Equilibrium pricing under relative performance concerns

Abstract

We investigate the effects of the social interactions of a finite set of agents on an equilibrium pricing mechanism. A derivative written on non-tradable underlyings is introduced to the market and priced in an equilibrium framework by agents who assess risk using convex dynamic risk measures expressed by Backward Stochastic Differential Equations (BSDE). Each agent is not only exposed to financial and non-financial risk factors, but she also faces performance concerns with respect to the other agents.

Within our proposed model we prove the existence and uniqueness of an equilibrium whose analysis involves systems of fully coupled multi-dimensional quadratic BSDEs. We extend the theory of the representative agent by showing that a non-standard aggregation of risk measures is possible via weighted-dilated infimal convolution. We analyze the impact of the problem’s parameters on the pricing mechanism, in particular how the agents’ performance concern rates affect prices and risk perceptions. In extreme situations, we find that the concern rates destroy the equilibrium while the risk measures themselves remain stable.

Keywords: Financial innovation, equilibrium pricing, social interactions, performance concerns, representative agent, -conditional risk measure, multidimensional quadratic BSDE, entropic risk.

2010 AMS subject classifications:

Primary: 91A10, 65C30; Secondary:

60H07,

60H20

,

60H35, 91B69.

JEL subject classifications:

G11, G12, G13, C73

1 Introduction

The importance of relative concerns in human behavior has been emphasized both in economic and sociological studies; making a EUR profit when everyone else made EUR “feels” distinctly different had everyone else lost EUR. A diverse literature handling problems dealing with some form of strategic and/or social interaction in the form of relative performance concerns exists: In both [HinzRudolphAntolinEtAl2010] and [Pedraza2013] the social interaction component appears in the form of peer-based under-performance penalties known as “Minimum Return Guarantees”; the comparison is usually done via tracking a relevant market index, something quite standard in pension fund management. Another type of performance concerns arises in problems where the agents’ consumption is taken into account. The utility functions used there exhibit a “keeping up with the Joneses” behavior as introduced in [Duesenberry1949] and developed by [Abel1990], [Abel1999] (see further [Gali1994], [ChanKogan2001], [Gomez2007] and [XiourosZapatero2009]); in other words, the benchmark for the standard of living is the averaged consumption of the population and one computes the individual’s consumption preferences in relation to that benchmark. Another type of concern criterion, an internal one, uses the past consumption of the agent as a benchmark for the current consumption; [HarlHeal1973] introduced this “habit formation” approach. A more mathematical finance approach, as well as a literature overview, can be found in [EspinosaTouzi2015] or [FreiDosReis2011]. These last two papers are the inspiration for this one.

In this paper we study the effects of social interaction between economic agents on a market equilibrium, the efficiency of a securitization mechanism and the global risk. We consider a finite set of agents having access to an incomplete market consisting of an exogenously priced liquidly traded financial asset. The incompleteness stems from a non-tradable external risk factor, such as the amount of rain or the temperature, to which those agents are exposed. In an attempt to reduce the individual and overall market risks, a social planner introduces to the market a derivative written on the external risk source, allowing the agents in to reduce their exposures by trading on it. The question of the actual completeness of the resulting market has been addressed in some generality in the literature, and we refer for instance to [Schwarz2015]. Questions about pricing and benefits of such securities written on non-tradable assets have been approached in the literature many times, we refer in particular to [HorstPirvuDosReis2010] where the new derivative is priced within an equilibrium framework according to supply and demand rules and more generally to [AndersonRaimondo2008]. Equilibrium analysis of incomplete markets is commonly confined to certain cases such as single agent models ([HeLeland1993], [GarleanuPedersenPoteshman2009]), multiple agent models where markets are complete in equilibrium ([DuffieHuang1985], [HorstPirvuDosReis2010], [KaratzasLehoczkyShreve1990]), or models with particular classes of goods ([JofreRockafellarWets2010]) or preferences ([CarmonaFehrHinzEtAl2010]). For a good overview of equilibrium issues stemming the from market incompleteness as well as some solutions we point the reader to [KardarasXingZitkovic2015] and references therein.

Although we follow ideas similar to those in [HorstPirvuDosReis2010], our goal is to understand how such a pricing mechanism and risk assessments are affected when the agents have relative performance concerns with respect to each other. Each agent has an endowment over the time period depending on both risk factors. Her investment strategy in stock and the newly introduced derivative induces a gains process . For a given performance concern rate the agent seeks to minimize the risk

| (1.1) |

where is a risk measure ( is further described below). The first two terms inside correspond to the classical situation of an isolated agent trading optimally in the market to profit from market movements and to hedge the financial risks inherent to . The last term is the relative performance concern and corresponds to the difference between her own trading gains and the average trading gains achieved by her peers. Intuitively, as increases, the agent is less concerned with the risks associated to her endowment and more concerned with how she fares against the average performance of the other agents in . For instance, given no endowments, if and agent made EUR from trading while the others all made EUR then she perceives no gain at all.

Each agent uses a monetary convex risk measure . The theory of monetary, possibly convex, possibly coherent, risk measures was initiated by [ArtznerDelbaenEberEtAl1999] and later extended by [FoellmerSchied2002] and [FrittelliRosazza2002]. One special class of risk measures, the so-called -conditional risk measures, which are closely related to the so-called -conditional expectations (see [Gianin2006]), are those defined through Backward Stochastic Differential Equations (BSDEs), see [Peng1997], [ElKarouiRavanelli2009] and [BarrieuElKaroui2009]. Our use of BSDEs is motivated by two general aspects. The first is that it generically allows to solve stochastic control problems away from the usual Markovian setup where one uses the HJB approach in combination with PDE theory, see e.g. [Touzi2013]. The second is that optimization can be carried out in closed sets of constraints without the assumption of convexity for which one usually uses duality theory, see [HuImkellerMuller2005].

The form of relative performance concern we use and its study using BSDEs can be traced back to [Espinosa2010] and [EspinosaTouzi2015]. Their setting is quite different from that presented here; the authors show the existence of a Nash equilibrium for a pure-interaction game of optimal investment without idiosyncratic endowments to hedge ( for all agents), and where the agents optimize, in a Black–Scholes stock market, the expected utility of the gains they make from trading under individual constraints. These two works are followed by [FreiDosReis2011], where a general discussion on the existence of equilibrium, with endowments, is given including counter examples to such existence.

Methodology and content of the paper. All agents optimize their respective functional given by (1.1) and, as the derivative is priced endogenously via an equilibrium framework, the market price of external risk is also part of the problem’s solution. Equilibrium in our game is a set of investment strategies and a market price of external risk giving rise to a certain martingale measure.

In the first part of this work, we show the existence of the Nash equilibrium in our problem and how to compute it for general risk measures induced by BSDEs. The analysis is carried out in two steps. The first involves solving the individual optimization problem for each agent given the other agents’ actions, the so-called best response problem. The second consists in showing that it is possible to find all best responses simultaneously in such a way that supply and demand for the derivative match, which, in turn, yields the market price of external risk. (We generally think of a market with a zero net supply of the derivative; however, the methodology allows to treat cases where some agents who were allowed to trade in the derivative left the market such that the (active) agents in hold together a non-zero position). We then verify that the market price of external risk associated to the best responses satisfies the necessary conditions.

This last step is more complex. Since the agents assess their risks using dynamic risk measures given by BSDEs, the general equilibrium analysis leads to a system of fully coupled non-linear multi-dimensional BSDEs (possibly quadratic). We proceed by extending the representative agent approach (see [Negishi1960]) where aggregation of the agents into a single economy and optimal Pareto risk sharing are equivalent to simultaneous individual optimization. From the works of [BarrieuElKaroui2005] and [BarrieuElKaroui2009], we extend their infimal convolution (short inf-convolution) technique to agents with interdependent utility functions. This approach yields a single risk measure that encompasses the risk preferences for each agent and through which it is possible to find a single representative economy. We point out that in order to cope with the cross dependence induced by the performance concern rates, standard inf-convolution techniques do not lead to a single representative economy. We use the technique in a non-standard fashion via weighted-dilations of each agent’s risk measure (see Section 3.2 in [BarrieuElKaroui2009] and Section 4 below); to the best of our knowledge this type of analysis is new and of independent interest. The closest reference to this is [Rueschendorf2013], where some form of weighted inf-convolution appears.

