Determinantal sampling designs

Abstract

In this article, recent results about point processes are used in sampling theory. Precisely, we define and study a new class of sampling designs: determinantal sampling designs. The law of such designs is known, and there exists a simple selection algorithm. We compute exactly the variance of linear estimators constructed upon these designs by using the first and second order inclusion probabilities. Moreover, we obtain asymptotic and finite sample theorems. We construct explicitly fixed size determinantal sampling designs with given first order inclusion probabilities. We also address the search of optimal determinantal sampling designs.

1 Introduction

The goal of sampling theory is to acquire knowledge of a parameter of interest using only partial information. The parameter is a function of , usually the sum or the mean of the ’s. This is done by means of a sampling design, through which a random subset is observed, and the construction of an estimator of based on this random sample. The properties of the sampling design are thus of crucial importance to get “good” estimators. In practice, the following issues are fundamental:

-

•

simplicity of the design,

-

•

knowledge of the first and, possibly, second order inclusion probabilities,

-

•

control of the size of the sample,

-

•

effective construction, in particular with prescribed unequal probabilities,

-

•

statistical amenability (consistency, central limit theorem,…),

-

•

low Mean Square Error (MSE)/Variance of the estimator.

In this article, we introduce a new parametric family of sampling designs indexed by Hermitian contracting matrices, determinantal sampling designs, that addresses all theses issues. Section 2 gives their definition and probabilistic properties. In particular, it is shown that for this family, inclusion probabilities are known for any order. Section 2 also provides a selection algorithm. Section 3 studies the statistical properties of linear estimators of a total. It gives algebraic and geometric formulas for the which provide necessary and sufficient conditions for obtaining a perfectly balanced determinantal sampling design. In addition, we give asymptotic theorems and concentration inequalities. Sections 4 and 5 provide effective constructions of fixed size determinantal sampling designs with fixed first order inclusion probabilities. Optimal properties are discussed in Section 6. Finally Section 7 shows simulation studies. In particular, we explore the empirical optimality of the sampling design based upon the matrix constructed in Section 5.

2 Definition and general properties

2.1 Definition

According to its definition, an unordered sampling design without replacement (simply called sampling design afterwards) is a simple point process on a finite set , that is to say a probability on , set of parts of (Borodin, (2009), Tillé, (2011)).

Among simple point processes, the general structure and properties of determinantal point processes have attracted a lot of attention recently (Borodin, (2009), Hough et al., (2006), Hough et al., (2009), Lyons, (2003), Soshnikov, (2000)). This is (in part) due to the ubiquity of determinantal point processes in probability theory. They appear for instance in the study of random structures such as uniform spanning trees, zeros of random polynomials and spectra of random matrices. In the case of a finite set , determinantal point processes are defined through associated matrices called kernels (such a kernel is however not unique). Many probabilistic properties of these processes therefore depend on algebraic properties of their kernels, but most of the results concern Hermitian matrices only. For this reason, and though there exist many interesting examples of determinantal point processes associated to non-Hermitian matrices, we restrict our attention to the Hermitian case.

Unless specifically stated, matrices will be complex matrices. For a complex number , is its conjugate and its modulus. We introduce the following notation. For any square matrix indexed by and , denotes the submatrix of whose rows and columns are indexed by . We will also use the following convention: the determinant of the empty matrix is , as is a product over the empty set . From the definition of determinantal point processes we derive the following definition of determinantal sampling designs:

Definition 2.1 (Determinantal sampling design)

A sampling design on a finite set is a determinantal sampling design if there exists a Hermitian matrix indexed by , called kernel, such that for all , This sampling design is denoted by .

A random variable with values in and law is called a determinantal random sample (with kernel ). It satisfies, for all ,

We will also write .

In the following we will always identify the finite population of size with . It follows from the definition that determinantal sampling designs are unordered and without replacement. Macchi, (1975) and Soshnikov, (2000) proved that a Hermitian matrix defines a determinantal point process, and as a consequence a , iff (if and only if) is a contracting matrix, that is a matrix whose eigenvalues are in . It follows from this fundamental result that determinantal sampling designs form a parametric family of sampling designs, parametrized by contracting matrices.

Example 2.1 (Poisson sampling)

Consider a diagonal matrix with diagonal elements with values in . It is a contracting matrix and the corresponding determinantal sampling design satisfies, for all ,

The inclusion-exclusion principle implies that

This is precisely the equation of the Poisson sampling design (with first order inclusion probabilities ), which therefore belongs to the family of determinantal sampling designs.

Let be a Hermitian projection matrix. Then and , hence is an orthogonal projection matrix. Therefore, we will make no distinction between projections and orthogonal projections. As the eigenvalues of are or , then is a contracting matrix. We can thus associate to a determinantal sampling design . We will see that enjoys interesting statistical and computational properties. Such determinantal point processes are sometimes called determinantal projection processes (Hough et al., (2006)) or elementary determinantal point processes (Kulesza and Taskar, (2011)) in the literature.

We will usually write the projection matrix as , where is the matrix of an orthonormal basis of the range of .

Among these sampling designs,we single out three particular cases.

Example 2.2 (Projection)

Let be the square matrix of size with all terms equal to .

-

1.

is the simple random sampling (SRS) of size .

-

2.

is the SRS of size .

-

3.

If is a diagonal projection matrix, is a degenerated (non-random) sampling design.

Apart from the cases and , Kulesza, (2012) proved that the SRS is not a determinantal sampling design.

2.2 Inclusion probabilities

The following formulas for the inclusion probabilities of order and follow from Definition 2.1. As usual in sampling theory, we denote them by and . In matrix formulation, for all setting

| (1) | |||||

| (2) | |||||

| (5) |

it holds that

| (6) |

where is the Schur-Hadamard (entrywise) matrix product.

Proposition 2.1

From (5) a determinantal sampling design satisfies the so-called Sen-Yates-Grundy conditions:

| (7) |

More generally, a determinantal sampling design has negative associations (Lyons, (2003)). In particular, for disjoint subsets and it holds that

It was shown recently that determinantal point processes actually enjoy the strong Rayleigh property (Borcea et al., (2009), Pemantle and Peres, (2014)), a technical property stronger than negative association. This property can be defined in terms of the localization of the zeros of the generating function of the process. These two properties (negative association, strong Rayleigh property) proved very useful for the study of statistics of determinantal processes (Yuan et al., (2003), Brändén and Jonasson, (2012), Pemantle and Peres, (2014)). Some results will be used in Section 3.

2.3 Sample size

Of major importance to statisticians is the sample size of the random sample. It is for instance very common in practice to work with fixed size samples, that is with samples whose size is non-random and given. The sample size of a determinantal random sample follows from Theorem in Hough et al., (2006). For a set , let denotes its cardinal and for a Hermitian matrix , let be the set of eigenvalues of (with their multiplicities).

Theorem 2.1 (Sample size)

Let . Then the random variable has the law of a sum of independent Bernoulli variables of parameters the elements of .

Corollary 2.1 (Sample size (2))

Let . Then

-

1.

.

-

2.

.

-

3.

iff .

-

4.

The total number of points of is less than or equal to .

-

5.

is a fixed size determinantal sampling design iff is a projection matrix.

Proof. Let be the vector of first inclusion probabilities. Then (see Särndal et al., (2003)). The other results follow directly from Theorem 2.1 and the spectral decomposition of Hermitian matrices.

