: if then ; if then and ; if then the function is unbounded as but integrable on .

This ”degenerate” case has an independent meaning in risk theory (see further Sect. 3.2).

3 Origin of the Problem: the Cramér-Lundberg Dynamic Insurance Models

3.1 The Classical C.-L. Insurance Model

Consider the classical risk process: . Here is the surplus of an insurance company at time , is the initial surplus, is the premium rate; is a Poisson process with parameter defining, for each , the number of claims applied on the interval ; is the series of independent identically distributed random values with some distribution (, ), describing the sequence of claims; these random values are also assumed to be independent of the process . For this model, the positiveness condition for the net expected income (”safety loading”) has the form (17).

Denote by the time of ruin, then is the probability of ruin at the infinite time interval.

A classical result in the C.-L. risk theory kony_Grand : under condition (17) and assuming existence of a constant (”the Lundberg coefficient”) such that equality holds, the probability of ruin as a function of the initial surplus admits the estimate , . Moreover, if the claims are exponentially distributed,

| (31) |

then , and the survival probability is given by the exact formula (23), i.e., coincides with the exact solution of the first ”degenerate” problem to which input singular problem (1)-(4) reduces formally as (see Sect. 2.3).

For as a bifurcation parameter, the value is critical: if then , .

3.2 The C.-L. Insurance Model with Investment into Risky Assets

Now consider the case where the surplus is invested continuously into shares with price dynamics described by geometric Brownian motion model:

| (32) |

Here is the share price at time , is the expected return on shares, is the volatility, is a standard Wiener process.

Denoting by the company’s surplus at time we get , where is the amount of shares in the portfolio. Then the surplus dynamics meets the relation Taking into account (32), we obtain:

| (33) |

In contrast with the classical model, condition (17) (the positiveness of ”safety loading”) is not assumed here.

For the dynamical process (33), the survival probability satisfies on the following linear IDE (see, e.g., kony_BelKonKur1 , kony_FKP and references therein):

| (34) |

From (34), assuming exponential distribution of claims (31) we get the initial IDE (1) under study.

3.3 The C.-L. Model with Investment into a Risk-Free Asset

The model under study comprises a more general case where only a constant part () of the surplus is invested in shares (with the expected return and volatility ) whereas remaining part is invested into a risk free asset (bank deposit with constant interest rate ): the case may be reduced to the case by a simple change of the parameters (shares characteristics), namely , .

Moreover, when the surplus is invested entirely into a risk free asset (bank deposit with constant interest rate), we obtain the second ”degenerate” problem (with or without premiums) to which the input singular problem (1)-(4) reduces formally as . For , , , , there exists the exact solution (26), (27) and the asymptotic representation (28) is valid (for details, see Sect. 2.3).

Thus when the surplus is entirely invested into a risk free asset then the survival probability is not equal to zero, for , even if premiums (insurance payments) are absent () and has a good asymptotic behavior as .

The formulas (26)-(28) see also in Paulsen Gj .

4 On the Approach to Main Problem and Proofs of Main Results

4.1 The Singular Problem for IDE: Uniqueness of the Solution and Its Monotonic Behavior

As shown in Sect. 3, we can formulate the input singular IDE problem in the form (6), (7), (9), where operator is defined by (5), is an unknown parameter whose value must be found, and, for the solution to the problem (6), (7), (9), the restrictions needed are (8).

Lemma 2

Proof.

-

1.

Supposing the opposite, let be any other solution to problem (6), (7), (9), i.e., . Then two cases may occur: the first one with , and the second one with .

For the first case, it follows that there exists a nontrivial solution of IDE (6) satisfying conditions . Let be its maximum point: (if takes only non-positive values then we consider the solution instead). Then , . But from IDE (6) a contradiction follows:

(35) For the second case, there exists a linear combination of solutions such that and satisfies conditions . If there exists a value with , then the first case argument is valid. Otherwise, the inequality contradicts to which follows from (7).

-

2.

The other assertions are proved analogously.

4.2 SCPs for Accompanying Linear ODEs

Reduction of the Second Order IDE to a Third-Order ODE

The known possibility of reducing the second order IDE (6) to a third order ODE is important for further exposition. First, we note that

| (36) |

Then differentiating IDE (6) in view of (36) gives a linear third order IDE

| (37) |

which also implies the limit condition

| (38) |

Together with the input limit condition (2) it implies the limit equality

| (39) |

In order to remove the integral term, we add IDE (37) and initial IDE (6) multiplied by and get the linear third order ODE (10). Then the same limit condition (39) must be fulfilled to provide a degeneration of this ODE as .

