The Sample Complexity of Auctions with Side Information††thanks: This is the fifth arXiv version of the paper. Importantly, this version presents a correct proof for the strong revenue monotonicity property, while the previous proof has a fatal bug. We have also rewritten most parts of the paper to improve exposition, and to clarify the scopes within which the technical ingredients hold.

Abstract

Traditionally, the Bayesian optimal auction design problem has been considered either when the bidder values are i.i.d., or when each bidder is individually identifiable via her value distribution. The latter is a reasonable approach when the bidders can be classified into a few categories, but there are many instances where the classification of bidders is a continuum. For example, the classification of the bidders may be based on their annual income, their propensity to buy an item based on past behavior, or in the case of ad auctions, the click through rate of their ads. We introduce an alternate model that captures this aspect, where bidders are a priori identical, but can be distinguished based (only) on some side information the auctioneer obtains at the time of the auction.

We extend the sample complexity approach of Dhangwatnotai, Roughgarden, and Yan (2014) and Cole and Roughgarden (2014) to this model and obtain almost matching upper and lower bounds. As an aside, we obtain a revenue monotonicity lemma which may be of independent interest. We also show how to use Empirical Risk Minimization techniques to improve the sample complexity bound of Cole and Roughgarden (2014) for the non-identical but independent value distribution case.

1 Introduction

A significant part of auction design theory is on auctions that maximize the revenue generated. The predominant model here is that of Bayesian Mechanism Design: the bidder values are assumed to be drawn from a given distribution, and the objective is the expected revenue, where the expectation is over the draw of values and randomization in the mechanism itself, if any. The seminal result in this field is the much celebrated Myerson’s [22] theory of optimal auctions. When bidders’ values are independently and identically distributed (i.i.d.), it gives the beautiful conclusion that a second price auction with a reserve price is revenue optimal among essentially all reasonable auction formats. When the bidders are distinguishable, via a distinct value distribution for each bidder (which is still independent of other bidders’ valuations), the theory completely characterizes the optimal auction, even though it is not as simple as in the i.i.d. case. We will refer to this as the Myerson model.

Sample Complexity

The question that we consider in this paper is that of sample complexity: how many samples from the distribution are necessary/sufficient to approximate the optimal auction?

The sample complexity approach to revenue maximization [9, 8, 19, 21] assumes that we are given access to samples from the value distribution and measures the number of samples that are necessary/sufficient to approximate the optimal auction. This study is motivated by the observation that the source of priors is really past data, both in principle and in practice [23]. The goal has been to put such practices on a sound theoretical footing, by identifying principled approaches and precisely quantifying the value of data.

Dhangwatnotai, Roughgarden, and Yan [9] initiated this line of research, by giving almost tight bounds for the case of a single agent. This was later extended to the Myerson model by Cole and Roughgarden [8].111They made an assumption that the distributions are regular, which implies that a certain revenue function is concave. This is a common assumption in the literature; see Section 2 for a definition. In this paper we improve their [8] upper bound, from to . Section 3 presents a detailed discussion of the upper and lower bounds for different variants, and comparisons with other related work such as Morgenstern and Roughgarden [21] and Huang, Mansour, and Roughgarden [19].

Side Information

The Myerson model could be applicable in practice when bidders can be classified into a few different categories, and market research provides a distribution for each of these. We observe that often, the classification of bidders is a continuum, rather than discrete. Suppose for instance that the auctioneer knows the incomes of all the bidders. It is reasonable to assume that bidders with higher incomes in general have higher valuations and thus use this information in the auction design.

In this paper, we propose a model where the side information that can be used to distinguish between the bidders comes from a continuum. A priori, bidders are identical: all bidders draw two numbers, a value and a “signal”, i.i.d. from a joint probability distribution. The signal is a real number in that captures the side information that the auctioneer has about the bidder; in other words the bidder can only lie about his value and not his signal. We will refer to this as the signals model.

From the Bayesian Mechanism Design perspective, Myerson’s theory readily extends to the signals model: once you condition on the signal for each buyer, you have a different (and independent) distribution for each buyer, and the setting reduces to the Myerson Model. The same is not true from the sample complexity perspective. Even when the bidder categories are discrete,222Our model can handle discrete categories as well, where the signal is just an encoding of the categories. there is a distribution over categories as well. If bidders from some categories appear more often than others, then it is more important that the auction does the right thing for these categories. This is represented in the samples as well: the number of samples for each category is different if you collect samples at random from the population. The sample complexity results in the Myerson model assume that the same number of samples are available for each category, or equivalently, the quantity in question is the minimum number of samples across all categories; this can lead to suboptimal guarantees.

Techniques

Cole and Roughgarden [8] approached the problem by approximating what is called the ‘Myerson virtual value function’333This is a function that depends on the probability distribution of values; see Section 2 for a definition. based on samples. We take quite a different approach: our improvement in the sample complexity upper bounds for the Myerson Model comes from an Empirical Risk Minimization (ERM) approach. The main step is to show how to discretize the value space with a (relatively) small support size, while losing only an fraction of the revenue for some given . This then allows us to bound the number of different mechanisms that we need to consider. Then we use a concentration inequality to argue that for each mechanism in this class, its revenue on the sample closely approximates its actual revenue from the distribution. Thus, using the best auction on the sample suffices.

As an important part of this approach we use a new concentration inequality.444We discovered this inequality without knowing that Babichenko, Barman, and Peretz [2] had earlier discovered a very similar version. Consider the revenue of a mechanism with agents in the Myerson Model. Consider a matrix of values, each drawn independently, with the values in column drawn from the distribution corresponding to agent . Standard concentration inequalities such as Bernstein inequality tell us that the revenue of a mechanism averaged over the row vectors of this matrix is close to its expected revenue with respect to (w.r.t.) the distribution. The concentration inequality we use gives the same conclusion for the revenue of the mechanism w.r.t. the product of the empirical distributions over each column of the matrix. Due to this, instead of finding the optimal auction for a correlated distribution, it is sufficient to find the optimal auction for a product distribution, a computationally easy task.

The signals model presents the following new conceptually important challenge: we cannot rely on having seen samples with exactly the same signals as the participants in the auction. This requires us to be able to interpolate using samples from different distributions, rather than use samples from the same distribution as in the Myerson Model.555This introduces additional difficulties such as that convex combinations of regular distributions are not regular, e.g., see Sivan and Syrgkanis [27]. We do this by using just the right number of signals in the sample immediately below the actual signal of an agent, and run a version of the Empirical Myerson auction: the Myerson auction run on the empirical value distributions given by the samples. The approximation factor is proved via a careful charging argument. Our bounds depend on the following function of the distribution: function specifies that an fraction of the revenue is contributed by the top fraction (in probability mass) of signals. For instance, when there is a single agent, we show that samples are sufficient and are necessary.666This is not a contradiction since it turns out that is always at most and is a monotone increasing function for small enough .

An essential component of interpolating from different distributions is revenue monotonicity. Consider the optimal auction for a given product distribution . If is run on values that come from a higher (component wise first order stochastic dominating) distribution, does it get a higher revenue? Surprisingly, as far as we know, this fundamental question about optimal auctions was unanswered prior to this paper; we resolve this in the affirmative. Another application of this property is in devising mechanisms when only certain statistics (such as the medians) of the value distributions are known (Azar et al. [1]).777A natural mechanism to consider in such a setting is the optimal mechanism w.r.t. the minimal distribution with the given statistics. Given the value of the median , the distribution which is 0 or with probability each is first order stochastically dominated by all other distributions with median . The proof of this property is a nontrivial amortization argument.888Direct approaches seem to fail here. Consider the following example, where increasing one component distribution first increases the revenue, and then increasing another component decreases the revenue (all w.r.t. an optimal mechanism for the original distribution). There are two bidders: bidder has value distribution and bidder has distribution . The virtual value functions are and respectively. If bidder ’s distribution is replaced by , the revenue strictly increases, since the probability of allocating the item to her (for a high price) increases. In fact bidder always gets the item, except when she has a value in and bidder has a value in with higher virtual value. When this occurs the item is sold to bidder for a low price. The probability of this event strictly increases when bidder ’s distribution is replaced with a point mass at , and thus the revenue slightly decreases. The net effect is still an increase in revenue, as guaranteed by our theorem. This also shows that revenue monotonicity is not true w.r.t any mechanism. We design two amortized gain functions whose expectations upper and lower bound an auction’s expected revenue respectively. We then couple the (randomized) revenue of Myerson’s optimal auction on distribution and its revenue on a higher distribution based on the quantiles of agents’ values. We show that for any given quantiles, the first amortized gain of the former is less than or equal to the second amortized gain of the latter. See Section 4 for details.

