Tel: +41 31 6318801

Fax: +41 31 631 3870

22email: andreas.haier@gmail.com, ilya.molchanov@stat.unibe.ch, michael.schmutz@stat.unibe.ch

Intragroup transfers, intragroup diversification and their risk assessment111The authors are grateful to Philipp Keller for many interesting and important remarks on the misuse of IGTs. The comments of the referee have lead to several improvements of the manuscript. IM was partially supported by Swiss National Foundation grant 200021_153597.

Abstract

When assessing group solvency, an important question is to what extent intragroup transfers may be taken into account, as this determines to which extent diversification can be achieved. We suggest a framework to explicitly describe the families of admissible transfers that range from the free movement of capital to excluding any transactions. The constraints on admissible transactions are described as random closed sets. The paper focuses on the corresponding solvency tests that amount to the existence of acceptable selections of the random sets of admissible transactions.

JEL Classifications: G32, C65, G20

Keywords:

Fungibility risks Intragroup diversification Intragroup transactions Set-valued risk measures Risk assessments for groups Solvency tests for groups1 Introduction

Risk-based solvency frameworks (such as Solvency II or the Swiss Solvency Test (SST)) assess the financial health of insurance companies by quantifying the capital adequacy through calculating the solvency capital requirement. Roughly speaking, companies can use their own economic capital models (internal models) for calculating the available capital amounts (net assets) after one year provided the internal model is approved by the insurance supervisor. The random variable given by the capital amount after one year is required to be acceptable with respect to a prescribed risk measure.

Since key market players are organized in groups, the question of setting appropriate solvency requirements for groups becomes highly relevant, and the quantification of risks for a group of different legal entities (agents) is an essential aim of regulators. The main feature of the group setting is the possibility of intragroup transfers (IGT) that may alter financial positions of individual agents. Section 2 surveys fundamental ideas in this relation that have been already mentioned in fil:kun08 ; fil:kup07 ; fil:kup08 ; kel07 ; lud07 and are intensively discussed in the financial industry. A key question is to what extent IGTs should be taken into account for the purpose of risk assessment.

The choice and admissibility of IGTs may influence the risk assessment. These admissible transfer instruments range from the free movement of capital between the agents (unconstrained approach) to the case when no transfers are allowed at all (strictly granular risk assessment). In between, we consider allowing transactions that prohibit transfers that render the giver bankrupt or those originating from a bankrupt agent. One might consider imposing some safety margins or taking into account fungibility issues, see Section 6.

Our aim is to provide a unified framework in order to explicitly describe such transfers and the relevant risk measures. So far the idea of using random closed sets (most importantly random cones) to describe multiasset portfolios is well established, see kab:saf09 . We show that a similar approach may be used to describe the sets of admissible IGTs. The key idea of our approach is to regard the group as acceptable if there exists an admissible transfer that renders acceptable the individual positions of all agents. The family of vectors representing the capital amounts added to (or released from) each agent that make the group acceptable serves as a risk measure for the group. This idea is similar to the risk assessment of multiasset portfolios from ham:hey:rud11 and cas:mol14 , while the main difference is the non-conical dependence of the set of admissible transfer instruments from the current capital position. As a result we end up with the new possibility to explicitly translate realistic (non-conical) transfer constraints in a quantitative risk management framework that assesses genuine intragroup diversification benefits.

Section 3 recalls major concepts related to random closed sets, their selections, thereby following and extending some results from cas:mol14 . Section 4 introduces the random sets of admissible IGTs. Furthermore, it formulates and analyses the relevant capital requirements in terms of set-valued risk assessment of the relevant random sets of admissible positions. Since the family of admissible IGTs typically depends to a large extent on the level of distress a group is faced with, this dependence creates non-conical and non-linear effects.

Section 5 recasts the classical granular and consolidated approaches into our setting. We show that, under some canonical assumptions, the granular approach can be obtained by restricting the set of IGTs in the unconstrained solvency test, i.e. in the test without any constraints on IGTs. In the coherent case, the latter corresponds to the consolidated solvency approach, which is frequently used in practice. Furthermore, we discuss the unconstrained solvency test in important non-coherent cases. Various restrictions of transfers are discussed in Section 6.

Section 7 deals with the setting of unequally placed companies, where some companies possess the capital of others and so simple addition of capital amounts would lead to double counting. It is shown that this setting can be naturally incorporated in our set-valued framework.

Separating the financial outcome after a certain period from the (possibly restricted) transfers between the companies (or in other applications between portfolios) can lead to diversification effects that are different from the usual case of convex risk measures, since not all of them work in the same direction, see Section 8.

In Section 9 we discuss the computation of the relevant sets, give inner and outer bounds which can be easily implemented and discuss some numerical examples.

Our setting differs from studies of systemic risk, where the individual acceptability of each agent does not suffice for the acceptability of the whole financial network, see amin:fil:min13 . While, in common with the studies of systemic risks in fein:rud:web15 , our approach involves inverting a set-valued risk measure, it does not rely on considering an equilibrium in the system of agents.

2 Existing solvency tests for groups

2.1 Legal entity approaches

A very basic but key observation for market regulators is that it is not in the obligation of an insurance group but of individual legal entities to pay for claims of policy holders. This basic observation can become particularly relevant under stress. In view of that, it has often been emphasized in the literature that risk assessment and capital requirements for groups of companies should take place on an individual basis, see e.g. fil:kun08 ; fil:kup07 ; fil:kup08 ; kel07 ; lud07 . This means that each legal entity is requested to set aside the capital necessary to make its risk acceptable. This approach is often called legal entity approach.

The legal entity approach appears in two basic variants: stand-alone and granular. In the stand-alone solvency assessment, the capital amounts (net assets) of each legal entity are modeled separately and regarded as random variables on a probability space that might differ between the legal entities. All other group members are considered as third parties, i.e. are treated in the same way as non-members of the group.

The granular approach aims at developing a joint model for all legal entities in a group. The existence of the group has an impact on the legal entities, meaning that effects of the group on individual entities should constitute a part of the model. These effects result from certain IGTs and ownership relations within the group and should hence be taken into account in the model. Typical examples are reinsurance agreements, financial guarantees, and intragroup loans.222For simplicity of representation we consider no hybrid instruments in this paper and we also do not enter in the important but non-mathematical debate about legal requirements IGTs should satisfy. While the whole collection of capital positions for all involved legal entities is modeled as a random vector, the granular approach assesses each of its components separately and these depend on the IGTs chosen by the group. In particular note that in this existing solvency test the capital requirement is not given by a single figure.

As opposed to the stand-alone approach, the granular approach relies on joint modeling of the capital amounts and IGTs so that the information on other entities and the random variables describing their capital positions flows directly and consistently333E.g. the terminal position of the legal entity usually depends on some risk factors (equity, interest rates, mortality etc.). In the stand-alone case the risk factor models do not need to be the same. In the granular case the terminal positions are modeled based on the same risk factors. into the modeling of any particular component. In other words, the granular approach relies on the modeling of each particular component on a richer probability space. This may lead to different marginal distributions between the stand-alone and the granular approach. Hence, it seems to be almost impossible to suitably model on a stand-alone basis the particularly dangerous situation where several group members simultaneously run into problems.

