Nonlinear PDEs risen when solving some optimization problems in finance, and their solutions111The views represented herein are the author own views and do not necessarily represent the views of New York University.

Abstract

We consider a specific type of nonlinear partial differential equations (PDE) that appear in mathematical finance as the result of solving some optimization problems. We review some existing in the literature examples of such problems, and discuss the properties of these PDEs. We also demonstrate how to solve them numerically in a general case, and analytically in some particular case.

keywords:

nonlinear PDE, optimization, finite-difference scheme1 Motivation and Introduction

In this paper we consider a special type of the nonlinear PDE that arises in mathematical finance by applying optimization to some financial problems. To make it clear we start with the example given by Lipton (2001) who considered an optimal consumption problem, first formulated in Merton (1971).

1.1 Lipton example

In Lipton (2001) Lipton considers a portfolio of domestic and foreign bonds. The relative value of the domestic bond is constant, i.e. , while that of the foreign bond is random and follows the Geometric Brownian motion with constant real-world drift and volatility , and is the time. Suppose is a predictable self-financing trading strategy with the corresponding linear wealth , and is the fraction of this wealth invested in foreign bonds. Self-finance of the strategy means that given one has

where is the Brownian Motion. The optimal consumption problem consists in finding the strategy which provides the expected wealth at maturity such that , while minimizing the variance of , i.e. , where is the expectation conditional to the initial moment . By using the Lagrange multiplier and the function , the previous statement is equivalent to the solution of the Hamilton-Jacobi-Bellman (HJB) problem

| (1) | ||||

As at function doesn’t depend on , so does the solution , and thus Eq.(1) reduces to

| (2) |

where . Assuming (see Lipton (2001) for further discussion), Eq.(1) has an explicit solution that can be substituted back to Eq.(1) to give rise to the following problem for :

| (3) |

This is a nonlinear equation of our interest. Based on the initial condition it can be solved analytically by representing as a quadratic form of with the coefficients being a function of . Further details can be found in Lipton (2001).

1.2 Carr example

In Carr (2014) Carr considers the call option price , with being the underlying spot price, to be the result of a maximization of some function, , with respect to some variable, , holding the parameters and constant. He shows that if the call value is a convex function of , then , where is the Legendre-Fenchel transform of the call value , namely: . He also shows that if the call value is a convex differentiable function of , the argument of the function is also the argument of the Legendre-Fenchel transform of , and is also the delta of the call, i.e. . This result motivates his dual approach to option pricing. That means that in the standard (primal) approach to option pricing, the spot price process is an input to the approach, while the stochastic process followed by the delta of the option is an output of the approach. In contrast, the Carr’s dual approach begins by specifying a stochastic process for the delta of a call, rather than for the spot price of the underlying asset.

Further on, Carr considers a forward contract on the same underlying and assumes that the value of the forward contract solves the stochastic differential equation:

| (4) |

where is a local volatility function. In other words, follows an arithmetic Brownian motion. Then the call value function solves the following parabolic PDE:

| (5) |

subject to the terminal condition:

| (6) |

Here is the expectation under the risk-neutral measure, sub-index 1 in in Carr’s notation means the first derivative on the first argument of , and subindex 2 denotes same with respect to the second argument. Accordingly, is the second derivative on the first argument.

Alternatively to the primal approach, in the dual approach Carr introduces to be now a function of , so the option price in these variables is

| (7) |

Accordingly, under some mild assumptions the first derivative of on the first argument is

| (8) |

since , and

| (9) |

by the inverse function theorem. Since implies , is convex in . Also based on the properties of the Legendre transform , and thus

| (10) |

Using Itô’s lemma, Carr also derives an important relationship between - the function relating the volatility of the delta process to the level of the call delta and to time :

| (11) |

and finally a dual PDE:

| (12) |

subject to the terminal condition

| (13) |

While the standard PDE in Eq.(5) is commonly referred to as a backward equation, the dual PDE in Eq.(12) is a forward equation.

