Embarrassingly Parallel Time Series Analysis for

Large Scale Weak Memory Systems

Abstract

Second order stationary models in time series analysis are based on the analysis of essential statistics whose computations follow a common pattern. In particular, with a map-reduce nomenclature, most of these operations can be modeled as mapping a kernel that only depends on short windows of consecutive data and reducing the results produced by each computation. This computational pattern stems from the ergodicity of the model under consideration and is often referred to as weak or short memory when it comes to data indexed with respect to time. In the following we will show how studying weak memory systems can be done in a scalable manner thanks to a framework relying on specifically designed overlapping distributed data structures that enable fragmentation and replication of the data across many machines as well as parallelism in computations. This scheme has been implemented for Apache Spark but is certainly not system specific. Indeed we prove it is also adapted to leveraging high bandwidth fragmented memory blocks on GPUs.

Introduction

Classic time series analysis and in particular that of second order

stationary processes has been widely studied for several decades and

reached a peak of popularity in the years 1980-1990 when computational

power became more common and allowed for practical implementation

of varied data sets. Monographs such as [1],

[2] and [3] offered

the opportunity for many researchers to better understand the intricacies

of time series analysis. The topics of univariate and monovariate

time series analysis were also well covered in [4, 5]

and many other publications. Software such as R or Matlab has given

the opportunity to many practitioners to examine data, enabling even

more applications of time series analysis and contributing to the

interest in that field. The amount of research dedicated to time series

analysis has been so important in the past decades that we do not

claim here to review it holistically. However, it is necessary to

contextualize the topic of the present article both in its theoretical

aspects and its practical implementation.

The development of distributed programming paradigms [6],

file systems [7], databases [8]

and in-memory computing engines [9]

for the modern commodity datacenter environment has led

us to consider new applications and implementations for time series

analysis. As opposed to small dataset applications such as those developed

in quantitative finance [10], climate studies

[11], network traffic analysis [12],

hydrology [13], we are now interested in analyzing

observations at scale in a data intensive environment such as [14]

with a standardized distributed library similar to MLlib [15].

This creates new challenges. In particular, we are dealing with data

sitting on a distributed cluster of machines whose memory layout has

an obvious bandwidth bottleneck when it comes to shuffling data across

an Ethernet network. This also creates new opportunities. Time series

estimation can now leverage recent theoretical developments

[16] as well as improvements in convex optimization

techniques [17, 18] that can

help get likelihood maximization based estimators faster.

In this new programming framework, we will start adapting the implementation

of the simplest class of models: linear time series models. These are the stochastic

counterparts of deterministic linear systems [19].

Estimating auto-regressive and moving average models (weak memory

models) will be the main focus of this document. More advanced topics

such as the identification of non linear dynamics [20, 21]

as well heteroscedastic systems [22] will

be the subject of subsequent work.

This document focuses on the presentation of a new data structure

dedicated to the representation of estimation-ready data sets for

time series analysis. As opposed to other frameworks such as SparkTS,

spark-timeseries or Thunder, the data is partitioned here with respect

to time. An overlapping block distributed data structure has been

devised which, given an appropriate padding expressed in units of

time, enables the computation of M and Z estimators for second order

stationary models in an embarrassingly parallel manner. This enables

in particular the calibration of multivariate time series models without

shuffling observations on a distributed in-memory computing engine.

Part I Theoretical background on time series analysis, estimators, motivation

Our intent is to provide a generic programming framework for scalable time series analysis in a distributed system. In the following, we review popular time series models that should be supported by the framework and establish the corresponding computational operations the related estimators require. Focus is set on second order stationary models and the the well known ARMA family.

1 Second order stationary time series

We start with the most common time series models. These are models in which observation are regularly spaced and for which there are no missing values. Practitioners of time series analysis are familiar with missing data, outliers and irregularly spaced timestamps. In such cases, an interpolation technique (linear interpolation or last-observation-carried-forward for instance) is often used in order to align observations on a regular time index grid. We focus on time series where each observation belongs in .

1.1 Second order stationarity

Second order stationary processes are common in time series analysis. Models in this family are simple, practical to estimate and yet have strong predictive power for a vast range of data sets related to economics, finance, industrial systems, data center monitoring and the climate.

Definition: Second order stationary time series

A time series is second order stationary if there exists an auto-covariance function so that for any value of ,

White noise is an example of second order stationary time series where the auto-covariance function is 0 everywhere except for .

Definition: lag operator

Let the operator such that .

1.2 Constant volatility linear time series models

A first family of models is concerned with modeling observations as the output of a linear system with constant variance perturbations.

Definition: multidimensional white noise

A process in is a multidimensional white noise if

and

In the following we assume white noise processes are always non-degenerate, i.e., we always have definite positive.

Definition: Auto-regressive models (AR)

A (centered) multivariate order auto-regressive time series is defined by matrices and a white noise process in with variance such that, for any value of in ,

This equation can be rewritten in reduced form with the lag operator. Let be the companion polynomial of the equation. A short hand for the AR equation above is

Equivalently, a Linear Time Invariant (LTI) system formulation of these equations is:

In the following we will mostly use the first AR formulation as the LTI formulation has a degenerate noise structure (the noise covariance matrix is not full rank).

Definition: Moving average models (MA)

A (centered) multivariate order moving average time series is defined by matrices and a white noise process in with variance such that, for any value of in ,

Letting the companion polynomial of the equation. A short hand for the MA equation above is

Definition: Auto-regressive moving average models (ARMA)

A (centered) multivariate order , auto-regressive moving average time series is defined by matrices and matrices and a white noise process in with variance such that, for any value of in ,

Such a model corresponds to a perturbed LTI system whose perturbations

are auto-correlated.

Letting and

the companion polynomials of the equation. A short hand for the ARMA

equation above is

1.3 Identification, causality and invertibility

In the following, we will consider the conditions that guarantee stability of the model and the fact that the equations above have one and only solution.

