University of Pennsylvania22affiliationtext: AT&T Labs33affiliationtext: The School of Engineering and Applied Science

University of Pennsylvania

A Risk Ratio Comparison of and Penalized Regression

Abstract

There has been an explosion of interest in using -regularization in place of -regularization for feature selection. We present theoretical results showing that while -penalized linear regression never outperforms -regularization by more than a constant factor, in some cases using an penalty is infinitely worse than using an penalty. We also show that the “optimal” solutions are often inferior to solutions found using stepwise regression.

We also compare algorithms for solving these two problems and show that although solutions can be found efficiently for the problem, the “optimal” solutions are often inferior to solutions found using greedy classic stepwise regression. Furthermore, we show that solutions obtained by solving the convex problem can be improved by selecting the best of the models (for different regularization penalties) by using an criterion. In other words, an approximate solution to the right problem can be better than the exact solution to the wrong problem.

Keywords: Variable Selection, Streaming Feature Selection, Regularization, Stepwise Regression, Submodularity

1 Introduction

In the past decade, a rich literature has been developed using -regularization for linear regression including Lasso (Tib96), LARS (Efron+04), fused lasso (Tib+05), elastic net (ZouH05), grouped lasso (YuanL06), adaptive lasso (Zou06), and relaxed lasso (Mein07). These methods, like the -penalized regression methods which preceded them (Aka74; Schwarz78; FosterG94), address variable selection problems in which there is a large set of potential features, only a few of which are likely to be helpful. This type of sparsity is common in machine learning tasks, such as predicting disease based on thousands of genes, or predicting the topic of a document based on the occurrences of hundreds of thousands of words.

-regularization is popular because, unlike the regularization historically used for feature selection in regression problems, the penalty gives rise to a convex problem that can be solved efficiently using convex optimization methods. methods have given reasonable results on a number of data sets, but there has been no careful analysis of how they perform when compared to methods. This paper provides a formal analysis of the two methods, and shows that can give arbitrarily worse models. We offer some intuition as to why this is the case – shrinks coefficients too much and does not zero out enough of them – and suggest how to use an penalty with optimization.

We study the problem of selecting predictive features from a large feature space. We assume the classic normal linear model {IEEEeqnarray*}rCl+rCl y& = Xβ+ ϵ ϵ ∼ N_n(0,σ^2 I_n) with observations and features , where is an “design matrix” of features, is the coefficient parameters, and error .

We expect most of the elements of to be 0. Hence, generating good predictions requires identifying the small subset of predictive features. This standard linear model proliferates the statistics and machine learning literature. In modern applications, can approach millions, making the selection of an appropriate subset of these features essential for prediction. The size and scope of these problems raise concerns about both the speed and statistical robustness of the selection procedure. Namely, it must be fast enough to be computationally feasible and must find signal without over-fitting the data.

The traditional statistical approach to this problem, namely, the regularization problem, finds an estimator that minimizes the penalized sum of squared errors,

| (1) |

where counts the number of nonzero coefficients. However, this problem is NP-hard (Nata95). A tractable problem relaxes the penalty to the norm, , and seeks

| (2) |

This is known as the -regularization problem (Tib96), which is convex. This problem can be solved efficiently using a variety of methods (Tib96; Efron+04; CanT07).

We assess our models using the predictive risk function (1) {IEEEeqnarray}rCcCl R(β, ^β) & = E_β ∥ ^y- E(y—X)∥_2^2 = E_β ∥X^β- Xβ∥_2^2. We are interested in the ratios of the risks of the estimates provided by these two criteria. Unlike risk functions, predictive risk measures the relevant prediction error on future observations, ignoring irreducible variance. Smaller risks imply better expected prediction performance. It is an ideal metric to analyze testing error or out-of-sample errors when the parameter distribution is assumed to be known. Recent literature has focused on selection consistency: whether or not the true variable can be identified in the limit. However, in real application, due to ubiquitous multicollinearity, predictors are hard to separate as “true” and “false”. Here, we focus on predictive accuracy and advocate the concept of predictive risk.