For lower bounds, we extend the instances used by Huang et al. [19], by packing scaled copies of them among the conditional distributions for different signals. We show that in order to achieve high revenue overall it is necessary to achieve high revenue in most of the conditionals. Moreover, in order to get good revenue from any conditional (even with exact knowledge of the rest) a reduction to classification shows that samples are necessary; the bound follows.

Extensions

Our results can be extended to more general single parameter families of auction environments. We can also get better upper bounds for the case of agents when we are required to optimize over a smaller class of auctions, such as VCG with reserve prices. We discuss these extensions in Section 8.

1.1 Other Related Work

Sample Complexity

Elkind [11] also considered a learning question very similar to the sample complexity line of work [9, 8, 19, 21], in the presence of an oracle that returns the expected profit of a given mechanism, for distributions with finite support. This line of work is also close in spirit to Balcan et al. [3], who used PAC learning techniques to design prior-free auctions in a general setting. In fact, Huang et al. [19] noted that the results of Balcan et al. [3] could be used to deduce sample complexity bounds in the i.i.d. model. In addition to the lower bound of for regular distributions, Huang et al. [19] also showed tight bounds of for MHR distributions. While all these results are for single parameter environments, Dughmi, Han, and Nisan [10] showed an exponential lower bound for a multi parameter setting.

Ad Auctions

Billions of auctions are run each day for ads, for search and display advertising. Setting reserve prices in these auctions has received a lot of attention [12, 28, 24, 23], and has been one of the prime applications of Myerson’s theory [23]. Common techniques in practice include using machine learning algorithms, to map features of an auction into one of few categories, and use the corresponding reserve price. Most commonly, the mapping results in a continuous variable, and an extra effort is required to map this into discrete categories. It would be more natural to use the continuous variable itself, which would correspond to the signal in our model.

1.2 Future Directions

Much of the auction theory since Myerson, in particular in the algorithmic game theory literature, is devoted to cases where the distributions are unknown. One can ask several ‘simple versus optimal’ questions in the signals model, such as an extension of the famous result of Bulow and Klemperer [5]: how much does the market size have to increase for the Vickrey auction to outperform the optimal auction. Another interesting direction is to ask for the design of a prior-independent mechanism in this model, which might be easier than a similar attempt in the prior-free setting by Leonardi and Roughgarden [20] and Bhattacharya et al. [4]. Finally, extending this model to align it even closer with how machine learning algorithms are used, by directly considering high dimensional signal space is a really exciting direction.

2 Preliminaries

Notations

For any positive integer , let denote the set of positive integers that are at most . For any binary vector , we abuse notation and let denote the set of bidders as well. Hence, if we write , it means that is identical to , except that its -th coordinate is set to while its -th coordinate is set to . Similarly, is a vector whose -th coordinate is if and only if and .

2.1 Single Parameter Revenue Maximization

Let there be an auctioneer with a single type of item for sale. Let there be bidders who are interested in getting a copy of the item (we simply say getting an item for brevity hereafter). The value of bidder for the item is , which is private information known only to bidder but not to the other bidders and the auctioneer. Let there be a feasible set of allocations ; for any allocation , each coordinate denotes the probability that bidder gets an item.

This paper considers three families of feasible sets , with each one more general than the previous one.

-

•

Single-item setting: . It corresponds to the case when the auctioneer has a single item for sale. This is arguably the simplest single parameter problem.

-

•

Matroid setting: is the convex hull of a matroid . Here, is a matroid if it satisfies the following properties. (1) It includes the empty allocation, i.e., (nonemptiness). In fact, we will further assume that all singleton sets are feasible; it is without loss of generality (wlog) up to the removal of irrelevant bidders. (2) It is downward-closed, i.e., for any (coordinate-wise), such that , we have (hereditary property). (3) For any distinct , such that allocates to more bidders than , there exists such that (augmentation property). For any problem in the matroid setting, all maximal feasible allocations have the same number of bidders, which is called the rank of the matroid. Let denote the rank of the matroid. The single-item constraint, and the more general case when the seller has copies of the item and hence can allocate to up to bidders, are both special cases of the matroid setting.

-

•

Downward-closed setting: Finally, we drop the third property in the matroid constraint and consider arbitrary feasible sets that are downward-closed. Let denote the maximum number of allocated bidders in any feasible allocation.

All results in this paper apply to the single-item setting. Most of them further generalize to the matroid setting, or even the downward-closed setting. Our theorem statements will explain the scope in which the results hold.

From the revelation principle, it is sufficient to consider direct revelation mechanisms: a mechanism is a pair of functions , both taking as input a reported value profile, often referred to as bids, . The allocation function has for each bidder , a component that represents her probability of winning the item. It further ensures feasibility, i.e., for any bids , we have . Similarly, the payment function has a component for the payment of each bidder . We will omit the bids for brevity when it is clear from the context. The utility of bidder is .

A mechanism is dominant strategy incentive compatible (DSIC) if the utility of a bidder is maximized, no matter what the other bidders report, by reporting her true value. A mechanism is individually rational (IR) if the utility of each bidder is non-negative, for all valuation profiles. In general, the bids need not equal the true values . Nonetheless, throughout the paper we only consider DSIC and IR mechanisms, and therefore omit qualifying mechanisms as DSIC and IR everywhere, and abuse notation and use to denote the bids as well.

The objective we consider in this paper is maximizing the revenue of a mechanism, when the values are drawn from a given probability distribution. We let denote the expected revenue of mechanism when is drawn from distribution :

The mechanism that maximizes for a given distribution , among all DSIC and IR mechanisms, is called the optimal auction, and its revenue is denoted by .

Myerson’s Optimal Auction:

Myerson [22] characterizes the optimal auction for the case of product distributions , which is also the focus of this paper. The optimal auction relies on a concept called virtual value. For simplicity, we explain it under the assumption that the distribution is continuous, as in the original paper of Myerson [22]. Let and denote the cumulative distribution function (cdf) and probability density function (pdf) respectively of distribution . The virtual value of a bidder when his value is is:

The optimal auction is simple to describe under the assumption that each is regular, which means that the virtual value is monotonically non-decreasing. Myerson [22] shows that the expected revenue of any truthful auction equals the expected virtual welfare, i.e.,

Hence, Myerson’s optimal auction allocates to a subset of bidders such that the above sum of virtual values is maximized; this is equivalent to allocating to the bidder with the highest non-negative virtual value in the single-item setting (breaking ties arbitrarily). Each winner pays the minimum bid that will make her win. For example, in the single-item setting, the payment by the winner is:

When the distributions are not regular, on the other hand, the optimal auctions must “iron” the virtual value function of each bidder to get an ironed virtual value, denoted as . Then, it allocates to a subset of bidders so that the sum of ironed virtual values is maximized (breaking ties arbitrarily); each winner pays the minimum bid that will make her win.

For the purpose of understanding most results and proofs in this paper, it is unimportant how the ironed virtual value is defined and how to generalize the definition to distribution with point masses; we will only use the fact that the optimal auction is an ironed virtual value maximizer characterized by the mapping from values to ironed virtual values for each of the bidders. The only place that makes use of the definition of ironed virtual value and the generalization to distribution with point masses is Section 4 and, hence, the formal definition is deferred to that section.

2.2 Myerson Model

Cole and Roughgarden [8] introduced a sample complexity approach to the design of optimal auctions.999See, also, Dhangwatnotai et al. [9] and Elkind [11] for some earlier works with a similar flavor. Assume that the distribution is unknown to the auctioneer, who instead has to design a mechanism with access to data only in the form of i.i.d. samples drawn from . The mechanism is then run on a fresh vector of values (the real input) drawn from .