1.3.1 Causal models:

If i.e. if the matrix

has its spectrum strictly bounded in absolute value by , the ARMA

equation has one and only stationary solution. This solution is said

to be causal. Such an ARMA equation can be interpreted as equivalent

to a stable LTI which is perturbed by auto-correlated noise.

In the following we will only consider causal models.

1.3.2 Invertible models:

If i.e. if the matrix

has its spectrum strictly bounded in absolute value by , for a stationary solution to the ARMA equations there exists a unique white noise process such that .

1.4 Integrated processes and differentiation

Definition: differentiated time series

For any time series one may

define its differentiated counterpart as .

In the case of actual and finite length data, we opt for the convention:

.

Definition: integrated processes

Formally, a time series is

said to be integrated of order if

is not second order stationary whenever and

is second order stationary.

Brownian motions are famous examples of order integrated processes

(there difference process is a white noise).

2 Estimators of sufficient statistics of second order stationary time series

In the following we review known estimators for multivariate time series in order to highlight the similarity of their computational structure. We are concerned with a theoretical process and have consecutive observations.

2.1 Estimators of interest

The following section goes through all the sufficient statistics to estimate a second order stationary process. In particular, it is noteworthy that the causal solution to an ARMA equation has a covariance structure that is entirely determined by the parameters of the equation [2] (that is , and ).

2.1.1 Mean

A consistent unbiased estimator for the mean of a second order time series is

This estimator is asymptotically normal with variance decaying with

rate.

In the following we assume that the mean has been estimated and accounted for

and is therefore centered.

2.1.2 Auto-covariance

A consistent unbiased estimator for the auto-covariance matrix at lag for a centered second order stationary time series is

This estimator is asymptotically normal with variance decaying with rate.

2.1.3 Auto-correlogram

Definition: auto-correlogram of a second order stationary time series

Let , order auto-correlation is

Auto-correlation estimator:

The estimator

is asymptotically convergent, it is in fact asymptotically normal with variance decaying with rate.

Definition: partial auto-correlogram of a second order stationary time series

Let the span of the random variables and the corresponding orthogonal projection. Let be defined by

is the partial auto-correlation matrix of order , we will denote it .

Property: from auto-correlation to partial auto-correlation

The projection matrices above solve the following linear system of equations:

Proof:

is an orthogonal projector therefore for any ,

Therefore,

Partial auto-correlation estimator:

An estimator can be obtained by inverting the linear system above where the actual auto-covariance is replaced by :

It is asymptotically unbiased and asymptotically normal with variance decaying with a rate.

3 AR, MA, ARMA fitting by frequentist methods

In the following we assume is a centered second order stationary process.

3.1 Determining the order of an AR, MA or ARMA model by frequentist methods

It is possible to choose an appropriate value of when estimating

an AR model simply by computing the partial auto-correlation of the

process. As soon as the partial auto-correlation at lag is not

significantly different from , an appropriate choice for

is . Indeed, for an AR model of order , partial auto-correlation

cancels out as soon as .

Similarly, if one considers a MA model of order , the auto-correlation

function is zero whenever . Therefore,

value of after which the auto-correlation function is no longer

significantly different from zero yields an indicator of the value

of one should choose prior to estimating the model.

For ARMA models, the analysis is more involved but only relies on

estimates of auto-covariance as well. In this case, it is more common

in practice to choose cutoff values for and based on a Bayesian

information criterion (AIC or BIC).

3.2 AR estimation based on Yule-Walker equations:

Assuming

the Yule-Walker equations give

or equivalently

Solving this block Toeplitz linear system with the auto-covariance estimators given above then yields the least square estimates of . Right multiplying the equation above by and computing the expectation gives an estimate of the diagonal variance matrix of the noise process:

The interesting point here, from a computational standpoint, is the

fact that auto-covariance estimates for are sufficient

to obtain estimates for the parameters of the model. In the univariate

case this comes down to inverting a Toeplitz matrix and is practically

achieved thanks to the well known Durbin-Levinson algorithm [2]

with time complexity.

The multivariate case is more in-line with the kind of large scale

analytics programming paradigm we discuss here. Indeed, what is key

to the present approach is to be able to fit AR models not specifically

with a large order but more with a large number of dimensions

. One is therefore interested in solving such a system with large

Toeplitz blocks (dimension ) and small order in comparison .

Akaike offered a recursive method to solve such a system with

extra space and in [23].

3.2.1 Issues when becomes very large:

The fact that, in this algorithm one has to invert matrices of size becomes problematic whenever becomes large ( or more). The time complexity of the block Toeplitz inversion procedure of Akaike is cubic with respect to which means practically that even on modern GPUs capable of 1 TFLOPs, it would generally take at least days to invert a row square matrix. Therefore we show how to conduct multivariate analysis when is high and the system under study features spatial stationarity thanks to a Bayesian approach.

3.3 MA estimation based on the innovation algorithm:

We want to estimate a model of the form

Let us assume that their exist such that for for any .

The sequence is a set of orthogonal vectors obtained by a Gram-Schmidt orthonormalization procedure. Indeed, it corresponds to the series of innovations of the time series. This implies, by orthogonality and decomposition on the Gram-Schmidt basis,

where is the variance matrix of the corresponding innovation process (perturbations to the linear model). is orthogonal to therefore

Substituting by we get

And, therefore,

Substituting by gives

and finally substituting by yields

Finally, Pythagora’s theorem for orthogonal projections implies that

Based on the estimates of given by the averaging procedure above, a recursive procedure, starting by yields consistent estimates for and . In the case of an order MA model, and therefore the we get the estimates of the parameters of the model. The complexity of the algorithm here is .

