Learning Instrumental Variables with Non-Gaussianity Assumptions:

Theoretical Limitations and Practical Algorithms

Ricardo Silva Shohei Shimizu

Department of Statistical Science / CSML University College London ricardo@stats.ucl.ac.uk Institute of Scientific and Industrial Research Osaka University sshimizu@ar.sanken.osaka-u.ac.jp

Abstract

Learning a causal effect from observational data is not straightforward, as this is not possible without further assumptions. If hidden common causes between treatment and outcome cannot be blocked by other measurements, one possibility is to use an instrumental variable. In principle, it is possible under some assumptions to discover whether a variable is structurally instrumental to a target causal effect , but current frameworks are somewhat lacking on how general these assumptions can be. A instrumental variable discovery problem is challenging, as no variable can be tested as an instrument in isolation but only in groups, but different variables might require different conditions to be considered an instrument. Moreover, identification constraints might be hard to detect statistically. In this paper, we give a theoretical characterization of instrumental variable discovery, highlighting identifiability problems and solutions, the need for non-Gaussianity assumptions, and how they fit within existing methods.

1 CONTRIBUTION

Consider a linear graphical causal model (Spirtes et al., 2000; Pearl, 2000), where given a directed acyclic graph (DAG) , we define a joint distribution in terms of conditional relationships between each variable and its given parents in :

| (1) |

That is, each random variable is also a vertex in , where are the parents of in and is an independent error term. Equation (1) is called a structural equation in the sense it encodes a relationship that remains stable under a perfect intervention on other variables. Using the notation of Pearl (2000), we use the index “” to denote the regime under which some variable is fixed to some level by an external agent. If is a parent of , the differential causal effect of on is given by:

| (2) |

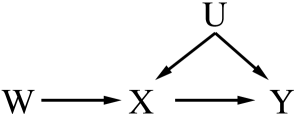

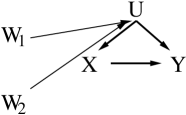

Each will be referred to as a structural coefficient. Our goal is to estimate the differential causal effect of some treatment on some outcome from observational data. If the common hidden causes of these two variables can be blocked by other observable variables, a formula such as the back-door adjustment of Pearl (2000) or the Prediction Algorithm of Spirtes et al. (2000) can be used to infer it. In general, unmeasured confounders of and might remain unblocked. In linear models, a possibility is to use an instrumental variable (or instrument, or IV): some observable variable that is not an effect of either and , it is unconfounded with , and has no direct effect on . Figure 1 illustrates one possible DAG containing an instrument, with further details in the next Section.

|

|

|

|

| (a) | (b) | (c) | (d) |

It is not possible to test whether some observable variable is an IV from its joint distribution with and , but IV assumptions can be tested under a variety of assumptions by exploiting constraints in the joint distribution of multiple observable variables (Chu et al., 2001; Brito and Pearl, 2002; Kuroki and Cai, 2005). However, existing contributions on parameter identification do not immediately translate to discovery algorithms. Our contribution are two IV discovery algorithms: a theoretical one, which is complete (in a sense to be made precise) with respect to a widely used graphical characterization of IVs; and a practical one, which although might not be complete, provides a practical alternative to the existing methods as the set of assumptions required is fundamentally different.

The structure of the paper is as follows. In Section 2, we discuss basic concepts of IV modeling, and the current state-of-the-art. We assume prior exposure to causal graphical models and structural equation models (Spirtes et al., 2000; Pearl, 2000; Bollen, 1989), including common concepts in causal graphical models such as d-separation, back-door paths, colliders and active paths111A partial summary for convenience: a vertex is active on a path with respect to a conditioning set if it is (i) a collider in this path and itself or one of its descendants is in ; OR (ii) not a collider and not in . A path is active if all of its vertices are active, blocked otherwise. A path between some and is into if the edge adjacent to in this path points to . A back-door (path) between and is a path without colliders that is into and .. In Section 3, we discuss the theory behind an IV discovery algorithm that is “complete” according to some equivalence class of models. The resulting algorithm has several practical issues, and a more realistic alternative is provided in Section 4, which is then validated experimentally in Section 5.

2 BACKGROUND

We assume a linear DAG causal model with observable variables . and do not precede any element of . does not precede . The goal is to estimate the differential causal effect of on .

This task is common in applied sciences, as in many cases we have a particular causal effect to be estimated, and a set of covariates preceding and is available. See Morgan and Winship (2015) for several examples. This is in contrast to the more familiar causal structure discovery tasks in the machine learning literature, where an equivalence class of a whole causal system is learned from data, and where some causal queries may or may not be identifiable (Spirtes et al., 2000). The focus here in on quantifying the strength of a particular causal query with background variables, as opposed to unveiling the directionalities and connections of a causal graph. This allows more focused algorithms that bypass a full graph estimation. This philosophy has been exploited by Entner et al. (2012) as a way of finding possible sets of observable variables that can block the effect of any hidden common cause of and . It does not, however, provide a causal effect estimate if such a set does not exist.

