New Computational Guarantees for Solving Convex Optimization Problems with First Order Methods, via a Function Growth Condition Measure

Abstract

Motivated by recent work of Renegar [21], we present new computational methods and associated computational guarantees for solving convex optimization problems using first-order methods. Our problem of interest is the general convex optimization problem , where we presume knowledge of a strict lower bound . [Indeed, is naturally known when optimizing many loss functions in statistics and machine learning (least-squares, logistic loss, exponential loss, total variation loss, etc.) as well as in Renegar’s transformed version of the standard conic optimization problem [21]; in all these cases one has .] We introduce a new functional measure called the growth constant for , that measures how quickly the level sets of grow relative to the function value, and that plays a fundamental role in the complexity analysis. When is non-smooth, we present new computational guarantees for the Subgradient Descent Method and for smoothing methods, that can improve existing computational guarantees in several ways, most notably when the initial iterate is far from the optimal solution set. When is smooth, we present a scheme for periodically restarting the Accelerated Gradient Method that can also improve existing computational guarantees when is far from the optimal solution set, and in the presence of added structure we present a scheme using parametrically increased smoothing that further improves the associated computational guarantees.

1 Problem Statement and Overview of Results

1.1 Problem Statement, Strict Lower Bound, and Function Growth Constant

Motivated by recent work of Renegar [21], we present new computational methods and associated computational guarantees for solving convex optimization problems using first-order methods. Our problem of interest is the following optimization problem:

| (1) |

where is a closed convex set and is a convex function. Let the set of optimal solutions of (1) be denoted as . For , let denote the distance from to the set of optimal solutions, namely .

Strict Lower Bound and Function Growth Constant . Let be a known and given strict lower bound on the optimal value of (1), namely . Such a known strict lower bound arises naturally when optimizing many loss functions in statistics and machine learning (least-squares loss, logistic loss, exponential loss, total variation loss, etc.) perhaps with the addition of a regularization term; in all these cases . A known strict lower bound also arises in Renegar’s transformed version of the standard conic optimization problem [21].

Let be given. Given the knowledge of the strict lower bound , it is natural to work with the notion of a relative measure of optimality. Let us define an -relative solution of (1) to be a point that satisfies:

| (2) |

Note that (2) is a relative error measure, relative to the optimal bound gap . We focus on an -relative solution rather than on an -absolute solution (), as the former seems more natural in the setting where a strict lower bound is part of the problem description. Indeed, consider the context of loss functions in statistics and machine learning where , in which case an -relative solution corresponds to , and hence is a multiplicative measure of optimality tolerance.

Let denote the smallest scalar satisfying:

| (3) |

By its definition one sees that measures how fast the distances from the optimal solution set grow relative to the bound gap . Therefore is a measure of the growth rate of the level sets of . We call the “growth constant” of the function for the given strict lower bound . Note that an equivalent definition of is given by:

| (4) |

Unlike the strict lower bound , we do not assume that is known, nor do we need any upper bounds on . Indeed, neither knowledge of nor the finiteness of are needed in order to implement the computational methods presented herein; however the finiteness of is needed for the analysis of the methods to be meaningful.

We will see in Sections 3 and 4 that the knowledge of the fixed strict lower bound and the concept of the function growth constant lead to different versions of first-order methods with different computational guarantees than the traditional analysis of first-order methods would dictate. Furthermore, these different computational guarantees can dominate the traditional guarantees in many cases but most notably when the initial iterate is far from the optimal solution. Roughly speaking, for several of the algorithms developed herein our computational guarantees grow like in contrast to traditional guarantees where the growth is proportional to and (in the smooth and nonsmooth settings, respectively).

In a departure from typical optimization approaches to lower bounds such as those arising from duality theory wherein one desires as tight a lower bound as possible, herein the lower bound is strict, namely , and it is fixed, i.e., it is not updated as part of a computational procedure. It is best to think of this lower bound as a structural lower bound that is easily connected to known properties of the function . Such a strict lower bound on arises naturally in the settings of statistics and machine learning in the case of loss functions and/or regularization functions, see for example [10]. Consider when is the logistic loss function or the exponential loss function , perhaps with the addition of a regularization term for some , , and . If the sample data is not strictly separable, which translated herein means that there is no satisfying unless , then it follows that and so is a strict lower bound and is quite natural in this setting. Another example is regularized least-squares regression such as the LASSO and its cousins, wherein ; it follows that and one can assert that under a variety of mild assumptions involving either or the data matrix . Other classes of examples for which is a strict lower bound on include total variation (TV) loss functions which are used in image de-noising, as well as the broad class of minimum norm problems in general, under mild assumptions. Another class of problems for which there is a natural strict lower bound on is the class of projectively transformed conic convex optimization problems under a particularly clever projective transformation, as developed by Renegar [21]; indeed it was this problem class and the results in [21] that gave rise to the line of research described herein.