Mathematically speaking, consider legal entities whose terminal capital positions are described by the vector . Since the main point of this paper is to separate the financial positions after the relevant time period from the set of admissible IGTs we will later assume that is the capital position of all agents without any IGTs.

It is assumed that the risks of the legal entities are evaluated using monetary risk measures, namely the risk measure for the th legal entity. The individual risks of each legal entity after IGTs build the vector

where the position represents the capital positions after IGTs. It is regarded acceptable if for all , meaning that , where the inequality between vectors is understood coordinatewisely and so means that has all non-positive components.

2.2 Consolidated approach vs. granular with fixed IGTs

Intragroup transactions can be used for increasing the “diversification” of risks within the group, and so they can be in the interest of all policy holders, see e.g. fil:kup08 , if they are applied in reality. In particular, IGTs may be used to offset the risks of some, e.g. poorly performing, legal entities, while not necessarily immediately diminishing the disposable assets of other legal entities.

Since the IGTs can reduce the solvency capital requirements, it is important that they are not of a purely hypothetical nature. Thus, they have to be realistic in situations when they are needed. The family of feasible transfers depends on whether or not the group is in a stressed situation, i.e. they are particularly exposed to fungibility risks, as is well-known in practice. Furthermore, note that not all policy holders (of different legal entities within a group) have the same interests. Hence, IGTs have to be “sufficiently balanced” with respect to the interests of all policy holders. It is important to note that IGTs have a general potential for being misused. Thus, even if transfers are based on legally binding and enforceable contracts, it is still possible that the corresponding transfers are not realistic, not sufficiently in line with the interests of some policy holders, etc., so that other/further restrictions may have to be taken into account. The decision about the restrictions, which are finally taken into account in a concrete solvency framework is a political and legal but not mathematical question, therefore it is not addressed in this paper. However, what we provide here is a tool to translate restrictions into a quantitative risk management framework.

It becomes increasingly popular in practice to regard the group as acceptable if the random variable

| (2.1) |

is acceptable with respect to a prescribed risk measure.444For simplicity of the representation we ignore here subtleties regarding the so-called (a)symmetric valuation. For a discussion of participation in subsidiaries we refer to Section 7. This approach is called the consolidated solvency test. It is a frequently discussed interpretation that the classical consolidated approach implicitly assumes full fungibility of capital between all different legal entities of the group, see e.g. kel07 ; lud07 .

Filipović and Kupper fil:kup07 ; fil:kup08 and Filipović and Kunz fil:kun08 made an important step towards understanding intra group diversification and quantifying regulatory schemes being sandwiched between the granular approach without any admissible IGTs, in the following called strictly granular, and the consolidated solvency tests. Concrete examples are based on dividend payments and reinsurance contracts and are described by some random transfer instruments (linearly independent random variables) , so that the terminal risk profile of each agent is given by

where the transferred amounts belong to a specified (feasible) subset of and satisfy the clearing condition

It is assumed in fil:kup08 that the group aims to minimise the aggregate required group capital

subject to the feasibility and clearing conditions on the weights .

Apart from the mentioned independency assumption, fil:kup08 assume a single currency setting, absence of transaction costs, that the weights are deterministic numbers and that the admissible transfers are restricted to be a linear combination of fixed instruments without explicit fungibility constraints that depends on the level of distress a group is exposed to.

Fungibility constraints on possible dividend payments are considered in the very concrete bottom-up group diversification analysis presented in fil:kun08 . The natural link between admissible IGTs and the minimization problem of the total required capital of the group, which is emphasized in fil:kup08 , relates this work to the extensive literature on optimal risk sharing, see e.g. acc07 ; acc:svi09 ; Asim:Bad:Tsan13 ; bar:elk05 ; bar:sca08 ; ger79 ; rav:svi14 and the literature cited therein. For optimization under restriction to certain so-called cash invariant sets we refer to fil:svi08 , partially based on fil:kup08 , for portfolios of risk vectors (including the influence of dependence on the risk of a portfolio) see kis:rue10 .

In the interest of brevity, the main focus of this paper concerning the granular approach is on the task to directly include concrete admissibility constraints for IGTs in a solvency framework without restricting the analysis to concretely given contracts, and we leave to agents the task of choosing specific IGTs from the family of admissible ones.

From a practical perspective, groups may not necessarily aim to minimize the total capital requirement, since some legal entities may have different placements or roles within the group (like subsidiaries and head offices), some may be reluctant to commit own capital in order to compensate the losses of other legal entities or may do this only given certain conditions (that are random), etc. In view of this, the total required capital for the group may not serve as a right utility for the group, or at least the agents might seek to minimize the total required capital only under additional constraints that do not seem to be reflected in the literature so far.

2.3 Consolidated test with fungibility constraints

The consolidated solvency approach is based on the acceptability of the random variable in (2.1), where the group is simply considered as if it were one “legal entity”. It is the default case in Solvency II. Since July 2015 the default case of the SST is also based on this approach. However the regulator may impose additional requirements concerning availability and fungibility of capital within the group and also impose capital add-ons in case of seriously restricted fungibility that is not reflected in the models. In view of that, it is essential to derive a proper and mathematically well-founded way of describing transfer possibilities within the group and to find and to derive a framework which allows to adequately include fungibility constraints into the consolidated framework.

By translating the consolidated test into the unconstrained solvency test in the subadditive case, we show that no fungibility constraints are taken into account in the risk-measurement. We also suggest a framework that represents fungibility constraints in a solvency test via simply and explicitly restricting the set of admissible transfers.

3 Set-valued portfolios and set-valued risks

A set is lower if (coordinatewisely) for implies that . The family of upper sets coincides with the family of reflected lower sets, i.e. is an upper set if and only if is a lower set. The topological closure of is denoted by and its boundary by . Denote .

Fix a complete probability space . Let be a lower random closed set in , i.e. is a random element taking values in the family of lower closed sets in . The measurability requirement on is understood as for all compact sets in , see mo1 . The set is called a set-valued portfolio in cas:mol14 . In our setting, the points of describe the terminal capitals of companies of a group after all admissible IGTs. In many cases, is almost surely convex, meaning that almost all its realizations are convex sets.

Let be the family of -integrable random vectors in , where is fixed. The choice yields the family of all random vectors. Denote by the -norm of for . A random vector in is said to be a selection of if almost surely. Such a random vector may be viewed as a particular terminal position achieved after a certain IGT. We assume throughout that is -integrable, i.e. possesses at least one -integrable selection. In other words, the family of all -integrable selections of is not empty.