The second part of this work focuses on the case of agents using entropic risk measures, which can be treated more explicitly and allows for an in-depth study of the impact of the concern rates. In identifying the Nash equilibrium, we are led to a system of fully coupled multi-dimensional quadratic BSDEs whose analysis is, in general, quite involved. Based on the works of [Espinosa2010] and [EspinosaTouzi2015], the authors of [FreiDosReis2011] give several counter examples to the existence of solutions; nonetheless, positive results do exist although none are very general, see e.g. [Tevzadze2008], [CheriditoNam2015], [Frei2014], [KramkovPulido2016], [HuTang2016], [XingZitkovic2016], [JamneshanKupperLuo2014] and [luo2015solvability]. In our case we are able to solve the system.

Findings. Within the case of entropic risk measures, we study in detail a model of two agents and with opposite exposures to the external risk factor, so that one has incentives to buy the derivative while the other has incentive to sell. In this model we are able to specify the structure of the equilibrium. Using both analytical methods and numerical computations, when the analytics are not tractable, we explore the behavior of the agents as the model parameters vary. We give particular attention to how the relative performance concern rates, and thereby the strength of the coupling between the agents, deviate from the standard case of non-interacting agents (when ).

We find that as either agent’s risk tolerance increases, their risk lowers. If any concern rate increases then the agents engage in less trading of the derivative. This is because every unit of derivative bought by one is a unit sold by the other and hence the gains of one are the losses of the other. Consequently, if an agent is more concerned about the relative performance, she will tend to trade less with the others. Also, as expected, we find that if it is the buyer of derivatives whose concern rate increases, the derivative’s price decreases, while it increases in the case of the seller.

Very interestingly, we find that the risk of a single agent increases if the other agents become more concerned with their relative performance but that it decreases as this agent becomes more concerned. Consequently, if the agents were to play this game repeatedly and their concern rate were to vary over time, they would both find it more advantageous to become more concerned (or jealous). As they both do so, the trading activity in the derivative decreases, but their activity in the stock increases and explodes - the equilibrium does not exist anymore. Surprisingly, this behavior is not captured at all by the risk measures! This non-trivial, and perhaps not desirable, behavior of the system after introduction of the derivative is not without similarities with what is found in the models of [CaccioliMarsiliVivo2009] and [CorsiMarmiLillo2013]. It is a reminder that, when evaluating the benefits of financial innovation, one should not focus of the economy of an individual agent (who sees clear benefits in the form of a risk reduction) but really have a systemic view of the impact of the new instrument.

Organization of the paper. In Section 2, we define the general market, agents, optimization problem and equilibrium that we consider. Sections 3 and 4 are devoted to solving the general optimization problem for a set of agents having arbitrary risk measures. In the former we solve the optimization problem for each agent, given the strategies of all others. In the latter we deal with the aggregation of individual risk measures and identification of the representative agent, and we solves the equilibrium for the whole system. Sections 5 and 6 contain the particular case where the agents use entropic risk measures. In this more tractable setting, Section 5 explores theoretically the influence of various parameters on the global risk while Section 6 focuses on a model with 2 agents with opposite risk profiles, and thoroughly explores the influence of the concern rates, in particular, on the individual behaviors, risks, and the consequences for the whole system. We also present numerical results. Section 7 concludes the study.

Acknowledgments. The authors would like to thank the two anonymous referees for their to-the-point and informative reports that have allowed us to improve several aspects of this work.

2 The model

We consider a finite set of agents, without loss of generality , with random endowments , , to be received at a terminal time . They trade continuously in the financial market which comprises a stock and a newly introduced structured security (called derivative), aiming to minimize their risk. For simplicity we assume that money can be lent or borrowed at the risk-free rate zero. Stock prices follow an exogenous diffusion process and are not affected by the agents’ demand. By contrast, the derivative is traded only by the agents from and priced endogenously such that demand matches supply. We point the reader to Appendix A for a full overview of the notation and stochastic setup.

2.1 The market

Sources of risk and underlyings

Throughout this paper . In our model, there are two independent sources of randomness, represented by a -dimensional standard Brownian motion on a standard filtered probability space , where is the filtration generated by and augmented by the -null sets. The Brownian motion drives the external and non-tradable risk process , which is thought of as a temperature process or a precipitation index. For analytical convenience we assume that follows a Brownian motion with drift being a stochastic process and constant volatility , i.e.,

| (2.1) |

The Brownian motion drives the stock price process according to

| (2.2) | ||||

We assume throughout this work that the stochastic processes are -adapted, with .

Market price of risk: financial and external

We recall (see e.g. [HorstMuller2007]) that any linear pricing scheme on the set of square integrable random variables with respect to can be identified with a -dimensional predictable process such that the exponential process defined by

| (2.3) |

is a uniformly integrable martingale. This ensures that the measure defined by having density against is indeed a probability measure (the pricing measure), and the present price of a random terminal payment is then given by , where denotes the expectation with respect to . For any such , we introduce the -Brownian motion

The first component of the vector is the market price of financial risk. Under the assumption that there is no arbitrage, must be a martingale under and, from the exogenously given dynamics of , is necessarily given by . The process on the other hand is unknown. It is the market price of external risk and will be derived endogenously by the market clearing condition (or constant net supply condition, see below).

The agents’ endowments and the derivative’s payoffs

The agents receive at time the income which depends on the financial and external risk factors. While the agents are able to trade in the financial market to hedge away some of their financial risk, a basis risk remains originating in the agent’s exposure to the non-tradable risk process . A derivative with payoff at maturity time is externally introduced in the market. By trading in the derivative , the agents have now a way to reduce their basis risk.

We give general conditions on the endowments, derivative payoff and coefficients appearing in the dynamics of and (see Appendix A for notation). Throughout the rest of this work the following assumption stands for all results.

Assumption 2.1 (Standing assumption on the data of the problem).

The processes , , and are bounded (belong to ). The random variables and , , are bounded (belong to ).

Price of the derivative, trading in the market and the agent’s strategies

Assuming no arbitrage opportunities, the price process of is given by its expected payoff under ; in other words . Since is bounded, writing the -martingale as a stochastic integral against the -Brownian motion (with the martingale representation theorem) yields a 2-dimensional square-integrable adapted process such that for

| (2.4) |

Note that we have . We denote by and the number of units agent holds in the stock and the derivative at time , respectively. Using a self-financing strategy valued in , her gains from trading up to time , under the pricing measure inducing the prices for the derivative, are given by

We require that the trading strategies be integrable against the prices, (i.e. ), so that the gains process are square-integrable martingales under .

2.2 Preferences, risk minimization and equilibrium

The agents’ measure of risk

The agents assess their risk using a dynamic convex time-consistent risk measure induced by a Backward Stochastic Differential Equation (BSDE). This means that the risk which agent associates at time with an -measurable random position is given by , where is the solution to the BSDE

The driver encodes the risk preferences of the agent. We assume that has the following properties:

Assumption 2.2.

The map is a deterministic continuous function. Its restriction to the space variable, , is continuously differentiable, strictly convex and attains its minimum.

For any fixed , the map is also strictly convex and attains its unique minimum at the point where its gradient vanishes. With this in mind we can define , where is the unique solution, in the unknown , to the equation

| (2.5) |

The agents’ risk measure given by the above BSDE is strongly time consistent, convex and translation invariant (or monetary). We do not give many details on the class of risk measures described by BSDEs, instead, we point the interested reader to [BarrieuElKaroui2005, Gianin2006, BarrieuElKaroui2009].

For convenience, we recall the relevant properties of the risk measures that play a role in this work: i) translation invariance: for any and any it holds that ; ii) time-consistency of the process : for any it holds that ; and iii) convexity: for any and for -measurable and we have .

The individual optimization problem

Agent ’s position at maturity is given by the sum of her terminal income and the trading gains over the time period . However, the agent compares her trading gains with the average gains of all other agents. Thus, we define the perceived total wealth of each of the agents in the market at time as

and is the concern rate (or jealousy factor) of agent (compare with (1.1)).

We make the following assumption on the concern rates , whose justification will become clear later on in Section 3.3.5.