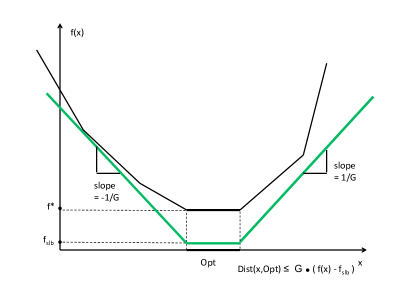

We can interpret as connected to a lower estimator of : rearranging (3), we obtain:

| (5) |

Therefore the convex function is a lower estimator of the function on . This interpretation is illustrated in Figure 1. As Figure 1 illustrates, the concept of the growth constant is somewhat related to the notion of the modulus of weak sharp minima for (1), see Polyak [17] and Burke and Ferris [3]; this relationship is discussed further in Appendix A.1.

A natural question to ask is under what circumstances is the growth constant finite? Roughly speaking, it holds that is finite except when the objective function level sets are ill-behaved relative to their recession cone. This is made precise in the following theorem, whose proof is given in Appendix A.2. For , let denote the -optimal level set of on , and let denote the recession cone of , namely . Note that is the (common) recession cone of for all .

Theorem 1.1.

Suppose that for some there exists a bounded set for which where is the recession cone of . Then for any given strict lower bound , the growth constant is finite. ∎

Let us briefly examine special cases of Theorem 1.1. Consider the case when where is a bounded convex set and is a subspace. Then for any it is easy to show that for some bounded set , in which case Theorem 1.1 implies that is finite. In particular, when itself is a bounded set, then we can set , and so Theorem 1.1 implies that is finite.

For an example wherein , consider the function on . It is straightforward to check that the Hessian matrix is positive semidefinite on and hence is convex on . We have and . However, the growth constant for any strict lower bound , since by letting for any we obtain using (4) that

1.2 Overview of Results

We use the knowledge of the fixed strict lower bound and the concept of the function growth constant to design and develop computational guarantees for new versions of first-order methods for solving the optimization problem (1). In Section 3 we present such methods when is non-smooth and Lipschitz continuous with Lipschitz constant . In Theorem 3.1 we present an iteration complexity of for a version of Subgradient Descent that simultaneously runs with two step-sizes and occasional re-starting, which strictly improves the standard computational complexity bound for Subgradient Descent when is a “cold start,” i.e., is large. In the special case when the optimal objective function value is known, Theorem 3.2 shows that the standard step-size rule for Subgradient Descent yields the same result. And when can be smoothed, we present further improved computational guarantees for a new method (Algorithm 4) that successively smooths and restarts the Accelerated Gradient Method, see Theorem 3.3 herein.

In Section 4 we present computational guarantees for new first-order methods when is smooth and has Lipschitz gradient with Lipschitz constant . We present a new first-order method (Algorithm 5) based on periodically restarting the Accelerated Gradient Method, that leads to an iteration complexity of (Theorem 4.1), which in many cases can improve the standard computational complexity bound for the Accelerated Gradient Method, most notably when is far from the optimal value and is small. And when has appropriate adjoint structure, we use parametric increased smoothing and restarting of the Accelerated Gradient Method to achieve a further improvement in the above computational guarantee (Theorem 4.2).

Algorithm A in Renegar [19] provides an interesting approach to the general convex optimization setting, that bears comparison to the approach and results contained herein – which are also designed for the general convex optimization setting. Both Algorithm A in [19] and the algorithms herein generalize the methodology for conic optimization developed in Renegar [20, 21] to the general convex optimization problems, but they do so in different ways. Herein the generalization is obtained by introducing the new function measure based on the strict lower bound , while in Algorithm A in [19] the original problem is transformed (implicitly or explicitly) to a conic optimization problem in a slightly lifted space. The resulting algorithms appear to be very different, and have different computational requirements and convergence bounds – Algorithm A in [19] requires a -dimensional root finding procedure each iteration, whereas Algorithm 3 herein requires orthogonal projection onto the feasible region. (And indeed it is rather remarkable that Algorithm A of [19] does not require such projection.) Algorithm A does not need a Lipschitz constant; however in the case of a smooth objective function Algorithm A cannot take advantage of such smoothness, unlike Algorithm 5 (and also Algorithm 4) herein.

The paper is organized as follows. Section 2 contains a brief review of the Subgradient Descent and an Accelerated Gradient Method. Section 3 contains first-order methods and computational guarantees when is non-smooth. Section 4 contains first-order methods and computational guarantees when is smooth.

Notation. Unless otherwise specified, the norm is the Euclidean (inner product) norm . We occasionally refer to the norm of a vector , which is denoted by . For , let denote the Euclidean projection operator onto , namely . We define . The set of optimal solutions of (1) is denoted by .

2 Review of Subgradient Descent and an Accelerated Gradient Method

We briefly review the Subgradient Descent Method and an Accelerated Gradient Method (as analyzed in Tseng [26]) for solving the convex optimization problem (1).

2.1 Subgradient Descent

Recall that is a subgradient of at if the following subgradient inequality holds:

Let denote the set of subgradients of at . Here we assume that is Lipschitz continuous on a relatively open set containing , namely, there is a scalar for which

| (6) |

It follows from (6) that for all and it holds that .

Algorithm 1 presents the standard subgradient scheme. In this method is the iterate at iteration , the best objective value among the first iterates is , and the best iterate among the first iterates is .

The following theorem summarize well-known computational guarantees associated with the subgradient descent method.

Theorem 2.1.