Recursive procedure:

One starts with and then for computes

and

3.4 ARMA model estimation:

We are now concerned with estimating the parameters of

We assume in the following that the model is causal. This implies in particular the existence of matrices such that . As is a white noise process, necessarily

where, by convention, whenever and whenever . By construction, can be estimated thanks to the innovation estimates provided by the innovation algorithm above. Then one has

As by convention, , necessarily, the estimates solve the following linear system:

Once this block Toeplitz system has been solved, the estimates can be determined thanks to

An estimate of the diagonal noise variance matrix is given by

The complexity of the algorithm is .

4 Predictions with linear time series models

Linear models for time series, however often very simplistic, offer linear predictors for the next events to occur given a series of previous observations. Linear predictors are simple to set up and offer good guarantees on the results they provide in the form of confidence intervals. This principle can also be extended to that of featurized predictions with a linear model that feeds on non-linear features. Predictions leverage parallelism with respect to process dimensions straightforwardly and are computed in an iterative fashion with respect to time. There is no contribution here in that regard except in that we highlight that predictions in the general case an ARMA process only depend on short range previously observed values and therefore prove corresponding computations feature weak memory.

4.1 Predictions in the AR case

The auto-regressive family of models is the simplest, the one step ahead predictor of , that will be denoted is trivially

and predictions more than one step ahead are obtained in a recursive fashion by re-injecting shorter range projections into the linear system above. The variance of predictions can then be computed based on (see [5] for details).

4.2 Predictions in the ARMA case

Moving average components introduce a supplementary difficulty in

predicting values based on passed observations. The aim of this section

is to show that predictions can be evaluated based on a recursive

procedure which, at each step, only considers previously observed

values on a short range.

In order to forecast an ARMA process one runs the innovation algorithms

on the observations so as to obtain an estimate of the innovations.

There exists a series of projection matrices

such that

Therefore, at each time-step , provided the innovation projection matrices have been computed (which has been done iteratively from to ), only observations and forecasts need to be taken into account. This algorithm can be run in a streaming fashion. This algorithm can be run in an approximate parallel manner in the case of stable models in which the importance of initialization errors decays exponentially.

5 AR, MA, ARMA estimation by Bayesian methods

Let us first focus on the estimation of AR models by Bayesian methods and prove they rely on weak memory computations.

5.1 Bayesian estimation of AR models

At each time-step one considers an equation of the form

We assume the errors have a parametric distribution where is a set of parameters in (which we assume is convex), is a function from onto and is a function from onto . We further assume that is log-strongly-concave with respect to its first argument. One will typically consider a centered Gaussian distribution for the white noise with variance . In other words

5.1.1 Iterative maximum conditional likelihood based estimation

In this section, one assumes we are given a series of samples where . We want to optimize the likelihood of samples considering that the first observations are not perturbed . The likelihood function decomposes as follows:

The log-likelihood is therefore

Our aim here is to find and so as to maximize . In the conditional likelihood framework we assume are known without perturbations and therefore the problem comes down to

Without prior knowledge on , or , the maximum likelihood problem can be rewritten as

The objective is strongly concave with respect and separately. An alternate maximization procedure therefore yields an argument-wise maximum (but not necessarily a global optimum).

5.1.2 Iterative un-conditional likelihood based estimation

In this setting we consider as unknown. We also restrict to the case in which is a Gaussian distribution with variance . In such a context, one can rewrite each as an infinite linear combination of . The variables are independent Gaussian vectors and therefore the infinite linear combination is also a Gaussian variable. Let the variance of . The problem becomes that of finding

It is somewhat similar yet somewhat more complex than the conditional likelihood based estimator.

5.1.3 First order methods based resolution

For strongly concave and Lipschitz gradient optimization problems, gradient ascent yields an exponential rate of convergence. The gradient of the conditional likelihood problem decomposes as

What is remarkable there is that only local data (namely

is needed to compute the term corresponding to datum .

For strongly concave and Lipschitz gradient optimization problems

consisting of a large sum, stochastic gradient descent has a squared

error that converges in

to with an appropriate hyperbolically decreasing step size. In

a big data context, if is so high that a holistically computation

of the gradient is too computationally expensive then one should use

a stochastic gradient method in order to estimate their model.

One should definitively avoid second order methods here if

and choose a deterministic or stochastic first order optimization

method. Practically this requires to sample out a certain value of

in and compute

and . There again, only local data is needed to compute the gradient contribution corresponding to .

6 When models become very highly dimensional

Let us come back to an order auto-regressive model with

spatial dimensions where . The Yule-Walker equations only

yield estimates that will require the inversion of a size square

matrix, this is not a scalable solution with respect to .

Let us assume the order of the model is (one can always rewrite

an order model in this manner):

where is sparse and rearranged so as to be a width banded matrix with . Such a sparsity pattern is quite frequent and arises for instance in numerical differentiation schemes. It is illustrated in Figure 1.

6.1 Efficient one-step-ahead prediction with spatially sparse models

If one observes at a given timestamp , then the best linear predictor of is

Let us assume we split into a row partitioned matrix as follows:

For any let us denote the

set of indices spanned by the rows of and

the set of indices spanned by .

The class of sparse models considered above is a linear specific case

belonging to the family

where

is a family of functions from

onto parametric by .

An efficient unbiased estimator of the one-step-ahead predicted value

can be written in a row partitioned manner:

In the linear case above, the time complexity of the operation is .

6.2 Efficient sparsity leveraging Bayesian estimation

We assume that is a Gaussian white noise whose precision matrix, is block diagonal with blocks corresponding to the sets of rows and columns .

The conditional log-likelihood of an observed process is therefore

Consider

We have assumed , therefore

and furthermore

Let us consider we want to maximize with respect to , we have

where, letting denote the number of parameters in the model,

What is remarkable with these expressions is that they enable embarrassingly

parallel computations provided one uses different nodes for any

, node holds the data corresponding

to .

This is also true if one plans on using a second order method.