When unmeasured confounding remains, the existence of a variable such as in a system such as the one in Figure 1 will provide an alternative estimator. Using to represent the (conditional) covariance of two variables and (given set ), the parameterization in (1) implies , . It follows that . We can estimate and from observations, allowing for a consistent estimate of . Notice that is required.

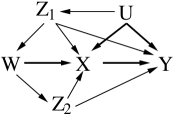

A variable that is not an IV may be a conditional IV. This means that if in the corresponding causal graph we find some set that deactive some relevant paths, then we can identify as . Figure 2(a) illustrates a case. A graphical condition for given is described by Brito and Pearl (2002) as follows:

-

1.

does not d-separate from in ;

-

2.

d-separates from in the graph obtained by removing the edge from ;

-

3.

are non-descendants of and in .

For the rest of the paper, we will call the above condition the graphical criteria for instrumental variable validity, or simply “Graphical Criteria.”

The simple inference methods we just described required knowing the causal graph. That being unavailable, the relevant structure needs to be learned from the data. The lack of an edge in Figure 1 is not testable (Chu et al., 2001), but in a situation such as Figure 2(b), the simultaneous lack of edges and has a testable implication, as in both cases we have and . This leads to what is known as a tetrad constraint,

| (3) |

which can be tested using observable data. Unfortunately, the tetrad constraint is necessary, but not sufficient, to establish that both elements in this pair of variables are instrumental.

Consider Figure 2(c). It is not hard to show that . However, the Graphical Criteria for IVs is not satisfied and, indeed, can be vastly different from . The core of our contribution is to show how we can complement conditions such as tetrad constraints with other conditions, tapping into the theory developed for linear non-Gaussian causal discovery introduced in the LiNGAM framework of Shimizu et al. (2006).

2.1 Previous Work

Hoyer et al. (2008) describes a method for inferring linear causal effects among pairs that are also confounded by hidden variables. The method, however, requires large sample sizes and the knowledge of the number of hidden common causes. Although finite, the number of possible differential causal effects that are compatible with the data increases with the number of assumed hidden variables.

The use of tetrad constraints for testing the validity of particular edge exclusions in linear causal models has a long history, dating back at least to Spearman (1904). More recently, it has been used in the discovery of latent variable model structure (Silva et al., 2006; Spirtes, 2013), where structures such as Figure 2(c) emerge but no direct relationships among observables (such as ) are discoverable. The combination of tetrad constraints and non-Gaussianity assumptions has been exploited by Shimizu et al. (2009), again with the target being relationships among latent variables. Tetrad tests for the validity of postulated IVs were discussed by Kuroki and Cai (2005). The literature on learning algorithms allowing for latent variables has been growing steadily for a long time, including the Fast Causal Inference algorithm of Spirtes et al. (2000) and more recent methods that exploit constraints other than independence constraints (Tashiro et al., 2014; Nowzohour et al., 2015), but none of these methods allow for the estimation of the causal effect of and when there is an unblocked unmeasured confounder between them. Phiromswad and Hoover (2013) introduced an algorithm for IV discovery, but it does not take into account unidentifiability issues that can be solved by exploring constraints other than covariance matrix constraints. Moreover, it attempts to recover a much complex graph than that is necessary to solve this particular question.

2.2 Directions

A recent algorithm for the discovery of instrumental variables has been introduced by Kang et al. (2015). It sidesteps the problems introduced by models such as the one in Figure 2(c) by a clever choice of assumptions: it is assumed that at least half of are “valid” IVs, by which this means that we can partition into two sets, , such that each is a conditional IV given . This is done without knowledge of which variables are valid and which are not. There are situations where this assumption is plausible, and the resulting algorithm (sisVIVE, “some invalid, some valid IV estimator”) is very elegant and computationally efficient.

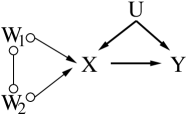

However, it does not take much to invalidate this assumption even when nearly all of can be used as instruments. Consider Figure 3 where we have an arbitrary number of IVs that are valid by conditioning on the empty set. None of them are valid by conditioning on , and in this situation sisVIVE may perform badly. In the following Sections, we introduce an alternative approach that exchanges the “at least half valid, given everybody else” condition with a less stringent condition on validity, combined with assumptions of non-Gaussianity and variations of the faithfulness assumption used in common causal discovery algorithms (Spirtes et al., 2000). In practice, however, we do exploit sisVIVE as a useful building block in a practical algorithm in Section 4. One difficulty is that for models such as in Figure 2(d), we will still not be able to directly reject as invalid and further assumptions would be needed.

3 THEORY

We assume our causal model is a LiNGAM model, a linear structural equation model with independent, non-Gaussian error terms, which may include latent variables (Shimizu et al., 2006). Some of the intermediate results in this Section will not require non-Gaussianity.

Algorithm 1 provides a method for inferring the causal effect of some given on some given , getting as input the joint distribution of . This is equivalent to having an oracle that replies yes or no to questions on particular tetrad and independence constraints. The goal is to show how we can provably find the correct causal effect in the limit of infinite data, or to say we cannot identify it (the “NA” return value). However, analogous to (Hoyer et al., 2008), there is some subtle but important equivalence class of results we need to consider. An algorithm for learning causal effects from empirical data is discussed in Section 4.

