∎

Tel.: +549-0223-4752426 x 234

22email: ivandegano@mdp.edu.ar 33institutetext: S. Ferrando, Ryerson University 44institutetext: 350 Victoria St., Toronto, Canada

Tel.: 416-979-5000 x 7415

44email: ferrando@ryerson.ca 55institutetext: A. Gonzalez, Universidad Nacional de Mar del Plata 66institutetext: 3350 Funes St., Mar del Plata, Argentina

Tel.: +549-0223-4752426 x 234

66email: algonzal@mdp.edu.ar

Trajectory based models.

Evaluation of minmax price bounds.

Abstract

The paper studies sub and super-replication price bounds for contingent claims defined on general trajectory based market models. No prior probabilistic or topological assumptions are placed on the trajectory space, trading is assumed to take place at a finite number of occasions but not bounded in number nor necessarily equally spaced in time. For a given option, there exists an interval bounding the set of possible fair prices; such interval exists under more general conditions than the usual no-arbitrage requirement. The paper develops a backward recursive method to evaluate the option bounds; the global minmax optimization, defining the price interval, is reduced to a local minmax optimization via dynamic programming. Trajectory sets are introduced for which existing non-probabilistic markets models are nested as a particular case. Several examples are presented, the effect of the presence of arbitrage on the price bounds is illustrated.

1 Introduction

In an incomplete market model, the classical theory shows that, under no arbitrage assumptions, there exists an interval of fair prices. Such an interval is given by the sub and super-replication bounds introduced first in a diffusion setting in elKaroui (see follmer for a general discrete time formulation). The super-replication price bound of an European contingent claim equals the supremum of its expectation over the set of equivalent martingale measures (with an analogous characterization for sub-replication). For a discrete time setting, such dual formulation can be found in follmer and cutland (the second reference assumes a finite probability space).

It turns out that for a large class of stochastic models the fair price interval degenerates to absolute (i.e. model independent as in (merton )) no-arbitrage bounds. This is shown in eberlein for continuous time and in carassus1 for discrete time. These results rely on the assumption of an unbounded range and a non atomic distribution for the increments of the modeling stochastic processes (i.e. the underlying). Reference carassus2 studies a class of stochastic models for which the fair price interval does not trivialize to absolute bounds. A popular alternative, in order to reduce the size of the fair price interval, is to allow trading with liquid options in order to better approximate an illiquid derivative. Presumably, this is a way to acknowledge the limitations of the original model proposed for the underlying in order to account for the degrees of freedom influencing the derivative’s market price.

There is uncertainty in the modelling of any assumed probabilistic distribution as well as in the specification of the support of the modelling stochastic process. An example of such uncertainty is the modelling of crashes (desmettre ) where, the number, timing and size of a downwards stock change (a crash) is treated without probabilistic assumptions. An example requiring a set of non equivalent measures is provided by the uncertain volatility model (avellaneda ). A related development is given by sublinear expectations and their associated stochastic calculus (peng ). In order to accommodate such uncertainties, our general setting requires no prior stochastic assumptions. Recent and related literature also develops results that weaken, or eliminate entirely, stochastic assumptions; as examples, we mention robust versions of FTAP in riedel , burzoni , burzoni2 and cheridito2 .

The present paper develops computational results of fair price bounds for a large class of non probabilistic models built around a trajectory space. The general framework in discrete time is developed in deganoI where detailed justifications and connections with standard stochastic models can be found. The setting grew as a generalization of a model proposed in BJN (see also the book exposition in rebonato ). A related reference is given by roorda . We show in examples that the resulting fair price intervals are much narrower that the ones given by the absolute bounds and that the task of modeling trajectory sets directly, as opposed to firstly prescribing a probability distribution and then obtaining its support as a by product, is a worthwhile modeling enterprise. Realistic models and preliminary comparison with market data can be found in fleck . A basic result in deganoI is the proof of existence of a fair price interval despite the presence of a certain kind of arbitrage. We show numerically the effect of such arbitrage on the price bounds.

It is natural to inquire about the differences between the fair price intervals for stochastic and trajectory based models. A main technical difference is that the superhedging inequalities in a stochastic setting are requested to hold a.e., this implies the need to evaluate essential infima and suprema which are, in general, computationally intractable. When non equivalent measures are involved there is the need to use polar sets. Literature providing a general approach to evaluate sub and super-replication bounds in a general discrete time setting is scarce, we are only aware of carassus1 . Our setting and results do not require to deal with sets of measure zero and hence complications of that nature are avoided from the outset. We establish general results that allow the evaluation of fair price bounds for a large class of trajectory based models. We restrict our attention to a single tradable asset but expect that the results obtained can be extended to higher dimensions without essential complications. For comparison purposes, we mention the reference kahale that also works in a model independent setting, in particular no apriori fixed measure is assumed, and allows for static and dynamic hedging in the super-replication portfolio.

The financial context is of a riskless bond with zero interest rates and one risky asset. We consider a financial discrete market , elements are trajectories. Coordinates are the values of the tradable underlying while the variable , possibly vector valued, represents values of other observable financial variables used to define the trajectory set (the coordinate is described later). are functions representing the trading strategies. The general class of models included in the formalism allow for certain arbitrage opportunities while, at the same time, providing a fair price interval for options without introducing logical or practical inconsistencies.

We present effective and rigorous results that allow to evaluate the super- and sub-replication pricing interval given by a minmax optimization in deganoI (see Definition 2.2 in the present paper). The resulting algorithm is a dynamic programming based optimization applicable to general trajectory sets . To efficiently deal with the resulting local minmax optimization, we propose a geometric procedure consisting in computing the convex hull of a set of future stock values (see Section 4). This represents the so called convex hull algorithm (introduced informally in BJN ) but here made rigurous and extended to a general setting. In contrast to available methods evaluating the convex hull (andrew , for example) we isolate a relevant sector of the convex hull containing the required solution. Moreover, our approach works for the case of an infinite number of points, its end effect is to reduce the local minmax to a single maximization. This last step is achieved by parametrizing the hedging parameter by a geometric ratio and represents the essence of the convex hull algorithm. The hedging ratio is a discretized version of the delta hedging term appearing in the stochastic setting and gives an optimal hedging. We provide a formal analysis of the procedure in a general setting.

The resulting algorithm allows to evaluate fair price bounds for a realistic class of options and a general class of trajectory sets. We prove that, for a class of models and options with convex payoff, the super-replication price is equal to the replication price in a Cox-Ross-Rubinstein model (see cox ): this result has been already obtained in roorda in a non probabilistic fixed time framework and carassus2 in a probabilistic context. Also, we extend a model from BJN (see also rebonato ) by allowing for trajectory dependent quadratic variation. Finally, relevant numerical examples illustrate the viability of the approach and some of the characteristics of the models studied.

The paper is organized as follows, Section 2 provides the general framework of the paper and describes notation and relevant results to be used in the remaining of the paper. That section introduces the notion of -neutral and the fair price interval. Section 3 establishes, under appropriate conditions, how to recover the global minmax optimization defining the bound prices by means of an iterative dynamic programming procedure. Section 4 describes how the iterative procedure described in Section 3 can actually be implemented by an efficient, geometric based method which we call convex hull algorithm. Section 5 describes some simple models as well as a class of models allowing trajectory dependent values of (sampled) quadratic variation. For this last case, we describe in Section 6 a data structure supporting the implementation of the models. Finally, Section 7 concludes by providing a perspective on the paper as well as some speculation on possible extensions. Appendices contain complementary and technical results.

2 General framework

Usually, financial discrete markets fixes a finite partition of the time interval where transactions are carried out. The index refers to time between and . For the sake of flexibility and generality, trajectories , are of the form where belongs to abstract sets from which we only require to have defined an equality relationship. Such coordinates are referred to as additional sources of uncertainty (analogously to the case of an augmented filtration containing the canonical filtration). In financial terms, the quantities are considered to be observable. This framework allows the investor to rebalance the portfolio as a result of an arbitrary market event, for example, the quadratic variation reached a certain value. So, time dependent trajectories are mapped to a space which depends on the variable which, presumably, better jointly constraints the sequence of pairs . As we will price options expiring with a finite time horizon, we need an extra information indicating when a trajectory has reached the final time . We denote this trajectory coordinate by . The introduction of is important to the calculation of the fair price interval as the generality of the setting does not necessarily require that the coordinate carries any explicit time information (see Section 5 for several examples). The coordinate could have been formally incorporated into but, for clarity, we decided not to do so.