Assumption 2.3 (Performance concern rates333The case of is, as we show in Section 3.3.5, not necessarily intractable, but the analysis of such a situation is beyond the scope of this paper.).

We have for each agent and .

For notational convenience we introduce the -valued vector and

| (2.6) |

The risk associated with the self-financing strategy evolves according to the BSDE

| (2.7) |

Now, we introduce a notion of admissibility for our problem.

Definition 2.4 (Admissibility).

Let , and be integrable strategies for the other agents. The -valued strategy process is called admissible with respect to the market price of risk if , where denotes the quadratic variation of and BSDE (2.7) has a unique solution. The set of admissible trading strategies for agent is denoted by .

We point out that in full generality each agent could have her own trading constraints, as in [EspinosaTouzi2015] or [FreiDosReis2011]. Here we assume that the agents have no trading constraints, aside from their strategies being integrable against the prices and leading to well-defined risk.

Each agent solves the following risk-minimization problem

Notice that, a priori, the risk for agent and the strategy chosen depend on the strategies of all other players, . This interdependence is an ever-present feature of our model. For the sake of presentation we leave it implicit whenever possible and we write the solution to the BSDE giving the risk for Agent as instead of . We will use the latter when the situation requires it.

Competitive equilibrium, equilibrium market price of risk and endogenous trading

We denote by the number of units of derivative present in the market. While each unit of derivative pays at time , the agents are free to buy and underwrite contracts for any amount of , so that is not necessarily an integer. We think essentially of the case , where every derivative held by an agent has been underwritten by another agent in , entailing essentially that agents share their risks with each other (see [BarrieuElKaroui2005, BarrieuElKaroui2009] or [HorstMuller2007]). Building upon [HorstPirvuDosReis2010] allows for a bit more flexibility as is possible444The situation would be possible if, prior to time , another agent was on the derivatives market and then stopped her activity, for instance might have had as objective to buy units, according to her own specific criteria, in which case .. In any case, over , only the agents in our set , with trading objectives as described above, are active in the market and so the total number of derivatives present is constant over time.

We assume that each agent seeks to minimize her risk measure independently, without cooperation with the other agents, so we are interested in Nash equilibria.

Definition 2.5 (Equilibrium and equilibrium MPR (EMPR)).

For a given Market Price of Risk (MPR) , we call an equilibrium if, for all , and

-

for any admissible strategy it holds that ,

i.e. individual optimality given the strategies of the other agents. We call Equilibrium MPR (EMPR) and Equilibrium Market Price of external Risk (EMPeR) if

-

1.

makes a true probability measure (equivalently, from (2.3) is a uniformly integrable martingale);

-

2.

there exists a unique equilibrium for ;

-

3.

satisfies the market clearing condition (or fixed supply condition) for the derivative (where denotes the Lebesgue measure):

(2.8)

3 The single agent’s optimization and unconstrained equilibrium

In this section and the one following, we study the solvability of the problem and the structure of the equilibrium for general risk measures induced by a BSDE. Finding an equilibrium market price of external risk is, essentially, an optimization under the fixed-supply constraint. So, prior to looking whether such an equilibrium MPR exists (postponed to Section 4), we start by fixing an arbitrary MPR and solve for the behavior of the system of agents given that MPR, without the fixed-supply constraint. For this, we first solve for the behavior of the individual agents given that the others have chosen their strategies (the so-called best response problem), and then solve for the Nash equilibrium for the system of agents.

3.1 Optimal response for one agent

In this subsection, in addition to a MPR being fixed, we assume given the strategies of the other agents, for a fixed agent , and we study the investment problem for a single agent whose preferences are encoded by .

Optimizing the residual risk

To solve the optimization problem for agent , we first recall from [HorstPirvuDosReis2010] that, at each time , the strategy chosen must minimize the residual risk: the additivity of the risk measure implies (writing and using the translation invariance) that

This suggests applying the following change of variables to (2.7) (using (2.6)),

| (3.1) |

If the strategies are not clear from the context, we also write . Direct computations yield a BSDE for given by

| (3.2) |

where the driver is defined as

| (3.3) | ||||

| (3.4) | ||||

Each individual agent seeks to minimize , the solution to (3.2), via her choice of investment strategy , in other words she aims at solving

| (3.5) |

Before we solve the individual optimization, we assume that the derivative does indeed complete the market. This must then be verified a posteriori (once the solution is computed) and case-by-case depending on the specific model.

Assumption 3.1.

Assume that , for any , -a.s. .

The pointwise minimizer for the single agent’s residual risk

In (3.2), the strategy appears only in the driver . The comparison theorem for BSDEs suggests that in order to minimize over one needs only to minimize the driver function over , for each fixed , , and . We define such pointwise minimizer as the random map

and as the minimized driver.

The pointwise minimization problem has, under Assumption 2.2, a unique minimizer which is characterized by the first order conditions (FOC) for , i.e. . Recall that . Using (3.4), the FOC is equivalently written as

| (3.6) | ||||

| (3.7) |

With from (2.5), the FOC system (3.6)–(3.7) is equivalent to . The expression for in (3.1) and elementary re-arrangements allow to rewrite as

| (3.8) |

Plugging into (3.3) yields an expression for the minimized (random) driver

| (3.9) |

Since is generic at this point, the process in not known precisely. Nonetheless, the general structure of and the minimized driver are determined. We stress two important things. First, is an affine driver with stochastic coefficients. Second, does not depend at all on . This means that while the optimal strategy (see below) depends on the strategies of the other agents, the minimized risk does not. In [HorstPirvuDosReis2010], the authors did not obtain this general form for the minimized driver.

Single-agent optimality

Since is an affine driver, and since , we have a unique solution to the BSDE with driver and terminal condition provided that the process is integrable enough, which we assume. Let then be the solution to BSDE (3.2) with driver (3.9) and define the strategy . We now prove that the above methodology indeed yields the solution to the individual risk minimization problem, in other words the so-called best response.

Theorem 3.2 (Optimality for one agent).

Assume the market price of risk and let Assumption 3.1 hold. Fix an agent and a set of integrable strategies for . Assume further that

-

•

for given by (3.9), , and

-

•

is admissible .

Then BSDE with driver (3.9) and terminal condition has a unique solution . Moreover, is the value of the optimization problem (3.5) (i.e. the minimized risk) for agent and is the unique optimal strategy.

Proof.

Given the structure of in (3.9) and the integrability assumption made, the existence and uniqueness of the BSDE’s solution in is straightforward.

We first use the comparison theorem to prove the minimality of , and hence the optimality of . Let . Take any strategy . First, from the definition of as a pointwise minimum, we naturally have that for all and , that is, . Second, is affine and thus Lipschitz, with Lipschitz coefficient process . By the comparison theorem, we therefore have, for any and in particular for , that . As this holds for any , this proves the minimality of and thus the optimality of .

We now argue the uniqueness of the optimizer . Let be an admissible strategy and let be the corresponding risk, i.e. solution to the BSDE (3.2) with strategy . We compute the difference , adding-and-substracting in the Lebesgue integral , and using the affine form of :

| (3.10) | ||||

By construction of as a minimizer, the difference in (3.1) is always positive. In particular, taking -expectation w.r.t. implies that for all . Assume that is an optimal strategy. Then and the LHS for vanishes. Under -expectation, the stochastic integral on the RHS also vanishes and we can conclude that the integrand in (3.1) is zero -a.e. Consequently, we obtain and hence . By uniqueness of the minimizer, we then have . ∎

Remark 3.3.

While Theorem 3.2 is stated as the optimal response of a single agent in the system with the other strategies being fixed, it is clear that it can more generally describe the optimal investment of an agent with preferences described by (equivalently, ) who trades in the assets and , which have the given MPR (one can think of making , or doing ). Following the same methods, the result could be generalized to a higher number of assets, with price processes given exogenously. This applies similarly to an agent trading in fewer assets, by setting the respective components to zero – see Theorem 4.5.

We now state a characterization of the optimal strategy via the FOC.

Lemma 3.4.

Proof.

By the assumptions on , means that , or equivalently . Therefore – recall (3.3). By uniqueness of the solution to the BSDE with driver and terminal condition , we have . Consequently, by the uniqueness of the FOC’s solution, . ∎

3.2 The unconstrained Nash equilibrium

Having solved the optimization problem for one agent, we now look at the existence and uniqueness of a Nash equilibrium, still for the MPR fixed at the beginning of this section, and still with no fixed-supply constraint.

