Demand Response with Communicating Rational Consumers

Abstract

The performance of an energy system under a real-time pricing mechanism depends on the consumption behavior of its customers, which involves uncertainties. In this paper, we consider a system operator that charges its customers with a real-time price that depends on the total realized consumption. Customers have unknown and heterogeneous consumption preferences. We propose behavior models in which customers act selfishly, altruistically or as welfare-maximizers. In addition, we consider information models where customers keep their consumption levels private, communicate with a neighboring set of customers, or receive broadcasted demand from the operator. Our analysis focuses on the dispersion of the system performance under different consumption models. To this end, for each pair of behavior and information model we define and characterize optimal rational behavior, and provide a local algorithm that can be implemented by the consumption scheduler devices. Analytical comparisons of the two extreme information models, namely, private and complete information models, show that communication model reduces demand uncertainty while having negligible effect on aggregate consumer utility and welfare. In addition, we show the impact of real-time price policy parameters have on the expected welfare loss due to selfish behavior affording critical policy insights.

I Introduction

00footnotetext: C. Eksin is with the School of Electrical and Computer Engineering and the School of Biological Sciences at the Georgia Institute of Technology, Atlanta, GA. H. Deliç is with the Wireless Communications Laboratory, Department of Electrical and Electronics Engineering, Boğaziçi University, Bebek 34342 Istanbul, Turkey. A. Ribeiro is with the Department of Electrical and Systems Engineering, University of Pennsylvania, Philadelphia, PA. Work supported by NSF CAREER CCF-0952867, NSF CCF-1017454, and the Boğaziçi University Research Fund under Grant 13A02P4.Demand response management (DRM) emerges as a prominent method to alleviate the complications in power balancing caused by uncertainties both on the consumer and the supply side. Changes in user consumption preferences create the uncertainty on the consumer side while the uncertainty on the supply side is due to renewable resources. DRM refers to the system operator’s effort to improve system performance by shaping consumption through pricing policies. Smart meters that can control the power consumption of customers, and enable information exchange between meters and the system operator (SO) provide the infrastructure to implement these policies.

Real-time pricing (RTP) is a pricing policy where the price depends on instantaneous consumption of the population [1, 2, 3]. In RTP, the SO shares part of the risk and reward with its customers by setting price based on the total consumption. In these models, it is natural to propose game-theoretic models of consumption behavior, where users strategically reason about the behavior of others to anticipate price and determine their individual consumption [1, 2, 3, 4, 5, 6, 7, 8]. The specifics of the behavior model and the information available impact the system welfare and is critical in assessing the benefits or disadvantages of a pricing scheme [8, 9]. Given an RTP mechanism, our goal in this paper is to characterize rational price-anticipatory behavior models under different information exchange schemes, and comparatively assess their impact on system performance measures.

We consider an RTP scheme in which customers agree to a price function that increases linearly with total consumption and that depends on an unknown renewable energy parameter (Section II-A). The individual customer utility at each time depends on the individual’s consumption preference and price both of which are in general unknown to others (Section II-B). Initially, the SO sends public information on its estimate of population’s consumption preferences and renewable source generation. Customers use the public information and their self-preferences to anticipate total consumption and renewable source’s effect on price, and respond rationally by consuming according to a Bayesian Nash equilibrium (BNE) strategy. In [10], based on this energy market model, we propose and show the effectiveness of a peak-to-average ratio (PAR)-minimizing pricing strategy.

In this paper we explore the effects of different consumer behavior models, where consumers respond rationally regarding their individual utility, the population’s aggregate utility or the welfare (Section II-C). As time progresses, past consumption decisions contain information about the preferences of others which individuals can use to make more informed decisions in the current time. Based on this observation, we propose three information exchange models, namely, private, action-sharing and broadcast (Section II-D). In the private model, users do not receive any information besides the initial public signal by the SO. In action-sharing there exists a communication network on which users exchange their latest consumption decisions with their immediate neighbors. In broadcasting, the SO broadcasts the total consumption after each time step. We assume that the customer’s power control scheduler can adjust the load consumption between time steps according to its preferences and information. That is, we are interested in modeling consumption behavior for shiftable appliances, e.g., electric vehicles, electronic devices, air conditioners, etc. [11]. We formulate each consumer behavior model and information exchange model pair as a repeated game of incomplete information and characterize BNE behavior (Section IV). We use the explicit characterization to rigorously analyze the effects of each pair of behavior and information exchange model on demand, aggregate user utility and welfare respectively in Sections V-VII. These sections present analytical derivations for the results shown numerically in [12]. In addition, we provide additional simulation results on sensitivity of the performance metrics with respect to the renewable energy parameter term in the price.

Our findings can be summarized as follows. While providing more information to the consumers through action-sharing or broadcasting models does not have a significant impact on the expected aggregate utility or on the welfare, which is defined as the sum of aggregate utility and the operator’s net revenue, it reduces the uncertainty in total demand. Action-sharing and broadcasting information exchange models eventually achieve the expected utility under complete information when the communication network is connected. Furthermore, while in a private information model increased correlation among preferences increases the demand uncertainty, in the broadcast model the demand variance tends to decrease with increasing correlation. When we consider the effects of behavior models –selfish, altruistic, or welfare maximizers,– we show that altruistic behavior achieves the highest expected aggregate utility and welfare maximizers achieve the highest expected welfare. Furthermore, we characterize the expected improvement in the considered performance metric with respect to selfish behavior model in terms of pricing parameters. Finally, we show that increased correlation among user preferences tends to adversely affect aggregate utility and welfare. We discuss the possible policy implications of these findings for the operator and policy makers in Section VIII.

II Demand Response Model

There are customers, each equipped with a power consumption scheduler. Individual power consumption of at time is denoted by . The total power consumed by customers at time is .

II-A Real-time pricing

The SO implements an adaptive pricing strategy whereby customers are charged a slot-dependent price that varies linearly with the total power consumption . The SO has a set of renewable source plants at its dispatch and incorporates renewable generation into the pricing strategy by a random renewable power term that depends on the amount of renewable power produced at time slot . The per-unit power price in time slot is set as

| (1) |

where is a policy parameter to be determined by the SO based on its objectives. The random variable is such that when renewable sources operate at their nominal benchmark capacity . If the realized production exceeds this benchmark, , the SO agrees to set to discount the energy price and to share its revenue from the windfall. If the realized production is below benchmark, i.e., , the SO sets to reflect the additional charge on the customers. The specific dependence of on the realized energy production and the policy parameter, , are part of the supply contract between the SO and its customers.

