Power law in random multiplicative processes

with spatio-temporal correlated multipliers

Satoru Morita

morita.satoru@shizuoka.ac.jpDepartment of Mathematical and Systems Engineering, Shizuoka University, Hamamatsu, 432-8561, Japan

Abstract

It is well known that random multiplicative processes

generate power-law probability distributions.

We study how the

spatio-temporal correlation of the multipliers

influences the power-law exponent.

We investigate two sources of the time correlation: the local environment and the global environment.

In addition, we introduce two simple models through which we analytically and numerically show that the local and global environments yield different trends in the power-law exponent.

over large scales. This expression is widely known as Pareto’s law pareto or

Zipf’s law zipf ,

and it has been well investigated using various models.

One well-known mechanism that generates power-law distribution is the random multiplicative process (RMP) render ; sornette ; biham ; sornette98 ; nakao ; sato .

This paper aims

to clarify the influence of the

spatio-temporal correlation of the multipliers on the power-law exponent .

is known to decrease as the correlation time length increases sato .

However, there is no general formulation of RMPs with

spatio-temporal correlation.

To fulfill our aim, we consider two simple models,

Model 1 and Model 2, in which the temporal correlation is led by the local environment and the global environment, respectively.

We show analytically and numerically that

the correlation time length influences

the power-law exponent in Model 1, whereas

it does not in Model 2.

This paper is organized as follows.

First, we introduce

a binomial multiplicative process,

in which the random multipliers can have only two values,

and revisit the case where the multipliers have no correlation.

Here, we propose a graphical method to estimate the exponent

.

Next, we separately analyze the cases of temporal and spatial correlation.

We then analyze

the effect of spatio-temporal correlation in Models 1 and 2.

The results of the numerical simulations are compared with theoretical predictions.

The paper concludes with a summary.

Here, we consider a simple version of RMP,

(2)

where denotes a discrete time step and

specifies the elements ().

The variable can represent any quantity such as population,

firm size, or income,

is a random multiplier, and

is an additive positive term. Although may be a stochastic variable,

we set as a constant because it does not influence

the following results.

The initial condition is set to so that

is always positive.

For simplicity, we assume that the stochastic multiplier

is or , each with probability .

Here, we set

and , so that

eq. (2) has a stationary distribution.

The cases of and are called good and bad

environments, respectively.

The mean of the multipliers is , and

their variance is given by .

First, we consider

the case of no correlation between the multipliers

:

The stationary distribution has a power-law tail,

where the exponent is

a positive root of

(3)

The power-law tail

exists because undergoes a random walk with a drift

toward smaller values and is repelled from

sornette ; biham .

Consequently,

follows an exponential distribution,

implying a power-law distribution in .

Condition (3) was proved

by Kesten kesten using renewal theory.

Intuitively, Eq. (3) can be derived as follows sato .

In the large-scale range (),

we raise both sides of eq. (2) to the power

and average them. Thus, we have

If eq. (1) holds,

will converge

when .

Consequently, the exponent is given by the critical value of ,

i.e., by eq. (3).

In many systems, is approximately one newman05 ; clauset .

In our model, is when .

Thus, if the values of and lie along the solid curve in Fig. 1,

then . Note that the condition is a

function of and .

Therefore, from the plot in Fig. 1, we can graphically estimate the exponent for general values of and .

When the parameters and are located beneath the solid curve,

is larger than 1.

In the parameter region between this curve and the diagonal dotted lines, .

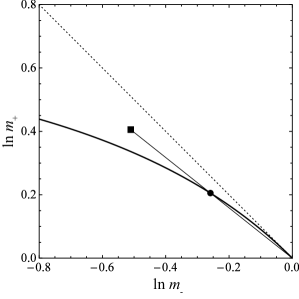

Figure 1:

Graphical method for estimating the exponent .

The vertical axis is and

the horizontal axis is .

The solid curve represents ,

i.e., .

For general values of and ,

satisfies ; thus,

can be estimated using this curve.

For example, consider the case of and

(indicated by the closed square).

