Computer-Supported Risk Identification for the Holistic Management of Risks

Abstract

Risk is part of the fabric of every business; surprisingly, there is little work on establishing best practices for systematic, repeatable risk identification, arguably the first step of any risk management process. In this paper, we present a proposal that constitutes a more holistic risk management approach, a methodology for computer-supported risk identification is proposed that may lead to more consistent (objective, repeatable) risk analysis.

1 Introduction

Pursuing any kind of business activity is inseparably interwoven with being exposed to different kinds of risk [4, 3, 5, 20, 10]: Is the customer I am dealing with liquid and honest, i.e. can I rely on being paid? Are my vendors delivering my supplies punctually, and to the quality I need? Am I in compliance with all applicable laws and regulations (commercial law, health & safety, financial reporting, tax, human resources etc.)? Are my products and services still relevant, or is demand shrinking or are markets disrupted by new inventions or commoditization of technologies? Are my competitors outperforming my product or undercutting my pricing? Does my business have the right staff in terms of skills? Am I setting the right priorities? Is the cash flow positive and are the profit margins acceptable? Am I exposed to currency exchange risk because many of my customers are in different currency zones? Are my offices in countries that are politically stable as well as free from natural disasters so that they can carry out their business activities in an undisturbed way?

The task of finding the comprehensive set of risks faced by an entity—its risk register—is known as Risk identification.

1.1 Motivation

Risk identification is the first step in any comprehensive risk management cycle, and to date it has been carried our for many several reasons:

-

•

The management of a business genuinely wants to learn about the risks that the business may suffer from, as part of business planning, project management [17] or strategic planning activities, or just for day-to-day operational use;

-

•

the business may be obliged to report risks to a regulator, for example in the case of U.S. public companies the Form 10-K filing must be annually submitted to the Securities and Exchange Commission (SEC), and it includes a section (“ITEM 7A. Quantitative and Qualitative Disclosures About Market Risk”) on risks [22];

-

•

before an acquisition or Initial Public Offering (IPO) material risks have to be formally disclosed to potential acquiring entities and potential investors/shareholders; or

-

•

a person looking for a job may want to learn about the risks of a potential employer before submitting a formal application to it, to ascertain the economic viability of the company and its the adherence to his or her ethical standards (or the other way round);

-

•

a bank may carry out a comprehensive risk analysis in order to establish whether or not to extend the credit line for a company that is one of their clients;

-

•

an investment manager may hold a portfolio of companies he or she has invested in, and may therefore want to ensure that the investment portfolio is risk-balanced: the less overlap there is in the kind of risks that the portfolio is exposed to, the better.

To date, there has been no automated tool support for the risk identification phase of the risk management process: traditionally, people have drawn up lists or spreadsheets of business risks from scratch by convening informal meetings, typical starting out with a blank sheet. The insufficiency of risk identification has been pointed out before, notably in the context of SEC filings, where risks are often obtained from competitors’ lists via copy & paste. This has a number of disadvantages. First, it is unlikely that a list created from scratch in one session is comprehensive. Second, the approach of making up the risk register in a meeting without looking at any data means the risk register will not be complete: very likely, the risks identified thus will only be the more obvious cases.

In this paper, we propose a technology that has the potential to provide the basis for a superior approach, a computer-supported risk identification process. It accomplishes this by supporting humans with automation help in eliciting evidence for risk exposure from archives and feeds of trusted prose text, such as news, earnings call transcripts or brokerage documents.

1.2 Definitions

A risk is a potential future event or situation that has adversarial implications; it is the possibility of something bad happening in the future. A bad event is when something that once was just a risk—whether it was recognized before or not—has materialized, i.e. it has actually happened. According to this terminology, a risk already incorporates a potential modality, and therefore it makes no sense to speak of a potential risk, as that is already implied in the risk term. Events can unfold, i.e. they can change their spatio-temporal scope, which may include other, dependent risks materializing in the process.