We assume that the SO uses a model on the renewable power generation – see, e.g.,[13] for the prediction of wind generation – to estimate the value of at the beginning of time slot . The mean estimate of the corresponding probability density function is made available to all customers prior to the time slot. We do not make any assumptions on the accuracy or the structure of these forecasts. Inclusion of a renewable dependent term in the price functions allows the operator to use the flexibility of consumption behavior to compensate for peaks in conventional energy reserves caused by intermittent renewable generation [14, 15, 16, 13]. We discuss its possible implications further in Section VIII.

The operator’s price function maps the amount of energy demanded to the market price. Observe that the price at time becomes known after the end of the time slot. This is because price value depends on the total demand and the value of which are unknown a priori. The SO can employ the pricing policy in (1) to achieve certain system performances, e.g., minimizing PAR, maximizing welfare, etc., by picking its policy parameter [10].

II-B Power consumer

User ’s consumption at time slot , , depends on his consumption preference , modeled as a random variable that may vary across time slots. When user consumes , its consumption utility increases linearly with its preference and decreases quadratically with a constant term , described as . The utility of at time slot is then captured by the difference between the consumption utility of and the monetary cost of consumption :

| (2) |

Note that even if the SO’s policy parameter is set to , the utility of user is maximized by . Note that we choose to be homogeneous among the consumers. Our results extend to the case where the constant is heterogeneous.

The utility of user depends on the total power, , consumed at , which implies that it depends on the powers that are consumed by other users in the current slot, denoted by . Power consumption of others, , depends partly on their respective self-preferences, i.e., preferences , which are, in general, unknown to user . We assume, however, that there is a probability density function on the vector of self-preferences from which these preferences are drawn. We further assume that is normal with mean where and is an vector with one in every element, and covariance matrix :

| (3) |

We use the operator to signify expectation with respect to and to denote the th entry of the covariance matrix . Having mean implies that all customers have equal average preferences in that for all . If for some pair , it means that the self-preferences of these customers are uncorrelated. In general, to account for correlated preferences due to, e.g., common weather. We assume that if there is a change in the consumption preferences from one time slot to the other, then the self-preferences and for different time slots are independent.

At the beginning of time slot , we assume that in (3) is correctly predicted by the SO based on past data and is announced to the customers. The SO also announces its policy parameter and its expectation of the renewable term . In addition, each customer knows its own consumption preference .

II-C Consumer behavior models

Consumption behavior determines the population’s aggregate utility at time ,

| (4) |

The net revenue of the SO is its revenue minus the cost

| (5) |

where is the cost of supplying Watts of power. When the generation cost per unit is constant, is a linear function of . More often, increasing the load results in increasing unit costs as the SO needs to dispatch power from more expensive sources. This results in superlinear cost functions with an approximate model being the quadratic form111It is possible to add linear and constant cost terms to and have all the results in this paper still hold. We exclude these terms to simplify notation.

| (6) |

for a given time dependent constant normalized by number of consumers . The cost in (6) has been experimentally validated for thermal generators [20], and it is otherwise widely accepted as a reasonable approximation [2, 1, 6]. The welfare of the overall system at time is the sum of the aggregate utility with the net revenue,

| (7) |

Consumer behavior can be selfish, altruistic or welfare-maximizing. User is selfish when it wants to maximize its individual utility in (2). It is altruistic when it considers the well-being of other users, that is, aims to maximize in (4). Finally, user might also consider the well-being of the whole system and aim to choose his consumption behavior to maximize the welfare in (7) given its information. We use the superscript {S, U, W} in to indicate that the consumer maximizes its selfish payoff S, aggregate utility U or the welfare W. All of these behavior models require strategic reasoning about the behavior of others which constitutes a Bayesian game. Bayesian games model interactions where users have incomplete information about the utility of others. Below we formalize a range of information exchange models.

II-D Information models

Consumption preference profile is partially known by the individuals. Consumption decisions of individuals at time can provide valuable information about these consumption preferences. This information is of use to consumer in estimating consumption for the next time slot if the preferences of the users do not change in that time slot, that is, . Otherwise, the information at time is not helpful in estimating the behaviors of others for time slot because we assume the change in the preference distribution to be independent. We let an uninterrupted sequence of time slots in which agents have the same consumption preference profile define a time zone. Formally, a time zone is defined as for a preference profile with prior probability density function where is ‘and’ operator and is ‘or’ operator. Next, we present a set of possible information exchange models within a time zone . We use to denote the set of information available to consumer at time slot for the information exchange model .

-

Private.

The information specific to consumers is the merest possible when it consists of the private preference , for .

-

Action-Sharing.

Power control schedulers are interconnected via a communication network represented by a graph with its nodes representing the customers and edges belonging to the set indicating the possibility of communication. User observes consumption levels of his neighbors in the network after each time slot. The vector of ’s neighbors is denoted by . Given the communication set-up, the information of user at time slot contains its self-preference and the consumption of his neighbors up to time , that is, where we define the actions of ’s neighbors at time by and denote the starting time slot of with . We assume that the power consumption schedulers keep the information received from neighbors private and know the network structure .

-

SO Broadcast.

The SO collects all the individual consumption behavior at each time and broadcasts the total consumption to all the customers, that is, .

When the time zone ends, we restart the information exchange process. The prediction of renewable source term is allowed to vary for . Behavior model, {S, U, W}, and the information exchange model, {P, AS, B}, determine the consumption decisions of user . In the following, we define the rational consumer behavior in Bayesian games within a time zone and then characterize the rational behavior for each behavior and information exchange model pair ().