3.1 Preliminaries

Following Spirtes (2013), we call a rank constraint in a matrix any constraint of the type , where is some constant. If is the cross-covariance submatrix given by variables indexing the rows, and indexing the columns, then the rank constraint implies , as the latter is the determinant of .

We will use this notion in tandem with t-separation (Sullivant et al., 2010). First, let a trek from to in a graph be an ordered pair of (possibly empty) directed paths where: has sink (vertex without children in ) ; has sink ; and have the same source (vertex in without parents in ). The ordered pair of vertex sets t-separates vertex set from vertex set if, for every trek from a vertex in to a vertex in , either contains a vertex in or contains a vertex in . See Spirtes (2013) and Sullivant et al. (2010) for a generalization of this notion and further examples.

Let be the cross-covariance matrix of set (rows) and set (columns). The DAG Trek Separation Theorem of Sullivant et al. (2010) says:

Theorem 1 (Trek Separation for DAGs). Let be a DAG with vertex set . Let and be subsets of . We have in all linear structural equation models with graph if and only if there exist subsets and of with such that t-separates from .

To jump from (testable) rank constraints to (unobservable) constraints in , we assume our model distribution is linearly rank-faithful to a DAG (Spirtes, 2013): that is, every rank-constraint holding on a covariance (sub)matrix derived from is entailed by every linear structural model Markov with respect to (Spirtes, 2013). Linear faithfulness, the assumption that vanishing partial correlations hold in the distribution if and only if a corresponding d-separation also holds in (Spirtes et al., 2000), is a special case of rank faithfulness, as t-separation implies d-separation (Sullivant et al., 2010).

3.2 The Role of Non-Gaussianity

In the Graphical Criteria introduced in Section 2, the challenging condition is the second, as the first is easily testable by faithfulness and the third is given by assumption. Another way of phrasing condition 2 is: 2a, there is no active (with respect to ) back-door path between and , nor any active path that includes a collider, that does not include ; 2b, there is no active directed path from to that does not include . In the next Section, we will partially address 2b. Here, we exploit non-Gaussianity assumptions to partially tackle 2a. Our proof holds “almost everywhere,” in the sense it holds for all but a (Lebesgue) measure zero subset of the set of possible structural coefficients .

The motivation for this concept is analogous to the different variations of faithfulness, see the discussion on generic identifiability by Foygel et al. (2011) and Sullivant et al. (2010) for more background on excluding vanishing polynomials that are not a function of the graphical structure. For instance, the completeness of the do-calculus (Shpitser and Pearl, 2006; Huang and Valtorta, 2006) would be of limited relevance if in many models there were other adjustments by conditioning and marginalization that did not follow from the graphical structure. More specifically, linear faithfulness also holds almost everywhere in linear DAG models and it is assumed implicitly.

The main result of this section is the following:

Theorem 2. Let be a set of variables in a zero-mean LiNGAM model where has no descendants. For some , let be its local Markov blanket (all that are d-connected to given ). Let be the residual of the least-squares regression of on , with being the corresponding least-squares coefficients. Analogously, let be the residual of the corresponding least-squares regression. Then, almost everywhere, if and only if there are no active (with respect to ) back-door paths between and , nor any active path that includes a collider.

The proofs of this and the next result are given in the Supplementary Material.

3.3 Equivalence Class Characterization

Even when using non-Gaussianity, there are still structures which are indistinguishable by Algorithm 1. They form an equivalence class characterized as follows:

Theorem 3 (Downstream Conditional Choke Point Equivalence Class). Suppose the outcome of Algorithm 1, found with respect to some , is not correct under rank faithfulness and the assumptions of Theorem 2. Then, for each : (i) there is a directed path from to that is not blocked by ; (ii) the possible common ancestors of and elements in this path are blocked by ; (iii) this path includes some , where all directed paths from to in are blocked by ; (iv) all directed paths from to are blocked by .

The result is that any tuple that satisfies the conditions used by Algorithm 1 in effect belongs to an equivalence class of possible tuples, some of which may provide an incorrect causal effect. The common graphical feature in this equivalence class is what we call a “downstream conditional choke point,” illustrated by vertex in Figure 2(d). The name “downstream” denotes that this point is a descendant of , and has no active back-door paths with them. The name “choke point” is due to the fact that other common causes might exist between and , but no active paths, other than the directed paths passing through this choke point, will exist between and 222The literature has characterizations of unconditional choke points (Shafer et al., 1993; Sullivant et al., 2010), relating them to unconditional tetrad constraints. To the best of our knowledge, this is the first time that conditional choke points are explicitly defined and used. This is not a direct reuse of previous results, as the DAG class is not closed under conditioning (Richardson and Spirtes, 2002). Previous results were derived either for DAGs or for special cases of conditioning (Sullivant et al., 2010)..