Suppose and rewrite ODE (10) in more canonical forms for ODEs with pole-type singularities at zero and infinity (for classification of isolated singularities of linear ODE systems and general theory of ODEs of this class, see, e.g., the monographs kony_cod , kony_Fedoryuk and kony_Wasov complementing each other). Now, for , we have to study the following singular ODEs: for small , we need to consider the equation

| (40) |

and for large , we shall consider the same equation in the form

| (41) |

We see that both ODE (40) and equivalent ODE (41) have irregular (strong) singularities of rank as and as .

Singularity at Zero: Replacement of the SIP for IDE by an Equivalent SCP for ODE

Proof of Lemma 1

First, we must show that the previous transformations permit us to replace the input SIP (6), (7) for an IDE by the SCP (10), (11) for an ODE.

In the straight direction (from the IDE SIP to the ODE SCP), the statement is evident. Now let be a solution of ODE SCP (10), (11). We have to prove that satisfies IDE (6).

Denote the left part of IDE (6) with the function by . We have to prove that . Indeed, the way ODE (10) was derived means that meets the first-order ODE

with the general solution of the form where is an arbitrary constant. Since meets conditions (11), it follows from IDE (6) that . This implies , i.e., .

The other statements of Lemma 1 follow from the results of kony_Kony1 (see kony_BelKonKur2 for details).

SCP at Infinity and Its Two-Parameter Family of Solutions

For , we have an SCP at infinity for the second order ODE (41) with the conditions

| (42) |

Using the known results for linear ODEs with irregular singularities, we obtain the following assertions (more complete in comparison with FKP-theorem).

Lemma 3

For ODE (41), suppose that , , whereas and are arbitrary real numbers (). Then:

- 1.

- 2.

- 3.

For a detailed proof of Lemma 3, see kony_BelKonKur2 .

Corollary 1

Summarizing all results, we obtain the proof of Theorem 2.1.

5 The Accompanying Singular Problem for Capital Stock Model (the Third ”Degenerate” Case: , , , , )

For this case, the input singular IDE problem has the form:

| (45) |

| (46) |

| (47) |

and restrictions (3) are needed for the solution.

The following lemma is analogous to Lemma 2 (with a similar proof).

Lemma 4

Analogously to the previous approach, the singular IDE problem (45)-(47) is equivalent to the following singular ODE problem:

| (48) |

| (49) |

| (50) |

First, consider SCP at regular (weak) singular point , i.e., SCP (48), (49) introducing notation:

| (51) |

| (52) |

The following lemma is analogous to Lemma 1.

Lemma 5

For IDE (45), let the values , , , be fixed with , , , . Then:

- 1.

-

2.

There exists a one-parameter family of solutions to the ODE SCP (48), (49) (therefore also to the equivalent IDE SIP (45), (46)) and the following representation holds:

(53) here is a parameter, is defined by (51), and is a solution to SCP

(54) (55) where and are defined by (52); there exists a unique solution to the SCP (54), (55) and it is a holomorphic function at the point ,

(56) where the coefficients may be found by formal substitution of series (56) into ODE (54), namely, from the recurrence relations:

(57) (58) moreover, if , then when ; when ; and at last when (but is integrable as ).

Summarizing the results and taking into account that Lemma 3 and Corollary 1 are valid for any , we obtain

Theorem 5.1

For IDE (45), let all the parameters , , , be fixed positive numbers and let inequality (16) of ”robustness of shares” be fulfilled. Then the following assertions are valid:

- 1.

- 2.

- 3.

-

4.

If then the solution is concave on ; moreover, if then , and if then but is an integrable on function.

-

5.

If then , and is convex on a certain interval where is an inflection point, .

-

6.

For large , the asymptotic representation (18) holds with where in general the value cannot be determined using local analysis methods.