III Bayesian Nash equilibria

User ’s load consumption at time is determined by his strategy that maps his information to a consumption level. This map depends on the belief of which is a conditional probability on and given its information, . We use to indicate conditional expectation with respect to its belief. While the model can account for the correlation between the random variables and , we assume that they are independent. In order to second-guess the consumption of other customers, user forms beliefs on preferences given the common prior and its information . User ’s load consumption at time is determined by its strategy which is a complete contingency plan that maps any possible local observation that it may have to its consumption; that is, for any . In particular, for user , its best response strategy is to maximize its expected utility given the strategies of other customers ,

| (8) |

Before we define the Bayesian Nash equilibrium (BNE) solution, we introduce the following lemma which characterizes the general form of the best response function for all the behavior models {S, U, W}.

Lemma 1

The best response strategy of to the strategies of others has the following general form for any behavior model

| (9) |

where are constants that take values based on the behavior model . If then . If then , . If then , , .

The proof follows by taking the derivative of the corresponding utility with respect ’s consumption , equating to zero and solving the equality for . Note that when and , the altruistic users have the same best response function as the welfare-maximizers. A BNE strategy profile for the game is a strategy in which each user maximizes its expected utility with respect to its own belief given that other users also maximize their expected utility [21, Ch.6].

Definition 1

A BNE strategy for the consumer behavior model is such that for all , , and ,

| (10) |

for any .

A BNE strategy (10) is computed using beliefs formed according to Bayes’ rule. Note that the BNE strategy profile is defined for all time slots. No user at any given time slot within has a profitable deviation to another strategy.

In (10), consumers estimate consumption decisions of others to respond optimally. Equivalently, a BNE strategy is one in which users play best response strategy given their individual beliefs as per (8) to best response strategies of other users – see [22, 23] for similar equilibrium concepts. As a result, the BNE strategy is defined by the following fixed point equations:

| (11) |

for all , , and . We denote ’s realized load consumption from the equilibrium strategy and information with . Using the definition in (11), we characterize the unique linear BNE strategy in the next section for any information exchange and consumer behavior model.

IV Consumers’ Bayesian Game

It suffices for customer to estimate the self-preference profile in order to estimate consumption of other users [22]. We define the self-preference profile augmented with mean as . The mean and error covariance matrix of ’s belief at time are denoted by and , respectively. The next result shows that there exists a unique BNE strategy that is a linear weighting of the mean estimate of for any information model . Furthermore, the weights of the linear strategy are obtained by solving a set of linear equations specific to the behavior model .

Proposition 1

Consider the Bayesian game defined by the payoff for . Let the information of customer at time be defined by the information exchange model . Given the normal prior on the self-preference profile , user ’s mean estimate of the preference profile at time can be written as a linear combination of . That is, where for all , and the unique equilibrium strategy for is linear in its estimate of the augmented self-preference profile,

| (12) |

where and are the strategy coefficients. The strategy coefficients are calculated by solving the following set of equations for the consumer behavior models

| (13) |

and

| (14) |

where are as defined in Lemma 1 for , and is the unit vector.

Proof : 222The proof is adopted from Proposition 1 in [22].Our plan is to propose a linear strategy and use the general form of the best response function (9) in the fixed point equations (11) to obtain the set of linear equations. We prove by induction. Assume that users have linear estimates at time , for all . We propose that users follow a strategy that is linear in their mean estimate as in (12). Using the fixed point definition of BNE strategy in (11), we have

| (15) |

for all from Lemma 1. The summation above includes user ’s expectation of user ’s expectation of the augmented preferences. By the induction hypothesis, we write this term as

| (16) |

Substituting the above equation for the corresponding terms in (15) and using the induction hypothesis for the expectation term on the left-hand side yields the set of equations

| (17) |

We equate the terms that multiply and the constants to obtain the set of equations in (13) and (14), respectively.

Since user consumption is based on its BNE strategy at time , it is linear in its estimate of the preferences; i.e., for all . We can then express the observations of user as a linear combination of by defining the observation matrix for any information exchange model . For the private information model, the observation matrix is zero, i.e., for any . For the action-sharing information model, the observations of consumer can be written using the observation matrix

| (18) |

and the vector , as Finally, when the SO broadcasts the total consumption , the observation matrix is a vector

| (19) |

and the total consumption can be written as Because the prior distribution on the preferences are Gaussian, the observations of user are Gaussian for all information exchange models . As a result, we can use a Kalman filter with gain matrix

| (20) |

to propagate mean beliefs in the following way:

| (21) |

We use the induction hypothesis for the first term on the right hand side of (21) and rearrange terms to get

| (22) |

Note that the mean estimate at time is a linear combination of . Specifically, we can express the linear weights of the mean estimate at time slot as

| (23) |

where the mean estimate is , completing the induction argument. Similarly, the updates for error covariance matrices follow standard Kalman updates [24, Ch. 12]

| (24) |

At the starting time slot , we have . Hence the induction assumption is true initially and for all .

Since the stage game has the same pay-off structure and the information is Gaussian, it suffices to show uniqueness for the stage game. The uniqueness of the stage game is proven in Proposition 1 in [10]. See also Proposition 2.1 in [25]. ∎

Proposition 1 presents how BNE consumption strategies are computed at each time slot. Accordingly, the scheduler repeatedly determines its consumption strategy given consumption behavior model and available information, receives information based on the information exchange model at the end of the time slot, and propagates its beliefs on self-preference profile to be used in the next time slot. For each consumption behavior {S, U, W} the user solves a different set of equations in (13)-(14) derived from the fixed point equations of the BNE (11). For Private information exchange model, users do not receive any new information within the horizon hence their mean estimate of do not change, that is, for , which implies the set of equations (13)-(14) need to be solved only once at the beginning to determine the strategy for the whole time horizon. For Action-Sharing information exchange model, upon observing actions of its neighbors, user has new relevant information about the preference profile which it can use to better predict the total consumption in future steps. Similarly in SO Broadcast model, each user receives the total consumption at each time which is useful in estimating total consumption in the following time slot.

