Optimal Portfolio Liquidation and Dynamic Mean-variance

Criterion

Jia-Wen Gu

Department of Mathematical Science, University of Copenhagen, Copenhagen,

Denmark. (email: kaman.jwgu@gmail.com).Mogens Steffensen

Department of Mathematical Science, University of Copenhagen, Copenhagen,

Denmark. (email: mogens@math.ku.dk).

Abstract

In this paper, we consider the optimal portfolio liquidation problem under

the dynamic mean-variance criterion and derive time-consistent solutions in

three important models. We give adapted optimal strategies under a reconsidered

mean-variance subject at any point in time. We get explicit trading strategies in

the basic model and when random pricing signals are incorporated. When we

consider stochastic liquidity and volatility, we construct a generalized HJB

equation under general assumptions for the parameters. We obtain an explicit

solution in stochastic volatility model with a given structure supported by

empirical studies.

1 Introduction

As quantitative trading is generally used by financial institutions and

hedge funds, the transactions are usually large in size and may involve the

purchase and sale of hundreds of thousands of shares and other securities.

However, quantitative trading is also commonly used by individual investors.

A fundamental part of agency algorithmic trading in equities and other asset

classes is trade scheduling. Given a trade target, that is, a number of

shares that must be bought or sold before a fixed time horizon, trade

scheduling means planning how many shares will be bought or sold by each

time instant between the beginning of trading and the horizon. This is done

so as to optimize some measure of execution quality, usually measured as the

final average execution price relative to some benchmark price. Almgren and

Chriss (2000) consider the execution of portfolio transactions with the aim

of minimizing a combination of volatility risk and transaction costs arising

from permanent and temporary market impact. Kharroubi and Huyên

Pham(2010) study the optimal portfolio liquidation problem over a finite

horizon in a limit order book with bid-ask spread and temporary market price

impact penalizing speedy execution trades, respectively. Almgren (2012)

considers the problem of mean-variance optimal agency execution strategies,

when the market liquidity and volatility vary randomly in time. He

constructs an HJB equation relying on ”small impact approximation” under

specific assumptions for the stochastic process satisfied by these

parameters.

The mean-variance analysis of Markowitz (1952) has long been recognized as

the cornerstone of modern portfolio theory. Attention is regained by

relating dynamic mean-variance optimization formalistically to quadratic

utility in Korn and Trautmann (1995), Korn (1997) and Zhou and Li (2000).

The same problem is categorized as mean-variance optimization with

pre-commitment (See Christiansen and Steffensen (2013) for detailed

illutrations). Recently, attention has been regained by Basak and Chabakauri

(2010) who challenge the pre-commitment (to the time 0-expected value as the

target of the quadratic utility) assumed by Zhou and Li (2000). They solve

the problem for the so-called sophisticated investor who updates his

non-linear mean-variance objective and takes future updates,

time-consistently, into account. In this paper, the dynamic mean-variance

criterion is applied to the optimal trading problem.

In this paper, we consider the quantitative trading problem under the

dynamic mean-variance criterion and derive time-consistent solutions in

three important models. Our paper contributes to the quantitative trading

literature in various aspects. Firstly, we solve the dynamic mean-variance

quantitative trading problems and derive time-consistent solutions. We give

optimal strategies under a reconsidered mean-variance subject at any point in time.

Previous

literature seems only give precommitment and deterministic control

solutions. Almgren (2012) gives the trading strategy in the basic model

where it is fixed rather than adaptive.

Secondly, we determine the explicit solutions when random pricing signals

are incorporated. A random pricing signal, gathering the information of the

index data, trading volume and public and private market events, can be

regarded as the indicator of the stock movements. Various methods have been

proposed to study the pricing signal in the literature. Introduction to the

literature is deferred to Section 3. In this paper, the trading strategy is

derived when the random pricing signal is assumed to be a diffusion process.

Thirdly, we consider the trading strategy in the case of stochastic

volatility and liquidity impact. We allow the liquidity and volatility to

vary randomly in time and the determined trading strategy is adapted to the

market state. We give the generalized HJB equations in the stochastic

volatility and liquidity impact models while early study reply on a ”small

impact approximation” (Almgren (2012)). We also get an explicit solution in

a stochastic volatility model with a given structure supported by empirical

study.