2 Risk Identification

2.1 Risk Identification as Part of Project Management

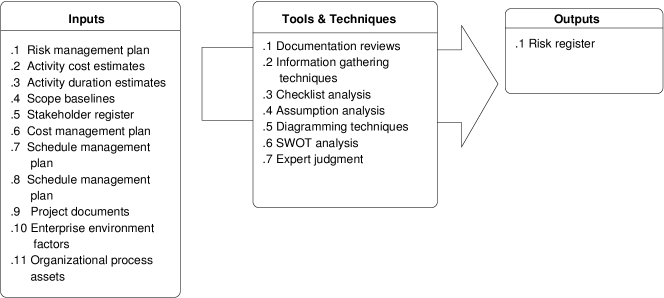

Traditional best practices for project management describe risk identification as an early step in a sequence of activities including Risk Management Planning, Risk Identification, Qualitative Risk Analysis, Quantitative Risk Analysis, Risk Response Planning and Risk Monitoring and Control [17]. However, while the importance of risk identification is acknowledged, automated tool support often is not addressed [12, 17].

The best practices in project management documented by the Project Management Institute (PMI) suggest the risk register be generated as output by a set of tools from a set of inputs (Fig. 1). “Participants in risk identification activities can include the following: project manager, project team members, risk management team (if assigned), customers, subject matter experts from outside the project team, end users, other project managers, stakeholders, and risk management experts.” [17, Section 11.2] Project documents and enterprise environmental factors are listed as inputs, and they include (ibd., partially cited):

-

•

Assumptions log

-

•

Other project information proven to be valuable in identifying risk

-

•

Published information, including commercial databases

-

•

Academic studies

-

•

Published checklists

-

•

Industry studies, and

-

•

Risk attitudes.

While some of these sources of evidence may include prose instances of risks, no mention is made of tool support to locate them. In this paper, we take the position that within large collections of text such as news archives, risk register elements can lie buried, and that we will need computer support to unravel them.

Kerzner (2009) recommends “surveys of the project, customer, and users for potential concerns” [12, p. 755], and gives a list of typical project risks; clearly as of its publication date, automatic tool support for risk identification was not yet on the horizon, and it is hoped that this paper will generate initial awareness in favor of automated or semi-automated methods to collect evidence from textual data.

2.2 Codification of Risk Identification in Standards

The International Organization for Standardization (ISO) and the International Engineering Commission (IEC) have produced a codification of terminology and best practices for risk management, including risk identification techniques [1, 2]. However, because the standard was issued in 2009, it predates first attempts to develop computerized tools to support the risk identification stage of the risk management process [14].

2.3 Three Aspects of a Risk

Key problems of risk management include (1) how to model risk, (2) how to obtain data for a chosen model so that it can be used in practice, and (3) what decisions to take based on the risks.

A risk basically has three properties to characterize it:

-

•

the risk type : a name for the description of the risk that characterizes the nature of the adversarial potential;

-

•

a likelihood : the estimated odds how likely the risk happens within a certain time frame (e.g. 6 months) or not;

-

•

its impact : if it materializes, what is the severity of the damage caused. This could be expressed as minimum, expected and maximum loss in USD, for example, akin to loss databases used by insurances.

We can write in short: . Unfortunately, the probability of an event and its impact are often confused by laypersons and experts alike. A particularly common error is to take the frequency of mention of a risk type as a proxy for its probability: while in some cases this makes sense, for example if there are increasingly frequent reports of political unrest coming from a country, this may indeed be suggestive of an imminent civil war or revolution, in many cases the frequent mention of a risk reflects a more extensive, detailed discussion, which may actually indicate less risk (well scrutinized means better understood). We will focus on the risk identification step in this paper; for risk likelihood assessment and impact assessment we refer the reader to the literature.

Regarding the modeling of risk, one of the easiest approaches is simply listing the risk types that a company is exposed to, the risk register (Figure 2(a)); at the most sophisticated end of the spectrum, complex mathematical graph-based models could simulate propagation of risk evidence, probabilities and causality through a graph-based model. The simple model does not help you forecast how likely what will happen, but it permits you to draw up a table of intended action to deal with each risk type. For the more complex models they may quantify probability111 The ratings “high”, “medium” and “low” in Figure 2(b) are given only for didactic purposes; a real assessment should quantify risk to avoid subjective differences in interpreation of these terms [8, pp. 491-513]. and impact, but it is often hard to obtain data for its parameters, and to validate its appropriateness as a model (are we modeling the world well?).