We identify with the family of all its -integrable selections. This is justified by the fact that, for almost all , is the closure of for a sequence , see (mo1, , Prop. 2.1.2).

In the following denotes the vector composed of monetary risk measures with finite values defined on the space for (called -risk measures). Canonical examples of such risk measures are the Value-at-Risk for all , the Average Value-at-Risk for or the entropic risk measure for .

Being finite -risk measures, the components of are Lipschitz in the -norm, see kain:rues09 . In particular, they are strongly continuous. If , additionally assume that the components of satisfy the Fatou property that corresponds to the weak-star lower semicontinuity (that is with respect to the bounded a.s. convergence).

Furthermore, is said to be coherent (resp. convex) if all its components are coherent (resp. convex) risk measures, and in this case we let , see kain:rues09 . The coherency or convexity assumptions are explicitly imposed whenever needed.

All convex (and coherent) risk measures are tacitly assumed to be law invariant and defined on a non-atomic probability space.

Definition 3.1

A set-valued portfolio is said to be acceptable, if it possesses a -integrable selection with all individually acceptable marginals, i.e. there exists such that . Then is called an acceptable selection of .

Definition 3.2

The selection risk measure is the closure of the set

Equivalently, the selection risk measure can be defined as

In ham:rud:yan13 , for and a cone is called a market extension of the regulator risk measure .

Example 3.1

On the line all lower sets are half-lines, so that each set-valued portfolio in is given by for a random variable . Then is acceptable if and only if is acceptable. Working with the half-line instead of does not alter financial realities, while being a useful tool in higher-dimensional situations.

If for -integrable random vector , then .

Example 3.2

Let for a random variable . The family of all essentially bounded selections of the boundary of was studied in detail in jouin:sch:touz08 for and is called the set of attainable allocations, see also ger79 .

In order to find acceptable selections of , it is sensible to look only at those points of that are not coordinatewisely dominated by any other selection of . These points build a subset of denoted by and are called Pareto optimal points of .

Lemma 3.1

If is convex, then is a random closed set.

Proof

Assume is a sequence converging to . By choosing subsequences, we can assume that all components converge monotonically. Let be the set of components converging strongly decreasing. Assume . Since is closed there exists such that and for some . Choose such that the set of all indices for which this inequality holds is maximal. If , then for sufficiently large , dominates , contradicting the Pareto optimality of . Assume that . By convexity, for . By taking sufficiently close to , we can achieve that for and for sufficiently large . Due to the strict monotonicity of , we also have , contradicting the maximality of . Thus, is closed.

For the measurability of , it suffices to check that , i.e. the graph of , is a measurable set in the -algebra , where is the Borel -algebra in . Indeed,

where is the family of positive rational numbers. This is justified, since a convex lower set is necessarily regular closed, i.e. coincides with the closure of its interior.

Lemma 3.2

A convex set-valued portfolio admits an acceptable selection if and only if admits an acceptable selection.

Proof

Assume that admits an acceptable selection . If is not Pareto optimal, consider the random closed set . All selections of are acceptable, is almost surely non-empty and has a measurable graph. By the measurable selection theorem (kab:saf09, , Th. 5.4.1), admits a measurable selection that is automatically acceptable.

The scaling transformation of a set-valued portfolio is defined as . The sum of set-valued portfolios is the set-valued portfolio being the closure of all sums of selections of and . It is known mo1 that such operations respect the measurability property, i.e. and are random closed sets.

The following result is proved in cas:mol14 for composed of coherent risk measures, while obvious changes lead to its version for general monetary risk measures.

Theorem 3.1

The selection risk measure takes values being upper closed sets, and also

-

(i)

for all deterministic (cash invariance);

-

(ii)

If a.s., then (monotonicity).

If is convex and are almost surely convex set-valued portfolios, then takes convex values, is law invariant, and

-

(iii)

for all deterministic (convexity).

If, additionally, the components of are all homogeneous (i.e. is coherent), then

-

(iv)

for all (homogeneity);

-

(v)

,

meaning that is a set-valued coherent risk measure, see ham:hey10 ; ham:hey:rud11 .

The set is said to be -integrably bounded if

If , this is the case if and only if is almost surely a subset of a deterministic bounded set. For the sake of completeness we provide a proof of the closedness of for all that does not use the coherency assumption as in (cas:mol14, , Th. 3.6).

Proposition 3.1

If is -integrably bounded with and is a convex -risk measure, then is a closed set.

Proof

Let and . By Lemma 3.2, there exists such that .

Assume first that . Since is -integrably bounded, all its selections have uniformly bounded -norms. By the Komlós theorem, see e.g. (kab:saf09, , Th. 5.2.1), and passing to a subsequence, converges a.s. to . Then almost surely belongs to the convex hull of , whence and . Thus, in . The -continuity of the components of yields that

so that .

If , the above inequality also applies in view of the assumed Fatou property and the fact that the norms of are all bounded by the essential supremum of .

Denote by

the support function of , where is the scalar product in . Then is a random variable for each that may take infinite values. The following result provides a simple outer bound for the selection risk measure of .

Theorem 3.2 (see Prop. 4.6 cas:mol14 )

Assume that has all identical components for a coherent -risk measure . Then

| (3.1) |

where if with a positive probability.

4 Admissible IGTs, attainable positions and their risks

4.1 Admissible IGTs

Recall that denotes the terminal positions of the legal entities evaluated on the granular basis, all expressed in the same currency. Assume that is -integrable.

A family of admissible IGTs is identified as the family of -integrable selections of a random closed set in . It is often the case that depends on the terminal capital positions and in this case is written as a function of that might also depend on additional randomness, e.g. random exchange rates. This gives the possibility to model the important feature that realistic transfer possibilities depend on the level of distress of the economic environment.

The attainable financial positions at the terminal time after admissible transfers form the family of selections of the random closed set

It is natural to regard the set of attainable positions preferable over another set if, for each selection , there is a selection such that with probability one. This partial order can be realized as the inclusion order if the sets of attainable positions are lower sets in . For this, we assume that with each admissible IGT given by a random vector , the set also includes points that are less than or equal to in the coordinatewise order, so that and are lower sets. The lower set assumption is useful to formulate mathematical properties of risks. While initially it might not seem reasonable to consider IGTs that involve a disposal of some of the assets, the monotonicity property of risk measures implies that the agents or their group in no circumstances would opt for an IGT that involves uncompensated disposal of assets and even if they would pursue such IGT, then the position without such a disposal is also acceptable.

We assume throughout the rest of the paper that is a lower set that almost surely contains the origin, and

| (4.1) |

It means that the nil-transfer is admissible and that admissible intragroup transfers are financed by the group. Sometimes is is useful to assume also that

| (4.2) |

for each . Equivalently, for all , meaning that the result cannot be improved by substituting one large transaction by several small ones.

It is essential to stress that is not necessarily a cone. In many examples, the set is convex, but it is not necessarily the case, e.g. for fixed transaction costs and indivisible assets.