Assume is a Nash equilibrium. Fix an agent . From the uniqueness of the optimal strategy, given by Theorem 3.2, one must have

where is the solution to the BSDE with terminal condition and driver given in (3.9). From the characterization (3.8) of , we therefore have, for all and ,

| (3.11) |

Note that, for any , the process does not depend on nor , seeing as neither nor does. Therefore, is also independent of the unknown , which is only present in the LHS of (3.11).

Conversely, assume we can solve for in Equation (3.11) and that is integrable against the prices. Then, since by (3.8), Theorem 3.2 guarantees that is the best response to , and we therefore have a Nash equilibrium.

So, the existence and uniqueness of a Nash equilibrium is equivalent to the existence and uniqueness of solutions to Equation (3.11).

Define the matrix by555Recall the notation that for sums and products over certain subsets of we identify with the set , where is the fixed finite number of agents.

| (3.12) |

i.e. the -th line has the entries , everywhere but for the -th one which is . Equation (3.11) can be rewritten as

| (3.13) |

where and , for .

Theorem 3.5.

Assume the market price of risk , that Assumption 3.1 and Assumption 2.3 hold, that, for all , is integrable against the prices and .

Then there exists a unique Nash equilibrium associated with the MPR , which is given by the unique solution to (3.13).

Proof.

The determinant of the is

where the sums run over indices from . If for all , then , so the matrix is not invertible. The determinant is strictly decreasing in each () and therefore also in . Hence, if for all and the product , then at least one factor must be strictly smaller than one and the determinant must be strictly positive (i.e. ). The invertibility of follows. This guarantees that one can solve system (3.11) (or, equivalently, (3.13)) for each to obtain . The integrability of follows from fact that each component is a linear combination of the integrable ’s. Finally, the Nash-optimality of was argued in the identification of the core Equation (3.11). ∎

We can now comment on Assumption 2.3. If for all , then is invertible independent of , i.e. in particular for . This shows that the condition that for all is not necessary, but merely a sufficient condition. Finally, if we were to allow for , then is not sufficient for invertibility of , e.g. in the case take and .

From now on we assume the agents’ optimization problems have a solution so that it makes sense to discuss the notion of equilibrium market price of risk (EMPR).

Remark 3.6.

Notice that at this point, as is given exogenously, we do not yet have a system of coupled BSDEs. For each , we obtain the value process as the solution to a BSDE where the terminal condition and driver , which does not depend on the strategies and only takes as argument. These processes are then used to solve for the Nash equilibrium of strategies , and so is the value process of the Nash equilibrium. This feature (no coupling of the BSDEs when solving for the optimal values), as well as the fact that solving for the optimizers of the Nash equilibrium reduces to solving a linear system (for which existence and uniqueness of the solution is equivalent to the invertibility of a matrix) is a consequence of the structure of the problem, i.e. the form of the concerns over the relative performance. In particular, it does not depend on the specific form of the individual risk measures (or equivalently, the drivers ). Finding the EMPR, later on in Section 4, leads to multi-dimensional quadratic BSDEs.

3.3 An example: the entropic risk measure case

We now illustrate the methodology and result of Theorem 3.2 for a particular risk measure, and prepare the ground for the model we study in Sections 5 and 6. We give a sequence of examples, in increasing order of complexity, that show how the structure of the optimal strategies is changing as features are added. As in the above, the examples do not yet take into account the market clearing condition but rather assume that a market price of risk is given. Nonetheless they give a flavor for the next section where the equilibrium market price of risk is derived.

Each agent is assessing her risk using the entropic risk measure for which the driver if given by

and is agent ’s risk aversion. This choice of relates to exponential utilities, and we have (see e.g. [Carmona2009], [FoellmerKnispel2011], [HuImkellerMuller2005] or [Rouge2000])

so that, equivalently, the agents are maximizing their expected (exponential) utility.

In what follows, the optimal strategies were computed using the techniques described so far and hence we omit the calculations. They boil down to finding the map arising from (2.5), then injecting it in (3.8) and (3.9) to obtain . We denote throughout by (for ) the optimal Nash equilibrium strategy.

3.3.1 The reference case of a single agent

For comparison, we first give the optimal strategy for a single agent who could trade liquidly in the stock of price and the derivative of price with (arbitrary and exogenously-given) market price of risk . She aims at minimizing her risk, with terminal endowment and trading gains . Here, other agents do not play a role. Since , it is easily found that . Injecting this in (3.9) yields the minimized driver ,

The minimized risk is then given by where is the solution to the BSDE with terminal condition and driver , while the optimal strategy is then given by

This result is expected and in line with canonical mathematical finance results. The particular structure of the optimal strategy follows from the fact that the second asset is correlated to the first when , and the inversion of the volatility matrix for the 2-dimensional price ,

The market faced by is complete, the driver for the minimized residual risk is affine and we have the explicit solution

The minimized risk measure is affine with respect to : the trend () in the prices leads to a constant risk reduction and the completeness of the market leads to an affine dependence on .

3.3.2 The reference case of a single agent that cannot trade in the derivative

It is also instructive, and will be useful later on, to look at the case where this single agent cannot trade in the derivative, and hence faces an incomplete market. We first enforce on (3.4), then we optimize over (see Remark 3.3). The minimized driver following the calculations is

Notice that is affine in the variable but retains the quadratic term in . The minimized risk is then given by where is the solution to the BSDE with terminal condition and the above driver , while the optimal strategy is

3.3.3 The case of multiple agents without relative performance concerns

We return to the full set of agents and take for all ; this is the setting covered in [HorstPirvuDosReis2010]. We find the minimized risk-driver for agent to be

The minimized risk is given by , where solves the BSDE with terminal condition and minimized driver , while the optimal strategies are given by

| (3.14) |

Observe that in this case the strategy followed by does not depend directly on the strategies of the other agents; its structure is the same as for the single agent case. However, when the price dynamics of the derivative is not fixed but emerges from the equilibrium, later on, the other agents’ strategies will appear indirectly via and .

3.3.4 The case of multiple agents without relative performance concerns in zero net supply

If one would want to take into account the endogenous trading of the derivative in the particular situation of pure risk trading, where one takes in (2.8), then the market price of external risk must be endogenously computed instead of being fixed arbitrarily as we have done so far.

It is not difficult to see, summing the last equation in (3.14) over and imposing the zero-net supply condition, , that this requires that . However the s are themselves found by solving a system of BSDEs which involve . Replacing by the expression above in the said system of equations leads to a fully coupled system of quadratic BSDEs that is hard to solve in general. We solve this problem with an alternative tool in Section 4.

3.3.5 The general case: multiple agents with performance concerns

In the general case (not assuming for all ), we obtain the minimal driver as being still

| (3.15) |

The minimized risk is then given by where is the solution to the BSDE with terminal condition and driver , while the optimal strategies are given by

| (3.16) | ||||

| (3.17) |

The general invertibility of the systems (3.16) and (3.17) given is guaranteed by Proposition 3.5.

3.3.6 The general case: multiple agents with performance concerns in zero net supply

If one imposes (2.8) with , implying that , then the linear system (3.17) for the investment in the derivative simplifies greatly and its solution is explicitly given by

| (3.18) |

Notice how the structure of the optimal investment strategy for the derivative in (3.18) is that of (3.14), scaled down by the factor . In Section 6 we study a model with two agents and computations will be done explicitly for the investment in the stock (i.e. the inversion of the system (3.16)).

3.4 Reduction to zero net supply

We now give an auxiliary result allowing to simplify the condition (2.8). We show how the initial holdings before/at the beginning of the game can be reduced to the case where . This allows us to apply (2.8) with , which will prove crucial in later computations. The reduction to is based on the monotonicity of the risk measures and the following lemma, stated from the point of view of one agent . The result is based on Lemma 3.9 in [HorstPirvuDosReis2010].

To avoid a notational overload, we omit explicit dependencies on in this subsection.

Lemma 3.8.