We reproduce some needed definitions from deganoI which should be consulted for further details.

Definition 1 (Trajectory Set)

Given the real numbers and , a set of (discrete) trajectories is a subset of the following set

where and are families of subsets of and . Elements are called trajectories.

We remark that if and are two trajectories, could take place in a different time than , although .

For we will use the notation for and define to be the projection function over the third coordinate of , that is . The following conditional spaces will play a key role. Let , for such that set:

Notice and that if , then . Whenever convenient, the tuple will be referred generically as a node.

A portfolio in our model will be a function over the set of trajectories as in deganoI , but we have modified slightly the non anticipative condition to accommodate the variable .

Definition 2 (Portfolio Set)

A portfolio is a sequence of (pairs of) functions with .

-

•

A portfolio is said to be admissible for if for each there exists a nonnegative integer such that for all and .

-

•

A portfolio is said to be self-financing at if for all ,

(2.1) -

•

A portfolio is called non-anticipative if for all , satisfying and for all with , it then follows that .

Given and a self-financing portfolio , the portfolio value defined by is equal to

during the period for . Of course, . Clearly, to specify self-financing portfolios, it is enough to provide sequences of non-anticipative functions and an associated real number .

As suggested above, the non-anticipative condition is slightly different to Definition 2 in deganoI ; the new condition is more general and it is useful in the setting of the present work. If and , we could alter the condition to to . The condition using is more general and it incorporates investors’ information. For each strategy the investor chooses a stage to liquidate the portfolio with respect to the trajectory taking into account the information of the market or merely his intuition. This selection could be different for a trajectory which is equal to . As a special case, in Section 3, we will impose for all .

A trajectory based discrete market (or trajectory market for short) is defined by where elements are admissible, non-anticipative and self-financing at each . The models are discrete in the sense that we index potential portfolio rebalances by integer numbers. Otherwise, stock charts and investment amounts can take values in general subsets of the real numbers and time can flow continuously. The zero portfolio is assumed to belong to and we take .

As indicated, some of the above definitions involve minor modifications from material in deganoI but most algebraic manipulations in that reference only involve the first coordinate (in the triples ). This remark can be used to show that the results we will rely upon from deganoI are valid in the setting of the current paper.

The following notion of discrete bounded market will be needed in several instances later in the paper.

Definition 3 (-Bounded Market)

A market is called -bounded if there exists a constant so that:

We refer to as bounded when reference to is immaterial.

We use the following definition of no-arbitrage market.

Definition 4 (Arbitrage-Free Market)

Given a discrete market , we will call an arbitrage strategy if:

-

•

, .

-

•

satisfying .

We will say is arbitrage-free if contains no arbitrage strategies.

Let denote a general function, from time to time, we will refer to such function informally as the derivative or payoff function. See Appendix A for general conditions on that guarantee finiteness of the quantities introduced below.

Definition 5 (Conditional Minmax Bounds)

Given a discrete market , and such that . Let a function defined on , define

| (2.2) |

Also define . Since and depend on only through , we adopt the notation and respectively. These quantities are called price bounds.

The price bounds can be recast in a more familiar way:

We know from financial stochastic models, that there exists an arbitrage-free price interval for the derivative if the market does not contain arbitrage strategies. In our context, the free arbitrage condition is replaced by the notion of a -neutral market that plays a key role.

Definition 6 (-Neutral Market)

The market is conditionally -neutral at node if

For , we will just refer to as -neutral.

The notion of -neutral market, taken from deganoI , was originally introduced in BJN and was considered equivalent to arbitrage-free in their context. In our general setting, it is only a necessary condition for a discrete market to be arbitrage-free (deganoI, , Corollary 1) while simultaneously allowing for arbitrage opportunities and a well defined theory of option pricing. -neutrality is key to obtain a well defined fair price interval. Theorem 2.1 is stated for a bounded market and assumed closed under addition. This is done to avoid introducing further notions, the result holds in more generality as can be seen in deganoI .

Theorem 2.1 (Price Interval)

Consider a bounded discrete market and a function defined on ; fix and . If is closed under addition and is conditionally -neutral, then

In particular

Proof

The result follows from the same calculations as in (deganoI, , Theorem 1). ∎

Under the assumption that , we will call the price interval of relative to . Appendix A, provides conditions for the boundedness of and .

The notion of attainability is basic in option pricing.

Definition 7

Given a discrete market , a function is called attainable if there exist such that

In stochastic frameworks there exists a unique fair price for an attainable option. The following analogue result holds in the present setting.

Corollary 1

Consider a discrete market , , and a function on and assume the conditions of Theorem 2.1. If is attainable then .

Proof

The proof is given in (deganoI, , Corollary 6). ∎

2.1 Global, Conditional and Local Concepts

Given the central role of -neutrality in our framework, it is imperative to find simple to check conditions guaranteeing a market to be -neutral. Definition 8 below introduces two basic concepts towards that goal: a local, and portfolio independent, analogue on of the -neutral property of and a strengthening of this notion representing the local analogue of the arbitrage free property.

Definition 8 (-Neutral & Arbitrage-Free Nodes)

Given a trajectory space and a node :

-

•

is called a -neutral node if

(2.3) -

•

is called an arbitrage-free node if

(2.4) or

(2.5)

is called locally -neutral if (2.3) holds at each node . is said to be locally arbitrage-free if either (2.4) or (2.5) hold at each node . If just (2.4) holds at each node, it is said that satisfies the up-down property. A node that satisfies (2.4) will be called an up-down node, and a node satisfying (2.5) will be called a flat node. A node that is -neutral but that is not an arbitrage-free node, will be called an arbitrage node.

The next Proposition gives local conditions ensuring that a discrete market is conditionally -neutral. As already pointed out, only the first coordinate (in the triples ) appear in most algebraic manipulations; therefore, the following results from deganoI hold in our setting.

Proposition 1

3 Dynamic Minmax Bounds

Arguably, attempting a direct evaluation of the minmax optimization required in (2.2) and in related expressions, is a daunting task. Moreover, the minmax formulation of the problem gives no clues on how to construct the hedging values , for a given payoff , by means of the unfolding path values

Consider next another pair of numbers namely and . These numbers are obtained through a dynamic, or iterative, definition each instance involving a local minmax optimization. Using these definitions we provide conditions under which the global and the iterated definitions coincide.

A special case of the iterative construction was introduced informally in BJN (see also kolokoltsov and roorda ) for a specific discrete market model. Here we formalize the validity of the approach in such a way that becomes available in a more general class of models and at the same time indicating the differences with the global minmax approach. The references bertsekas and bertsekasAndShreves provide a dynamic programming version of a global minmax optimization. Our approach differs as we make use of specific hypothesis present in our setting.

Markets will be assumed to be bounded and that all portfolios are liquidated on the expiration time ; that is, for each , . Further restrictions on will be introduced as needed.

The following inductive definition gives the basic dynamic programming formulation to compute .

Definition 9 (Dynamic Bounds)

Consider an -bounded, discrete market ; for a given function defined on , any , and set

| (3.1) |

Also define .

Remark 1

-

1.

Since and depend on only through , we adopt the notation and , respectively.

-

2.

Note that in Definition 9, for all .

The next remark shows that whenever is a stopping time, in the sense of Definition 15 in Appendix A, the dynamic bounds depend only on the history of the trajectory.

Remark 2

Assume is a stopping time and fix . Let and be such that for all . If , then and it follows by definition that . If since is stopping time, belongs to . Consequently, and

Therefore for all such that for all and .

For any and , we let to be the set of portfolio values at node , in other words

| (3.2) |

Thus, by item in Remark 1, we can rewrite the expression in (3.1) for ,

| (3.3) |

As we mentioned earlier, one of the purpose is to compare the global bound with the dynamic bound . Without any assumptions, we have the following general relationship.

Theorem 3.1

For any function defined on a discrete -bounded market and , the following inequality holds:

| (3.4) |

for all such that . Furthermore is also valid.

Proof

We proceed by backward induction on . For and with , all satisfy . Then, we have from (2.2) and Definition 9 that

Let us now assume that (3.4) holds for and consider a node with . Fix , for all with we have

| (3.5) |

since for all . Consider now with . Then, by inductive hypothesis,

Therefore, for ,

| (3.6) | |||||

Finally, from (3.5) and (3.6) it follows that

and since was taken to be arbitrary (3.4) follows. ∎

The next corollary, being a consequence of Proposition 1 and Theorem 3.1, represents the dynamic analogue of the -neutral condition,

Corollary 2

Let a discrete -bounded market model and a function defined on . If satisfies the local -neutral property, then for any and :

-

1.