Example 4.1

If there is a fixed range of admissible IGTs given by , then generally

is a non-convex set that does not depend on .

4.2 Risks of a group

The position together with the corresponding admissible IGTs given by (or the corresponding set of attainable positions) is acceptable if . The conventional definition of risk measures in its set-valued variant ham:hey10 ; cas:mol14 suggests passing from the acceptability criterion to the risk measure by considering the set of all such that is acceptable.

Definition 4.1

The group risk associated with the attainability set is

| (4.3) |

Remark 4.1

The group risk can be regarded as the inverse of the set-valued function , see aub:fra90 . A similar inverse appears in fein:rud:web15 as an approach sensitive to the capital levels, where denotes the set of capital amounts for agents, is the set of equilibrium prices, and the inverse of the selection risk measure of (in our notation) determines the systemic risk associated with the system of agents. Definition 4.1 can be applied to determine the risks of some multiasset portfolios from (cas:mol14, , Sec. 2.3) that depend non-linearly on the financial position. Note that the first argument of in (4.3) is a function.

Remark 4.2

If is a convex cone that does not depend on , like it is the case for the conical model of proportional transaction costs (see ham:hey:rud11 ; kab:saf09 ; cas:mol14 ), then , so that , whence is a convex set. As we see later on, in many cases of assessing the group risk, the set depends on , so that may substantially differ from . Then may become non-convex and so considerably more complicated to compute.

Proposition 4.1

-

(i)

If for all , then .

-

(ii)

contains .

-

(iii)

If (4.2) holds, then is an upper set and is non-decreasing as function of , that is if a.s.

Proof

(i) In this case and so the inverse function given by (4.3) is also monotone.

(ii) Since , we have

so that by (i).

(iii) Assume that , so that . By (4.1), , whence (4.2) yields that . Thus, and , and the total risk is monotonic by (i).

If , then the above applies to instead of and instead of , so that , whence if , then also .

If all agents operate with the same currency, it is possible to quantify the risk using a single real number by considering the minimal total capital requirement for the group.

Definition 4.2

The total risk associated with (also called the total group risk) is defined by

| (4.4) |

The total risk does not change if is replaced by for a deterministic vector with . By Proposition 4.1,

It is easy to see that the total risk is the support function of in direction . In particular, the acceptability of yields that , but the opposite conclusion is not necessarily true. The non-positivity of the total risk yields only the existence of transfers with the total capital requirement being zero that make acceptable. If the infimum in (4.4) is attained, then the vectors that provide the infimum give possible allocations of the total risk between the legal entities. Then there is an acceptable selection of , and the regulator could possibly request conclusion of legally binding contracts for transfers in order to arrive from to .

The set-valued map is said to be upper semicontinuous as function of if, for all , , and any sequence that converges to ,

| (4.5) |

where is the closed ball of radius centred at the origin and . This property can be equivalently formulated for .

Proposition 4.2

Let be a coherent -risk measure with . If is -integrably bounded for all and is upper semicontinuous as function of , then the set is closed. If also for at least one and all , then the infimum in (4.4) is attained.

Proof

For each , the set is closed by Proposition 3.1. Assume that , , and . By Theorem 3.1(ii),

For each selection of , there exists a selection of such that . Since the components of are Lipschitz in the -norm (see kain:rues09 ), for a constant , so that

for . Thus, for all . In view of the closedness of , it contains the origin, so that .

The monotonicity of the group risk (see Proposition 4.1) yields that , and so the attainability of the infimum follows.

The following basic properties of the introduced risks are easy to prove.

Proposition 4.3

-

(i)

The group risk and the total risk are cash invariant, i.e.

-

(ii)

If used to construct the selection risk measure is a homogeneous risk measure and for all , then and for all .

-

(iii)

If (4.2) holds, then for .

Remark 4.3

Despite the group risk has natural properties of a monetary set-valued risk measure and the total risk is similar to monetary risk measures, we avoid calling them risk measures, since they depend on two arguments: a random closed set and a specific random point inside this set.

It is known lep:mol16 that risk assessment for multiasset models with random exchange rates may be subject to the so-called risk arbitrage meaning that it is possible to find a sequence of selections that can be made acceptable by adding capital that tends to minus infinity, so that it is possible to release an infinite capital maintaining the acceptability of the position. This is the case if and only if the total risk attains the value . We will show that this is impossible for convex risk measures due to condition (4.1). However, it may become a relevant issue in the multi-currency setting with random exchange rates, see Section 6.5, and for general monetary risk measures. Recall that inf-convolution of coherent risk measures is defined by taking the closed convex hull of their acceptance sets, see delb12 .

Proposition 4.4

If is a convex risk measure with all identical components or a coherent risk measure with a non-trivial inf-convolution of its components, then the corresponding total risk is different from for all sets of IGTs that satisfy (4.1).

Proof

Condition (4.1) yields that , so that . Thus, it suffices to consider the latter set. Assume first that is coherent and there exists a sequence in such that as and for all . Therefore, there exist , , such that a.s. and . Denote by the inf-convolution of the components of . Then for all . By subadditivity,

Thus, , which is excluded by the condition. In the convex case the proof is similar with and the sums replaced by convex combinations with weights .

The following example shows that using non-convex risk measures (like the Value-at-Risk) may lead to risk arbitrage in the high-dimensional setting. This kind of arbitrage is intimately related to the notions of divisibility of risk measures as can be seen when comparing the following example to the proof of Proposition 2.2 in wang14 . Throughout the paper we use the following definition of the Value-at-Risk

| (4.6) |

for a random variable .

Example 4.2

Assume that has all identical components . Furthermore, assume that almost surely on a non-atomic probability space, and in , where dimension satisfies . Partition into subsets of probability each. Let for and otherwise, . Then , so that . Further, , since outside a set of probability .

Such a construction is not possible if . In this case, the limit property of yields that for any large and all , outside a set of probability at most . Since , the union of all these sets does not cover . This means that all components of exceed simultaneously with positive probability, so that is not a selection of .

Remark 4.4

In the two-dimensional setting, the existence of the risk arbitrage for and the risk measure means that

for a sequence , . This is clearly impossible if is convex or if with , while it might be the case if .

4.3 Absolute acceptability

The main setting in the theory of multivariate risk measures concerns the case of a single agent operating with several currencies or on various markets. In this case, the existence of an acceptable selection from the set of attainable positions is a natural acceptability requirement.

In contrary, the interests of agents, and in particular of policy holders of different legal entities in a group may differ. When trying to balance policy holder interests across the whole group, one may particularly appreciate transfers that do not worsen the situation of any policy holder, in other words satisfy the individual rationality constraints, see jouin:sch:touz08 .

Definition 4.3

The pair is called absolutely acceptable if admits a selection such that and .

In other words, such selection has all individually acceptable components and each of its components has lower risk than the corresponding component of . Financially, this may be interpreted as an admissible IGT that leads to acceptable positions of all agents without worsening the individual risk assessment of each individual agent.