Recall that in case of fixed size sampling designs we have the formula (see Särndal et al., (2003)): for any ,

| (8) |

2.4 Additional properties

We give here some other general probabilistic results on determinantal sampling designs and their interpretation in terms of sampling theory. We refer to Lyons, (2003) and Hough et al., (2006) for their probabilistic versions.

Proposition 2.2 (Complementary sample)

Let . The complementary random sample is a determinantal random sample with kernel .

Proposition 2.3 (Domain)

Let be a determinantal sampling design on with kernel , and let be a subpopulation (or domain). Then the restriction of to is determinantal sampling design on with kernel , the submatrix of whose rows and columns are indexed by :

Proposition 2.4 (Stratification)

Let be a partition of into strata. is stratified iff the matrix admits a block diagonal decomposition relative to these strata, that is implies .

By using the inclusion-exclusion principle, Lyons, (2003) shows that the probabilities of disjunction are also given by a determinant (Theorem 5.1 Equation (5.2) for fixed size designs and Equation (8.1) for random size designs).

2.5 Algorithm

A general algorithm for simulating a determinantal sampling design is provided in Hough et al., (2006), including a proof of its validity in a very general setup. Other implementations of this algorithm can be found in Scardicchio et al., (2009) and Lavancier et al., (2015). We consider the latter since it is more suitable and efficient when is large and can be written as , a situation that we will often encounter in Sections 4 and 5.

The first algorithm samples from fixed size determinantal sampling designs. Let be a projection matrix, and be the line of .

Algorithm 2.1

-

•

Sample one element of with probabilities , .

-

•

Set

-

•

For i = (n-1) to 1 do:

-

–

sample one of with probabilities , ,

-

–

set and .

-

–

-

•

End for.

-

•

Return

The resulting sample is a realization of .

The next algorithm describes a procedure to sample from any determinantal sampling design, by expressing it as a mixture of fixed size sampling designs (Theorem 7 in Hough et al., (2006)).

Let be a contracting matrix with rank one decomposition

Algorithm 2.2

-

1.

Simulate a vector whose components are independant Bernoulli variables with parameter .the elements of

-

2.

Construct the projection matrix .

-

3.

Sample from by Algorithm 2.1.

The resulting sample is a realization of .

3 Estimation of a total

3.1 Linear estimators and the Horvitz-Thompson estimator

Let be a variable of interest on the population . Typical parameters to estimate are the total , sum of the values of the variable of interest over the whole population, or the mean value . An estimator of is called linear and homogeneous if there exist weights (that may depend on the sample) such that the estimator writes

When the weights do not depend on the sample, the Mean Square Error () decomposes as:

| (10) | |||||

where is defined by Equation (5).

Obviously, the only unbiaised estimator should satisfy , for all . The corresponding estimator,

is known as the Horvitz-Thompson estimator (Horvitz and Thompson, (1952)).

3.2 Mean Square Error

In the case of a determinantal sampling design, the of an homogeneous linear estimator of the total of a variable of interest admits algebraic and geometric formulations. They enable us to provide necessary and sufficient conditions for a perfect estimation of the total of auxiliary variables.

We introduce the following notations. For a vector , denotes the diagonal matrix with diagonal . For any two matrices , denotes the canonical scalar product on . The associated Frobenius norm is denoted by . We also define (Schur-Hadamard product) and diagonal matrices , where the square root is taken in the complex sense for negative . Finally, we pose . Note that and , two equalities that we will use thoroughly in the rest of this section.

Proposition 3.1 (Algebraic and Geometric forms of the )

The of satisfies

| (11) | |||||

| (12) |

and, in the case of the Horvitz-Thompson estimator,

Proof. These formulas follow from the classical equality and the following equality relating the trace on the Schur-Hadamard product Horn and Johnson, (1991): for any two vectors and any two matrices it holds that

The bilinear form is indefinite in general. However, it holds by Moutard-Fejer’s Theorem (De Klerk, (2006) Appendix A) that for any two positive semidefinite matrices and ,

since and are positive semidefinite.

Recently, Deville, (2012) raised the following question. For a given vector , when can we estimate perfectly (without error, ) the total , using a sampling design with fixed first order inclusion probabilties (and an homogeneous linear estimator)? Using the previous equations, we provide a necessary and sufficient condition within determinantal sampling designs. Obviously, the estimator must be unbiaised. Therefore we consider the Horvitz-Thompson estimator only (), and positive first order inclusion probabilities.

Theorem 3.1 (Perfect Estimation)

Assume takes only non-zero values, and let be a determinantal sampling design. Let be the distinct values of , and be the associated sets of indices such that .

Then the following statements are equivalent:

-

1.

The total is perfectly estimated () by ,

-

2.

is a projection with positive diagonal that commutes with ,

-

3.

is a stratified determinantal sampling design with strata , of fixed size within each stratum.

Proof.

-

By Moutard-Fejer’s Theorem, it holds that for any two semidefinite matrices and , with equality iff . Assume . Then . As and are semidefinite, then . Multiplying on the left and on the right by yields and taking the conjugate transpose gives . Thus and commute It also follows that . By multiplying the equality on the left by we get , and is a projection.

-

Reorder the population by strata. Then the commutant of is the set of block diagonal matrices with respect to these stratas, and is block diagonal. As is also a projection, each block is actually a projection, and is of fixed size within each stratum.

is straightforward.

Finally, we provide an alternative view on the variance that comes from the general theory of point processes and spatial statistics. The quantity can be interpreted as a ponderated measure of global repulsiveness for point processes on a discrete space (Biscio et al., (2016) and Lavancier et al., (2015) in the continuous setting). As determinantal point processes are repulsive, we then expect DSDs to achieve small variance within all sampling designs. This is validated by our empirical studies in Section 7. In the next section, we consider the problem of minimization of this variance.

3.3 Statistical properties of the estimator

The classical settings for the study of asymptotic properties are either the superpopulation models (Deming and Stephan, (1941), Cassel et al., (1977) chapter 4), or the models of nested (finite) populations as described by Isaki and Fuller Isaki and Fuller, (1982). We consider this second setting here. In particular, is a nested sequence of finite populations (). The variable of interest may depend on , is a sequence of vectors of size . Also is a sequence of positive vectors of size . In all this section, is a sequence of determinantal sampling designs on the populations with kernel , whose diagonal terms are positive, and is the sequence of associated linear estimators of with weights . To simplify notations, we consider as before , and omit the superscript , writing , , and instead of and .

We focus successively on consistency, central limit theorems and concentration/deviation inequalities.

In this setting, most results about consistency concern the mean square convergence of the Horvitz-Thompson estimator of the mean , see Isaki and Fuller, (1982), Robinson, (1982), Dol et al., (1996) in the case of fixed size sampling designs and Cardot et al., (2010), Chauvet, (2014) in the general case. A classical condition within these references is that the sequence is bounded. Using Schur’s Theorem Schur, (1911) on semidefinite matrices we improve the previous condition for determinantal sampling designs. The theorem also applies to other linear homogeneous estimators than the Horvitz-Thompson one. We pose .

Theorem 3.2 (Mean-square convergence)

If

-

1.

,

-

2.

,

then tends to in mean square.

In particular a sufficient condition for the convergence of towards in mean square is

Proof. By Proposition 3.1

As the matrices , , and are positive semidefinite, it holds that , and are positive semidefinite by Schur Theorem. Since then it also holds that for the partial order on positive semidefinite matrices. It follows that

Moreover the bias satisfies

by Cauchy-Schwartz-inequality. From these inequalities we get

which goes to by assumptions. This completes the proof.