By isolating this feature, we know how to explain the possible disparities obtained by letting a modified Algorithm 1 return the causal effects implied by each acceptable tuple. By knowing there is a single choke point per pair, which is unconfounded with the “candidate IVs,” and which lies on all unblocked directed paths from to , more sophisticated algorithms, combined with background knowledge, can be constructed that exploit this piece of information. However, different pairs might have different choke points, and we leave the description of a more complex algorithm for future work. If all tuples agree and we assume there is at least one valid tuple where are indeed IVs conditional on , then we are done, as guaranteed by this simple result:

Theorem 4 (Completeness). If there is a pair of observable variables are IVs conditioned on some according to the Graphical Criteria, and each has no active back-door path with given , nor any active path that includes a collider, then Algorithm 1 will find one.

Proof of Theorem 4. The test in Step 4 will not reject any such pair by linear faithfulness, as by the Graphical Criteria, d-connects the pair to . The test in Step 14 will not reject any such pair, since by Theorem 2 the test will reject the pair only if there is an active back-door path or a collider path between and . These situations are excluded by the Graphical Criteria, except in the case where such paths exist between and , as the concatenation of those with the edge would exclude from consideration.

To summarize: Algorithm 1 is sound, in the limit of infinite data, if we assume no downstream conditional choke point exists in the graph. A necessary but not sufficient test to falsify this assumption is by allowing a exhaustive check of all tuples with a minimal , and verifying whether they imply the same causal effect. The algorithm is complete in the case where for at least on pair the conditioning set also blocks active back-door/collider paths into . This means, for example, that the algorithm will not find answers in models where and have common causes that cannot be blocked, even if is a valid IV by not having common causes with . For example, is a valid IV in the model with paths , , but will be discarded due to the back-door path between and that is unblocked by not conditioning on .

4 CHALLENGES AND A PARTIAL SOLUTION

There are two major issues with Algorithm 1. First, testing (conditional) tetrad constraints often lead to many statistical errors, which can be mitigated by some elaborated tricks to take into account the redundancy of some constraints (Silva et al., 2006; Spirtes, 2013). This however leads to a complicated and not necessarily robust method. Second, an exhaustive search is in general not computationally feasible.

Instead, we combine ideas inspired by the theoretical findings of the previous Section with ideas underlying sisVIVE (Kang et al., 2015). One practical issue properly addressed by sisVIVE is that we want to discover as many (conditional) IVs as possible, as typically they individually will be weakly associated with the outcome .

Algorithm 2 modifies sisVIVE in the following way. In lines 1-3, we score each variable by estimating its least-squares residual , where is the vector formed by the local Markov Blanket of within all remaining variables in (see definition in Algorithm 1). Least-squares residuals are also estimated. We use a measure of dependence between the two residuals to define . In our implementation, tested in the next Section, we used the negative of the p-value of Hoeffding’s independence test between and , but other measures such as the HSIC (Gretton et al., 2007) could be used instead. The idea is to flag variables which might be linked to by “strong” active back-door paths, as motivated by Theorem 2, by marking a proportion of them (as given by parameter ) as unsuitable IV candidates. In our experiments, the proportion is set to .

Line 5 executes sisVIVE for a preliminary run, where we indicate: and , the treatment and outcome variables; a set , background variables to condition on but not to consider as possible instrumental variables; and a set which will be split into a set of (“valid”) IVs and a set of (“invalid”) conditioning variables . As discussed in Section 2, a weak point of sisVIVE is the impossibility of discarding “bad” conditioning variables. At this stage, however, we are still conditioning on all variables, but aiming at avoiding some of the most catastrophic mistakes of including a strongly confounded variable (given everything else) into the pool of IVs.

A refinement takes place in lines 6-14. We shrink a conditional set initialized with . Function BScore (“back-door score”) aims at measuring how “strong” paths are between elements of and that might go through back-doors or by conditioning on a sequence of colliders that ends in a back-door with . The actual implementation of BScore, used in the next Section, is simple: for each , estimate residual conditional on and the p-value of its dependence with (defined by least-squares of on ). The score is the product of all p-values over the elements of . We then shrink set to a local optimal. A last run of sisVIVE is then performed, returning the estimated differential causal effect dce.

We are aware of several shortcomings of this algorithm333It is a greedy method, and bad local optimal might happen. For instance, once a variable is excluded from the pool of possible IVs, it never goes back. Parameter should be chosen in a way that we believe a reasonable number of conditional IVs will remain. There is no formal guarantee that in an example such as Figure 3, variable will be ranked higher than by resDependenceScore, although heuristically this is justified by dependences typically decaying as longer paths are traversed in a graph.. The algorithm still relies on the underlying assumptions of sisVIVE, but relaxing it to require or more of valid IVs only on the subset . All these concerns are valid, but our point is to provide a reasonably simple algorithm that is justified by (i) how Theorem 2 provides a recipe to remove bad conditioning variables for sisVive; (ii) how Theorem 3 justifies relying on further assumptions, adapted from sisVIVE, as non-Gaussianity by itself is shown not to rule out invalid structures. Complex, more refined, algorithms will be object of future work. For now, we will show empirically how even a partial solution such as Algorithm 2 can provide improvements over the state-of-the-art method.