.

-

2.

.

Proof

For we proceed by induction backwards, since

this is so by definition as for any , . Assume , for some and any . For fixed , if then or . On the other hand, if , since satisfies the local -neutral property at , for any

Thus

and then .

Continuing the analogy between global and dynamic bounds, we obtain an analogue of Theorem 2.1. First we need the following lemma.

Lemma 1

Let an -bounded discrete market and assume is closed under addition. Set and . Assume and are real valued functions defined on then,

| (3.7) |

Proof

We proceed by backward induction; consider first , if ,

If

Assume (3.7) holds for some and any . If then, as before, we have

Let and elements of so, , then if we have

Therefore, since and are generic elements of , it follows that

∎

Theorem 3.2

Consider an -bounded discrete market , a function defined on and fixed. If satisfies the local -neutral property and is closed under addition, then

| (3.8) |

The next Corollary shows that the dynamic and global bounds coincide for an attainable .

Corollary 3

Consider an -bounded discrete market , fixed and with . Let a function on and assume is locally -neutral and is closed under addition. If is attainable with portfolio and , then

Proof

3.1 Full Set of Portfolios

We are interested in obtaining the reverse of inequality (3.4) when is not attainable. To achieve that goal, it will be necessary to introduce some conditions on the set of portfolios, as well as other conditions, that imply equality in the inequality (3.4) and also lead to an efficient method to compute the dynamic bounds. Results in bertsekas suggest that having all possible portfolios may lead to establishing the desired equality; this motivates the definition of Full set of portfolios.

Definition 10

Let , a function is said to be -non-anticipative if for each satisfying and , for all , it then follows that .

Definition 11 (FULL Set of Portfolios)

Given a discrete market , consider , , and range set,

We will say that is FULL, if the set of functions with domain and range , which are -non-anticipative coincides, for any such and , with the set of functions where .

Observe that for , which justifies the notation . A particular, but convenient possibility, is the case when , for any , and .

Theorem 3.3 below shows that equality in (3.4) holds for a bounded market with a FULL portfolio set. The latter is natural in the sense that any of the values , taken by a portfolio at a rebalancing instance for some , should also be taken at any if . This implies that there exists such that . Actually, any set of portfolios can be extended to a set which is FULL as we explain next.

For and a -non-anticipative function, define

we show next that is non-anticipative. Let such that and for all with . Assume first . It is not possible that, for example, if , then and which is a contradiction. Then, . Since is -non-anticipative, it follows

Finally, the case is trivial because .

Theorem 3.3

For a general -bounded market , where is FULL, and for a given function defined on , we have

| (3.9) |

Proof

Because of Theorem 3.1 we only need to prove the inequality,

| (3.10) |

We proceed by induction on . For , for all we have . Then, from (2.2) and Definition 9,

Let us now assume that (3.10) holds for every -bounded discrete market model and consider an -bounded one, . Fix , and let such that . We can then apply Lemma 3 and it follows that is an -bounded market and where , , , are introduced in Definition 18 (this definition and lemma are located in Appendix B). Then, by the inductive hypothesis,

Thus, we can assume that , and consequently for , . Fix , then there exists , such that

Therefore,

| (3.11) |

Since is FULL, there exist such that, and for any

the functions are well defined since the family is a partition of . From (3.11) it follows that

| (3.12) |

Assume now with , then

since for all . Therefore

| (3.13) |

Finally from (3.12) and (3.13) it follows that

and then

Since was taken arbitrarily, (3.10) follows. ∎

3.2 u-Complete Set of Portfolios

We introduce another condition that allows to derive the equality . Most of the proofs and some required new notation for this section are provided in Appendix B.2.

Definition 12 (-Complete Market)

We will say that an -bounded discrete market is u-complete with respect to a real function defined on , if for any , and , there exists verifying

Theorem 3.4

If is an -bounded discrete market u-complete with respect to a given function defined on , then

Proof

As in the proof of Theorem 3.3 the required equality for is clear, we complete the proof by induction on . Assume is an -bounded discrete market which is u-complete, then by Lemma 5, item , in Appendix B.2, is -bounded and u-complete. Thus, resorting now to item of Lemma 5 and the inductive hypothesis,

By u-completeness, for any there exists such that

If ,

and if , , since . In any case

The reverse inequality follows from Proposition 3.1. ∎

Considered together, Propositions 2 and 3 below provide practical and useful hypothesis for an application of Theorem 3.4 above.

Proposition 2

Consider an -bounded discrete market and a node with . Assume one of the hypothesis below hold:

-

1.

is a compact subset of ,

-

2.

satisfies the up-down property (as per Definition 8) at node and .

Then, there exists , verifying that

| (3.14) |

Moreover, in the case , there exists such that .

Proof

Define , by

assuming that for all . Assume first that hypothesis above holds, since for any , the functions given by are affine, then its supremum is lower semicontinuous and convex. If is compact, by lower semicontinuity, there exists verifying . The proof for the case when hypothesis holds is provided in Appendix B.2. ∎

Notice that for the case when is a stopping time, and then, the left side of (3.14) is .

Proposition 3

Proof

See Appendix B.2. ∎

4 Convex Envelope for Dynamic Minimax Bounds

This section presents a rigorous method to calculate the dynamic bounds introduced in the previous section. In what follows, we will assume that the dynamic bounds are finite, this, for example, follows by an application of Theorem 3.1 or under the assumptions of Proposition 7 in Appendix A.

We will consider an -bounded discrete market (as per Definition 3). For , and we are going to give a geometric procedure, originally introduced in BJN for a specific example, in order to compute the dynamic bounds. For an arbitrary, but momentarily fixed, , set

i.e. the line in the plane, through the point with slope . Thus,

is the intersection of with the vertical straight line . Therefore, for each fixed , with some abuse of language

is the largest of the ordinates of the points of intersection between the straight lines and . Then becomes the lowest value of these largest intersections.

To complete the geometric procedure, assume for and that,

| (4.1) |

These sets are nonempty if, for example, the node is -neutral and there exist a trajectory such that or is an up-down node. For and denote by the slope of the straight line in the plane through the points and :

Theorem 4.1 below will show that

| (4.2) |

that is, , is the largest intersection of the referred lines with the vertical line .

Remark 3

-

1.

For any and

-

2.

The sets defined on (4.1) can also be defined in an alternative way interchanging the strict inequality, namely,

Proposition 4

Let be an -bounded discrete market. Then, for all and such that the node is a -neutral node,

Proof

We consider first the case . Let , then there is and such that

For such that ,

On the other hand, if , observing that by Remark 3,

Then

for all and for all . Therefore

Assume now . Then, for an arbitrary constant there exist and such that

A similar reasoning as above shows that for all . Therefore ∎

The next Theorem, which requires extra assumptions, gives an easier way to solve the optimization problem for the case while allowing for a more efficient algorithm. We remark that the assumption is a convenient way of guaranteeing .

Theorem 4.1

Let be an -bounded discrete market. If for any assume at least one the two following conditions for below hold,

-

1.

for some and .

-

2.

For any , ( and may depend on ).

Then,

Proof

It is enough to prove as the reverse inequality follows immediately from Proposition 4. We need only to consider the case when . Let , then there exist and such that

Observe that, in case , the above equation holds for and that appear in the statement in case . Also, since

there exists such that

Consider first the case when the hypothesis holds. If , one should have

otherwise which leads to the contradiction Therefore,

On the other hand, if , in a similar way results

Thus

Then, the proof for the case when hypothesis applies is complete.

In the case when hypothesis holds, assume first that and define . We are going to show, by contradiction, that

| (4.3) |

Towards this end assume

then

which leads to

The latter is a contradiction with the definition of . Then, since (4.3) holds,

now, since , it follows

While if , in a similar way results

for . Since , it follows from (4)

Then, the proof for the case when hypothesis applies is complete. ∎

Below we obtain some simplifications that apply to arbitrage -neutral nodes, towards this end, we refine Definition 8.

Definition 13

Consider a discrete market , and a -neutral node .

-

1.

We call a positive arbitrage node if

-

2.

We call a negative arbitrage node if

-

3.