For a given MPR and admissible strategies , consider the dynamics of the residual risk BSDE

| (3.19) |

associated with the preferences of agent using an admissible strategy . Assume further that (3.19) has a unique solution for any given -measurable bounded terminal condition . Let . Then,

-

•

if minimizes the solution to (3.19) for a terminal condition ,

then is optimal for the terminal condition ; -

•

if minimizes the solution for a terminal condition ,

then is optimal for the terminal condition .

Proof.

We prove only the first assertion, as the second is equivalent. Let . Assume that is optimal for (3.19) with , i.e. for any one has . Define further, for any , the strategies

To show that for any where solves (3.19) with we first show an identity result between the BSDEs with different terminal conditions. The second step is the optimality.

Step 1: We show that the process solves BSDE

| (3.20) |

To this end, we reformulate (2.4) as a BSDE:

| (3.21) |

The difference between (3.19) and times (3.21) yields

In view of (3.4), we can manipulate the terms inside driver above and obtain

Given the assumed uniqueness of BSDE (3.19) the assertion follows.

This lemma intuitively states that an agent , owning at time a portion of units of , can be regarded as being in fact endowed with . One then looks only at the relative portfolio , which counts the derivatives bought and sold only from time onwards: the optimization problem is equivalent. The argument can be extended to all other agents. We note that this reduction is only possible because we do not consider trading constraints in this work, so that the strategies and are equally admissible.

For the rest of this work we assume that each agent receives at a portion666Many possibilities for this reduction to zero net supply exist, including endowing one agent with the total amount of derivatives or endowing each agent with their initial portions of the derivative . We make the judicious choice of for simplicity. of the derivative . By doing so, the market clearing condition in Definition 2.5 transforms into

and we refer to it as the zero net supply condition.

For clarity, we recall that agent now assesses her risk by solving the dynamics provided by BSDE (2.7) with terminal condition

| (3.22) |

(instead of that in (2.7)). Moreover, by applying the change of variables (3.1) to BSDE (2.7) with terminal condition (3.22), we reach

| (3.23) |

with given by (3.4) (and relates to via the change of variables (3.1)).

4 The equilibrium market price of external risk

In the previous section we saw how to compute the Nash equilibrium for a given market price of risk , without the global constraint on trading (market clearing condition). In this section we solve the equilibrium problem, as posed by Definition 2.5, by finding the Equilibrium Market Price of external Risk (EMPeR) .

The literature contains many results on equilibria in complete markets that link competitive equilibria to an optimization problem for a representative agent, and this is the approach we use here. The preferences of the representative agent are usually given by a weighted average of the individual agents’ preferences with the weights depending on the competitive equilibrium to be supported by the representative agent, see [Negishi1960]. This dependence results in complex fixed point problems which renders the analysis and computation of equilibria quite cumbersome. The many results on risk sharing under translation invariant preferences, in particular [BarrieuElKaroui2005, JouiniSchachermayerTouzi2006, FilipovicKupper2008], suggest that when the preferences are translation invariant, then all the weights are equal. This was an effective strategy in [HorstPirvuDosReis2010] and it would be so here if, for all , , or .

In a market without performance concerns, [HorstPirvuDosReis2010, BarrieuElKaroui2009] show that the infimal convolution of risk measures gives rise to a suitable risk measure for the representative agent which, for -conditional risk measures, corresponds to infimal convolution of the drivers. Due to the performance concerns, we use a weighted-dilated infimal convolution and, in Theorem 4.5 we show that indeed minimizing the risk of our representative agent is equivalent to finding a competitive equilibrium in our market.

4.1 The representative agent

Aggregation of risks and aggregation of drivers

Inspired by the above mentioned results and having in mind [Rueschendorf2013] (see Remark 4.9 below) we deal with the added inter-dependency arising from the fixed-supply condition and the additional unknown (see examples in 3.3.4 and 3.3.6) by defining a new risk measure . For a set of positive weights satisfying , we define

| (4.1) |

In the case of risk measures induced by BSDEs, [BarrieuElKaroui2005] shows that the measure defined by inf-convolution of risk measures is again induced by a BSDE, whose driver is simply the inf-convolution of the BSDE drivers for the risk measures . For the set of weights , we define the driver as the weighted-dilated inf-convolution of the drivers for ,

| (4.2) |

where the notation is that of the standard inf-convolution.

Lemma 4.1 (Properties of ).

The map defined by (4.2) is a deterministic continuous function, strictly convex and continuously differentiable. Moreover, there exists a unique solution of in .

For a such that , one has if and only if there exists such that, for all , . In that case, one has .

Proof.

The weighted inf-convolution transfers the properties of the ’s to , in particular continuity, strict convexity and differentiability. We do not show these as they follow from a simple adaptation of known arguments, see [BarrieuElKaroui2005, BarrieuElKaroui2009, HorstPirvuDosReis2010].

Since the function being minimized () is convex and the function defining the constraint () is also convex, because affine, the minimization defining is equivalent to finding a critical point for the associated Lagrangian, . Therefore, for a such that , is a minimizer if and only if there exists such that, for all , . Then, where is the Lagrange multiplier associated with . ∎

The risk of the random terminal wealth , measured through , is given by where is the solution to the BSDE

| (4.3) |

Since the weights are required to satisfy , the risk measure associated to the BSDE with the above driver is a monetary risk measure. Translation invariance and monotonicity follow from the fact that the driver is independent of . Convexity follows from the convexity of , which in turns follows from that of the ’s by the envelope theorem.

Remark 4.2.

Notice that (4.2) can be rewritten

In this way, is seen as the usual -weighted infimal convolution of the -dilated drivers , in the terminology from [BarrieuElKaroui2009] (p.137). For more on dilated risk measures, see Proposition 3.4 in [BarrieuElKaroui2009].

Example 4.3 (Entropic risk measure).

For entropic agents, i.e. with drivers , one obtains

| (4.4) |

Trading and the risky position of the representative agent

Having defined the aggregated risk measure and the associated driver , we now introduce a strategy and associated trading gains for a representative agent whose preferences are described by . Direct computations from (4.1) entail that we assign to the representative agent the terminal gains

where , is the representative agent’s portfolio, is the representative agent’s wealth process and

| (4.5) |

is defined as the representative agent’s terminal endowment.

We now choose the weights such that for any for some , i.e.

| (4.6) |

Direct verification yields and, furthermore, for all ,

Notice that . In other words, the zero net supply condition for the individual agents (i.e. ) is equivalent to the representative agent not investing in (i.e. ). From now on, the family of weights is fixed and is given by (4.6).

The pointwise minimizer for the representative agent’s residual risk

We now show that the approach by aggregated risk and representative agent, as motivated above, allows to identify the equilibrium market price of risk as a by-product of minimizing the risk of the representative agent. This risk is given by the solution to BSDE (4.3) with terminal condition , for admissible strategies of the form . The -valued strategy process is said to be admissible () if and the BSDE (4.3) has a unique solution. Following Section 3 we introduce the residual risk processes

The pair satisfies the BSDE with terminal condition and random driver , defined for , by

where (compare with (3.1)-(3.4)). Since , the representative agent then equivalently aims at solving for .

Following the methodology used for the single agent in Section 3, we first look at minimizing the driver pointwise. We define as the optimizer for , setting as to enforce the zero-net supply condition. Since is strictly convex, so is the function , and the minimum is characterized by the solution to first-order condition

We denote the minimized (random) driver by

| (4.7) |

Remark 4.4 (The structure for the optimized driver (4.7) under a separation assumption).

Here, unlike for the optimization of individual agents who trade in and under a fixed MPR , we do not have a nice structure like in (3.9) for in all generality on (hence on the ’s).

Assume that for some we have , then the first-order condition would translate to . Denoting by the solution in to the equation , the structure for is given by

and the structure for the optimized driver is given by

The special case of entropic drivers, that falls in this category, is discussed below in Example 4.6.

Optimimality for the representative agent and the equilibrium market price of external risk

We assume that the BSDE with driver defined in (4.7) and terminal condition has a unique solution in . Define the strategy by . Like for the individual agents in Section 3, the following theorem asserts that is the optimal strategy and is the minimized risk for the representative agent. Moreover, the theorem relates the equilibrium market price of risk (EMPR) (recall Definition 2.5) to the solution of the representative agent’s optimization problem. Recall the family of weights given by (4.6).

Theorem 4.5.

