Approximate option pricing in the Lévy Libor model

Abstract.

In this paper we consider the pricing of options on interest rates such as caplets

and swaptions in the Lévy Libor model developed by \citeNEberleinOezkan05. This model is an extension to Lévy driving processes of the

classical log-normal Libor market model (LMM) driven by a Brownian motion. Option

pricing is significantly less tractable in this model than in the LMM

due to the appearance of stochastic terms in the jump part of the

driving process when performing the measure changes which are standard

in pricing of interest rate derivatives. To obtain explicit

approximation for option prices, we propose to

treat a given Lévy Libor model as a suitable perturbation of the log-normal LMM. The method is inspired by recent works by \citeNCernyDenklKallsen13 and \citeNMenasseTankov15. The approximate option

prices in the Lévy Libor model are given as the corresponding LMM

prices plus correction terms which depend on the characteristics of

the underlying Lévy process and some additional terms obtained from

the LMM model.

Key words: Libor market model, caplet, swaption, Lévy Libor model, asymptotic approximation.

1. Introduction

The goal of this paper is to develop explicit approximations for option prices in the Lévy Libor model introduced by \citeNEberleinOezkan05. In particular, we shall be interested in price approximations for caplets, whose pay-off is a function of only one underlying Libor rate and swaptions, which can be regarded as options on a “basket” of multiple Libor rates of different maturities.

A full-fledged model of Libor rates such as the Lévy Libor model is typically used for the purposes of pricing and risk management of exotic interest rate products. The prices and hedge ratios must be consistent with the market-quoted prices of liquid options, which means that the model must be calibrated to the available prices / implied volatilities of caplets and swaptions. To perform such a calibration efficiently, one therefore needs explicit formulas or fast numerical algorithms for caplet and swaption prices.

Computation of option prices in the Lévy Libor model to arbitrary precision is only possible via Monte Carlo. Efficient simulation algorithms suitable for pricing exotic options have been proposed in [\citeauthoryearKohatsu-Higa and TankovKohatsu-Higa and Tankov2010, \citeauthoryearPapapantoleon, Schoenmakers, and SkovmandPapapantoleon et al.2012], however, these Monte Carlo algorithms are probably not an option for the purposes of calibration because the computation is still too slow due to the presence of both discretization and statistical error.

EberleinOezkan05, \citeNKluge05 and [\citeauthoryearBelomestny and SchoenmakersBelomestny and Schoenmakers2011] propose fast methods for computing caplet prices which are based on Fourier transform inversion and use the fact that the characteristic function of many parametric Lévy processes is known explicitly. Since in the Lévy Libor model, the Libor rate is not a geometric Lévy process under the corresponding probability measure , unless (see Remark 3.1 below for details), using these methods for requires an additional approximation (some random terms appearing in the compensator of the jump measure of are approximated by their values at time , a method known as freezing).

In this paper we take an alternative route and develop approximate formulas for caplets and swaptions using asymptotic expansion techniques. Inspired by methods used in \citeNCernyDenklKallsen13 and \citeNMenasseTankov15 (see also [\citeauthoryearBenhamou, Gobet, and MiriBenhamou et al.2009, \citeauthoryearBenhamou, Gobet, and MiriBenhamou et al.2010] for related expansions “around a Black-Scholes proxy” in other models), we consider a given Lévy Libor model as a perturbation of the log-normal LMM. Starting from the driving Lévy process of the Lévy Libor model, assumed to have zero expectation, we introduce a family of processes parameterized by , together with the corresponding family of Lévy Libor models. For one recovers the original Lévy Libor model. When , the family converges weakly in Skorokhod topology to a Brownian motion, and the option prices in the Lévy Libor model corresponding to the process converge to the prices in the log-normal LMM. The option prices in the original Lévy Libor model can then be approximated by their second-order expansions in the parameter , around the value . This leads to an asymptotic approximation formula for a derivative price expressed as a linear combination of the derivative price stemming from the LMM and correction terms depending on the characteristics of the driving Lévy process. The terms of this expansion are often much easier to compute than the option prices in the Lévy Libor model. In particular, we shall see the expansion for caplets is expressed in terms of the derivatives of the standard Black’s formula, and the various terms of the expansion for swaptions can be approximated using one of the many swaption approximations for the log-normal LMM available in the literature.