| Acme Inc. |

|---|

| Risk Type |

| office fire risk |

| cash-flow risk |

| litigation risk |

| demand risk |

| Acme Inc. | |||

|---|---|---|---|

| No. | Risk Type | Likelihood | Impact |

| 1 | office fire risk | low | high |

| 2 | cash-flow risk | medium | fatal |

| 3 | litigation risk | medium | high |

| 4 | demand risk | medium | high |

2.4 Evaluating Risk Register Quality

A risk register’s merit can be judged along a couple of dimensions:

-

•

comprehensiveness: does it contain all or at least most risks that the entity it pertains to is exposed to? This is difficult because in reality we do not have access to the complete universe of risks for an entity to compare to.

-

•

currency: does it contain the risks significantly before they materialize?

-

•

correctness: how correct are the risks in the risk register? This can be measured by Precision, the percentage of correct risks that are also present in the risk register. A risk can be deemed correct at different levels: at the most basic level, a risk is correctly included in a risk register for an entity e if the linguistic context from which the risk mention of r was extracted supports the inclusion decision. I.e., more human analysts would include, independently from each other, the risk in the risk register based on the evidence than those that don’t (human agreement is always an upper bound of machine performance, at least if machines are evaluated against a human “ground truth”, “gold standard” or “reference solution”).

-

•

cost: all things being equal, a risk register is better than another if it can be produced more cheaply than another.

In the absence of an “oracle” that provides the complete set of risks which could be used for an absolute evaluation, one work-around is to have multiple systems developed by different groups using different methods for risk identification, each producing their own risk register for any given entity. Then the set union of all of them could be formed and reviewed by human judges, to create a resource that will be defined as the gold standard, and against which also coverage and recall can be measured to accommodate the aforementioned “completeness” quality criterion. This methodology, known as pooling, has been applied successfully in the evaluation of search engines at the US National Institute of Standards and Technology (NIST) in the Text Retrieval Conferences (TREC).

2.5 Of Obvious Risks, Gray Swans and Black Swans

We can distinguish between three types of risks based on how surprised we would be if they materialized:222This is consistent with information theory’s view of surprise as information content (less surpising more predictible smaller information content).

-

•

Obvious risks333 Taleb also speaks of White Swans: “A White Swan for me would be a bridge that can only handle these trucks, of course, and you are certain because you have seen from a helicopter a few big six-ton trucks coming on the highway, and so you know the bridge is going to collapse, it’s only a matter of time.” [18] can be important to bring to one’s attention (when their materialization is imminent), but often we will want a filter to see only the not-so-obvious;

-

•

Gray Swans are defined by Taleb [20] as risks that are hard to anticipate because they are unlikely, and they may have huge impact once they materialize; and

-

•

Black Swan risks are defined by Taleb [20] as risks that cannot in principle be anticipated, they have a very low likelihood, yet their impact is enormous (black swans were believed not to exist until some very finally discovered). If there exists a class of risks that cannot by definition be anticipated, it naturally is outside of the scope of computer-supported techniques for detecting them (which is why we can focus on “gray swans” here).

