Symmetric matrices, Catalan paths, and correlations

Bernd Sturmfels

, Emmanuel Tsukerman

and Lauren Williams

Abstract.

Kenyon and Pemantle (2014) gave a

formula for the entries of a square matrix in terms

of connected principal and almost-principal minors.

Each entry is an explicit Laurent polynomial whose terms

are the weights of

domino tilings of a half Aztec diamond. They conjectured an

analogue of this parametrization for symmetric matrices,

where the Laurent monomials are indexed by Catalan paths.

In this paper we prove the Kenyon-Pemantle conjecture,

and apply this to a statistics problem pioneered by Joe (2006).

Correlation matrices are represented by an explicit

bijection from the cube to the elliptope.

1. Introduction

In this paper we present a formula for each entry of a

symmetric matrix

as a Laurent polynomial in

distinguished minors of . Our result verifies a conjecture of

Kenyon and Pemantle from [3].

Let and be subsets of with

.

Let denote the minor of with row indices and column indices .

Here the indices in and are always taken in increasing order.

The following signed minors will be used:

We call and the principal

and almost-principal minors, respectively.

The minors , and are called connected

if and .

The -minors

and are connected when

and .

These definitions make sense for every matrix ,

even if is not symmetric.

A general matrix has principal minors,

of which are connected. It also has

almost-principal minors, of which are connected.

A symmetric matrix has

distinct almost-principal minors

, of which are connected.

A Catalan path is

a path in the -plane which starts at and ends on the -axis,

always stays at or above the -axis, and

consists of steps

northeast and southeast .

We say that has size if its endpoints

have distance from each other.

Let denote the set of Catalan paths of size .

Its cardinality equals the Catalan number

Let denote the planar graph whose vertices

are the lattice points with

and even,

and edges are northeast and southeast steps.

Thus consists of the paths from to in .

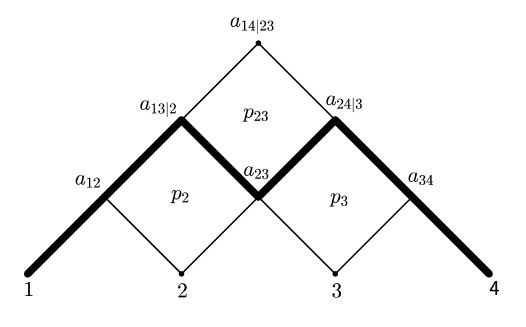

We label the nodes and regions of as follows.

We assign label to the node , label to the node ,

and label to the region below that node.

Thus, connected principal and almost-principal minors of

are identified in the graph

with regions and nodes strictly above the -axis.

The weight of a Catalan path

is a Laurent monomial, derived from the drawing of

in the graph . Its numerator is the product

of the labels of the nodes of that are local maxima

or local minima of ,

and its denominator is the product of the labels of the regions

which are either immediately

below a local maximum or immediately above a local minimum.

Thus is a Laurent monomial of degree .

There is no lower bound on the degree;

for instance, has degree and

appears for .

The following result was

conjectured by Kenyon and Pemantle in

[3, Conjecture 1].

Theorem 1.1.

The entries of an symmetric matrix satisfy the identity

(1)

where the sum is over all Catalan paths between

node and node in

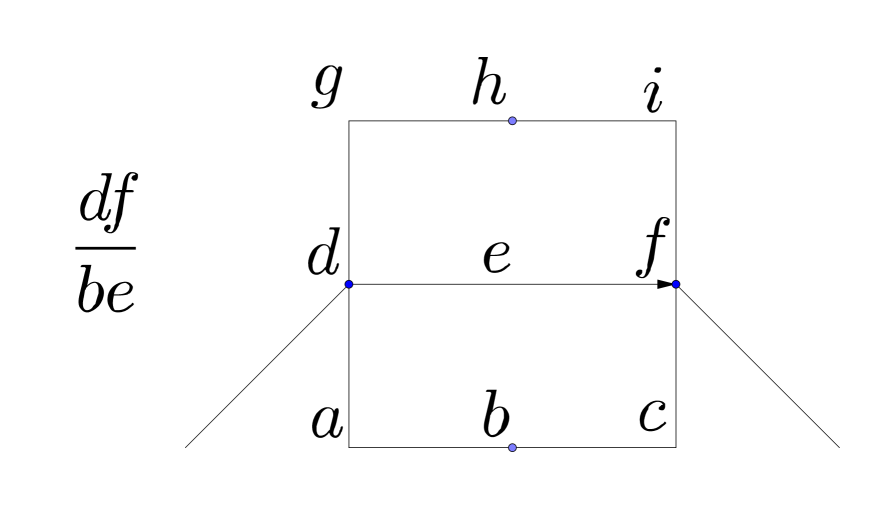

Figure 1. A Catalan path in the planar graph

with weight

.