Assume that

-

•

the BSDE with driver , (4.7), and has a unique solution in ,

-

•

the comparison theorem holds for the BSDE with driver ,

-

•

is integrable against the prices and ,

then is the minimized risk for the representative agent and is the unique optimal strategy that minimizes his risk.

If, for the process , with defined by

| (4.8) |

the conditions of Theorem 3.5 hold, then is the unique EMPR for the agents in .

Additionally, the minimized aggregated risk is linked to the individual minimized risks through the identity (the same holds for ). Moreover, the Nash equilibrium for the agents in satisfies .

Example 4.6 (The entropic case).

In the entropic case, we have found , so we have . The minimized driver is then

as was found in Subsection 3.3. This driver is quadratic and regular, and the terminal condition is bounded. From [Kobylanski2000, ImkellerDosReis2010] there is a unique solution in and the comparison theorem applies (see [Kobylanski2000, MaYao2010]). The optimal strategies are

With and bounded, is integrable against . This verifies the first three assumptions of the theorem. Furthermore, with (4.8) and since and is bounded, we find that

| (4.9) |

Following on Remark 3.3, the optimality of and , for an agent with preferences described by and trades in , is obtained exactly in the same way as the optimality for a single agent in Theorem 3.2. So we prove only the claims of Theorem 4.5 related to the EMPR . First, however, we state a counterpart to Lemma 3.4 to the case when no trading in is possible.

Lemma 4.7.

Under the assumptions of Theorem 4.5, let be an admissible strategy and be the associated risk process, i.e. the solution to the BSDE with driver and terminal condition . Assume that the FOC holds for these processes, i.e.

Then and .

Proof.

Recalling the properties of (see Lemma 4.1) and the definition of , the condition means that . We have then (recall (4.7)). By the assumed uniqueness of the solution to the BSDE with driver and terminal condition , we have . Consequently, by the uniqueness of the FOC’s solution, . Since both strategies have second component equal to zero, we have therefore . ∎

The next result, to be used in the proof of Theorem 4.5, states that aggregating the solutions to the individual optimization problems leads to an optimum for the aggregated preference and identifies the BSDE of the aggregation with the weighted sum of the agents’ BSDEs.

Lemma 4.8.

Let be a MPR and assume the conditions of Theorem 3.5. Let then be the unconstrained Nash equilibrium associated with , and let be the solution to the minimized-risk BSDE for each agent (BSDE (3.2) with driver (3.9)). Define and .

Then and are the minimal risk and optimal strategy for a single agent whose preferences are given by , who can invest in (without trading constraints).

Proof.

Proof of Theorem 4.5.

The first part of the proof of the theorem, the optimization for the representative agent, follows through arguments similar to those used in the single agent case, see Theorem 3.2 and Remark 3.3. Hence we omit it.

Existence of the EMPR. Here we prove that , defined through (4.8), is indeed an EMPR. Since and the conditions of Theorem 3.5 hold, let be the unique unconstrained Nash equilibrium under the MPR , and let be the solution to the minimized-risk BSDE for each agent . Our goal now is to prove that .

Let us introduce and . From Lemma 4.8, and are the optimal strategy and risk for a single agent with risk preferences encoded by trading and under without trading constraints.

Meanwhile, we defined as the optimal strategy for an agent with preferences encoded by and who can only invest in (with MPR ). By construction of , we have

It results from Lemma 3.4 that is also the optimal strategy for an agent with preferences and who can invest in and , with given MPR . By the uniqueness in Lemma 3.4 we therefore have . This implies in particular that . We have therefore proved that the Nash equilibrium associated with satisfies the zero-net supply condition, hence the constructed is an EMPR.

Uniqueness of the EMPR. Assume that is also an EMPR and let be the associated Nash equilibrium for which, by definition of EMPR, the zero-net supply condition is satisfied. Let also be the solution to the minimized-risk BSDE for each agent . As above, we define and . By Lemma 4.8, we obtain that and are optimal for an agent who trades in and under the given MPR for a single agent economy. Consequently, using the characterization between the optimizer and the FOC condition, we have

where as is an EMPR. By Lemma 4.7, the first equation guarantees that and are optimal for an agent with preferences who trades in . By the construction of and (for the MPR ), and the uniqueness recalled in Lemma 4.7, we have and . As a consequence, we have from the second FOC equation

Hence the uniqueness of the EMPR . ∎

From Theorem 4.5 we point out that is only a MPR for the representative agent’s economy as the representative agent trades in an incomplete market where she is not able trade the risk from — recall (2.1). Nonetheless, is the only MPR leading to a complete market for the agents where the Nash equilibrium they form satisfies the zero net supply condition. We close this remark by adding that the representative agent approach for complete market leads to Arrow-Debreu equilibria for the acting agents (see [HorstPirvuDosReis2010, KardarasXingZitkovic2015] and references therein).

Remark 4.9.

In [Rueschendorf2013] a “weighted minimal convolution” of risk measures is introduced via

(see page 271, Equation (11.25)) for and for some .

Observe that aggregation in our context would not work without the dilation weights in the argument of the driver. This can be seen in Step 2 of the proof of Theorem 4.5. The reason is that is the sum of with the strategies plugged in as arguments and of an additional term with the strategies multiplied by the weights. For the aggregation as a single strategy this adjustment is necessary.

4.2 A shortcut to the EMPeR in the case of entropic risk measures

In the previous subsection we gave a result on the existence and uniqueness of the equilibrium market price of risk via the inf-convolution of the risk measures, for general preferences. In the particular case of the entropic risk measure, the general computations are considerably simpler and an easier path allows to compute what the EMPeR is (if it exists) without the representative agent. Although the BSDE for the representative agent derived above will appear in the following computations, with only these computations one cannot show that the computed is indeed an EMPR. This shorter path consists, as was hinted in Section 3.3.4, in a direct linear combination of the BSDEs (3.2) with the minimized driver given by (3.15).

Following the computations from Section 3.3.5, we see that the market clearing condition requires

if we define , with and . Notice that here we do not need to normalize the family so that , since we are not considering an aggregated risk measure. Any rescaling of would give the same . We present it in this way for consistency with the general case.

Now, replacing the term by the above value in the minimized driver given by (3.15), we find that the optimal risk processes for each agent solve the BSDEs with driver given by

| (4.10) |

The BSDEs with these drivers form a system of coupled BSDEs with quadratic growth, which, in general, are difficult to solve, see [EspinosaTouzi2015], [Espinosa2010], [FreiDosReis2011] or more recently [Frei2014, KramkovPulido2016]. Fortunately, one can take advantage of the structure of (4.10) and find a simpler BSDE for the process . It is easily seen that , as in (4.5). Linearly combining the BSDEs (3.2) with drivers expressed as in (4.10), we find

| (4.11) |

This is exactly the same BSDE as in Example 4.6. Given that and are bounded, this BSDE falls in the standard class of quadratic growth BSDE and the existence and uniqueness of is easily guaranteed. This allows one to compute as and in turn one can finally solve the BSDEs giving the minimized risk processes for each agents, using the driver as given by (3.15).

Remark 4.10 (No trade-off between risk tolerance and performance concern rate).

Each agent’s individual preferences are specified by the parameters and , i.e. risk tolerance and performance concern respectively. One may ask whether a parametric relation between those parameters exists such that an agent with and another agent with would exhibit the same behaviour and have the same optimal strategies. Indeed, in most formulas the two parameters appear as coupled. However, one can see that the terminal condition is independent of the risk tolerance parameter , hence by changing and of any one fixed agent , one cannot obtain the same outcome.

5 Further results on the entropic risk measure case

In this section we investigate further the entropic case. We introduce a structure that allows to use the theory developed in the previous section and, moreover, to design such that Assumption 3.1 holds true. The ultimate goal of this section is to understand how the concern rates affect prices and risks. The first two parts of the section verify that Assumption 3.1 holds and the third sheds light on the behavior of the aggregated risk and derivative price as the parameters vary.

We now make further assumptions (commented below) on the structure of the random variables introduced Section 2. Namely, we assume that the endowments for and the derivative have the form

| (5.1) |

for some deterministic functions . This structure for the derivative and endowments is interpreted as each agent receiving a lump sum at maturity time .

