Palaiseau, France

claisse@cmap.polytechnique.fr 33institutetext: Gaoyue Guo 44institutetext: University of Oxford

Oxford, United Kingdom

guo.gaoyue@gmail.com 55institutetext: Pierre Henry-Labordère 66institutetext: Société Générale

Paris, France

pierre.henry-labordere@sgcib.com

Some Results on Skorokhod Embedding and Robust Hedging with Local Time

Abstract

In this paper, we provide some results on Skorokhod embedding with local time and its applications to the robust hedging problem in finance. First we investigate the robust hedging of options depending on the local time by using the recently introduced stochastic control approach, in order to identify the optimal hedging strategies, as well as the market models that realize the extremal no-arbitrage prices. As a by-product, the optimality of Vallois’ Skorokhod embeddings is recovered. In addition, under appropriate conditions, we derive a new solution to the two-marginal Skorokhod embedding as a generalization of the Vallois solution. It turns out from our analysis that one needs to relax the monotonicity assumption on the embedding functions in order to embed a larger class of marginal distributions. Finally, in a full-marginal setting where the stopping times given by Vallois are well-ordered, we construct a remarkable Markov martingale which provides a new example of fake Brownian motion.

Keywords:

Skorokhod embedding Model-free pricing Robust hedging Local time Fake Brownian motionMSC:

60G40 60G44 91G20 91G801 Introduction

The Skorokhod embedding problem (SEP for short) consists in choosing a stopping time in order to represent a given probability on the real line as the distribution of a stopped Brownian motion. First formulated and solved by Skorokhod skorokhod-61 , this problem has given rise to important literature and a large number of solutions have been provided. We refer the reader to the survey paper by Oblój obloj-04 for a detailed description of the known solutions. Among them, the solution provided by Vallois vallois-83 is based on the local time (at zero) of the Brownian motion. As proved later by Vallois vallois-92 , it has the property to maximize the expectation of any convex function of the local time among all solutions to the SEP. Similarly, many solutions to the SEP satisfy such an optimality property. This feature has given rise to important applications in finance as it allows to solve the so-called robust hedging problem which we describe below.

The classical pricing paradigm of contingent claims consists in postulating first a model, i.e., a risk-neutral measure, under which forward prices are required to be martingales according to the no-arbitrage framework. Then the price of any European derivative is obtained as the expectation of its discounted payoff under this measure. Additionally, the model may be required to be calibrated to the market prices of liquid options such as call options that are available for hedging the exotic derivative under consideration. This could lead to a wide range of prices when evaluated using different models calibrated to the same market data. To account for the model uncertainty, it is natural to consider simultaneously a family of (non-dominated) market models. Then the seller (resp. buyer) aims to construct a portfolio to super-replicate (resp. sub-replicate) the derivative under any market scenario by trading dynamically in the underlying assets and statically in a range of Vanilla options. This lead to an interval of no-arbitrage prices whose bounds are given by the minimal super-replication and the maximal sub-replication prices. The robust hedging problem is to compute these bounds as well as the corresponding trading strategies.

We consider the classical framework where all European call options having the same maturity as the exotic derivative are available for trading. As observed by Breeden and Litzenberger breeden-litzenberger-78 , the marginal distribution of the underlying price process at maturity is uniquely determined by the market prices of these call options. In this setting, the robust hedging problem is classically approached by means of the SEP. This approach relies on the fact that every continuous martingale can be considered as a time-changed Brownian motion. Thus, for payoffs invariant under time change, the problem can be formulated in terms of finding a solution to the SEP which optimizes the criterion given by the payoff. This approach was initiated by Hobson who considered the robust superhedging problem for lookback options in his seminal paper hobson-98 . Since then, the SEP has received substantial attention from the mathematical finance community and this approach was subsequently exploited in Brown, Hobson and Rogers brown-hobson-rogers-01-2 for barrier options, in Cox, Hobson and Oblój cox-hobson-obloj-08 for options on local time, in Cox and Oblój cox-obloj-11 for double-barrier options and in Cox and Wang cox-wang-13 for options on variance. One of the key steps in the SEP approach is to guess the form of the optimal hedging strategies from a well-chosen pathwise inequality.

Recently, a new approach to study the robust hedging problem was developed by Galichon, Henry-Labordère and Touzi galichon-henry-touzi-14 . It is based on a dual representation of the robust hedging problem, which can be addressed by means of the stochastic control theory. It appears that the stochastic control approach is remarkably devised to provide candidates for the optimal hedging strategies. Once postulated, the hedging inequality can be verified independently. This is illustrated by the study of Henry-Labordère et al. henry-al-15 , where they solve the robust hedging problem for lookback options when a finite number of marginals are known. To the best of our knowledge, it is the first paper to address the multi-marginal problem, at the exception of Brown, Hobson and Rogers brown-hobson-rogers-01-1 and Hobson and Neuberger hobson-neuberger-12 who considered the two-marginal case. In addition, it led to the first (nontrivial) solution of the multi-marginal SEP, which can be seen as a generalization of the Azéma-Yor solution, see Oblój and Spoida obloj-spoida-13 .