For symmetric matrices of size , Theorem 1.1 states the

following formula:

(2)

The entry is the sum of

five Laurent monomials, one for each Catalan path

from node to node .

The last term

equals for the path

shown in Figure 1.

The proof of Theorem 1.1

is given in Section 4.

We start in Section 2 by reviewing

a theorem of Kenyon and Pemantle [3]

which expresses the entries of an arbitrary square matrix in terms of almost-principal and principal minors,

as a sum of Laurent monomials that are in bijection with domino tilings of a

half Aztec diamond. In Section 3,

we give a bijection between these domino tilings and

Schröder paths, and restate their theorem using Schröder paths.

We then prove our theorem

by constructing a projection from

Schröder paths to Catalan paths and applying the relation (7)

among minors of symmetric matrices.

In Section 5 we connect Theorem 1.1

to an application in statistics, developed in work of

Joe, Kurowicka and Lewandowski [2, 5].

Namely, we focus on symmetric matrices that are positive

definite and have all diagonal entries equal to .

These are the correlation matrices, and they

form a convex set that is known in optimization as the elliptope [1, 4].

Our formula yields an explicit bijection between

the elliptope and the open cube .

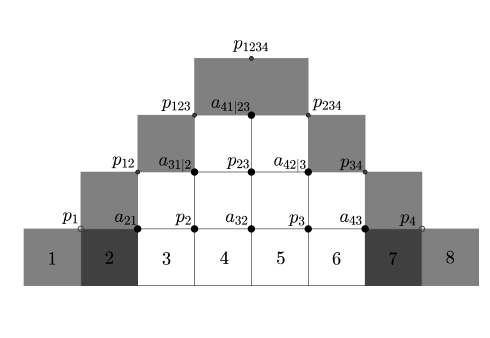

2. Square matrices and tilings of the half Aztec diamond

In this section we review the Kenyon-Pemantle formula in [3, Theorem 4.4].

The half Aztec diamond of order is the

union of the unit squares whose vertices are in the set

We label the boxes in the bottom row of by the numbers through , from

left to right.

We label certain lattice points of by minors

as follows. Fix .

The connected principal minors such that

are assigned to the lattice points with even.

The connected almost-principal minors with and

are assigned to the lattice points with odd.

In both cases, the assignment is from left to right using

the lexicographic order on .

The case is shown in Figure 2.

Figure 2. The half Aztec diamond .

The white boxes are to be tiled.

Fix integers and such that is even, is odd, and

. We define the colored half Aztec diamond

by coloring the boxes of black, grey, or white.

First color boxes and in the bottom row black.

Let be the diagonal line of slope through box ,

and let be the line of slope through box .

If a box (or any part of it) lies to the left of or to the right of , then color it grey.

All other boxes are white.

A domino

tiling (or simply a tiling)

of is a tiling of the white boxes by

and rectangles.

Let denote the set of tilings of .