1.3 Further notes

The above consideration implicitly assumes that the local volatility function of the delta process is known somehow for all necessary values of and . And then the forward PDE Eq.(12) with the terminal condition Eq.(13) solves the problem. From a practical point of view this assumption, however, could be unrealistic in a sense that the market doesn’t provide explicitly. At the first glance one of the possible approaches to overcome this could be first to solve the backward problem, and then use the condition Eq.(11) to restore from the precomputed values of the option gammas given a map . However, this is not fully correct. Indeed, suppose that we solved the backward problem, e.g., using a finite difference method, and now have at every point on the two-dimensional grid in . Hence, at we have the values of on this grid. Assume that we now want to solve the forward problem, and use these values of as our grid. Further on, let us make one step in time forward with a time step . Obviously, . Therefore, if we still use the -grid constructed by using the values with the -grid fixed at , the inverse map doesn’t coincide with . As a consequence, the values of and defined at the grid has to be re-interpolated at time onto the grid.

Even worse, for doing that we need to know which correspond to the grid defined at . So either we need also to store in memory all values of during the backward recursion, or use the connection . In the later case the forward linear equation Eq.(12) becomes nonlinear, because based on Eq.(11) we need to use the map where , in turn, is a function of . Below when presenting the numerical results we will discuss the peculiarities of the map in more detail.

Also it is worth mentioning that this approach, in general, has some pitfalls. First, once the backward problem is solved, most likely we don’t need the solution of the dual problem. A possible exclusion is related to valuation of the long-dated options. Second, storing all values of gammas (and perhaps deltas) on the grid in and could be memory consuming. Therefore, we present an alternative view to this problem.

In doing that below we relax the above assumption that the local volatility function of is known. Instead we assume that the only local volatility of the forward process is known. We express it in the new variables , and to eliminate any confusion introduce new notation for thus expressed function , namely . Note, that in order to build a map we still need to know the option values and deltas at which depend on the option expiration .

As per this assumption is now not an independent input of the model. Rather, it is determined by Eq.(11) where , in turn, connects to by Eq.(9). Collecting all these expressions together and rearranging terms we arrive at the following equation.

| (14) |

This is a nonlinear equation with the terminal condition given by Eq.(13). To the best of our knowledge this type of equations has not been considered in the theory of the nonlinear PDEs as well as in mathematical finance with the exception of the Lipton case considered earlier in this section.

Despite a lack of the initial condition, this is still a forward equation in a sense that the calendar time runs from 0 to . However, because of the terminal condition, this problem is not the standard Cauchy boundary problem. In physics this type of problems is well-known and usually is solved using either invariant imbedding, Bellman and Wing (1992), or the shooting method, Roberts and Shipman (1972).

Therefore, the main contributions of this paper are i) recognition that the Carr’s dual approach gives rise to a certain type of non-linear PDEs, that in the simplest form of the local volatility function linear in the underlying process have a predecessors, see Lipton (2001), but in general are more complex; and ii) an algorithm of how to efficiently solve these equations using a finite-difference method.

The rest of the paper is organized as follows. In the next section we make analysis of the derived nonlinear PDE and also provide an example (a Black-Scholes setting) when it can be solved analytically. In section 3 we propose a new numerical method to solve the full nonlinear equation which is unconditionally stable and of the second order of approximation in space and time. In section 4 we present some numerical experiments and discuss their results. The final section concludes and provides suggestions for the future research.

2 Analysis of the new nonlinear PDE

A direct analysis shows that despite an unusual form Eq.(14) is well behaved. Indeed, the Legendre transform’s Gamma is nonnegative, therefore the Legendre transform’s theta should also be nonnegative. As this means that when runs forward the values of decrease in the absolute value and in the limit reach their correct terminal value . On the other hand, as has a bell-shaped profile, as per Eq.(9) has an inverse bell-shaped profile. In other words, for deep ITM and OTM options tends to infinity, while close to ATM it is positive and close to zero. That means that is zero at and and is positive at the intermediate values of . So the evolution of should be that as presented in Fig. 3.