To ease the analysis we will assume throughout a Black-Scholes market (i.e are constants). Such an assumption is not strictly necessary for the results we obtain here, but we wish to focus on the qualitative analysis and not on obfuscating mathematical techniques. Throughout the rest of this section the next assumption holds.

Assumption 5.1.

Let Assumption 2.1 hold. Let and (and hence also . For any the functions are strictly positive, their derivatives are uniformly Lipschitz continuous w.r.t. the non-financial risk and satisfy for any .

The assumption concerning the strict positivity of the involved maps or that are the key in proving that Assumption 3.1 is indeed verified for the example we present. The assumption on the form of and reduces the BSDE to the Markovian case, giving us access to the many existing BSDE regularity results, which we will use below in their full scope. It would be possible (this is left open to future research) to remain in the non-Markovian setting of general -measurable and and use link between non-Markovian BSDE and path-dependent PDEs (see e.g. [EkrenKellerTouziEtAl2014]). Indeed, tools on general Malliavin differentiability of BSDE solutions in the non-Markovian setting can be found in [AnkirchnerImkellerReis2010] or in more generality in [DosReis2011, MastroliaPossamaiReveillac2014].

We recall that our goal, in the example below, is to analyze the impact of the parameters on the risk processes (single and representative agent), derivative price process and EMPeR.

Remark 5.2 (On notation for the section).

In this section we work mainly with the representative agent BSDE (see Example 4.6 or (4.11)) and the derivative price BSDE (3.21).

To avoid a notation overload in what the BSDE for the representative agent is concerned, we drop the tilde notation and define as the solution to the mentioned BSDE; not to be confused with (4.3) which plays no role here. The solution to the derivative price BSDE is denoted by .

5.1 The aggregated risk

The BSDE (4.11) is not difficult to analyze given the existing literature on BSDEs of quadratic growth. Recall that and (since it is a weighted sum of bounded random variables). We shortly recall that is the space of 1st order Malliavin differentiable processes and denotes the Malliavin derivative operator, we point the reader to Appendix A.1 for further Malliavin calculus references.

Theorem 5.3.

The BSDE (4.11) has a unique solution . Moreover, there exists a strictly negative function such that for any

-

i)

For any , it holds that

and in particular -a.s. for any .

-

ii)

There exists a constant such that for any , i.e. and . Moreover, .

-

iii)

The process belongs to .

Proof.

By assumption we have and which allows to quote Theorem 2.6 in [ImkellerDosReis2010] and hence that . Moreover, given that , a strict comparison principle for quadratic BSDEs (see e.g. [MaYao2010]*Property (5)) yields easily that for any and hence that .

Proposition A.3 ensures that the payoffs and , and hence , are Malliavin differentiable with bounded Malliavin derivatives. Combining this further with , the Malliavin differentiability of (4.11) follows from Theorem 2.9 in [ImkellerDosReis2010]. Under Assumption 5.1 the results in [ImkellerDosReis2010] (or Chapter 4 of [DosReis2011]) along with Theorem 7.6 in [AnkirchnerImkellerReis2010] yield the Markov property for and the parametric differentiability result for the (quadratic) BSDE.

Proof of i): Since by direct application of the Malliavin differential we have for

It now follows that for any -a.s..

Proof of ii): Define now the probability measure (equivalent to ) as

| (5.2) |

The measure is well defined since and . Then for we have (Theorem 2.9 in [ImkellerDosReis2010])

| (5.3) | ||||

The results in Proposition A.3 and the definition of imply that . Path regularity results for BSDEs along with their usual representation formulas (see [ImkellerDosReis2010]) yield that ; the boundedness of follows in an obvious way. As a consequence, since and (4.9) holds.

Proof of iii): Using now the fact that , we apply Theorem 2.6 in [ImkellerDosReis2010] to (5.3) and obtain that . The BMO norm of depends only on some real constants and , , and (see again Theorem 2.6 in [ImkellerDosReis2010]). ∎

In the next result we show that the mapping is Lipschitz. Denote by and the solutions to (2.1) with and respectively; denote as well by and the solutions to BSDE (4.11) for the underlying processes and respectively.

Proposition 5.4.

For any the map is Lipschitz continuous uniformly in and . In particular the process is -a.s. bounded.

Proof.

Let and define , for and (intuitively) . Then, following from (5.3) written under from (5.2), we have

Define now the process

| (5.4) |

where the integrability of follows from Lemma A.1. Observe next that by the results of Theorem 5.3 one has . Applying Itô’s formula to , using the just mentioned identity and taking -conditional expectations it follows at that

The last line is a consequence of Proposition A.3 combined with the fact that () is finite due to the BMO properties of , see Lemma A.1. The constant is independent of and . Although is a BMO martingale under , the integrability still carries under ; this is the same argument as in the final step of the proof of Lemma 3.1 in [ImkellerDosReis2010] (see also Lemma 2.2 and Remark 2.7 of the cited work).

The extension of the above result to the whole time interval follows via the Markov property of the BSDE solution. This relates to the close link between BSDEs of the Markovian type and certain classes of quasi-linear parabolic PDEs (see e.g. Section 4 in [ElKarouiPengQuenez1997]).

Finally, the boundedness of follows from the Lipschitz property of and the boundedness of , see Proposition A.3, ii). ∎

5.2 The EMPR and the derivative’s BSDE

Theorem 5.5 (Market completion).

The derivative completes the market, i.e. -a.s. for any . Moreover, and for any .

Before proving the above result we need an intermediary one. Recall that BSDE (3.21) describes the dynamics of the price process , that and (following from Assumption 5.1 and Theorem 5.3).

Proposition 5.6.

The pair belongs to and their Malliavin derivatives satisfy for the dynamics

| (5.5) |

The representation holds -a.s. for any .

Proof.

Let . Observe that BSDE (3.21) is a BSDE with a linear driver and a bounded terminal condition. The existence and uniqueness of a solution follows from the results of [ElKarouiPengQuenez1997]. Moreover, the estimation techniques used in [ImkellerDosReis2010] yield that (see Theorem 2.6 in [ImkellerDosReis2010]). The Malliavin differentiability of follows from Proposition 5.3 in [ElKarouiPengQuenez1997] and the remark following it since (see Theorem 5.3). The quoted result and Proposition A.3 yield (5.5) for . Moreover, from Theorem 2.9 in [ImkellerDosReis2010] we have for -a.e..

We now prove a finer result on and , namely that holds -a.s. for any instead of just -a.e.. This is done by showing that is jointly continuous.

Remark that the map for is given by (5.5) and hence it is continuous in time (). Note now that Proposition 5.4 and Proposition A.3 yield that is bounded and for any . These properties hold as well for via the identity .

Using the measure (introduced in (2.3)), that and the identity , one can rewrite (5.5) as

| (5.6) |

Writing the same BSDE as above, but for a parameter (instead of ) we have

where we used the results of Proposition A.3. Since the solution to (5.6) is unique and the BSDE just above has exactly the same parameters as (5.6), we must conclude that for any and for it holds . From the continuity of follows now the joint continuity of in its time parameters and hence the representation holds -a.s. for any . ∎

We can now prove Theorem 5.5.

Proof of Theorem 5.5.

We proceed in the same way as in the proof of Proposition 5.4. The argument goes as follows: define the process just like in (5.4); apply Itô’s formula to and write the resulting equation under (just like (5.6)); take conditional expectations. At this point a remaining Lebesgue integral is still in the dynamics:

where from the first to the second line we used Proposition 5.6, i.e. that -a.s. for any .

Recalling and the dynamics of given by (2.1), we see that (by the chain rule) . Since is either always positive or always negative and since -a.s. for any , it follows that -a.s. for all . More precisely, depending on the sign of , is -a.s. either always positive or always negative777For any positive random variable ( -a.s.) one has for any sigma-field . Since the measure change is done for a strictly positive density function, the inequality for the new conditional expectation is still strict., giving . ∎

5.3 Parameter Analysis

It is possible to justify at a theoretical level some of the predictable behavior of the processes , and with relation to the problem’s parameters: , , and for .

Theorem 5.7.

Let be the EMPR. The process solving BSDE (4.11) is differentiable with relation to for any , and (see (4.4) and (4.6)).

Fix agent . If the differences

| (5.7) |

are positive (negative respectively) then is negative (positive respectively) for any .