In this paper, we aim to collect a number of new results regarding Skorokhod embedding with local time and its applications. First we are concerned with the robust hedging problem for options written on the local time of the underlying price process. Such derivatives appear naturally in finance when considering payoffs depending on the portfolio value of an at-the-money call option delta hedged with the naive strategy holding one unit of the risky asset if in the money, else nothing, as expressed mathematically by Itô-Tanaka’s formula. By using the stochastic control approach, we first recover the results on the robust superhedging problem obtained by Cox, Hobson and Oblój cox-hobson-obloj-08 , i.e., we identify optimal superhedging strategies and the upperbound of the no-arbitrage interval. Then we derive the corresponding results for the robust subhedging problem. The last result is new to the literature.

In addition, we provide a new solution to the two-marginal SEP as a generalization of the Vallois solution. To this end, we have to make rather strong assumptions on the marginals that we aim to embed. However it is remarkable that these assumptions are to a certain extent necessary to derive a solution without relaxing the monotonicity assumption on the embedding functions. To the best of our knowledge, this is one of the first solution to the multi-marginal SEP to appear in the literature. In addition to the purely theoretical interest of this result, it is also a first step toward a solution to the robust hedging problem in the two-marginal setting, i.e., when the investor can trade on Vanilla option with an intermediate maturity.

Finally, we consider a special full-marginal setting when the stopping times given by Vallois are well-ordered. In the spirit of Madan and Yor madan-yor-02 , we construct a remarkable Markov martingale via the family of Vallois’ embeddings and compute its generator. In particular, it provides a new example of fake Brownian motion. From a financial viewpoint, our result characterizes the arbitrage-free model calibrated to the full implied volatility surface, which attains the upper bound of the no-arbitrage interval when the investor can trade in Vanilla options maturing at any time.

The paper is organized as follows. We briefly introduce in Section 2 the framework of robust hedging of exotic derivatives and its relation with the martingale optimal transport problem and the SEP. In Section 3, using the stochastic control approach, we provide explicit formulas for the bounds of the no-arbitrage interval and the optimal hedging strategies for the robust hedging problem. Then we introduce our new solution to the two-marginal SEP in Section 4. We illustrate this result by studying a numerical example. Finally, we consider in Section 5 the full-marginal setting and construct our new example of fake Brownian motion.

2 Formulation of the Robust Hedging Problem

2.1 Modeling the Model Uncertainty

We consider a financial market consisting of one risky asset, which may be traded at any time , where denotes some fixed maturity. We pursue a robust approach and do not specify the dynamics of the underlying price process. Namely, given an initial value , we introduce the set of continuous paths as the canonical space equipped with the uniform norm . Let be the canonical process and be the natural filtration, i.e., and . In this setting, stands for the underlying price process with initial value . In order to account for model uncertainty, we introduce the set of all probability measures on such that is a martingale. The restriction to martingale measures is motivated by the classical no-arbitrage framework in mathematical finance. For the sake of generality, we do not restrict to but consider the general case .

In addition, all call options with maturity are assumed to be available for trading. A model is said to be calibrated to the market if it satisfies for all , where denotes the market price of a call option with strike . For such a model, as observed by Breeden and Litzenberger breeden-litzenberger-78 , it follows by direct differentiation that

Hence the marginal distribution of is uniquely specified by the market prices. Let be the set of calibrated market models, i.e.,

Clearly, if and only if is centered at or, equivalently,

| and |

2.2 Semi-Static Hedging Portfolios

We denote by the collection of all predictable processes and, for every ,

A dynamic trading strategy is defined by a process , where corresponds to the number of shares of the underlying asset held by the investor at time . Under the self-financing condition, the portfolio value process of initial wealth induced by a dynamic trading strategy is given by 111 Both the quadratic variation and the stochastic integral depend a priori on the probability measure under consideration. However, under the Continuum Hypothesis, it follows by Nutz nutz-12 that they can be universally defined.

In addition to the dynamic trading on the underlying security, we assume that the investor can take static positions in call options for all strikes. Consequently, up to integrability, the European derivative defined by the payoff , which can be statically replicated by -call options in view of the celebrated Carr-Madan formula, has an unambiguous market price

The set of Vanilla payoffs which may be used by the trader has naturally the following form

A pair is called a semi-static hedging strategy, and induces the final value of the self-financing portfolio:

indicating that the investor has the possibility of buying at initial time any derivative with payoff for the price .