Regarding equal probability determinantal sampling designs with expected size ( for all ) and a bounded variable , a sufficient condition for convergence of the Horvitz-Thompson estimator of the mean is simply . More generally

Corollary 3.1

Set . If

-

1.

there exists , such tht for all and all , ,

-

2.

the sequence is bounded,

-

3.

the expected size of the samples .

Then in mean square.

The second assumption appears for instance in Robinson, (1982).

Apart consistency, some authors have considered the existence of central limit theorems for sampling designs. However, this proves generally a difficult task even for means or totals, and existing results either focus on a particular class of sampling designs (equal probability sampling designs: Erdös and Rényi, (1959), Hájek, (1960), rejective Poisson sampling: Hájek, (1964)), or assume entropy conditions (Berger, (1998)). Assuming only that the determinantal sampling design is “random enough”, we obtain a central limit theorem by applying the results of Soshnikov (Soshnikov, (2000),Soshnikov, (2002)). These articles contain several theorems on the asymptotic normality of functionals of determinantal point processes. Theorem on linear statistics of bounded measurable functions in Soshnikov, (2002) can be applied straightforwardly to the study of determinantal sampling designs and their associated linear homogeneous estimators (whose weight do not depend on the random sample).

Theorem 3.3 (Central Limit Theorem)

Define for all the homogeneous linear estimators

If the variance as and if

for any and some , then

The assumptions of the theorem call for some comments. The assumption is natural to get a CLT, but a lower bound on the variance is given by the smallest eigenvalue of , that is for instance for fixed size sampling designs. The two other assumptions are more technical. We present a specific case where they are met.

Corollary 3.2

If for some , and then

This applies in particular to the Horvitz-Thompson estimation of a bounded variable with .

As usual, we can replace the true variance by any weakly consistent estimator of this variance, using Slutsky theorem. A classical variance estimator is the Horvitz-Thompson estimator of the variance (Horvitz and Thompson, (1952)):

In case of fixed size sampling designs, an alternative formula for the variance can be used and we get the Sen-Yates-Grundy estimator (Yates and Grundy, (1953), Sen, (1953)):

which is itself a Horvitz-Thomson estimator (but of a different sum). The first and second order inclusion probabilities of these new sampling designs can be calculated by means of the matrix associated to , and we can use the classical criteria of convergence of the Horvitz-Thompson estimator Isaki and Fuller, (1982), Robinson, (1982), Dol et al., (1996), Cardot et al., (2010), Chauvet, (2014) that depend only on these inclusion probabilities.

As previously recorded, from a very different perspective, the work of Berger, (1998) proves asymptotic normality for fixed size sampling designs under asymptotically maximal entropy conditions (the sampling is asymptotically rejective). Recently, the asymptotic normality has also been studied for more general classes of processes (that include the determinantal ones): processes with negative or positive associations (Patterson et al., (2001), Yuan et al., (2003)), and processes that satisfy the strong Rayleigh property Brändén and Jonasson, (2012). We adapt here Theorem 2.4 of Patterson et al., (2001) in the case of the Horvitz-Thompson estimator of the total based on determinantal sampling designs. The variance of the Horvitz-Thompson estimator decomposes as

Set , and .

Theorem 3.4

If , and , then

For processes satisfying the strong Rayleigh property, Pemantle and Peres, (2014) recently proved concentration and deviation inequalities that extend those of Lyons, (2003) for the number of points of determinantal processes in a subdomain. Their application to sampling theory allows derivation of the following finite distance results.

Theorem 3.5 (Deviation and concentration inequalities)

Set and set For all ,

Moreover, if is of fixed size , then

Proof. Function is -Lipschitz for the Hamming distance. Theorems and of Pemantle and Peres, (2014) apply and yield the stated results.

From this concentration inequality, we derive a new criterion for the convergence in probability of :

Corollary 3.3

If then

Proof. Set , . It holds that

By assumption and , and the right hand term above tends to .

4 Constructing equal probability determinantal sampling designs

In practice, one mainly uses sampling designs with fixed first order inclusion probabilities. It is thus of crucial importance to be able to build such sampling designs with additional interesting properties, such as a fixed size. The parametric description of determinantal sampling designs proves a formidable tool to achieve this goal.

Sampling designs with constant first order inclusion probabilities are a particular instance of sampling designs with fixed first order inclusion probabilities, called equal probability sampling designs. We consider such designs in this section (next section will be devoted to sampling designs with any prescribed probabilities). We first consider the existence of determinantal sampling designs having the same first and second order probabilities as a SRS. Second, we provide an explicit construction of fixed size and equal probability determinantal sampling designs relying on the -th primary unit roots. We finally relax the fixed size constraint to build new examples of equal probability determinantal sampling designs.

4.1 -simple determinantal sampling designs

SRS is not determinantal in general. This negative result does not however settle the question of the existence of a determinantal sampling design with the same first and second order inclusion probabilities as the SRS of size , that is such that and

Definition 4.1 (-simple designs)

A sampling design (on of size ) is -simple if its inclusion probabilities satisfy

Since the variance of only depends on the first and second order probabilities, which are those of SRS, and as SRS is of fixed size, it follows that a -simple sampling design is of fixed size . In particular, the kernel of a -simple determinantal sampling design is a projection of rank .

Applying Equations (1) and (2) to a -simple determinantal sampling design, we get that its kernel also satisfies

Let be a matrix such that is an orthonormal basis of the range of () ,where is the kernel of a -simple determinantal sampling design. It holds that:

-

1.

For all , ,

-

2.

There exists a nonnegative such that (),

-

3.

.

These properties are exactly those defining an Equiangular Tight Frame (ETF) according to Tropp, (2005) and Sustik et al., (2007). Thus

Theorem 4.1 (-simple designs and ETFs)

is a -simple sampling design iff , where is an of .

As a consequence of Theorem 4.1, a necessary and sufficient condition for the existence of ETFs would solve the problem of the existence of -simple determinantal sampling designs. However, such a condition is not known for the moment. But there exist necessary conditions. In Theorem 4.2, we apply some existing results on ETFs to -simple determinantal sampling designs (this a only a small part of a rich literature on the subject, going from strongly regular graphs Waldron, (2009) to Gauss sums and finite field theory Strohmer, (2008)).

Theorem 4.2

Let be two integers.

-

1.

There exists a determinantal sampling design only if (Tropp, (2005)).

-

2.

There exists a determinantal sampling design with a real kernel only if (Sustik et al., (2007) Theorem C).

-

3.

When , a necessary condition of the existence of a -simple determinantal sampling design with real kernel is that the following two quantities be odd integers:

When , it is necessary that be odd and that be the sum of two squares (Sustik et al., (2007) Theorem A and Casazza et al., (2008) Theorem 4.1)

Numerical studies compensate for the absence of general existence conditions. We deduce from Sustik et al., (2007) and Casazza et al., (2008) the existence of -simple determinantal sampling designs with real kernel for respectively (Sustik et al., (2007) Table I) and (Casazza et al., (2008) Table III). Tables II and III in Sustik et al., (2007) also give the existence of -simple determinantal sampling designs with complex kernels. Table 1 summarizes this information for In the table, the symbol indicates that no -simple determinantal sampling design with real kernel exists, but that one with complex kernel does exist (this justifies a posteriori the use of complex matrices).

| 3 | 3 | 4 | 4 | 5 | 5 | 6 | 6 | 6 | 7 | 7 | 7 | 8 | 8 | 8 | |

| 6 | 7 | 7 | 13 | 10 | 11 | 11 | 16 | 31 | 14 | 15 | 28 | 15 | 29 | 57 | |

Example 4.1 ((6,3)-simple determinantal sampling design)

Let

is a projection, and is -simple. It is not a simple sampling as the samples and do not have the same probabilities ( and respectively).

