A queueing/inventory and an insurance risk model

Abstract.

We study an -type queueing model with the following additional feature.

The server works continuously, at fixed speed, even if there are no service requirements.

In the latter case, it is building up inventory, which can be interpreted as negative workload.

At random times, with an intensity when the inventory is at level ,

the present inventory is removed, instantaneously reducing the inventory to zero.

We study the steady-state distribution of the (positive and negative) workload levels

for the cases is constant and .

The key tool is the Wiener-Hopf factorisation technique. When is constant, no specific assumptions will be made on the

service requirement distribution. However, in the linear case, we need some algebraic hypotheses concerning the

Laplace-Stieltjes transform of the service requirement distribution.

Throughout the paper, we also study a closely related model coming from insurance risk theory.

Keywords: M/G/1 queue, Cramér-Lundberg insurance risk model, workload, inventory, ruin probability, Wiener-Hopf technique.

2010 Mathematics Subject Classification: 60K25, 90B22, 91B30, 47A68.

1. Introduction

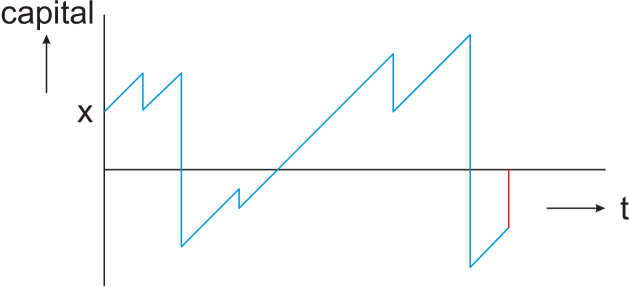

In this paper, we study two related stochastic models: a queueing/inventory model and an insurance risk model. The insurance risk model is a relaxation of the classical Cramér-Lundberg model. Unlike that model, when the capital of the insurance company becomes negative, the company continues to operate in the same way. However, during periods of negative surplus, the company can go bankrupt. It goes bankrupt according to some bankruptcy rate when the negative surplus equals ; see Figure 1.

This relaxation of the ruin concept was introduced in [3], and studied in [5] for exponential claim sizes and various bankruptcy rates. One of our goals in the present paper is to extend some of the results in [5] to general claim size distributions. In particular, we aim to study the bankruptcy probability when starting at , for both positive and negative values of .

It is well-known that the Cramér-Lundberg model is dual to the queueing model with the same arrival rate and with a service time distribution that equals the claim size distribution in the Cramér-Lundberg model. More precisely, cf. [6], p. 52: The probability of ruin in the Cramér-Lundberg model with initial capital equals the probability that the steady-state virtual waiting time (or workload) in the queue exceeds . This has led us to think about queueing models that are relaxations of the queue in a similar way as the Albrecher-Lautscham bankruptcy model is a relaxation of the Cramér-Lundberg model; see also [2].

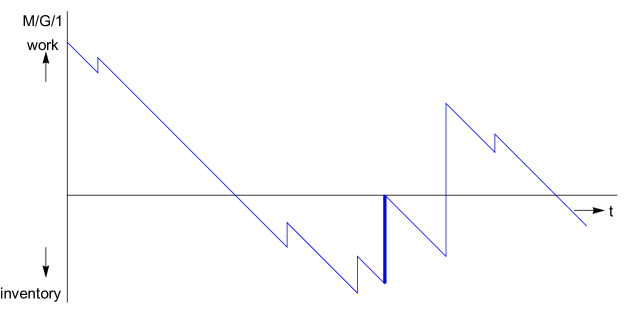

In this paper we study the following queueing/inventory model. Customers arrive according to a Poisson process, and require i.i.d. service times. When there are customers, the server works at unit speed. So far, this is the setting. However, when there are no customers, the server still keeps on working at the same speed. In that way, it is building up inventory. During periods in which there are no customers, inventory is instantaneously removed according to a Poisson process with rate when the amount of inventory equals . That inventory is, e.g., sold. The server just keeps on working; and when a customer arrives and its service request can be satisfied from the inventory, then that is done instantaneously. See Figure 2. In [2] this two sided queueing/inventory model has been analysed for the case of exponentially distributed service times. Our queueing/inventory model is related to classical and inventory models. An important inventory model is the basestock model, in which a server produces products until the inventory has reached a certain basestock level, with requests for products arriving according to a Poisson process. A request that cannot immediately be satisfied joins a backorder queue. However, that model has a finite basestock level, and hence essentially differs from our model. Two papers which are to some extent related to our paper are [7] and [13]. These consider a production/inventory model with a so-called sporadic clearing policy. The system is continuously filled at fixed rate, and satisfies demands at Poisson epochs. Under the sporadic clearing policy, clearing of all inventory takes place at a random time (which in [13] is independent of the content process). The authors obtain explicit results for an expected discounted cost functional. [13] allows the demands to have a general distribution, whereas these are exponentially distributed in [7].