2.3 Robust Hedging and Martingale Optimal Transport

Given a derivative of payoff -measurable, we consider the corresponding problem of robust (semi-static) hedging. The investor can trade as discussed in the previous section. However we need to impose a further admissibility condition to rule out doubling strategies. Let (resp. ) consist of all processes whose induced portfolio value process is a supermartingale (resp. submartingale) for all . The robust superhedging and subhedging costs are then defined by

Selling at a price higher than — or buying it at a price lower than — the trader could set up a portfolio with a negative initial cost and a non-negative payoff under any market scenario leading to a strong (model-independent) arbitrage opportunity.

By taking expectation in the hedging inequalities under , we obtain the usual pricing–hedging inequalities:

| and |

where and are continuous-time martingale optimal transport problems. They consist in maximizing or minimizing the criterion defined by the payoff so as to transport the Dirac measure at to the given distribution by means of a continuous-time process restricted to be a martingale.

The study of martingale optimal transportation was recently initiated by Beiglböck, Henry-Labordère and Penkner beigblock-al-13 in discrete-time and by Galichon, Henry-Labordère and Touzi galichon-henry-touzi-14 in continuous-time. By analogy with the classical optimal transportation theory, one expects to establish a sort of Kantorovitch duality and to characterize the optimizers for both the primal and dual problems. The dual formulation has a natural financial interpretation in terms of robust hedging, which explains the keen interest of the mathematical finance community in martingale optimal transport. When the payoff is invariant under time-change, the SEP and the stochastic control approach turn out to be powerful tools to derive the duality and compute explicitly the optimizers as illustrated in this paper. For duality results with more general payoffs, we refer to the recent studies by Dolinsky and Soner dolinsky-soner-14 , Hou and Oblój hou-obloj-15 and Guo, Tan and Touzi guo-tan-touzi-15-2 .

2.4 Robust Hedging of Options on Local Time

In this paper, we focus on the robust hedging problem of options whose payoff is given by

where is the local time of at . Below, under appropriate conditions, we will exhibit the optimizers for both the robust hedging and the martingale optimal transport problems, and show further that there is no duality gap, i.e., and .

The payoff can be interpreted as a payoff depending on the portfolio value at maturity of an at-the-money call option delta hedged with the naive strategy holding one unit of the risky asset if in the money, else nothing, mathematically expressed by Itô-Tanaka’s formula: 222 In view of the pathwise construction of stochastic integrals in Nutz nutz-12 , Itô-Tanaka’s formula implies that the local time can also be universally defined.

Since the local time is invariant under time-change, 333 Namely, given a family of stopping times such that is continuous and increasing, we have where denote the local time at of the process . the martingale optimal transport problem can be formulated as an optimal stopping problem. Indeed, it follows (formally) from the Dambis-Dubins-Schwartz theorem that

| and | (1) |

where is the local time at zero of a Brownian motion and is the collection of solutions to the SEP, i.e., stopping times such that

| and |

See Galichon, Henry-Labordère and Touzi galichon-henry-touzi-14 and Guo, Tan and Touzi guo-tan-touzi-15 for more details. Here, the formulation (1) is directly searching for a solution to the SEP which maximizes or minimizes the criterion defined by the payoff.

It is well known that, if is a convex (or concave) function, the optimal solutions are of the form

for some monotone functions . This result was first obtained in Vallois vallois-92 , where he gives explicit constructions for the functions . It was then recovered by Cox, Hobson and Oblój cox-hobson-obloj-08 from a well-chosen pathwise inequality. More recently, it was derived by Beiglböck, Cox and Huesmann beiglboeck-cox-huesmann-13 as a consequence of their monotonicity principle, which characterizes optimal solutions to the SEP by means of their geometrical support. However, the explicit computation of is not provided by this approach. See also Guo, Tan and Touzi guo-tan-touzi-16 on the monotonicity principle.

3 Solution of the Robust Hedging Problem

Using the stochastic control approach, we reproduce in this section the results for the robust superhedging problem — optimizers and duality — obtained in Cox, Hobson and Oblój cox-hobson-obloj-08 . In addition, we provide the corresponding results for the robust subhedging problem. Throughout this section, we take for the sake of clarity and we work under the following assumption on the function and on the marginal . In particular, in contrast with cox-hobson-obloj-08 , we do not need to assume that is nondecreasing.

Assumption 3.1

is a Lipschitz convex function.

Assumption 3.2

is a centered probability distribution without mass at zero.

3.1 Robust Superhedging Problem

In this section, under Assumptions 3.1 and 3.2, we provide the optimal hedging strategy for as well as the optimal measure for and we show that there is no duality gap, i.e., . The key idea is that for any suitable pair of monotone functions , we may construct a super-replication strategy . The optimality then results from taking the pair of functions given by Vallois that embeds the distribution .