(Convergence Bounds for Subgradient Descent [18, 13])

(i) Consider the subgradient descent method (Algorithm 1). Then for all , the following inequality holds:

(ii) Suppose that is known, and let the step-sizes for Algorithm 1 be . Then for all , the following inequality holds:

Suppose that we seek to bound the number of iterations of the Subgradient Descent method required to compute an (absolute) -optimal solution of (1), which is a point that satisfies . If is given, and the step-sizes are chosen as , then it follows from part of Theorem 2.1 that for all

| (7) |

If instead we know (or can bound from above) , and the step-sizes are chosen as where satisfies (7), then it also follows from part of Theorem 2.1 that . And if is known, then the bound (7) is also sufficient to guarantee if the steps-sizes are chosen as in part of Theorem 2.1. Furthermore, it follows from [12] that the bound (7) cannot in general be improved in the black-box oracle model of computation with complexity bounds depending only on , , and . In this regard, we note that the dependence on additional parameters, namely the strict lower bound and the function growth constant , which are used throughout this paper, shows how we can achieve different (and better in many cases) complexity bounds by including additional parameters and appropriately amending algorithms and their analysis.

2.2 Accelerated Gradient Method for Smooth Optimization

Here we assume that is differentiable with Lipschitz continuous gradient on , namely, there is a scalar for which

| (8) |

Algorithm 2 presents a standard Accelerated Gradient Method as in Tseng [26].

For define the level set . For , let denote the distance from to the level set , namely . The following theorem is a computational guarantee for the Accelerated Gradient Method due to Tseng [26].

Theorem 2.2.

3 Computational Guarantees when is Non-Smooth

Let be given. We aspire to compute an -relative solution of (1), which recall from (2) is a point satisfying: . In this section we present three new computational guarantees for first-order methods applied to computing a -relative solution of problem (1) that are based on the strict lower bound and growth constant . The first guarantee is for a new algorithm based on Subgradient Descent that runs two different step-sizes simultaneously with occasional re-starts. The second guarantee is for the standard Subgradient Method using a standard step-size rule in the case when the optimal value is known. The third guarantee is for the case when the function can be smoothed and then solved using an algorithm based on the Accelerated Gradient Method.

3.1 Subgradient Descent using Two Step-Size Rules Running Simultaneously

We consider solving (1) using a version of subgradient descent that simultaneously runs two versions of the Subgradient Descent Method – each with a different step-size rule – with occasional simultaneous re-starts of both versions. The formal description of our method is given in Algorithm 3. In the algorithm, the notation “” denotes assigning to the next value of the Subgradient Descent Method applied to the optimization problem (1) with objective function with current point using the step-size and the subgradient , along with updates of the best objective function value obtained thus far with the corresponding best iterate computed .

We now walk through the structure of Algorithm 3. The algorithm requires as input the starting point and the desired relative accuracy value used to define an -relative solution, see (2). The algorithm then defines an absolute constant . The two values and are then used as aspirational goals for simultaneously running the standard Subgradient Descent Method in search of either an -relative solution of (1) or an -relative solution of (1). For notational ease, both and are converted to a slightly different form by defining and . At the start of the outer iteration, Algorithm 3 runs the Subgradient Descent Method simultaneously using two different step-size rules (but starting at the same point ), and so generates inner iterations and for based on computed subgradients and and step-sizes and , respectively. The only structural difference between the two instantiations of Subgradient Descent is that the steps-sizes use in their definition whereas use in their definition. The number of inner iterations that are run in the outer iteration is initially set to be . If either or makes sufficient progress relative to the starting value as determined in the ratio test at the start of Step (2.), then the outer iteration is concluded and , which counts the number of inner iterations therein, is updated to . Finally, the next outer iteration starting values are re-set to either or , depending on which of or satisfies the ratio test.

Many of the ideas used in the construction of Algorithm 3 were motivated from similar notions developed in Algorithm 2 of [21] as well as the algorithm “MainAlgo” in [22] (which uses the construct of running two algorithms simultaneously with different parameters).

Regarding counting of iterates , that are computed of Algorithm 3, we will say that the algorithm has computed an iterate whenever it computes a subgradient and then calls . There are therefore two iterates computed at each inner iteration. We have:

Theorem 3.1.

Since , the computational guarantee in Theorem 3.1 can itself be bounded by:

| (9) |

which is qualitatively different from the guarantee of the standard Subgradient Descent Method (Algorithm 1) in (7) in two interesting ways. First, the dependence in (7) on is quadratic, whereas in (9) it is logarithmic. Second, although both guarantees are linear in the inverse square of the desired relative accuracy (from (2) an -relative solution corresponds to an absolute solution of (1)), however affects this factor multiplicatively through in (7), whereas the factor is independent of in (9).

Let us also quantitatively compare the computational guarantee of Theorem 3.1 with the standard guarantee for Subgradient Descent given by (7). The standard computational guarantee (7) can be written as:

Let us presume that is small, whereby . Then the ratio of the new guarantee (9) from Theorem 3.1 to the standard guarantee (7) is at most

| (10) |

Notice from (10) that for any instance of (1), when is sufficiently large the right-hand side of (10) can be made arbitrarily small, thereby showing that in these cases the computational guarantee in Theorem 3.1 can be made arbitrarily better than the standard guarantee (7) for Subgradient Descent.