The main contributions of our paper are (i) an exact analysis of the Albrecher-Lautscham bankruptcy model and the queueing/inventory model, with generally distributed claim sizes, respectively generally distributed service requirements, for the case of ; and (ii) a detailed analysis of the queueing/inventory model for the case of . The latter case turns out to lead to an inhomogeneous first order differential equation with removable singularities, and its analysis gives rise to intricate calculations that are given in an appendix. A key tool that we are using in the analysis of the two models is Wiener-Hopf factorization. The results of the present paper might be used for optimization purposes; for example, one might try to choose or (in the case ) such that a particular objective function is optimized.

The paper is organized as follows. The queueing/inventory and insurance risk model are both described in detail in Section 2. Integral equations for the main performance measures (workload and inventory densities in the queueing/inventory model, bankruptcy probability when starting at level in the insurance risk model) are presented in Section 3. In Section 4 these equations are solved for and general service requirement distribution, respectively general claim size distribution. The queueing/inventory model is treated in Section 5 for the case . That analysis makes use of Laplace transforms and complex analysis. We assume that the service requirements having a rational Laplace transform; see also the appendix, that is devoted to a detailed exposition of technical complications which arise when one tries to determine the Laplace transform of the density of the inventory level by solving a first order algebraic differential equation with singularities. Section 6 considers that very same case, under the assumption of exponentially distributed service requirements, without resorting to Laplace transforms.

2. Model description

2.1. Queueing/inventory model

We study the following model (cf. Figure 2). Customers arrive according to a Poisson process with rate . Their service requirements

are independent, identically distributed random variables with common distribution and LST (Laplace-Stieltjes Transform)

. The server works continuously, at a fixed speed which is normalized to - even if there are no service requirements. In the latter case, the server is building up inventory, which can be interpreted as negative workload. At random

times, with an intensity when the inventory is at level , the present inventory is removed, instantaneously reducing the inventory to zero. Put differently, inventory is removed according to a Poisson process with a rate that depends on the amount of inventory present.

Denote the required work per time unit by . We assume that . This ensures that the steady state workload distribution exists. Let , denote this steady-state workload distribution, and its density.

During the times in which the inventory level is positive, there is an upward drift of that inventory level; but when

for sufficiently large, the inventory level will always eventually return to zero, and the steady-state inventory distribution will exist.

Let , denote this steady state distribution, and its density.

2.2. Insurance risk model

The problem that we will deal with here was introduced by Albrecher, Gerber and Shiu [3] and investigated by Albrecher and Lautscham in [5]. We will examine the bankruptcy probability for a surplus process with jumps. Consider a Cramér-Lundberg setup to describe the insurer’s surplus at time as

| (1) |

where is the initial surplus, is the premium rate, and is the aggregate claim amount up to time modeled as a compound Poisson process with intensity and positive jump sizes with cumulative distribution function . In order to compare the results for the bankruptcy model with those for the queueing/inventory model, we shall take , so its LST is . It is assumed here that the insurer may be allowed to continue the business despite a temporary negative surplus. Concretely, consider a suitable locally bounded bankruptcy rate function depending on the size of the negative surplus . If no bankruptcy event has occurred yet at time , then the probability of bankruptcy in the time interval is . We assume that and for to reflect that the likelihood of bankruptcy does not decrease as the surplus becomes more negative. Let be the resulting time of bankruptcy, and define the overall probability of bankruptcy as

| (2) |

The idea is that whenever the surplus level becomes negative, there may still be a chance to survive, and survival is less likely the lower such a negative surplus is.

For , set , and .

3. Main equations

In this section we present integral equations for the main performance measures (workload and inventory densities in the queueing/inventory model, bankruptcy probability when starting at level in the insurance risk model).

3.1. Queueing model

The level crossing technique [8] yields the following integral equations for the workload and inventory densities, by equating the rates at which level is downcrossed and upcrossed in steady state:

| (3) |

| (4) |

We introduce the Laplace transforms and for . Multiplying both sides of (3) with for and both sides of (4) with for , integrating and adding both equations gives, after some calculations:

| (5) |

3.2. Insurance model

According to [5], one can write

| (6) | |||||

| (7) |

Adding and subtracting , Equation (7) is equivalent to

| (8) |

One can dominate the function

by the classic ruin function and under assumptions on the existence of the second moment of , the classic ruin function

is integrable. Hence, the function is integrable. Similarly, one can argue that the function is integrable.