3 “Risk Mining” from Textual Sources

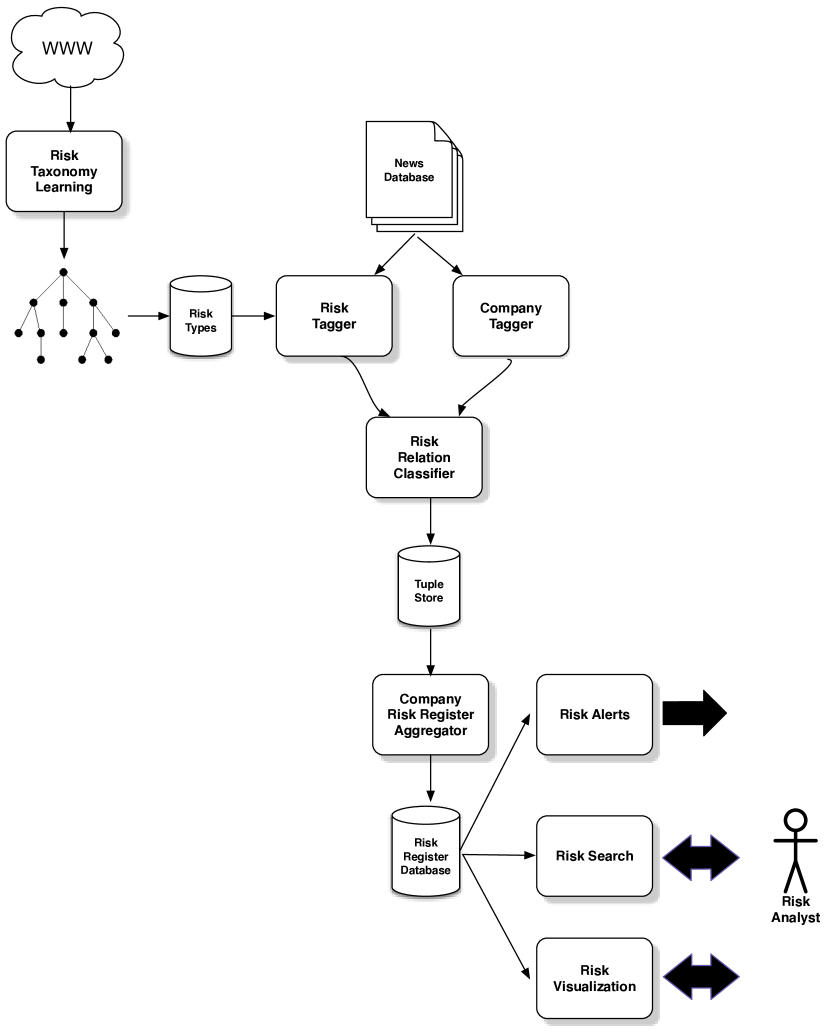

In this section, a method for computer-supported risk identification is described at the conceptual level (Figure 3); for more detail, see [14, 16].

The method takes three inputs: (i) the World Wide Web, as indexed by a search engine, (ii) a set of company names, the risks of which we are interested in (e.g. a list of suppliers or an investment portfolio) and (iii) a news archive comprising trusted news and analysis. The World Wide Web (WWW) is used to mine a taxonomy of risk types, regardless of the entity that is exposed to them; the WWW was chosen because it is the largest existing online source of English prose. The news archive is the source of information, from which we can extract the risks, essentially using journalists’ insights to “crowdsource” risk mentions from their reporting. The company list is the real (variable) input, and the output is a risk register for each company.

The method comprises of three steps: a taxonomy learning step, which is run at least once to obtain an inventory of possible names for risks, a tagging step in which company names and risk type names, respectively, are annotated in the text of the news feed and/or news archive (by simple look-up, or possibly by a more sophisticated process such as machine learning); and a classification step, in which a machine learning process decides whether a risk mention instance candidate pair comprising a company name mention and a risk type mention (co-occurring in the same sentence) are indeed related to each other, and that they indeed express a risk exposure situation.

3.1 Machine Learning of Risk Type Taxonomies

The first step in our method creates a taxonomy of risk terms or phrases, which we refer to as the risk taxonomy. Unlike human-created taxonomy, the output is very rich in detail, but messy, “by machines, for machines” in a way. We try to obtain a graph with as many IS-A relationships as possible and “risk” as its root node by remote-controlling a Web search engine with search queries for linguistic patterns likely to retrieve risk terms or phrases.

The method, desribed by Leidner and Schilder in more detail in [14], makes use of so-called “Hearst patterns” (“financial risks such as ” is likely to retrieve Web pages, in which this pattern is followed by “bankruptcy”, for instance) to induce a rich risk type vocabulary.

3.2 Tagging Company Names and Risk Type Names

Software to automatically annotate prose text with company names is easily available today. Popular methods are based on name dictionaries (gazetteers), linguistic rules and/or machine learning.

Likewise, terms and phrases from our risk taxonomy can be tagged or looked up in sentences.