This paper is structured as follows. In Section 2 we briefly review the Lévy Libor model. In Section 3 we show how the prices of European-style options may be expressed as solutions of partial integro-differential equations (PIDE). These PIDEs form the basis of our asymptotic method, presented in detail in Section 4. Finally, numerical illustrations are provided in Section 5.

2. Presentation of the model

In this section we present a slight modification of the Lévy Libor model by \citeNEberleinOezkan05, which is a generalization, based on Lévy processes, of the Libor market model driven by a Brownian motion, introduced by \shortciteNSandmannSondermannMiltersen95, \shortciteNBraceGatarekMusiela97 and \shortciteNMiltersenSandmannSondermann97.

Let a discrete tenor structure be given, and set , for . We assume that zero-coupon bonds with maturities , , are traded in the market. The time- price of a bond with maturity is denoted by with .

For every tenor date , , the forward Libor rate at time for the accrual period is a discretely compounded interest rate defined as

| (2.1) |

For all , we set .

To set up the Libor model, one needs to specify the forward Libor rates , , such that each Libor rate is a martingale with respect to the corresponding forward measure using the bond with maturity as numéraire. We recall that the forward measures are interconnected via the Libor rates themselves and hence each Libor rate depends also on some other Libor rates as we shall see below. More precisely, assuming that the forward measure for the most distant maturity (i.e. with numéraire ) is given, the link between the forward measure and is provided by

| (2.2) |

for every . The forward measure is referred to as the terminal forward measure.

2.1. The driving process

Let us denote by a complete stochastic basis and let be an -valued Lévy process on this stochastic basis with Lévy measure and diffusion matrix . The filtration is generated by and is the forward measure associated with the date , i.e. with the numeraire . The process is assumed without loss of generality to be driftless under .

Moreover, we assume that . This implies in addition that is a special semimartingale and allows to choose the truncation function , for . The canonical representation of is given by

| (2.3) |

where denotes a standard -dimensional Brownian motion with respect to the measure , is the random measure of jumps of and is the -compensator of .

2.2. The model

Denote by the column vector of forward Libor rates. We assume that under the terminal measure , the dynamics of is given by the following SDE

| (2.4) |

where is the drift term and a deterministic volatility matrix. We write , where denotes the -dimensional volatility vector of the Libor rate and assuming that , for .

One typically assumes that the jumps of are bounded from below, i.e. , for all and for some strictly negative constant , which is chosen such that it ensures the positivity of the Libor rates given by (2.4).

The drift is determined by the no-arbitrage requirement that has to be a martingale with respect to , for every . This yields

| (2.5) | ||||

The above drift condition follows from (2.2) and Girsanov’s theorem for semimartingales noticing that

where

| (2.6) |

is a special semimartingale with a -dimensional -Brownian motion given by

| (2.7) |

and the -compensator of given by

with

| (2.9) |

Equalities (2.7) and (2.2), and consequently also the drift condition (2.5), are implied by Girsanov’s theorem for semimartingales applied first to the measure change from to and then proceeding backwards. We refer to \citeN[Proposition 2.6]Kallsen06 for a version of Girsanov’s theorem that can be directly applied in this case. Note that the random terms appear in the measure change due to the fact that for each we have

| (2.10) |

We point out that the predictable random terms can be replaced with in equalities (2.5), (2.7) and (2.2) due to absolute continuity of the characteristics of .

Therefore, the vector process of Libor rates , given in (2.4)

with the drift (2.5), is a time-inhomogeneous Markov process and its infinitesimal generator under is given by

| (2.11) | ||||

for a function and with the function , for and , given by

Remark 2.1 (Connection to the Lévy Libor model of \citeNEberleinOezkan05).

The dynamics of the forward Libor rate , for all , in the Lévy Libor model of \citeNEberleinOezkan05 (compare also \citeNEberleinKluge07) is given as an ordinary exponential of the following form

| (2.12) |

for some deterministic volatility vector and the drift which has to be chosen such that the Libor rate is a martingale under the forward measure . Here is a -dimensional Lévy process given by

with the -characteristics , where . The Lévy measure has to satisfy the usual integrability conditions ensuring the finiteness of the exponential moments. The dynamics of is thus given by the following SDE

for all , where is a time-inhomogeneous Lévy process given by

and the drift is given by

3. Option pricing via PIDEs

Below we present the pricing PIDEs related to general option payoffs and then more specifically to caplets and swaptions. We price all options under the given terminal measure .

