On the Efficient Market Hypothesis of Stock Market Indexes:

The Role of Non-synchronous Trading and Portfolio Effects

Abstract

In this article, the long-term behavior of the stock market index of the New York Stock Exchange is studied, for the period 1950 to 2013. Specifically, the CRSP Value-Weighted and CRSP Equal-Weighted index are analyzed in terms of market efficiency, using the standard ratio variance test, considering over 1600 one week rolling windows. For the equally weighted index, the null hypothesis of random walk is rejected in the whole period, while for the weighted market value index, the null hypothesis start to be accepted from the 1990s. In order to explain this difference, we raised the hypothesis that this behavior can be explained by the joint action of portfolios and non-synchronous trading effects. To check the feasibility of the above assumption, we performed a simulation of both effects, on two- and six-asset portfolios. The results showed that it is possible to explain the empirical difference between the two index, almost entirely by the joint effects of portfolio and non-synchronous trading.

Keyword: Efficient market hypothesis, variance ratio test, non-synchronous trading, portfolio effects, CRSP Value-Weighted index and CRSP Equal-Weighted index.

1 Introduction

The efficient financial markets hypothesis developed by Fama (1970)

established that no investor could profit in excess in a systematic

way using public or private information. That is, asset prices instantly

reflect all information about financial assets in the capital market.

In order to prove this hypothesis, transactions and information costs

must be zero at all times [Grossman and Stiglitz (1980)].

Since, there will always be transaction and information costs, different

versions of the efficient market hypothesis have been introduced:

the weak, semi-strong, and strong ways, see Robert (1967)111The weak way implies that the asset prices reflect all past information

obtained from the historical series of prices. The semi-strong way

assumes that prices reflect the information contained in the historical

series and also all the public information related to the price determination

of financial assets. And finally, the strong way implies that prices

reflect all the information kept in the historical series of prices,

all public information, and all private information about the financial

asset in the analysis.. Provided that transactions and information costs are definitely

higher than zero, the strong version of efficient capital market hypothesis

is always false [Fama (1991)]. For this reason,

there is a growing agreement that, for all practical purposes, only

the weak version of an efficient market is feasible (see for example

Fama (1965), Jensen (1978), Lo and MacKinlay (1988),

Fama (1991), Campbell et al. (1997)). This

weak version states that no investor can profit on excess by taking

a position in the market only observing the behavior of past prices

of financial assets.

It is often argued that, if there are some investors with more information

than that contained in the historical data and with a higher ability

to analyze it, then these investors will be capable of getting a higher

return than others who only take into account historical info. However,

the additional benefit obtained can involve more costs due to the

operation of obtaining and processing this extra data. In this way,

the net return earned is virtually null. Thus, this weak version has

a higher economic sense, because it states that prices reflect (at

every moment) the point where the marginal benefit of using the information

does not exceed the marginal cost of obtaining this same information

[Jensen (1978)].

Nevertheless, the existence of transactions and information costs

is not the main obstacle to making inferences about market efficiency.

This hypothesis must be necessarily be tested with a price equilibrium

model, that is, a model for the evaluation of financial assets. Therefore,

if there is evidence of an anomalous behavior of returns, we must

be wary of whether the culprit is the market failure or an inaccuracy

in the proposed equilibrium price model [Fama (1970)].

Within the tests that allow evaluation of the efficiency market hypothesis,

the ratio variance test proposed by Lo and MacKinlay (1988) is highlighted.

This test is based on the following argument: If a series of logarithms

of prices shows no linear autocorrelation, then the variance of the

sum of k periods must be equal to k times the variance of one period.

Thus, the random walk hypothesis can be measured by comparing data

variances from different time spans.

Applications of the ratio variance test in the decade of the 1980s

had a strong influence on the acceptance of the claim that financial

asset prices do not follow a random walk movement. This test was designed

to be robust to a variety of types of heteroskedasticity and not normality.