Draw a straight line between the square and the origin .

The closed circle represents the intersection of the curve and the straight line.

The exponent is determined by

the ratio of the distance between the circle and the origin

to the distance between the square and the origin.

In this case, we obtain .

Above the diagonal dotted line (),

there is no stationary distribution.

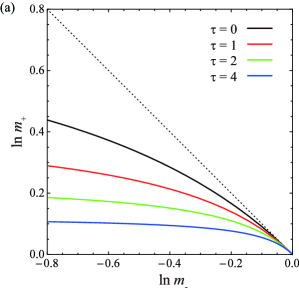

Figure 2:

A set of and for which for several cases. From these curves, we can estimate the exponent

for general values of and , as in Fig. 1.

(a)

The case in which has only temporal correlation (4).

The correlation time length is set as .

The curves are given by

.

(b)

The case in which has only spatial correlation (7).

The correlation coefficient is set as .

The curves represent

.

Second, we consider the case of temporally correlated :

(4)

where is the correlation time length.

To obtain a stochastic time series satisfying

(4), we use a Markov

chain with the transition probability matrix

(5)

where .

For example, the first-row, second-column element of the matrix

represents the probability that the multiplier changes from

to .

Let and be defined as

the total in the good and bad local environments,

respectively:

Then,

Since the exponent is the critical value of ,

it is determined by solving the following equation such that

the dominant eigenvalue of

equals one.

Using a simple calculation, we show that

the exponent is given by a solution of

(6)

Figure 2(a) plots the curves of (6) for

for various values of .

For general values of and ,

the exponent can be estimated from these curves,

as demonstrated in Fig. 1.

This result indicates that the exponent

decreases as the correlation time length increases,

which is consistent with the previous work by Sato et al. sato .

Third, we consider the case of spatially correlated :

(7)

where and is the correlation coefficient.

We now introduce the global environment, which can independently be

good or bad with probability at each time.

In a good global environment at time ,

the multiplier is with

probability

or with probability .

Conversely, in a bad global environment, is with

probability or with probability .

By simple algebra, we obtain

When ,

the mean of is given by

the geometrical mean of the average growth rates

in both global environments:

Thus, the exponent is obtained by solving

(8)

Figure 2(b) plots the curves (8) for for various spatial correlations .

The exponent is graphically estimated as before.

We find that increases with increasing spatial correlation.

To analyze the spatio-temporal correlation of , we expand the previous model and introduce two new models,

Model 1 and Model 2, in which the time correlation is sourced from the local and global environments, respectively.

In Model 1, the local environment in a good global environment is governed by the transition probability matrix

where .

In a bad global environment, the transition probability matrix is

The global environment is independently good or bad with

probability ; therefore, the transition probability matrix of the multiplier

for each should be the average of and (), which is given in eq. (5).

Thus, the autocorrelation of is .

Moreover, a simple calculation gives

(9)

where the correlation coefficient is given by

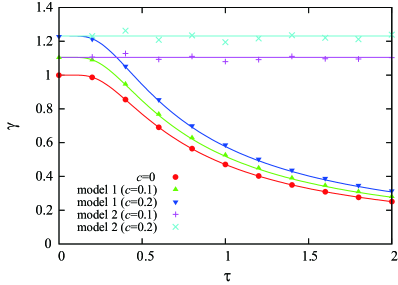

Figure 3: Exponent of the power-law tail

as a function of the correlation time .

Here, we estimate for and 200 samples.

The other parameters are set to , .

The symbols and curves represent the numerical estimations and theoretical predictions, respectively.

In this case, the dynamics of are determined as

or

with probability .

If is given as

then follows a one-dimensional Markov chain:

or

with probability .

Thus, the statistical state of

is characterized by its stationary density distribution

,

which can be numerically calculated lasota ; morita02 ; morita12 .

In addition, when , we have

Consequently,

as the exponent is the critical value of ,

it is obtained by solving

Setting and using

the graphical method,

we can obtain for general values of and .