We call a flat arbitrage node if

Observe that in a negative arbitrage node

while in a positive arbitrage node

Corollary 4

Let be an -bounded discrete market and assume the hypothesis of Theorem 4.1 item holds. For any node , , which is either a negative arbitrage node or a positive arbitrage node and is nonempty, it holds that

5 Examples: Trajectory Sets Via Another Source of Uncertainty

This section provides examples of trajectory sets defined by means of an additional source of uncertainty, denoted by , besides the stock. A general class of models and a discretized version of them are developed as well as concrete examples: the classical binomial and trinomial models and a model based on sampled quadratic variation.

5.1 Interval Markets

One should not develop the wrong impression that there is a small possible collection of models supported by the formalism described in the paper, on the contrary, the approach allows for trajectory sets that could be constructed from historical data, random samples from large collection of trajectories, etc. We refer to deganoI where trajectory sets are constructed by sampling paths of continuous time martingales and to fleck where, the so called, operational models are introduced and compared to market data.

The general principle guiding the constructions presented in this section is to isolate an observable quantity (representing a variable of interest) and proceed to define a trajectory space by imposing constraints relating the trajectories and a free variable representing this observable. In some cases, this process allows to impose natural constraints that follow from the discrete nature of the financial transactions. In the present examples, for simplicity, is chosen to be one dimensional and in applications is meant to be associated to the values taken by an observable quantity which unfolds along the stock chart . This latter quantity could unfold in continuous time and its future values be influenced by a source of uncertainty encoded in .

There is no essential result in our paper that requires , but, doing so makes it easier to connect with the usual models. The definition below assumes given: , , and sets and .

Definition 14

We will say that a trajectory set is an interval trajectory set if for real numbers and and a subset each verifies:

-

1.

for all ,

-

2.

for all

-

3.

.

For a set of portfolios , we set and call an interval market.

Given an interval trajectory set, recall that if we have two trajectories such that for all , it does not follow that . In particular, it could be the case that and and, therefore, and .

Remark 4

We can consider the special case and for an . Then, condition in the above Definition could equally be replaced by

we return to this case later.

An interval trajectory set , as characterized above, does not need to be, in general, the set of all trajectories satisfying the listed constraints in Definition 14. Interval trajectory sets can be used to model the unfolding of a data chart by mapping , one index at a time (i.e. as the chart unfolds), to its closest path . Here is an observable quantity that changes as the path unfolds; it can represent any variable of interest such as number or volume of transactions, time, quadratic variation, etc. In the context of an option contract expiring at time , will be a possible value being taken by . The introduction of as an independent variable allows to widen the scope of applicability of the model given by Definition 14 and it allows to incorporate arbitrage -neutral nodes (see Section 6.2.1).

Specific instances of interval sets or their finite versions (that we present below) will in fact impose further constraints on admissible trajectories. Once these further specifications are established, the resulting trajectory sets are defined in a combinatorial way i.e. by allowing membership to to all possible satisfying the constraints. This way of defining trajectory sets will make it easy to check if the local properties of -neutral or up-down are satisfied. For example, assume an interval model such that for all , for all and fix a node . Clearly, there exists the possibility of choosing trajectories such that , and respectively, so any node is up-down, and in that case the market results locally arbitrage-free (see Definition 8).

The figure below illustrates a typical step of a trajectory in an interval market.

The next two subsections provide concrete examples of interval markets and some of their properties. At first, we do not assume that the interval markets contain all the trajectories satisfying the constrains.

5.1.1 Fixed Time Partition

Consider a fixed time partition , that is, for the time interval , we fix being the only times at which a portfolio could be rebalanced. Set for all , then for all . Also, since the option expires at , we need to impose . Therefore a trajectory , under the above restriction, has the form .

Remark 5

For any portfolio set , the discrete market with under the above constrains is an -bounded discrete market. Note that in the general formalism the trajectories are infinite sequences of real numbers, as is an -bounded market, it is inconsequential to define the values of for .

The condition for all implies that . Then, in order to define a subset of in the terms of Definition 14, the set only must contain the element , namely . Also, we define , and then condition in Definition 14 holds. Finally, given , we denote by a subset of satisfying the remaining conditions Definition 14 for and the set . For any portfolio set , we will call the associated market a fixed time interval market.

Note that if for each node condition (4.1) holds, then is locally -neutral, independently of the intermediate values between and , and then, the associated market is -neutral. Therefore, by Theorem 2.1, is a fair price interval for the option and the bounds can be evaluated with the methods developed in the paper.

For the next result we need to define a particular kind of derivative in general markets. Indeed an European option defined on a trajectory set will be called convex if its payoff function is given by a convex real variable function as follows: for any . The next proposition shows that, in an interval market, the dynamic bounds for a convex European option are convex. This result is proven in roorda , we provide an alternative proof using Theorem 4.1.

Notice that the parameters and appearing in the next Proposition could depend on .

Proposition 5

Let . Consider a fixed time interval market . Let be the payoff function of an European derivative.

-

1.

Assume that is convex and for all and there exists such that and . Then, the dynamic bounds are convex and given by

(5.1) -

2.

Assume that is concave and that for all and condition (4.1) holds and there exists such that . Then, the dynamic bounds are concave and given by

Proof

Let ; since for any and convex,

Similarly, since for any and convex, it follows

Then by Lemma C.1 in Appendix C,

for all and . Therefore, hypothesis of Theorem 4.1 holds and so,

Since the property of convexity is preserved under scaling and under taking positive linear combinations, it is seen from the above that is convex and only depends on the value of . We proceed now by backward induction; let and suppose that is convex and given by (5.1). Then, with the same calculations that we use for the case , we can prove that is convex and given by (5.1) for all . This concludes the proof of (5.1).

Consider now the statement and assumptions in the case of our theorem and take . Since is concave, it follows that

for all and . In particular

Therefore, hypothesis of Theorem 4.1 holds, and then . Furthermore, is concave. Finally, by backward induction we obtain the desired result. ∎

The standard binomial tree model presented in cox is a particular situation of fixed time interval market. In a typical node of this model, the value of can only be or for each .

Binomial models are important because they can be used to approximate continuous time models by letting the time step tend to zero. The next Proposition shows that for a binomial model coincides with the Cox-Ross-Rubinstein price of the derivative. This can be seen to be a special case of the general result ((deganoI, , Theorem 8)) showing the equality of the risk neutral price with the price bounds of an associated trajectory based discrete market. As a complement, note that the binomial model is a complete market ((cutland, , Theorem 6.8)), then by Corollary 1 we will have a unique fair price.

Proposition 6

Consider a binomial market with parameters and , where . Let be the payoff function of a European derivative. Then, and are given by the Cox-Ross-Rubinstein price:

Proof

We will prove it by induction over . Let , then by Proposition 5,

which is the price given by Cox-Ross-Rubinstein for a -step binomial model. Suppose now that is the Cox-Ross-Rubinstein price for all binomial -bounded market and let a binomial -bounded market. It follows by Theorem 3.3 and Proposition 5,

where such that and . Then, by Lemma 3 and Theorem 3.3,

where is a binomial -bounded market, and and . Then, by inductive hypothesis,

Finally, replacing and changing variable, we obtain

which is the Cox-Ross-Rubinstein for a -step binomial model. ∎

The trinomial tree model was originally presented in boyle and offers more flexibility than binomial trees. The stock price can move up, down or can also take an intermediate price between and at each node, as shown in the diagram below.

Hence, , and it is not necessary that . Such market model is incomplete and, then, the technique of determining the value of an option via a replicating portfolio does not work. We can however find upper and lower bounds for the option values.

The next Theorem characterizes the minmax bounds and for general incomplete fixed time interval markets . It shows that the bounds are completely determined for an European convex payoff . The result can also be found in kolokoltsov and roorda .

Theorem 5.1

Consider a fixed time interval market where . Let be the payoff function of an European derivative and assume it is convex.

-

1.

If for all and there exists such that and , then are given by the Cox-Ross-Rubinstein price of the derivative in the binomial tree model with the same parameters as the interval model.

-

2.

If for all and condition (4.1) holds and there exists such that , then .

Proof

The Theorem assumes that the constant trajectory belongs to , namely, by Proposition 5, item , for each node , there exists a trajectory such that . If this condition does not hold, then part of the above Theorem is not true. For example, if we consider a trinomial market with , it is easy to see that if and, clearly, tends to when tends to .