4.2 Fixed size equal probability sampling designs

In this section, we construct an explicit family of fixed size, equal probability sampling designs. The matrices involved are special Toeplitz matrices constructed upon primitive th roots of the unity.

Theorem 4.3

Let be three integers such that and with two relatively prime integers. Let be the determinantal sampling design with kernel :

is of fixed size , and its first and second order inclusion probabilities satisfy

Proof. Let be a any primitive th root of the unity with two relatively prime integers. Set and define for all the vectors . They define, by construction, an orthonormal family and is a projection of rank , where . Its diagonal elements satisfy

for all . Its off-diagonal elements satisfy

The second order inclusion probabilities follows from Equation (2).

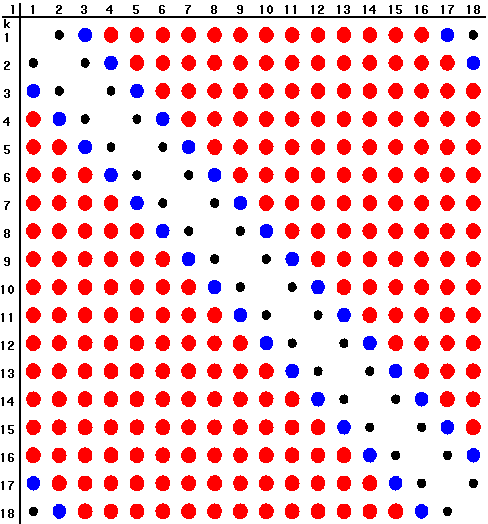

Figure 1 shows those probabilities in the following case :

Circle with radius proportional to (, ,.)

Corollary 4.1

Let be three integers such that and with two relatively prime integers. Then

Proof. We apply Equation (8) with .

4.3 Other equal probability determinantal sampling designs

Relaxing the fixed size constraint leads to new families of determinantal sampling designs, as shown in the following results.

Theorem 4.4

Let be two integers such that , and let be the determinantal sampling design with kernel :

is of random size , and its first and second order inclusion probabilities satisfy

Proof. The characteristic polynomial of can be computed as a Hurwitz determinant: . is thus a contracting matrix with as maximal eigenvalue, and by Corollary 2.1, . As is not a projection, is not of fixed size.

Actually, is the mean of the previous kernels .

Lemma 4.1

Let be prime and . Then .

Proof.

This results is also true when is not prime, but in that case, for some values of , might not be contracting.

We conclude this section by providing two general methods to construct (non-fixed size) equal probability determinantal sampling designs. The first one relies on positive definite kernel functions and takes into account auxiliary information in We illustrate the method with the Laplacian kernel, but other kernels are also available (linear, Gaussian).

Example 4.2 (Laplacian kernel)

Set and let be an auxiliary variable. For large enough, there exists a determinantal sampling design with first and second order inclusion probabilities

Indeed, the Laplacian kernel function is positive semidefinite on with and . The matrix defined by is thus positive semidefinite. For large enough, its eigenvalues are less than . The quantity is the average size of the random sample. If , then and will never be sampled simultaneously.

The second method relies on (infinite) Hermitian Toeplitz matrices, see for instance Grenander and Szegö, (1958). From this theory we directly obtain the following result.

Proposition 4.1 (Toeplitz Designs)

Let be a real square integrable function on . Then for any , the matrix with coefficients is a contracting matrix, with constant diagonal , and is an equal probability determinantal sampling design of average size .

5 Constructing fixed size, unequal probabilities determinantal sampling designs

To derive estimators with a low MSE, it is common to work with unequal probabilities sampling designs, that is sampling designs with unequal first order inclusion probabilities. These designs are preferably of fixed size, for both practical and theoretical reasons. Indeed, as shown for instance by Theorem 3.1 in the determinantal case, the total will be perfectly estimated by the Horvitz-Thompson estimator iff the vector of first order inclusion probabilities is proportional to the vector and the sampling design is of fixed size. In this section we first give a general existence result of fixed size determinantal sampling designs with prescribed inclusion probabilities. Then we discuss the effective construction of such designs. A major improvement compared to existing methods (systematic designs, cube method,…) is that the second order inclusion probabilities are completely known. This allows a precise description of these sampling designs (Corollary 5.1).

5.1 Theoretical approach

Let be a vector of size such that . There exists a very simple determinantal sampling design satisfying for all : the Poisson sampling (2.1) with kernel defined by and . Unfortunately this design is not of fixed size. According to Corollary 2.1, constructing a fixed size determinantal sampling design with prescribed inclusion probabilities is equivalent to constructing a projection matrix with a prescribed diagonal. The latter problem is a particular case of the more general issue of constructing Hermitian matrices with prescribed diagonal and spectrum that has re-attracted attention over the last years (Schur, (1911), Horn, (1954), Kadison, (2002), Fickus et al., (2013), Dhillon et al., (2005)).

Obviously, since is the expected number of points in the sample, a necessary condition to obtain fixed size sampling designs with is that is an integer. The next theorem proves that this is actually a sufficient condition. It is a direct consequence of the Schur-Horn Theorem (Horn, (1954)).

Theorem 5.1 (Fixed size DSD with prescribed unequal probabilities (Existence))

Let be a vector of size such that and . There exists a determinantal sampling design of fixed size whose first order inclusion probabilities satisfy .

The original proof of the Schur-Horn theorem is non-constructive. In the next section, we give an explicit construction of the sampling design.

5.2 Effective construction

Up to now, the effective constructions found in the literature are algorithmic and do not provide a closed form for the matrix . For instance Kadison, (2002) and Dhillon et al., (2005) provide algorithms based on plane rotations whereas Fickus et al., (2013) recently describe a Top Kill algorithm using frame theory. In the two dimensional case, Dhillon et al., (2005) explicitly construct a (real) plane rotation so that the diagonal vector of equals a prescribed vector , while having the same spectrum as . Assuming (without loss of generality) that , then

where

| (13) | |||||

Using these plane rotations and the ideas behind the proof of Theorem 7 in Kadison, (2002) we are able to derive a closed-form expression of a specific projection matrix , denoted afterwards, and of its joint inclusion probabilities for all

Let be a vector of size such that and . Set and for all integer such that , let

-

•

be the integer such that ,

-

•

and if ,

-

•

for ,

-

•

for , otherwise.

Then define a real symmetric kernel as follows:

-

•

for all , ,

-

•

for all :

Table 2: Values of : Values of Values of

Theorem 5.2 (Fixed size DSD with prescribed unequal probabilities (Construction))

The matrix is a real projection matrix, and is a fixed size sampling designs with first order inclusion probabilities .

Proof. Let be a matrix whose entries are apart from entries, whose values are . The proof of Theorem in Kadison, (2002) consists in constructing the sequence , , where is the unitary operator whose matrix relative to the canonical basis has at the () and () entries, and at the and entries, respectively, 1 at all other diagonal entries, and at all other off-diagonal entries. is the angle enabling to have at the entry of , without changing the first and the last diagonal entries. We build on this proof and on formulas 5.2 to give explicit calculations of and we finally end up with the following coefficients for :

| (14) | |||||

| (15) |

where and when . and otherwise.