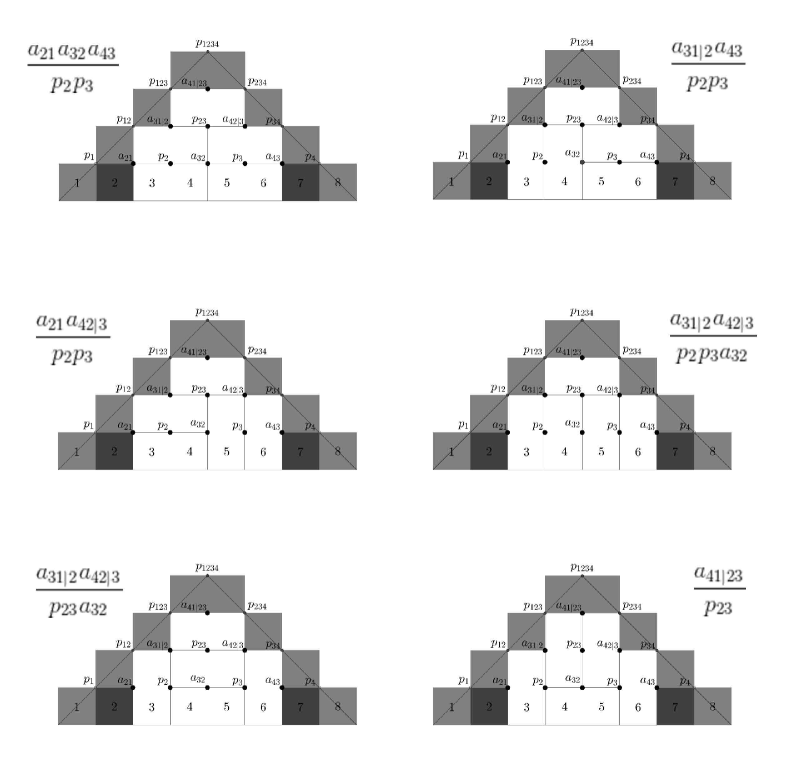

Figure 3

shows the set , i.e. the six tilings of , with lines

and superimposed on the tilings.

Figure 3.

The six tilings of

the colored half Aztec diamond .

Each tiling of the colored half Aztec diamond

gets a Laurent monomial weight, which we now define.

We regard as a simple graph whose nodes

are the lattice points of

, and whose edges are induced

by the edges of the rectangles in the tiling together with the

edges of the unit squares outside the tiling.

An interior lattice point of is a lattice point which lies strictly

to the right of and strictly to the left of . The interior lattice points

that will concern us are shown in bold in Figures

2

and 3.

Each of these is labeled by a variable

which is a connected principal or almost-principal minor.

The weight of a tiling is defined to be

the Laurent monomial

where ranges over the interior lattice points of and

is the degree of in .

Theorem 4.4 in [3] also gives a similar formula for

with , but we omit that formula, as it is not needed here.

Example 2.2.

Figure 3 shows the six tilings of with

their weights. By Theorem 2.1,

the upper right matrix entry for is

the sum of these six Laurent monomials:

(3)

The full matrix is shown

on page 8 of [3], albeit with different notation.

3. Square matrices and Schröder paths

In this section we continue our discussion

of arbitrary square matrices.

A Schröder path is a path in the -plane which starts at ,

always stays at or above the -axis, and

consists of steps which are either

northeast , southeast , or horizontal .

A Schröder path has order if it ends at .

Let denote the planar graph whose

nodes are the lattice points with

and even,

with edges given by northeast, southeast and horizontal steps.

The set of Schröder paths of order

is identified with the left-to-right paths in from

to .

The cardinality of is the Schröder number,

which is given by the generating function

The graph is labeled by connected minors.

We assign to the node for ,

and we assign to the triangle below that node.

We refer to as node .