Representative results are plotted in Fig. 3. Clearly, increases as

increases or as decreases.

Model 2 assumes that the global environment

is auto-correlated as .

To obtain such a time series, we again apply the Markov chain with (5).

At the same time step, the correlation between

the multiplier

and the global environment is .

Thus, we obtain

(10)

where

In this model, eq. (10) also holds for .

This condition marks an important difference between Models 1 and 2.

Because we have

the exponent is again given by eq. (8).

Thus, in Model 2, the exponent is independent of the

correlation time .

To confirm the above predictions, numerical simulations are performed in (see Fig. 3).

To numerically estimate ,

we set ,

employ the method of clauset , and average over 200 samples.

Figure 3 shows that the theoretical predictions are highly consistent with the numerical simulation results.

In summary,

we investigated how the

spatio-temporal correlation of the multipliers

influences the power-law exponent.

On separately considering the temporal and spatial correlations,

we found that

increased when

increased or when decreased.

In socioeconomic dynamics, such trends imply that the gap between the rich and the poor widens as the temporal correlation becomes stronger or as the

spatial correlation becomes weaker.

However, in a simultaneous treatment of the spatio-temporal correlation, the temporal correlation did not necessarily reduce the exponent (in Model 2).

At first sight, eqs. (9) and (10) are similar and

there is barely any difference between the correlation structures of Models 1 and 2.

However, this slight difference significantly affects the power-law exponent.

Acknowledgements.

This work was supported by a Grant-in-Aid for Scientific Research (No. 26400388) and CREST, JST.

Some of the numerical calculations were performed on machines at YITP of Kyoto University.

References

(1)

M. E. J. Newman,

Contemp. Phys. 46, 323 (2005).

(2)

A. Clauset, C. R. Shalizi and M. E. J. Newman,

SIAM Rev. 51, 661 (2009).

(3)

X. Gabaix,

Annu. Rev. Econ. 1, 255 (2009).

(4)

X. Gabaix

Q. J. Econ. 114, 739 (1999).

(5)

Y. M. Ioannides and H. G. Overman,

Reg. Sci. Urban Econ. 33, 127 (2003).

(6)

J. J. Ramsden and Gy. Kiss-Haypál

Physica A 277, 220 (2000).

(7)

R. L. Axtell,

Science, 293, 18 (2001).

(8)

B. Mandelbrot,

J. Bus. 36, 394 (1963).

(9)

X. Gabaix, P. Gopikrishnan, V. Plerou and H. E. Stanley,

Nature 423, 267 (2003).

(10)

D. G. Champernowne,

Econ. J. 63, 318 (1953).

(11)

W. J. Reed,

Physica A 319, 469 (2003).

(12)

V. Pareto,

Cours d’économie politique.

F. Rouge, Lausanne (1896).

(13)

G. K. Zipf, Human Behavior and the Principle of Least Effort.

Addison-Wesley (1949).

(14)

S. Render,

Am. J. Phys. 58, 267 (1990).

(15)

D. Sornette and R. Cont,

J. Phys. I 7, 431 (1997).

(16)

O. Biham, O. Malcai, M. Levy, and S. Solomon,

Phys. Rev. E 58, 1352 (1998).

(17)

D. Sornette,

Phys. Rev. E 57, 4811 (1998).

(18)

H. Nakao,

Phys. Rev. E 58, 1591 (1998).

(19)

A. -H. Sato, H. Takayasu, and Y. Sawada

Phys. Rev. E 61, 1081 (2000).

(20)

H. Kesten,

Acta. Math. 131, 207 (1973).

(21)

S. Morita and Jin Yoshimura,

Phys. Rev. E 88, 052809 (2013).

(22)

A. Lasota and M. C. Mackey,

Probabilistic Properties of Deterministic Systems.

(Cambridge University, New York, 1985).

(23)

S. Morita and T. Chawanya,

Phys. Rev. E 65, 046201 (2002).

(24)

S. Morita and J. Yoshimura,

Phys. Rev. E 86, 045102R (2012).