5.1.2 Sampled Quadratic Variation (SQV)

This section introduces a discrete market model where is intended to model with the chart stock and represents the sampled quadratic variation of the trajectories, that is

| (5.4) |

Notice that when using one should use the word charts for the data , instead of as we do, but we allow ourselves some abuse of language at this point.

The general constraints defining interval models in Definition 14 can, in the present case, be interpreted as imposing constraints on the consumed quadratic variation and on the absolute value of the change on chart values, both in between consecutive trading instances. Let , as indicated in Remark 4 , we can restrict

| (5.5) |

The condition means we deal with trajectories whose total sampled quadratic variation in the interval belongs to the a-priori given subset and taking , the constraint in Definition 14 holds. We denote by a subset of satisfying the condition of Definition 14 for , , and . For any portfolio set , we will call the associated market as sampled quadratic variation interval market (or SQV market for short).

A typical node is shown below,

The trajectory set introduced in BJN can be recovered as a special case of Definition 14 by taking .

In the next section we will study how to evaluate the interval price for a finite version of intervals markets, in particular SQV markets. We will consider a finite set , which does not necessary contain a unique element. We present next an appropriate discretization for this kind of trajectories, as well as a grid data structure which will allow us to calculate the dynamic bounds for these examples.

6 Discretization and Grid Data Structure

6.1 Finite Interval Markets

A natural finite discretization leading to an implementation of interval markets defined in Section 5 is obtained by introducing real numbers and natural numbers . We assume in this section that the coordinates are associated to chart values by , using the exponential function makes it easier to connect with the usual geometric stochastic models. Then, and are restricted to belong to the sets

| (6.1) |

The parameters and provide a natural discretization of the chart exponentials.

Remark 6

If the variable is directly related to the samples , for instance, in a SQV market from Section 5.1.2, it is natural to have a unique discretization parameter for and . On the other hand, if the sets are discrete apriori, there is no need to implement a discretization. This is the case, for example, of a fixed time interval market where has a unique element.

Note that for any trajectory , in an interval market always holds that . Therefore, if there exists such that , must be equal to . Then, a trajectory with and defined by (6.1) necessarily have . Therefore, the coordinate are restricted to belong to the set

| (6.2) |

and so, by Definition 3, the corresponding markets will be -bounded.

In order to define a subset of satisfying the properties listed in Definition 14, let be a collection of positive integers and define . Without loss of generality, we can assume that . For positive integers and , we denote by a subset of with , and defined by (6.1) and (6.2) satisfying the conditions of Definition 14 (in the terms of Remark 4) for , and . We will refer to this class of trajectories as finite interval trajectory sets and as finite interval markets for the associated markets

where is a portfolio set. It is clear that finite trajectory sets will have finite cardinality.

The parameters and play a key role in the local behavior of a finite discrete market. Assume the trajectory belongs to a finite trajectory set . Taking into account the constraint

the largest value that can attain corresponds to the value . Then, in order to allow for this kind of trajectory, we must take . In the case that , there could exist trajectories with arbitrage nodes, in the sense of Definition 8. For example, assume the trajectory defined by

belongs to with , it satisfies and so, one more step is available. Then, for any trajectory it follows that

and, therefore, is an arbitrage node.

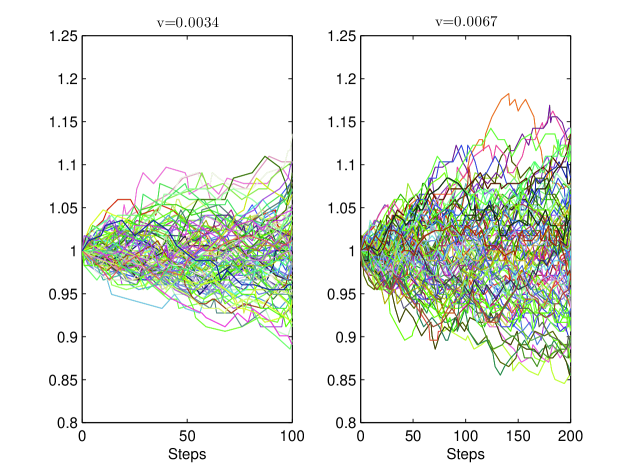

Figure 1 displays random trajectories in a finite trajectory set with , , , , , , and . It shows random trajectories in each display. The first one corresponds to trajectories with , then they must have ; while the second one corresponds to trajectories with and then, they must have . The trajectories are shown in different displays for convenience but they belong to the same trajectory set .

We refer to Appendix D for a description of a data structure and an algorithm implementing finite interval markets.

6.2 Numerical Results

This section provides numerical results illustrating some characteristics of the model described in Section 5.1.2. We compute the minmax option bound prices using the finite models from Section 6.1 and data structure and algorithm from Appendix D. The output illustrates the super-replication price for call options with respect to the maximum number of steps and different jump sizes and its variation on the presence of arbitrage nodes. Finally, some superhedging and underhedging approximations and the effect of variable volatility are presented. For reasons of space we do not provide details related to the software implementation. Other numerical results, for a different class of models, and based on market, data can be found in fleck .

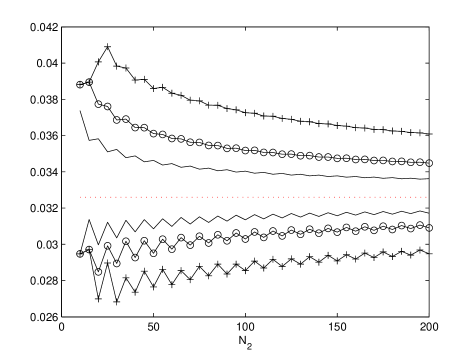

Consider a two-month European call option with strike of $1 on a stock that pays no dividends, with current price $1 and the volatility of the stock is taken to be equal to %. The Black & Scholes price for this assumptions is $0.0326 when . Define

We build a sampled quadratic variation trajectory set by taking and defining by (5.4). Recall that is the maximum number of steps for a trajectory in the model, therefore

Then, for a given , we have a unique value for . Since is defined in term of , we only need a unique parameter in order to build a finite version of a SQV market. Then, we assume in the following and, in consecuence, . Thus, for , and , we will consider the finite SQV trajectory set , where and . In this part we will consider all the trajectories in the sets (6.1) satisfying conditions (5.5).

Let the associated market for a full set of portfolios . Figure 2 shows the convergence behavior of and when with ranging from to . When the jump unit, , is greater than one, clearly, the interval price range is more narrow as increases and the Black & Scholes price belongs to the interval. Also, we can see that the interval becomes wider as increases. The reason for this is that if are two jump sizes then the set of trajectories with with parameter is included in the set of trajectories with parameter . Therefore, when we calculate the bounds, the maximum over the set with parameter is higher than the maximum over the set with parameter .

Notice a detail, when and , in the case of the jump units are 3 and 5, the upper bounds are equal. When the maximum jump that the algorithm can take is . Therefore, although we can run the program for the jump unit 5, this jump does not really take into account and thus does not affect the price of the option in the algorithm. Similarly for the lower bounds.

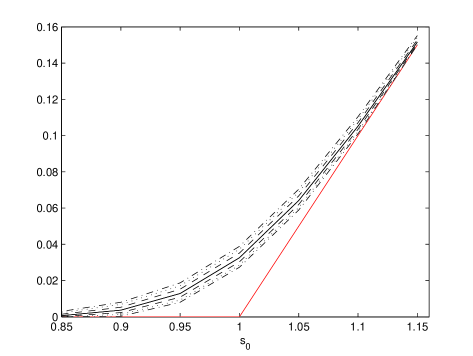

Now we fix and we will calculate the interval price for different starting levels of the stock . Let the associated market for a full set of portfolios . Figure 3 displays and for different jump units . We can see that the price increase when increases. We notice that the minmax bounds are very narrow for the higher starting level . Therefore, jumps have less of an effect on the bound of the option prices for higher values of the stock.