The condition may be relaxed by requiring that for a cone that describes the set of individual risks that are considered acceptable by all agents within the group. For a discussion of generalized individual rationality constraints we refer to rav:svi14 .

Clearly, is absolutely acceptable if is acceptable, while the following example shows that the converse is not necessarily the case.

Example 4.3

Let for , and let have two identical components being the Expected Shortfall () at level . Assume that , say with having the standard normal distribution, and let for some , say . Then is clearly not acceptable, and so is not acceptable. But is absolutely acceptable. It is possible to reduce the risk of by a transfer without worsening the risk of , simply because the non-acceptability of stems from its behaviour on a set on which takes rather high values. More specifically, if , then is acceptable. Because , we have . Furthermore, , since on the event that has probability at least . Hence, the -quantiles (and all lower quantiles) of and coincide, and we conclude . Hence is acceptable and has a componentwisely lower risk than .

In many cases, it is impossible to ensure that none of the agents suffers a deterioration of risk after the optimal risk allocation. The following result shows that it is possible to achieve individual rationality after an initial capital transfer.

Proposition 4.5

Assume that there exists such that . Then there exists such that and .

Proof

The set contains . Furthermore,

since otherwise would be lower than the total risk. For any , satisfies the requirements.

The vector from Proposition 4.5 determines the prices of risk that the agents pay (or receive) at time zero in order that the resulting positions do not worsen the risk of any agent and that the total group risk is the smallest. This result was obtained in (jouin:sch:touz08, , Th. 3.3) for two agents.

5 Granular and consolidated tests

5.1 Strictly granular test

The strictly granular approach presumes that no non-trivial IGTs are allowed, so that , and

Then all selections from have risks that are not better than , so that and for all monetary risk measures.

5.2 Consolidated and unconstrained tests

Recall that the increasingly popular consolidated approach requires the random variable defined in (2.1) to be acceptable with respect to a prescribed risk measure. It turns out that, in the coherent case, this setting corresponds to the largest set of admissible IGTs and would imply unrestricted fungibility for all assets, i.e. at the end of the considered time period assets can be freely used to settle any liabilities within the group. In this case,

is a half-space, and

| (5.1) |

Note that is -integrable if and only if has a -integrable selection. This may be the case even if itself is not -integrable.

We call the solvency test that requires from (5.1) to be acceptable the unconstrained solvency test. In this case, and

| (5.2) |

In the case of two agents, this situation is studied in depth in jouin:sch:touz08 . The following result provides an independent analysis of this setting for with all identical components and extends it for the convex case and any number of agents.

Theorem 5.1

Let be a -integrable random vector and let for a monetary -risk measure . Furthermore, let be given by (5.1).

-

i)

If is coherent, then admits an acceptable selection if and only if . In this case, the infimum in (5.2) is attained at and .

-

ii)

Assume that, for any -integrable random vector , admits an acceptable selection if and only if . Then is subadditive.

-

iii)

If is convex, then admits an acceptable selection if and only if . The infimum in (5.2) is attained at and .

-

iv)

Assume that, for any and for any , the acceptability of the random vector yields the acceptability of . Then is convex.

Proof

i) Assume that and define , which is a selection of . Since is positive homogeneous, all components of are acceptable, and yields the corresponding IGT. Note that the sum of coordinates of vanishes almost surely.

Conversely, assume that there exists a selection of such that . Let be the projection of onto the boundary of . Note that . Then , with such that a.s. Hence,

The infimum in (4.4) equals the infimum of all such that and so is attained.

ii) For any -integrable random vector , define . By the monetary property, , so every is acceptable. By the assumption, is acceptable, while the monetary property yields that

as desired.

iii) If , then is an acceptable selection. Conversely, assume is an acceptable selection. Then , hence . By convexity,

iv) By the cash invariance, the assumption is equivalent to

We have to show that

for any and . Due to the strong continuity of the components of , it suffices to show this for rational . Applying the assumption to the random vector consisting of copies of and copies of yields that

hence, the assertion is proved.

If the components of are not necessarily coherent, then the classical consolidated approach and the unconstrained approach do not necessarily result in the same risks. If is acceptable, then admits an acceptable selection, which is given, e.g., by . However, neither the acceptability of nor of can be concluded from the existence of an acceptable selection in the non-convex case, see Proposition 5.1. Thus, the group risk calculated on the basis of the unconstrained solvency test may be too optimistic in comparison with the classical consolidated test in the non-convex setting.

Proposition 5.1

Assume that and has identical components being the Value-at-Risk.

-

(i)

If are acceptable for , then is acceptable for .

-

(ii)

If , then there are random variables such that is acceptable for , but is not acceptable for . In particular, this is the case for .

Proof

(i) The assumption yields , for each . Then

implying the acceptability of under .

(ii) Choose a non-atomic probability space and let be mutually disjoint events of probability . Define for , and otherwise. Then for all , while

so that is not acceptable for .

6 Restrictions of transfers

6.1 Restrictions of transfers and the total risk

In the general single currency setting, the sets of admissible terminal portfolios are sandwiched between the strictly granular approach and unconstrained approach. Which IGTs are accepted as admissible is not primarily a mathematical question. In the sequel we show how considerations regarding solvency assessment, transaction costs, and some sources of risks might be reflected in the design of the set of admissible IGTs.

The choice corresponds to the unconstrained risk assessment and so yields the largest possible set of admissible IGTs in the single currency setting.

The monotonicity property from Proposition 4.1 in a coherent case yields that, under any restrictions, the group will never achieve better risks comparing to those obtained by performing the unconstrained solvency test approach. This is formalized in the following proposition.

Proposition 6.1

Let be a -integrable random vector and let for a convex -risk measure . If is any family of admissible IGTs, then the corresponding total risk is at least , which is the total risk of the unconstrained solvency test.

A restriction of increases the complexity of the set-valued solvency tests considerably. In view of that it is natural to ask whether the impact on the resulting capital requirements is material or not compared to the unconstrained and strictly granular approaches.

Proposition 6.2

Assume that for a coherent -risk measure . If the unconstrained total group risk does not increase by restricting the transfers to , then, for some with , the set contains a -integrable selection such that

| (6.1) |

Proof

If the total risk in the restricted setting does not increase in comparison with the unrestricted one, then there exists with , such that

for a selection of . The monetary property yields that

and the subadditivity property together with yield the equality.

6.2 No transfers causing or worsening bankruptcy

For any policy holder, one of the most important events to be avoided is bankruptcy of their counter-party. Hence, in order to balance the interests of all policy holders of all legal entities within the group, a natural restriction for admissible IGTs could be to exclude transfers that exceed the capital of a legal entity, if this capital is positive. Furthermore, it could also be argued that it would not be in line with policy holder interests of the bankrupt company if their bankruptcy’s dividend were reduced by intragroup transactions. It is also clear that fungibility is dramatically restricted in case of bankruptcy, e.g. to a certain bankruptcy’s dividend if legally binding and enforceable intragroup contract exist. Hence, in order to at least partially protect policy holder interests of a bankrupt subsidiary and in order to include some fungibility aspects it seems reasonable to prohibit transfers out of a company with negative capital.