3.1. General payoff

Consider a European-type payoff with maturity given by , for some tenor date . Its time- price is given by the following risk-neutral pricing formula

where is the solution of the following PIDE111A detailed proof of this statement is out of scope of this note. Here we simply assume that Equation (3.1) admits a unique solution which is sufficiently regular and is of polynomial growth. The existence of such a solution may be established first by Fourier methods for the case when there is no drift and then by a fixed-point theorem in Sobolev spaces using the regularizing properties of the Lévy kernel for the general case (see [\citeauthoryearDe FrancoDe Franco2012, Chapter 7] for similar arguments). Once the existence of a regular solution has been established, the expression for the option price follows by the standard Feynman-Kac formula.

| (3.1) | ||||

and denotes the transformed payoff function given by

In what follows we shall in particular focus on two most liquid interest rate options: caps (caplets) and swaptions.

3.2. Caplet

Consider a caplet with strike and payoff at time . Note that here the payoff is in fact a -measurable random variable and it is paid at time . This is known as payment in arrears. There exist also other conventions for caplet payoffs, but this one is the one typically used.

The time- price of the caplet, denoted by is thus given by

| (3.2) | ||||

where is the solution to

| (3.3) | ||||

with

For the second equality in (3.2) we have used the measure change from to given in (2.2).

Remark 3.1.

Noting that the payoff of the caplet depends on one single underlying forward Libor rate , it is often more convenient to price it directly under the corresponding forward measure , using the first equality in (3.2). Thus, one has

where is the solution to

| (3.4) | ||||

with and where is the generator of under the forward measure . In the log-normal LMM this leads directly to the Black’s formula for caplet prices. However, in the Lévy Libor model the driving process under the forward measure is not a Lévy process anymore since its compensator of the random measure of jumps becomes stochastic (see (2.9)). Therefore, passing to the forward measure in this case does not lead to a closed-form pricing formula and does not bring any particular advantage. This is why in the forthcoming section we shall work directly under the terminal measure .

3.3. Swaptions

Let us consider a swaption, written on a fixed-for-floating (payer) interest rate swap with inception date , payment dates and nominal . We denote by the swaption strike rate and assume for simplicity that the maturity of the swaption coincides with the inception date of the underlying swap, i.e. we assume . Therefore, the payoff of the swaption at maturity is given by , where denotes the value of the swap with fixed rate at time given by

where

| (3.5) |

is the swap rate i.e. the fixed rate such that the time- price of the swap is equal to zero. Here we denote

| (3.6) |

Note that . Dividing the numerator and the denominator in (3.5) by and using the telescopic products together with (2.1) we see that for a function given by

| (3.7) |

for .

Therefore, the swaption price at time is given by

| (3.8) | ||||

where is the solution to

| (3.9) | ||||

with .

4. Approximate pricing

4.1. Approximate pricing for general payoffs under the terminal measure

Following an approach introduced by \citeNCernyDenklKallsen13, we introduce a small parameter into the model by defining the rescaled Lévy process with . The process is a martingale Lévy process under the terminal measure with characteristic triplet with respect to the truncation function , where

We now consider a family of Lévy Libor models driven by the processes , , and defined by

| (4.1) |

where the drift is given by (2.5) with replaced by . Substituting the explicit form of , we obtain

where we define

| (4.2) |

for all , and

| (4.3) |

for all . We denote the infinitesimal generator of by . For a smooth function , the infinitesimal generator can be expanded in powers of as follows:

Consider now a financial product whose price is given by a generic PIDE of the form (3.1) with replaced by . Assuming sufficient regularity222See [\citeauthoryearMénassé and TankovMénassé and Tankov2015] for rigorous arguments in a simplified but similar setting., one may expand the solution in powers of :

| (4.4) |

Substituting the expansions for and into this equation, and gathering terms with the same power of , we obtain an ’open-ended’ system of PIDE for the terms in the expansion of .

The zero-order term satisfies

with

| (4.5) | ||||

| (4.6) |

Hence, by the Feynman-Kac formula

| (4.7) |

where the process satisfies the stochastic differential equation

| (4.8) |

with a -dimensional standard Brownian motion with respect to and an -dimensional matrix such that .

To obtain an explicit approximation for the higher order terms and given above, we consider the following proposition.

Proposition 4.1.

Let be an -dimensional log-normal process whose components follow the dynamics

where and are measurable functions such that

and for all and some ,

We denote by the process starting from at time , and by the -th component of this process. Let be a bounded measurable function and define

Then, for all , the process

is a martingale.