For , introduce the Laplace transforms

,

and .

Multiply both sides of (6)

with for and both sides of (8)

with for ; integrate and add

both equations for . After some calculations and using the fact that the continuity

of the function in zero implies , we obtain:

In the next section, we restrict ourselves to the case where the function is constant.

4. Analysis for constant

4.1. Queueing model

Assume in this section that the function introduced in Subsection 2.1 is constant, i.e., there exist such that for all , one has . Equation (5) becomes

| (10) |

We are going to determine both unknown functions and for by formulating and solving

a Wiener-Hopf problem (cf. [9]). A key step in this procedure is to rewrite Equation (10) such that the lefthand side is

analytic on and the righthand side is analytic on . Liouville’s theorem can subsequently be used

to identify the lefthand and righthand side.

Set

and .

According to [10] p. , the constant being positive, the function has only one zero

and this zero is simple satisfying .

In fact, as is real in our case, a plot of versus immediately shows that this zero is real.

Also, the function has as its only zero and this zero is simple. In particular the functions

and are analytic on , continuous on and take non-zero values on .

One can rewrite Equation (10) for as:

| (11) |

We now use the Wiener-Hopf factorization technique. The lefthand side of (11) is analytic on and continuous on ; the righthand side is analytic on and continuous on . In addition, both sides coincide on . Then by Liouville’s theorem (cf. [15], p.), there exist and a polynomial of degree such that:

| (12) | |||||

| (13) |

Using Equation (12) and the fact that , one has ; say where . One gets

| (14) |

in particular

| (15) |

On the other hand, Equation (13) yields

| (16) |

After some calculations and using the notations introduced above and Equation (15), one gets

| (17) |

We now calculate the unknown constant , and through Relations (15) and (17) we determine the functions and . Note that , therefore one can write for :

| (18) |

the function clearly being analytic for and continuous for

.

One has

| (19) |

But

| (20) |

One also has . Then,

| (21) |

Using the relation , and Equations (15) and (21), one gets

which implies

| (22) |

Finally we obtain the following expressions for for and for for :

| (23) | |||||

| (24) |

One imediately sees that the density is exponential:

| (25) |

One can rewrite the expression for in the following form:

| (26) |

Remark. The previous formula expresses the function as a product of the Laplace transform of the density of the M/G/1 workload, viz., and a second factor. That fact has led us to the observation that the queue behaves like an M/G/1 queue with different first service time in a busy period (cf. Welch [16] or pages 392-394 and 401 of Wolff [17]). Let us explain this in some detail.

When restricting ourselves to the time intervals with a positive workload in the queue, behaves like the workload density in an queue with Poisson() arrival process and with i.i.d. service times with distribution and LST , but with the first service time of each busy period having a different distribution with LST . Indeed, is distributed like the overshoot above of a service time , when starting from some negative value which, by PASTA, has steady-state density . In fact, it is easy to determine , since is exponentially distributed with parameter , as seen in (25). For simplicity of notation, we write . Then

| (27) | |||||

and

| (28) |

From [16] or p. 401 of [17] it is seen that the LST of the steady-state workload (and waiting time) distribution in this queueing model with exceptional first service is given by

| (29) |

with the probability of an empty system, and hence

| (30) |

A balance argument, or the observation that the expressions in (30) should equal for , and that the Laplace-Stieltjes transforms of the residual ordinary service time and of the residual special service time equal for , readily yields that

| (31) |

It readily follows from (28) that here

| (32) |

Now compare (30) and (24). We claim they agree up to a multiplicative constant, which is . Indeed, one can rewrite the term between square brackets in (24) as (replace by , using the fact that , which follows from the definition of as the zero of ),

| (33) |

Now use relation (28)

to see that the factor between square brackets in (33) equals

the factor

in (30).

Remark. It may at first sight seem surprising that is an exponential density. The fact that is exponential may be explained as follows. Consider the inventory process, so look at Figure upside down (“process ”). Next, consider this figure (now reproduced as the top figure in Figure ) by looking from right to left (“process ”). Subsequently, replace the line segments that go up at an angle of 45 degrees by upwards jumps equal to the increase along the line segment; and replace the jumps downward by line segments that go down at an angle of 45 degrees, by an amount equal to the jump (“process ”; see the bottom figure in Figure ). One now has the representation of the workload process in a busy period of a queue. Indeed, the jumps upward (service times) are exp() distributed, and the intervals between jumps have distribution . Notice in particular that the waiting times in the queue are identical to the heights after jumps in process . By PASTA, these heights have the same distribution as the steady-state workload distribution in process , and hence also in process . Finally use the fact that the waiting time in the queue is exponentially distributed.