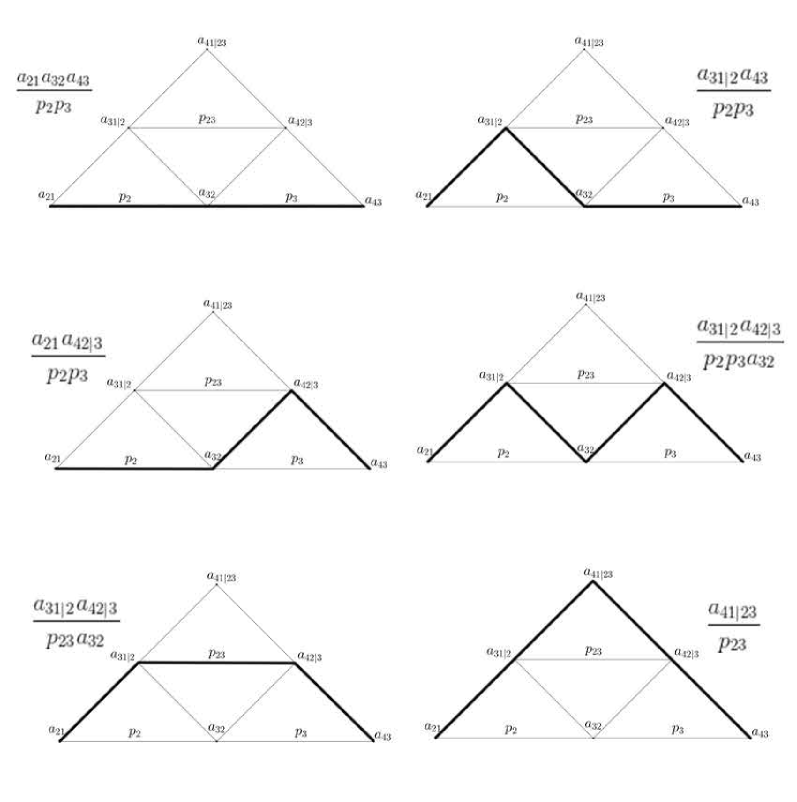

Figure 4 shows the case .

The six Schröder paths in

are shown in Figure 6.

Figure 4. The graph encodes the Schröder paths of order .

We now define the weight of a Schröder path on .

We regard as a graph with vertices and edges .

Given a Schröder path on ,

we define the sets

Each of these is regarded as a monomial

by taking the product of all labels.

Then we define

(4)

Figure 6 shows

the six Schröder paths for , together with their weights.

The sum of these weights is the Laurent polynomial in (3),

which evaluates to the matrix entry .

The main result of this section is a reformulation of Theorem 2.1

in terms of Schröder paths.

We write for the set of all Schröder paths

from node to node in .

Theorem 3.1.

The entries of an matrix

satisfy

We shall present a weight-preserving bijection

between tilings and Schröder paths.

Note that we can superimpose the graph on the graph

so that the labels (connected minors) match up.

When we do this, the vertex (respectively, ) of gets

identified with the top right corner

of the square (respectively, the top left corner of the square

) in . We draw a Schröder path

on top of a tiling , as in Figure 5.

We may then think of the path as

an element of .

Figure 5. How to construct a Schröder path from a tiling.Figure 6. The six Schröder paths in together with their weights.

More formally, given ,

the path is defined as follows.

Its starting point is the top right corner of square in .

We inductively add steps to depending on the local behavior

of the tiling, as shown in Figure 5.

Let denote the endpoint of the path that we have built so far.

Then we proceed as follows:

•

If there is a vertical tile to the east of ,

then we add a northeast step to our path.

•

If there is a vertical tile to the southeast of , such that is

at its northwest corner, then we add a southeast step to our path.

•

If there is a horizontal tile to the southeast of , then

add an east step to our path.

•

If is already at the top left corner of square , then we stop.

The map maps the six tilings in Figure

3

to the six Schröder paths in Figure

6.

Lemma 3.2.

The map is well-defined and is

a bijection.

Proof.

This is the solution to Exercise 6.49 in

[7], based on an idea of Dana Randall.

∎

Proposition 3.4 states that this bijection is weight-preserving.

First, another lemma:

Lemma 3.3.

The local move shown in the top of Figure 7

alters the weight of both the tiling and the corresponding Schröder path

by the same factor: when passing from the left to the right,

the exponents of and increase by ,

while those of

and decrease by .

Figure 7. A flip of a tiling and the corresponding local move on Schröder paths.

Proof.

The statement is clear by inspection for the tilings. Checking the assertion for Schröder paths

is more complicated. We need to examine the various cases of what the

path looks like on the left and right of the square being modified.

In other words, we need to specify whether the path increases, stays flat or

decreases as it enters node , and ditto for when it leaves node .

One such case is seen in Figure 8.

When we perform that local move,

the exponents of and in (4) increase by ,

while the exponents of both and decrease by .

All other cases are similar.

∎

Figure 8. This local move multiplies the weight of the Schröder path by

.

Proposition 3.4.

If is a tiling in ,

where , then

.

Proof.

It is well known [6] that two domino tilings of a simply connected region

can always be connected by a sequence of flips,

where a flip is the local move that

switches two horizontal tiles for two vertical tiles or vice-versa, as

seen in Figure 7.

Let be the tiling consisting only of horizontal tiles.

The corresponding Schröder path

is a horizontal path. Here,

the two objects have the same weight:

(5)

By Lemma 3.3, if and is obtained by a flip,

then .