We will prove Theorem 3.1 by first establishing eight propositions. The reader familiar with [21] will notice certain resemblances between aspects of the proof constructs below and the proof of Theorem 3.8 of [21], see also [19]. Throughout, for notational convenience, we will work with three constants , , and that must be chosen to satisfy the conditions:

and whose specific values in Algorithm 3 are set to , , and , where is the base of the natural logarithm.

Let play the role of either or , and also define (analogous to the definitions of and ).

The first two propositions below apply to the generic setting of the Subgradient Descent Method.

Proposition 3.1.

Let be given, and suppose we run the Subgradient Descent Method (Algorithm 1) with starting iterate , using step-sizes:

for all iterations . Then for all it holds that

Proof: Define . Then . It follows from part of Theorem 2.1 that

where the second inequality uses the definition of and the inequality , and the third inequality uses the definition of . Simplifying the last expression completes the proof. ∎

Proposition 3.2.

Proof: Suppose that . This rearranges to: , whereby

| (11) |

Invoking Proposition 3.1 we have:

where the second inequality follows since , and the last inequality uses (11). Rearranging the final inequality and dividing by then yields , which completes the proof. ∎

Proposition 3.3.

Proof: Let us apply Proposition 3.2 with , , and . If , then by definition of it holds that . Therefore from Proposition 3.2 it holds that . ∎

Proposition 3.4.

Proof: Let us similarly apply Proposition 3.2 with , , and . If , then by definition of it holds that . Therefore from Proposition 3.2 it holds that . Combining these inequalities we obtain:

and rearranging yields the result. ∎

In the next proposition we use the standard notation for the nonnegative part of a scalar .

Proposition 3.5.

Proof: If then the result holds trivially, so let us suppose that . It then follows using induction on that

and taking logarithms yields

from which the result follows. ∎

In the following proposition, as well as others later on, we use the standard notational convention that for .

Proposition 3.6.

Proof: If then the results holds trivially since

Next suppose that , and consider any outer iteration . Then since

it follows from Proposition 3.4 that . This also implies that exists and therefore must satisfy

Finally, since , it therefore follows that . ∎

Proposition 3.7.

Let denote the number of outer iterations for which is finite. Then

where is as defined in Proposition 3.5.

Proof: It follows from Proposition 3.6 that . Therefore , where we have used the properties of in Proposition 3.6. Taking logarithms yields

from which the result follows. ∎

Proposition 3.8.

Proof: Let denote the index of the first outer iteration for which . Notice that since it must hold that . It follows from Proposition 3.3 that and hence for some it holds that . Let us now count the number of iterates computed after and prior to and including . This number is bounded above by:

where the first inequality follows since for , and the last inequality uses . ∎

We now use these propositions to prove Theorem 3.1.

Proof of Theorem 3.1: Utilizing the definitions of , , , , and in Propositions 3.3, 3.4, 3.5, 3.7, and 3.8, it follows from Propositions 3.6 and 3.8 that the total number of iterates computed prior to and including is at most . Substituting the values of and and using the bounds on and in Propositions 3.5 and 3.7 yields:

where the second inequality follows from substituting in the values , , and , and rounding terms upward. This last expression then is rounded upward to yield the desired iteration bound. ∎

3.2 Subgradient Descent when is known

In the special case when is known, we can obtain a computational guarantee that is of the same order as that of Theorem 3.1 by directly using the standard Subgradient Descent Method (Algorithm 1) with the (standard) step-size rule . This is shown in the following theorem.

Theorem 3.2.

The computational guarantee above is an almost-exact generalization of Theorem 3.7 of Renegar [21], which therein pertains to a specific transformed conic optimization problem. The proof of this theorem follows the logic for the proof of Theorem 3.7 of [21] in many respects as well.

Notice that up to an absolute constant, the computational guarantee of Theorem 3.2 is essentially the same as that of Theorem 3.1 in the worst case.

Proof of Theorem 3.2: We will presume that , since otherwise (12) is satisfied trivially for all . Let be a given fractional quantity. Define , and for all such that define inductively as the smallest iteration index of Subgradient Descent for which . Notice that so long as it follows using part of Theorem 2.1 that exists (i.e., is finite). Let be the smallest sub-index for which . It follows from the initial presumption above that , and it holds for any satisfying that , from which it follows that , and hence also , is finite. Furthermore, it holds for any satisfying that:

| (13) |

Using in (13) and taking logarithms yields:

| (14) |

If exists (i.e., is finite), then it follows from part of Theorem 2.1 that:

This last inequality can be rearranged to yield:

| (15) |

where the second inequality uses the definition of the growth constant as well as the fact that . Now putting all of this together we obtain:

where the first inequality is from (15), the second inequality uses (13), the third inequality replaces the two finite geometric series with corresponding infinite series, and the fourth inequality uses (14). Finally, using the value of and substituting into the above yields the result.∎

We remark that one obtains the precise constants of Theorem 3.7 of [21] by using . Choosing to optimize the absolute constant of the term yields and the absolute constants as presented in the statement of the threorem. Choosing to optimize the absolute constant of the term would yield with the coefficient of in the terms.