Assumption 3.3

(resp. ) is right-continuous and nondecreasing (resp. nonincreasing) such that and where, for all ,

Let us denote by the right-continuous inverses of . We also define the functions via by

| (2) | |||||

| (3) |

Throughout this paper, the derivatives under consideration are in the sense of distributions, and whenever possible, we pick a “nice” representative for such distribution. In particular, in the formula above, and stand for the right derivative of and the Lebesgue-Stieltjes measure relative to respectively, which are well-defined since is a convex function.

3.1.1 Quasi-Sure Inequality

We start by showing a quasi-sure inequality, which is a key step in our analysis. It implies that, in order to construct a super-replication strategy, it suffices to consider a pair satisfying Assumption 3.3. The duality and the optimality will follow once we find an optimal pair as it will be shown in the next section.

Remark 1

The derivation of the semi-static strategy is performed in Section 3.3 by means of the stochastic control approach.

Before giving the proof of Proposition 1, we show that the quasi-sure inequality yields an upper bound for .

Proof

In view of Proposition 1, it suffices to show that and . As proved in Lemma 1 below, the maps are bounded. In particular, is bounded and thus . In addition, is bounded and thus . It remains to prove that the local martingale is a supermartingale. The quasi-sure inequality (4) implies that for all ,

where . Denote and . Given a sequence of stopping times that reduces , it follows by Fatou’s Lemma that for all ,

| (7) |

In addition, clearly, is a non-negative submartingale and thus it holds

In particular, the sequence is uniformly integrable. Hence, it follows immediately from (7) that is a supermartingale. ∎

The rest of the section is devoted to the proof of Proposition 1. We start by establishing a technical lemma.

Lemma 1

With the notations of Proposition 1, the maps are uniformly bounded on and it holds for all ,

| (8) | |||||

| (9) |

Proof

(i) Let us start by proving (8). We observe first that

In addition, Fubini-Tonelli’s theorem yields that

The desired result follows immediately.

(ii) Let us show next that is bounded. Clearly,

In addition, we have

where the second line follows from (8). We deduce that . Similarly, it holds .

(iii) Let us turn now to the proof of (9). By change of variable, we get

In addition, integration by parts (see, e.g., Bogachev (bogachev-07, , Ex.5.8.112)) yields that

Using further , we obtain

| (10) |

Similarly, coincides with the r.h.s. above, which ends the proof. ∎

Proof (of Proposition 1)

Let us define by

(i) We start by proving that for all , . Clearly, the restriction of to (resp. ) is a convex function and we have

Thus, it holds

This yields that for all , . Similarly, we have

Using further (9), we conclude that for all , .

(ii) Let us show next that

Using successively Itô-Tanaka’s formula and the relation (8), we derive

We deduce that

The desired result follows immediately by using (10).

(iii) We conclude the proof as follows:

where the first inequality comes from Part (i) above. ∎

3.1.2 Optimality and Duality

In view of Corollary 1, the duality is achieved once we find a suitable pair such that the corresponding static strategy satisfies the relation . In this section, we use Vallois’ solution to the SEP to construct such a pair and to provide optimizers for both and .

We start by stating a proposition due to Vallois, which provides a solution to the SEP based on the local time. Recall that and denote a Brownian motion and its local time at zero respectively.

Proposition 2

Proof

We refer to Vallois vallois-83 or Cox, Hobson and Oblój cox-hobson-obloj-08 for a proof. ∎

Remark 3

If admits a positive density w.r.t. the Lebesgue measure, it holds

If we assume further that is symmetric, then and

where denotes the inverse of .

The following theorem, which is the main result of this section, shows that the pair given by Vallois yields the duality and the optimizers for both and .

Theorem 3.1

Proof

(i) We start by constructing a candidate for the optimizer . Denote by the law of the process given by

The process clearly is a continuous martingale w.r.t. its natural filtration such that . In other words, the probability measure belongs to .

(ii) Let us turn now to the proof of (11). We define by

where is given by (2)–(3) with . Since the local time is invariant under time-change, we have

Notice that in view of Assumption 3.2. Thus, using (9) for the case , it holds

Further, Part (ii) of the proof of Proposition 1 ensures that

Notice that the pair satisfies Assumption 3.3 in view of Proposition 2.