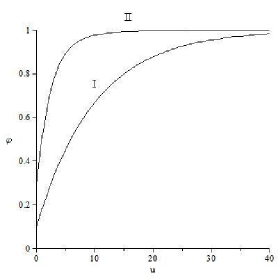

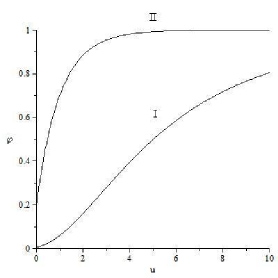

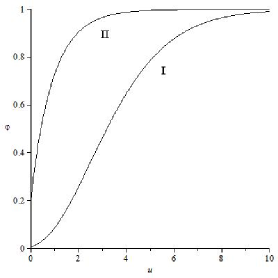

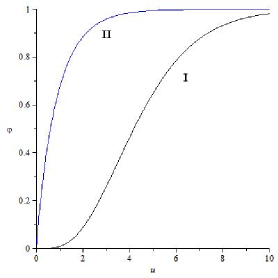

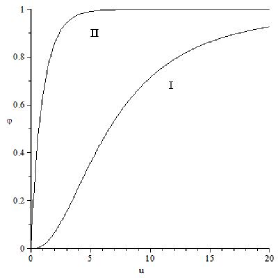

6 Numerical Examples and Their Interpretation

For the main case , our study shows that the input singular IDE problem (1)-(4) may be reduced to the auxiliary ODE SCP (10), (11) with the parameter to be defined, . The asymptotic expansion of the solutions at zero (12) is used to transfer the limit initial conditions (11) from the singular point to a nearby regular point ; the derivatives of the solution may be evaluated by formal differentiation of the representation (12). Consequently, a regular Cauchy problem is to be solved starting from the point . The parameter in (12) is evaluated numerically to satisfy the condition .

For the additional case , the singular IDE problem (45)-(47) is equivalent to the singular ODE problem (48)-(50). To solve this problem we use formula (59) and the auxiliary SCP (54), (55). The convergent power series (56)-(58) is used to transfer limit initial conditions (55) from the singular point to a regular point , and then a regular Cauchy problem is to be solved starting from this point.

Maple programming package was used as a numerical tool.

For all examples, we put , , and, for , , the shares are ”robust”: (Figs.1–5).

7 Conclusions

The study shows that use of risky assets is not favorable for non-ruin with large initial surplus values and constant structure of the portfolio. However, the study of the cases when positiveness of the safety loading does not hold shows risky assets to be effective for small initial surplus values: while ruin is inevitable in the case without investing, the survival probability grows considerably as grows in presence of investing even if the premiums are absent (moreover, the second derivative of the solution for small is positive!). The study in kony_BelKonKur1 , kony_BelKonKur2 of the optimal strategy for exponential distribution of claims shows that the part of risky investments should be as present surplus tends to infinity.

Acknowledgements.

This work was supported by the Russian Fund for Basic Research: Grants RFBR 10-01-00767 and RFBR 11-01-00219.References

- (1) Azcue, P., Muler, N.: Optimal investment strategy to minimize the ruin probability of an insurance company under borrowng constraints. Insurance Math. Econom. 44(1) 26–34 (2009)

- (2) Bateman, H., Erdélyi, A.: Higher Transcendental Functions. McGraw-Hill, New York (1953)

- (3) Belkina, T.A., Konyukhova, N.B., Kurkina, A.O.: Optimal investment problem in the dynamic insurance models: I. Investment strategies and the ruin probability. Survey on Applied and Industrial Mathematics. 16(6), 961–981 (2009) [in Russian]

- (4) Belkina, T.A., Konyukhova, N.B., Kurkina, A.O.: Optimal investment problem in the dynamic insurance models: II. Cramér-Lundberg model with the exponential claims. Survey on Applied and Industrial Mathematics. 17(1), 3–24 (2010) [in Russian]

- (5) Coddington, E.A., Levinson, N.: Theory of Ordinary Differential Equations. McGraw-Hill, New York (1955)

- (6) Fedoryuk, M.V.: Asymptotic Analysis: Linear Ordinary Differential Equations. Springer, Berlin (1993)

- (7) Frolova, A., Kabanov, Yu., Pergamenshchikov, S.: In the insurance business risky investments are dangerous. Finance Stochast. 6(2), 227–235 (2002)

- (8) Grandell, J.: Aspects of Risk Theory. Springer, Berlin (1991)

- (9) Konyukhova, N.B.: Singular Cauchy problems for systems of ordinary differential equations. U.S.S.R. Comput. Maths. Math. Phys. 23(3), 72–82 (1983)

- (10) Paulsen, J. and Gjessing, H.K.: Ruin theory with stochastic return on investments. Adv. Appl. Probab. 29(4), 965–985 (1997)

- (11) Wasov, W.: Asymptotic Expansions for Ordinary Differential Equations. Dover, New York (1987)