The Bayesian belief propagation for Gaussian prior beliefs corresponds to Kalman filter updates at each step for any information exchange model. In particular, beliefs remain Gaussian and the mean estimates are linear combinations of private signals at all times for any information exchange model. In order to compute the BNE strategy, it does not suffice for scheduler to form beliefs on the preference . It also needs to keep track of beliefs of others. Knowing the estimate of all the other schedulers is not possible for . However, this is not required to compute an estimate of other schedulers’ estimates. It is only required that user knows how other schedulers compute their mean estimates which implies knowing the estimation weights . Even though scheduler does not know , it can keep track of via the weight recursion equation in (23), which can be computed using public information. Note that cannot compute self-mean estimate of preferences, , via multiplying by since this computation would require knowledge of . Instead, user computes its mean estimate by a Kalman filter. We detail the local computations of a scheduler in Algorithm 1.

In Algorithm 1, we provide a local algorithm for user to compute its consumption level and propagate its belief given a behavior model {S, U, W} and the information exchange model AS. We point to modifications specific to the other information exchange models here in our explanation. User initializes its belief on at the beginning of the time zone according to the preference distribution in (3). It also determines the estimation weights and error covariance matrix at the beginning for . Note that user does not need any local information from other users in this initialization. Using the estimation weights , it can locally construct the equations in (13) and (14), and solve for the strategy coefficients . In Step 2, consumes the amount based on its local estimate of the augmented self-preferences – see (12).

Once the consumption occurs, the information becomes available according to the information exchange model . At this point, if the upcoming time slot has the same prior preference distribution (3) as , that is, if , propagates its belief on the self-preference profile given the new information. The propagation of beliefs starts by computing observation matrices of all the users in Step 3 based on the information exchange model . When the model is action-sharing, AS, each observed action is a linear combination of with the observation matrix computed by (18). If the model is broadcast, B, the observation matrix is a vector computed by (19). If the model is private, P, there is no new information available hence scheduler goes back to Step 2 with the same strategy coefficients. Next, uses these observation matrices in computing the gain matrices in Step 4 of all the users. In Step 5, propagates the estimation weights and error covariance matrix . Note that in Steps 3-5 user does a full network simulation in which it emulates the Kalman filter estimates of everyone using public information, that is, estimation weights , strategy coefficients and network topology . Finally in Step 6, propagates its own mean estimate by using its own local observation, which is for AS or for B.

IV-A Private and complete information games

In Step 2 of Algorithm 1 the user solves a set of linear equations. This computation can be avoided in situations where the information of each consumer remains the same. The information is static in the two extreme cases. The first extreme case is when the information exchange model is private ( P). For the private information case, there exists a closed-form solution to the set of equations in (13)-(14) that is symmetric when the preference correlation is homogeneous. We state this result in the following.

Proposition 2

Consider the Bayesian game defined by the payoff for and the the private information exchange model . Assume the preferences of users are -correlated at time , that is, the off-diagonal elements of are the same for all and and its diagonal elements equal to 1. Then, the unique BNE strategy of user is linear in , , for such that

| (25) |

where we define constants , , and .

Proof : See Proposition 1 and 2 in [10] for the proof of the selfish case ( S). Proofs for the other cases follow the same steps where we consider the best response function in (9) of the corresponding behavior model. ∎

Second extreme case of static information is when all the users have complete information. For the game we consider, for each customer, his private preference and the cumulative realized preference form a sufficient statistic of the realized preferences for the homogeneously correlated preference games {S, U, W} – see [26]. Next we provide an explicit characterization of BNE strategies when users have complete information.

Proposition 3

Consider the Bayesian game defined by the payoff for . Let the information of customer at time be . Assume the preferences of users are -correlated at time as defined in Proposition 2. Then, the unique BNE strategy of user is linear in , , for all such that

| (26) |

where we define constants , and .

Proof : Proof follows along the similar lines of the proof of Proposition 2. ∎

Complete information is achieved when the SO broadcasts total consumption and the preference correlation is homogeneous. That is, the total consumption conveys the cumulative realized preference when the preferences are homogeneously correlated. Thus, in the broadcast information exchange model, , consumers play a private information game in the first time slot, and they have complete information from the second slot onwards.

These characterizations allow for computation of BNE behavior by putting the available information into the linear strategy functions instead of following the steps of Algorithm 1. In the following sections, these characterizations allow for analytical comparison of performance measures with respect to different behavior and information exchange models.

V Effects of behavior and information exchange models on demand

We first focus on the effect private and complete information models have on demand. In both of these cases information is static. Hence it suffices to focus on demand at a given time for comparison. In the following, we drop the sub-index from the notation until we consider the action-sharing information exchange model. We define demand for a consumer behavior model as .

For the private and complete information cases, when the preferences are -correlated, the expected consumption of individuals are the same as per (25) and (26). Moreover, both the private and complete information models have the same expected total consumption,

| (27) |

by the fact that has the same value in Propositions 2 and 3. This means that allowing users to exchange information does not alter the demand forecasts of the operator. We can also read from the expected demand above that a welfare-maximizing user is not impacted by the changes in because . On the other hand, consumption of selfish and altruistic users decreases with slope as the renewable term increases.

Given the explicit expected demand above, we compare the effects of different consumer behavior models. Throughout the analysis, we assume the preferences are -correlated where the diagonal elements of the covariance matrix are equal to 1 and off-diagonal elements are equal to .

Corollary 1

For large number of consumers, , we have

-

1.

.

-

2.

If then , which is greater than 1 for .

-

3.

If then , which is greater than 1 for .

Proof : When is large, we can approximate the behavior constants given in Proposition 2 as , and . The comparisons follow from (27). ∎

The above result says that the expected consumption of a selfish individual is higher than an altruistic user. Furthermore, the ordering of expected consumptions follow when . This range of price parameter is of importance because the realized rate of return of the operator is approximately . Hence, the operator is likely to select the pricing policy from this range [10].

Next, we consider demand variance as an indicator of uncertainty that an operator has in its demand forecast. We first focus on the private information model.

Corollary 2

Consider the P information model with -correlated preferences. We have the variance of normalized demand as follows:

| (28) |

where is as defined in Proposition 2.

Proof : From the definition of the variance of normalized demand, we have

In the second equality we use (25) to cancel out the squared mean of consumption. The result follows from the above equation. ∎

Given the explicit representation of variance, we can make the following comparison about the effects of consumption behavior models on demand uncertainty.

Corollary 3

Consider the P information model with -correlated preferences. For large number of consumers, , we have:

-

1.

, where is as defined in Lemma 1 for .

-

2.