Since the tilings in are connected by flips, the assertion follows.

∎

This follows from Theorem 2.1, Lemma 3.2 and

Proposition 3.4.

∎

4. Back to symmetric matrices

The strategy for proving Theorem 1.1 is to

combine Theorem 3.1 with a projection

from Schröder paths to Catalan paths.

Let be any Schröder path in . The associated Catalan path

in is defined by

•

replacing each horizontal step in with a strict local minimum, i.e. a

southeast step followed by a

northeast step;

•

adding a northeast step at the beginning of

and a southeast step at the end of .

If starts at and ends at in then

starts at and ends at in .

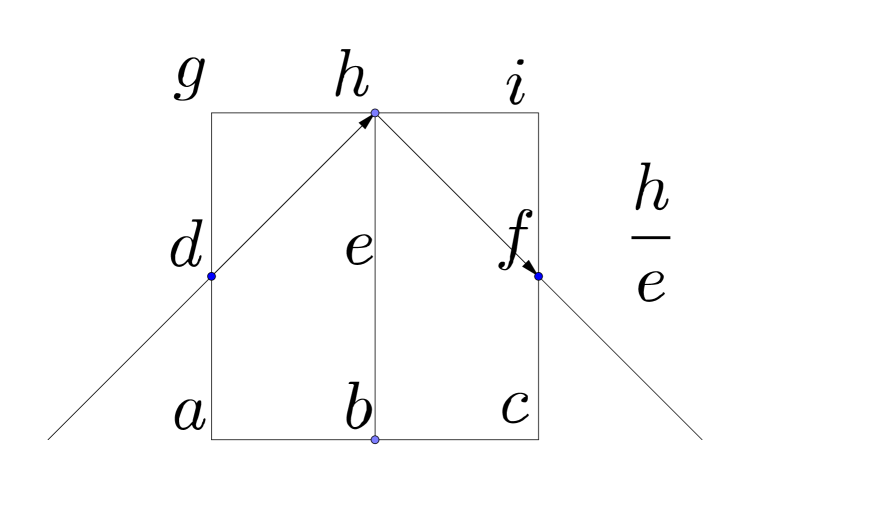

Figure 9 shows how four of the six Schröder paths in

map to four of the five Catalan paths in

. The two other Schröder paths

in Figure 6

map to the Catalan path in Figure 1.

Figure 9. The Schröder paths (left) are projected to the Catalan paths (right).

Theorem 2.1 is an immediate consequence of

Theorem 3.1 and the following proposition.

Proposition 4.1.

The weight of a Catalan path is the sum of the weights of the Schröder

paths in its preimage under the projection , i.e.

(6)

Here the labels of the paths come from a symmetric matrix, i.e.

for all and .

The proof will rely on equation (7) and Lemma 4.2.

Using Muir’s law of extensible minors, we obtain the following identity

that expresses connected almost-principal minors

of a symmetric matrix

in terms of connected principal minors:

(7)

We now use this identity to prove the following claim.

Lemma 4.2.

Let and be two Schröder paths in that

are related as shown in the

bottom row of Figure 7 (with on

the left and on the right). If the

labels come from a symmetric matrix, then

the resulting weights of these paths satisfy

(8)

Proof.

The label of the local minimum in is an almost-principal minor,

while are principal minors.

By (7), it satisfies , and hence

. By Lemma 3.3, we have

This implies .

∎

Example 4.3.

Let and be the fourth and fifth Schröder paths

in Figure 6, with labels

given by

a symmetric matrix. Using the identity

, as in (7), we find

This explains how the

six terms in (3) become the five terms of shown in (2).

Namely, the weight of the Catalan path in Figure 1 is

the sum of the fourth and fifth terms in (3).

Let be a Catalan path with

local minima. It has

local maxima.

Let and denote the variables

at the local minima and maxima, respectively.

Let and denote the face variables

located directly above the minima and directly below the maxima, respectively.

Then

(9)

We also denote the face variables located directly below the local minima

by .

There are Schröder paths that project to via . These

correspond to the choices of either preserving a local minimum,

or replacing it by a horizontal edge.

We denote the Schröder paths in by

, where

if the local minimum at was preserved and

if it was replaced by a horizontal edge.

By Lemma 4.2, we have

Therefore

the sum of the weights of the Schröder paths in is equal to

.