At the end of this step, each sentence that contains a mention of a company

name and a risk type name has both marked up, which creates candidate pairs

(tuples). Note that the pair (Microsoft, fine) could be generated by

both these sentences, one correct and one incorrect (i.e., undesirable in a

risk mining context):

(a) Microsoft are facing a fine , said Bill Gates .

(b) I feel fine , said Microsoft ’s Bill Gates .

What we need is another step that filters out such false positives.

3.3 Machine Learning of Entity-Risk Type Relation Instances

In order to eliminate spourious false positives in our list of candidate risk exposure relationship tuples, we can use the method described in Nugent and Leidner [16] to classify each pair comprising a company name and a risk term or phrase, taking into account the sentential context in which they occur. For example, supervised machine learning is capable of distinguishing cases (a) and (b) in the previous section after a few hundred training sentences have been annotated by human experts to induce a statistical model from that generalizes the evidence provided in these.

3.4 Aggregating Risk Registers

Once risk company-relation mentions have been identified and stored, they can be aggregated so as to form the actual risk register. The naive way of doing this is by forming the set of all risk mention instance tuples for each company , i.e. to gather for all s to get the risk register for one company .

| Acme Inc. |

|---|

| Risk Type |

| office fire risk |

| cash-flow risk |

| copyright litigation risk |

| demand risk |

| Acme Inc. | |

| Risk Type | Count |

| office fire risk | 1 |

| cash-flow risk | 2 |

| copyright litigation risk | 1 |

| demand risk | 14 |

Note that a higher frequency indicates merely an increased number of mentions of a risk, which is not identical, but may in some cases be correlated with, a higher likelihood for the risk to materialize: a spike in mentions of “earthquake” is likely to result from imminent or actual earthquakes, but a spike in “acquisition” may or not preceed the acquisition of a company; some risks are less likely to materialize just because they are mentioned often, and that is because all public focus is on the topic, so the risk is at least not overlooked.

Once a risk register is aggregated, it can be shown to a human analyst for his or her perusal; however, it makes sense to regularly update the risk register as part of the Risk Monitoring and Control activity [17] based on new relationships mined that may not have been seen by the system before.

By retrieving mentions of risks related to companies, risk mining from text supports the three goals of risk measurement according to Coleman [7]: (1) uncovering “known” risks, (2) making the known risks easier to see, and (3) trying to understand and uncover the “unknown” or unanticipated risks.

3.5 Case Study: Starbucks Corporation

At the time of writing, Starbucks Corporation is a US-American coffee company that is operating coffee retail stores internationally. Civil unrest risk is perhaps not the most obvious risk type associated with this venture, yet our system, Thomson Reuters Risk IdentifierTM, included this risk type in Starbucks’ risk register. Was it an error? Well, the evidence showed that a Starbucks cafe was used by student protesters as a base to organize their demonstration. If you think about it, it makes sense, as the perfect place for organizing a demo is centrally located, has free wireless Internet access, and serves coffee.

Once this risk type is entering the radar of the corporate risk manager of Starbucks, they can act on it. There are many ways to handle the risk (either installing house rules that ban demo organizers, or embracing the student protesters by launching a campaign “We welcome the student revolution!”); the point is that it would be unlikely that this kind of risk could be conceived using traditional risk identification techniques (i.e., a boardroom meeting with an empty Excel spreadsheet).

4 Managing Identified Risks

Once the risk identification, likelihood and impact assessments have concluded, a risk management plan [17] should define the actions to be taken to influence the risks in the company’s favor (Figure 5).

| Acme Inc. | |

|---|---|

| Risk Type | Management |

| office fire risk | transfer (buy fire insurance) |

| cash-flow risk | mitigate (apply for credit line) |

| copyright litigation | mitigate (submit manuscripts to plagiarism checker) |

| demand risk | accept (do nothing) |

5 From Individual Risk to Risk Ecosystem

5.1 Individual vs Systemic Risk

Risks can be investigated in isolation; however, quite often, a chain of follow-up risks is conceivable. Risk-risk connections can be causal or correlated in nature: if a country is exposed to earthquake risk, then its citizen may be exposed to hygiene risk since it is likely that water pipes may burst. The propagation of risk functions regardless of the type of risk, from hygiene risks to financial risks.