The proof can be carried out by direct differentiation for smooth

together with a standard approximation argument for a general measurable .

Furthermore, we assume the following simplification for the drift terms:

-

For all and , the random quantities in the terms in the expansion of the drift of the Libor rates under the terminal measure are constant and equal to their value at time , i.e. for all :

(4.9) This simplification is known as freezing of the drift and is often used for pricing in the Libor market models.

Coming back now to the first-order term , we see that it is the solution of

| (4.10) |

with

| (4.11) | ||||

and the drift term

| (4.12) |

Moreover,

We have

Lemma 4.2.

Proof.

Similarly, the second-order term is the solution of

| (4.15) |

with

| (4.16) | ||||

and the drift

| (4.17) |

Lemma 4.3.

Proof.

Once again by the Feynman-Kac formula applied to (4.15) we have

| (4.25) | ||||

In order to obtain an explicit expression for , we apply Proposition 4.1 combined with the simplification (4.9) for the drift terms and above. More precisely, the expressions for the third and the fourth expectation, which are present in the terms and , follow by a straightforward application of Proposition 4.1 after using the simplification for . We get

To obtain explicit expressions for and , firstly we insert the expression for as given by (4.1). After some straightforward calculations, based again on the application of Proposition 4.1 and the simplification (4.9) for , which yields

Collecting the terms above concludes the proof. ∎

Summarizing, we get the following expansion for the time- price of the payoff when .

Proposition 4.4.

Consider the model (4.1) and a European-type payoff with maturity given by . Assuming (4.9), its time- price for satisfies

| (4.26) |

with

where denotes the time- price of the payoff in the log-normal LMM with covariance matrix and the drift given by (4.6), and are given by (4.3), by (4.7) and and by (4.2) and (4.18), respectively.

4.2. Approximate pricing of caplets

Recalling that the caplet price is given by (3.2), where is the solution of the PIDE (3.3), we can approximate this price using the development

where the zero-order term satisfies

The solution to the above PDE can be found via the Feynman-Kac formula, where the conditional expectation is computed in the log-normal LMM model with covariation matrix as in Section 4.1. Performing a measure change from to and denoting by the Black-Scholes price of a call option with variance ,

we see that the zero-order term is given by

| (4.27) |

where

| (4.28) |

Now, in complete analogy to the case of a general payoff, the first-order term and the second-order term are given by (4.1) and (4.1), respectively, with as in (4.27). Noting that depends only on , the derivatives of with respect to are zero and the sums in (4.1) and (4.1) in fact start from the index . An application of Proposition 4.1 and simplification (4.9) thus yields the following proposition, which provides an approximation of the caplet price when .

Proposition 4.5.

Remark 4.6.

Recalling that

we see that the functions and given by

for all and

for all , and , become in fact linear combinations of the terms which are polynomials in multiplied by derivatives of up to order three.

4.3. Approximate pricing of swaptions

Let us consider a swaption defined in Section 3.3. For swaption pricing we again use the general result under the terminal measure given in Proposition 4.4. The price of the swaption then satisfies

where the function satisfies the equation

with . We see that the zero-order term corresponds to the price of the swaption in the log-normal LMM model with volatility matrix .

The function related to the swaption price in the log-normal LMM is of course not known in explicit form but one can use various approximations developed in the literature [\citeauthoryearJäckel and RebonatoJäckel and Rebonato2003, \citeauthoryearSchoenmakersSchoenmakers2005]. To introduce the approximation of [\citeauthoryearJäckel and RebonatoJäckel and Rebonato2003], we compute the quadratic variation of the log swap rate expressed as function of Libor rates:

The approximation of [\citeauthoryearJäckel and RebonatoJäckel and Rebonato2003] consists in replacing all stochastic processes in the above integral by their values at time ; in other words, the swap rate becomes a log-normal random variable such that has variance

The function can then be approximated by applying the Black-Scholes formula:

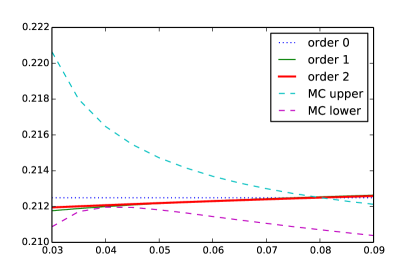

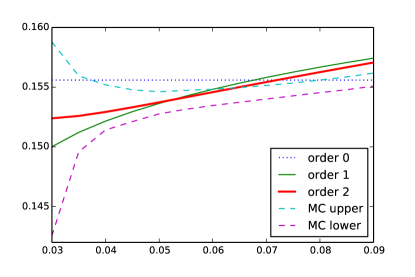

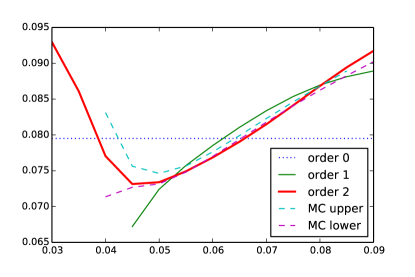

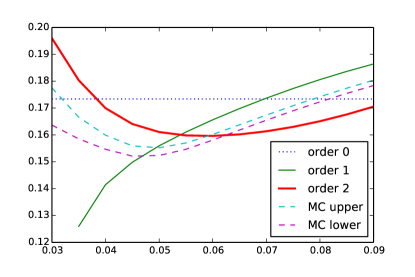

5. Numerical examples

In this section, we test the performance of our approximation at pricing caplets on Libor rates in the model (2.4), where is a unidimensional CGMY process [\citeauthoryearCarr, Geman, Madan, and YorCarr et al.2007]. The CGMY process is a pure jump process, so that , with Lévy measure

The jumps of this process are not bouded from below but the parameters we choose ensure that the probability of having a negative Libor rate value is negligible. We choose the time grid , , … , the volatility parameters , , the initial forward Libor rates , and the bond price for the first maturity . The CGMY model parameters are chosen according to four different cases described in the following table, which also gives the standard deviation and excess kurtosis of for each case. Case 1 corresponds to a Lévy process that is close to the Brownian motion ( close to and and large) and Case 4 is a Lévy process that is very far from Brownian motion.

Case Volatility Excess kurtosis 1 0.01 10 20 1.8 23.2% 0.028 2 0.1 10 20 1.2 17% 0.36 3 0.2 10 20 0.5 8.7% 3.97 4 0.2 3 5 0.2 18.9% 12.7

We first calculate the price of the ATM caplet with maturity written on the Libor rate with the zero-order, first-order and second-order approximation, using as benchmark the jump-adapted Euler scheme of \citeNkohatsu2010jump. The first Libor rate is chosen to maximize the nonlinear effects related to the drift of the Libor rates, since the first maturity is the farthest from the terminal date. The results are shown in Table 1. We see that for all four cases, the price computed by second-order approximation is within or at the boundary of the Monte Carlo confidence interval, which is itself quite narrow (computed with trajectories).

Secondly, we evaluate the prices of caplets with strikes ranging from to and explore the performance of our analytic approximation for estimating the caplet implied volatility smile. The results are shown in Figure 5.1. We see that in cases 1, 2 and 3, which correspond to the parameter values most relevant in practice given the value of the excess kurtosis, the second order approximation reproduces the volatility smile quite well (in case 1 there is actually no smile, see the scale on the axis of the graph). In case 4, which corresponds to very violent jumps and pronounced smile, the qualitative shape of the smile is correctly reproduced, but the actual values are often outside the Monte Carlo interval. This means that in this extreme case the model is too far from the Gaussian LMM for our approximation to be precise. We also note that the algorithm runs in , for the second order approximation, due to the number of partial derivatives that one has to calculate. The algorithm may therefore run slowly, should become too large.

| Case 1 | Case 2 | Case 3 | Case 4 | |

|---|---|---|---|---|

| Order 0 | 0.008684 | 0.006392 | 0.003281 | 0.007112 |

| Order 1 | 0.008677 | 0.006361 | 0.003241 | 0.006799 |

| Order 2 | 0.008677 | 0.006351 | 0.003172 | 0.006556 |

| MC lower bound | 0.008626 | 0.006306 | 0.003178 | 0.006493 |

| MC upper bound | 0.008712 | 0.006361 | 0.003204 | 0.006578 |

6. Acknowledgement

This research of Peter Tankov is partly supported by the Chair Financial Risks of the Risk Foundation sponsored by Société Générale.

References

- [\citeauthoryearBelomestny and SchoenmakersBelomestny and Schoenmakers2011] Belomestny, D. and J. Schoenmakers (2011). A jump-diffusion libor model and its robust calibration. Quantitative Finance 11(4), 529–546.

- [\citeauthoryearBenhamou, Gobet, and MiriBenhamou et al.2009] Benhamou, E., E. Gobet, and M. Miri (2009). Smart expansion and fast calibration for jump diffusions. Finance and Stochastics 13(4), 563–589.