∎

Remark 4.4.

The expression in Theorem 1.1 is not the only way to

express the entries of a symmetric matrix in terms of the

connected almost-principal and principal minors.

The ideal of polynomial relations among these minors is generated by

the quadrics in (7).

Indeed, Theorem 1.1 ensures that the algebra generated

by these minors has dimension , so their relation ideal

has codimension .

The relations (7) lie in that ideal and they generate a

complete intersection. That complete intersection is a prime ideal because

none of the lie in the subalgebra generated by

the principal minors.

For instance, for , our prime ideal is principal. It is

.

5. Parametrizing Correlation Matrices

We now specialize to real symmetric matrices

that are positive definite and have all diagonal entries equal to .

Such matrices are known as correlation matrices.

They play an important role in statistics, notably in the study of

multivariate normal distributions.

The set of all correlation matrices

is an open convex set of dimension .

Its closure is a convex body, known in optimization theory [1, 4]

under the name elliptope.

In certain statistical applications it is desirable to

generate random correlation matrices. Specifically,

one wishes to sample from the uniform distribution on the

elliptope . A solution to this problem was given

by Joe [2] and further refined

by Lewandowski et al. [5].

The underlying geometric idea is to construct a parametrization from the standard cube:

The papers [2, 5] describe such

maps that are algebraic and bijective, so they identify the open cube

with the open elliptope. However, the construction is recursive.

In what follows we revisit the formula in [2]

and we make it completely explicit. Remarkably, it is precisely the

restriction of our Laurent polynomial parametrization

in Theorem 1.1 to the region where

all connected principal minors are positive and .

Let be a real symmetric matrix.

We assume that is positive definite, i.e. all

principal minors are strictly positive. In statistics,

such an serves as the covariance matrix

of a normal distribution on , whose

partial correlations are given by

(10)

For , we obtain the entries

of the correlation matrix , namely

The partial correlation in (10) is called connected if

.

Theorem 5.1.

The entries of a correlation matrix

can be written uniquely in terms of the connected

partial correlations .

Explicit formulas are derived from those in Theorem 1.1

by first replacing each occurrence of a parameter by

and thereafter replacing each occurrence of a

parameter by the

product of the expressions

where

and .

The resulting map

is a bjection between and .

Proof.

The replacement formula for is

seen in (10). The formula for the signed

principal minors

in terms of connected partial correlations

is due to Joe [2, Theorem 1].

It can be derived by recursively applying the following version of

(7) in concert with (10):

(11)

Our formulas give an algebraic map

between affine spaces of dimension .

This map is invertible on because each partial correlation

can be written via (10)

in terms of the entries of the correlation matrix.

All partial correlations are real numbers strictly between and .

The connected partial correlations

can vary freely, as explained in [2, page 2179].

From this, we get the desired bijection.

∎

We now illustrate our parametrization of correlation matrices

in the two smallest cases.

Example 5.2().

We consider the open -dimensional cube defined by the inequalities

Our bijection identifies each point in this cube with a

correlation matrix:

One checks that this matrix is positive definite, and,

as in [2, Theorem 1],

its determinant

defines the facets of the cube.

It is instructive to draw how the boundary of the cube maps onto

the boundary of the elliptope .

The latter is depicted in [1, Figure 5.8, page 232].

The combinatorics of our planar graph and its Catalan paths

can be seen in a different guise in [2, 5].

These correspond to the structures called D-vines in these papers.