To sum up, there are several reasons to exclude transfers turning a non-bankrupt legal entity into a bankrupt one and also transfers out of a bankrupt one to another one (from the same group). We use the abbreviation NTB (No Transfers causing or worsening Bankruptcy) for this kind of IGTs. Here we make the simplifying assumption that bankruptcy is defined with respect to the terminal capital position and not with respect to a different balance sheet, i.e. transfers may not turn a non-negative component of into a negative one.

The corresponding set of attainable positions is given by

where for . Note that (4.2) holds in this case and non-linearly depends on . Furthermore, is -integrably bounded and upper semicontinuous, so that and the group risk are closed sets in the coherent case, see Proposition 4.2.

For a group consisting of two agents, the set of terminal positions has vertices at and , see Figure 1. Therefore,

| (6.2) |

for .

6.3 Safety margin

Allowing transfers to vanishing capital for some agents (as it is possible under NTB) may still be considered too progressive, since the agents might end up with no capital buffer after IGTs, i.e. they are almost bankrupt. In view of that it is worth noticing that requirements on admissible IGTs can be made more stringent if the set is replaced by for a fixed vector with non-negative components that set safety margins for terminal capital amounts. If , then

so that the group risk is obtained by inverting the selection risk measure at point , cf. (4.3).

In the case of proportional safety margins, is replaced by , where for .

6.4 Fungibility costs

So far we have assumed that capital can be transferred either in full or not at all. Due to fungibility constraints, the capital may only flow via complicated constructs that involve taking loans and cause serious future fungibility costs, in particular for transitional funding. This can be included in our framework by adapting the set of attainable terminal positions.

In the interest of brevity, we illustrate the construction with the help of a bivariate example. In the single currency setting is a curve that passes through and has slope at that point if . The fungibility difficulties may be modeled by changing the slope of this line according to increasing fungibility costs for agents with low capital. If the capital amounts of the firms are large, and the transfers are small (so that the capital amounts after transfer exceed thresholds and ), it is well possible that fungibility costs from one company to another one vanish. However, if the capital of a company is small and the transfer is relatively large, then this can cause serious fungibility costs, which are getting larger the closer the company comes to bankruptcy after a transfer. Then e.g. for a modified NTB setting the boundary can be modeled using two differential equations

| (6.3) |

depending on whether we want to transfer money from the second to the first company (first equation, , in the considered modified NTB setting only relevant if ), or from the first to the second company (second equation, , in the considered modified NTB setting only relevant if ). Close to bankruptcy, the fungibility costs become immense and for all non-positive values of capital of the donor company no transfer is possible anymore. The parameter can be used for calibration to the company specific situations. The solution of these two equations together with the initial condition produces a curve on the plane that yields . Note that satisfies (4.2).

6.5 Transaction costs

Consider the case, where transfers are subject to transaction costs, however unrestricted otherwise. In case of proportional transaction costs, each recipient surrenders a proportion of the amount determined by a factor . For simplicity, we assume to be deterministic and the same for all legal entities. For two legal entities, the set of admissible IGTs for proportional transaction costs is

which is a convex cone that does not depend on the capital position . The corresponding risks have been studied in depth in ham:hey10 ; ham:hey:rud11 and cas:mol14 . The results of these papers for deterministic exchange cones apply in our setting. In particular, is the selection risk measure of the set-valued portfolio .

In case of fixed transaction costs, each recipient surrenders a fixed amount , so that

This provides an example of a non-convex set of IGTs that also does not depend on .

A particularly important case of transaction costs relates to the case where agents operate in different currencies. Then transfers between the currencies are subject to transaction costs and may also involve random exchange rates. In this case, it is also problematic to consider the total risk, since there is no natural reference currency to express the risks of all agents. We leave this setting for future work.

7 Unequally placed agents

Most financial groups exhibit some hierarchical structures, namely there are parent and subsidiary agents, and even cross-holdings between different members of the same group often exist. For simplicity, consider the case of two agents: the first agent with capital is a subsidiary and the second one with capital is a holding (or parent). The parent company owns an option on the (full) available capital of the subsidiary, e.g. via liquidation, i.e. the parent has a long position in the derivative with payoff . Assume that the parent has no other assets or liabilities, so that her capital is .

In this case, adding capital amounts would incur double counting of the positive part of . Such double counting is typically excluded in previous works on optimal risk sharing, see fil:kun08 . In our framework, it is possible to avoid double counting by adjusting the random set of attainable positions.

In view of the fact that a parent company ultimately has the legal right to get the (full) capital from the subsidiary, without an additional contract the parent can add the positive part of the capital of the subsidiary to its assets, and hence, to its capital. Consequently the subsidiary acquires the corresponding short position, which has to be considered in the risk calculation of the subsidiary, so that its consistent capital becomes , where is the so-called limited liability put option. Thus, the net capital of the subsidiary is never strictly positive, for instance, the subsidiary would never be acceptable, except in cases where the capital of the subsidiary after taking into account the participations is concentrated at zero, which might happen, if the subsidiary were “long only” in assets while being completely financed by equity.

For the capital position , in the strictly granular setting the random set of attainable positions is given by

so that . Assume that the risks of the both group members are assessed using the same coherent risk measure . Thus, in the strictly granular setting, the total risk amounts to

Allowing for IGTs, for any state of the world one has to fix the transfer from the parent to the subsidiary, which is the only feasible transfer direction. For this, the parent obtains a loan secured upon , and we do not take into account any fungibility difficulties that might occur in this relation. From this loan a random amount is due to be transferred to the subsidiary at the terminal time. If , then the transferred amount is immediately recovered and the loan is repaid, while if , then the parent recovers . The set of attainable positions is characterized by given by for all possible transfers , which are random variables taking values in . The corresponding “total risk” becomes

in view of the subadditivity of the risk measure. In the hypothetical case of an unlimited credit line, the equality, and thus, the optimal transfer is achieved if .

The policy holders of a parent could benefit from the investment in the subsidiary without directly affecting reserves of the policy holders of the subsidiary, if the parent sells the subsidiary at the terminal time to a third party. Since this strategy needs a buyer in a potentially stressed market it is possibly, from the initial time point of view, recommendable not to fully take into account this possibility in a prudent regulation.

8 Diversification effects

Filipović and Kunz fil:kun08 present a bottom-up approach to analyse intragroup diversification in a very concrete setting with given distributions and choice of predefined IGTs. For a rather recent similar analysis, see also mas13 .