Example 4.1.

Exponential service requirements in the queueing/inventory model

We will keep the same notations as previously.

In this case, one has with and

for , ;

, .

The functions and in this case are given by

| (34) |

The function has two zeros:

The functions and are then given by

| (35) |

is given by Equation (22). The function for is given by (25), so:

Using Relations (18) and (35), and after some calculations, one gets for :

| (37) |

Consequently, one can deduce for :

| (38) |

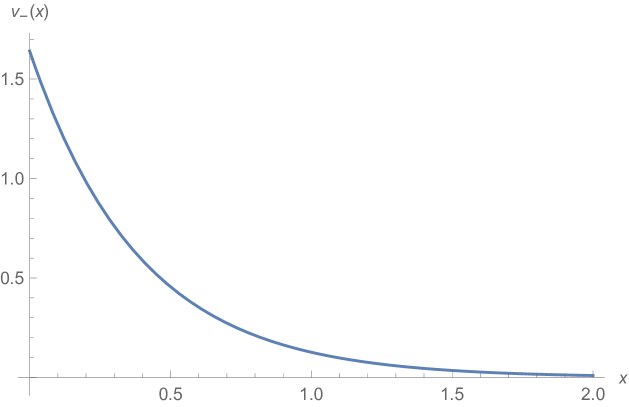

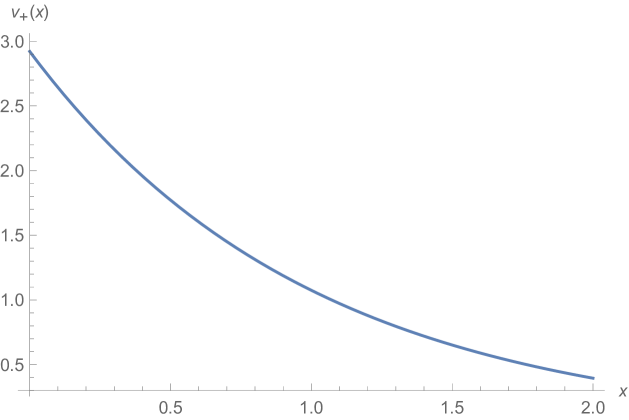

The following figures represent respectively the steady state inventory density and the steady state workload density , in the exponential service requirements case for the particular values and .

4.2. Insurance model

We now turn to the insurance risk model with bankruptcy. Equation (3.2) becomes, for :

| (39) |

In particular, when in (39), one has , which implies

| (40) |

We follow the same procedure as in the queueing/inventory model: We reformulate Equation (39) into a Wiener-Hopf problem. Set and . According to [10] p. , the constant being positive, the function has one zero and this zero is simple satisfying . Also, the function has as its only zero and this zero is simple. In particular the functions and are analytic for , continuous for and take non-zero values on . Dividing by and multiplying by in (39), one gets for :

| (41) | |||

Clearly, the lefthand side of (41) is analytic for and continuous for ; on the other hand, the righthand side is analytic for and continuous for . In addition, both sides coincide for . By Liouville’s theorem, there exist and a polynomial of degree such that

| (42) | |||

| (43) |

Since and using Equation (43), we can deduce that must be ; say . Consequently, one has

| (44) | |||||

| (45) |

In particular, Equation (45) implies

| (46) |

Let us now identify the constant .

Set

Plugging in Equation (39) and combining it with Relation (46), one gets

| (47) |

thanks to Equation (45), the latter relation completely determines the function for . In this case, one can immediately deduce , which is the survival probability when starting at a negative surplus , and so also the ruin probability . One has for ,

| (48) |

Finally, since the constant is known, we can identify the function for . Rewriting Equation (44), one has

| (49) |

Set , so . Equation (47) implies that . Then one has

| (50) |

the function being analytic for , continuous for

with .

The Laplace transform of the survival probability when starting at a positive surplus , given by the function ,

equals:

| (51) |

Example 4.2.

Exponential claim sizes in the insurance model

We will keep the same notations as previously. Fix .