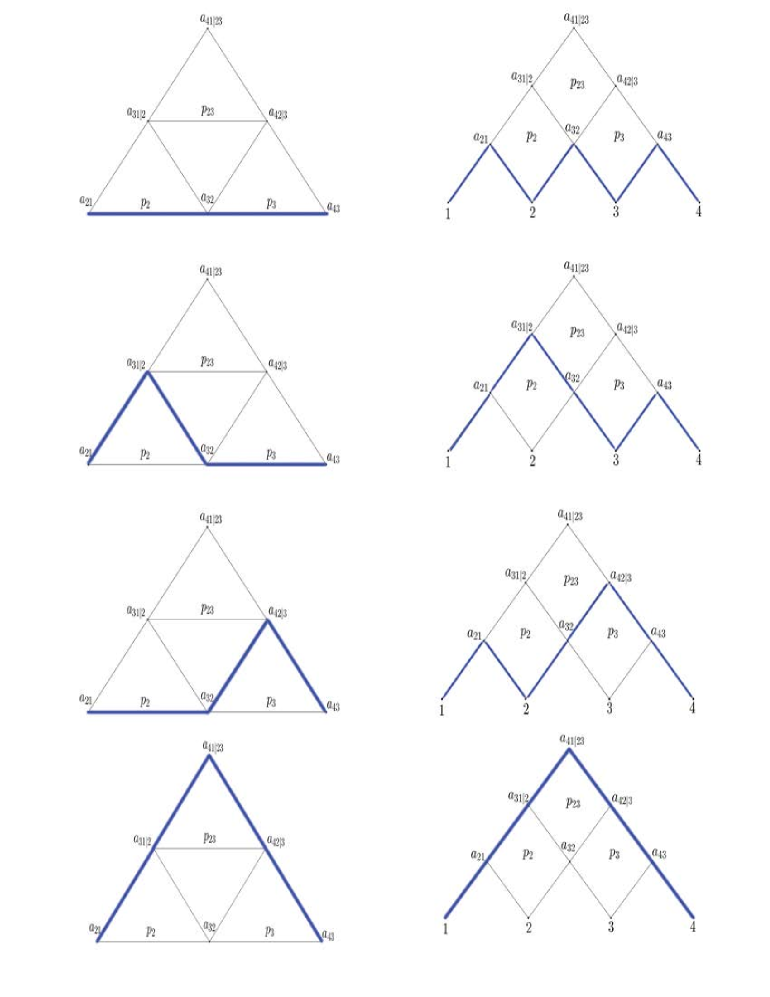

Figure 10 shows the standard D-vine for . Its edges

are naturally labeled with the six coordinates of the cube, namely

.

These correspond to the six almost-principal minors

in the labeled

graph in Figure 1.

Figure 10.

The standard D-vine for four random variables.

Example 5.3().

The correlation matrix is obtained from the matrix

in (2) by

performing the replacements that are described in Theorem 5.1.

We first substitute

and then we eliminate the connected principal minors as follows:

This results in the formulas for the six entries of in terms of

.

These give the bijection between the cube and

the elliptope, both of dimension six.

It is instructive to verify that is the product of

the facet-defining expressions .

The paper [5] argues that C-vines are better than

D-vines when it comes to sampling from the elliptope .

It would be interesting to examine both C-vines and D-vines

from the network perspective of [3] and to explore

whether Catalan-type formulas for can be derived from these as well.

Could such vines play a role in the theory of cluster algebras?

Acknowledgements.

We thank Richard Kenyon, Robin Pemantle and Caroline Uhler

for helpful conversations. This project was supported

by the National Science Foundation

(DMS-1419018, DGE-1106400, DMS-1049513).

References

[1]

Grigoriy Blekherman, Pablo Parrilo and Rekha Thomas:

Semidefinite Optimization and Convex Algebraic Geometry,

MOS-SIAM Ser. Optim., 13, SIAM, Philadelphia, PA, 2013.

[2]

Harry Joe:

Generating random correlation matrices based on partial correlations,

J. Multivariate Anal., 97(10):2177–2189, 2006.

[3]

Richard Kenyon and Robin Pemantle:

Principal minors and rhombus tilings,

J. Phys. A: Math. Theor., 47:474010, 2014.

[4] Monique Laurent and Svatopluk Poljak:

On the facial structure of the set of correlation matrices,

SIAM J. Matrix Anal. Appl. 17: 530–547, 1996.

[5]

Daniel Lewandowski, Dorota Kurowicka, and Harry Joe:

Generating random correlation matrices based on vines and extended

onion method,

J. Multivariate Anal., 100(9):1989–2001, 2009.

[6]

Nicolau Saldanha and Carlos Tomei:

An overview of domino and lozenge tilings,

Resenhas IME-USP, 2(2):239–252, 1995.

[7]

Richard P. Stanley:

Enumerative Combinatorics, Vol. 2, volume 62 of Cambridge Studies in Advanced Mathematics,

Cambridge University Press, 1999.

Authors’ address:

Department of Mathematics, University of California,

Berkeley, CA 94720-3840, USA