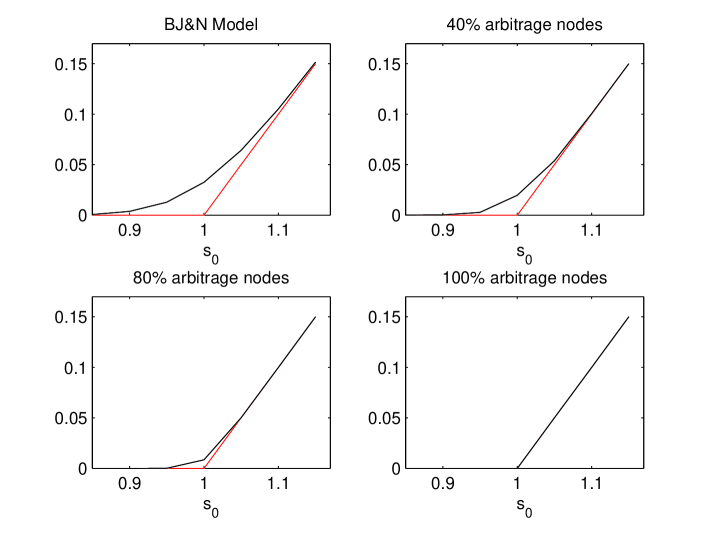

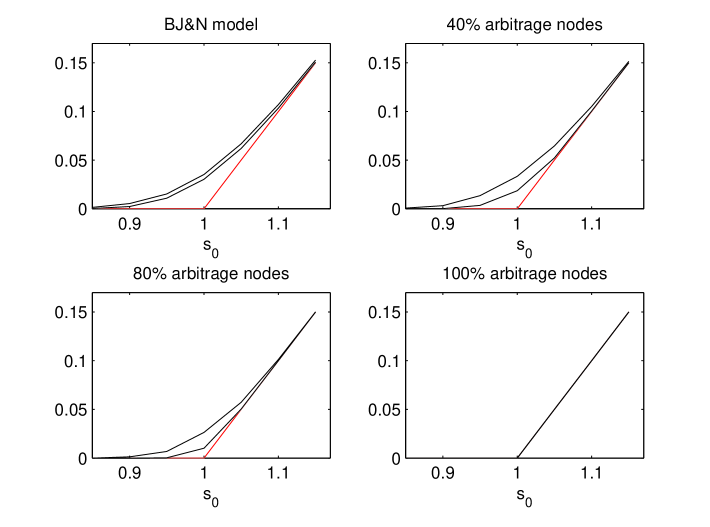

6.2.1 Effect of arbitrage nodes on minmax bounds

It is interesting to see the effect of arbitrage nodes (in the sense of Definition 8) on the model proposed above. We consider again the finite SQV trajectory set with the same parameters as above, but now the coordinates are not defined by (5.4). Namely, does not depend on the stock values. Such trajectory set is now modified in order to incorporate arbitrage nodes: let the trajectory grid corresponding to (as per Section D). Nodes are selected randomly and we change its reachable nodes as follows:

-

•

If , the reachable nodes are where

-

•

If , the reachable nodes are where

These definitions give new trajectory sets which we denote by , where arb refers to arbitrage. Observe that the modified trajectory set has trajectories with passing through an arbitrage node.

Figure 4 displays the upper and lower bound as a function of for the market and the modified with adding different percentages of arbitrage nodes. In the same way, Figure 5 displays the upper and lower bound as a function of with .

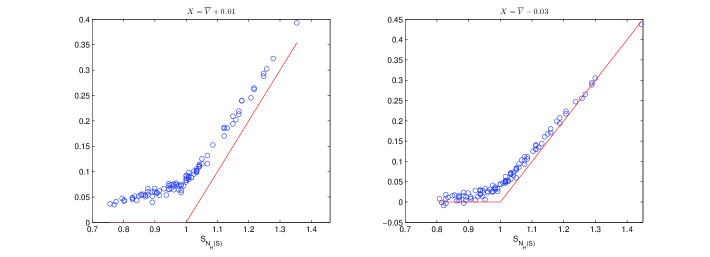

6.2.2 Hedging

The algorithm presented allow us to calculate not only the value of but also the optimal portfolio providing the investments along each possible trajectory in . On each vertex of the data grid given in Section D.1, the dynamic upper bound is available and corresponds to an optimal value given by equation (D.4). Recall that and so give a unique value for any trajectory passing through that vertex. Therefore, we can define an optimal strategy on by:

This optimal strategy is non-anticipative.

It is interesting to study how actually approximates , as function of a trajectory , for an initial portfolio value . In a short position the hedging values are given by

| (6.3) |

with the initial portfolio value.

Figure 6 shows the hedging values (6.3) with and , for random trajectories with , and with respect to an European call for the model studied at the begin of the Subsection. We can see that the values from (6.3) superhedge the payoff value in the first case. For the case , the values tightly approximate the payoff values.

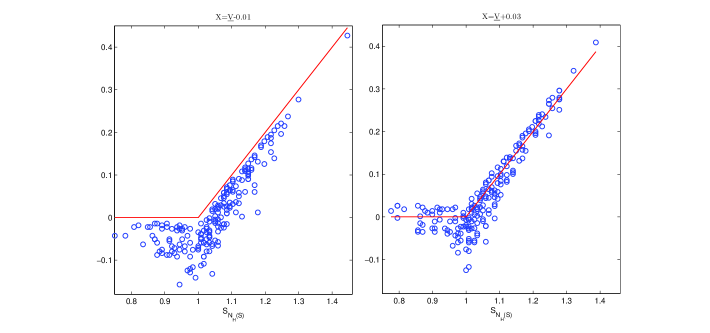

In a long position, the hedging values are given by

| (6.4) |

with the initial portfolio value. The underhedging portfolio is computed in a similar way than the upperhedging one , but using the values which gives the lower bounds instead of the upper bounds. Figure 7 displays the values from equation (6.4) with and , for random trajectories with respect an European call . In this case, we can see that the values from (6.4) underhedge the payoff value for . For , the values better approximate the payoff.

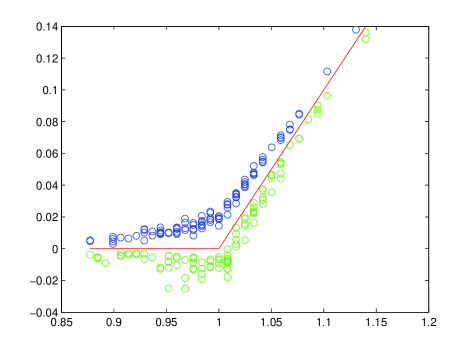

Finally, it is of interest to superimpose the upperhedging and lower hedging using and respectively. Figure 8 does this for with , and .

6.2.3 Effect of Variable Volatility

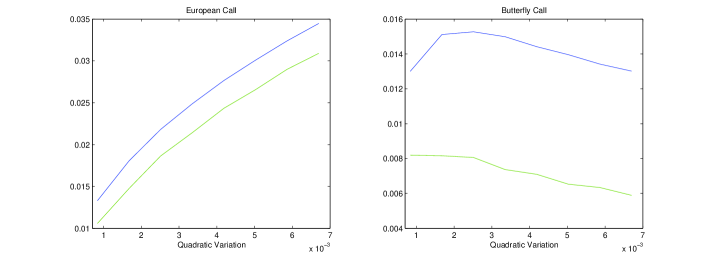

This section illustrates the minmax bounds for several finite SQV markets (introduced in Section 5.1.2) related to the selection of the set . Recall that gives the possible values of quadratic variation of the trajectories in the market.

We consider first markets where is a singleton set with and . The corresponding markets are denoted by , , where . Figure 9 shows the lower and upper bound as function of increasing values of the quadratic variation for two different options. A European call and a butterfly call option with strikes is defined by

We will consider , , and ranging from to . So we build eight finite SQV markets .

It is observed that the bounds increase monotonically with respect to the quadratic variation for the case of an European Call but, for the case of a butterfly Call, the behavior is not monotonic. It is important to remark that the payoff of an European call is a convex function and the butterfly call is neither convex nor concave.

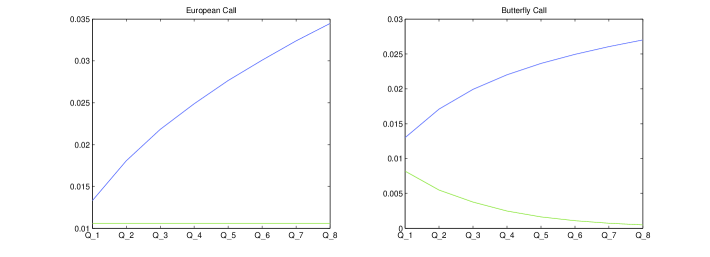

We now incorporate several possible quadratic variation values to the set . To this end, we build the finite SQV market where, in this case, . Figure 10 shows the lower and upper bound as function of the sets for a European call and a butterfly call.