The exact knowledge of the coefficients enables a precise characterization of the sampling designs so constructed.

Corollary 5.1

Let be the matrix previously constructed, and the associated sampling design.

-

1.

If then .

-

2.

If , , then .

-

3.

Set . Then is an eigenvalue of multiplicity and an eigenvalue of multiplicity of : the random sample has or elements in ().

-

4.

If is large then , and the events and are asymptotically independent. In practice also holds for small values of .

-

5.

Let be the set of values of such that , and set . Then is stratified with strata . In particular, for constant and if divides then the sampling design picks exactly one element according to the in each of the strata.

The first two points follow from the calculations of the respective and determinant. Using Sarrus rule, we get that , where:

has the same spectrum as proving point .

Point follows from the expression of as a product of cosine. Finally, point follows from the following fact: if then and for in different strata.

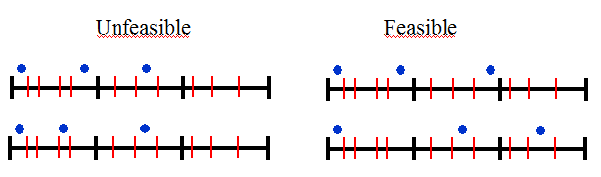

These results call for some comments. The construction of actually leads to a partition of the population into intervals

such that, if , then:

-

•

has at most one point into each open interval ,

-

•

has at least one and at most three points into each closed interval .

-

•

has at most two points into each open interval ,

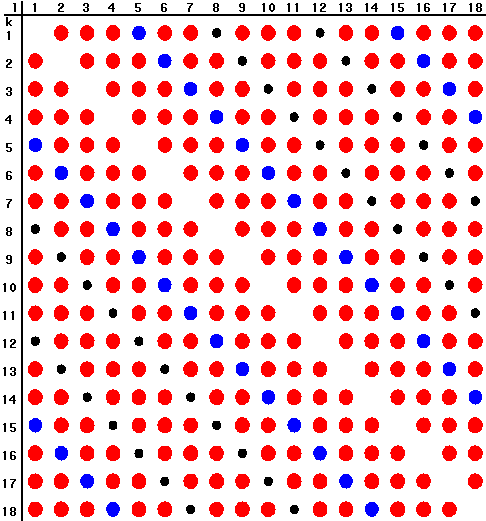

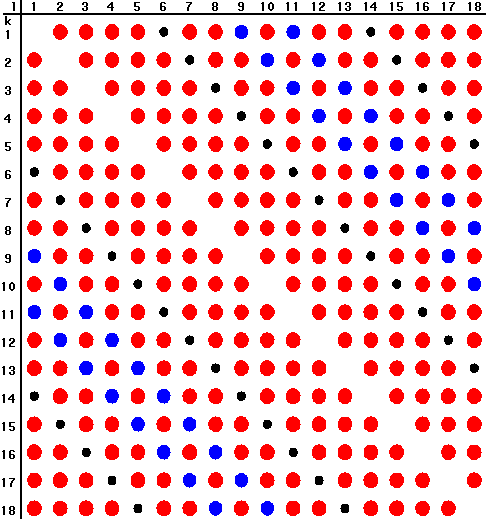

To help understand the way a sample is drawn, Figure 3 shows various feasible and unfeasible samples for , giving a graphical representation of the previous properties.

We finally provide an example of two matrices built by the previous method.

Example 5.1

Let and . Observe that is a permutation of , and that . Then

6 Optimal sampling designs

6.1 A generic optimization problem

In this section, we are given a fixed vector of weights , and we estimate any variable by the linear estimator of weight , . It is common to search for sampling designs providing representative or balanced samples for a set of auxiliary variables, where a sample is representative for if . Deville and Tillé, (2004) provide a general method, called the cube method, for selecting approximately balanced samples with (equal or unequal) fixed inclusion probabilities (usually , so that the linear estimator is the Horvitz-Thompson estimator), and any number of auxiliary variables.

Regarding DSDs, our approach to provide approximately balanced samples is to interpret representativity as follows: a sampling design is representative if for all This approach is for instance considered in Fuller, (2009), but the inclusion probabilities of the optimal sampling design are then unknown. As the MSE is available in a closed form for DSDs, we consider representativity as an optimization problem. Precisely, we minimize the sum of the over the set of determinantal sampling designs with first order inclusion probabilities , that is over the set

of contracting matrices of diagonal . Since the diagonal of is fixed the bias is constant, and the problem admits the following formulations (we pose ):

Problem 6.1

Find

We now analyze this optimization problem.

-

•

Problem 6.1 is well-posed, because we consider the optimization of a continuous function on the (convex) compact set of contracting matrices.

-

•

The parameter set is a projected spectrahedron, that is the projection of the intersection of the cone of positive semidefinite matrices and an affine space. The optimization problem we consider here is then a particular case of the semidefinite optimization problems.

-

•

This problem is nonetheless a non-convex problem, because the objective function for the minimization problem is non-convex. Algorithmic difficulties can thus be challenging, notably when is large.

-

•

Consider the case of nonnegative variables . In this case the objective function of the minimization problem is concave in , and the mimimum is thus attained at an extremal point of the convex set .

The number of studies on semidefinite optimization has been growing rapidly (in the convex and linear setting) since the 90’s (see for instanceBlekherman et al., (2013), Vandenberghe and Boyd, (1996)). But while efficient algorithms exist in the case of a strictly convex objective function, problems are extremely difficult otherwise. One of the difficulties in the case of linear or concave objective functions is that the extreme points of spectrahedra do not generally admit a simple characterization. Indeed, the problem of deciding whether a given matrix is an extreme point of a given spectrahedron is NP-hard for many spectrahedra. This is for instance the case for the elliptope of correlation matrices.

In practice, existing semidefinite optimization algorithms fail to produce optimal solutions when is large. Indeed, we have seen in Section 5 that producing a projection element in (projections are extreme points, but not all extreme points are projections) is in itself a difficult task. However, we will see in our simulation studies (Section 7) that the construction of a specific DSD (the of Theorem 5.2) leads to (empirical) optimal solutions for one auxiliary variable. In the following, we treat the following cases:

-

•

Theoritical results for .

-

•

Algorithmic minimization results, .

-

•

Presentation of an empirical algorithm.

The performances of the empirical algorithm are presented in Section 7, for .

6.2 Minimization over sampling designs of average size (less than) one

We first consider equal-probability determinantal sampling designs of average size one. In this case, the parameter space for Problem 6.1 is , the spectrahedron of positive semidefinite matrices of diagonal (this set is homothetic to the set of correlation matrices, also known as the elliptope, which is the set of positive semidefinite matrices of diagonal ). The literature on the elliptope and linear optimization over it is abundant, see for instance Ycart, (1985), Grone et al., (1990), Laurent and Poljak, (1995), Laurent and Poljak, (1996), Kurowicka and Cooke, (2003), Laurent and Varvitsiotis, (2014). It is known that (for real matrices):

Theorem 6.1 (Linear optimization over the elliptope)

-

1.

For any integer such that , there exists a matrix of rank that is an extreme point of ( Grone et al., (1990) Theorem 2).

-

2.

The vertices of (extreme points where the normal cone to is of rank ) are the projections of (rank matrices).

-

3.

It is NP-hard to decide whether the optimum of linear optimization problem is reached at a vertex.