The remainder of the paper is structured as follows. In Section 2, we give

the trading strategy in the basic model which is adopted from Section 1 of Almgen (2012). In Section 3, optimal strategy is

presented when random pricing signals are incorporated. In Section 4, we

consider stochastic volatility and liquidity model. Conclusions are given in

Section 5.

2 The Basic Model

In this section, we consider the basic model adopted from Almgren (2012). In

the model, the price of a stock is govern by the SDE,

(1)

where is the time-dependent volatility of the stock and

is a standard Brownian motion. The price actually received on each trade is

where is the coefficient of temporary market impact, also

time-varying and is the rate of buying. The volatility and

impact functions and are assumed to be continuous

functions of to account for trading seasonality. The trader begins at

time with a purchase target of shares, which must be completed by

time . The number of shares yet to be purchased at time is the

trajectory , with and . Hence

(2)

The cost of trading, is the total dollars paid to purchase shares

subtracting the initial market value:

By integration by parts, we rewrite

(3)

We determine the optimal trajectory by the dynamic mean-variance criterion

This is newly proposed by Basak and Chabakuri (2010), who come up with the

dynamic mean-variance criterion challenging the pre-commitment mean-variance

assumed by Korn (1997) and Zhou and Li (2000). Basak and Chabakuri (2010)

use this criterion in asset allocation problem for the so-called

sophisticated investor who updates his nonlinear mean-variance objective and

takes future updates, time-consistently, into account.

To address the optimal trading problem, we define a process by

Using the It’s lemma, (2), (4) and after inserting ,

hence (13) follows and the optimal strategy is given by . Together with (10), (14)

follows.

Consequently, the two PDEs for and can be derived as follows

(15)

(16)

From (5), we see that the optimal strategy

does not depend on and for . Hence, depends only on and . Combining (2), is a deterministic control and is a deterministic process.

Therefore, (15) reduced to

(17)

The initial data for the PDE (17) is a local asymptotic

condition. Considering (12), near expiration , the terms

with become negligible, then we must liquidate on a linear trajectory and hence the function has local behavior

We look for a candidate solution to HJB in the form Plugging

into the HJB, we see that should satisfy the ODE:

and

The optimal strategy is given by

If we restrict and to be constant,

The optimal strategy can be expressed as

This is the same strategy as the one obtained by Almgren (2012). However, it is important to realize that the problem formulations are different. Whereas Almgren (2012) finds the best deterministic strategy for a classical mean-variance problem, we find the best stochastic strategy for a time-consistent formulation of the mean-variance problem. Since the best strategy is deterministic, time-consistency does not distinguish the two problems and the two strategies coincide. However, when we proceed and add randomness from signals, volatility, and liquidity, this coincidence is lost, since our strategies become adapted and reflect specifically the time-consistency of the problem formulation.

3 Random Pricing Signals

We consider the trading problem of mean-variance optimal agency execution

strategies, when a random pricing signal is included. A random pricing

signal, gathering the information of index data, trading volume and public

and private market events, can be regarded as the indicator of the stock

movement. Various research work have considered pricing signals for the

support and prediction of limit and market order placement strategies of

traders. Interested readers are advised to refer to Milgrom and Stokey

(1982) and Suominen (2001).

The model with random pricing signals enhances the trading quantity for two

reasons. First, the incorporation of pricing signals relates stock returns

to market returns. One can identify the pricing signals by investigating

statistical and normal relationships between an asset’s returns and market

factors. Some notable examples of understanding the relationships between

stock returns and market returns include the CAMP model by Sharpe (1964),

the common risk factor model by Fama and French (1993), the Extended

four-factor model by Carhart (1997) and the GARCH model by Lamoureux and

Lastrapes (1990). Second, the model replies on the belief that extreme price

movements are caused by temporary liquidity shortage and manipulation and

would be followed by a price reversal, which is consistent with the market

behavior. In our model, the price reversal is described be a reverting

process with rate .

Another example of the incorporation of random pricing signals is pairs

trading. The strategy monitors performance of two historically correlated

securities, e.g. Coca-Cola (KO) and Pepsi (PEP). When the correlation

between the two securities temporarily weakens, i.e. one stock moves up

while the other moves down, the pairs trade would be to short the

outperforming stock and to long the underperforming one, betting that the

”spread” between the two would eventually converge (See Mudchanatongsuk et

al. (2008)). One can identify the pricing signals by investigating the

average stock movements of the pair of stocks and finding the optimal

trading strategy under the mean-variance criterion by our approach.