Lemma 2

With the notations of Theorem 3.1, it holds

Proof

This result is a slight extension of Lemma 2.1 in Cox, Hobson and Oblój cox-hobson-obloj-08 . The proof relies on similar arguments, which we repeat here for the sake of completeness. Using the invariance of the local time under time-change, we observe first that the desired result is equivalent to

For the sake of clarity, we omit the index in the notations and we denote instead of in the rest of the proof. Let , , and . We also denote

From Itô-Tanaka’s formula, it follows that

We deduce that the stopped local martingale is bounded. Hence, it is a uniformly integrable martingale and we have

where the last equality follows from . It yields that

By the monotone convergence theorem, as tends to infinity, we obtain

Then, as tends to infinity, the l.h.s. converges, again by the monotone convergence theorem, to

As for the r.h.s., using the fact that are bounded and are uniformly integrable, it converges to

Hence, we obtain

where both sides are finite. This ends the proof. ∎

3.2 Robust Subhedging Problem

In this section, we address the robust subhedging problem. Namely, we derive the lower bound to the no-arbitrage interval and the corresponding optimal subhedging strategy. These results are new to the literature. The idea is to proceed along the lines of Section 3.1, but to reverse the monotonicity assumption on the functions and .

Assumption 3.4

(resp. ) is right-continuous and nonincreasing (resp. nondecreasing).

As in Section 2.3, we denote by the right-continuous inverses of and

We also define the new functions via by

| (12) |

3.2.1 Quasi-Sure Inequality

We start by showing the quasi-sure inequality corresponding to the subhedging problem. Together with the second solution provided by Vallois to the SEP, it leads to the solution of the robust subhedging problem.

Proposition 3

The proof of Corollary 2 is identical to the proof of Corollary 1. However, the proof of the quasi-sure inequality (13) is not completely straightforward and thus we provide some details below.

Proof (of Proposition 3)

Let us show first that once again we have

The first identity follows from Fubini-Tonelli’s theorem as was (8) in Lemma 1. As for the second one, by change of variables and integration by parts, we have

Using further , we obtain

Similarly, we can show that coincides with the r.h.s. above. The rest of the proof follows by repeating the arguments of Proposition 1 using the fact that the restriction of to (resp. ) is now concave. ∎

3.2.2 Optimality and Duality

Using another solution to the SEP provided by Vallois, we derive the duality and provide optimizers for both and .

Proposition 4

Proof

We refer to Vallois vallois-92 for a proof. ∎

Theorem 3.2

The proof of this result is identical to the proof of Theorem 3.1.

Remark 4

The assumption that has no mass at zero can be dropped in Theorem 3.2. In this case, can reach zero and we can assume w.l.o.g. that . Then we need to modify slightly the definitions of by replacing the upper bound in the integral term by .

3.3 On the Stochastic Control Approach

As already mentioned, the results of Section 3.1 can be found in Cox, Hobson and Oblój cox-hobson-obloj-08 . The actual novelty here comes from our approach which is based on the stochastic control theory. In this section, we give some insights on the arguments that led us to consider the quasi-sure inequality (4).

We start by observing that

Further, the Dambis-Dubins-Schwarz theorem implies (formally) that

where is the collection of stopping times such that is a uniformly integrable martingale. Inspired by Galichon, Henry-Labordère and Touzi galichon-henry-touzi-14 , we study the problem on the r.h.s. above as it turns out to be equivalent to the robust superhedging problem.

For any , we consider the optimal stopping problem

where denotes the conditional expectation operator . Using the formal representation where denotes the Dirac delta function, the Hamilton-Jacobi-Bellman (HJB for short) equation corresponding to this optimal stopping problem reads formally as

| (17) |

We look for a solution of the form

where with satisfying Assumption 3.3. For the sake of simplicity, we assume that are strictly monotone such that and and that all the functions involved are smooth enough to allow the calculation sketched below. Differentiating twice w.r.t. to creates a delta function which cancels out the delta function appearing in the term provided that . Then we impose the continuity and the smooth fit conditions at the boundary :

| and |

We deduce that

In addition, the function has to satisfy the following system of ODEs:

This system of ODE can be solved explicitly and it characterizes as in (2) up to a constant such that

Thus is given by (6) if we pick . Conversely, provided that is convex, is also convex on (resp. ). It follows that satisfies the variational inequality (17) in view of Part (i) of the proof of Proposition 1. Further, we observe that another solution of (17) is given by

Then, given any solution to the variational PDE (17), it is straightforward to derive heuristically a quasi-sure inequality. Indeed, using the formal representation , Itô’s formula yields for all ,

In particular, if coincides with , we recover the quasi-sure inequality (4). Further, if we denote by the distribution of where

we obtain

4 Two-Marginal Skorokhod Embedding Problem

In this section, we provide a new solution to the two-marginal SEP as an extension of the Vallois embedding. Let be a centered peacock, i.e., and are centered probability distributions such that for all convex. We aim to construct a pair of stopping rules based on the local time such that , , and is uniformly integrable. A natural idea is to take the Vallois embeddings corresponding to and . However these stopping times are not ordered in general and thus we need to be more careful. For technical reasons, we make the following assumption on the marginals.