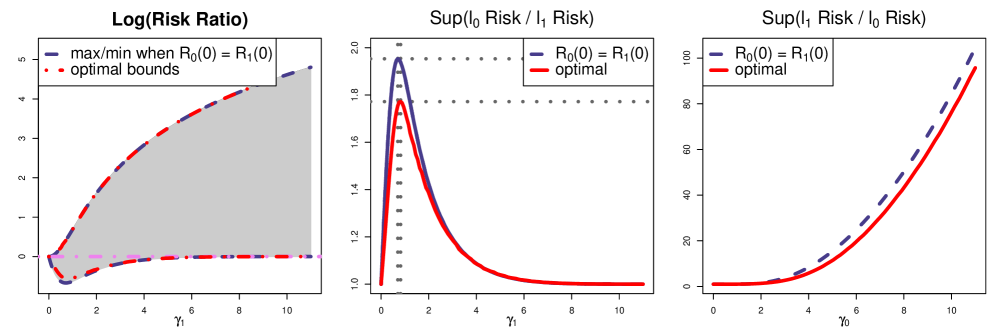

Our first result in this paper, given below as Theorems 1 and 2 in Section 2, is that estimates provide more accurate predictions than estimates do, in the sense of minimax risk ratios. This is illustrated in Figure 1. Proofs of these theorems are in Appendix A.

-

•

is bounded by a small constant; furthermore, it is close to one for most s, especially for large s, which are mostly used in sparse systems.

-

•

tends to infinity quadratically; in an extremely sparse system, the estimate may perform arbitrarily badly.

-

•

is more likely to have a larger risk than does. backgroundcolor=blue!20!white,inline, bordercolor=red]how is “more likely” defined?

A detailed discussion on the risk ratios will be presented in Section 2, along with a discussion of other advantages of regularization. Our other comparative results include showing that applying the criterion on an subset searching path can find the best performing model (Section 2.3.1) and running stepwise regression and Lasso on a reduced NP hard example shows that stepwise regression gives better solutions (Section 2.3.2).

backgroundcolor=blue!20!white,inline, bordercolor=red]Check all assumptions or remove. We compare vs. penalties under three assumptions about the structure of the feature matrix : independence, incoherence (near independence) and NP-hard. For independence, we find provide the theoretical results mentioned above. For near independence, we find that penalized regression followed by outperforms selection. For the NP-hard case, we find that if one could do the search, then the risk ratio could be arbitrarily bad for relative to .

2 Risk Ratio Comparison

We assess our models using the predictive risk function (1) {IEEEeqnarray}rCcCl R(β,^β) & = E_β ∥ ^y- E(y—X) ∥_2^2 = E_β ∥X^β- Xβ∥_2^2.

This is the relevant component after decomposing the expected squared error loss

from predicting a new observation. This is clear from the following standard

decomposition. For increased generality, let and be the

projection onto the column space of . Then

{IEEEeqnarray*}rCl

E∥y^* - X^β∥^2 & = E∥y^*-η∥^2 + E∥η- H_Xη∥^2 +

E∥H_Xη- X^β∥^2

= ⏟n σ^2_common error +

⏟∥(I- H_X)η∥^2_wrong +

⏟E∥H_Xη- X^β∥^2_predictive risk

The first term, common error, is unavoidable, regardless of the method being used. All methods we consider, namely linear methods based on , suffer the error from incorrect . Since is given, it is more instructive to consider the projection of onto the column space of , defining . Ignoring these two forms of error, leaves the predictive risk function (1).

backgroundcolor=blue!20!white,inline, bordercolor=red] citations: BarbB04; content: what is it, why is it good, where has it been used; risk vs consistence; and relation to out-of-sample error

Predictive risk has guided selection procedures such as Mallow’s and RIC. The former results from an unbiased estimate of the predictive risk, while the later provides minimax control of the risk in during model selection. We maintain this minimax viewpoint and show that in terms of the removable variation in prediction, performs better than .