In the exponential claim sizes case, we assume claim size density

, and hence

In particular . In this case, one obtains

| (52) |

This function has two zeros:

Therefore,

| (53) |

Applying Equation (47), one gets

| (54) |

Using the relation between the zeros and ,

one obtains

| (55) |

Applying Equation (48), one gets for ,

| (56) |

These results agree with results of Albrecher and Lautscham in [5], Section 2.1.1. To explicitly determine the function as given in (50), and so , one has to make the function explicit in this case. After some calculations, one gets for ,

| (57) |

One now can use Equation (50) and deduce for

| (58) |

Notice here that the condition is equivalent to . Finally, one obtains for :

| (59) |

Note that using equations (56) and (59), one can check immediately that .

Furthermore, note that

(56) and (59)

coincide with Formula (18) in [5].

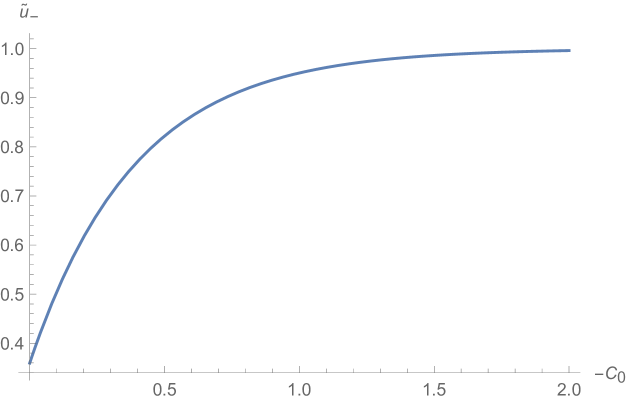

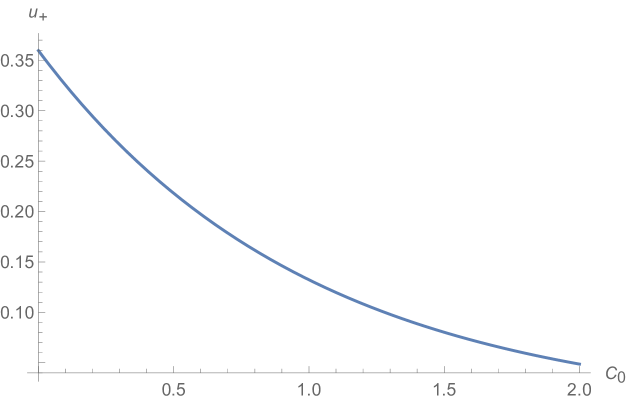

The following figures represent respectively the bankruptcy probability starting from a negative surplus against the initial surplus

and the bankruptcy probability starting from a positive surplus against the initial surplus , in the exponential claim sizes case for the particular values and .

Remark 4.3.

The queueing/inventory and insurance risk models that we treat in this paper are clearly closely related, although they are not dual in the sense discussed in, e.g., Section III.2 of [6]. The results that we obtain for the densities and their Laplace transforms are indeed very similar; cf. Equations (24) and (49), and (25) and (48). It would be interesting to construct a queueing/inventory model that is completely dual to the insurance risk model.

Remark 4.4.

Albrecher and Ivanovs [4] have recently studied exit problems for Lévy processes where the first passage time over a threshold is detected either immediately (’ruin’) or at Poisson observation epochs (’bankruptcy’). They relate the two exit problems via a nice identity. In the case of the Cramér-Lundberg insurance risk model, their identity reads as follows:

| (60) |

where is the survival probability in the case of the Cramér-Lundberg model with initial capital

and is the survival probability in the corresponding model

with Poisson() observations (notice that );

finally, is an exp() distributed random variable, where is the inverse of the Laplace exponent

of the spectrally negative Lévy process corresponding to the Cramér-Lundberg model. In other words,

is the zero of . We conclude that .

It follows from (60) that

| (61) |

When is explicitly known, then one can determine explicitly using (61). In particular, in the case of exp() claim sizes, one has (cf. [6])

| (62) |

and hence

| (63) |

Using the definition of , it is readily verified that this formula is indeed in agreement with the expression for in (59).

5. Analysis for linear

In this section we focus on the queueing/inventory model. We assume in this section that the function introduced in Section 2.1 is linear, i.e., there exists a constant such that for all , one has

| (64) |

Equation (5) becomes

| (65) |

Set . After integrating by parts, one gets

| (66) |

We will discuss here the case where the function is rational: suppose that there exist and polynomials and in such that , , , i.e they do not have a common factor and . In this configuration, necessarily, the polynomial has no zeros for and zeros for (counted with multiplicities). Denote them by with . Set and for , where and are complex numbers. Notice that implies that . Multiplying Equation (66) by , one obtains for :

| (67) |

Using the same techniques as previously, one can deduce that there exists a polynomial such that

| (68) | |||||

| (69) |

Since and using Equation (68), one can deduce that

.