To be more specific, the price of a stock is govern by SDEs:

(18)

where is a random pricing signal, the rate by

which the shock dissipate and the variable reverts towards the signal, is the volatility of the stock and and

are independent standard Brownian motions. We assume , , and are continuously time-varying to

account for trading seasonality.

The cost of trading, is the total dollars paid to purchase shares

subtracting the initial market value:

We determine the optimal trajectory by the dynamic mean-variance criterion

We now follow the recipe presented in the previous section and define a

process as

(19)

such that . Our objective becomes

Suppose that we are given an optimal trading strategy , and the corresponding value of . The value

function is defined as

Using the It’s lemma, (2), (25), (26) and after inserting ,

hence (27) follows and the optimal strategy is given by . Together with (23), (28) follows.

Consequently, the two PDEs for and can be derived as follows

(29)

(30)

Similar to the local asymptotic condition in the basic model, near

expiration, one must liquidate on a linear trajectory. Therefore,

We look for a candidate solution to PDEs in the form

(31)

We plug (31) into (29) (30) and obtain a

system of ODEs.

(32)

From (32), one can find that solutions to are trivial, i.e.,

. Hence the optimal strategy becomes

which only evolves and . Therefore, (32) can be reduced to (33), which gives the optimal strategy.

(33)

To summarize, the optimal strategy is given by

Example 1

If we set , then this model reduces to be the basic one. From (32), one can find solutions to are trivial if ,

i.e., . Consequently,

If we restrict and to be constant, we obtain,

and

4 Stochastic Liquidity and Volatility

In this section, we consider the liquidity impact and

in the basic model to de dependent on the trading position and an

independent variable representing the “market

state”, i.e.,

where and are known function of and is a

Brownian motion independent of . A derivation corresponding to the

previous sections leads to the value function

where

We also have

where

(34)

Proposition 3

The HJB equation concerning the optimal trading problem is given by

(35)

where the minimum is clearly and

satisfies

(36)

Proof:

As usual we have

Using the It’s lemma and after inserting ,

hence (35) follows and the optimal strategy is given by . Together with (34), (36)

follows.

Consequently, the two PDEs for and can be derived as follows

(37)

(38)

Finding an explicit solution to the system of PDEs is difficult but we can

still find one under some assumptions.

Example 2

Here we provide an example to capture stochastic volatility and time-varying

liquidity impact, where we assume . Blais and Protter (2010) examine the structure of the supply curve using

tick data. They find that for highly liquid stocks, the supply curve is

effectively linear, with a slope that varies with time. Their empirical

analysis also indicates the slope has a small variance. This supports we use

a time-varying liquidity impact . Empirical investigations (Jones,

Kaul and Lipson (1994)) reveal a significantly positive relation between

trade size, volume of transactions and stock volatility. If from time to

, liquidity of the stock is mainly provided by the trader. There is a

positive relation between the volatility and speed of liquidity. The average

speed of liquidity is fixed from to , i.e., . So there is a

negative relation between the volatility at time and the average speed

of liquidity from to , i.e., . This supports our

assumption .

We look for a solution of the form:

(39)

with

Consequently, we obtain a system of ODEs.

(40)

The optimal strategy becomes

5 Numerical Illustrations

In this section, we give numerical examples of our three models for

quantitative trading with dynamic mean variance criterion. Our trading

target is to buying 100 shares of stock () within a week (5 working

days, i.e. ) and we set parameter .