(29) -

3.

If , then the variance of normalized demand is the same for all behavior models .

-

4.

If , then .

-

5.

If , then which is less than 1 for .

Proof : When is large, we have the constant from Proposition 2 where is as defined in Lemma 1. The comparisons follow from (28). ∎

Equation (29) shows that, with increasing , the demand variance grows as long as while it decreases with increasing when . Furthermore, the change in variance slows as becomes larger. From the fourth observation we see that selfish behavior achieves a higher demand variance in comparison to altruistic behavior. Next we focus on the demand variance in the complete information case that is reached after the operator broadcasts the total consumption information.

|

|

| (a) | (b) |

|

|

| (c) | (d) |

Corollary 4

Consider the complete information model with -correlated preferences. We have the variance of as

| (30) |

where is as defined in Proposition 3.

Proof : From the definition of the variance of normalized demand,

| (31) |

In the second step we substitute the consumption decisions of individuals from (26) and cancel out the mean of consumption squared. The third step expands the quadratic sum where we have in the last equality. Now consider the first expectation inside the last equality above:

| (32) |

The second expectation inside (31) is

| (33) |

The result follows by substituting the above two identities into (31) and then simplifying the terms. ∎ We have the following observations for the variance of demand in the complete information case.

Corollary 5

Consider the complete information model with -correlated preferences. For large number of consumers, ,

-

1.

for any model .

-

2.

The change of variance with respect to is zero.

Proof : When is large, we have the constant from Proposition 3 for any . The observations above follow when we substitute this approximation in (30). ∎

The results above are in sharp contrast to the observations given by items 1 and 2 of Corollary 3 for the variance of demand in the private information model. In summary, while giving information to the consumers does not affect the expected demand as per (27), it reduces the uncertainty in demand forecasts.

So far, we have compared the private information and complete information cases. As aforementioned, complete information is achieved after the first time step in the broadcast information exchange model during a time zone. In the action-sharing information exchange model, we expect to observe effects on demand similar to the complete information case. However, an analytical comparison between and is not possible because we do not have a closed form solution to the consumption behavior when as per Proposition 1.

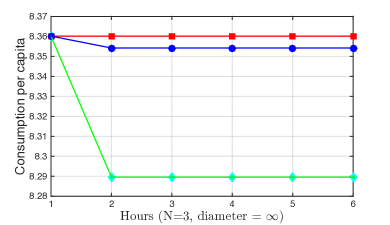

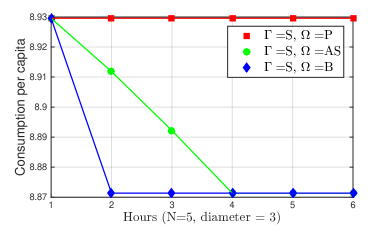

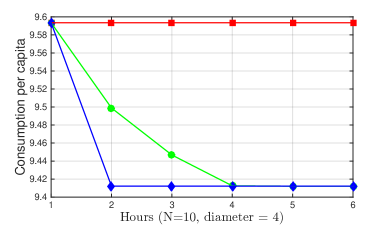

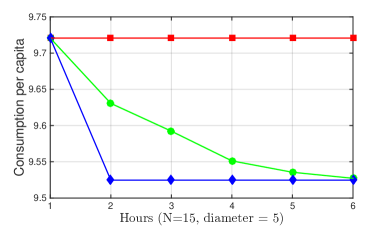

In the sequel, we numerically analyze the effects of the action-sharing information exchange model on expected consumption and its variance. Note that in the action-sharing (AS) information exchange model, we need to consider multiple time steps in a time zone to measure the effects of information. In AS, consumers follow the steps in Algorithm 1 to compute their BNE strategies. Figs. 1(a)-(d) exhibit the total consumption with respect to hours for the population sizes , respectively. Given a population size plot, each line corresponds to a different information exchange model for the selfish consumer behavior model – see the legend in Fig. 1(b). We observe that when the network is connected (Figs. 1(b)-(d)), the total consumption in AS model converges to the total consumption in the B model. Furthermore, convergence time is proportional to the diameter of the network. When the network is not connected (Fig. 1(a)), convergence does not necessarily happen. Finally, we compare the normalized demand variance for the cases considered in Fig. 1 in Table I. As expected, the AS model has a demand variance that is smaller than the private information model but larger than the broadcast model.

| N | ||||

|---|---|---|---|---|

| 3 | 5 | 10 | 15 | |

| P | 3.5 | 1.7 | 1.2 | 1.1 |

| AS | 3 | 1.1 | 0.7 | 0.6 |

| B | 2.1 | 0.9 | 0.5 | 0.5 |

VI Effects of behavior and information exchange models on aggregate utility

We begin by comparing the effects of private and complete information models on aggregate utility. In both of cases, behavior is static. Hence we focus on demand at a fixed hour and remove the sub-index from the notation. We then give an explicit characterization of the expected aggregate utility for the symmetric BNE strategies of the form given by (25) or (26).

Lemma 2

For the symmetric BNE strategies of the form , we have the following characterization of normalized expected aggregate utility when :

| (34) |

Proof : From the definition of aggregate utility in (4) and the definition of individual utility, we have

| (35) |

From the above relationship there are three expectation terms we need to compute. The first term is given by

| (36) |

The second term is

| (37) |

The third expectation is

| (38) |

Combining the three terms above in (35), we have

| (39) |

Reorganizing and simplifying gives the desired result. ∎

We compare the effects of private and complete information exchange models on aggregate utility next.

Corollary 6

Consider the private and complete information models for -correlated preferences for large number of consumers, .

-

1.

The expected normalized aggregate utility is larger in the private information model than in the complete information model.

-

2.

The difference in expected normalized aggregate utilities between the two information models becomes negligible as increases.

Proof : For large in private information case, from Proposition 2, where is as defined in Lemma 1. For large in the complete information case, from Proposition 3 for any . In addition, the term is the same for both private and complete information models. The first observation is established by substituting these constants for the BNE behavior of both private (25) and complete information (26) models in (34) and taking the difference. The second relationship is deduced by noting that when increases, while the expected utility in (34) increases, the difference between the two models remains the same because the constant is the same for both models. ∎

The results above imply that at high mean consumption preference, the broadcast information has negligible effect on aggregate utility. We now compare the effects of behavior models.