5 EXPERIMENTS

We assess how Algorithm 2 (which we will call B-sisVIVE, as in “back-door protected sisVIVE”) compares to other methods in a series of simulations.

| 100/0.25 | 1000/0.25 | 5000/0.25 | 100/0.50 | 1000/0.50 | 5000/0.50 | |

|---|---|---|---|---|---|---|

| NAIVE1 | 0.25 | 0.24 | 0.24 | 0.51 | 0.50 | 0.51 |

| NAIVE2 | 0.28 | 0.27 | 0.26 | 0.53 | 0.54 | 0.55 |

| NAIVE3 | 0.22 | 0.19 | 0.19 | 0.40 | 0.41 | 0.41 |

| ORACLE | 0.12 | 0.03 | 0.01 | 0.22 | 0.05 | 0.02 |

| W-ORACLE | 0.17 | 0.09 | 0.07 | 0.30 | 0.20 | 0.19 |

| S-ORACLE | 0.18 | 0.07 | 0.03 | 0.36 | 0.14 | 0.05 |

| SISVIVE | 0.20 | 0.13 | 0.15 | 0.41 | 0.38 | 0.42 |

| B-SISVIVE | 0.16 | 0.16 | 0.12 | 0.38 | 0.33 | 0.28 |

| B-SISNAIVE | 0.18 | 0.15 | 0.14 | 0.38 | 0.36 | 0.32 |

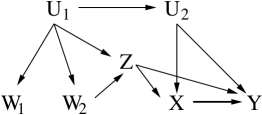

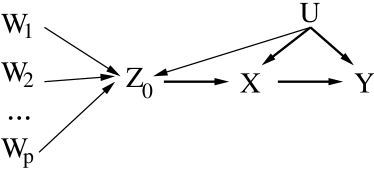

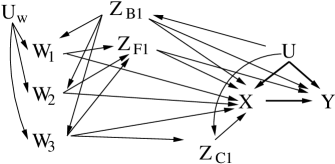

The simulations are performed as follows: we generate synthetic graphs by four groups of variables. Group are variables which can be used as conditional IVs. Group are variables which lie on directed paths from to and . Group are variables which are children of and , the unmeasured confounder between and . Finally, group are children of and parents of 444More precisely, the children of are in and its parents are and a second latent variable . The children of are , its parents are . The children of is only , its parents are . The children of are and its parent is only .. Figure 4 shows an example where .

The methods we compare against are: NAIVE1, obtained by least-squares of on , assuming no confounding; NAIVE2, two-stage least squares (TSLS) using all variables as instruments; NAIVE3, regression on and all other variables, assuming no confounding; ORACLE, using TSLS on the right set of IVs and adjustment set; W-ORACLE, uses as IVs, but conditions on all of the other variables; S-ORACLE, sisVIVE performed by first correctly removing the set ; SISVIVE, the Kang et al. (2015) algorithm taking all variables as input; B-SISVIVE, our method, with the same input; B-SISNAIVE, a variation of Algorithm 2, by skipping steps 7-14.

All error variables and latent variables are zero-mean Laplacian distributed, and coefficients are sampled from Gaussians, such that the observed variables have a variance of 1. Models are rejected until the causal effect has an absolute value of 0.05 or more. Coefficients are fixed at two levels, , the higher the harder, as this makes unmeasured confounding stronger. Sample sizes are set at 100, 1000, 5000. Comparisons are shown in Table 1, with the setup , , , . This satisfies the criterion of being more than the number of remaining variables, although only the 11 variables should be used.

The message in Table 1 seems clear. In particular, increasing the amount of confounding can make the problem considerably harder; sisVIVE works very well under the correct assumptions (as seen by the performance of S-ORACLE, which is just sisVIVE given the – usually unknown – information about which variables one should not condition on for validating the possible instrumental variables); otherwise, it can perform poorly (SISVIVE, which does hardly better than some naïve approaches); our method (B-SISVIVE) can provide some sizeable improvements over this state-of-the-art method. This is true even in its more straightforward variation, which does not refine its choice of conditioning set but only forbids some variables to be selected as instruments (B-SISNAIVE). We conclude these are important lessons in the estimation of causal effects with observational data.

6 CONCLUSION

Finding instrumental variables is one of the most fundamental problems in causal inference. To the best of our knowledge, this paper provides the first treatment on how this can be systematically achieved by exploiting non-Gaussianity and clarifying to which extent an equivalence class of solutions remains. We then proceeded to show how non-Gaussianity can be exploited in a pragmatic way, by adapting a state-of-the-art algorithm. Finally, we illustrated how improvement can be considerable under some conditions.

We expect that theoretical challenges in instrumental variable discovery can be further tackled by building on the findings shown here. In particular, as also hinted by Kang et al. (2015), some of the ideas here raised extend to non-linear (additive) and binary models. Methods developed in Peters et al. (2014) can potentially provide a starting point on how to allow for non-linearities in the context of instrumental variables.

More sophisticated graphical criteria for the identification of causal effects in linear systems were introduced by Brito and Pearl (2002). Further work has led to rich graphical criteria to identify causal effects in confounded pairs (Foygel et al., 2011). This goes far beyond the standard IV criteria discussed in Section 2. It also opens up the possibility of more elaborated discovery algorithms where back-door blocking (Entner et al., 2012) and the methods in this paper cannot provide a solution, but how to perform this task in a computationally and statistically tractable way remains an open question.