It turns out that Eq.(14) also admits a dual representation. To show this, we start with Eq.(12), take into account Eq.(9) and also the equation

| (15) |

derived in Carr (2014) (since ). Also use the definition of Delta to be and make a change of time from forward to backward . Thus transformed Eq.(14) now reads

| (16) |

2.0.1 Example.

Consider a particular case when the local volatility function is . In other words this corresponds to the displaced lognormal model

| (17) |

where is the option strike. Substituting this definition of into Eq.(14) we arrive at the following nonlinear equation

| (18) |

One can easily see that this is exactly Eq.(3) despite with subject to different boundary and initial conditions. We remind that in Lipton (2001) Eq.(18) was solved by assuming that (in this section notation) is a quadratic function of . However, in our case this ansatz doesn’t obey the boundary and terminal conditions for . Nevertheless, Eq.(18) admits a semi-explicit closed form solution.

To obtain this solution, we re-write the definition of in Eq.(7) in the form . As we assumed that , obeys the following stochastic SDE (Geometric Brownian motion)

By the Feynman-Kac theorem solves

| (19) |

subject to the following conditions

The explicit solution of Eq.(19) can be obtained as a sum of two branches.

At the solution is . Indeed, this expression solves Eq.(19) as well as obeys the terminal condition and the boundary condition at infinity.

At Eq.(19) gives the price of the up-and-out call with the upper barrier at and the strike written on the negative process (so ). Therefore, it reads, see Howison (1995)

| (20) | ||||

Here , is the Black-Scholes call option price, , . In our case , and, therefore, Eq.(20) simplifies to

| (21) | ||||

As at we have , this solution provides the correct boundary value of . Also at we have .

Thus, these two branches of solve Eq.(18), provide the correct boundary values, and obey the terminal condition. What remains to prove is that this solution is continuous at . Indeed, the first branch at in the limit provides . The second branch at in the limit also provides . The latter is not obvious because , and it seems that the first term in the square brackets in Eq.(21) multiplied by doesn’t converge to 0 at . However, one has to have in mind, that Eq.(21) is obtained by using the method of images. And it could be shown that at the second line in Eq.(21) vanishes regardless of the value in the square brackets, because the multiplier vanishes.

To complete the solution we need to take into account that . To obtain this dependence in closed form, observe that

From this expression

| (23) |

Thus

where Inv means the inverse function. Having an explicit representation for this map can be computed numerically.

Aside of this example the obvious question is: how to solve Eq.(14) with allowance for all its peculiarities and non-linearity. For doing that below we propose an iterative numerical scheme which assumes that the initial value is somehow known.

3 Numerical method

As our intention is to solve Eq.(14) numerically, and, moreover, iteratively, we introduce index which counts the current iteration number. Index starts from 1 and runs up to a certain number at which the scheme converges in some norm. Also for simplicity of notation in this section we omit superscript ∗ in the definition of the Legendre transformed option price , and use instead of . Thus, below we denote it as .

We start by re-writing Eq.(14) in the form

| (24) |

where

If is a function of and only, Eq.(24) would be a linear heat equation. However, in our case itself is a function of , and even worse - a function of its derivative . Nevertheless, the discrete solution of the Eq.(24) could be represented in the operator form

| (25) |

where is a finite difference approximation of the second derivative on the grid. For instance, on a uniform grid in with step

which approximates with . By using Taylor series expansion of Eq.(25) it could be validated that this scheme approximates Eq.(14) with and is exact in .

Note that again, using the Taylor series expansion one can verify that the following scheme

| (26) |

also provides same order of approximation of Eq.(14) in . Combining them together we finally propose to use a scheme

| (27) |

Now we setup an iterative algorithm to solve this discrete nonlinear equation.

-

1.

At the first iteration we re-write Eq.(25) in the form

(28) In the expression the superscript (k) marks the value of found at the -th iteration of the numerical procedure. In other words, at the first iteration we set but use this substitution only to compute in the RHS of Eq.(27). The Eq.(28) could be solved by either computing the discrete matrix exponential given the grid in (which could be done with complexity , be the number of the grid points), or by using any sort of Páde approximation of the exponent. For instance, Páde approximation leads to the well-known Crank-Nicholson scheme which could be solved with the linear complexity in .