Given such an algorithm that maps collections of samples to mechanisms, the sample complexity of it against a given class of distributions is specified as a function of , the number of bidders , and potentially other attributes of the class of distributions and the set of feasible allocations. It is defined to be the smallest number of samples such that for all distributions in the given class, it holds that:

Here it is implicit that the mechanism depends on the samples . Further, even though the above definition states the approximation guarantee only in expectation, essentially all positive results in the literature, including those in this paper, achieve the approximation ratio with high probability.

We will refer to it as the Myerson model in this paper.

2.3 Signals Model

In this paper, we introduce a model where the auctioneer has some information correlated with the bidders’ values. We assume that each bidder has a value-signal pair , drawn from a joint distribution . As before, is her valuation for the item and is a signal observed by the auctioneer, e.g., her annual income, or her propensity to buy an item based on past behavior, or in case of ad auctions the click-through rate of her ad. For a given signal , we denote the conditional distribution over values by . It is convenient to think of as a family of -dimensional distributions , along with the marginal distribution over , given by the cdf . We assume throughout this paper that is such that if , then first order stochastically dominates (denoted by ). The mechanism now has as input the actual signals, in addition to the reported values.

We extend the sample complexity approach to this model: the auctioneer first observes i.i.d. value-signal pairs sampled from the given distribution, and the signals of bidders whose value-signal pairs are fresh samples (the real input); then, based on the samples, the auctioneer designs a mechanism that is tailored to the realized signals of the bidders. The sample complexity will as before depends on (among other parameters), and is defined as the minimum number of samples required to achieve a fraction of the optimal revenue , defined as:

The role of signals in this model is similar to that of contexts in the contextual bandit problem. Therefore, we will refer to this model as the signals model.

The signals model is incomparable to the Myerson model. Note that in this model, the bidders are a priori identical, but become non-identical once the signals are observed. This allows a mechanism to be a priori symmetric, and distinguish between the bidders based only on the signals. Also in this model, the samples may contain entirely different signals than the actual ones. In other words, it might be that the actual signals are never seen in the samples; the algorithm must nonetheless be able to learn approximately optimal auctions w.r.t. the actual signals from the samples. Further, there is a distribution over signals themselves which affects the definition of . Both models however generalize the special case of the Myerson model when bidders have i.i.d. value distributions.

We call a distribution regular if is regular for any .

3 Main Results

Table 1 summarizes the main results in this paper. The results come in two flavors: improved sample complexity upper bounds for the Myerson model without signals, as well as lower and upper bounds for the signals model introduced in this paper. Finally, we highlight some of the technical lemmas that would be of independent interest.

| Model | Number of Agents | Distributions | Lower Bound | Upper Bound |

| Myerson Model | Regular | [19] | [9] | |

| Regular | [8] [19] | (Section 6) | ||

| MHR | [8] [19] | (Section 6, see also [21]11footnotemark: 1) | ||

| Support | [19] | (Section 6, see also [21]11footnotemark: 122footnotemark: 2) | ||

| Support additive error | (folklore) | (Section 6, see also [13]22footnotemark: 2) | ||

| Signals Model | 1 | Regular -bounded tail | (Section 7.3) | (Section 7.1) |

| Regular -bounded tail | (Section 7.2) | |||

| 11footnotemark: 1 The bounds from previous work are information theoretic while ours are computationally efficient. 22footnotemark: 2 The bounds were not explicit in the papers but to our understanding can be derived from their methods. | ||||

3.1 Sample Complexity: Regular Distributions

We show a sample complexity upper bound of for learning revenue optimal auctions with non-i.i.d. regular value distributions. It significantly reduces the gap between the upper and lower bounds from Cole and Roughgarden [8], which were respectively and . For the case of , Huang et al. [19] showed a lower bound of .

3.2 Sample Complexity: Beyond Regular Distributions and a Single Item

The conference version of this paper focused mainly on regular distributions, but our techniques are general enough to handle other classes of distributions considered in the literature, including monotone hazard rate (MHR) distributions, distributions with bounded support in , and distributions with bounded support in but aiming for an additive approximation instead of a multiplicative one.

The first two classes were studied by Morgenstern and Roughgarden [21], who showed information theoretic upper bounds of for the -bounded distributions, and for MHR distributions. They used the technique of bounding the pseudo-dimension, from statistical learning theory, as compared to our more elementary technique of building an -net explicitly; these two approaches are similar in spirit. To our understanding, the upper bound from their approach for the -bounded case can be improved to by using Bernstein instead of Chernoff as the concentration inequality.

A simple modification of our techniques obtains matching upper bounds of for -bounded distributions, and for MHR distributions. Importantly, with a concentration inequality for product distributions that we shall explain shortly, our results are constructive and computationally efficient while the ones in Morgenstern and Roughgarden [21] are not.

Subsequent to the conference version of this paper, Gonczarowski and Nisan [13] proved a sample complexity upper bound of for the -bounded case. To the best of our understanding, the precise bound from their approach is , which is also what the techniques in this paper give. The main difference lies in the proof of why a discretized Myerson auction can give almost optimal revenue up to an additive factor. Our proof builds on an interpretation of the Myerson auction in the quantile space, while Gonczarowski and Nisan [13] gave an explicit rounding of the Myerson auction based on the virtual values. Gonczarowski and Nisan [13] extended their results beyond single-item auction with a worse yet still polynomial sample complexity upper bound. We explain in Section 8 why our techniques apply to -bounded case; interested readers may apply our techniques to get essentially the same bound (with minor differences in logarithmic factors) as Gonczarowski and Nisan [13].

Roughgarden and Schrijvers [25] considered the special case of i.i.d. bidders with -bounded support, and showed a sample complexity of . Their bound is incomparable with ours in that ours has a worse dependence in while theirs has a worse dependence in . We stress that our upper bound holds for the more general non-i.i.d. case.

We rewrite our technical sections (Section 6 and Section 8) to clarify how our techniques are general enough to be applied to these other classes of distributions.

Beyond the Techniques of This Paper

Subsequent results by Guo, Huang, and Zhang [15], Guo et al. [16], and Chen et al. [7] built on the notion of revenue monotonicity introduced in this paper to characterize the optimal sample complexity up to logarithmic factors for all single parameter auction settings. For the more general multi parameter auctions, Gonczarowski and Weinberg [14] proved the first polynomial sample complexity upper bounds when bidders have additive or unit demand valuations, which were later further improved by Guo et al. [16].

3.3 Signals Model

Our sample complexity bounds for the signals model depend on the following property of the joint distribution of value-signal pairs. The property is defined via a function such that ignoring the top quantiles in the signal space reduces the revenue by less than an fraction.

Definition 1 (Small-tail in signal space).

Given a function , we say that a distribution has a -bounded tail in the signal space if:

Intuitively, the sample complexity needs to have at least a linear dependence on , since we need at least that many samples to even see a single in the top quantile. If you do not see any signal from this range, then there is no hope of capturing their contribution to the revenue, which could be an fraction. Another important observation is that because of the monotonicity of in the signal space, the top quantile contributes at least an fraction of the revenue. This implies that is always no larger than .

For the case of a single bidder, we show a sample complexity upper bound of in the signals model, which is larger than the corresponding optimal bound in the Myerson model by essentially a factor of . We also complement our positive result with a lower bound of , which is larger than the corresponding optimal bound in the Myerson model by a factor of . It is to be expected that the signals model requires more samples, since we need to cover the entire spectrum of different ’s.

With bidders, we show an upper bound of . Note that one sample in the Myerson model is actually values, whereas one sample in the signals model is only one value. Taking this into account, the upper bounds still differ by a factor of . We currently do not have any lower bounds for the signals model in the multi-bidder case, since in this model, having more agents might actually help! Closing the gap between the bounds, or parameterizing the bounds using other reasonable quantities are interesting open questions.

3.4 Strong Revenue Monotonicity

We say that a product distribution component-wise stochastically dominates another product distribution , and denote it by , if for each , we have that . We prove the following theorem which is of independent interest:

Theorem 3.1 (Strong Revenue Monotonicity).