2.1 solutions give more accurate predictions.

Suppose that is an estimator of . For this section, we assume is orthogonal. (For example, wavelets, Fourier transforms, and PCA all are orthogonal). The problem (1) can then be solved by simply picking those predictors with least squares estimates , where the choice of depends on the penalty in (1). It was shown (DonJ94; FosterG94) that is optimal in the sense that it asymptotically minimizes the maximum predictive risk inflation due to selection.

Let {IEEEeqnarray}rCl ^β_l_0 (γ_0) & = ( ^β_1 I_{—^β_1— ¿ γ_0}, …, ^β_p I_{ —^β_p— ¿ γ_0})’ be the estimator that solves (1), and let the solution to (2) be {IEEEeqnarray}rCl ^β_l_1 (γ_1) & = ( sign(^β_1) (—^β_1—-γ_1)_+, …, sign (^β_p) (—^β_p—-γ_1)_+)’, where the ’s are the least squares estimates.

We are interested in the ratios of the risks of these two estimates, {IEEEeqnarray*}c’C’c R(β, ^βl0(γ0))R(β, ^βl1(γ1)) & and R(β, ^βl1(γ1))R(β, ^βl0(γ0)).

I.e., we want to know how the risk is inflated when another criterion is used. The smaller the risk ratio, the less risky (and hence better) the numerator estimate is, compared to the denominator estimate. Specifically, a risk ratio less than one implies that the top estimate is better than the bottom estimate.

Formally, we have the following theorems, whose proofs are given in Appendix A:

Theorem 1.

There exists a constant such that for any , {IEEEeqnarray*}rCl inf_γ_1sup_βR(β,^βl1(γ1))R(β, ^βl0(γ0))≥C_1+γ_0.

I.e., given , for any , there exist ’s such that the ratio becomes extremely large.

Contrast this with the protection provided by :

Theorem 2.

There exists a constant such that for any , {IEEEeqnarray*}rCl inf_γ_0sup_βR(β,^βl0(γ0))R(β, ^βl1(γ1)) & ≤ 1+C_2γ_1^-1.

I.e., for any , we can pick the cutoff so that we perform almost as good as , even in the worst case.

The above theorems can definitely be strengthened, as demonstrated by the bounds

shown in Figure 1, but at the cost of complicating the

proofs. We conjecture that there exist constants , and ,

such that

{IEEEeqnarray}rCl

inf_γ_1 sup_β R(β, ^βl1(γ1))R(β, ^βl0(γ0))

& ≥ 1+C_3 γ_0^r,

inf_γ_0 sup_β R(β, ^βl0(γ0))R(β, ^βl1(γ1))

≤ 1+C_4γ_1 e^-C_5γ_1.

These theorems suggest that for any chosen by the algorithm, we can always adapt such that outperforms most of the time and loses out a little for some ’s; but for any chosen, no can perform consistently well on all ’s.

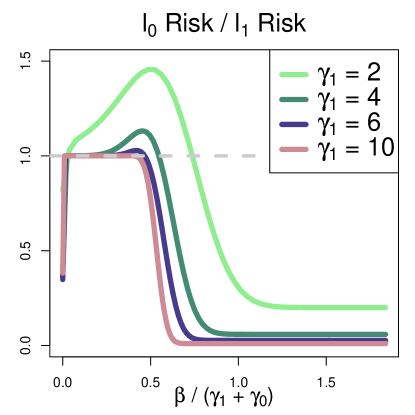

Because of the additivity of risk functions, (see appendix equations (LABEL:eqn:l0risk) and (LABEL:eqn:l1risk)), due to the orthogonality assumption, we focus on the individual behavior of for each single feature. Also the risk functions are symmetric on , so only the cases of will be displayed. Figure 2 illustrates that given , we can pick a , s.t. the risk ratio is below 1 for most except around , yet this ratio does not exceed one by more than a small factor, even for the worst case.