In fact, Lo and MacKinlay (1988) in a very influential work reported

that the null hypothesis of market efficiency in the form of random

walk was rejected for the CRSP NYSE Value-Weighted and CRSP NYSE Equal-Weighted

index for a sample of weekly data from September 6, 1962, to December

26, 1985.

Nearly 25 years after Lo and MacKinlay’s work, we looked into these

conclusions by applying the variance ratio test to the main stock

market indexes, but this time by considering a larger weekly return

data sample, from 1950 to 2013. In order to appreciate the evolution

of results for this test we used 1600 one week rolling windows. The

results obtained using this entire period indicated that the random

walk hypothesis could be ruled out for the CRSP NYSE Equally Weighted

index. In contrast, for the CRSP NYSE Value Weighted index, the random

walk hypothesis started to not be rejected, with growing strength

from the 1990s.

Note that, given the CRSP NYSE Value Weighted Index tended to be more

representative of the way a diversified person invests, the above

evidence has significant future implications for investors. Since

these results are different from conclusions given by Lo and MacKinlay

(1988), we carried out a study to show the evolution of behavior of

these indexes in time. In this way, to be sure that these conclusions

are reliable, we applied a test to estimate the empirical distribution

of the statistics by using the bootstrapping method [Kim (2006)].

This last test overcame the drawbacks of finite samples and estimates

of variance with overlapping. The conclusions obtained using this

last test were the same.

Naturally, the following question emerges: Why do two indexes built on the same assets show different responses to the random walk test? In order to explain the above effects, we carry out an analysis of the combined effects of non-synchronous trading and portfolio asset location over the variance ratio test of the random walk hypothesis. The results show that the acceptance/rejection of the random walk hypothesis depends on:

-

1.

The asset structure in which the portfolio is built and

-

2.

The non-trading possibilities of the same goods.

Even when the individual asset returns have no autocorrelations, the

combined effects of non-synchronous trading and portfolio can induce,

in some cases, positive autocorrelations when the correlation between

various assets is positive. These spurious autocorrelations thus can

explain the different behaviors for the ratio variance test when it

is applied to equal-weighted and value-weighted index.

Here, the modeling and simulation of both the non-trading effect and

the portfolio effect is executed and the results show that the combined

effects can cause a rejection of the null hypothesis for some portfolios.

The positive autocorrelation in some index is produced by the update

of the return of assets with non-trading problems in relation to the

return of normal trading assets.

The article is organized in the following way: in section 2, a review of literature is presented. Section 3, it gives the specifications of the statistical model with which the ratio-variances test is performed. Section 4 analyzes the evolution of the ratio variance test over the principal index of the New York Exchanges. In section 5, we explore the possibility that the non-synchronous trading and portfolio effects explain the divergence between the results of equally weighted index and index weighted by market value. Finally, the conclusions are delivered in section 6.

2 Literature Review

In the traditional capital assets pricing theory, it is proposed that

for a higher non diversifiable risk, a higher return should be obtained.

It is assumed that investors will receive on average a return proportional

to the non diversifiable risk that they take. In practice, the real

returns fluctuate randomly around their expected value. Differences

between returns realized and expected are unpredictable, and in this

sense they follow random walks. If this is true, then the capital

market hypothesis in its weak version is not refused [Campbell et al. (1997)].

The hypothesis that the returns of assets follow a random walk suggests

that no one can systematically predict changes in the asset prices

in order to obtain higher returns. Whether the changes in prices are

predictable based on past price changes (or whether changes in prices

do not follow a random walk) is still a subject of controversy and

empirical research.

In the literature on the random walk theory, three types of hypothesis

have been suggested [Campbell et al. (1997)]: Random

Walk 1 (RW1), Random Walk 2 (RW2), and Random Walk 3 (RW3).

- i)

-

The RW1 hypothesis assumes that continuously composed returns are independent and identically distributed.

- ii)

-

The RW2 hypothesis assumes that returns are independent and allow that the distribution of assets changes over time.