Consider any single parameter mechanism design problem in the matroid setting. Let be a product distribution, and be an optimal auction for . Then, for any product distribution , we have:

Remark 3.1.

All optimal auctions are virtual welfare maximizers, identical up to tie breaking rules. We can make the optimal auction for a product distribution unique as follows: add an infinitesimal to all values in the (finite) support of , such that . In the new product distribution the revenue is the same, but the only optimal tie breaking rule is lexicographical.

Hart and Reny [17] considered a weaker notion of revenue monotonicity, namely, the optimal revenue w.r.t. the dominating distribution is weakly higher than that of the dominated distribution . The weaker version holds for arbitrary single parameter mechanism design problems. The main insight from Hart and Reny [17] on this topic is that even the weaker version of revenue monotonicity ceases to hold in the multi parameter setting, even with only one bidder. Note that the stronger notion in Theorem 3.1 directly implies the weaker one.

Subsequent work by Chen et al. [7] showed that the stronger notion no longer holds beyond the matroid setting. Nevertheless, they recovered an approximate version of strong revenue monotonicity which still suffices for proving sample complexity upper bounds. Whether an approximate version of weak/strong revenue monotonicity notion holds for multi parameter mechanism design problems is an interesting open question.

3.5 Concentration Inequality for Product Distributions

We prove the following concentration inequality, which is useful for showing that the revenue of a mechanism on a given product distribution is close to its revenue on the empirical product distribution, which is defined to be a product distribution whose components are uniform distributions over the corresponding sample values. Subsequent to the conference version, we found out that a very similar theorem was known due to Babichenko et al. [2]. The main difference is that we use Bernstein instead of Chernoff in the proof to get a better bound when the expectation of the random variable is much smaller than the maximum value in its support. We include the proof in Section 5 for completeness.

Theorem 3.2.

Let be an arbitrary measurable set, be an arbitrary function from to . Let be distributions over , and . Suppose . Let be i.i.d. samples from . Let be the uniform distribution over for each , and . Then, we have:

3.6 Organization of the Proofs

We begin with the proofs of the technical lemmas, i.e., Theorem 3.1 and Theorem 3.2, in Section 4 and Section 5 respectively. Eager readers may skip these two sections without any problems understanding the sample complexity analysis in the rest of the paper. The sample complexity bounds for single item auctions in the Myerson model are in Section 6, and the bounds for the signals model are in Section 7. The extensions to more general single parameter environments are in Section 8.

4 Proof of Strong Revenue Monotonicity

This section proves Theorem 3.1. The proof in this version of the paper is different from the one in the original conference version, which has a subtle bug. The new proof further allows us to handle general distributions (instead of those with discrete supports as in the original version) and the more general matroid constraint (instead of single-item auction as in the original version).

4.1 Ironed Virtual Value

We start with the formal definition of ironed virtual values, given the value distribution of a bidder. First, we define the quantile (w.r.t. ) of a value in the support of to be:

For continuous distributions, we have where is the cdf of distribution . It induces an inverse mapping from quantiles to values such that given any quantile :

Next, we define revenue curves. Let us start with the simpler case when the distribution is continuous. The revenue curve, in the quantile space, is a function:

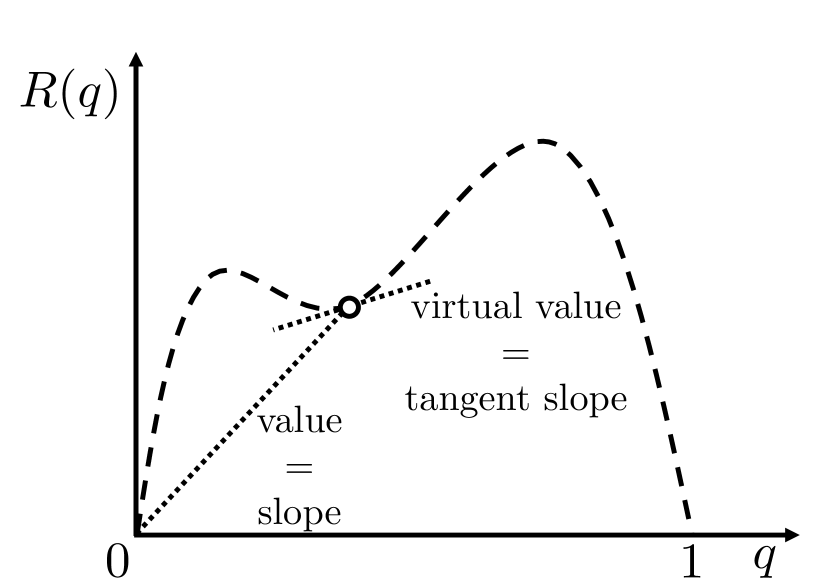

That is, equals the revenue obtained by setting a take-it-or-leave-it price such that the sale probability is equal to . Given any point on the revenue curve, the slope of the line connecting the point with the origin is equal to the value by definition. Further, it is known that the slop of the tangent line equals the corresponding virtual value when the distribution is continuous. See Figure 1(a) for an illustrative picture of the revenue curve.

Defining the revenue curve and virtual values for distributions with point masses is more subtle. To begin with, plot points for any value in the support and the corresponding sale probability . Note that if is not a point mass. However, there will be discontinuities in the plot that correspond to the point masses. Concretely, for any point mass with and , the curve is currently undefined on the semi-open interval ; extend the definition of the revenue curve by letting it be the straight segment connecting and on this semi-open interval. Note that can be interpreted as the expected revenue obtained by setting a take-it-or-leave-it price that randomizes between and appropriately such that the sale probability is equal to . Then, the virtual value of any value with quantile is the right derivative of the revenue curve at .

For example, consider a discrete distribution with support with probability masses . Let for any . Then, first plot the points , ; let for notational convenience. Note that . Connecting neighboring points, the revenue curve is defined to be the following when the quantile is between and :

The virtual value of is equal to:

This is consistent with the definition of virtual values for discrete distributions, e.g., by Elkind [11].

Following the notation in auction theory, let denote the virtual value of a given value . The next lemma follows by the above definition of virtual values.

Lemma 4.1.

For any quantile , we have:

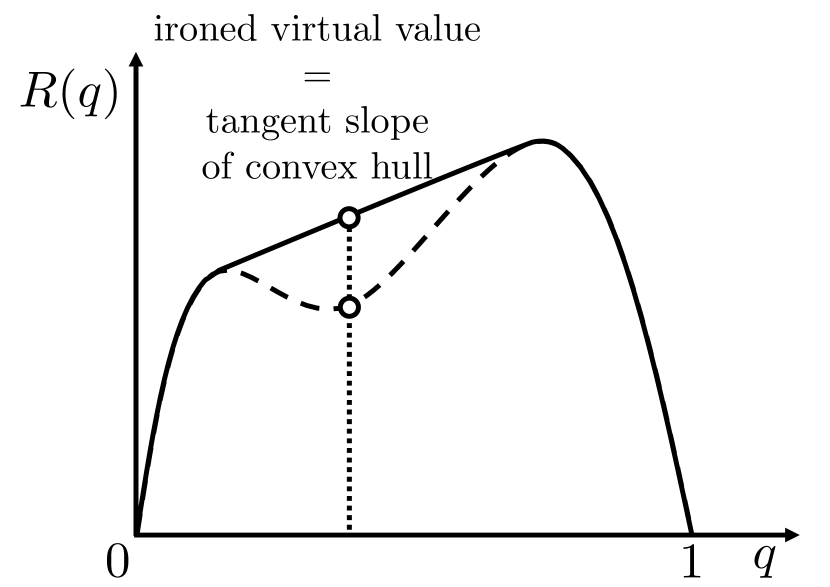

Finally, let be the convex hull of . can be viewed as the maximum revenue achievable via a randomized take-it-or-leave-it price, subject to having an overall sale-probability of . Then, the ironed virtual value of the value with quantile is equal to the slope of the tangent line w.r.t. . See Figure 1(b) for an illustrative picture.