3.3 Non-Smooth Optimization using a New Smooth Approximations Method

As first proposed by Nesterov [14], there are many practical settings wherein one can approximate the non-smooth convex function by a smooth convex function , where the sense of the approximation depends on the parameter . If the smooth approximation is computationally easy to work with, one can then use the Accelerated Gradient Method (Algorithm 2) to approximately optimize (thereby also approximately optimizing ) on the feasible set . There are a variety of techniques that can be used to construct a parametric family of smooth functions depending on the known structure of and , see [14] as well as [15] and Beck and Teboulle [1] among others. For our purposes herein, we will suppose that there is a smoothing technique with the following two properties:

(i) there is a known constant such that for any given we can construct a smooth convex function which is not far from , namely:

| (16) |

(ii) has Lipschitz continuous gradient on with Lipschitz constant satisfying

| (17) |

for some known positive constant .

These properties can be used to design an implementation of the Accelerated Gradient Method (Algorithm 2) applied to , that can be used to compute an absolute -optimal solution of the original optimization problem (1). Using the scheme developed in [14] in conjunction with the Accelerated Gradient Method (Algorithm 2) yields an iteration complexity bound of

| (18) |

to obtain an (absolute) -optimal solution of (1) for a suitably designed version of the basic method [14].

Herein we develop a variant of the basic smoothing method to solve the optimization problem (1) that yields a new computational guarantee that can improve on (18) in many cases. Algorithm 4 presents parametric smoothing and restarting method for computing an -relative solution of the optimization problem (1) for the non-smooth objective function based on successive smooth approximations and re-starting of the Accelerated Gradient Method (Algorithm 2). In the description of Algorithm 4 the general notation “” denotes assigning to the iterate of the Accelerated Gradient Method applied to the optimization problem (1) with objective function using the initial point .

At the outer iteration of Algorithm 4, the algorithm sets two different smoothing parameters in Step (1.), namely and , where differs from by the relative accuracy input value . The algorithm then runs the Accelerated Gradient Method with starting point simultaneously on the two smoothed functions and , using the double indexing notation of and to denote iteration of the Accelerated Gradient Method initialized at the point for optimizing and on , respectively. Notice that the smoothing parameters and decrease over the course of the outer iterations, as it makes more sense to set these values higher at first and then decrease them as the solution is approached. The outer iteration runs until the ratio test in Step (3a.) fails, at which point the current point becomes the starting point of the next outer iteration, namely . The counter records the number of inner iterations of outer iteration . Regarding counting of iterates computed in Algorithm 4, we will say that the algorithm has computed an iterate whenever it calls . There are therefore two computed iterates at each inner iteration.

Restarting for accelerated gradient methods for strongly convex functions has been studied in [16] and [25]. To the best of our knowledge, restarting of accelerated methods in the absence of strong convexity was first used in Renegar [20], and Algorithm 4 exploits this and other ideas from [20] and [22] as well. We have the following computational guarantee associated with Algorithm 4.

Theorem 3.3.

Similar to Theorem 3.1, the dependence in Theorem 3.3 on the quality of the initial iterate is logarithmic in the initial optimality gap . Also, the factor involving in Theorem 3.3 is independent of the quality of the initial iterate, unlike that of the standard bound for the smoothing method given in (18). We will prove Theorem 3.3 by first establishing several propositions. Throughout, for notational convenience, we will work with two constants and that must be chosen to satisfy

and whose specific values are set to and in Algorithm 4.

The following proposition applies to the generic setting of the Accelerated Gradient Method applied to the smoothed function . Recall that denotes the Lipschitz constant of the gradient of on .

Proposition 3.9.

Given the smoothing parameter and a given constant , define . Let denote the iterate of the Accelerated Gradient Method applied to the function with starting point . For it holds that:

| (19) |

Proof: Note that for any it holds that , whereby . It then follows from Theorem 2.2 applied to the function and using that for any we have:

where the second inequality uses the fact that , the third inequality uses the definition of , and the last inequality uses the value of .

Note from (16) that , whereby:

We now apply Proposition 3.9 to the setting of the Parametric Smoothing/Restarting Method (Algorithm 4).

Proposition 3.10.

Let be the index of an outer iteration of Algorithm 4. Define . If and exists, then it holds that:

Proof: The proof follows by applying Proposition 3.9 with , , , and . It then follows that

where the second inequality uses from (17) and from substituting in the values of and . ∎

Proposition 3.11.

Let be the index of an outer iteration of Algorithm 4. Define . If and exists, then it holds that:

Proof: The proof follows by applying Proposition 3.9 with , , , and . It then follows that

where the second inequality uses from (17) and the final equality derives from substituting in the values of and . ∎

The next three propositions pertain to Algorithm 4 as well as to a more general setting which will be used in Section 4 to prove computational guarantees for algorithms when is smooth. The more general setting is described in the body of the following proposition.

Proposition 3.12.