With a first order method, the time complexity of computing the gradient

for each node is

where the cardinal of the overlapping partition

which can be as low as . This implies that this solution

is scalable with respect to the size of the model as it leverages

the prior knowledge of the model’s sparsity. To the best of our knowledge,

there is no equivalent computational result with the matrix inversion

and Yule-Walker equation based methods above.

6.3 Gradient descent, step size and rate of convergence

This section focuses on the maximization of the conditional likelihood of a Gaussian AR process. In order to simplify notations we only consider the AR1 case. The conclusions below are trivially extended to the general case. Letting the precision matrix of the process’ noise, maximizing the conditional likelihood of the process is equivalent to maximizing

and

We consider has already been estimated by . Maximizing with respect to then comes down to a gradient ascent update by . In several particular cases this update matrix takes a remarkable form:

-

•

If , . In this case the Hessian of is a block diagonal matrix whose blocks are . Therefore finding the smallest and largest eigenvalues of is sufficient to compute . This step size is of importance as it provably achieves an exponential rate of convergence to the optimum in a gradient ascent.

-

•

If is diagonal, . The Hessian is then the Kronecker product of and which means it is sufficient to compute the smallest and largest eigenvalues of and in order to find a converging step size to the gradient ascent. The rate of convergence in that case will be linear.

-

•

In any case, a line search method also enables convergence to the maximum.

For the detail of these convergence rates we refer the reader to

7 Common access patterns, fragmentation of data, distribution of computations

The M (frequentist, average based) and Z (bayesian, maximum likelihood based) estimators above rely on similar computational needs. Namely, one computes the output of a kernel function evaluated on neighboring data and then averages the results.

7.1 Map reduce for M kernel based estimators

There is a very common computation pattern to the estimators. Frequentist estimators rely on the estimation of a covariance function. In the centered case, this can be computed by considering a finite covariance matrix which can be estimated by computing quantities

for . This means that the vector of square matrices

can be approximately estimated as

This estimator is biased but asymptotically unbiased. Computing this estimator of the auto-covariance matrix is quite straightforward with map-reduce operators. One maps the computation of the local kernel

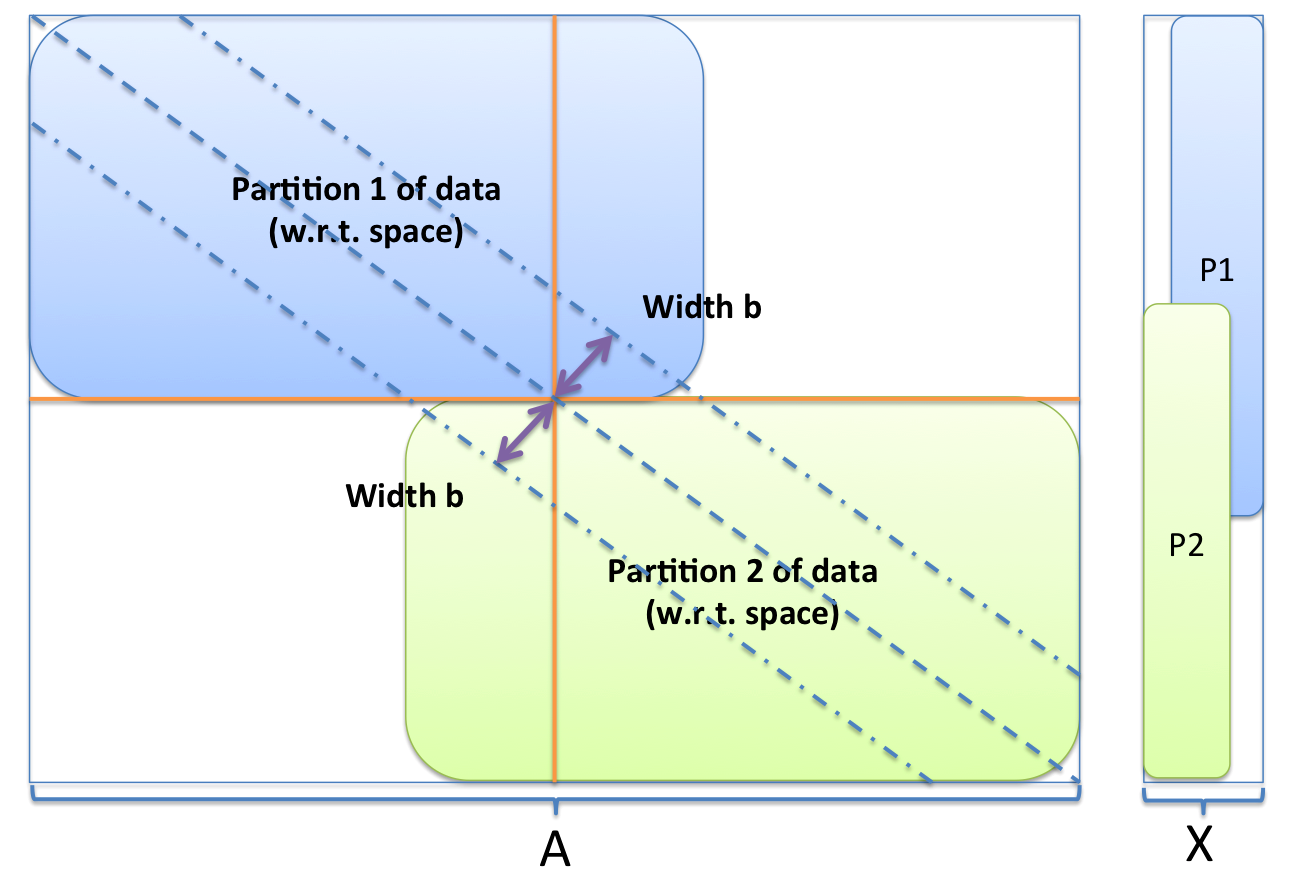

and then reduces with a sum operator prior to normalizing by . Such a computational schema is represented in Figure 2. This estimator is asymptotically normal with a convergence rate.