Corollary 7

Consider the private and complete information models for -correlated preferences. We have the following relations in terms of the normalized expected aggregate utility for large and for both information models:

-

1.

The ratio of expected aggregate utility when consumers act selfish versus altruistic is given by

(40) That is, altruist behavior achieves a strictly higher aggregate utility.

-

2.

The ratio of expected aggregate utility when consumers act as welfare maximizers versus altruistic is given by

(41) which is strictly less than 1 for any parameter value .

Proof : Note that for large , we have , and for both the private and complete information models. Proof follows by substituting the related constants of the behavior models in (34) and only considering terms that multiply . ∎

As expected altruistic behavior model attains a higher aggregate utility than any other consumer behavior model regardless of the information exchange model. Furthermore, the ratio of increase in (40) when compared to selfish behavior increases as the price policy parameter increases. We next consider the impact of changes in -correlation on the expected aggregate utility.

Corollary 8

Consider the private and complete information models for -correlated preferences.

-

1.

When information is private and is large, the sensitivity of expected aggregate utility to correlation constant is negative for models and for when . In addition, the decrease in aggregate utility with respect to slows as grows.

-

2.

When information is complete and is large, the sensitivity of expected aggregate utility is given by

(42)

Proof : Note that terms in (34) do not depend on . The results follow by substituting the values of terms when is large for the corresponding information model in (34) and then taking the derivative with respect to . ∎

The above results show that the increasing correlation among user consumption preferences decreases aggregate user utility irrespective of the information model.

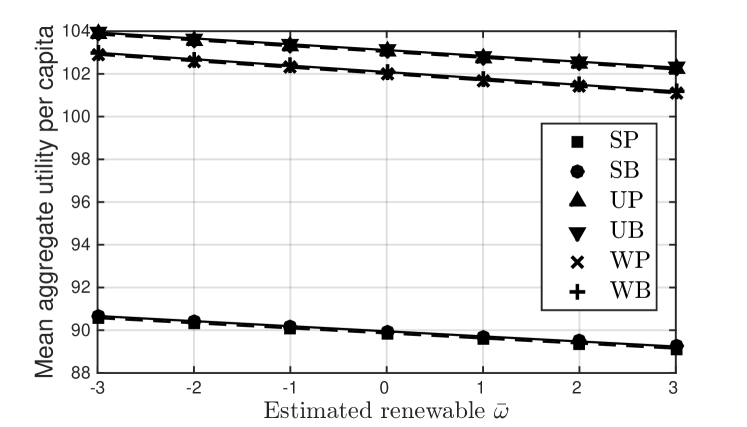

Lastly, we consider the effect of the reported mean estimate of the renewable energy term in (1) on aggregate utility. In Fig. 2, we plot normalized expected aggregate utility per capita with respect to . We observe private (dashed line) and complete (solid line) information models have negligible difference in for a given behavior model as per Corollary 6. Aggregate utility decreases for all behavior and information exchange models as increases. While the slope of decrease is the same for selfish and aggregate utility maximizers, this decrease is slightly faster for welfare maximizers.

We compared the effects of behavior models in the context of the two static information exchange models. Results indicate that the expected aggregate utility is not affected by the information that users may be given. We also explicitly characterized the extent of the effect of consumer behavior models on aggregate utility, and concluded that consumer behavior models are the primary determinant of expected aggregate utility. We confirm this intuition by considering the average aggregate utility from an ensemble of runs in the set-up of Fig. 1.

|

VII Effects of behavior and information exchange models on welfare

We follow a similar path as the previous section. We focus on the two extreme information models, private and complete, when consumers have static information. Hence, we remove the time sub-index. The following result provides an explicit characterization of the expected welfare for symmetric BNE strategies.

Lemma 3

For the symmetric BNE strategies of the form , we have the following characterization of normalized expected welfare when :

| (43) |

Proof : Recall the definition of welfare in (7) and note that is equal to (35) when we replace with and let in (35). The rest follows along the same lines as in the proof of Lemma 2. ∎

The effects of information models, private or complete, are similar to the results for aggregate utility in Corollary 6 as the functional form of welfare in (43) is identical. That is, for large , the private information model is slightly preferable. If the mean preference is large in comparison to the decay parameter , the information models have a negligible effect on welfare. Next, we compare the impact of consumer behavior models.

Corollary 9

Consider the private and complete information models for -correlated preferences. We have the following relationships in terms of the normalized expected welfare for large and in both information models:

-

1.

The ratio of expected welfare when consumers act selfish versus welfare-maximizing is

(44) That is, welfare-maximizing behavior achieves a strictly higher welfare except when they are equal at .

-

2.

The ratio of expected welfare when consumers act altruistic versus welfare-maximizing is

(45) which is strictly less than 1 for any parameter value except when welfares are equal at .

Proof : Note that for large , we have , and for both the private and complete information models. Proof follows by substituting the related constants of the behavior models in (43) and only considering terms that multiply . To prove that (44) is less than 1, we need to show that . Observe that this relationship is equivalent to , which is true except for . Similarly, showing that (45) is less than 1 amounts to . This is equivalent to , which is true if . ∎

As expected, welfare-maximizing behavior attains a higher welfare than any other consumer behavior model regardless of the information exchange model. Furthermore, the ratio of increase in (44), when compared to selfish behavior, grows as the price policy parameter increases. Next we consider the effect of -correlation on expected welfare.

Corollary 10

Consider the private and complete information models for -correlated preferences.

-

1.

When information is private and is large, the sensitivity of expected welfare to correlation constant is negative if and . In addition, the decrease in welfare with respect to slows as grows.

-

2.

When information is complete and is large, the sensitivity of welfare is given by

(46)

Proof : Note that the terms in (43) do not depend on . The results follow by substituting the values of terms when is large for the corresponding information model in (43) and then taking the derivative with respect to . ∎

The above results show that increasing correlation among user consumption preferences decreases welfare irrespective of the information model.