4.2 Simplifications

We start with some simplifying treatments that are wlog. Recall that our goal is to show that an optimum auction for gets at least as much revenue when run on . Let be the optimal Myerson auction for . Let and denote the virtual values that correspond to a value w.r.t. distribution and , respectively, for any bidder . Given any value profile, picks the bidder with the highest ironed virtual value w.r.t. as the winner. We assume that breaks ties deterministically by the lexicographical order of bidders. We write to mean that either the virtual value of is strictly larger than that of , or they are equal and .

For each bidder , let denote the subset of values whose corresponding points on the revenue curve are on the convex hull. We may assume wlog that both and have support ; the reason is as follows. The ironed virtual value of bidder is the derivative of the convex hull of the revenue curve of , in the quantile space. We can interpret as rounding the value of each bidder down to the closest one in , and then using the virtual values w.r.t. the distributions of the rounded values to choose the winner. We do the same for values in the support of but not . With this treatment, is regular in the sense that for every bidder , every value in the support of is on the convex hull of its revenue curve and, thus, is also the ironed virtual value. Note that, however, may not be regular.

4.3 Failing Strategies

To build up the intuition and to motivate our approach, we continue with some brief discussions on how two seemingly natural strategies fail, even in the case of a single item.

Failing Strategy 1: Direct Comparison of Payments.

Suppose we realize the values of bidders as follows. First, draw a quantile profile such that each is i.i.d. from the uniform distribution over . Then, for every bidder , let denote the value that corresponds to quantile w.r.t. ; define similarly w.r.t. . Let and be the corresponding value profiles. Then, the expected revenues of w.r.t. and can be written as:

and

A naïve strategy is to show that for any quantile profile . This inequality does not hold in general because it is known that the optimal mechanism may involve price discrimination. It is possible that, for example, as bidder ’s value gets larger moving from to , she may become the winner even though her payment is still lower than what the original winner pays.

Failing Strategy 2: Amortization via Virtual Values.

An alternative approach is to amortize the gains in the quantile space using virtual values. Note that is also the ironed virtual value due to the aforementioned treatments, i.e., it is monotonically non-decreasing in . Note that similar claims do not hold for in general. Let denote the set of winners that picks when the value profiles is . By Myerson’s characterization [22], the expected revenues can be written as follows:

and

Then, one may try to show that the amortized gain is weakly higher in than in for any quantile profile , i.e.:

| (1) |

However, this inequality does not hold in general either, even in the special case of selling a single item, i.e., when is either empty or a singleton set for any value profile . If picks the same winner for and , inequality (1) may not hold because stochastic dominance does not imply dominance in terms of virtual values, in the quantile space, that is:

may not hold in general.

If picks different winners, e.g., it picks bidder when the value profile is , and picks bidder when the value profile is . Then, inequality (1) becomes:

However, the definition of indicates a different inequality that:

since it picks the winner with the highest virtual value w.r.t. , when the value profile is . Again, inequality (1) may not hold in general due to the subtle mismatches on both sides of the two inequalities.

4.4 Proof of Theorem 3.1

4.4.1 Our Amortization

We will design a more subtle amortization. Specifically, we will design non-negative amortized gain functions and for distributions and respectively, with the following properties.

-

(a)

The expected revenue is bounded by the expectation amortized gain for both distributions, in the respective directions:

(2) and

(3) -

(b)

For any quantile profile, and any common winner picked by the mechanism for both distributions, the amortized gain w.r.t. is weakly higher than that w.r.t. . That is, for any bidder , we have:

(4) -

(c)

For any bidder who is a winner only w.r.t. , and any bidder who is a winner only w.r.t. , such that replacing bidder with bidder in the set of winners w.r.t. is feasible, i.e., , we have that

We do not know how to do this directly; instead we do this in two steps. For any bidder who is a winner only w.r.t. , and any non-winner who could have been swapped with bidder while maintaining feasibility, i.e., , we have:

(5) For any bidder who is a winner only w.r.t. , we have:

(6)

Amortized Analysis.

Next, we present the proof of the theorem assuming the existence of such amortized gain functions and , deferring the construction of these functions to the next subsection. By property (a), to prove that , it suffices to show:

In fact, we will prove a stronger claim that the inequality holds for any given quantile profile , rather than only in expectation over the randomness of . That is, for any :

| (7) |

We use the well known exchange property of matroids to start from the winners in and move towards the winners in .

Lemma 4.2 (Exchange property, e.g., Schrijver [26], Corollary 39.12a).

For any of equal size, i.e., , there is a one-to-one mapping from and such that for any , we have:

We need to show one more thing, that the number of winners in is at least the number of winners in . This is fairly easy, and follows from the monotonicity of ironed virtual values, and the exchange property.

Lemma 4.3.

For any quantile profile , we have:

Proof.

Suppose not. Then, by the augmentation property of matroids, we get that there exists a bidder who is a winner only w.r.t. such that mechanism could have added bidder to the set of winners w.r.t. , i.e.:

Recall that is the optimal auction w.r.t. , which picks a feasible set of winners to allocate to to maximize the sum of their ironed virtual values. Here, and in the rest of the proof, ironed virtual values are evaluated according to distributions . The decision of not including bidder in the set of winners indicates that her ironed virtual value, for value , is negative.

However, by that , we have . Monotonicity of ironed virtual values implies that the ironed virtual value of is at least that of , which must be non-negative since mechanism chooses bidder when the value profile is . We have a contradiction. ∎

By Lemma 4.3, there are weakly more winners in than in . Let . Let be a subset of , obtained by removing some bidders in so that it has the same size as . Let be the mapping from to in Lemma 4.2. Then, the next lemma follows as a corollary of property (c).

Lemma 4.4.

For any , we have:

4.4.2 Construction of the Amortized Gain Functions

It remains to show that there are such non-negative amortized gain functions and with the aforementioned properties. We start with some notations and simplifications.

The first simplification relies on the notion of threshold quantile above which a bidder becomes a winner. For any bidder , and any quantile profile of the bidders other than , let denote the threshold quantile below which is the winner when is run on . That is:

Define similarly as the threshold quantile when is run on . That is:

Then, we may wlog let for any quantile of bidder that is below the threshold, since and thus, they are irrelevant to the properties that need to be satisfied. Similarly, we may wlog let for any . It remains to design and for quantile below the corresponding thresholds.

Property (a) is where the amortization happens: in particular, we only need to amortize over ’s own randomization, for any fixed profile of all other bidders. We formalize that below. We begin by rewriting the expected revenue of running on and respectively using the virtual values à la Myerson [22]:

and

To satisfy property (a), it suffices to ensure that for any bidder and any quantile profile of the other bidders, we have:

| (8) |

and

| (9) |

Construction of .

Construction of .

This part is the crux of the proof and needs to be further divided into two cases. Concretely, let us fix any bidder , and any quantile profile of the bidders other than . We will construct the amortized gain function for quantile profiles of the form for any to ensure the relevant inequalities in the properties. In the following discussions, let be the revenue curve, in the quantile space, w.r.t. distribution . Define similarly w.r.t. distribution . The cases depend on the order of the threshold quantiles for bidder in the two distributions given .

Case 1: .

This is the easy in which we just let be the virtual value. For any , let:

The relevant inequality for property (a), i.e., Eqn. (8), holds as follows:

| (definition of virtual values) | ||||

| () | ||||

| (definition of virtual values) | ||||

| (definition of ) |

The relevant inequality for property (b) is Eqn. (4) when , i.e.:

By our construction, it holds with equality.

We do not need to worry about property (c), since in this case we have and thus bidder is a winner in both and .

Case 2: .

We first give the geometric intuition behind the construction. Suppose we define as the slope of a curve that starts at the origin. We first reinterpret what the three properties mean in terms of this curve and the revenue curves and .

- Property (a):

-

The curve should meet the revenue curve at .

- Property (b):

-

The slope of the curve should be at least that of , in the interval .

- Property (c):

-

This corresponds to the interval . This property is hard to interpret geometrically, but a sufficient condition will be that the slope is at least the threshold value above which bidder is a winner in . We denote this threshold value by .