7.2 Map reduce for Z kernel based estimators

Computing the gradient of parameters in an auto-regressive model of finite order can also be formulated in terms of a similar computational schema. For instance, when one tries to solve the conditional maximum likelihood problem for an AR model

by a first order method, the gradient can also be computed as a sum over a large number of terms of locally computable quantities. Indeed, let be the function

Then, by linearity of the gradient,

For any , computing

only relies on data .

7.3 Overlapping data

These quantities are straightforward to compute in a serial manner

on a single CPU. However, when it comes to using a distributed system

of computation such as Apache Spark, one has to take into account the requirement

for data to be partitioned. In order to speed up the computation process

and avoid the inter-node communication bottleneck one will want to

mostly use a data partitioning scheme that, once loaded in the RAM

of a cluster of machines, will enable embarrassingly parallel computations.

For GPU units to speed further up the process, it is also interesting

to consider data partitioning as global memory units are usually slower

to access than shared one. Furthermore, one will want to be able to

run the computations above in an embarrassingly parallel way once

appropriate parallelization steps have been undertaken.

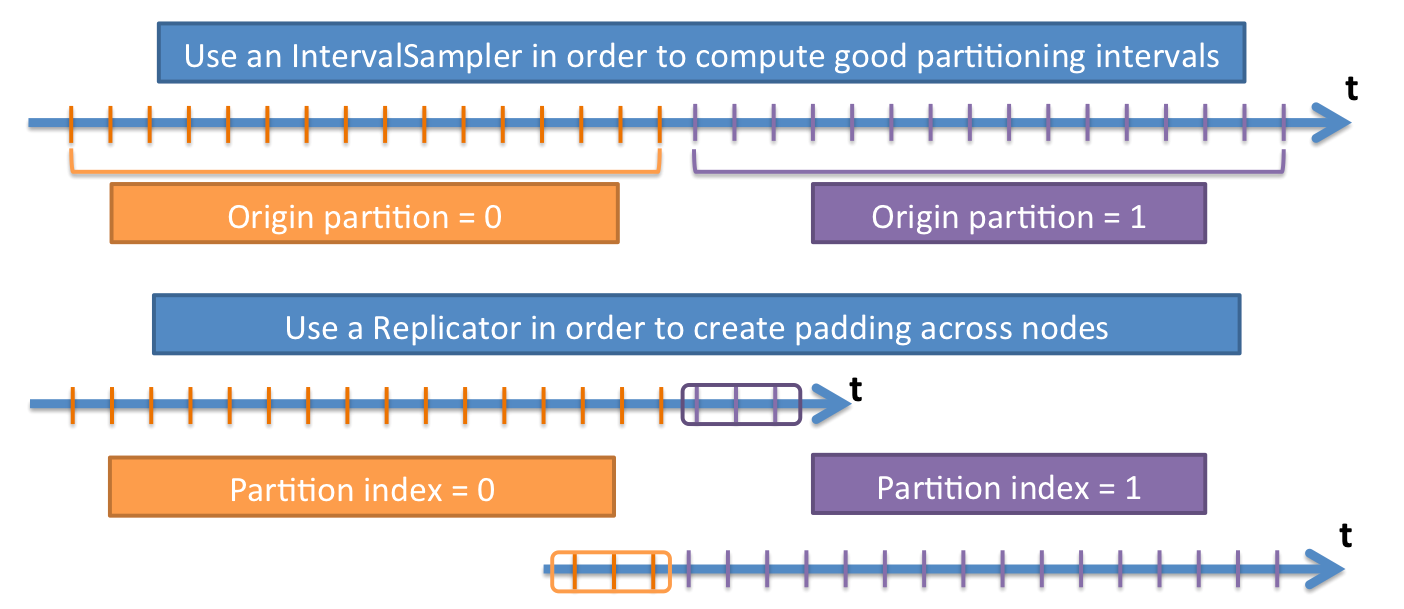

As we explain in the following, this preparation step consists of

replicating the data so as to create overlapping partitioning. The

next part will explain the theoretical foundations of the scheme and

how to choose its padding horizon parameter appropriately with respect

to the calibration of a certain model. In particular, we introduce

the fundamental data structure that has been designed to enable large

scale analysis of time series: distributed overlapping blocks.

Part II A general programming paradigm for weak memory estimation

In this paragraph we will give formal definitions of the notions of

weak memory from a computational standpoint. The following enables

general purpose time series analysis calculus to run on partitioned

data architecture in an embarrassingly parallel manner. In particular,

the distributed overlapping block data structure enables partitioning

with respect to both the different dimensions of a time series (different

signals, sources of data) and with respect to time, which is new to

the best of our knowledge. The paradigm is simple and therefore can

easily be adapted to other systems. This non system specific principle

of overlapping blocks is very powerful though as it enables in-RAM

computations on time series with an EC2 cluster in an embarrassingly

parallel way as well as GPU parallelization of time series calculus

thanks to CUDA.

The package created for Apache Spark, SparkGeoTS, that follows this scheme

enables time series analysis at an unprecedented scale, both in terms

of density of time stamps along the time axis and in terms of very

highly dimensional time series analysis. It supports data analytics

for both regularly time stamped data and irregularly spaced time series.

Its novelty stems from leveraging the informational properties of

weak memory in ergodic time series. It is not adapted to the non-ergodic

context which is not an actual shortcoming as in this case most usual

estimators for time series are not even convergent.

8 Weak memory computation for estimators

The first part of this document reviewed a vast class of time series models that feature weak memory computational needs. In the following we formalize that notion. Let us consider data in the form of .

Definition: Order weak memory estimator

An estimator features order weak memory if there exists an integer (horizon in number of steps) such that sufficient statistics for that estimator can be computed by reducing kernel computation results feeding on a data point and the neighbors of that point that are less than time steps away on the time index.

Example: Second order stationary time series

We have shown above that usual estimators for AR models are weak memory estimators, similarly with MA ( weak memory) and ARMA models ( weak memory).