Code for the procedure and to generate synthetic studies is available at http://www.homepages.ucl.ac.uk/~ucgtrbd/code/iv_discovery.

References

- Bollen (1989) K. Bollen. Structural Equations with Latent Variables. John Wiley & Sons, 1989.

- Brito and Pearl (2002) C. Brito and J. Pearl. Generalized instrumental variables. Proceedings of 18th Conference on Uncertainty in Artificial Intelligence, 2002.

- Chu et al. (2001) T. Chu, R. Scheines, and P. Spirtes. Semi-instrumental variables: a test for instrument admissibility. Proceedings of the Seventeenth Conference on Uncertainty in Artificial Intelligence (UAI 2001), pages 83–90, 2001.

- Darmois (1953) G. Darmois. Analyse générale des liaisons stochastiques. Review of the International Statistical Institute, 21:2–8, 1953.

- Entner et al. (2012) D. Entner, P.O. Hoyer, and P. Spirtes. Statistical test for consistent estimation of causal effects in linear non-Gaussian models. Proceedings of the 15th International Conference on Artificial Intelligence and Statistics (AISTATS 2012), pages 364–372, 2012.

- Foygel et al. (2011) R. Foygel, J. Draisma, and M. Drton. Half-trek criterion for generic identifiability of linear structural equation models. Annals of Statistics, 40:1682–1713, 2011.

- Gretton et al. (2007) A. Gretton, K. Fukumizu, C. Teo, L. Song, B. Schölkopf, and A. Smola. A kernel statistical test of independence. Advances in Neural Information Processing Systems, 20:585–592, 2007.

- Hoyer et al. (2008) P. Hoyer, S. Shimizu, A. Kerminen, and M. Palviainen. Estimation of causal effects using linear non-Gaussian causal models with hidden variables. International Journal of Approximate Reasoning, 49:362–378, 2008.

- Huang and Valtorta (2006) Y. Huang and M. Valtorta. Pearl’s calculus of intervention is complete. Proceedings of the Twenty-Second Conference on Uncertainty in Artificial Intelligence (UAI 2006), pages 217–224, 2006.

- Kang et al. (2015) H. Kang, A. Zhang, T. Cai, and D. Small. Instrumental variables estimation with some invalid instruments and its application to mendelian randomization. Journal of the American Statistical Association, page To appear, 2015.

- Kuroki and Cai (2005) M. Kuroki and Z. Cai. Instrumental variable tests for directed acyclic graph models. Tenth workshop on Artificial Intelligence and Statistics (AISTATS 2005), 2005.

- Morgan and Winship (2015) S. Morgan and C. Winship. Counterfactuals and Causal Inference: Methods and Principles for Social Research. Cambridge University Press, 2015.

- Nowzohour et al. (2015) C. Nowzohour, M. Maathuis, and P. Bühlmann. Structure learning with bow-free acyclic path diagrams. arXiv:1508.01717, 2015.

- Pearl (2000) J. Pearl. Causality: Models, Reasoning and Inference. Cambridge University Press, 2000.

- Peters et al. (2014) J. Peters, J. M. Mooij, D. Janzing, and B. Schölkopf. Causal discovery with continuous additive noise models. Journal of Machine Learning Research, 15:2009–2053, 2014.

- Phiromswad and Hoover (2013) P. Phiromswad and K. Hoover. Selecting instrumental variables: A graph-theoretic approach. Working paper. Available at SSRN: http://ssrn.com/abstract=2318552 or http://dx.doi.org/10.2139/ssrn.2318552, 2013.

- Richardson and Spirtes (2002) T. Richardson and P. Spirtes. Ancestral graph Markov models. Annals of Statistics, 30:962–1030, 2002.

- Shafer et al. (1993) G. Shafer, A. Kogan, and P.Spirtes. Generalization of the tetrad representation theorem. DIMACS Technical Report, 1993.

- Shimizu et al. (2006) S. Shimizu, P. Hoyer, A. Hyvärinen, and Antti Kerminen. A linear non-gaussian acyclic model for causal discovery. Journal of Machine Learning Research, 7:2003–2030, 2006.

- Shimizu et al. (2009) S. Shimizu, P. Hoyer, and A. Hyvärinen. Estimation of linear non-gaussian acyclic models for latent factors. Neurocomputing, 72:2024–2027, 2009.

- Shpitser and Pearl (2006) I. Shpitser and J. Pearl. Identification of conditional interventional distribution. Proceedings of the Twenty-Second Conference on Uncertainty in Artificial Intelligence (UAI 2006), pages 437–444, 2006.

- Silva et al. (2006) R. Silva, R. Scheines, C. Glymour, and P. Spirtes. Learning the structure of linear latent variable models. Journal of Machine Learning Research, 7:191–246, 2006.

- Skitovitch (1953) W. Skitovitch. On a property of the normal distribution. Doklady Akademii Nauk SSSR, 89:217 ??–219, 1953.