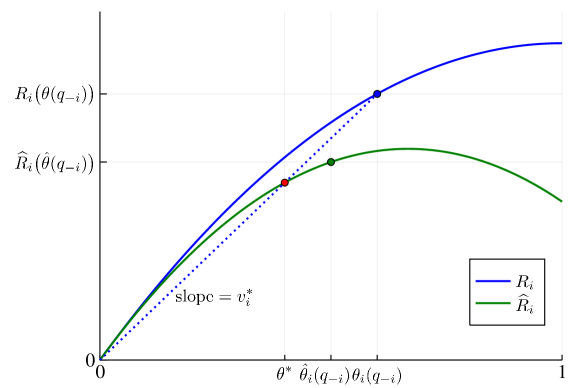

Refer to Figure 2 for an illustration. The value is the slope of the line joining the origin to the revenue curve at . The curve defining follows until it touches this line, and then follows this straight line until it touches . It is easy to verify that this curve satisfies the geometric interpretation of the 3 properties as described above. We now give a formal description of this construction, and complete the proof.

Let be , i.e., the threshold value that corresponds to the threshold quantile w.r.t. such that becomes the winner when its value is at least , when mechanism is run on , and when the other bidders quantile profile is . By its definition, we have:

Let denote the sale probability of w.r.t. .

By , we have . We further need the following technical lemma.

Lemma 4.5.

.

Proof.

Similarly, let be , i.e., the threshold value above which wins when is run on and when the other bidders’ quantile profile is . By its definition, we have that:

For any , by and the monotonicity of , we have that and, thus, . Therefore, we have that by their definitions, i.e., the threshold value above which wins against is weakly higher than that against , because the former is weakly larger coordinate-wise. The lemma follows since and are the quantiles of and in respectively. ∎

We now define the amortized gain function as follows.

The relevant inequality for property (a), i.e., Eqn. (8), holds with equality as follows:

| (definition of virtual values) | ||||

| (definition of ) | ||||

| (definition of ) | ||||

| (definition of virtual values) | ||||

5 Proof of Concentration Inequality for Product Distributions

In this section we prove Theorems 3.2. The following lemma follows by Bernstein inequality.

Lemma 5.1.

Let be i.i.d. samples from . Then, we have

We relate the random variables in Theorem 3.2 and Lemma 5.1 as follows. First, draw samples i.i.d. from for all , and draw permutations of independently and uniformly at random. Then, let be for all . We have the following properties which will be useful in the proof:

-

a)

are i.i.d. samples from over the randomness of both and .

-

b)

Fixed any (and, thus, ), for any , follows distribution over the randomness of . Different ’s are, however, correlated.

Next, we bound the difference between the expectation over the product empirical distribution and the true expectation . We have the following inequalities:

| (Property b: ) | ||||

| (Convexity of absolute value) | ||||

| (By ) | ||||

Hence, we get that:

| (10) |

It remains the bound the right hand side. By property a) and Lemma 5.1, we have:

Equivalently,

Thus, by Markov’s inequality,

| (11) |

6 Single-item Auctions in the Myerson Model

6.1 Finite and Bounded-support Distributions

In this subsection, consider the case that the support of the distributions is a finite subset for some and suppose we aim to an additive approximation up to a factor. We propose an algorithm for constructing an empirical Myerson auction (Algorithm 1) and present a meta analysis of its sample complexity upper bound. They will serve as important building blocks in the analysis of the other classes of distributions.

Concretely, we will show the following theorem, whose proof follows the standard concentration plus union bounds combo, using the concentration bound for product distributions introduced in Section 3.5, whose proof is in Section 5.

Theorem 6.1.

For any upper bound of the values , any finite support of the value distributions , any upper bound of the optimal revenue , and any additive error bound , Algorithm 1 takes samples and learns an empirical Myerson auction that gets an expected revenue of at least with probability at least if is at least:

Remark 6.1.

Importantly, all the parameters , , , and are used only in the analysis. The algorithm does not need to know them in advance.

Proof.

For any product distribution over , Myerson’s optimal auction picks the bidder with the largest non-negative ironed virtual value. As any tie-breaking rules give the same expected revenue, we assume wlog that the optimal auction breaks ties deterministically. Then, the auction is characterized by a mapping such that is the rank of bidder with value among all possible bidder-value pairs, and is the rank of having zero ironed virtual value. Given any value profile , Myerson’s optimal auction does not allocate the item to anyone if , and otherwise allocates the item to bidder . Hence, there are at most different Myerson’s auctions for different product distributions over . Let denote the auction that corresponds to such a mapping .

For any given , we apply Theorem 3.2 with being the revenue of when the values are , dividing it by so that , with , and with at least:

samples (for a sufficiently large constant inside the big- notation). Note that the expectation is the expected revenue of a mechanism, which is at most and, thus, by the definition of . We get the following inequalities (where the probability is over the randomness of the samples):

By union bound, we have that with probability at least , for any it holds that:

Since Algorithm 1 returns the optimal auction w.r.t. , it gets at least revenue in expectation on . ∎

6.2 Bounded-support Distributions: Additive Approximation

In this subsection, consider the case that the distributions have a bounded support for some . We seek to learn a mechanism that is optimal up to an additive loss in the expected revenue. We show the following theorem.

Theorem 6.2.

Suppose the value distributions have bounded supports in . Then, for any , there is an algorithm that takes samples and learns a mechanism with revenue at least with probability at least if is at least:

We will prove the theorem by reducing it to the finite-support case. To do so, we first introduce a technical lemma showing that a standard discretization of the value space decreases the optimal revenue by at most additively.

Lemma 6.3 (Additive discretization of the value space).

Given any product value distribution , and any , let be the distribution obtained by rounding the values from to the closest multiple of from below. Then, we have:

The lemma holds for any single parameter problem, replacing with on the right-hand-side.

Assume for simplicity of exposition that itself is a multiple of .

Proof.

We will prove the lemma by explicitly constructing a mechanism that gets expected revenue at least on distribution . Let be the optimal mechanism w.r.t. . We will assume wlog that breaks ties deterministically over bidders with equal ironed virtual values. Consider a mechanism for distribution with an allocation rule that proceeds as follows:

-

1.

Suppose the reported value profile is from .

-

2.

For any bidder , sample independently from conditioned on .

-

3.

Use the allocation of mechanism for values profile .

Suppose we fix the randomness used in step 2 of the above allocation rule. Then, note that is a - step function of every bidder ’s value fixing the other bidders’ values. Further, step maps values in the support of to values in the support of monotonically. Hence, the above allocation rule is a - step function of every bidder ’s value fixing the other bidders’ values. Therefore, we can make it a DSIC mechanism by using a payment rule that charges the winner the threshold value above which she is the winner. Since it is DSIC for every realization of its random bits, the overall mechanism is DSIC (in fact, uniformly truthful).

Next, we analyze the expected revenue of . We will do so by coupling two random variables, the revenue of over a valuation profile sampled from , and the revenue of over a valuation profile sampled from . In particular, we will couple the value profiles and , such that is the output of step 2 of the allocation rule of .

For such a pair of value profiles, by the definition of , the allocation of on is the same as that of on . Suppose bidder is the winner. Further, the payment of each mechanism is equal to the threshold value of above which bidder is a winner. By definition, the threshold value in is obtained by rounding the threshold value in down to the closet multiple of . Therefore, for any bidder who get an item, her payments in both mechanisms differ by no more than . So the lemma follows by that there are at most winners in any feasible allocation. ∎

By rounding the values to their closest multiples of from below, we reduce the problem to the finite-support case with support , which has size . As a result, we prove Theorem 6.2 with Algorithm 2.

Proof of Theorem 6.2.

Let denote the distribution obtained by rounding sample values from down to the closest multiple of . Since the output mechanism, denoted as , treats any value as the closest multiple of from below, running it on and gives the same revenue. That is,

By Theorem 6.1, we have that with probability at least :

Further, by Lemma 6.3, and that , we get that:

Putting together the above equations proves the lemma. ∎

6.3 Bounded-support Distributions: Multiplicative Bound

In this subsection, we consider the case that the value distributions have bounded supports in for some . We seek to learn a mechanism that is optimal up to a multiplicative factor in term of the expected revenue. We show the following theorem.

Theorem 6.4.