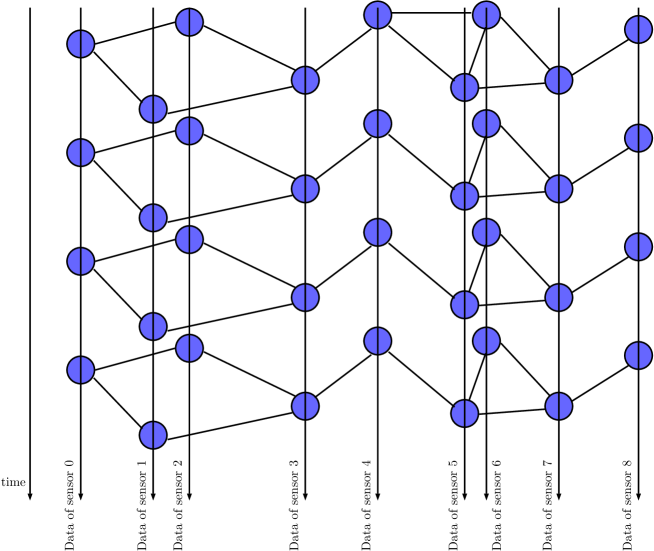

9 Weak memory in time series graphs

If one considers a system in which sensors are included in a relational

graph then the time series of readings produced by these sensors are

naturally embedded in a graph. An example of the resulting data lattice

is represented in Figure 3.

A regularly indexed time series graph is a sequence

where the set of vertices of the graph is tied together by a set

of edges with uniform weight .

9.1 Data with regularly indexed timestamps

Definition: Order weak memory estimator

An estimator is said to feature order weak memory if sufficient statistics can be computed by reducing kernel computations that, for each vertex state , only feed on the states of neighbors that are at most hops away in the graph on a time window that does not go further than time steps away from .

Example: queuing model for arterial traffic

A traffic network can be mapped to a graph where vertices represent intersections and edges correspond to roads. Such a mapping correspond to a primal whose dual graph consists of vertices modeling roads and edges accounting for the binding intersections represent. One considers a discrete model in which the state of congestion at time on vertex only depends on the state of congestion of its upstream and downstream neighbors. This assumption is very usual in traffic as soon as the discretization resolution is such that where is the length of the shortest road, the time discretization resolution and the maximum speed of vehicles in the network.

10 Embarrassingly parallel weak memory time series distributed representations

In this section we define a programming paradigm to leverage the informational structure of short memory time series in order to make their analysis distributed and embarrassingly parallel. In particular we focus on the case where both the sampling rate and the number of dimensions of the time series under consideration are high enough so that the data cannot fit in a reasonable amount of RAM on a single machine.

10.1 Very high dimensional short memory time series

Strategies have been developed to parallelize the analysis of time

series on distributed clusters or high performance computers. For

Apache Spark, libraries such as SparkTS and Thunder divide the time series

into smaller data sets by splitting it along dimensions. This paradigm

is efficient whenever each dimension has few enough timestamp for

its entire data to fit a node’s RAM. Also, for multivariate analysis,

it is more suitable to preserve data locality across dimensions. The

statistical estimation code that should be used then needs not be

aware of the partitioning scheme. What is more, there is a gain in

terms of efficiency as joins on timestamps are not necessary.

In the following we devise data structures that leverage the informational

properties of short memory time series in order to make their analysis

embarrassingly parallel. From a design standpoint, a map-reduce programming

scheme is adopted so that pre-existing estimation tools can be used

with that distributed container.

10.2 The overlapping data model

Going back to the definition of short memory in time series, it is

obvious now that any local operation only needs to be aware of its

neighborhood. Neighborhoods are defined in terms of steps for

regularly spaced data and units of time for irregularly spaced data.

Considering the data of a time series

and an estimation kernel

(with window width ), any estimation based on a reduced

quantity of the results of this kernel can become embarrassingly parallel

provided data is partitioned, partially replicated and contained in

an overlapping partitioning with overlap at least .

10.2.1 Map-reduce based estimation with a kernel of width

Let an estimator

where stands for any commutative and associative operation.

Let us assume that the data has been partitioned in partitions

with an overlap of width between partitions. The computation

flow is illustrated in the case of the estimation of an auto-covariance

function in Figure 2. The presence

of an overlap directly enables one to make that computational embarrassingly

parallel with no communication needed between computational nodes

holding different partitions of the data. Such a representation of

data is illustrated in Figure 4.

10.2.2 Overlapping data set with respect to space

Time is not the only dimension along which overlapping partitioning

can be computed. Obviously the scheme can be adapted to spatial meshes

with regular indexing such as images. The case of data points irregularly

arranged on a map falls under the same paradigm. More interesting

is the case of data where no Euclidian distance is available in a

straightforward way. Graphs correspond to that kind of data.

Local operations on graphs are straightforwardly defined in terms

of reduced kernels provided they are only interested in the parenthood

degree of the neighbors of the target. Therefore the same scheme can

be adapted as illustrated in Figure 5.

10.3 Long memory case

Time series such as stock valuations on the stock market or volatility are known to feature long memory. In other words, the informational footprint of an event never completely fades away in the system. After having computed its consecutive differences, any integrated process comes down to a short memory time series. This means that the data representation paradigm above is valid in a vast range of cases. It can be extended to partially integrated processes thanks to partial differentiation provided the partial differentiation kernel is approximated by a finite support kernel.

11 Embarrassingly parallel representation of time series embedded in graphs

This section will be dedicated to finding applications of the graph overlapping paradigm above in vast systems where information flows within a sparse Dynamic Bayesian Network.

11.1 Sparse spatial dynamic bayesian network

Studying arterial network dynamics in traffic often comes down to considering the series of states of vertices (road links) bound together by intersections. In order to compute the current number of vehicles on a link, one takes into account the number of vehicles that are effectively leaving, baring the constraints of downstream occupancy capacity, to the current occupancy and adds up the number of vehicles flowing from upstream.