Let be constants satisfying , . Consider an algorithm with outer and inner iterations indexed with counters and , respectively (such as Algorithm 4), with initial iterate that is used to set in simultaneous running of the Accelerated Gradient Method using the same indexing notation as in Algorithm 4, and where where denotes the first index for which . Suppose that there are sequences and indexed over the outer iteration counter such that the following conditions are satisfied:

(i) for all it holds that , and

(ii) for all it holds that .

Let denote the number of outer iterations for which is finite. Then

Furthermore, if and , then .

Proof: If the results follow trivially, so let us suppose that , whereby is finite and exists. It then follows that , and taking logarithms yields the proof of the bound on .

Suppose additionally that and . Let us assume that , from which we will derive a contradiction. We have

where the first inequality uses condition and the second inequality uses . Also, , whereby exists and therefore satisfies . Combining this inequality with that above yields , which rearranges to yield:

and which contradicts the definition of . Therefore . ∎

Proposition 3.13.

Under the same setting, notation, and conditions and of Proposition 3.12, let be the index of an outer iteration. If and exists, then:

Furthermore, if also , then

Proof: Since it follows from condition that

and also since exists then , whereby:

It then follows from these two inequalities that

If also , then we have from condition that

where the first inequality is from condition , the second inequality uses (3.3), and the third inequality uses . ∎

Proposition 3.14.

Proof: First consider the case when . Then and therefore with we have exists for , whereby from Proposition 3.13 it holds that satisfies (2). In this case and therefore of (20) is satisfied.

Next consider the case where and . Let be the index of an outer iterate. If it follows from Proposition 3.12 that . For it holds for this case that , and it follows from Proposition 3.13 that exists for and therefore satisfies (2). In this case and whereby of (20) is satisfied.

Next consider the case where and and also . Let be the index of an outer iterate. If it follows from Proposition 3.12 that . Since it follows that exists for , whereby from Proposition 3.13 we have satisfies (2). And since in this case, it follows that , and therefore of (20) is satisfied.

The last case is where and and also . Then just as in the third case above, we arrive at , and thus of (20) is satisfied, thereby proving (20). ∎

Proof of Theorem 3.3: Algorithm 4 satisfies the setting of Proposition 3.12, and it follows from Propositions 3.10 and 3.11 that Algorithm 4 satisfies conditions and of Proposition 3.12 by letting , , and for all outer iterations . Therefore the conclusions of Propositions 3.12, 3.13, and 3.14 all hold true. Let denote the total number of iterates of Algorithm 4 computed prior to and including the first iterate that is an -relative solution (2). Since two iterates are computed at each iteration, we have (where is defined in Proposition 3.14) and it follows from Proposition 3.14 that , since the right-side of this inequality dominates both bounds and of (20). Substituting in the values of and and the bound on from Proposition 3.12 we obtain:

where the third inequality follows from substituting in the values and , which then rounds up to the desired bound in the theorem. ∎

4 Computational Guarantees when is Smooth

In this section we study the computational complexity of solving (1) in the case when is convex and differentiable on . We assume that is Lipschitz on as defined in (8).

Let us first consider directly applying the Accelerated Gradient Method (Algorithm 2) to solve (1), and let us apply Theorem 2.2. Let denote the relative accuracy, and note again that an -relative solution of (1) corresponds to an absolute -solution for . Let be the initial point. It then follows from Theorem 2.2 using (whereby ) that if

| (21) |

then

Herein we will derive a new computational guarantee for a version of the Accelerated Gradient Method that can improve on (21) in many cases. Our new version of the Accelerated Gradient Method periodically restarts the method with an appropriate rule for deciding when to do the restarts, and is presented in Algorithm 5. At the outer iteration of Algorithm 5 the algorithm starts the Accelerated Gradient Method at the point for optimizing on . The outer iteration runs until the ratio test in Step (2a.) fails, at which point the current point becomes the starting point of the next outer iteration, namely . The counter records the number of inner iterations computed in outer iteration . Similar to the notation in Algorithm 4, the notation “” in Algorithm 5 denotes assigning to the iterate of the Accelerated Gradient Method applied to the optimization problem (1) with objective function using the initial point .

We have the following computational guarantee associated with Algorithm 5.

Theorem 4.1.

(Complexity Bound for Accelerated Gradient Method with Simple Restarting) Within a total number of computed iterates that does not exceed

the Accelerated Gradient Method with Simple Restarting (Algorithm 5) will compute an iterate for which

The computational guarantee in Theorem 4.1 can itself be bounded by:

| (22) |

which follows from the chain of inequalities:

Comparing (22) with the standard bound for the Accelerated Gradient Method given in (21), we see that the factor involving in (22) is independent of , unlike the standard bound (21). Towards the proof of Theorem 4.1, for notational convenience we will work with two constants and that must be chosen to satisfy

| (23) |

and whose specific values are set to in Algorithm 4, and .

Proposition 4.1.

Let be the index of an outer iteration of Algorithm 5. Define

. If and exists, then it holds that:

| (24) |

Proof: It follows from Theorem 2.2 applied to the function and using that for any we have:

where the second inequality uses the definition of , and the last inequality uses the value of . ∎

Proposition 4.2.