-

2.

To proceed we represent Eq.(27) in the form

(29) So the next approximation to can be found by again either computing the matrix exponential, or by using some Páde approximation. Having this machinery in hands we can proceed in the same manner until the entire procedure converges, i.e. the condition

is reached after iterations with being the method tolerance.

To apply this algorithm we construct an appropriate discrete nonuniform grid in the delta space. For the sake of concreteness let Eq.(14) be solved at the space domain , using a nonuniform grid with nodes () and space steps . We define a central difference approximation of the second derivative, see, e.g., In’t Hout and Foulon (2010)

| (30) |

where

Proposition 3.1

-

Proof

See Appendix.

4 Numerical experiments

In the first test we solve the problem Eq.(12) assuming that the local volatility function is known. For doing that we first solve the backward problem using the following parameters of the model yrs. Our grid contained nodes in and 100 steps in time. We used the local volatility function given in Table 1

| 70 | 80 | 90 | 100 | 110 | 120 | 130 | 140 | 150 | |

| 0.1 | 0.447 | 0.455 | 0.459 | 0.462 | 0.465 | 0.467 | 0.468 | 0.470 | 0.471 |

| 0.2 | 0.500 | 0.507 | 0.511 | 0.514 | 0.516 | 0.518 | 0.519 | 0.520 | 0.522 |

| 0.4 | 0.548 | 0.554 | 0.558 | 0.560 | 0.562 | 0.564 | 0.565 | 0.566 | 0.567 |

| 0.6 | 0.592 | 0.597 | 0.601 | 0.603 | 0.605 | 0.607 | 0.608 | 0.609 | 0.610 |

| 0.8 | 0.632 | 0.638 | 0.641 | 0.643 | 0.645 | 0.646 | 0.648 | 0.649 | 0.650 |

The non-uniform grid in was constructed similar to Itkin and Carr (2011). We solved the backward equation to obtain the option prices and deltas on the grid at , and then used such obtained deltas as a grid. This simultaneously provided us with the map

Using thus obtained values of we computed the Legendre transform at using the definition in Eq.(7). We then solved Eq.(12) forward in time. As was mentioned in the previous sections, this equation is nonlinear, because in Eq.(11) we computed the map using the relation . Therefore, we solved it using an iterative scheme similar to Eq.(27). Having that map at every iteration we re-interpolated the values of found and stored during the backward run to the corresponding grid in .