Assumption 4.1

is a centered peacock such that and are symmetric and equivalent to the Lebesgue measure.

4.1 Construction

For the first stopping time, we take the solution given by Vallois vallois-83 that embeds , i.e.,

where is the inverse of

| (18) |

For the second stopping time, we look for an increasing function such that

Notice that by definition. In particular, if on a non-empty interval, it can happen that for some . As before, is defined through its inverse . Let us denote

Then we set

| (19) |

To ensure that , we need to assume that on a neighborhood of zero. If , the construction is over. This corresponds to the case when the Vallois embeddings are well-ordered. Otherwise, we proceed by induction as follows:

(i) if , we denote

Then we set for all ,

| (20) |

(ii) if , we denote

Then we set for all ,

| (21) |

To ensure that is well-defined and increasing, we need to make the following assumption. In particular, the point (iii) below ensures that and .

Assumption 4.2

(i) and on a neighborhood of zero;

(ii) whenever ;

(iii) for some .

Theorem 4.1

The proof of this result will be performed in the next section. Notice already that both points (i) and (ii) of Assumption 4.2 are to a certain extent necessary conditions to ensure the existence of an increasing function that solves the two-marginal SEP as above. See Remark 5 below for more details. This suggests that one needs to relax the monotonicity assumption on in order to iterate the Vallois embedding for a larger class of marginals. However, our approach does not allow to compute the function in this general setting.

4.2 Proof of Theorem 4.1

Let us start by a technical lemma which is a key step in the proofs of Theorem 4.1 and Theorem 5.1 below.

Lemma 3

Let be given as in Assumption 3.3 and denote

For any bounded such that is of bounded variation, it holds for all , ,

where denotes the conditional expectation operator and

Proof

Let be the process given by

By applying Itô-Tanaka’s formula and using further

we deduce that

Hence, the process is a local martingale. Further, the stopped process is bounded since and . It follows that

To conclude, it remains to see that by definition. ∎

We are now in a position to complete the proof of Theorem 4.1. For the sake of clarity, we omit the index in the notations and we split the proof in three steps.

First step. We start by showing that the distribution of admits a density w.r.t. the Lebesgue measure. Let us assume here that the function is increasing and satisfies and where . This will be proved in Step 3 below. Notice first that the distribution of is symmetric by construction. By the strong Markov property and Lemma 3, if we take the function for some , it holds

where

By a straightforward calculation, we get

Hence, we obtain

We deduce by direct differentiation of the identity above that the distribution of admits a density w.r.t. the Lebesgue measure given by

| (22) |

where

Second step. Let us show now that coincides with when is defined as (19)–(21). Notice first that the relation (18) yields that

Using further the identities (20) and (21), it follows that

where we denote and

To conclude, it remains to show that for all and for all . As a by-product, this proves that

| (23) |

and thus is well-defined. For , it follows from the relation (19) that

Assume that for all . It results from the relation (20) that

Hence, we deduce that for all ,

Further, it results from the relation (21) that

Hence, we deduce that for all ,

Third step. We are now in a position to complete the proof. The relation (21) clearly imposes that is increasing on every interval such that . Under Assumption 4.2 (ii), the relation (20) together with (23) ensures that is increasing on every interval such that . In addition, it follows immediately from (19) that . Further, in view of Assumption 4.1 (iii), one easily checks by a straightforward calculation that . It remains to prove that the stopped process is uniformly integrable. Since for all , the uniform integrability follows immediately from the assumption that admits a finite first moment. ∎

Remark 5

The first step of the proof does not rely on the specific form of the increasing function . For this reason, the relation (22) sheds new light on Assumption 4.2. For instance, if near zero, then we see that near zero. Else near zero. Thus, one cannot expect to solve the two-marginal SEP as above, if and on a neighborhood of zero. In addition, since by construction, we deduce that is increasing if and only if whenever .

4.3 A Numerical Example

As an example, we consider the pair of symmetric densities given by

where is a parameter satisfying . The corresponding embedding maps and are given by

| and |

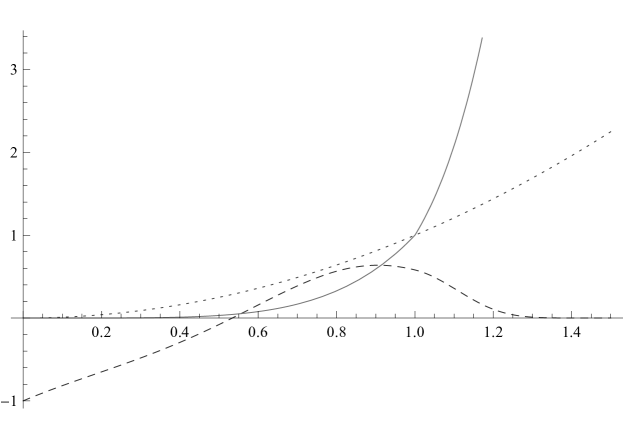

All the assumptions in Theorem 4.1 are satisfied as can be seen in Figure 1.