The key property of coherent risk measures is their subadditivity that corresponds to the fact that diversification decreases risk. The non-linear feature of the IGTs brings new features to the diversification effects. For example, in many cases, e.g. in the NTB case,

| (8.1) |

where both and are -dimensional vectors of capital values. Then the diversification of assets and liabilities narrows the range of admissible IGTs. On the other side, there exists a classical benefit from diversification effects. A similar situation arises in the diversification effects for systemic risks, see fein:rud:web15 .

Example 8.1 (Univariate case)

In order to understand the diversification effects in the group setting, consider the one-dimensional case from the point of view of the group. Let and be two -integrable random variables and let be a univariate coherent -risk measure. Define to be a random vector in and let . In view of the subadditivity of the total risk of with the IGTs given by equals , while if , then the total risk becomes . Thus, the classical diversification benefit can be phrased as the advantage that corresponds to increasing the set of admissible IGTs from to , in other words, from altering the strictly granular approach to the unconstrained one. Related to that, it should be stressed that a solvency test should never include unrealistic transfers, since otherwise the solvency test tends to underestimate the real risks a group is faced with. Furthermore, it should be noted that classical diversification compares with the risk of a particular selection of , namely that of .

The classical concept of diversification is inherent for a single agent, who might have several business units with unrestricted capital flows between them. In case of groups, we see two basic effects:

-

•

consolidation that amounts to increasing the set of admissible IGTs;

-

•

granularization that corresponds to restricting the family of admissible IGTs.

In particular, a merger of two legal entities removes all fungibility barriers between them, as in the case of unconstrained approach, and so is a simple example of consolidation. On the contrary, a split may lead to some additional restrictions in capital transfers that can be viewed as granularization.

Example 8.2

Consider the group and assume that the first agent splits its operation into two subsidiaries so that . The effect of such granularization on the total risk depends on the set of admissible transfers between the two created subsidiaries and between them and the rest of the group. For instance, the total risk is retained if the two subsidiaries are considered on the unconstrained basis.

Example 8.3

Consider a single agent with terminal capital that is split into , so that . The total risk after such granularization under a coherent risk measure lies between in the unconstrained case and in the strictly granular setting.

Example 8.4

If two groups are merged, a classical question is, whether or not also some of the legal entities (like two life- or non-life companies) should also be merged. Consider two groups and . Their merge creates a new group with legal entities, so that one has to specify the family of admissible IGTs. It is natural to assume that and , meaning that the families and of admissible IGTs within each of two primary groups are admissible after the merge. Still the larger group may be allowed to transfer capital between the components of and . In view of this,

Note that the coherence of components of is not needed for this. Hence, if two groups are merged without any merger of the legal entities we can expect (e.g. if the above assumptions are satisfied) the total risk to be subadditive. However, if we start to merge also legal entities, the situation is less clear due to reverse effects from (8.1).

Thus, in the context of risk assessment for groups, the diversification advantage can be formulated as follows.

Granularization does not diminish the risk, while consolidation does not increase the risk.

This fact is the sole monotonicity property of the set of admissible IGTs and does not rely on the subadditivity property of the involved risk measures.

9 Calculating the group risk

The calculation of the group risk requires finding such that the selection risk measure of contains the origin. This is a serious computational problem, that can be solved by means of multicriterial optimization algorithms, see e.g. ham:rud:yan13 . However, bounds on the group risk can be obtained as follows, see Theorem 3.2.

Proposition 9.1

Let be a coherent -risk measure with identical components. Let be any selection of for . Then

| (9.1) |

In the following, assume that has all identical coherent components. In case of two agents, the calculation of the superset for the group risk can often be simplified by the following proposition.

Proposition 9.2

Assume that is almost surely convex in with . Then the superset in (9.1) does not change if the intersection is reduced to .

Proof

It suffices to show that if for the three above mentioned , then the inequality holds for all . Without loss of generality assume that . The condition means that is the segment with two end-points and , where are two non-negative random variables that might depend on . Then

If , then

The coherency of the risk measure yields that the risk of is acceptable if both and are. The case of is similar.

In the following we choose the NTB restrictions for two agents, possibly with safety margins, where Proposition 9.2 clearly applies. In case of a fixed safety margin , the group risk is a subset of

| (9.2) |

Note that the last inequality defines a half-plane corresponding to the unconstrained setting. In the case of zero safety margin, the first two inequalities are superfluous, and so the superset from Proposition 9.1 does not differ from the group risk in the unconstrained setting. Indeed, if , then without loss of generality we can assume the equality, so that . Then the first inequality in (9.2) requires

or, equivalently,

which always holds, since .

In order to obtain a subset of , choose the selection as the point of that is nearest to the diagonal line . Then if . If , then in case , if , and if . Thus, is acceptable if

The inner approximation in (9.1) is obtained as the set of all such that the above inequalities hold with replaced by , where denotes the fixed safety margin. An upper bound for the total risk is obtained by finding the minimum of that satisfy these inequalities.

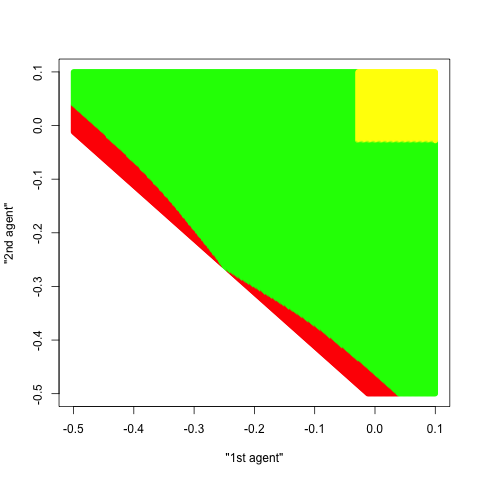

Example 9.1

Consider the NTB setting without safety margin and with as the underlying risk measure. Figure 2(a) shows the superset and the subset of the group risk for i.i.d. having the uniform distribution on . The outer bound equals the group risk in the unconstrained setting. The upper right corner shows the group risk in the strictly granular case. While the bounds for given by Proposition 9.1 clearly differ, they both yield the same value of the total risk. This means that the total risk in the NTB setting for this example coincides with the unconstrained group risk. While the same phenomenon appears in all simulated examples with exchangeable , we do not have a theoretical confirmation of this observation.

Figure 2(b) shows the bounds for the group risk in case has the standard normal distribution independent of having the exponential distribution of mean one. In this case the inner approximation to the group risk does not touch the outer approximation, however close they are.