11.1.1 Order time and space memory Directed Acyclic Bayesian network

Such a setting is a particular instantiation of a short time and space

memory time series graph. It is illustrated in Figure 6.

In such a framework, the next state of a given vertex can be computed

as the result of the convolution of a kernel from its direct parents.

Therefore, the overlapping data structure can be used in order to

make the corresponding study embarrassingly parallel. This can be

used for retrospective data analysis and simulation as well provided

the same random number series are provided to edge representing identical

forward state computations.

11.2 Cross-product of overlapping representations

In order to maintain reasonable size partitions, that is to say, partitions

that can fit in the RAM of a non HPC machine, one can combine overlapping

partitioning with respect to time and the corresponding time series

graph in a cross-product fashion. This creates more redundant data

but still provides a representation of data that enables embarrassingly

parallel computations if short memory is leveraged.

If the informational structure of the data set is as presented in

Figure 7, then the cross product

partitioning illustrated in Figure 8 enables

its embarrassingly parallel analysis.

12 Speeding up computations on a GPU

Here we prove that the overlapping block scheme is not system specific and can be adapted to another kind of hardware: Graphical Processing Unit (SIMD systems).

12.1 Memory hierarchy

Here we focus on the memory hierarchy highlighted by Nvidia’s CUDA

GPGPU language. It is possible to write data from the RAM to both

the global device memory and shared memory.

The shared memory is only accessible by threads of the same block

and only lives as long as a kernel execution. However, it enables

one to leverage the computational power of the GPU as its bandwidth

is often times that of the global memory.

Time series analysis relies on computation of local kernels in which

data is mostly accessed redundantly by several threads of the same

block. Therefore, it seems reasonable to try and leverage this shared

memory. Each block of this memory is only accessible to the corresponding

threads and the size is much less than that of the global memory (by

a factor of ).

We show here that overlapping blocks enable us to conduct time series

analysis in a weak memory context in an embarrassingly parallel manner

while leveraging the high bandwidth of shared GPU memory.

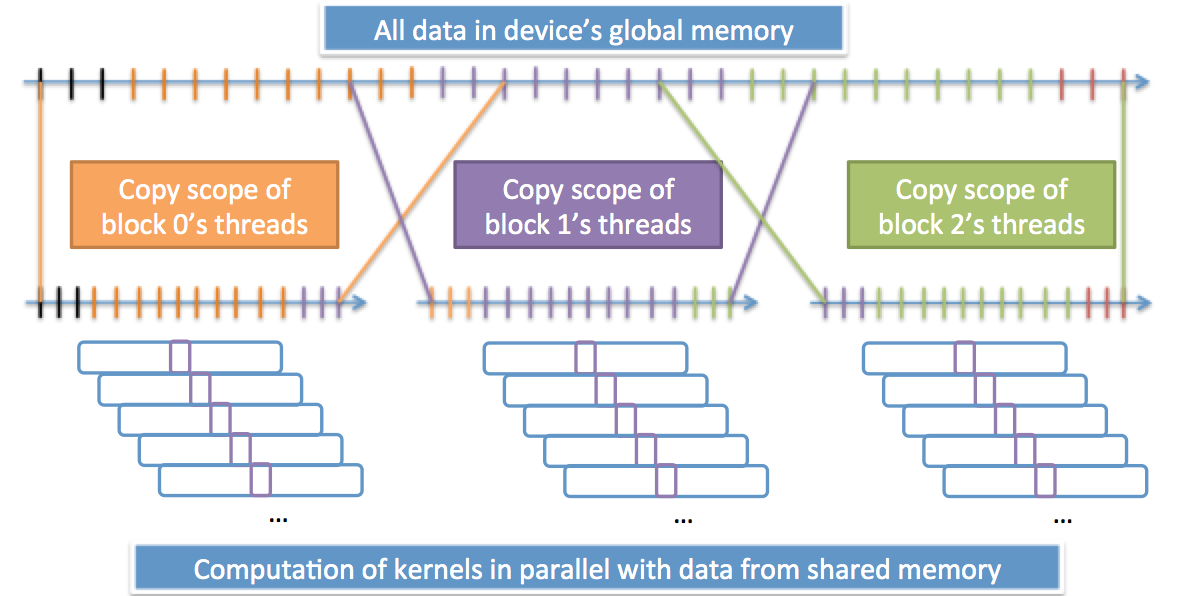

12.2 Parallel computation and overlapping blocks in shared memory for regularly spaced time series

In the following we illustrate the use of overlapping blocks on GPUs

with regularly spaced time series.

We assume the data has been copied in the global

GPU memory and one wants to execute a kernel of width prior

to conducting a reduction on the results.

Let the thread of the thread block.

We assume blocks are of size where is small enough

so the shared memory of each block is not saturated. will

copy from the global memory (address

) to the shared memory (local address ).

Then each thread with index will

compute a kernel based on data contained in local addresses corresponding

to the appropriate data, namely that contained in the shared memory

addresses ranging from to .

Provided the kernel width outweighs the cost of the copy from the

global device memory to the block’s shared memory, this provides a

speed up and optimized embarrassingly parallel data analysis for weak

memory systems. The flow of computations is represented in Figure

9.

12.3 Parallel computation and overlapping blocks in shared memory for irregularly spaced time series

For irregularly spaced data, computations are slightly more challenging

as the data that needs to be taken into account by the computation

of a local kernel does not straightforwardly correspond to a range

of memory addresses. However, we make a weak memory assumption that

no data further away than needs to taken into account in order

to compute a kernel around a datum.

One creates an overlapping partitioning of the data with overlap

and baring the memory size constraint of the shared memory blocks.