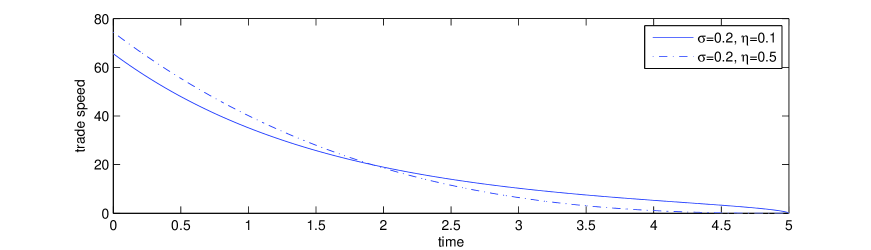

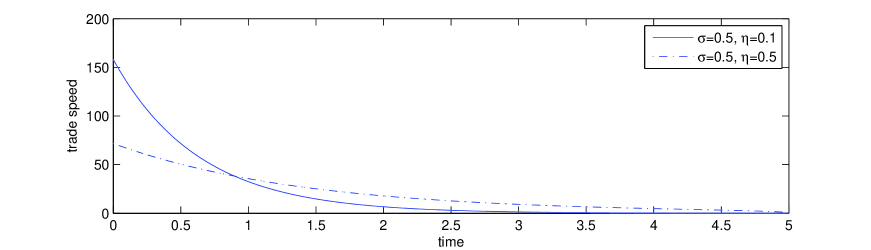

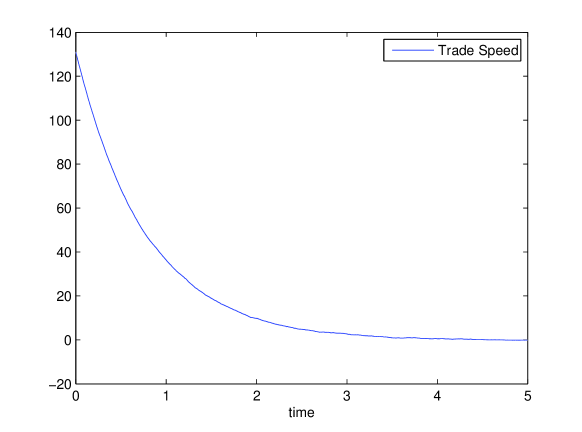

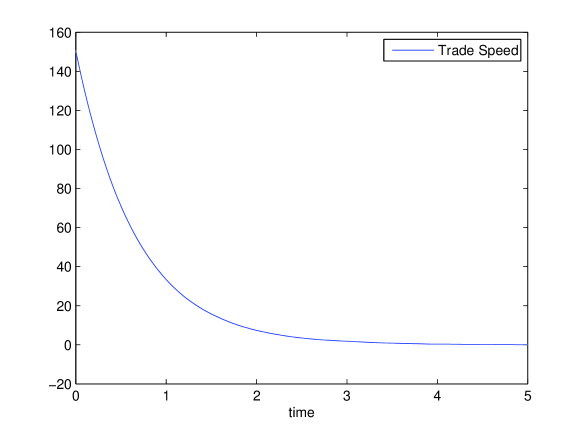

Figure 1 gives the trade strategy in the basic model with various constant

values for volatility and liquidity impact.