Note that for the European call, the upper bound graph coincide with the upper bound graph in Figure 9. It means that the upper bound only depends on the maximum value of the set . Instead, the lower bound is constant for all given that the lower bound only depends on the minimum value of the set . In the case of the butterfly call the upper bound increases monotonically and the lower bound decrease monotonically as the size of increases and, so, reflecting a general feature of minmax pricing.

7 Conclusion

General results are obtained to evaluate minmax bounds in an effective way and for general classes of trajectory markets assuming a bound on the number of possible trades. We perform explicit computations for the usual options, covering a new model where trajectories have different values of (sampled) quadratic variation. The numerical experiments indicate some of the phenomena that may occur in a trajectory based approach for the examples introduced. In particular, the effect of arbitrage nodes on prices is illustrated. Testing with different trajectory sets, we obtain narrower price intervals for European options. We conclude that designing suitable trajectory sets for different setups is a relevant task. The reference fleck introduces models reflecting practical constraints with parameters estimated to market data.

Appendix A Minmax Functions Results

This Appendix provides the main results on minmax function and the relation with the boundedness of and . We will need the following definition.

Definition 15 (Stopping Time)

Given a trajectory space a trajectory based stopping time (or stopping time for short) is a function such that if with and for then .

The integrability conditions, required for payoffs in a probabilistic setting, are replaced in the proposed framework by the, so called, minmax functions (introduced in (deganoI, , Definition 14)). In what follows consider a discrete market , and a function defined on .

Definition 16

(Upper and Lower Minmax Functions) Given a finite sequence of stopping times with for , a real sequence , and , we call an upper minmax function if

Similarly, is called a lower minmax function if

Given a finite sequence of stopping times with for , and a real sequence , set (set for convenience), define

| (A.1) |

Also, for , define the functions , for , by

| (A.2) |

The fact that , in the above definition, is a portfolio on , for any , is proven in the next Lemma. Observe first that, for a fixed and we have . Then

| (A.3) |

Lemma 2

Assume for each . For , defined by (A.2) is a portfolio on .

Proof

Follows trivially from the above Lemma that for , and any ,

| (A.5) |

Next natural Proposition gives the key statements for the boundless of and .

Proposition 7

Let be fixed, and , then

-

1.

if and only if there exists and such that

(A.6) In any case .

-

2.

If there exists and such that

(A.7) and either of the two statements below hold:

-

(a)

is conditionally -neutral at and for any , defined by if and if , with and , belongs to .

-

(b)

is -bounded such that satisfies the local -neutral property.

Then .

-

(a)

Proof

Proof of part (1). Since , there exist and such that

From where (A.6) holds. Conversely, if (A.6) is valid, it is clear that

Proof of part (2): is a non-anticipative function, then by the general hypothesis

| (A.8) | |||||

Using now the condidtions in , it follows that

For the hypothesis , consider the set of portfolios consisting of all with defined in , then the market is -bounded and local -neutral, and then, by Proposition 1, conditionally 0-neutral. Thus the right hand side of (A.8) is equal to . ∎

Proposition 7 holds in a more general scenario. The -bounded condition in the second part can be replaced by the initially bounded condition defined in deganoI , as follows.

Definition 17

Given a discrete market and ; we will call initially bounded if there exists a bounded function (which may depend on ) such that for all :

| (A.9) |

Under this hypothesis, Theorem 1 keep holding and then, we could formulate the next Proposition in this terms. But as the present work focus in -bounded markets, we present the proof of Proposition 8 for this kind of markets. Observe that if is bounded, it is initially bounded, satisfies the definition.

Proposition 8

Let be a discrete market and a function defined on . Consider a finite sequence of stopping times with for with for all , a real sequence , and . Fix and an integer . Then the following statements are valid:

-

1.

If is an upper minmax function and , then:

-

2.

If is a lower minmax function and , then:

Furthermore:

-

3.

If is a lower minmax function and either of the two statements below hold:

-

(a)

is conditionally -neutral at and for any , .

-

(b)

is -bounded such that satisfies the local -neutral property and is bounded.

Then:

(A.10) -

(a)

-

4.

If is an upper minmax function and either of the two statements below hold:

-

(a)

is conditionally -neutral at and for any , .

-

(b)

is -bounded such that satisfies the local -neutral property and is bounded.

Then:

-

(a)

Where for the sequences are given by (A.1), and respectively, for each item.

Proof

Proof of item (2). From hypothesis , and , it follows from (1) that

Proof of item (3). For any it follows from (A.3), and similar computation as in the proof of part (1), that

| (A.11) | |||||

Under assumption (a) in item (3), we know that , therefore by -conditional property,

Assume now in item (3) and such that for all . Let be any set containing the portfolios and for each . Then, the market is -bounded, where . Thus Theorem 1 shows that is conditionally -neutral at all nodes, in particular at ; therefore, taking the supremum over in both sides of (A.11), evaluating the infimum over in the right hand side, and using the conditional -neutral property of we obtain (A.10).

The proof of item (4) follows from (3) in a similar way than (2) from (1). ∎

Appendix B Some Technical Results

Here are located some definitions and auxiliary lemmas required for results in subsections 3.1 and 3.2. Recall that at this section we assume for all .

B.1 Auxiliary Results for Subsection 3.1

Definition 18

Consider a discrete market model , and a function defined on . Fix , and such that . Set and . For and define

-

•

, and . Then .

-

•

where and (recall ).

Also define

and for any ,

Lemma 3

Under the conditions of Definition 18, for any and with ,

-

1.

is a discrete market model, with initial value and . Moreover it is -bounded if is -bounded.

-

2.

Assuming is -bounded, for any ,

-

3.

.

Proof

By definition, consist of sequences in , with and for any . is a family of sequences of functions with . Lets see is non-anticipative. Set such that and , for with . Then by definition and , for with . Therefore

since is non-anticipative. Thus is a set of portfolios on . Furthermore, if is -bounded, for each , we have . This proves .

For , we proceed by induction backwards over . Let and , then since is -bounded. If , then and

But if , then and . Therefore . Now assume is valid for . Set and suppose first . Similar analysis shows that . Suppose now , then

by inductive hypothesis and Definition 18. Then we get .

Now we will prove . Since , it follows that

∎

Lemma 4

Consider the -bounded market , given in definition 18, for and some in an -bounded market . Then is FULL if so is also .

Proof

Assume is FULL. Let , , and . We are going to prove that for , any function

non-anticipative with respect to , is the -coordinate of a portfolio . For it, we will find such that on .

We need to show that if and only if . Let , and , then

On the other hand

If , and , , it means that . Since is FULL it then follows that exists such that is given by . ∎

B.2 Proofs for u-Complete Markets Section

Consider a discrete -bounded market . For any define by for and

Set and define . results an -bounded discrete market.

If is a derivative function defined on , then is defined on by

for any .

Moreover

Lemma 5

Let an -bounded discrete market. Then

-

1.

For any , and ,

-

2.

If is u-complete for , so is for .

Proof

Reasoning by induction backwards, for , and ,

| if | ||||

| if |

Since if , , and if , . Assume is valid for some . If , then and, , since its common value is or . If , then ( implies , then !), and by inductive hypothesis and definition of ,

For , let , and a derivative function . Since is u-complete there exists , such that

Last equalities hold for . ∎

Proof

of Proposition 2. Define , by

assuming that . Since for any , the functions given by are affine, then its supremum is lower semicontinuous, and convex.

If is compact, by lower semicontinuity, there exists verifying

If and satisfies the local up-down property at and , is also coercive. Indeed, there exist such that and . Let and

If , , then . On the other hand, if , since , then .

Thus, by Corollary 4.3 in agheksanterian , from (kurdila, , Thm 7.3.1) attains a minimizer.

Finally, by coercivity, there exists such that, if . Then

∎

Proof

of Proposition 3. First it is necessary to show that defined by (3.15) is non-anticipative. Let with for with , then and since is a stopping time for all , so .

For the u-completion of , we first prove by backward induction that for any . It is clear that , for all . Let such that for all . Then

since . Assume now such that for all and suppose for all . Then

since . Finally for (3.14), for any ,

with . ∎

Appendix C Auxiliary results

The next geometric Lemma is used in section 4.