Otherwise stated, the minimization of a linear function over the elliptope can be considerably hard, and the solution may not be a projection matrix.

Surprisingly, for this particular set (equal probability determinantal sampling designs of average size ), the quadratic problem is much more simpler than the linear one. Actually, the minimization Problem 6.1 for all unequal-probability sampling designs of average size less than (not only the determinantal ones) admits a simple solution.

Theorem 6.2 (Optimal sampling design, average size less than )

Let be a vector of inclusion probabilities such that , and be nonnegative variables. There exists a unique sampling design that minimize within all sampling designs with fixed first order inclusion probabilities . It is the determinantal sampling design , where is any rank matrix with the prescribed diagonal. This sampling design consists in sampling no element with probability , and the single element with probability .

Proof. Let be any sampling design with fixed first order inclusion probabilities . As for , then

with equality iff for , that is .

The only sampling design that satisfies these equalities is , which is thus the optimal design.

Consider now a rank one matrix with the prescribed diagonal. Then , and is a contraction of rank . it follows that exists, and has no more than element by Corollary 2.1, so that , . Finally achieves this lower bound, and .

If (in particular if ) we get the following corollaries:

Corollary 6.1 (Minimization over the elliptope)

Corollary 6.2 (SRS is optimal)

The sampling design with equal first order inclusion probabilities that minimizes the sum of the MSEs for nonnegative variables is the SRS of size , which is determinantal.

Nonnegativity is crucial in the previous results. Consider the following example:

Example 6.1

Let U={1,2}, and . Then the variance of any equal-weighted sampling design of average size one that satisfies the Sen-Yates-Grundy conditions is , which is the variance of the estimator under Poisson sampling.

For more complex spectrahedra (), a characterization of the solutions of the problem 6.1 is unknown. In particular, the question whether the solutions are always projections for integer sums remains open.

6.3 Results of the minimization algorithm,

We performed nonlinear semidefinite optimization using specific algorithms (Polyak, (1992), (Tütüncü et al., (2001)), for various vectors of inclusion probabilities, integers (size of the population) and auxiliary variables . And our empirical conclusions are:

-

•

When is an integer, the minimizer is always a projection.

-

•

When and divides , and for one auxiliary variable only (), the optimal determinantal sampling design is stratified, that is the solution matrix is (up to a change of base) a block diagonal matrix, with each block a rank one projection.

-

•

However, for more than one auxiliary variable () the solution is generally not stratified, for and divides .

6.4 An empirical algorithm

The previous results suggest that the following method will produce a low MSE/variance estimator, but for nonnegative auxiliary variable only. As before, we search for a sampling design with fixed first order inclusion probabilities such that , and the vector of weights is fixed.

Algorithm 6.1

Indeed, the algorithm will actually produce a perfect estimator for a stratified auxiliary variable (Theorem 3.1 and Corollary 5.1). And if the conditions of Theorem 3.1 are not fulfilled, then the matrix will nonetheless be quasi-stratified, and a rank contraction matrix on each stratum. Therefore, restricted to each stratum, the solution will achieve the minimal variance by Theorem 6.2.

We finally describe a method that improves Algorithm 6.1 by performing rotations that decrease the objective function (MSE of the estimator in our case). In Subsection 5.2, we described a rotation that changes two diagonal coefficients and into two new elements and . By letting and in the formulas (with ), we end up with two rotation matrices. The trivial solution () and a second non-trivial solution that changes the off-diagonal elements without altering neither the diagonal nor the spectrum:

For a given matrix with diagonal , this provides for any pair such that a rotation matrix that changes only the elements and . We thus derive a “greedy” improvement of Algorithm 6.1.

7 Simulation studies

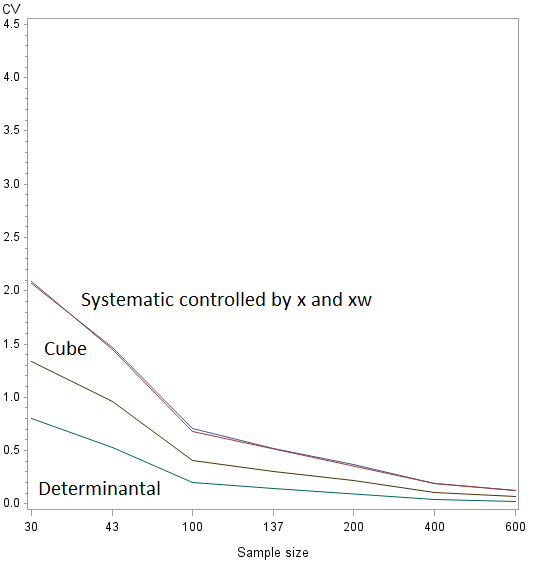

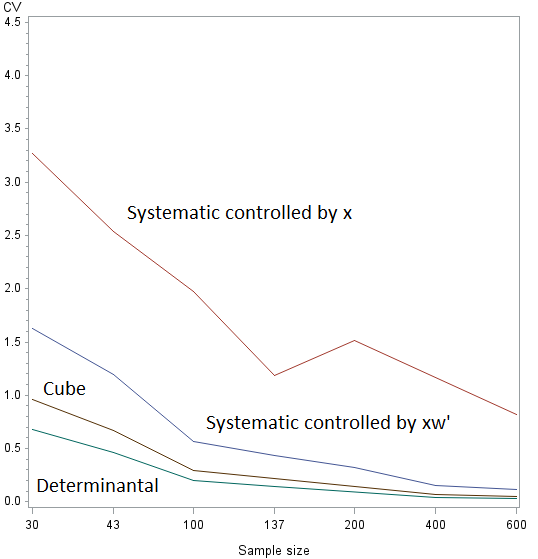

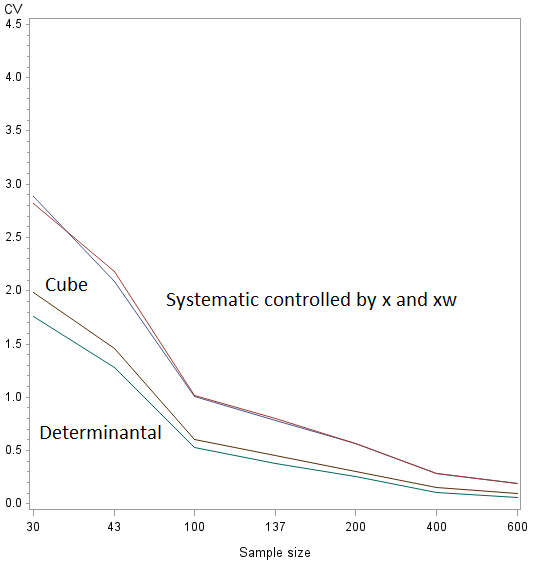

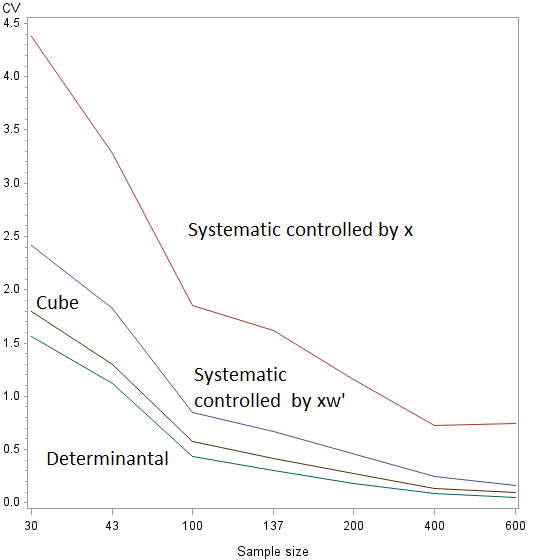

We present below our simulations studies. They are based on real data sets of auxiliary variables. We consider the problem of selecting primary units (PUs) for the French master sample. The population consists of geographical entities partitioning the French Continental territory (figure 4).