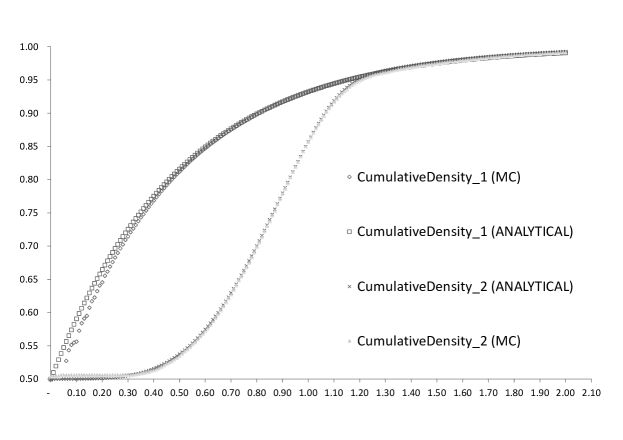

In Figure 2, we provide a comparison of the analytical cumulative distributions of and with their Monte-Carlo estimations using paths. We find a very good match except on a neighborhood of zero. Note that the simulation of and are quite difficult as we need to simulate the local time of a Brownian motion, which is a highly irregular object. We have chosen to simulate the local time at a time step using

with and . Since the derivatives of and are infinite at zero, the accuracy of our Monte Carlo estimations near zero depends strongly on the discretization of the local time, which explains the small mismatch in Figure 2.

5 A Remarkable Markov Martingale with Full Marginals

In this section, we exhibit a remarkable Markov martingale under the assumption that all the marginals of the process are known. In particular, it provides a new example of fake Brownian motion.

5.1 Infinitesimal Generator

We consider that all the marginals of the process are known. For the sake of simplicity, we assume that is symmetric and equivalent to the Lebesgue measure for every . Denote by (resp. ) the stopping time (resp. the map) given by Vallois vallois-83 that embed the distribution .

Assumption 5.1

For all , , or equivalently, .

The next result gives the generator of the Markov process . It is analogous to the study of Madan and Yor madan-yor-02 with the Azéma-Yor solution to the SEP. In particular, the process is a pure jump process, which corresponds to an example of local Lévy model introduced in Carr et al. carr-al-04 .

Theorem 5.1

Proof

The process is clearly an inhomogeneous Markov martingale, see Madan and Yor madan-yor-02 for more details. It remains to compute the generator. For each , we denote

Then it follows from Lemma 3 that

with

By definition, the generator is given by, for all ,

Differentiating the relation w.r.t. , we obtain

Using the formula above, a straightforward calculation yields that for all ,

Similarly, it holds for all ,

Hence, we obtain

The desired result follows by using further

5.2 Fake Brownian Motion

As an application, we provide a new example of fake Brownian motion. If is a continuous Gaussian peacock, i.e.,

it satisfies Assumption 5.1 in view of Lemma 4 below. Then the process is a fake Brownian motion, i.e., a Markov martingale with the same marginal distributions as a Brownian motion that is not a Brownian motion.

Lemma 4

If is a continuous Gaussian peacock, then the map is decreasing for all .

Proof

For the sake of clarity, we denote in this proof. By integration by parts, it holds for all ,

Further, by change of variable, we have . To conclude, it is clearly enough to prove that the map is increasing for all and . By direct differentiation, we see that its derivative has the same sign as

It remains to observe that the quantity above is positive since

6 Conclusions

This paper makes contribution on several topics related to the Vallois embedding and its applications. In particular, we provide a complete study of the robust hedging problem for options on local time in the one-marginal case by using the stochastic control approach. In addition, we derive a new solution to the two-marginal Skorokhod embedding when the marginal distributions are symmetric. Under appropriate assumptions, we compute the corresponding monotone embedding functions. A natural direction for future research is to relax the monotonicity assumption in order to embed more marginals. Besides it would be of interest to iterate the stochastic control approach to deal with the multi-marginal robust hedging problem in the spirit of Henry-Labordère et al. henry-al-15 . However the problem is less tractable than one might hope and we have not yet been able to provide a complete solution.

Acknowledgements.

Julien Claisse is grateful to the financial support of ERC Advanced Grant 321111 ROFIRM.References

- (1) A. V. Skorohod, Issledovaniya po teorii sluchainykh protsessov (Stokhasticheskie differentsialnye uravneniya i predelnye teoremy dlya protsessov Markova). Izdat. Kiev. Univ., Kiev, 1961.