Equation (68) implies that . Hence set for , where .

It follows from (68) that

| (70) |

Using Equation (70), one can also express in . Indeed

| (71) |

Since , one can also deduce

| (72) |

Notice that by plugging for in Equation (69), one gets the relations

| (73) |

For , introduce the following notations: , and . Now, putting in Equation (69), the function is a solution of the following first order differential equation:

| (74) |

One can write the previous equation in the following form:

| (75) |

Equation (73) implies that the function is analytic on and continuous on . Equation (74) is a first order algebraic differential equation on the complex half plane . It has m singularities ; Relation (75) shows that these singularities are removable.

In principle one can solve this first order algebraic differential equation. However, the singularities give rise to several technical difficulties. Below we consider the case , i.e., distributed service requirements, yielding one singularity . In Subsection 5.1 we sketch its analysis. We formally solve the differential equation (75) only for , where is the singularity. We also determine the two missing constants and . In addition, we formally invert the Laplace transform to find , but this inversion is not considered in detail.

In the appendix we treat the solution of differential equation (75) in much more detail. We consider both the case (Subsection 7.1) and the case (Subsection 7.2), and we determine the two missing constants and . It turns out that the value of plays a key role in the analysis. One has to distinguish the case of non-integer (consider , for each ) and the case of integer . In the latter case, we also invert , finding an explicit expression for in terms of Hermite polynomials. We have included the appendix because it exposes both a series of technical difficulties – even for the case of just a single singularity – in handling differential equation (75) as well as a mathematical approach to handle such difficulties.

In Section 6 we briefly outline a completely different approach to the problem of finding and for the case and exp() service requirements. In that section we do not use Laplace transforms, but differentiate (4) twice to get a second order non-linear differential equation in , and we differentiate (3) once to get a simple first order differential equation in . The latter equation is easily solved; the solution of the former differential equation is expressed in hypergeometric functions. For integer, this hypergeometric function reduces to the Hermite polynomial found in Subsection 7.8.

Finally, we should add that we do not see how the approach in Section 6 can be extended to the case of an Erlang, hyperexponential or, more generally, phase-type service requirement distribution, as such distributions will give rise to a higher-order non-linear differential equation for . On the other hand, the approach of the appendix towards the differential equation (75) seems promising for such service requirement distributions, even though they give rise to multiple singularities .

5.1. The Exponential service requirements case

In this case, one has with and for , ( and ). Then and since , we obtain that where . Equation (74) becomes

| (76) |

Equation (76) is a first order algebraic differential equation on the complex half plane . It has one singularity which is . That makes the study of this differential equation more complicated; therefore, in this paper, we dedicate an appendix to a further study concerning this differential equation. Remembering that and writing Equation (76) in the following form:

| (77) |

one deduces that this singularity is regular. Solving Equation (76) on , using the fact that , one gets

| (78) |

(notice here that for every , we consider the principal value of the function ). For , we introduce . The function is analytic on and one can check by the l’Hopital rule that the function can be analytically continued in for . Now fixing , Equation (78) can be written as follows:

| (79) |

We will denote by the inverse Laplace transform, and apply what is commonly known as Mellin inverse formula or the Bromwich integral: let be any real number such that , then one has

| (80) |

Since the constant here is chosen to be larger than , one can use the expression of given in Equation (79). Set . One gets

| (81) |

Integrating the previous equation, one obtains where . According to Relation (72), one has , and hence

| (82) |

Set ; multiplying Equation (81) by , integrating it and remembering the fact that , one obtains

| (83) |

Thanks to Relations (82) and (83), one can deduce the constants and ; using Equation (81), one can then completely determine the function .

Finally, using Equation (70), we obtain

| (84) |

It is not surprising that the density of the workload, when positive, is exponentially distributed

with the same rate as in the corresponding queue (arrival rate , service requirements exp())

without inventory.

Indeed, every time the workload becomes positive, this occurs because of a customer arrival, and the memoryless property implies that the

residual part of the service requirement which makes that workload positive is distributed.

6. Direct approach

In this section, we use the analysis developed in [2] to state some explicit results when in the exponential service requirements case. In [2], the authors study directly the functions and without considering their Laplace transforms. Indeed, differentiating Equations (3) and (4), one can show that the functions and satisfy some well known differential equations.