Let be the index of an outer iteration of Algorithm 5. Define

. If and exists, then it holds that:

Proof: The proof follows using identical logic as in Proposition 4.1. ∎

Proof of Theorem 4.1: Even though Algorithm 5 does not simultaneously run two versions of the Accelerated Gradient Method, we can still view Algorithm 5 as an instance of the general algorithm setting of Proposition 3.12 by simply defining for all . It follows from Propositions 4.1 and 4.2 that Algorithm 5 satisfies conditions and of Proposition 3.12, and therefore Propositions 3.12, 3.13, and 3.14 hold for Algorithm 5. Substituting in the values of and using the fact that for all iteration counters , we obtain:

Next observe that , whereby it follows from Proposition 3.13 with that , and therefore it holds that:

Also, if , then similarly applying Proposition 3.13 with using the logic above implies that .

Let denote the total number of iterates of Algorithm 5 computed prior to and including the first iterate that is an -relative solution (2). Then where is defined in Proposition 3.14. In either case (i) or (ii) of (20), it follows from Proposition 3.14 that:

where the third inequality follows from substituting in the values and , which then rounds up to the bound stated in the theorem. ∎

It turns out that we can further improve the computational guarantee of Theorem 4.1 by further modifying the Accelerated Gradient Method with Simple Restarting (Algorithm 5), if we know and can easily work with an adjoint representation of to do “extra smoothing.” Let us see how this can be done. We will assume that has the representation:

| (25) |

where is a convex set and is a strongly convex function on with strong convexity parameter and for which . (See [13] for properties of strongly convex functions.) It then follows that is a globally smooth convex function with Lipschitz constant at most , see Nesterov [14]. We presume further that , , and are given and that the optimization problem in (25) is simple to solve. That being the case, for a given , if solves the optimization problem (25), then it holds that and .

In a similar spirit as the smoothing technique employed in Section 3.3, we will consider parametrically working with a modification of that is more smooth than by increasing the weight on the the strongly convex function in (25). For any define the function by:

| (26) |

If is bounded, then is finite, and the above smoothing technique has the following two properties:

(i) is not far from ,

| (27) |

(ii) has Lipschitz continuous gradient on with Lipschitz constant satisfying

| (28) |

This setting is very similar to the properties we have for smoothing of a non-smooth function in Section 3.3, and the only difference is that the Lipschitz constant here is bounded above by instead of by as was the case in (17).

Let be given. As before, we aspire to compute an -relative solution of (1) as defined in (2). We will use and analyze the Parametric Smoothing/Rescaling Method (Algorithm 4) but with defined by (26) and hence satisfying (27) and (28). We have the following computational guarantee associated with Algorithm 4 applied to the case when is smooth and is given by (26).

Theorem 4.2.

The dependence in Theorem 4.2 on the quality of the initial point is logarithmic in the optimality gap , while it is the square root of the optimality gap in Theorem 4.1. We will prove Theorem 4.2 by first proving two propositions. For notational convenience we will work with two constants and , whose specific values are and .

Proposition 4.3.

Let be the index of an outer iteration of Algorithm 4. Define . If and exists, then:

Proof: The proof follows by applying Proposition 3.9 with , , , and . It then follows that

where the second inequality uses from (28) and the final equality derives from substituting in the values of and . ∎

Proposition 4.4.

Let be the index of an outer iteration of Algorithm 4. Define

. If and exists, then:

Proof: The proof follows by applying Proposition 3.9 with , , , and . It then follows that

where the second inequality uses from (28) and the final equality derives from substituting in the values of and . ∎

Proof of Theorem 4.2: Algorithm 4 satisfies the setting of Proposition 3.12, and it follows from Propositions 4.3 and 4.4 that Algorithm 4 satisfies conditions and of Proposition 3.12 by letting and for all outer iterations . Therefore the conclusions of Propositions 3.12, 3.13, and 3.14 all hold true. Let denote the total number of iterates of Algorithm 4 computed prior to and including the first iterate that is an -relative solution (2). Since two iterates are computed at each iteration, we have , where is defined in Proposition 3.14 and is bounded by either or of (20).

Note that , whereby it follows from Proposition 3.13 that , and therefore

Similarly, if , similar logic demonstrates that . Therefore, in either case or of (20) it holds that:

where the third inequality follows from substituting in the values and , which then rounds up to the desired bound in the theorem. ∎

Appendix A Appendix

A.1 Growth Constant and the Modulus of Weak Sharp Minima

The optimal solution set of (1) is called a set of weak sharp minima with modulus if it holds that:

| (29) |

This concept was first developed by Polyak [17] when is a singleton, and generalized by Burke and Ferris [3] to include the possibility of multiple optima. The modulus of weak sharp minima has been a useful tool in sensitivity analysis [8, 11], convergence analysis for certain problem classes [7, 3], linear regularity and error bounds [4, 5, 6], perturbation properties of nonlinear optimization [23, 24, 2], as well as in the finite termination of certain algorithms [18], [9], and [7].

Comparing (29) to (5), we see that the modulus of weak sharp minima is a close cousin of the growth constant . Indeed, if we were to loosen the restriction that be a strict lower bound and instead allow it to take the value in the definition of in (3), then we would obtain precisely that . However, the notion of being a strict lower bound is fundamental for the results herein.