Suppose the value distributions have bounded supports in . Then, for any , there is an algorithm that takes samples and learns a mechanism with revenue at least with probability at least if is at least:

We will again prove the theorem by reducing it to the finite support case. First, we introduce a technical lemma showing that a standard discretization of the value space, tailored for an multiplicative approximation, decreases the optimal revenue by at most a multiplicative factor.

Lemma 6.5 (Multiplicative discretization of the value space).

Given any product value distribution , and any , let be the distribution obtained by rounding the values from down to the closest power of . Then, we have:

The lemma holds for any single parameter problem.

The proof is almost a verbatim of that of Lemma 6.3, replacing the additive discretization with a multiplicative one. We include it for completeness. Assume for simplicity of exposition that itself is a power of .

Proof.

Similar to the proof of Lemma 6.3, we will prove the lemma by explicitly constructing a mechanism that gets expected revenue at least on distribution . Let be the optimal mechanism w.r.t. . We will assume wlog that breaks ties deterministically over bidders with equal ironed virtual values. Consider a mechanism for distribution with an allocation rule that proceeds as follows:

-

1.

Suppose the reported value profile is from .

-

2.

For any , sample independently from conditioned on .

-

3.

Use the allocation of mechanism for values profile .

Suppose we fix the randomness used in step 2 of the above allocation rule. Then, note that is a - step function of every bidder ’s value fixing the other bidders’ values. Further, step maps values in the support of to values in the support of monotonically. Hence, the above allocation rule is a - step function of every bidder ’s value fixing the other bidders’ values. Therefore, we can make it a DSIC mechanism by using a payment rule that charges the winner the threshold value above which she is the winner. Since it is DSIC for every realization of its random bits, the overall mechanism is DSIC (in fact, uniformly truthful).

Next, we analyze the expected revenue of . Similar to the corresponding part in the proof of Lemma 6.3, we will do so by coupling two random variables, the revenue of over a valuation profile sampled from , and the revenue of over a valuation profile sampled from . In particular, we will couple the value profiles and , such that is the output of step 2 of the allocation rule of .

For such a pair of value profiles, by the definition of , the allocation of on is the same as that of on . Suppose bidder is the winner. Further, the payment of each mechanism is equal to the threshold value of above which bidder is a winner. By definition, the threshold value in is obtained by rounding the threshold value in down to the closet power of . Therefore, the payments of both mechanisms differ by no more than . So the lemma follows. ∎

By rounding the values to their closest powers of from below for some , we reduce the problem to the finite-support case with support , which has size . As a result, we prove Theorem 6.4 with Algorithm 3.

Proof of Theorem 6.4.

Let denote the distribution obtained by rounding sample values from down to the closest power of . Since the output mechanism, denoted as , treats any value as the closest power of from below, running it on and gives the same revenue. That is,

By Theorem 6.1, we have that with probability at least :

Further, by Lemma 6.5, and that , we get that:

Putting together the above equations proves the lemma. ∎

6.4 Regular Distributions

In this subsection, we show an upper bound on the sample complexity of learning the optimal auction in the Myerson model when the value distributions are regular. Given what we have shown for the bound-support distributions, the new challenge of this case is that the support of the distributions could be unbounded. The main technical ingredient that overcomes this challenge is to show that we can truncate the values down to a high enough finite quantity without losing too much revenue. This is captured in the following lemma, whose proof is deferred to Subsection 6.4.3.

Lemma 6.6.

For any product regular distribution , any , and any , let be the distributions obtained by truncating at , i.e., a sample from is obtained by first sampling from and then letting . Then, we have:

This lemma holds generally in the downward-closed setting.

Analysis Assuming is Given.

Let us first explain what the analysis looks like assuming that is known. Let with a sufficiently small constant inside the big- notation. Let be the distribution obtained by truncating values at as in Lemma 6.6. The lemma gives:

Let be the distribution obtained by first sampling from and then rounding values smaller than down to . Since a bidder with value less than cannot pay more than her value, we have:

Let be the distribution obtained by rounding samples from down to the closest power of . Lemma 6.5 gives:

By Theorem 6.1, with , , , and , running Algorithm 1 with samples from returns a mechanism that with high probability gets an expected revenue at least:

Finally, note that if we run on truncating and rounding values to get a value in the support of , the expected revenue is the same as we run on by the definition of . That is,

Putting together the sequence of equations and , for a sufficiently small constant , proves the desired sample complexity upper bound for regular value distributions.

Rest of the Subsection.

It is not difficult to see that it suffices to have an estimate of up to a constant factor in order to instantiate the above analysis of sample complexity upper bound. We will proceed with Subsection 6.4.1 which explains how to get a constant approximation of using a small number of samples from . Then, Subsection 6.4.2 will formally present the theorem statement, the algorithm, and the corresponding proof for the case of regular distributions. Finally, we prove the above technical lemma (Lemma 6.6) in Subsection 6.4.3.

6.4.1 Estimating the Optimal Revenue

Now we design an algorithm that estimates the optimal revenue w.r.t. a regular value distribution up to a constant factor using a small number of samples from it. To achieve this, we employ a bootstrapping approach that makes use of two families of simple mechanisms:

-

•

The first one considers having copies of the item and sell to each bidder separately.

-

•

The second one is running the VCG mechanism with two copies of each bidder, whose values are independently sampled.101010Another potential approach is to use VCG with monopoly reserves, which also gives similar guarantees.

-

-

Its optimal revenue is a -approximate of (Hartline and Roughgarden [18], Theorem 4.4).

-

-

We run these simpler mechanisms with samples from to find a constant approximation of optimal revenue using Algorithm 4, whose formal approximation guarantee is given in Lemma 6.8 below.

We will first prove the following straightforward lemma that bounds the approximation guarantee from the first stage of the above algorithm.

Lemma 6.7.

Suppose SRev is computed via Algorithm 4. Then, with probability , we have:

This lemma holds generally in the downward-closed setting.

Proof.

First of all, step 2 is estimating the expected revenue of the -guarded empirical pricing with , which gives a -approximation of the optimal revenue of selling only to a single bidder for each with probability at least (e.g., Huang et al. [19]). That is, we have:

Then, by the union bound, the above holds for all with probability at least .

Note that since ignoring all bidders other than and posting the monopoly price w.r.t. is a feasible mechanism for the case with bidders. Hence, we have:

On the other hand, equals the optimal revenue when the auctioneer has copies of the item, which is weakly highly than when she has only one copy. Therefore, we have:

∎

Now we are ready to analyze the approximation guarantee of the final output Apx given by Algorithm 4, and show that it is a constant approximation of with high probability.

Lemma 6.8.

Suppose Apx is computed via Algorithm 4. Then, with probability , we have:

This lemma holds up to the matroid setting.

Proof.

We will assume that the conclusion of Lemma 6.7 holds, which happens with probability at least . Next, we show that under this assumption, Apx satisfies the claimed approximation with probability at least . The lemma then follows by the union bound.

Let be the distribution obtained by first sampling from and then truncating values higher than down to as in step 4 of the algorithm. By Lemma 6.7 we know that . Then, by Lemma 6.6 (with ), truncating values at decreases the revenue by at most a factor of . That is, we have:

Further, the truncated distributions are also regular due to the followings. For any , the virtual value of in the truncated distribution is now , which is weakly higher than the virtual value in original distribution , the virtual value of any value remains unchanged by the definition of virtual values (e.g., for continuous value distributions, neither nor is affected by the truncation). Putting together we get that is still monotonically non-decreasing for all .

As a result, the expected revenue of running the VCG mechanism with two copies of each bidder with values from , denoted as , is a -approximation of the optimal revenue of (Hartline and Roughgarden [18], Theorem 4.4). That is, we have:

| (12) |

On the other hand, having two copies of each bidder at best doubles the optimal revenue. Hence, we have that:

| (13) |

Finally, the maximum value in the support of is

| (Lemma 6.7) | ||||

| (Eqn. (12)) |

which also upper bounds the revenue from each sample run in step 4 of the algorithm. In other words, the maximum revenue from a single sample run is at most times larger than the expected revenue of the VCG mechanism with two copies of each bidder. Therefore, with sample runs, Bernstein inequality shows that with probability at least , we have:

6.4.2 Sample Complexity Upper Bound

The final algorithm is essentially what we have sketched at the beginning of Section 6.4, replacing the precise value of with the constant approximation Apx obtained through Algorithm 4 in the previous subsection. This is formalized as Algorithm 5.