In 1995, Barings Bank failed (caused by unauthorized trading by Nick Leeson, its head derivatives trader in Singapore) due to particular risks specific only to Barings (operational risk), whereas the 2008 failure of Lehman Brothers, AIG, and others was part of a systemic meltdown of global financial systems caused by bad risk management in the real estate and credit markets.444This example is taken from.[7, Chapter 1]

5.2 Risk Propagation Along The Supply Chain

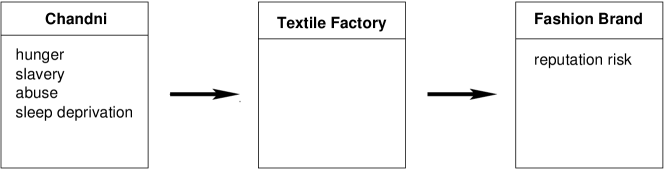

Imagine Chandni, a textile worker in an old but crowded factory building (“sweat shop”) in Bangladesh. At the time of writing, she earns $0.19 per hour, although she is only twelve years old. She is hungry and lacks sleep, but kept like a slave, forced to work long hours, and locked in the factory so she cannot leave. Figure 6 shows how Chandni’s personal risk register does not affect her direct employer much (if she dies, there will be another likely victim replacing her at the same cost), but the human rights violations she faces can become a reputation risk for the international fashion brand that subcontracted the textile factory that employs her.555While Chandni’s name is made up, the example was inspired by a documentary showing real cases similar to hers. Location, salary and work conditions are unfortunately not fictional.

The suicides of several employees of Foxconn (also known as Hon Hai Precision Industry Co., Ltd.), an electronics manufacturer that is a subcontractor for Apple Inc. (inter alia), has been a prime example of reputation damage by association. Foxconn was reported to exploit its workers, and some of them took their lives. This in turn caused outrage by Apple Inc.’s customers when reported by news media [19]666 The truth is often much more complex than journalistic headlines suggest; according to Wikipedia (“Foxconn”), the suicide rate of Foxconn is actually below national average in China. Note, however, that the fact whether or not Foxconn’s workers’ suicides is above or below national average does not undo the reputation damage Foxconn, and by implication Apple, suffered. .

Another example is a manufacturer of cars, which may source its engines from a vendor. The engine may contain spark plugs from yet another vendor. If the spark plug vendor produces a very customized version for the engine manufacturer that cannot easily be replaced, a cash-flow problem of the spark plug vendor may delay or even halt production for the car manufacturer if no alternatives can be sourced easily. The more remote and indirect in the supply chain graph the risk is from the company that is ultimately (transitively) exposed, the harder it is to anticipate the problem in the risk identification process. A solution could be the overlaying of risk registers onto the supply chain graph (Figure 7).

5.3 Risk Model and Real World

For risk modeling to work very well, it ought to be connected to the real world; in the risk case, such a “calibration” means the model is more grounded in physical reality, and that it is aligned with actual truth as opposed to mere predictions, which ultimately are a form of fiction. A risk model that is informed by real-life signals like loss databases (e.g. from the insurance sector), project management databases (as gathered by the project management offices in corporations) will compare favorable to one that is not linked to the business operation.

Ideally this connection between risk model and risk reality is bidirectional: the world informs the model, the model makes predictions, predictions are compared with real outcomes as risk do or do not materialize, and outcomes are fed back to improve models. For example, an identified cash flow risk could be measured legal by how small we permit cash reserves to become, and by comparing the current balance to the lowest previous low. Or, when identifying legal risk, we ought to measure actual legal services and litigation cost and feed it back into our model.

For an organization to be effective, risk modeling and risk management cannot operate separately from other parts of the business (financial, legal, operational departments).

5.4 Portfolio Risk

Given two publishing companies, Acme Inc. and Rainforest Publishing Inc., they will have very different risk registers (Fig. LABEL:fig:portof; they share the risks common to all publishing companies, but there will be a set of risks peculiar to individual companies based on their unique name (e.g. trademark violation risk), location (demand risk), pricing (competitive risk), kind of publications offered (sourcing risk, demand risk), advertising and marketing mix (operational risk), and so on.