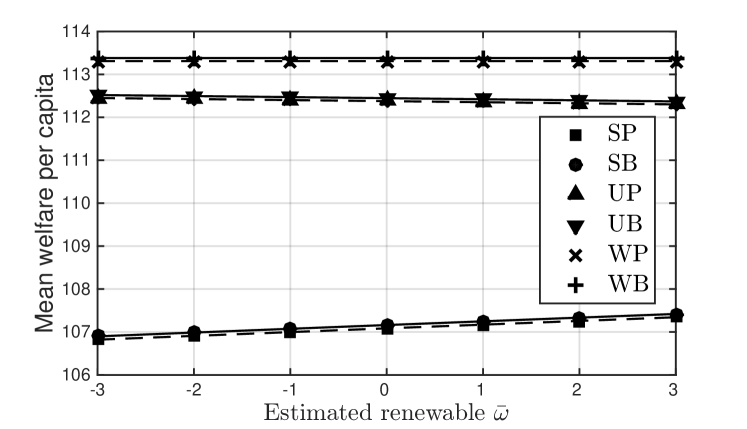

Lastly, we consider the effect of reported mean estimate of the renewable energy term in (1) on welfare. In Fig. 3, we plot expected normalized welfare with respect to . We observe private (dashed lines) and complete (solid lines) information models have negligible differences in for a given behavior model. does not change for welfare maximizers because users do not respond to changes is . increases for selfish users while it decreases for aggregate utility maximizers. To see why, recall Corollary 1 from which we have for . When increases, decreases by (27) and gets closer to causing the increase of . When increases, decreases and moves away from causing the decrease of . Considering the drop in expected aggregate utility of selfish users in Fig. 2, increasing implies a higher revenue for the operator when users are selfish because welfare is the sum of aggregate utility and net revenue in (7).

We compared the effects of behavior models in the context of the two static information exchange models. In sum, the results indicate that the expected welfare is not affected by the information that users may be given. We also explicitly characterized the extent to which consumer behavior models affected expected welfare. Since the latter are the primary determinants of expected welfare, we expect the action-sharing information exchange model to perform similar to the private and broadcasting information exchange models.

|

VIII Discussion

We proposed a demand response management model based on the real-time pricing scheme where an operator responsible for supplying electricity to a set of consumers employed real-time demand dependent price. The pricing function is such that it linearly increases with total consumption per capita and decreases with increasing renewable energy generation in the time slot. This and other RTP policies proposed in the literature [27] allow the operator to shape consumer behavior in order to improve system level performances, e.g., demand uncertainty reduction, welfare maximization, PAR minimization, etc. However, the implications and the extent of the success of the RTP policies depend on consumer behavior, as well as information consumers have, which are unknown to the SO. This paper provided an extensive analysis of the sensitivity of the system performance measures to consumer behavior and information under an RTP mechanism. Our results illustrated that communication among consumers reduced demand uncertainty and showed the extent to which the flexibility that an RTP mechanism provides in managing shiftable demand of the consumers could impact system performance.

From the perspective of the SO, giving information to the consumers is beneficial in that it reduces demand uncertainty which can reduce the conventional energy reserves held for worst case scenarios. Furthermore, our results on sensitivity of demand and welfare on the renewable energy term in the price provide clear tradeoffs to be considered by the SO. On one hand, renewable energy term can shape shiftable consumption according to the abundance or the scarcity of renewables. On the other hand, these manipulations cause significant changes to the aggregate user utility. From the perspective of a regulator, who is responsible for the well-being of the system and consumers, the relationship established between the expected aggregate consumer utility when users are altruistic and the expected aggregate consumer utility when users are selfish provides insight on the harm caused by the RTP mechanism parameters to the consumers. Moreover, the relationship between the expected welfares when users are selfish versus welfare-maximizing provides a guideline on how to select pricing policy parameters based on system cost parameters to maximize expected welfare. These insights can guide limitations that the regulator can put to the SO’s RTP policy. Lastly, the illustrated positive effects of giving additional information to the consumers is a push toward investing in a communication network of smart meters among consumers. From the perspective of consumers that are self-interested, these results show that sharing their information will not have adverse effects in expected utility.

It should be observed that the aforementioned implications depend on specific modeling choices, namely, on the demand side the assumption of Bayesian information processing, and on the supply side the use of a quadratic form for the SO’s cost. These choices may be simplistic. But in the following we claim that the results outlined here still provide meaningful guidelines if these restrictions are lifted. On the demand side, with regard to the model of Bayesian information processing, we remark that this is a benchmark model of information processing, and in our analysis we consider the two extremes of consumer information access, namely, private and complete information. The analysis of the two extreme cases provide the range of results we can expect from the performance measures in an information sharing consumer model. Hence, if we are to consider another information sharing model that is not Bayesian and has a lower computational complexity, e.g. [28], we would expect our insights to be similar to the action-sharing model considered here as long as the proposed model aggregates information approximately correctly. As for the use of quadratic energy costs on the supply side, it is better to consider a model in which the cost for each device can be modeled as a linear function of the power dispatched from each device. In this case the cost model is an increasing piecewise linear function of total consumption as power is dispatched from more costly generators with increasing total consumption [16]. The quadratic cost function is a tractable approximation for the piecewise linear cost function and captures the fundamental property that higher energy production requires dispatching from more costly sources. The quantitative specifics may change for piecewise linear functions but the qualitative conclusions will be similar.

A prominent feature of the vision for the electricity grid of the future is that consumers play an active role in balancing supply and demand through communication with the operator and amongst the consumers themselves. Furthermore, the grid of the future should be cleaner by allowing for increased renewable energy penetration. In order to attain this vision, we need to address two main challenges. First, making consumers active entities in balancing demand and supply can have unintended consequences such as increasing uncertainty in the system, and thus inflating environmental and monetary costs [8, 9]. Second, we have to address the fact that renewables are inherently intermittent and hard to predict, and hence, if not dealt with systematically, can increase the need for conventional energy reserves defying their primary purpose. This paper took a step in the direction to overcome these challenges in order to realize the vision for the electricity grid.

References

- [1] A. H. Mohsenian-Rad, V. W. Wong, J. Jatskevich, R. Schober, and A. Leon-Garcia, “Autonomous demand-side management based on game-theoretic energy consumption scheduling for the future smart grid,” IEEE Trans. Smart Grid, vol. 1, no. 3, pp. 320–331, Dec. 2010.