Lemma 6

Let , with and . If and , then

| (C.1) |

Proof

Appendix D Computational Grid

Here we are going to introduce a grid of pairs of integer numbers , which will be used to represent the trajectories of a finite discrete market. The purpose of the grid is to give a combinatorial way to build finite trajectory sets and implement an efficient algorithm in order to evaluate the dynamic bounds for a finite discrete market. Consequently, under appropriate conditions, we will obtain also the global bound .

Given the discretization parameters and , we call trajectory grid to

For any , each node of a trajectory can be represented by a vertex , such that

| (D.1) |

It has shown in Section 6.1 that it is enough that . Also observe that the constrains of Definition 14 are translated to the grid information: if then

| (D.2) |

Remark 7

Note that if such that and for all , and , then and are associated with the same vertex in , but and with .

On the other hand, any sequence , with the constrains listed on the left side of (D), corresponds by the same association (D.1), to a trajectory satisfying the constrains of Definition 14. Then, given a trajectory grid with parameters and , we can build a finite trajectory set for appropiate and , in such way that any possible path in with the constrains listed on corresponds to a trajectory in , and the inverse implication also holds.

Remark 8

Note that a grid does not contain necessarily all the path satisfying the constrains listed in (D). For example, the next grid satisfies the conditions for and and do not contain the path such that .

D.1 Computation of Prices in the Grid

The trajectory grid presented above will be used to compute the dynamic bounds where is the finite discrete market associated to the grid with parameters and . To this end, we will using Theorem 4.1. For reasons of space, we will use the abbreviated notation .

Let an European option defined on . The option is assumed independent of the trajectory history, namely for a real variable function . This condition on allows to compute the dynamic bounds on the vertices of as follows. For simplicity we will use the notation . Also assume that the set of portfolios is composed for sequences including any function from to , non anticipative with respect to , thus is FULL.

Now we describe an algorithm that works for the case . The dynamic bounds for , can be associated to the vertices of . Indeed since the node corresponds by (D.1) to some (), then . Moreover whenever the trajectory has a node , will have

Now, the grid node correspond to a trajectory at stage . We know from Definition 9 and Theorem 4.1 that only depends on , and , where . Then, by (D), those quantities are associated to the vertices with

| (D.3) |

Vertices verifying (D.3) are called reachable from .

can be associated with the vertex , via a function with domain in such way that . Thus, for each vertex we define by the following procedure. Since any vertex corresponds to a trajectory , with , define

Now assume, for fixed , was defined for any , and any . For fixed and any pairs , verifying

| and | |||||

| and | (D.4) |

set

Being a trajectory such that corresponds by (D.1) to , it is important to notice that the pairs and verifying (D.4) are reachable from , if verify that and corresponds respectively to and , then and . Consequently Theorem 4.1 is applicable and is defined according to it, by

| (D.5) |

Therefore, the above recursive procedure allows to obtain , since the hypothesis of Theorem 3.3 are satisfied.

We now extend the procedure to an strictly increasing -tuple with . Now for some , then the node of some trajectory corresponds by (D.1) to some , and . But observe that if also corresponds to a node of a trajectory with , by Definition 9 and Theorem 4.1

We start the analysis from column . Any vertex corresponds to the node of a trajectory in , then define

For a vertex with , and , is given by (D.5). The vertices on the column in , correspond by (D.1) to trajectories that could have at that node, it is , or continue to get . Thus for , should take the value in the first case, while in the second case its value at that vertex, should be given by (D.5). Both situations must be contemplated to compute for , by mean of (D.5), when any of the vertices is reachable from . Then, observing that the maximum of these two values is the one which contributes to (4.2), in the referred computation, and by Theorem 4.1, we have

Following the same considerations, is defined by (D.5) for all with and . For with and

where is given by (D.5).

To summarize, for and is given by

where is given by (D.5). With this recursive procedure we can calculate the value of .

Recalling that , the lower dynamic bounds are computed by a similar procedure.

References

- (1) Alvarez A, Ferrando S, Olivares P (2013) Arbitrage and hedging in a non probabilistic framework. Mathematics and Financial Economics 7(1): 1-28.

- (2) Alvarez A, Ferrando S (2016) Trajectory based models, arbitrage and continuity. International Journal of Theoretical and Applied Finance 19(3): 34 pages.

- (3) Alexanderian A (2007) Some results on Optimization in Hilbert Spaces. Lecture notes.

- (4) Andrew A. (1979). Another efficient algorithm for convex hulls in two dimensions. Inf. Process. Lett. 9(5): 216-219.

- (5) Avellaneda M, Levy A, Paras A (1995) Pricing and hedging derivative securities in markets with uncertain volatilities. Applied Mathematical Finance 2: 73–88

- (6) Bernhard P, Engwerda J, Roorda B, Shumacher J, Kolokoltsov V, Saint-Pierre P, Aubin J.P. (2013) The interval market model in mathematical finance. Birkhauser, Game-Theoretic Models.

- (7) Bertsekas D (2012) Dynamic Programming and Optimal Control. Athena Scientific.

- (8) Bertsekas D, Shreve S.E. (1978) Stochastic Optimal Control: the Discrete Case. Mathematics in Science and Engineering, Vol 139.

- (9) Boyle P (1986) Option Valuation Using a Three-Jump Process. International Options Journal, 3:7-12.

- (10) Britten-Jones M, Neuberger A (1996) Arbitrage pricing with incomplete markets. Applied Mathematical Finance, 3:347-363.

- (11) Burzoni M, Frittelli M, Maggis M (2016) Universal arbitrage aggregator in discrete-time markets under uncertainty , Finance Stoch. 20:1-50.

- (12) Burzoni M, Frittelli M, Maggis M (2016) Model-free superhedging duality, arXiv:1506.06608v3 [q-fin.PR]

- (13) Carassus L, Gobet E, Temam E (2007) A class of financial products and models where super-replication prices are explicit. Proceedings of the 6th Ritsumeikan International Symposium on Stochastic Processes and Applications to Mathematical Finance, 67-84.

- (14) Carassus, L. and Vargiolu, T. (2010). Super-replication price for asset prices having bounded increments in discrete time. https://hal.archives-ouvertes.fr/hal-00511665

- (15) Cheridito P, Kupper M, Tangpi L (2016) Duality formulas for robust pricing and hedging in discrete time. arXiv:1602.06177v2 [q-fin.PR]

- (16) Cox J, Ross S, Rubinstein M (1979) Option pricing: a simplified approach. Journal of Financial Economics,7:229-263.

- (17) Cutland N, Roux A (2013) Derivative pricing in discrete time. Springer-Verlag London.

- (18) Ferrando S, González A, Degano I, Rahsepar M (2016) Discrete, Non Probabilistic Market Models. Arbitrage and Pricing Intervals. Submitted for publication, available at http://arxiv.org/abs/1407.1769

- (19) Desmettre S, Korn R, Seifried F.T. (2015) Robust worst-case optimal investment. OR Spectrum, 37(3):677-701.

- (20) Eberlein E, Jacod J (1997) On The range of option prices. Finance Stoch, 1:131-140.

- (21) El Karoui, N, Quenez M (1995) Dynammic programming and pricing of contingent claims in an incomplete market. SIAM Journal on Control and Optimization, 33:29-66.

- (22) Fleck A (2016) Trajectory based market models with operational assumptions. Department of Mathematics, Ryerson University. MSc tesis.

- (23) Föllmer H, Schied A (2011) Stochastic Finance: An Introduction in Discrete Time, Third Edition. Walter de Gruyter.

- (24) Kahalé N (2016) Super-replication of financial derivatives via convex programming. Available at SSRN http://ssrn.com/abstract=2172315.

- (25) Kolokoltsov V (1998) Nonexpansive maps and option pricing theory. Kybernetika, 34:713-724.

- (26) Kurdila, A. and Zabarankin M (2005) Convex Functional Analysis. Springer.

- (27) Merton R (1973) Theory of rational option pricing. Bell Journal of Economics and Management Science, 4(1):141-183.

- (28) Peng S. (2010) Nonlinear Expectations and Stochastic Calculus under Uncertainty. http://arxiv.org/abs/1002.4546

- (29) Riedel F (2015) Financial economics without probabilistic prior assumptions. Decisions in Economics and Finance, 38:75–91.

- (30) Roorda, B. Engwerda, J. and Schumacher, J. (2005) Performance of hedging strategies in interval models. Kybernetika, 41.5, 575-592.

- (31) Rebonato, R. (2004) Volatility and Correlation: The Perfect Hedger and the Fox, 2nd Edition. Wiley, New York.