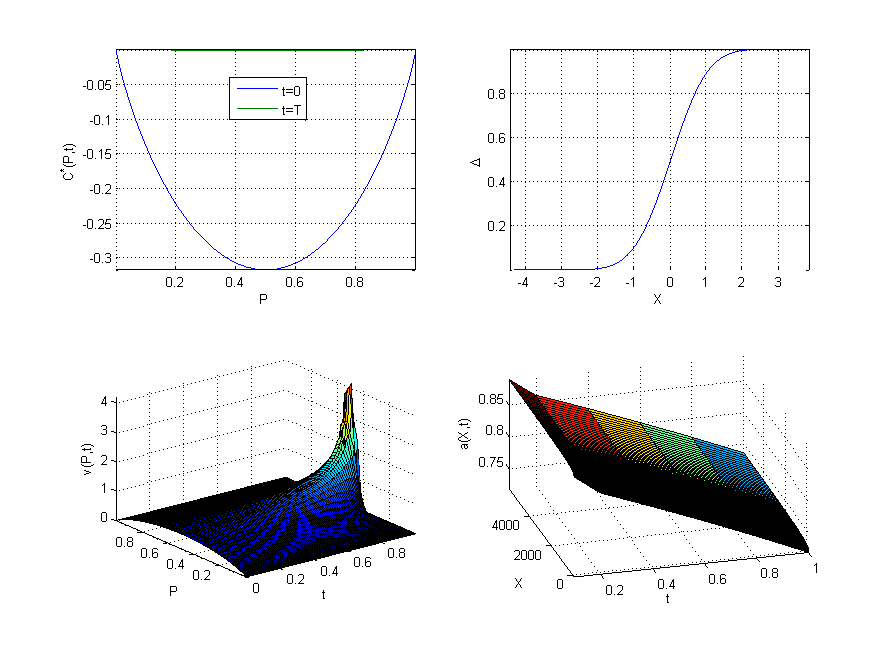

In Fig. 1 the computed results are presented in four graphs. The top left graph shows the initial function computed using the solution of the backward equation, and the final solution computed using Eq.(12). The top right plot in Fig. 1 demonstrates the map computed using the solution of the backward equation at . The bottom right graph represents our local volatility function given in Table. Eq.(1). And the bottom left graph shows computed in this experiment.

It is seen that the Legendre transform converges to its terminal value . Two important points, however, should be taken into account. First, the solution is very sensitive to the accuracy of Gammas. Suppose that the backward equation is solved using a standard, second order accurate in space, scheme. Then the accuracy of Gamma is which is not sufficient (and could be error-prone) for computing . Therefore, in this situation it would be reasonable to use a higher order scheme in or , for instance a HOC finite difference scheme of the forth order, see, e.g., Chawla et al. (2000).

Second, when our map degenerates. Indeed, if we fix , at the map is regular, i.e. for every it provides a unique value of . At for the call option for any the value of could be either 0 or 1. Therefore, multiple values of are connected to the same value of . Obviously, the inverse statement is also true. Suppose that at we fix the grid in , and then for every a unique value of could be found. However, at all these values of will connect to the value , because and . This degeneracy of the map produces additional problems with computing the accurate values of .

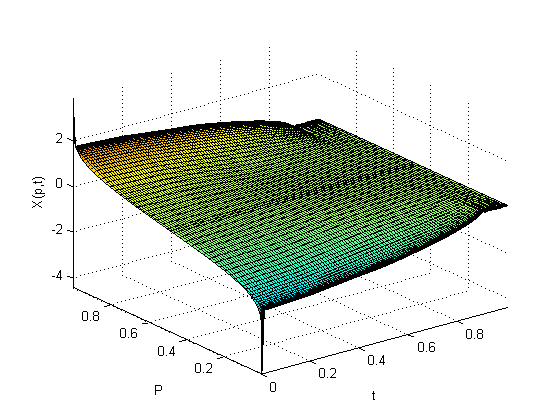

Fig. 2 shows computed plot of obtained in this experiment.

It is seen that at this plot replicates the top right graph in Fig. 1, and at it vanishes.

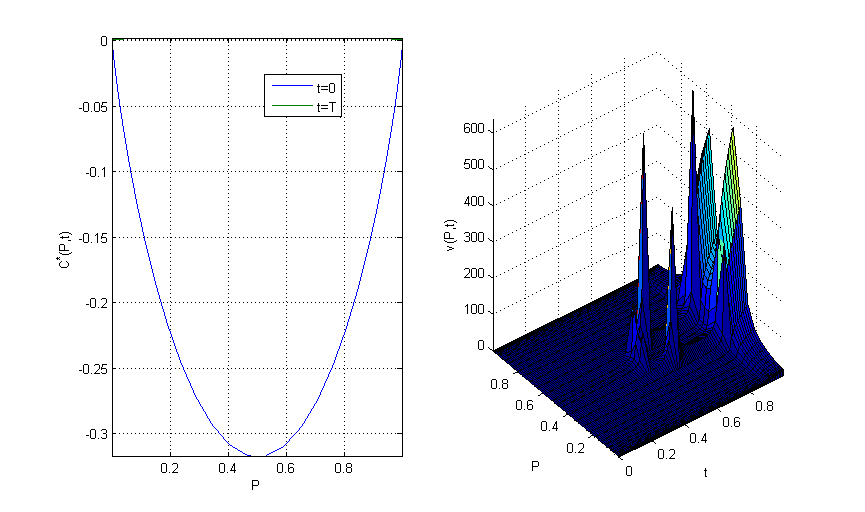

In the second test we solve the problem Eq.(14). Again we first solve the backward problem and find the initial values of as was described in above. And then using the scheme Eq.(27) propagate the solution forward in calendar time up to the maturity .