If the kernel considers all data points with timestamps in

in order to compute its output about a datum at , then letting

each thread assigned with a kernel computation look backward and forward

from for the first indices whose timestamps are out of range

and then run the kernel convolution on the data within range solves

the problem.

When kernel centers do not necessarily to data points within the data

set under consideration, things get more complicated but can be made

computationally efficient thanks to binary search. One may also create

a skip list in the global memory of the device for each thread to

access and figure out the range of the data it needs to consider.

This skip list of timestamps may sit in the global memory as it will

be accessed only once by each thread. Copying it to shared memory

blocks would cost too much overhead.

Conclusion

In this document we have shown how weak memory models in time series

analysis can be estimated and used in the context of big distributed

data sets. Identifying how many lagged values are necessary to the

calibration of the model the user wants to implement is a necessary

preliminary step. It paves the way to building up a distributed set

of overlapping partitions. This overlapping partition scheme corresponds

to partitioning with respect to time which is the new contribution

the present document presents. We show how this can also be extended

to spatial partitioning when banded causal relationship models are

being considered.

The new overlapping distributed data set presented here enables a

new any-scale any-dimensional analysis of data without the need

for shuffling observations between computation nodes once the appropriate

data representation has been created. This provides the user with

the opportunity to calibrate linear weak memory time series at scale

in a reactive manner and the possibility to quickly assess how much

a given model is appropriate in terms of goodness of fit and complexity.

This paradigm can also be extended to the calibration of conditionally

heteroscedastic models [24] as well as long

memory models [25, 26]. This

is the subject of ongoing work.

References

- [1] D. R. Brillinger, Time series: data analysis and theory, vol. 36. Siam, 1981.

- [2] P. J. Brockwell and R. A. Davis, Time Series: Theory and Methods. New York, NY, USA: Springer-Verlag New York, Inc., 1986.

- [3] J. D. Hamilton, “Time series analysis princeton university press,” Princeton, NJ, 1994.

- [4] A. C. Harvey and A. Harvey, Time series models, vol. 2. Harvester Wheatsheaf New York, 1993.

- [5] H. Ltkepohl, New Introduction to Multiple Time Series Analysis. Springer Publishing Company, Incorporated, 2007.

- [6] J. Dean and S. Ghemawat, “Mapreduce: simplified data processing on large clusters,” Communications of the ACM, vol. 51, no. 1, pp. 107–113, 2008.

- [7] K. Shvachko, H. Kuang, S. Radia, and R. Chansler, “The hadoop distributed file system,” in Mass Storage Systems and Technologies (MSST), 2010 IEEE 26th Symposium on, pp. 1–10, IEEE, 2010.

- [8] A. Thusoo, J. S. Sarma, N. Jain, Z. Shao, P. Chakka, N. Zhang, S. Antony, H. Liu, and R. Murthy, “Hive-a petabyte scale data warehouse using hadoop,” in Data Engineering (ICDE), 2010 IEEE 26th International Conference on, pp. 996–1005, IEEE, 2010.

- [9] M. Zaharia, M. Chowdhury, T. Das, A. Dave, J. Ma, M. McCauley, M. J. Franklin, S. Shenker, and I. Stoica, “Resilient distributed datasets: A fault-tolerant abstraction for in-memory cluster computing,” in Proceedings of the 9th USENIX conference on Networked Systems Design and Implementation, pp. 2–2, USENIX Association, 2012.

- [10] R. S. Tsay, Analysis of financial time series, vol. 543. John Wiley & Sons, 2005.

- [11] M. Mudelsee, “Climate time series analysis,” Atmospheric and, vol. 397, 2010.

- [12] S. Basu, A. Mukherjee, and S. Klivansky, “Time series models for internet traffic,” in INFOCOM’96. Fifteenth Annual Joint Conference of the IEEE Computer Societies. Networking the Next Generation. Proceedings IEEE, vol. 2, pp. 611–620, IEEE, 1996.

- [13] K. W. Hipel and A. I. McLeod, Time series modelling of water resources and environmental systems. Elsevier, 1994.

- [14] T. Hunter, T. Moldovan, M. Zaharia, S. Merzgui, J. Ma, M. J. Franklin, P. Abbeel, and A. M. Bayen, “Scaling the mobile millennium system in the cloud,” in Proceedings of the 2nd ACM Symposium on Cloud Computing, p. 28, ACM, 2011.

- [15] M. Franklin et al., “Mllib: A distributed machine learning library,” NIPS Machine Learning Open Source Software, 2013.

- [16] J. Durbin and S. J. Koopman, Time series analysis by state space methods. No. 38, Oxford University Press, 2012.

- [17] S. Boyd and L. Vandenberghe, Convex optimization. Cambridge university press, 2004.

- [18] D. P. Bertsekas, “Nonlinear programming,” 1999.

- [19] F. M. Callier and C. A. Desoer, Linear system theory. Springer Science & Business Media, 2012.

- [20] H. Kantz and T. Schreiber, Nonlinear time series analysis, vol. 7. Cambridge university press, 2004.

- [21] J. Fan and Q. Yao, Nonlinear time series: nonparametric and parametric methods. Springer Science & Business Media, 2003.

- [22] Straumann and T. Mikosch, “Estimation in conditionally heteroscedastic time series models,” tech. rep., Lecture Notes in Statist. 181, 2005.

- [23] H. Akaike, “Block toeplitz matrix inversion,” SIAM Journal on Applied Mathematics, vol. 24, no. 2, pp. 234–241, 1973.

- [24] R. Lund, “Estimation in conditionally heteroscedastic time series models,” Journal of the American Statistical Association, vol. 101, no. 475, p. 1319, 2006.

- [25] P. Doukhan, G. Oppenheim, and M. S. Taqqu, Theory and applications of long-range dependence. Springer Science & Business Media, 2003.

- [26] B. B. Mandelbrot, Fractals and Scaling in Finance: Discontinuity, Concentration, Risk. Selecta Volume E. Springer Science & Business Media, 2013.