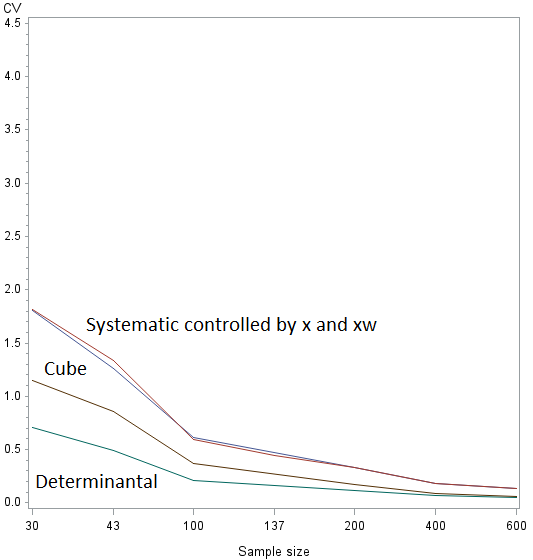

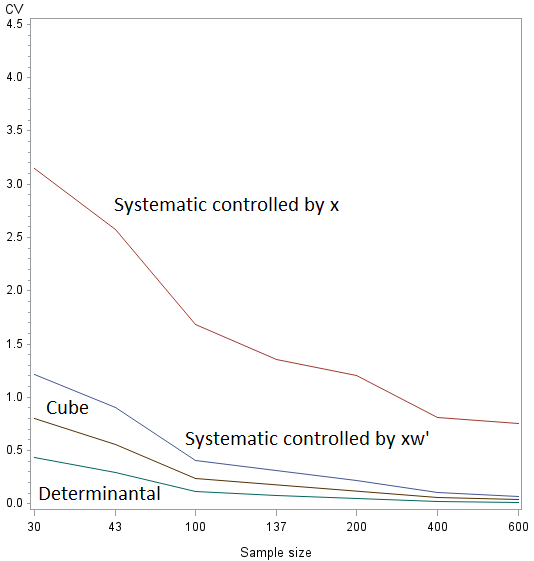

For each PU we observe the number of main dwellings (), the total amount of pensions paid to the inhabitants (), of unemployment benefit (), of revenues from economic activity (), normalized so that each total is . Computing the variance of these normalized variables is then equivalent with computing the coefficient of variation (CV) of the original variables. We then consider two sets of inclusion probabilities: and for =

We perform (approximated) balanced sampling on each single variable. Precisely, for each variable , , each sample size and each set of inclusion probabilities we perform the first two steps of Algorithm 6.1 with the weights corresponding to those of the Horvitz-Thompson estimator: and . We then compute the exact variance of this estimator for using Proposition 3.1. We compare the result with the variance obtained for other popular sampling designs: a same size systematic sampling design controlled by , a second one controlled by , and a sampling design resulting from the cube method balanced on (Deville and Tillé, (2004)). For these other designs, the variance has to be computed by Monte-Carlo simulations. Systematic sampling is both simple to implement and known to achieve low variance for ranked data, and the cube method is considered as one of the best method to produce near optimal estimators. These two types of sampling are now commonly used in official statistics.

In each case the determinantal sampling design leads to the lowest CV (figure 5). For the second set of inclusion probabilities, the systematic design has better results when controlled by rather than by just . Moreover, for the latter, the CV might locally increase with the sample size.

8 Acknowledgments

We acknowledge Xu Kai from the French National School of Statistics and Economic Administration (ENSAE) for his helpful implementation of semidefinite optimization with MATLAB. We also thank Martin Brady from the Australian Bureau of Statistics (ABS) and Antoine Chambaz from Modal’X (Université Paris-Nanterre) for their useful comments.

References

References

- Berger, (1998) Berger, Y. G. (1998). Rate of convergence for asymptotic variance of the horvitz–thompson estimator. Journal of Statistical Planning and Inference, 74(1):149–168.

- Biscio et al., (2016) Biscio, C. A. N., Lavancier, F., et al. (2016). Quantifying repulsiveness of determinantal point processes. Bernoulli, 22(4):2001–2028.

- Blekherman et al., (2013) Blekherman, G., Parrilo, P. A., and Thomas, R. R. (2013). Semidefinite optimization and convex algebraic geometry, volume 13. Siam.

- Borcea et al., (2009) Borcea, J., Brändén, P., and Liggett, T. (2009). Negative dependence and the geometry of polynomials. Journal of the American Mathematical Society, 22(2):521–567.

- Borodin, (2009) Borodin, A. (2009). Determinantal point processes. arXiv preprint arXiv:0911.1153.

- Brändén and Jonasson, (2012) Brändén, P. and Jonasson, J. (2012). Negative dependence in sampling. Scandinavian Journal of Statistics, 39(4):830–838.

- Cardot et al., (2010) Cardot, H., Chaouch, M., Goga, C., and Labruère, C. (2010). Properties of design-based functional principal components analysis. Journal of statistical planning and inference, 140(1):75–91.

- Casazza et al., (2008) Casazza, P. G., Redmond, D., and Tremain, J. C. (2008). Real equiangular frames. In CISS, pages 715–720. Citeseer.

- Cassel et al., (1977) Cassel, C.-M., Särndal, C. E., and Wretman, J. H. (1977). Foundations of inference in survey sampling. Wiley.

- Chauvet, (2014) Chauvet, G. (2014). A note on the consistency of the narain-horvitz-thompson estimator. arXiv preprint arXiv:1412.2887.

- De Klerk, (2006) De Klerk, E. (2006). Aspects of semidefinite programming: interior point algorithms and selected applications, volume 65. Springer Science & Business Media.

- Deming and Stephan, (1941) Deming, W. E. and Stephan, F. F. (1941). On the interpretation of censuses as samples. Journal of the American Statistical Association, 36(213):45–49.

- Deville, (2012) Deville, J.-C. (2012). Comment conserver l’équilibre dans un sondage: la quête du graal et la suite. Septième Colloque francophone sur les sondages, Rennes.

- Deville and Tillé, (2004) Deville, J.-C. and Tillé, Y. (2004). Efficient balanced sampling: the cube method. Biometrika, 91(4):893–912.

- Dhillon et al., (2005) Dhillon, I. S., Heath Jr, R. W., Sustik, M. A., and Tropp, J. A. (2005). Generalized finite algorithms for constructing hermitian matrices with prescribed diagonal and spectrum. SIAM Journal on Matrix Analysis and Applications, 27(1):61–71.

- Dol et al., (1996) Dol, W., Steerneman, T., and Wansbeek, T. (1996). Matrix algebra and sampling theory: The case of the horvitz-thompson estimator. Linear algebra and its applications, 237:225–238.

- Erdös and Rényi, (1959) Erdös, P. and Rényi, A. (1959). On the central limit theorem for samples from a finite population. Publ. Math. Inst. Hungar. Acad. Sci, 4:49–61.

- Fickus et al., (2013) Fickus, M., Mixon, D. G., Poteet, M. J., and Strawn, N. (2013). Constructing all self-adjoint matrices with prescribed spectrum and diagonal. Advances in Computational Mathematics, 39(3-4):585–609.