In Fig. 3 thus computed results are presented in two graphs similar to the left top and bottom ones in Fig, 1.

Observe, that the option value at is equal to payoff, hence the option gamma is the Dirac’s delta function. Accordingly, the local delta volatility is also the delta function if the local forward volatility is finite. That brings some technical difficulties to the numerical solution. The computed value of is depicted in the right plot in Fig. 3. At every this function demonstrates the correct behavior by vanishing at and , and showing a positive bell-shaped profile at the intermediate values. At it tends to the delta function. The accuracy of the solution, accordingly, significantly drops down.

Certainly, for our scheme Eq.(27) the number of iterations to converge depends on the chosen level of tolerance . Our experiments show that this number significantly depends on the smoothness of at every time step. As gammas are computed by numerical differentiation, producing a smooth local volatility function similar in the shape to the Dirac’s delta function is not simple. As we already mentioned, even if the second order scheme in is used to find , gammas are computed with the approximation . Therefore, at every iteration after the solution was computed a polynomial smoothing was applied. In particular, we fitted the solution with the polynomial of the 4th order, and then computed the second derivative of this polynomial. This provides a significant speedup in convergence.

If gammas were computed by numerical differentiation, at the first time step the number of iterations was the highest, while when increases rapidly decreases. For instance, in the above test at the first step in time requires 280 iterations, while starting from the time step 6 it decreases to 5 iterations per one time step. However, still at some values of the model parameters the entire scheme could diverge. Nevertheless, when using the polynomial fit the typical number of iterations was 2-3 at every time step even with , and the scheme rapidly converged.

We need to underline that despite the dual problem was formulated in Eq.(14) subject to the given terminal condition, here we solved this problem assuming that the initial condition at is known from the solution of the backward PDE. We then demonstrated that this solution converges to the correct terminal value of within the error of our numerical procedure. That is definitely because we used the correct initial value. If, however, the initial condition is not known, one can use either the shooting method, or the invariant imbedding method referenced in the above. This, certainly, will significantly increase the computational time.

5 Conclusions

This paper deals with a certain type of nonlinear PDE which naturally appears in mathematical finance when solving some problems formulated as optimization. As the known examples of these problems we considered an optimal consumption problem presented in Merton (1971) and then in detail in Lipton (2001) and a dual approach to option pricing invented by Carr (2014). We showed that Carr’s dual equation can be translated into the nonlinear PDE, and that the nonlinear PDE of Lipton (2001) is a particular case of the former when the volatility function is linear in the underlying variable. Further on, we described some properties of the general nonlinear PDE, provided its analytical solution in the Black-Scholes case, and proposed a new numerical method to solve it which is unconditionally stable and of the second order in both time and space. Stability of the method and approximation are proved by the corresponding Theorem formulated and proved in the paper. We also presented some results of our numerical experiments. All these results are new.

As far as the practical applications of this approach is concerned, as mentioned in Carr (2014), for some valuation problems, it may in fact be easier to specify the problem in the dual domain. This could be important, e.g., for doing delta hedge for equity options, or in the FX market where the quotes are expressed in terms of implied volatility as a function of the Black Scholes delta. Also for American options working in the delta space would make it much easier to setup the exercise boundary. Therefore, it does make sense to extend the dual technology, and, perhaps, also including jumps into consideration. From this prospective, these extensions would require new numerical methods for nonlinear PDEs most likely similar to those considered in this paper.

Acknowledgments

We are grateful to Peter Carr and Alex Lipton for their comments. They are not responsible for any errors.

References

References

- Bellman and Wing (1992) Bellman, R., Wing, G., 1992. An Introduction to Invariant Imbedding. Society for Industrial and Applied Mathematics.

- Berman and Plemmons (1994) Berman, A., Plemmons, R., 1994. Nonnegative matrices in mathematical sciences. SIAM.

- Carr (2014) Carr, P., July 2014. Options as optimizations: A dual approach to derivatives pricing. Quant USA. New York.