- Spearman (1904) C. Spearman. “General intelligence,” objectively determined and measured. American Journal of Psychology, 15:210–293, 1904.

- Spirtes (2013) P. Spirtes. Calculation of entailed rank constraints in partially non-linear and cyclic models. Proceedings of the Twenty-Ninth Conference on Uncertainty in Artificial Intelligence (UAI 2013), pages 606–615, 2013.

- Spirtes et al. (2000) P. Spirtes, C. Glymour, and R. Scheines. Causation, Prediction and Search. Cambridge University Press, 2000.

- Sullivant et al. (2010) S. Sullivant, K. Talaska, and J. Draisma. Trek separation for Gaussian graphical models. Annals of Statistics, 38:1665–1685, 2010.

- Tashiro et al. (2014) T. Tashiro, S. Shimizu, A. Hyvärinen, and T. Washio. ParceLiNGAM: A causal ordering method robust against latent confounders. Neural Computation, 26:57–83, 2014.

APPENDIX: Supplementary Material

We present here proofs of Theorems 2 and 3. The result for Theorem 2 depends on this standard theorem (Darmois, 1953; Skitovitch, 1953):

Theorem 5. (Darmois-Skitovitch Theorem) Let be independent random variables, . Let , for some coefficients , . If and are independent, then those for which , are Gaussian.

The idea is that if we assume are not Gaussian, share a common source if and only if they are dependent. See (Shimizu et al., 2006; Entner et al., 2012) for a deeper discussion on how this theorem is used in causal discovery.

For the main results, we will assume particular algebraic (polynomial) identities implied by the model graph do not vanish at the particular parameter values of the given model (which we called “almost everywhere” results in the theorem). We will in particular consider ways of “expanding” the structural equations of each vertex according to exogenous variables, that is, any variable which is either an error term or latent variable (assuming without loss of generality that latent variables have no parents).

For each vertex in the model, and each exogenous ancestor of , let be the set of all directed paths from to . For each path , define , the product of all coefficients along this path for where (that is, is the parent of in this path. We multiply coefficients following a sequence ). From this,

| (4) |

where is the set of exogenous ancestors of , where for we have and path is given by the single edge . We refer to the idea of expansion a few times in the proofs as a way of describing how the models can be written as polynomial functions of the coefficients .

Overall, for a LiNGAM model with DAG , we denote by the set of exogenous variables of , and by the expanded graph of the graph augmented with the error terms and the corresponding edges for all observable vertices in .

The main result used in the proof of Theorem 2 comes from the following Lemma. Notice that the non-Gaussianity assumption and the Darmois-Skitovitch Theorem are not necessary for its proof.

Lemma 6. Let be the set of variables in a zero-mean LiNGAM model , where are the latent variables of the model. For some , let be . Let be the residual of the least-squares regression of on , with being the corresponding least-squares coefficients. Then, almost everywhere, can be written as a linear function of the exogeneous variables of , , where if and only if is d-connected to given in the expanded graph of .

Proof of Lemma 6. Without loss of generality, assume that each latent variable in has no parents. We will sometimes use as another representation of any particular model variable (observable, latent or error term), with the index indicating particular variables in and error terms, depending on the context.

One way of obtaining is by first performing least-squares regression of each model variable on , for some in , and calculating residuals . Define as the set of all residuals , . We then repeat the process by regressing on some element of , iterating until we are left with containing the single element , where is the size of and . The elimination sequence can be arbitrary.

Let be a vertex in . Let be the structural coefficient between and any . We define if is not a parent of . Since

we have

where is the covariance of and and here represents the covariance of and . This implies,

| (5) |

where is the least-squares regression coefficient of on . This means can be written as

| (6) |

with and defined analogously.

We can iterate this process until we are left with :

| (7) |

where . Variable is the residual of the regression of on , similarly for .

What we will show next is that within (7) each and can be expanded as polynomial functions of and , and the end result will contain non-vanishing monomials that are a (linear) function of only the exogenous variables which are d-connected to given in the expanded graph of . Since the monomials cannot vanish except for a strict subset of lower dimensionality than that of the set of possible , the result will hold almost everywhere.

Since we are free to choose the elimination ordering leading to , as they all lead to the same equivalent relation (7), let us define it in a way that a vertex can be eliminated at stage only when its has no ancestors in (where ).

For , the only exogenous variables which will have a non-zero coefficient multiplying in the least-squares regression are the parents of in the expanded graph, since has no other ancestors555Assuming is not a child of . In this case, without loss of generality we assume that the parents of are added to the parents of , and remove from the model at any iteration .. Let be the residual of some latent parent of ,

| (8) |

where if is a latent variable, or 1 if . Moreover, , where is the variance parameter of and is a polynomial function of . We can multiply both sides of the equation above by (as well all equations referring to any or such as (6)) to get a new system of variables that is polynomial in . We will adopt this step implicitly and claim that from (8) we have that can be expanded as parameters that are polynomial functions of . Moreover, it is clear from (8) that there will be at least one non-vanishing monomial containing each . In what follows, we refer to any expression analogous to (8) as the expansion of for .