The intuition as to why fares better than in the risk ratio results is that must make a “devil’s choice” between shrinking the coefficients too much or putting in too many spurious features. penalized regression avoids this problem.

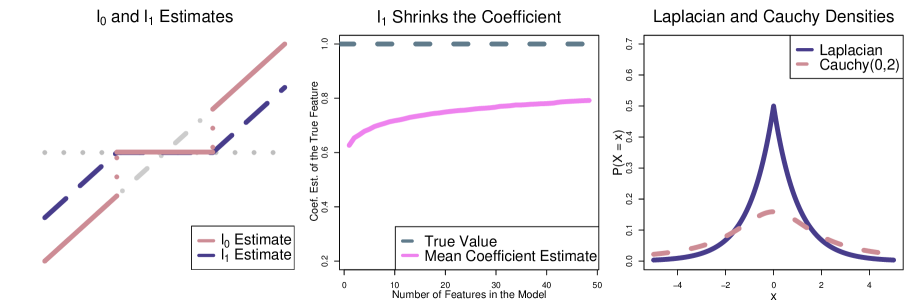

2.2 shrinks coefficients too much

From a frequentist’s point of view, the estimator (2.1) shrinks the coefficients and thus is biased (Figure 3). In practice, can be substantially shrunk towards zero when the system is sparse, as shown in the middle panel of Figure 3.

From a Bayesian’s perspective, the penalty is equivalent to putting a Laplacian prior on (Tib96; Efron+04), while the penalty can be approximated by Cauchy priors (JohnS05; FosterS05). The right panel of Figure 3 shows that the Cauchy distribution has a much heavier tail than the Laplacian distribution does. This implies that when the true is far away from 0, the penalty will substantially shrink the estimate toward zero.

The bias caused by the shrinkage increases the predictive risk proportionally to the squared amount of the shrinkage. The sparser the problem is, the greater the shrinkage is, thus the larger the risk is. These results show that in theory the estimate has a lower risk and provides a more accurate solution. Empirically, stepwise regression performs well in large data sets, where a sparse solution is particularly preferred (GeorgeF00; FosterS04; Zhou+06).

2.3 Simulations for Risk Ratio/flaws with l1

backgroundcolor=blue!20!white,inline, bordercolor=red]should mix some of the 1.2 and 1.3

2.3.1 optimization using an criterion

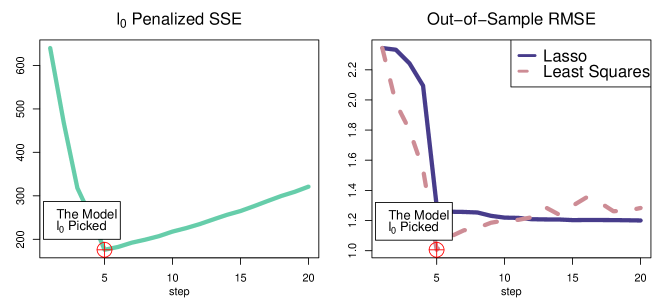

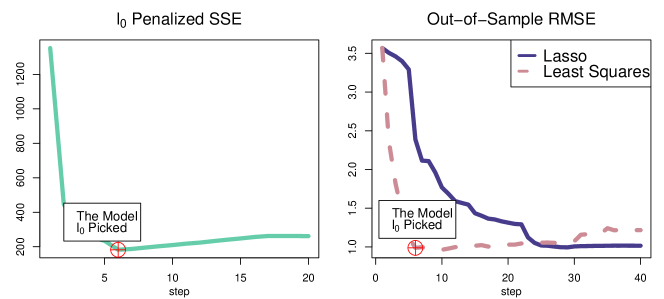

We can make use of the LARS algorithm to generate a set of candidate solutions and then use the criterion to find the best of the solutions along the regularization path. We evaluated this method as follows. We simulated from a thousand features, only 4 of which have nonzero contributions, plus a random noise distributed as . Both the training set and the test set have size . We apply the Lasso algorithm implemented by LARS on this synthetic data set. For each step on the regularization path, this algorithm selects a subset of features that are included in the model. We then adopt a modified RIC criterion suggested in GeorgeF00:

| (3) |

to find an optimal . The crucial part here is that the coefficient estimate being used in (3) is the least squares estimate of the true obtained by fitting on , and not the Lasso estimate provided by the algorithm. We also use this least squares estimate in out-of-sample calculations.