- [2] P. Samadi, A. H. Mohsenian-Rad, R. Schober, and V. W. Wong, “Advanced demand side management for the future smart grid using mechanism design,” IEEE Trans. Smart Grid, vol. 3, no. 3, pp. 1170–1180, Sept. 2012.

- [3] J. Lunén, S. Werner, and V. Koivunen, “Distributed demand-side optimization with load uncertainty,” in Int. Conf. Acoustics, Speech and Signal Process., Vancouver, Canada, May 2012, pp. 5229–5232.

- [4] J. Xu and M. van der Schaar, “Incentive-compatible demand-side management for smart grids based on review strategies,” EURASIP Journal on Advances in Signal Processing, vol. 51, pp. 1–17, Dec. 2015.

- [5] N. Li, L. Chen, and S. H. Low, “Optimal demand response based on utility maximization in power networks,” in IEEE Power and Energy Society General Meeting, July 2011, pp. 1–8.

- [6] I. Atzeni, L. Ord ez, G. Scutari, D. Palomar, and J. Fonollosa, “Demand-side management via distributed energy generation and storage optimization,” IEEE Trans. Smart Grid, vol. 4, no. 2, pp. 866–876, June 2013.

- [7] P. Yang, G. Tang, and A. Nehorai, “A game-theoretic approach for optimal time-of-use electricity pricing,” IEEE Trans. Power Systems, vol. 28, no. 2, pp. 884–892, May 2013.

- [8] S. Depuru, L. Wang, and V. Devabhaktuni, “Smart meters for power grid: Challenges, issues, advantages and status,” Renewable and Sustainable Energy Reviews, vol. 15, no. 6, pp. 2736–2742, Aug. 2011.

- [9] Y. Wang, W. Saad, N. B. Mandayam, and H. V. Poor, “Integrating energy storage into the smart grid: A prospect theoretic approach,” in IEEE Int. Conf. Acoustics, Speech and Signal Process., May 2014, pp. 7779–7783.

- [10] C. Eksin, H. Deliç, and A. Ribeiro, “Demand response management in smart grids with heterogeneous consumer preferences,” IEEE Trans. Smart Grid, vol. 6, no. 6, pp. 3082–3094, Nov. 2015.

- [11] M. Roozbehani, A. Faghih, M. I. Ohannessian, and M. A. Dahleh, “The intertemporal utility of demand and price elasticity of consumption in power grids with shiftable loads,” in 50th IEEE Conf. Dec. and Control, and European Control Conf., Dec. 2011, pp. 1539–1544.

- [12] C. Eksin, H. Deliç, and A. Ribeiro, “Rational consumer behavior models in smart pricing,” in Proc. IEEE Int. Conf. Acoustics, Speech and Signal Process., Brisbane, Australia, Apr. 2015, pp. 3167–3171.

- [13] C. Wu, H. Mohsenian-Rad, J. Huang, and A. Y. Wang, “Demand side management for wind power integration in microgrid using dynamic potential game theory,” in IEEE GLOBECOM Workshops, Dec. 2011, pp. 1199–1204.

- [14] L. Gan, A. Wierman, U. Topcu, N. Chen, and S. H. Low, “Real-time deferrable load control: handling the uncertainties of renewable generation,” in 4th Int. Conf. Future Energy Systems, Jan. 2013, pp. 113–124.

- [15] R. Sioshansi and W. Short, “Evaluating the impacts of real time pricing on the usage of wind power generation,” IEEE Trans. Power Systems, vol. 24, no. 2, pp. 516–524, May 2009.

- [16] A. Papavasiliou and S. Oren, “Large-scale integration of deferrable demand and renewable energy sources,” IEEE Trans. Power Systems, vol. 29, no. 1, pp. 489–499, Jan. 2014.

- [17] P. Samadi, A.-H. Mohsenian-Rad, R. Schober, V. W. Wong, and J. Jatskevich, “Optimal real-time pricing algorithm based on utility maximization for smart grid,” in 1st IEEE Int. Conf. Smart Grid Comm., Oct. 2010, pp. 415–420.

- [18] P. Chakraborty and P. P. Khargonekar, “A demand response game and its robust price of anarchy,” in IEEE Int. Conf. Smart Grid Comm., Nov. 2014, pp. 644–649.

- [19] L. Jiang and S. H. Low, “Multi-period optimal energy procurement and demand response in smart grid with uncertain supply,” in 50th IEEE Conf. Dec. and Control, and European Control Conf., Dec. 2011, pp. 4348–4353.

- [20] A. J. Wood and B. F. Wollenberg, Power generation, operation, and control. New York, NY: John Wiley & Sons, 2012.

- [21] D. Fudenberg and J. Tirole, Game Theory. Cambridge, Massachusetts 393: MIT Press, 1991.

- [22] C. Eksin, P. Molavi, A. Ribeiro, and A. Jadbabaie, “Bayesian quadratic network game filters,” IEEE Trans. Signal Process., vol. 62, no. 9, pp. 2250–2264, May 2014.

- [23] Y. C. Ho and K. Chu, “Team decision theory and information structures in optimal control problems: Part I,” IEEE Trans. on Autom. Control, vol. 17, no. 1, pp. 15–22, 1972.

- [24] S. Kay, Fundamentals of Statistical Signal Processing: Estimation Theory, 1st ed. Prentice Hall, Englewood Cliffs, New Jersey, 1993.

- [25] X. Vives, Information and Learning in Markets. Princeton University Press, 2008.

- [26] ——, “Strategic supply function competition with private information,” Econometrica, vol. 79, no. 6, pp. 1919–1966, 2011.

- [27] Q. Huang, M. Roozbehani, and M. A. Dahleh, “Efficiency-risk tradeoffs in electricity markets with dynamic demand response,” IEEE Trans. on Smart Grid, vol. 6, no. 1, pp. 279–290, Jan. 2015.

- [28] N. Forouzandehmehr, S. M. Perlaza, Z. Han, and H. V. Poor, “A satisfaction game for heating, ventilation and air conditioning control of smart buildings,” in IEEE Global Communications Conf., Dec. 2013, pp. 3164–3169.