We define a DAG with vertices , where will assume as children all and only the such that is a parent of in the original extended graph of the model. That is, is the extended graph over residuals after the first regression. The respective model is given by equations of type (6) with parameters coming from 666To be more precise, polynomial functions of such parameters, as we are implicitly multiplying each equation by ..

For any , let be the vertex being eliminated. Each in which is a parent of in will be a polynomial function of and a linear function the union of the exogenous variables present in the expansion of each parent of : the expansion analogous to (8) in the new model will always introduce new symbols into existing monomials, or create new monomials with , as vertex had no eliminated descendants up to iteration . As such, no exogenous variable will be eliminated from the algebraic expansion of the respective .

Finally, the expansion of in (7) will not cancel any monomial in the expansion of some other : since and are both parents of , no monomial in the expansion of can differ from a monomial in the expansion of by a factor of . So (7) will depend algebraically on the union of the exogenous terms leading to each .

To prove the Lemma, we start by pointing out that will have a latent/error parent of some in its expansion if and only if there is at least one sequence of vertices where is an observable child of and any two consecutive elements in this sequence have at least one common latent parent in (the sequence can be a singleton, ). To see this, notice that the different form an equivalence relation: each with a child which is being eliminated at iteration will include into its expansion the exogenous variables found in the expansion of the other parents of . This partitions into sets in which each vertex can “reach” some other vertex by first moving to some which shares a latent parent with and which can “reach” . The latent parents of are then partitioned according to their observed children.

To finalize the proof, suppose is d-separated from a latent/error parent of given . This happens if and only if all latent parents of (and ) are d-separated from given . Let be a latent parent of (or its error term). Then cannot have in its expansion. If this was the case, by the previous paragraph would be d-connected to all latent parents of , meaning would be d-connected to them. This implies . Conversely, suppose is d-connected to the error term or a latent parents of given . Then again by the previous paragraph, for any latent parent of , will have the latent parents of as terms in its expansion, implying almost everywhere.

We can now prove Theorem 2.

Proof of Theorem 2. Considering the system for , we can represent the model in an equivalent way where all latent variables are exogenous. Applying Lemma 6 to both and , and by Theorem 5, these variables will be dependent if and only if they are a non-trivial linear function of at least one common exogeneous variable in the model. By Lemma 6, this happens if and only if is d-connected to given and is d-connected to given and . If is d-connected to given only, and since the concatenation of the path with path must be by either colliding at the same child of , or connected through some , where is in the path connected to (which needs to be into ) and is in the path connect to (which is into ), the theorem holds. If is not d-connected to given only, then must be d-connected to given by a path that is into , and the claim again follows.

The proof of the final result is as follows:

Proof of Theorem 3. Point (i): according to the Graphical Criteria for IVs, there should be an active path from to that does not include , or otherwise the algorithm would return the right answer. This path has to be directed, as any other possible active path based on back-doors or conditioning on colliders has been ruled out by the non-Gaussian residual test (Theorem 2).

Point (ii) is related: if there was an active back-door path between and some connected to by an active directed path, then the concatenation of the two paths would lead to an active back-door path between and , contrary to the result of the residual test.

Now we show point (iii). Since , the covariance submatrix formed by using as rows and as columns has determinant , which follows from standard block matrix decompositions. Rank faithfulness, combined with the Trek Separation Theorem, and the fact that is of minimal size (i.e., there is no proper subset of it satisfying the tests in Algorithm 1), implies there is a pair of sets such that the rank of the covariance submatrix is . There are (trivial) treks of zero edges between elements of , implying all of is necessary for the t-separation to hold. Moreover, as is minimal, it is not possible for a vertex in to be both in and , as this would create an active path from to colliding at , contrary to the tests in the algorithm. Therefore, there is exactly one other vertex not in needed for the t-separation to hold. Then any treks from to will have to go through this vertex, which by point (ii) have to be directed paths.

For point (iv): if there is an unblocked path from to not going through , this would contradict that , as there would be no elements left to cover this extra trek.

Remarks: The assumptions are stronger than, for instance, the ones used in the proofs of Tashiro et al. (2014). A closely related result in that paper is its Lemma 2, a result identifying the dependence between the residual of the regression of a variable on its children. It does not use any variation of the faithfulness assumption. This is because, in their context, it is enough to detect the dependence between the residual and some children. So if some path cancellations take place, some other path cancellations cannot occur. But we need the dependence of our and every relevant error term, because we cannot claim that depends on some error terms or latent variables, while depends on some error terms or latent variables, if these two sets do not overlap. Although some of the ideas by Tashiro et al. (2014) could be used in our context to build partial models and from the deduce instrumental variables, it goes against our framework of solving a particular prediction problem (causal effect of a target treatment-outcome) directly, instead of doing it by recovering parts of a broader causal graph.

Finally, we have not provided an explicit discussion on how to validate the non-Gaussianity assumption by testing the non-Gaussianity of the residuals, as done by Entner et al. (2012). Or, more precisely, showing which assumptions are necessary so that testing non-Gaussianity of the residuals is equivalent to testing non-Gaussianity of the error terms. This is left as future work.