Ed G. Reedy is an investment manager in charge of 250 million US$ investment assets. At any time, he holds a portfolio of securities (e.g. shares, options, forward contracts), which make him a stakeholder in the well-being, and therefore also in the risk exposure, of the underlying companies that make up his portfolio.

His portfolio comprises five companies, each exposed to a number of partly different, partly overlapping risks (Fig. 8), and it was assembled in a way that ensures the companies have high-growth potential, and their risk as far as “fundamentals” (financial base numbers like revenue, EBITDA etc.) are not strongly correlated [15]. Once we can look at the risk register for a company (after extracting it from news text using risk mining, and having the output vetted by a human analyst), we can scrutinize the portfolio risk based on the qualitative risk types (as opposed to scrutinizing it based on fundamentals-based correlation only) by looking at risk overlap, to get a different perspektive on risk.777 [21] suggests that including a diversity of sources of evidence (expert diversity) is one of the cornerstones of the best practices of forecasting.

| Risk A | Risk B | Risk C | Risk D | … | Risk J | Risk K | |

|---|---|---|---|---|---|---|---|

| Company A | ❚ | ❚ | |||||

| Company B | ❚ | ❚ | |||||

| Company C | ❚ | ❚ | |||||

| Company D | ❚ | ||||||

| Company E | ❚ | ❚ |

5.5 Collective Behavior and Regulatory Impact

Companies that pay only lip service to regulation (i.e., they do whatever is needed to formally comply in order to comply rather than in order to actually reduce the risk exposure of their company) are generating a spiral of ever-increasing regulatory oversight: because they have only a minimal interest in actual risk reduction, more new disasters happen. Then based on markets with dysfunctional self-regulation, regulatory bodies generate more and stricter regulations and impose them on companies. As a consequence, the cost of compliance is increased by an attitude of “mere compliance”. Of course, subsequent rounds of regulations will cause more expenses in order to meet even minimal compliance be compliant, which in turn re-inforces the “mere compliance” attitude further. This leads to a spiral of ever-increasing regulation that may put markets in a regulatory gridlock resulting in paralysis of the system (Fig. 9).

Therefore, it is crucial to implement risk management for its own sake, and not just to be compliant. This might require re-aligning, re-vitalizing or even re-building compliance functions. [6] points out the importance of culture change in implementing better risk management regimes.

Appendix A Some Notes on Traditional Axiomatic Probability Theory

The beginning of every kind of probabilistic modeling is the definition of the set of possible events that make up the total event universe , consistent with Kolmogorov’s axiomatization of probability [13]. For example, when dealing with probabilities of a series of throws of coins . However, it is an essential—even defining—property of each model to leave out parts of reality, and what exactly is included or not can vitally contribute to a model’s success. For example, a “better” (in the sense of more complete) model could include the—admittedly extremely rare—case that a coin lands on neither head nor tail, but on its side: . In the case of the toss of a coin, we may disagree on the utility of including more and more (very unlikely) cases888 The coin could land on its edge, or it could fall from the table. in the definition of the event space , but in risk identification in general, spanning up a very fine-grained or detailed universe or inventory of possibilities is actually crucial: if excluded, a hypothetical outcome cannot be even assigned any probability (not even ) in the later stages.

The traditional definition of is as a static set, and this

implies that either an omniscient vantage point is required for who defines

it, or there will be disastrous consequences of omission. An alternative way to

set up probability theory could conceivably define as a function of

time, which incrementally grows and also gets more fragmented as new evidence

(about what can happen) surfaces. Such a dynamic version of probability

theory, especially under a Bayesian999based on belief revision interpretation

of probability, could potentially account for “knowledge updates” of .

Imagine this sequence of events:

1. (Start):

2. A tossed coin lands on “Tail”

3. Another toss of the same coin produces “Head”

… (Lots of events, but always either “Head” or “Tail”)

1,000,000. Another toss of the same coin produces “Tail”

(i.e., no further updates of the set occurred). ❚

Acknowledgements

The author gratefully acknowledges discussions on the topic of risk with Frank Schilder, Khalid Al-Kofahi, Tim Nugent, Chris Brew, Shaun Sibley and Nayeem Sayed.