Theorem 6.9.

Suppose the value distribution is regular. Then, for any , Algorithm 5 takes samples and learns a mechanism with revenue at least with probability at least if is at least:

Proof.

Let be the distribution obtained by first sampling from and than rounding values larger than down to . Lemma 6.6 gives:

Let be the distribution obtained by first sampling from and then rounding values smaller than down to . Since a bidder with value less than cannot pay more than her value, we have:

Let be the distribution obtained by rounding samples from down to the closest power of . Lemma 6.5 gives:

By Theorem 6.1, with , , , and , and failure probability , running Algorithm 1 with at least:

samples from returns a mechanism that, with probability at least , gets an expected revenue at least:

Finally, note that if we run on rounding values down to the closest element of , effectively we are running on by the definition of . Hence, we have:

Putting together the sequence of equations and proves the desired sample complexity upper bound for regular value distributions. ∎

6.4.3 Proof of Lemma 6.6

Recall that we seek to prove the lemma not only for the single-item setting which is the focus of this section, but also more generally for an arbitrary problem in the downward-closed setting.

When there is only one bidder and, thus, we may assume wlog that there is a single item, the lemma is folklore as it follows by concavity of the revenue curves of regular distributions. What are the extra challenges with multiple bidders? If the bidders’ values are all below the truncation point , the virtual values are the same in both and and, thus, the revenue remains the same. If exactly one of the bidders’ value is larger than , the analysis is similar to the single bidder case. It remains to bound the revenue when more than one bidders’ values are larger than , in which case the competition among the bidders may give an extra edge to the untruncated distribution over the truncated one . The key observation is that, the condition of implies that truncations are so rare such that the difference in revenue from the third case can be charged to the revenue of from the second case. Below we formalize this intuition.

Truncations are Rare.

Let denote the quantile of value w.r.t. for any bidder . We abuse notation and let and denote the virtual value of the corresponding value and with quantile in and respectively. Then, we have:

First, observe the following straightforward bound of ’s.

Lemma 6.10.

For any bidder , we have:

Proof.

Note that we could have ignored all bidders other than and offer a take-it-or-leave-it price of to bidder . The resulting revenue would be . This must be at most . The lemma then follows by . ∎

We further show the following more refined bounds on ’s.

Lemma 6.11.

The probability that at least one buyer has value greater than or equal to is at most and is at least , i.e.,

Proof.

We first show the first inequality. Suppose we offer a take-it-or-leave-it price of to the bidders one by one in lexicographical order and give it to the first bidder who accepts the offer (if such a bidder exists). Then, the expected revenue equals the price multiplied by the probability that there is at least one bidder with value at least . The latter equals

Note that this expected revenue must be no larger than the optimal . The inequality then follows by .

Next, we turn to the second inequality. The probability that there is at least one bidder with value at least is lower bounded by the probability that there is exactly one bidder with value at least . That is, we have:

Further, note that for any bidder , we have:

Here, the last inequality is what we have shown in the first part of the proof. Therefore, the second inequality in the lemma follows. ∎

Charging Argument.

Note that both and are regular. In both cases, the revenue optimal auction is Myerson’s auction, which allocates to the bidder with the largest non-negative virtual value. Further, the revenue is the virtual welfare. Define to simplify the notations in the following arguments. We have:

and

We partition the quantile space into two parts, the area with at least one high value, i.e., , and the area with all low values, i.e., . We will account for their contributions to separately.

On the other hand, we will upper bound the optimal revenue w.r.t. by allowing it to choose two feasible sets of winners, one from the bidders whose values are at least , and the other from the bidders whose values are less than . Concretely, given a quantile vector , let:

denote the subset of bidders whose values are at least . Let:

denote the set of bidders whose values are less than . Then, we have:

It suffices to show the following inequalities:

| (14) |

and

| (15) |

Proof of Eqn. (14):

Note that for any bidder , whenever its quantile satisfies that , we have . Thus, for any quantile profile , we have:

On the other hand, the right-hand-side (omitting the factor) is upper bounded by:

Therefore, to show Eqn. (14), it suffices to show that for any bidder :

Let denote the revenue of a single-bidder auction with a reserve price that has quantile w.r.t. . The left-hand-side of the above inequality is the revenue of a single-bidder auction with reserve price w.r.t. , i.e., . The right-hand-side is the maximum revenue of a single-bidder auction with a reserve price at least , i.e., . Note that is regular, which implies that is a concave function over and . Thus, we have that . The inequality then follows by (Lemma 6.10).

Proof of Eqn. (15):

Note that for any , we have for all , and . So we can rewrite the left-hand-side of Eqn. (15) as follows:

Comparing the above integration with that in the right-hand-side of Eqn. (15), the only difference lies in the domain. The formal is over while the latter is over the entire quantile space . It remains to bound their difference by a factor of .

We will do so with a hybrid argument. Let . We will show that for any :

| (16) |

For any , any , consider and . We have that , and for any , . Thus, we get the following inequality:

which implies Eqn. (16).

Then, putting together Eqn. (16) for , we get that:

6.5 MHR Distributions

In this subsection, we show an upper bound on the sample complexity of learning a mechanism that is a -approximation when the value distribution is MHR. The algorithm is almost identical to that for regular distributions, except that we have a better tail bound due to the MHR assumption. In particular, we will make use of the following extreme value theorem by Cai and Daskalakis [6].

Lemma 6.12 (Cai and Daskalakis [6], Theorem 18).

For any MHR value distribution , any , any for a sufficiently large constant , let be the distribution obtained by first sampling from and then rounding values larger than down to . Then, we have that:

We present the formal definition of the algorithm in Algorithm 6. Both the algorithm and its analysis are almost verbatim to their counterparts for regular value distributions, differing only in the upper bound above which we truncate the values, and the corresponding parameters when we apply the base-case theorem (Theorem 6.1).

Theorem 6.13.

Suppose the value distribution is MHR. Then, for any , Algorithm 6 takes samples and learns a mechanism with revenue at least with probability at least if is at least:

Proof.

Let be the distribution obtained by first sampling from and than rounding values larger than down to . Lemma 6.12 gives:

Let be the distribution obtained by first sampling from and then rounding values smaller than down to . Since a bidder with value less than cannot pay more than her value, we have:

Let be the distribution obtained by rounding samples from down to the closest power of . Lemma 6.5 gives:

By Theorem 6.1, with , , , and , and failure probability , running Algorithm 1 with at least:

samples from returns a mechanism that, with probability at least , gets an expected revenue at least:

Finally, note that if we run on rounding values down to the closest element of , effectively we are running on by the definition of . Hence, we have:

Putting together the sequence of equations and proves the desired sample complexity upper bound for MHR value distributions. ∎

7 Signals Model

7.1 Single Bidder Upper Bound

In this subsection we present a proof of the upper bound for the single bidder case of the signals model, i.e., . In the special case of a single bidder, an auction is simply a posted price. The main challenge is the scarcity of samples with the same signal as the buyer (in fact, there might be none). The idea is to find an auxiliary distribution such that (1) we have enough samples from it to find a nearly optimal price for it, and (2) it is stochastically dominated by the buyer’s prior. Then, we can lower bound the revenue of the auction with the optimal revenue of the auxiliary distribution. To this end, we consider a number of signals in the samples that are just below the signal of the bidder, and use the mixture of the corresponding distributions as our auxiliary distribution. The price posted is the best price for the empirical distribution of values corresponding to these signals, guarded against using too few of these values. The algorithm is summarized in Algorithm 7.

Theorem 7.1.

The expected revenue of Algorithm 7 is a approximation in the signals model with samples from regular and -bounded distributions if is at least:

7.1.1 The Analysis in an Idealized World

Before we dive into the technical details of the actual analysis, let us first considered an idealized world assuming the followings:

-

1.

; and

-

2.

the signal is uniformly distributed over .