- Chawla et al. (2000) Chawla, M. M., Al-Zanadi, M. A., Al-Aslab, M. G., 2000. Extended one-step time-integration schemes for convection-diffusion equations. Computers and Mathematics with Applications 39, 71–84.

- Howison (1995) Howison, S., 1995. Barrier options. Available at https://people.maths.ox.ac.uk/howison/barriers.pdf.

- In’t Hout and Foulon (2010) In’t Hout, K. J., Foulon, S., 2010. ADI finite difference schemes for option pricing in the Heston model with correlation. International journal of numerical analysis and modeling 7 (2), 303–320.

- Itkin and Carr (2011) Itkin, A., Carr, P., 2011. Jumps without tears: A new splitting technology for barrier options. International Journal of Numerical Analysis and Modeling 8 (4), 667–704.

- Li et al. (2010) Li, B., Lu, B., Wang, Z., McCammon, J., 2010. Solutions to a reduced poisson–-nernst–-planck system and determination of reaction rates. Physica A 389, 1329–1345.

- Lipton (2001) Lipton, A., 2001. Mathematical Methods For Foreign Exchange: A Financial Engineer’s Approach. World Scientific.

- Merton (1971) Merton, R. C., December 1971. Optimum consumption and portfolio rules in a continuous-time model. Journal of Economic Theory 3 (4), 373–413.

- Roberts and Shipman (1972) Roberts, S., Shipman, J., 1972. Two-Point Boundary Value Problems: Shooting Methods. American Elsevier Pub. Co.

- Starzak (1989) Starzak, M., 1989. Mathematical methods in chemistry and physcis. Springer, New York.

Appendix A Proof of Proposition 3.1

Let us remind that the solution of Eq.(14) is given by Eq.(25) in the operator form

| (31) |

where

Consider a discrete analog of the operator which could be obtained on the grid by using finite-difference approximation Eq.(30). Observe, that is the Metzler matrix, see Berman and Plemmons (1994). Indeed, it has all negative elements on the main diagonal, and all nonnegative elements outside of the main diagonal. Also is a tridiagonal matrix.

Now observe that and . Therefore, matrix is also the Metzler matrix.

By the properties of the Metzler matrix its exponent is a nonnegative matrix. Therefore, preserves the sign of the vector . Also all eigenvalues of the Metzler matrix have a negative real part. Therefore, the spectral norm of the matrix follows

Thus, the map is contractual, and hence, Eq.(31) is unconditional stable.

Now we prove that the matrix is the second order approximation of the operator . That follows from the fact that matrix approximates the operator with the second order, i.e. on the non-uniform grid it provides approximation .

The last point is to prove the convergence of the fixed point Picard iterations. For doing that denote by the exact solution of Eq.(24). According to Eq.(25) it could be represented as

| (32) |

where

Observe, that at every is a linear bounded operator because it is Lipschitz

since as it was shown earlier in the the spectral norm .

Then by the mean-value theorem for operators we have

where is a convex combination of and , and denotes the Fréchet derivative of the operator at the space of all bounded linear operators, see, e.g., Li et al. (2010).

To compute the norm of the Fréchet derivative recall that by definition

If , then

and, therefore

| (33) |

It is well-known that, Starzak (1989)

where is the size of the matrix . Therefore, and could be easily chosen such that . It is important, that thus chosen values are independent, and, therefore, the scheme remains to be almost” unconditionally stable.

To explain what almost” means let us compare our condition with the familiar stability condition for the Euler explicit finite-difference scheme, which reads

| (34) |

with being some diffusion coefficient. As it can be seen, the latter condition is restrictive, because it sets the upper limit on the time step given the space step . In contrast, our condition reads

In the worst case scenario this could be re-written as

So comparing this with Eq.(34) one can see, that the stability is conditional. However it is considerably relaxed as compared with that in Eq.(34) because of the presence of the multiplier in the left hand side. Indeed, we need where the right hands part is usually a huge value unless the local volatility is very very high which is impractical. Therefore, for any practical application theoretical restrictions on are not important.