Set . Differentiating Equation (3), one has

| (85) |

This is in agreement with (84), which we obtained following a Laplace transform approach. On the other hand, differentiating Equation (4), one gets the following equation for :

| (86) |

Now, differentiating the expression in Equation (86), the function satisfies the following second order differential equation

| (87) |

Introduce the function . The function is a solution of Equation (87) if and only if the function is a solution of the following second order differential equation:

| (88) |

One can check that is a solution of Equation (88) if and only if where and and is a solution of the degenerate hypergeometric equation:

| (89) |

According to [11] (page 322) and [12] (page 143), Equation (89) has two standard solutions denoted by and , the so called Kummer functions. Provided that , the function is given by

where . The function is uniquely determined by the property when goes to . In our case (), one has

| (90) |

The following analysis is developed in detail in [2], using knowledge of the degenerate hypergeometric equation (see for example [11] page 322). It appears that one needs to distinguish between two cases:

Case : i.e .

Denote by

In this case, according to [2], one has

| (91) |

where . Relations (85) and (91) imply that to determine completely the functions and , it is enough to determine the constants and . According to [2], these constants are given by the following system of equations:

| (92) | |||

| (93) |

In particular, if is odd, i.e. , where , from [2], one has

| (94) |

where, for , is the Hermite polynomial of order (see [1], Page 775) given by the formula

.

Case : i.e. .

In this case, according to [2], one has, for all ,

| (95) |

where . Furthermore, similarly to case , one can find two linear equations involving the unknowns and and then determine them. One can see that Equations (94) and (95) have the same shape. Notice that Equation (95) coincides with Equation (163), the latter one being obtained in the appendix by a different method.

7. Appendix: Analysis of first order differential equation

We consider the differential equation (76)

| (96) |

where are known positive constants with , and and are unknown. It was argued in Section that is the Laplace transform of a non-negative, integrable function , , with . Hence, is continuous, positive for and analytic in the half plane for . Furthermore, as . The objective is to compute and and to determine , from this information and from the fact that

| (97) |

The first equality in (97) follows directly from (96) by setting , and the second one follows from Equation

(72) (see Section 5).

The standard calculus solution,

| (98) |

of the problem

| (99) |

with

| (100) |

is awkward to use since Equation (96) gives rise to functions and that are non-integrable around . Below, we will use a dedicated form of the standard solution, separately on the ranges and .

7.1. Considerations for

We let

| (101) |

where the series converges for . It follows easily from the fact that is the Laplace transform of an integrable non-negative function that all . With notation (101), Equation (96) becomes

| (102) |

where the auxiliary quantities and are defined by

| (103) |

From Equation (102), there follows the recursion

| (104) | |||||

| (105) | |||||

| (106) |

We set

| (107) |

where is such that

| (108) |

i.e., From Equation (102), we have that

| (109) |

Therefore, Equation (102) can be rewritten as

| (110) |

Writing the functions , and that occur in Equation (110) in terms of and , a careful administration with the recursion in Relations (104-106) gives

| (111) |

Observing that and dividing Equation (111) by , we get

| (112) |

The right hand side of Equation (112) is integrable at because of the choice of in Equation (108). Hence, the formula (98) can be used with and , where we note that

| (113) |

This yields for :

| (114) |

and for :

| (115) |

where

| (116) |

and

| (117) |

with a constant when . Also, observe from Equation (108) that in Equations (116-117).

7.2. Considerations for

We now let

| (118) |

where and we set

| (119) |

With a similar analysis as in Subsection 7.1, we get for :

| (120) |

and for :

| (121) |

where

| (122) |

and

| (123) |

with a constant when

7.3. Boundary condition at

7.4. Boundary condition at

7.5. Rewriting all unknowns in terms of

We have from Equations (103) and (104-105)

| (131) |

and so

| (132) |

Furthermore, from the first item in Equations (103) and (104),

| (133) |

We next use the recursion in Equation (106) in backward order to write all in terms of where for the case that , we have by equations (128), (130),

| (134) |

We find

| (135) |

where the are given recursively according to

| (136) |

with and given in Equation (134).

7.6. Solving for and finding and

We have from Equations (116-117)

| (137) |

where the term with vanishes when , and

| (138) |

The right-hand side of Equation (126) can then be written as

| (139) |

where

| (140) |

For the left-hand side of Equation (126) we use Relation (133) and we bring the term to the right-hand side. Then using and treating the term with separately, we find for Relation (126)

| (141) |

In Equation (141), all quantities in the parentheses are known, and so we have found . Then, with Equations (134) and (135) all can be found, and, finally, Equation (132) yields and .