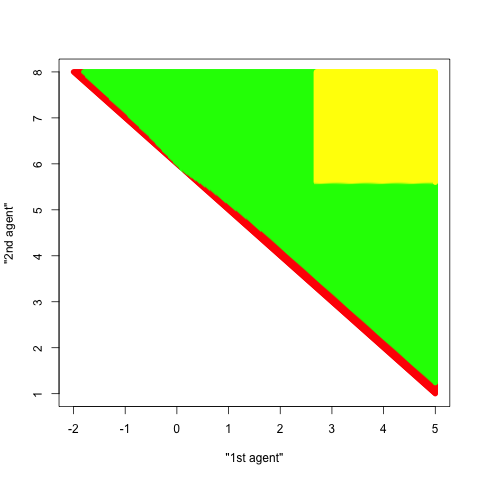

Example 9.2

Take and let be normally distributed with mean zero and the covariance matrix

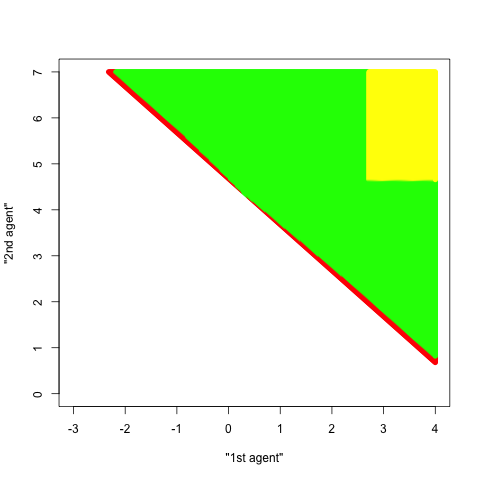

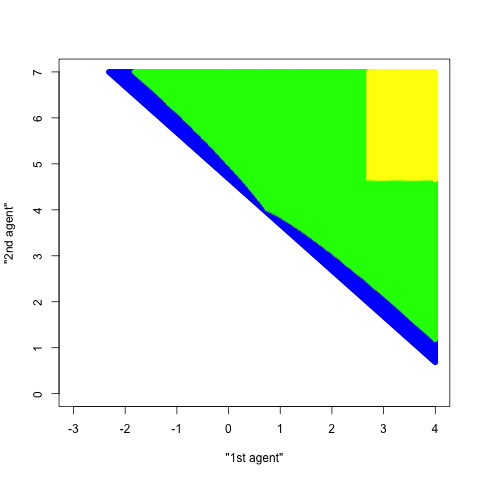

Figure 3(a) shows approximations to the group risk without safety margin. Here the outer approximation coincides with the group risk in the unconstrained setting, while the inner approximation touches it and so shows that the total risk in the NTB setting coincides with the unconstrained total risk. Figure 3(b) shows the results for the fixed safety margin set to for the both agents. In this case the outer approximation in (9.1) coincides with the inner approximation and so yields the group risk. The outer set corresponds to the unconstrained setting. An indication for the high potential of IGTs for intragroup diversification is seen by comparing the strictly granular group risk (shown in yellow) with other ones.

References

- (1) Acciaio, B.: Optimal risk sharing with non-monotone monetary functionals. Finance and Stochastics 11, 267–289 (2007)

- (2) Acciaio, B., Svindland, G.: Optimal risk sharing with different reference probabilities. Insurance Math. Econom. 44, 426–433 (2009)

- (3) Amini, H., Filipović, D., Minca, A.: Systemic risk with cetral counterparty clearing. Research paper series 13-34, Swiss Finance Institute (2013)

- (4) Asimit, A.V., Badescu, A.M., Tsanakas, A.: Optimal risk transfers in insurance groups. Eur. Actuar. J. 3, 159–190 (2013)

- (5) Aubin, J.P., Frankowska, H.: Set-Valued Analysis, System and Control, Foundation and Applications, vol. 2. Birkhäuser, Boston (1990)

- (6) Barrieu, P., El Karoui, N.: Inf-convolution of risk measures and optimal risk transfer. Finance and Stochastics 9, 269–298 (2005)

- (7) Barrieu, P., Scandolo, G.: General Pareto optimal allocations and applications to multi-period risks. Astin. Bull. 38, 105–136 (2008)

- (8) Delbaen, F.: Monetary Utility Functions. Osaka University Press, Osaka (2012)

- (9) Feinstein, Z., Rudloff, B., Weber, S.: Measures of systemic risk. Tech. rep., arXiv:1502.07961v2 [q-fin.RM] (2015)

- (10) Filipović, D., Kunz, A.: Realizable group diversification effects. Life & Pensions pp. 33–40 (2008, May)

- (11) Filipović, D., Kupper, M.: On the group level Swiss Solvency Test. Bulletin of the Swiss Association of Actuaries 1, 97–115 (2007)

- (12) Filipović, D., Kupper, M.: Optimal capital and risk transfers for group diversification. Math. Finance 18, 55–76 (2008)

- (13) Filipović, D., Svindland, G.: Optimal capital and risk allocations for law- and cash-invariant convex functions. Finance and Stochastics 12, 423–439 (2008)

- (14) Gerber, H.U.: An Introduction to Mathematical Risk Theory, Huebner Foundation Monograph, vol. 8. Wharton School, University of Pennsylvania (1979)

- (15) Hamel, A.H., Heyde, F.: Duality for set-valued measures of risk. SIAM J. Financial Math. 1, 66–95 (2010)

- (16) Hamel, A.H., Heyde, F., Rudloff, B.: Set-valued risk measures for conical market models. Math. Finan. Economics 5, 1–28 (2011)

- (17) Hamel, A.H., Rudloff, B., Yankova, M.: Set-valued average value at risk and its computation. Math. Finan. Economics 7, 229–246 (2013)

- (18) Jouini, E., Schachermayer, W., Touzi, N.: Optimal risk sharing for law invariant monetary utility functions. Math. Finance 18, 269–292 (2008)

- (19) Kabanov, Y.M., Safarian, M.: Markets with Transaction Costs. Mathematical Theory. Springer, Berlin (2009)

- (20) Kaina, M., Rüschendorf, L.: On convex risk measures on -spaces. Math. Meth. Oper. Res. 69, 475–495 (2009)

- (21) Keller, P.: Group diversification. Geneva Pap 38, 382–392 (2007)

- (22) Kiesel, L., Rüschendorf, L.: On optimal allocation of risk vectors. Insurance Math. Econom. 47, 167–175 (2010)

- (23) Lépinette, E., Molchanov, I.: Risk arbitrage and hedging to acceptability. Tech. rep., arXiv:1605.07884 [q-fin.RM] (2016)

- (24) Luder, T.: Modelling of risks in insurance groups for the Swiss Solvency Test. Bulletin of the Swiss Association of Actuaries 1, 85–96 (2007)

- (25) Masayasu, K.: Insurance group risk management model for the next-generation solvency framework. APJRI 7, 27–52 (2013)

- (26) Molchanov, I.: Theory of Random Sets. Springer, London (2005)

- (27) Molchanov, I., Cascos, I.: Multivariate risk measures: a constructive approach based on selections. Math. Finance 26, 867––900 (2016)

- (28) Ravanelli, C., Svindland, G.: Comonotone Pareto optimal allocations for law invariant robust utilities on . Finance and Stochastics 18, 249–269 (2014)

- (29) Wang, R.: Subadditivity and indivisibility (2014). Preprint, University of Waterloo