- (2) J. Oblój, “The skorokhod embedding problem and its offspring,” Probab. Surveys, vol. 1, pp. 321–392, 2004.

- (3) P. Vallois, “Le problème de Skorokhod sur : une approche avec le temps local,” in Seminar on probability, XVII, vol. 986 of Lecture Notes in Math., pp. 227–239, Springer, Berlin, 1983.

- (4) P. Vallois, “Quelques inégalités avec le temps local en zero du mouvement brownien,” Stochastic Process. Appl., vol. 41, no. 1, pp. 117–155, 1992.

- (5) D. T. Breeden and R. H. Litzenberger, “Prices of State-contingent Claims Implicit in Option Prices,” The Journal of Business, vol. 51, no. 4, pp. 621–51, 1978.

- (6) D. G. Hobson, “Robust hedging of the lookback option,” Finance and Stochastics, vol. 2, no. 4, pp. 329–347, 1998.

- (7) H. Brown, D. Hobson, and L. C. G. Rogers, “Robust hedging of barrier options,” Math. Finance, vol. 11, no. 3, pp. 285–314, 2001.

- (8) A. M. G. Cox, D. Hobson, and J. Oblój, “Pathwise inequalities for local time: applications to Skorokhod embeddings and optimal stopping,” Ann. Appl. Probab., vol. 18, no. 5, pp. 1870–1896, 2008.

- (9) A. M. G. Cox and J. Oblój, “Robust pricing and hedging of double no-touch options,” Finance Stoch., vol. 15, no. 3, pp. 573–605, 2011.

- (10) A. M. G. Cox and J. Wang, “Root’s barrier: construction, optimality and applications to variance options,” Ann. Appl. Probab., vol. 23, no. 3, pp. 859–894, 2013.

- (11) A. Galichon, P. Henry-Labordère, and N. Touzi, “A stochastic control approach to no-arbitrage bounds given marginals, with an application to lookback options,” Ann. Appl. Probab., vol. 24, no. 1, pp. 312–336, 2014.

- (12) P. Henry-Labordere, J. Oblój, P. Spoida, and N. Touzi, “The maximum maximum of a martingale with given n marginals,” Ann. Appl. Probab., 2015.

- (13) H. Brown, D. Hobson, and L. C. G. Rogers, “The maximum maximum of a martingale constrained by an intermediate law,” Probab. Theory Related Fields, vol. 119, no. 4, pp. 558–578, 2001.

- (14) D. Hobson and A. Neuberger, “Robust bounds for forward start options,” Math. Finance, vol. 22, no. 1, pp. 31–56, 2012.

- (15) J. Oblój and P. Spoida, “An Iterated Azéma-Yor Type Embedding for Finitely Many Marginals,” ArXiv e-prints, 2013.

- (16) D. B. Madan and M. Yor, “Making Markov martingales meet marginals: with explicit constructions,” Bernoulli, vol. 8, no. 4, pp. 509–536, 2002.

- (17) M. Nutz, “Pathwise construction of stochastic integrals,” Electron. Commun. Probab., vol. 17, pp. no. 24, 7, 2012.

- (18) M. Beiglböck, P. Henry-Labordère, and F. Penkner, “Model-independent bounds for option prices—a mass transport approach,” Finance Stoch., vol. 17, no. 3, pp. 477–501, 2013.

- (19) Y. Dolinsky and H. M. Soner, “Martingale optimal transport and robust hedging in continuous time,” Probab. Theory Related Fields, vol. 160, no. 1-2, pp. 391–427, 2014.

- (20) Z. Hou and J. Oblój, “On robust pricing-hedging duality in continuous time,” ArXiv e-prints, 2015.

- (21) G. Guo, X. Tan, and N. Touzi, “Tightness and duality of martingale transport on the Skorokhod space,” ArXiv e-prints, 2015.

- (22) G. Guo, X. Tan, and N. Touzi, “Optimal Skorokhod Embedding Under Finitely Many Marginal Constraints,” SIAM J. Control Optim., vol. 54, no. 4, pp. 2174–2201, 2016.

- (23) M. Beiglboeck, A. M. G. Cox, and M. Huesmann, “Optimal Transport and Skorokhod Embedding,” ArXiv e-prints, July 2013.

- (24) G. Guo, X. Tan, and N. Touzi, “On the Monotonicity Principle of Optimal Skorokhod Embedding Problem,” SIAM J. Control Optim., vol. 54, no. 5, pp. 2478–2489, 2016.

- (25) V. I. Bogachev, Measure theory. Vol. I, II. Springer-Verlag, Berlin, 2007.

- (26) P. Carr, H. Geman, D. B. Madan, and M. Yor, “From local volatility to local Lévy models,” Quant. Finance, vol. 4, no. 5, pp. 581–588, 2004.