For any we have that

Furthermore,

Part of the results are in some way expected. Introducing more derivatives leads to an overall risk reduction and as more derivatives are placed in the market, the derivative is worth less (per unit). If is interpreted as the representative agent’s risk tolerance, then as increases we have a decrease in risk ( decreases) since it represents an increase in the single agents’ risk tolerance (i.e. ).

The main message of the above theorem is that the effect of the performance concern of one agent on the aggregate risk depends essentially on how the agent is positioned with respect to the others, both in terms of risk tolerance as well as the personal endowments. If the agent’s risk tolerance is higher than the aggregate risk tolerance and her endowment position dominates by the aggregate endowment position, then an increase in the agent’s concern rate leads to an increase of the aggregate risk.

Before proving the above result we remark that condition (5.7) simplifies under certain conditions; such simplifications are summarized in the below corollary. All results follow by direct manipulation of the involved quantities.

Corollary 5.8.

Let the conditions of Theorem 5.7 hold.

If for all , then .

If , then and hence

Similarly and . Moreover, it holds that

| (5.8) |

Proof of Theorem 5.7.

Let and . Theorem 3.1.9 in [DosReis2011] (see also Theorem 2.8 in [ImkellerDosReis2010]) ensures the differentiability of BSDE (4.11) with respect to , , and .

The derivative of in : Applying to BSDE (4.11) and writing it under the probability measure defined in (5.2) yields the dynamics

Taking -conditional expectations and noticing that the Lebesgue integral term is strictly negative for any , we have then for any .

The derivative of in : This case follows from the previous one as is defined by (4.4) and the weights (see (4.6)) are independent of .

and finally . The statement follows.

The derivatives of in : We compute only the derivatives with respect to in order to present simplified calculations as . Calculating the involved derivatives leads to

Combining the above results with the BSDE for under the -measure (just as in the previous two steps) yields

Since is equivalent to , the statement follows.

The derivative of in : Applying to BSDE (4.11) and writing it under the probability measure defined in (5.2) yields the dynamics

where the last sign follows from the definition of and .

The derivative of in : The analysis of and hence of with respect to and follows from the analysis of (5.3). Given representation (4.9), applying to BSDE (5.3) and writing it under the probability measure defined in (5.2) yields the dynamics

where is as in (5.4) and the argumentation is similar to that back there. Notice now that with the terminal condition we have

Given Assumption 5.1, we are able to conclude that , and hence, from (4.9) that .

The derivative of in : We use justifications similar to those used in Proposition 5.6 and hence we do not give all the details. Recall (3.21), apply the -operator to the equation and do the usual change of measure (with ) to obtain

By the previous result we have and from Theorem 5.5 we have . It easily follows that . ∎

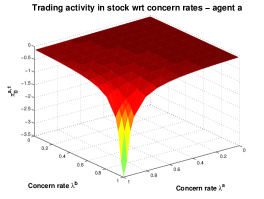

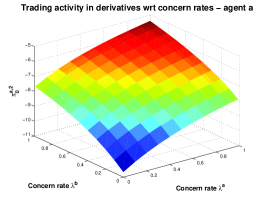

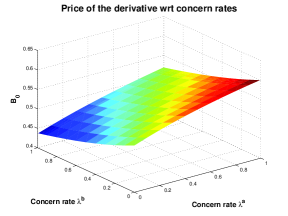

Unfortunately the conditions used above do not allow for similar results on the behavior of, say or . The conditions required for such results are too restrictive to be of any usefulness. Nonetheless, we will investigate them in Section 6 via numerical simulation.

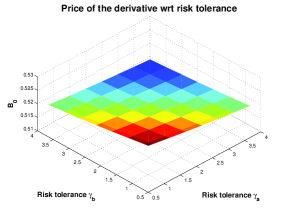

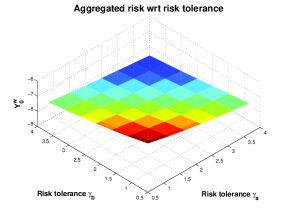

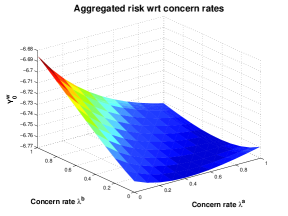

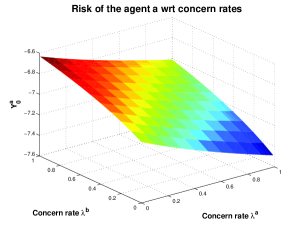

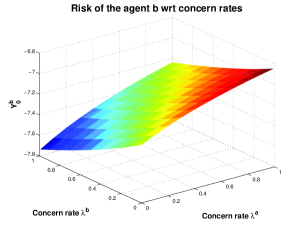

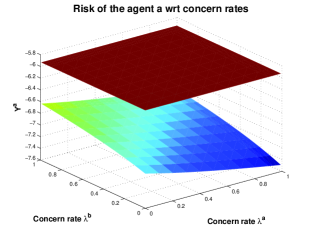

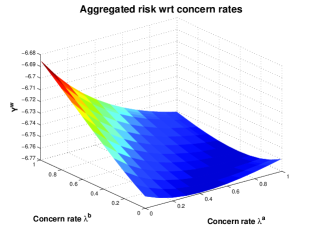

6 Study of a particular model with two agents

In this section, we investigate a model economy consisting of two agents using entropic risk measures and having opposed exposures to the external non-financial risk. We give particular attention to the impact of the relative performance concern rates on the equilibrium related processes. The model is simple enough to allow extended tractability, when compared with Sections 3, 4 and 5, and nonetheless still sufficiently general as to produce a rich set of results and interpretations. In particular, we explicitly describe the structure of the equilibrium. Using numerical simulations, we are able to explore the dependence of individual quantities (such as the optimal portfolios and minimized risks ) on the various parameters, thus complementing the results in Theorem 5.7.

6.1 The particular model and numerical methodology

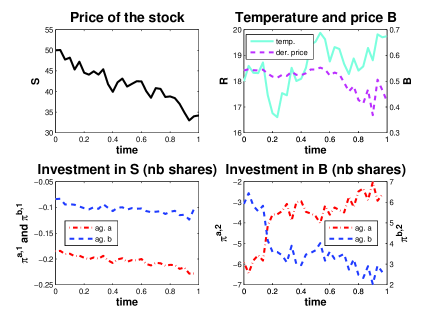

We consider a stylized market consisting of two agents. We argue that a larger set of agents with certain exposures to the external risk can be clustered in two groups: those profiting from the high values of and those profiting from the low values of , and we can apply the weighted aggregation technique used in Section 4 to each group. Our two agents can therefore be thought of as representative agents for each group. The external risk process is taken to be the temperature affecting the two agents, who also have access to a stock market.

Temperature and Stock models

We study one period of one month () We study one period of month where the temperatures follow an SDE (2.1) with constant coefficients:

and for the stock we take a standard Black–Scholes model:

where the coefficients are , and for the temperature process, and , and (so ) for the stock price process.

Agents’ parameters, endowments and the derivative

Define . The agents’ endowments, and , are taken to be

Agent profits from higher temperatures while agent profits from lower ones. The derivative has a payoff that does not depend on the stock , and is given by

so that it allows to transfer purely the external risk. All functions satisfy Assumptions 2.1 and 5.1. Given the agents’ opposite exposures to and the design of , agent will act as a seller while agent will act as the buyer, thus establishing a viable market for the derivative.

We assume throughout that the total supply of derivative is zero, , i.e. every unit of derivative one agent owns is underwritten by the other. The risk tolerance coefficients of the agents are fixed at unless we are analyzing some behavior with respect to them. Similarly, unless otherwise specified, the concern rates are fixed to be unless we are analyzing some behavior with respect to them.

The numerical procedure

The simulation of the processes involves a time discretization and Monte Carlo simulations. We use directly the forward processes’ explicit solutions; all BSDEs are solved numerically. Regarding their time discretization, we use a standard backward Euler scheme, see [BouchardTouzi2004], and we complement the time-discretization procedure with the control variate technique stated in Section 5.4.2 of [LionnetReisSzpruch2015]. The approximation of the conditional expectations in the backward induction steps is done via projection over basis functions, see the Least-Squares Monte Carlo method used in [GobetTurkedjiev2014].