- Fuller, (2009) Fuller, W. A. (2009). Some design properties of a rejective sampling procedure. Biometrika, 96(4):933–944.

- Grenander and Szegö, (1958) Grenander, U. and Szegö, G. (1958). Toeplitz Form and Their Applications. University of California Press, Berkeley and Los Angeles.

- Grone et al., (1990) Grone, R., Pierce, S., and Watkins, W. (1990). Extremal correlation matrices. Linear Algebra and its Applications, 134:63–70.

- Hájek, (1960) Hájek, J. (1960). Limiting distributions in simple random sampling from a finite population. Publications of the Mathematics Institute of the Hungarian Academy of Science, 5(361):74.

- Hájek, (1964) Hájek, J. (1964). Asymptotic theory of rejective sampling with varying probabilities from a finite population. The Annals of Mathematical Statistics, pages 1491–1523.

- Horn, (1954) Horn, A. (1954). Doubly stochastic matrices and the diagonal of a rotation matrix. American Journal of Mathematics, 76(3):620–630.

- Horn and Johnson, (1991) Horn, R. A. and Johnson, C. R. (1991). Topics in matrix analysis. Cambridge Univ. Press.

- Horvitz and Thompson, (1952) Horvitz, D. G. and Thompson, D. J. (1952). A generalization of sampling without replacement from a finite universe. Journal of the American statistical Association, 47(260):663–685.

- Hough et al., (2009) Hough, J. B., Krishnapur, M., Peres, Y., and Virág, B. (2009). Zeros of Gaussian analytic functions and determinantal point processes, volume 51. American Mathematical Society Providence, RI.

- Hough et al., (2006) Hough, J. B., Krishnapur, M., Peres, Y., Virág, B., et al. (2006). Determinantal processes and independence. Probab. Surv, 3:206–229.

- Isaki and Fuller, (1982) Isaki, C. T. and Fuller, W. A. (1982). Survey design under the regression superpopulation model. Journal of the American Statistical Association, 77(377):89–96.

- Kadison, (2002) Kadison, R. V. (2002). The pythagorean theorem: I. the finite case. Proceedings of the National Academy of Sciences, 99(7):4178–4184.

- Kulesza, (2012) Kulesza, A. (2012). Learning with Determinantal Point Processes. PhD thesis, University of Pennsylvania.

- Kulesza and Taskar, (2011) Kulesza, A. and Taskar, B. (2011). Learning determinantal point processes.

- Kurowicka and Cooke, (2003) Kurowicka, D. and Cooke, R. (2003). A parameterization of positive definite matrices in terms of partial correlation vines. Linear Algebra and its Applications, 372:225–251.

- Laurent and Poljak, (1995) Laurent, M. and Poljak, S. (1995). On a positive semidefinite relaxation of the cut polytope. Linear Algebra and its Applications, 223:439–461.

- Laurent and Poljak, (1996) Laurent, M. and Poljak, S. (1996). On the facial structure of the set of correlation matrices. SIAM Journal on Matrix Analysis and Applications, 17(3):530–547.

- Laurent and Varvitsiotis, (2014) Laurent, M. and Varvitsiotis, A. (2014). A new graph parameter related to bounded rank positive semidefinite matrix completions. Mathematical Programming, 145(1-2):291–325.

- Lavancier et al., (2015) Lavancier, F., Møller, J., and Rubak, E. (2015). Determinantal point process models and statistical inference. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 77(4):853–877.

- Lyons, (2003) Lyons, R. (2003). Determinantal probability measures. Publications Mathématiques de l’Institut des Hautes Études Scientifiques, 98:167–212.

- Macchi, (1975) Macchi, O. (1975). The coincidence approach to stochastic point processes. Advances in Applied Probability, pages 83–122.

- Patterson et al., (2001) Patterson, R. F., Smith, W. D., Taylor, R. L., and Bozorgnia, A. (2001). Limit theorems for negatively dependent random variables. Nonlinear Analysis: Theory, Methods & Applications, 47(2):1283–1295.

- Pemantle and Peres, (2014) Pemantle, R. and Peres, Y. (2014). Concentration of lipschitz functionals of determinantal and other strong rayleigh measures. Combinatorics, Probability and Computing, 23(01):140–160.

- Polyak, (1992) Polyak, R. (1992). Modified barrier functions (theory and methods). Mathematical programming, 54(1-3):177–222.

- Robinson, (1982) Robinson, P. (1982). On the convergence of the horvitz-thompson estimator. Australian Journal of Statistics, 24(2):234–238.

- Särndal et al., (2003) Särndal, C.-E., Swensson, B., and Wretman, J. (2003). Model assisted survey sampling. Springer Science & Business Media.

- Scardicchio et al., (2009) Scardicchio, A., Zachary, C. E., and Torquato, S. (2009). Statistical properties of determinantal point processes in high-dimensional euclidean spaces. Physical Review E, 79(4):041108.

- Schur, (1911) Schur, J. (1911). Bemerkungen zur theorie der beschränkten bilinearformen mit unendlich vielen veränderlichen. Journal für die reine und Angewandte Mathematik, 140:1–28.

- Sen, (1953) Sen, A. R. (1953). On the estimate of the variance in sampling with varying probabilities. Journal of the Indian Society of Agricultural Statistics, 5(1194):127.

- Soshnikov, (2000) Soshnikov, A. (2000). Determinantal random point fields. Russian Mathematical Surveys, 55(5):923–975.

- Soshnikov, (2002) Soshnikov, A. (2002). Gaussian limit for determinantal random point fields. Annals of probability, pages 171–187.

- Strohmer, (2008) Strohmer, T. (2008). A note on equiangular tight frames. Linear Algebra and its Applications, 429(1):326–330.

- Sustik et al., (2007) Sustik, M. A., Tropp, J. A., Dhillon, I. S., and Heath, R. W. (2007). On the existence of equiangular tight frames. Linear Algebra and its applications, 426(2):619–635.

- Tillé, (2011) Tillé, Y. (2011). Sampling algorithms. Springer.

- Tropp, (2005) Tropp, J. A. (2005). Complex equiangular tight frames. In Optics & Photonics 2005, pages 591401–591401. International Society for Optics and Photonics.

- Tütüncü et al., (2001) Tütüncü, R., Toh, K., and Todd, M. (2001). Sdpt3—a matlab software package for semidefinite-quadratic-linear programming, version 3.0. Web page http://www. math. nus. edu. sg/~ mattohkc/sdpt3. html.

- Vandenberghe and Boyd, (1996) Vandenberghe, L. and Boyd, S. (1996). Semidefinite programming. SIAM review, 38(1):49–95.

- Waldron, (2009) Waldron, S. (2009). On the construction of equiangular frames from graphs. Linear Algebra and its Applications, 431(11):2228–2242.

- Yates and Grundy, (1953) Yates, F. and Grundy, P. (1953). Selection without replacement from within strata with probability proportional to size. Journal of the Royal Statistical Society. Series B (Methodological), pages 253–261.

- Ycart, (1985) Ycart, B. (1985). Extreme points in convex sets of symmetric matrices. Proceedings of the American Mathematical Society, 95(4):607–612.

- Yuan et al., (2003) Yuan, M., Su, C., and Hu, T. (2003). A central limit theorem for random fields of negatively associated processes. Journal of Theoretical Probability, 16(2):309–323.