We compare two cases: the ’s are generated independently of each other, meaning that is diagonal, and the ’s are generated with a pairwise correlation . As shown in Figure 4, in the independent feature case, the model picked by the modified RIC criterion always outperforms any Lasso model on the test set. In the case with correlated predictors (Figure 5), there is little difference between the out-of-sample accuracies of the -picked model and the best Lasso model in this case, but Lasso adds around 50 more spurious variables.

Thus, by combining the computational efficiency of an algorithm and the sparsity guaranteed by the penalization, we can easily select an accurate model without cross validation.

2.3.2 and NP-hardness

The problem is NP-hard and hence, at least in theory, intractable. (In practice, of course, people often use approximate solutions to problems that in the worst case can be NP-hard.) One of the attractions of -regularization is that it is convex, hence solvable in polynomial time. In this section, we compare how the two approaches fare on a known NP-hard regression problem. We start with a simple constructive proof that the risk ratio for to can be arbitrarily bad. Construct data as follows. Pick a large number of independent features . Construct new features and and. Let plus noise. Then the correct model is . Include the rest of the features as spurious features.

In Nata95 the known NP hard problem of “the exact cover of 3-sets” was reduced to the best subset selection problem as below: , is an binary matrix with each column having three nonzero elements: , is a vector, and we want to solve {IEEEeqnarray}r’c’l min_β ∥β∥_0, & s.t. ∥ y- Xβ∥_2¡ε. Note that if there is a solution to this problem, the number of features being chosen should be .

We then ask which method comes closer to solving this problem: a greedy approximation to the problem or an exact solution to the problem. To this end, we applied Lasso and forward stepwise regression on various ’s. For small ’s, we took full collections of the three subsets, i.e., equals choose 3; for larger ’s, we took . Table 1 and 2 list the number of subsets included in the model. Forward stepwise regression always finds fewer subsets, and hence a better solution, than Lasso.

| Method | ||||||||

|---|---|---|---|---|---|---|---|---|

| Lasso | 6 | 10 | 11 | 17 | 19 | 21 | 22 | 29 |

| Stepwise | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

| Method | |||||

|---|---|---|---|---|---|

| Lasso | 93 | 219 | 504 | 812 | 1372 |

| () | () | () | () | () | |

| Stepwise | 40 | 96 | 223 | 364 | 595 |

| () | () | () | () | () |

All of our experiments on both synthetic and real data sets show that greedy search algorithms, such as stepwise regression, aimed at minimizing -regularized error provide sparser results. This is because penalizes the sparsity directly, while does not. It is easy to construct an example where will pick a solution with a smaller norm but with a less sparse solution (CanWB07).

3 Conclusion

In many statistical contexts, the regularization criterion is superior to that of regularization; generally provides a more accurate solution and controls the false discovery rate better. can give arbitrarily worse predictive accuracy than , since regularization tends to shrink coefficients too much to include many spurious features. Computationally, appears to be more attractive; convex programming makes the computation feasible and efficient. In practice, however, approximate solutions to the problem are often better than than exact solutions to the problem. The best properties of the two methods can be combined. Superior results were obtained by using convex optimization of the problem to generate a set of candidate models (the regularization path generated by LARS), and then selecting the best model by minimizing the -penalized training error.

Appendix A Risk Ratio Proofs

We will drop the ’s when the situation is clear, and denote as and as for simplicity.

Without loss of generality, we assume and . The risk can be written as

rCl R(β,^β_l_0) & = E_β ∥Xβ-X^β∥^2 = E_β ∑