Note that (29) specifies the exact local growth of away from the set of optimal solutions. And although as defined in (29) the weak sharp minima is a global property, due to convexity it is essentially a local property and indeed its usefulness derives from the local nature of the weak sharp minima in a neighborhood of the optimal solution set. This is in contrast to the growth constant as defined in (3), which by its nature is a global property as illustrated in the constructions in Figure 1. Last of all we point out that while one can easily have for weak sharp minima (just let be a differentiable convex function whose optimum is attained in the relative interior of ), Theorem 1.1 shows that is finite for all reasonably-behaved convex functions.

A.2 Proof of Theorem 1.1

Proof of Theorem 1.1: Let us fix an optimal solution , and define and define . We will prove that for any , the following inequality holds:

| (30) |

which then implies that is finite. We consider two cases as follows:

Case (i): . In this case we have where and . Since is in the recession cone of it holds that , whereby

| (31) |

and therefore

which shows (30) in this case.

Case (ii): . Let be the projection of onto and let be the point on the line segment from to that satisfies . (Existence of is guaranteed by continuity of .) Then

References

- [1] Amir Beck and Marc Teboulle, Smoothing and first order methods: A unified framework, SIAM Journal on Optimization 22 (2012), no. 2, 557–580.

- [2] J. Frederic Bonnans and Alexander D. Ioffe, Quadratic growth and stability in convex programming problems with multiple solutions, Tech. report, INRIA Research Report RR-2403, 1994.

- [3] J. V. Burke and M.C. Ferris, Weak sharp minima in mathematical programming, SIAM Journal on Control and Optimization 31 (1993), no. 5, 1340–1359.

- [4] James V. Burke and Sien Deng, Weak sharp minima revisited, part I: basic theory, Control and Cybernetics 31 (2002), no. 3, 439–469.

- [5] , Weak sharp minima revisited, part II: application to linear regularity and error bounds, Mathematical programming 104 (2005), no. 2-3, 235–261.

- [6] , Weak sharp minima revisited, part III: Error bounds for differentiable convex inclusions, Mathematical Programming 116 (2009), no. 1-2, 37–56.

- [7] James V. Burke and Michael C. Ferris, A Gauss-Newton method for convex composite optimization, Mathematical Programming 71 (1995), no. 2, 179–194.

- [8] James V. Burke, Adrian S. Lewis, and Michael L. Overton, Optimal stability and eigenvalue multiplicity, Foundations of Computational Mathematics 1 (2001), no. 2, 205–225.

- [9] Michael C. Ferris, Finite termination of the proximal point algorithm, Mathematical Programming 50 (1991), no. 1-3, 359–366.

- [10] Trevor Hastie, Robert Tibshirani, and Jerome Friedman, Elements of statistical learning, second ed., Springer Series in Statistics, Springer, New York, 2009.

- [11] Abderrahim Jourani, Hoffman’s error bound, local controllability, and sensitivity analysis, SIAM Journal on Control and Optimization 38 (2000), no. 3, 947–970.

- [12] A. S. Nemirovsky and D. B. Yudin, Problem complexity and method efficiency in optimization, Wiley, New York, 1983.

- [13] Y.E. Nesterov, Introductory lectures on convex optimization: a basic course, Kluwer Academic Publishers, Boston, 2003.

- [14] Y.E. Nesterov, Smooth minimization of non-smooth functions, Mathematical Programming 103 (2005), no. 1, 127–152.

- [15] Yurii Nesterov, Smoothing technique and its applications in semidefinite optimization, Mathematical Programming 110 (2007), no. 2, 245–259.

- [16] Brendan O’Donoghue and Emmanuel Candes, Adaptive restart for accelerated gradient schemes, Foundations of Computational Mathematics 15 (2013), no. 3, 715–732.

- [17] B. Polyak, Sharp minima, Proceedings of the IIASA Workshop on Generalized Lagrangians and Their Applications, Laxenburg, Austria. Institute of Control Sciences Lecture Notes, Moscow, 1979.

- [18] B. Polyak, Introduction to optimization, Optimization Software, Inc., New York, 1987.

- [19] J. Renegar, “Efficient” subgradient methods for general convex optimization, SIAM Journal on Optimization, to appear.

- [20] , Efficient first-order methods for linear programming and semidefinite programming, Tech. report, Cornell University, 2014.

- [21] , A framework for applying subgradient methods to conic optimization problems, version 2, Tech. report, Cornell University, 2015.

- [22] , Accelerated first-order methods for hyperbolic programming, Tech. report, Cornell University, 2016.

- [23] Alexander Shapiro, Perturbation theory of nonlinear programs when the set of optimal solutions is not a singleton, Applied Mathematics and Optimization 18 (1988), no. 1, 215–229.

- [24] , Perturbation analysis of optimization problems in Banach spaces, Numerical Functional Analysis and Optimization 13 (1992), no. 1-2, 97–116.

- [25] Weijie Su, Stephen Boyd, and Emmanuel Candes, A differential equation for modeling Nesterov’s accelerated gradient method: theory and insights, Advances in Neural Information Processing Systems, 2014, pp. 2510–2518.

- [26] P. Tseng, On accelerated proximal gradient methods for convex-concave optimization, Tech. report, May 21, 2008.