- [\citeauthoryearBenhamou, Gobet, and MiriBenhamou et al.2010] Benhamou, E., E. Gobet, and M. Miri (2010). Time dependent heston model. SIAM Journal on Financial Mathematics 1(1), 289–325.

- [\citeauthoryearBrace, Ga̧tarek, and MusielaBrace et al.1997] Brace, A., D. Ga̧tarek, and M. Musiela (1997). The market model of interest rate dynamics. Mathematical Finance 7, 127–155.

- [\citeauthoryearCarr, Geman, Madan, and YorCarr et al.2007] Carr, P., H. Geman, D. B. Madan, and M. Yor (2007). Self-decomposability and option pricing. Mathematical Finance 17, 31–57.

- [\citeauthoryearČerný, Denkl, and KallsenČerný et al.2013] Černý, A., S. Denkl, and J. Kallsen (2013). Hedging in Lévy models and the time step equivalent of jumps. Preprint, arXiv:1309.7833.

- [\citeauthoryearDe FrancoDe Franco2012] De Franco, C. (2012). Two studies in risk management: portfolio insurance under risk measure constraint and quadratic hedge for jump processes. Ph. D. thesis, University Paris Diderot.

- [\citeauthoryearEberlein and KlugeEberlein and Kluge2007] Eberlein, E. and W. Kluge (2007). Calibration of Lévy term structure models. In M. Fu, R. A. Jarrow, J.-Y. Yen, and R. J. Elliott (Eds.), Advances in Mathematical Finance: In Honor of D. B. Madan, pp. 147–172. Birkhäuser.

- [\citeauthoryearEberlein and ÖzkanEberlein and Özkan2005] Eberlein, E. and F. Özkan (2005). The Lévy Libor model. Finance and Stochastics 9, 327–348.

- [\citeauthoryearJäckel and RebonatoJäckel and Rebonato2003] Jäckel, P. and R. Rebonato (2003). The link between caplet and swaption volatilities in a Brace-Gatarek-Musiela/Jamshidian framework: approximate solutions and empirical evidence. Journal of Computational Finance 6(4), 41–60.

- [\citeauthoryearKallsenKallsen2006] Kallsen, J. (2006). A didactic note on affine stochastic volatility models. In Y. Kabanov, R. Lipster, and J. Stoyanov (Eds.), From Stochastic Calculus to Mathematical Finance: The Shiryaev Festschrift, pp. 343–368. Springer.

- [\citeauthoryearKlugeKluge2005] Kluge, W. (2005). Time-Inhomogeneous Lévy Processes in Interest Rate and Credit Risk Models. Ph. D. thesis, University of Freiburg.

- [\citeauthoryearKohatsu-Higa and TankovKohatsu-Higa and Tankov2010] Kohatsu-Higa, A. and P. Tankov (2010). Jump-adapted discretization schemes for Lévy-driven sdes. Stochastic Processes and their Applications 120(11), 2258–2285.

- [\citeauthoryearMénassé and TankovMénassé and Tankov2015] Ménassé, C. and P. Tankov (2015). Asymptotic indifference pricing in exponential Lévy models. Preprint, arXiv:1502.03359.

- [\citeauthoryearMiltersen, Sandmann, and SondermannMiltersen et al.1997] Miltersen, K. R., K. Sandmann, and D. Sondermann (1997). Closed form solutions for term structure derivatives with log-normal interest rates. The Journal of Finance 52, 409–430.

- [\citeauthoryearPapapantoleon, Schoenmakers, and SkovmandPapapantoleon et al.2012] Papapantoleon, A., J. Schoenmakers, and D. Skovmand (2012). Efficient and accurate log-Lévy approximations to Lévy driven LIBOR models. Journal of Computational Finance 15(4), 3–44.

- [\citeauthoryearSandmann, Sondermann, and MiltersenSandmann et al.1995] Sandmann, K., D. Sondermann, and K. R. Miltersen (1995). Closed form term structure derivatives in a Heath–Jarrow–Morton model with log-normal annually compounded interest rates. In Proceedings of the Seventh Annual European Futures Research Symposium Bonn, pp. 145–165. Chicago Board of Trade.

- [\citeauthoryearSchoenmakersSchoenmakers2005] Schoenmakers, J. (2005). Robust Libor modelling and pricing of derivative products. CRC Press.