Figure 1: Trade Strategy in the Basic Model with various values for

volatility and liquidity Impact

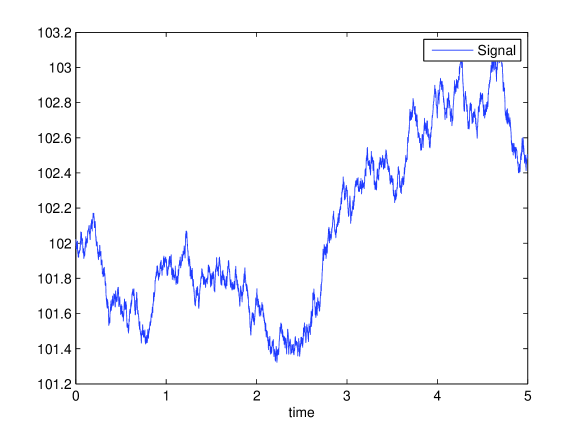

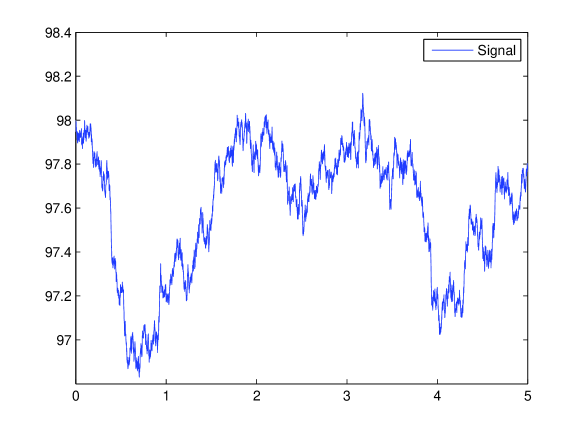

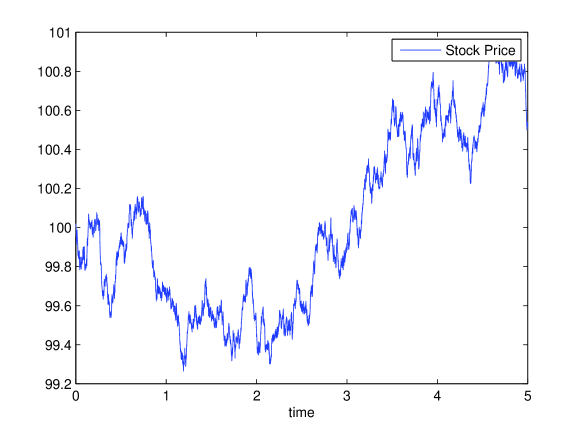

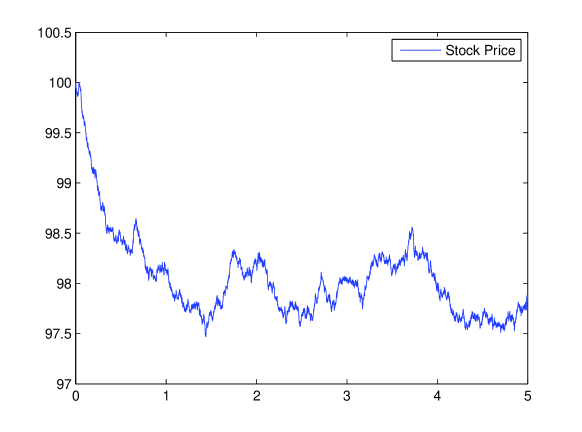

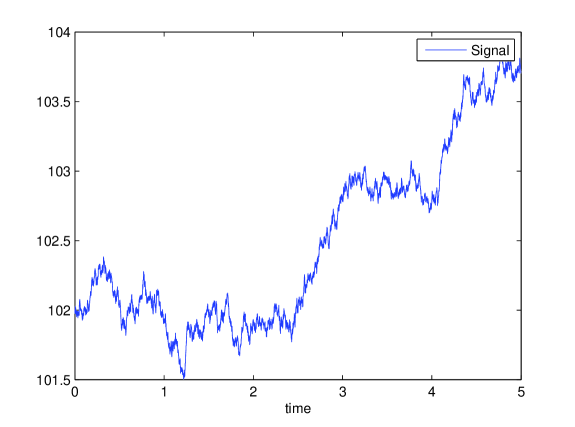

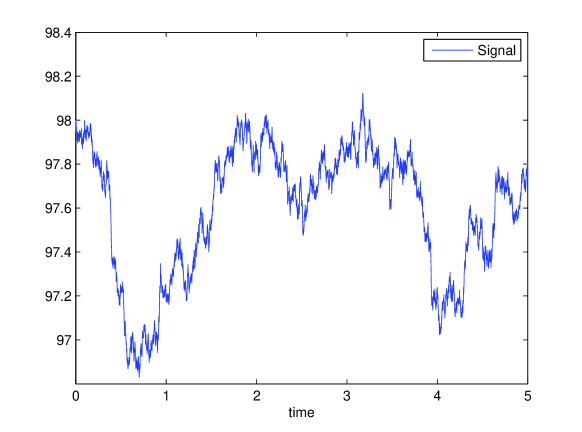

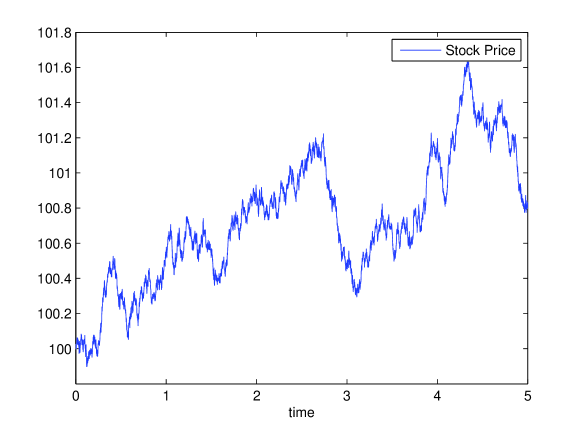

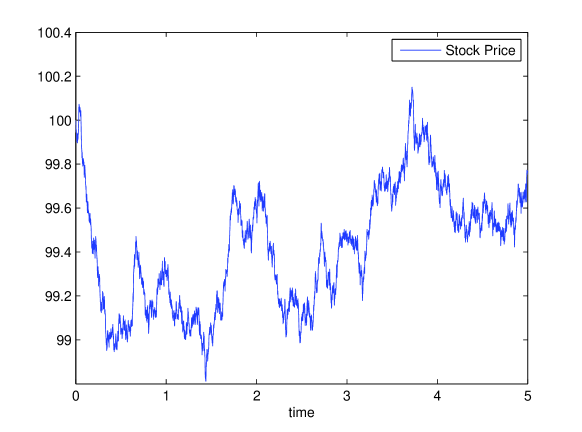

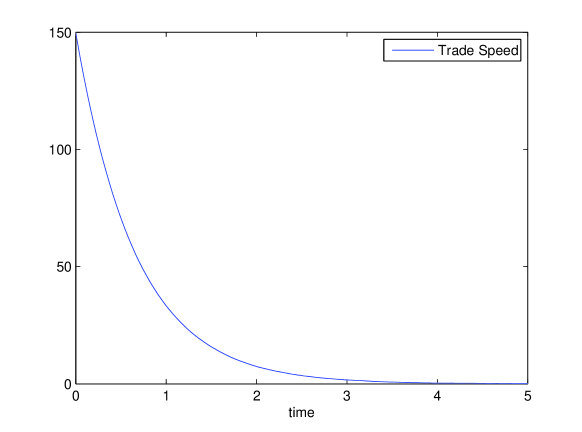

In Figure 2, we present the trading strategy on four simulated paths of

stock price and pricing signals. For simplicity we assume that the

time-varying parameters to be constant and we summarize the values for

various parameters as . Figures

(2a), (2c), (2e) gives the trading speed in the case , Figures (2b), (2d), (2f) gives that in the case , Figures (3a), (3c), (3e) gives that in the case while Figures (3b), (3d), (3f) gives that in

the case . When , the model with

random signal degenerates to be the basic one.

Figure 2: Trade Strategy with Random Pricing Signals(I)

Figure 3: Trade Strategy with Random Pricing Signals(II)