7.7. Special attention for the case

When , we can find and from Equations (141) and (134). We note here that

| (142) |

With , see Equation (108), we then get

| (143) |

| (144) |

Finally, and is obtained from Relation (132) as

| (145) |

From and

| (146) |

we see that Equation (144) yields that both quantities in Relation (146) are between and (see Equation (97)).

In the case that , we have that , and we get consequently

| (147) |

| (148) |

| (149) |

7.8. Laplace transform representation of when

In the case that , we have from Subsection 7.2 that

| (150) |

From Equation (130) and , we find

| (151) |

and this yields

| (152) |

By analyticity of in and the right-hand side in , we have that Equation (152) holds for all . We manipulate now the right-hand side of Equation (152) to find as the Laplace transform of a non-negative function – which of course is . With and , we have from Equation (122)

| (153) |

Therefore,

| (154) |

where for the second step the substitution has been made. Setting

| (155) |

we thus have for

| (156) |

From basic properties of the Laplace transform, we have

| (157) |

for Hence, by Newton’s binomium for we get

| (158) |

where is a polynomial. Since and the integral at the right-hand side of Equation (158) go to as we have . It is a consequence of the formula

| (159) |

and the generating function

| (160) |

of the Hermite polynomials that

| (161) |

Then using that we finally obtain

| (162) |

where

| (163) |

This displays in the form of a Laplace transform, and we have found which equals . One can notice that Equation

(163) agrees with the result obtained previously in Equation (95).

From

| (164) |

we see that in Equation (163) is positive for . Here we have used [14], Theorem 6.32 on pp that implies

that the largest zero of is less than .

Acknowledgment

The authors gratefully acknowledge stimulating discussions with Hansjoerg Albrecher.

The research of Onno Boxma was supported by the NETWORKS project, which is being funded by the Dutch government. The research of Rim Essifi

was supported by the ERC CritiQueue program.

References

- [1] M. Abramowitz and I.A. Stegun (1968). Handbook of Mathematical Functions (5th ed.). Dover Publ. Inc., New York.

- [2] H. Albrecher, O.J. Boxma, R. Essifi and R.A.C. Kuijstermans (2015). A queueing model with randomized depletion of inventory. Eurandom report, Submitted for publication, 2015.

- [3] H. Albrecher, H.U. Gerber and E.S.W. Shiu (2011). The optimal dividend barrier in the Gamma-Omega model. European Actuarial Journal 1, 43-56.

- [4] H. Albrecher and J. Ivanovs (2015). Strikingly simple identities relating exit problems for Lévy processes under continuous and Poisson observations. Report University of Lausanne, August 2015; arXiv:1507.03848.

- [5] H. Albrecher and V. Lautscham (2013). From ruin to bankruptcy for compound Poisson surplus processes. ASTIN Bulletin 43, 213-243.

- [6] S. Asmussen and H. Albrecher (2010). Ruin Probabilities, 2nd ed. World Scientific, Singapore.

- [7] O. Berman, M. Parlar, D. Perry and M.J.M. Posner (2005). Production/clearing models under continuous and sporadic review. Methodology and Computing in Applied Probability 7, 203-224.

- [8] P.H. Brill (2008). Level Crossing Methods in Stochastic Models. Springer, New York.

- [9] J.W. Cohen (1975). The Wiener-Hopf technique in applied probability. In: Perspectives in Probability and Statistics. J. Gani, ed.; papers in honour of M.S. Bartlett (Academic Press, London), pp. 145-156.

- [10] J.W. Cohen (1982). The Single Server Queue, 2nd ed. North-Holland Publ. Cy., Amsterdam.

- [11] F.W.J. Olver, D.W. Lozier, R.F. Boisvert and C.W. Clark (2010). NIST Handbook of Mathematical Functions. NIST, Cambridge University Press.

- [12] A.D. Polyanin and V.F. Zaitsev (2003). Handbook of Exact Solutions for Ordinary Differential Equations, 2nd ed. CRC Press, Boca Raton.

- [13] D. Perry, W. Stadje and S. Zacks (2005). Sporadic and continuous clearing policies for a production/inventory system under an demand process. Mathematics of Operations Research 30, 354-368.

- [14] G. Szegö (1975). Orthogonal Polynomials. 4th ed., AMS, Providence.

- [15] E.C. Titchmarsh (1939). The Theory of Functions. Oxford University Press, Oxford.

- [16] P.D. Welch (1964). On a generalized queueing process in which the first customer of each busy period receives exceptional service. Oper. Res. 12, 736-752.

- [17] R.W. Wolff (1989). Stochastic Modeling and the Theory of Queues. Prentice-Hall, Englewood Cliffs (NJ).