About the Author

Jochen L. Leidner, Ph.D. is a Director of Research with Thomson Reuters, where he heads up the R&D group in London. He holds a Ph.D. in Informatics from the University of Edinburgh, a Master’s in Computer Speech, Text and Internet Technologies from the University of Cambridge and a Master’s in Computational Linguistics, English Lanugage and Literature and Computer Science from Friedrich-Alexander Universität Erlangen-Nürnberg. Prior to Thomson Reuters, he held a Royal Society of Edinburgh Enterprise Fellowship in Electronic Markets for his work on mobile question answering at the University of Edinburgh. In the past, he also held roles as a software developer at SAP AG, and served as a paramedic with the German Red Cross. He is a certified project management professional (PMP) and member of PMI, IEEE, ACL and ACM.

References

- [1] ISO 31000:2009 — principles and guidelines on implementation, 2009.

- [2] ISO/IEC 31010:2009 — risk management — risk assessment techniques, 2009.

- [3] John Adams. Risk. Routledge, 1995.

- [4] U. Beck. Risk Society: Towards a New Modernity. Sage, Beverly Hills, CA, 1992.

- [5] Peter L. Bernstein. Against the Gods: The Remarkable Story of Risk. Wiley, 1998.

- [6] Philippe Carrel. The Handbook of Risk Management: Implementing a Post Crisis Corporate Culture. Wiley, New York, NY, USA, 2010.

- [7] Thomas S. Coleman. A Practical Guide to Risk Management Paperback. Research Foundation of CFA Institute, 2011.

- [8] Edmund H. Conrow. Effective Risk Management: Some Keys to Success. American Institute of Aeronautics and Astronautics, Reston, VA, USA, 2nd edition, 2003.

- [9] The World Economic Forum. Global Risks 2015 (10th edition). Technical report, WEF, Geneva, Switzerland, 2015. http://www.weforum.org/reports/global-risks-report-2015.

- [10] Gerd Gigerenzer. Risik Savvy: How to Make Good Decisions. Penguin, New York, NY, USA, 2013.

- [11] Witold J. Henisz and Bennet A. Zelner. The hidden risks in emerging markets. Harvard Business Review, 2010.

- [12] Harold R. Kerzner. Project Management: A Systems Approach to Planning, Scheduling, and Controlling. Wiley, 10th edition, 2009.

- [13] A. N. Kolmogorov. Grundbegriffe der Wahrscheinlichkeitrechnung. Ergebnisse Der Mathematik. Springer, 1933. Translated as Foundations of Probability, New York: Chelsea Publishing Company, 1950.

- [14] Jochen L. Leidner and Frank Schilder. Hunting for the Black Swan: Risk Mining from text. In Proceedings of Annual Meeting of the Association for Computational Linguistics (ACL), pages 54–59, Uppsala, Sweden, 2010. ACL.

- [15] Allan M. Malz. Financial Risk Management: Models, History, and Institutions. Wiley, Hoboken, NJ, USA, 2011.

- [16] Tim Nugent and Jochen L. Leidner. Computer-supported risk identification with a taxonomy learner and a company-risk relation classifier. N.N., in prep.

- [17] PMI. A Guide to the Project Management Body of Knowledge (PMBOK Guide). The Project Management Institute Inc. (PMI), Newtown Square, PA, USA, 5th edition, 2013.

- [18] Jessica Pressler. Nassim Taleb: There are actually three types of swans. New York Magazine, 2010. (online) cited 2015-10-01, http://nymag.com/daily/intelligencer/2010/06/nassim_taleb_there_are_actuall.html.

- [19] Jonathan Standing. Hon Hai to raise China wages after spate of suicides. Reuters News, 2010. (online) cited 2015-10-01, http://www.reuters.com/article/2010/05/28/us-china-foxconn-death-idUSTRE64Q14420100528.

- [20] Nassim Nicholas Taleb. The Black Swan: The Impact of the Highly Improbable Hardcover. Allen Lane, 2007.

- [21] Philip Tetlock and Dan Gardner. Superforecasting: The Art and Science of Prediction. Crown, 2015.

- [22] U.S. Congress. Securities Exchange Act of 1934. 15 U.S.C. § 78a et seq., 1934.