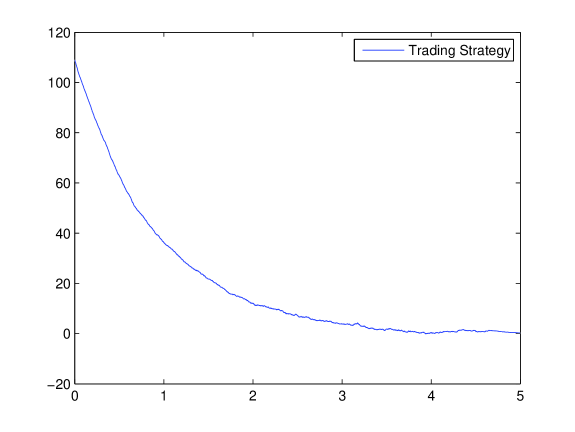

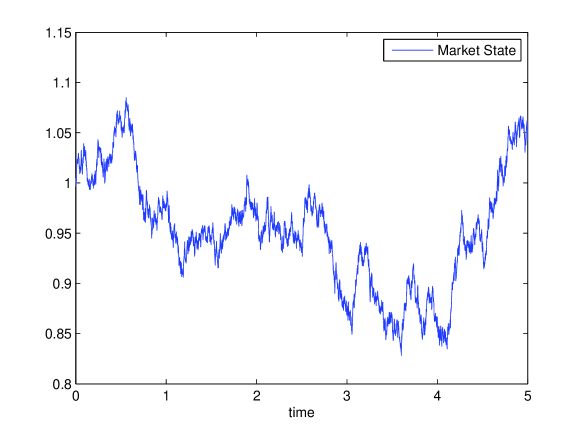

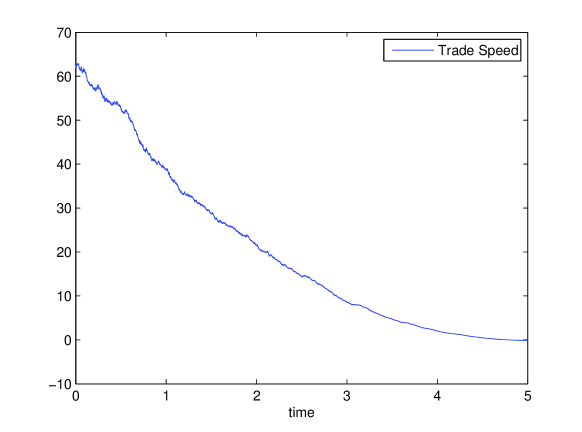

Figure 3 shows the trading strategy in the stochastic volatility model

(example 1). For simplicity, we assume and are constants

and we summarize the values of the parameters are as follows .

Figure 4: Trade Strategy in Stochastic Volatility Model

6 Conclusions

In this paper, we consider the quantitative trading problem under the

dynamic mean-variance criterion and derive time-consistent solutions in

three important models. We give a optimal strategy under a reconsidered mean-variance subject at any point in time.

We also get an explicit trading

strategy when random pricing signals are incorporated. When consider

stochastic liquidity and volatility, we give the exact HJB equations. We

obtain an explicit solution in stochastic volatility model with a given

structure supported by empirical study.

References

[1] R. Almgren, (2012), Optimal trading with stochastic

liquidity and volatility, SIAM J. Financial Math., 3, 163-181.

[2] R. Almgren and N. Chriss, (2000), Optimal execution of

portfolio transactions, J. Risk, 3, 5-39.

[3] S. Basak and G. Chabakauri, (2010), Dynamic mean-variance

asset allocation, Rev. Finance, 23, 2970-3016.

[4] M. Blais and P. Protter, (2010), An Analysis of the

Supply Curve for Liquidity Risk through Book Data, Int. J. Theor. Appl. Finance, 13, 821-838.

[5] M. Carhart, (1997), On persistence in mutual fund

performance, J. Finance, 52, 57-82.

[6] M. Christiansen and M. Steffensen, (2013), Determ inistic

mean-v ariance-optimal consumption and investment, Stochastics: An

International Journal of Probability and Stochastic Processes, 85(4),

620-636.

[7] E. Fama and K. French, (1993), Common risk factors in the

returns on stocks and bonds, J. Financial Economics, 33, 3-56.

[8] I. Kharroubi and H. Pham (2010), Optimal Portfolio

Liquidation with Execution Cost and Risk, SIAM J. Financial Math., 1,

897-931.

[9] R. Korn, Some applications of -hedging with a

non-negative wealth process, Appl. Math. Financ. 4(1) (1997), 64-79.

[10] R. Korn and S. Trautmann, (1995), Continuous-time

portfolio optimization under terminal wealth constraints, Z. Oper. Res.,

42(1), 69-92.

[11] C. M. Jones, G. Kaul and M. L. Lipson (1994), Transactions, volume, and volatility, Rev. Financ. Stud., 7, 631-651.

[12] C.G. Lamoureux and W.D. Lastrapes, (1997), Heteroskedasticity in stock return data: volume versus GARCH effects , J.

Finance, 45, 221-229.

[13] H.M. Markowitz, (1952), Portfolio selection, J. Financ.,

7(1), 77-91.

[14] P. Milgrom and N. Stokey, (1982), Information, Trade and

Common Knowledge, J. Economic Theory, 26, 17-27.

[15] S. Mudchanatongsuk, J.A., Primbs, W. Wong, (2008) Optimal

pairs trading: A stochastic control approach, American Control Conference,

1035-1039.

[16] W. Sharpe, (1964), Capital asset prices: a theory of

market equilibrium under conditions of risk, J. Finance, 3, 425-442.

[17] M. Suominen, (2001), Trading volume and information

revelation in stock markets, J. Financial and Quantitative Analysis, 36,

545-565.

[18] X. Zhou and D. Li, (2000), Continuous-time mean-variance

portfolio selection: A stochastic LQ framework, Appl. Math. Optim., 42,

19-33.