- iii)

-

The RW3 hypothesis is the most general and implies that returns in different periods are not linearly correlated.

It is typical in the latter case to assume processes do not have linear dependence but have quadratic dependency asymptotically decreasing to zero. For example, stochastic models with heteroskedasticity, such as GARCH processes, can be considered [Engle (1982) and Bollerslev (1986)].

2.1 On the ratio variance test

The ratio variance test used to evaluate the RW3 hypothesis is built

on the following argument: If a series of returns compounded continuously

do not show linear autocorrelation, then the variance of the sum of

returns of periods must be equal to times the variance of

one period return.

For example, consider the accumulated returns of two periods:

| (1) |

Then the variance ratio is defined by

| (2) |

can be used as a measure of the efficiency with which the time series satisfies the random walk scenario. In addition, if the process is stationary, that is, and , then

Note that if the time series satisfies RW3, then VR(2) is equal to

1.

In general, for periods it is obtained that

If the autocorrelations are higher than zero, the variance ratio is

greater than one, and if the autocorrelations are negative, the variance

ratio is less than one. The variance ratio test then seeks to determine

where VR(k) is different from one.

In the work of Lo and MacKinlay (1988), the variance ratio test became

a relevant statistical test. They proved the RW3 hypothesis using

a sample of weekly returns covering the period between 1962 and 1985.

They applied this test to two of the main index of the New York stock

market and a set of different portfolios sorted by size. They concluded

the random walk hypothesis was rejected for each of the considered

series.

In order to perform statistical inference from the statistic VR(k),

certain assumptions about the return generating process must be made,

and these assumptions must be consistent with the observed empirical

distributions of returns. In general, the assets return time series

showed time-dependent volatility and that the empirical distributions

of returns show leptokurtosis.

The above-mentioned aspects are in the proposal of the variance ratio

test considered by Lo and MacKinlay (1988). In fact, they explicitly

assume that returns are generated by a process of mixing [White (1980)].

The mixing assumption allows making inferences by using the

asymptotic distribution of the statistic.

It should be noted here that the inference proves all these assumptions

in a joint and unfolding way. Therefore, if the random walk hypothesis

is rejected, it might be because the process followed by return is

not a random walk one or because some of the model hypothesis assumed

for generating the returns process is wrong.

The VR test proposed by Lo and MacKinlay (1988) has other problems, such as:

a) The VR test is an asymptotic test; that is, it is valid in principle for an infinite sampling data size. Hence, it cannot be reliable for small finite sampling.

b) The VR test typically uses overlapping data to compute the variance

of the long-horizon returns. It adds difficulty to analyzing the exact

statistical distribution of the sample variance ratio.

After the contribution by Lo and MacKinlay (1988), certain improvements

of the inference of the VR test were proposed to surpass the above-mentioned

issues. In fact, a number of distinct tests done with samples of finite

sizes were proposed, for example:

-

•

A modified ratio variance test [Chen and Deo (2006)].

-

•

A test based on ranking and sign changing [Wright (2000)].

-

•

A test that uses subsample methods [Whang and Kim (2003)].

-

•

The bootstrapping method [Kim (2006)].

These tests have been used to estimate the empirical distribution

of ratio-variance statistics and to improve the inference process.

On the other hand, the test by Lo and MacKinlay (1988) is considered

a simple test that can be applied in time intervals of different spans

(for example 2, 4, 8, and 16 week periods). Observe, that it is enough

the test is rejected for one of these intervals, in order that the

random walk hypothesis is to be turned away. Due that these tests

are applied independently and at the same time, this procedure leads

to an oversized test. Therefore, multiple comparison tests have been

proposed [Chow and Denning (1993)], [Richardson and Smith (1991)],

[Cecchetti and Lam (1994)].

2.2 On the nature of distribution of returns

Another issue in which literature has paid attention is, regarding

the random walk hypothesis, it is the nature of the empirical probability

distribution of price changes in financial assets. It is an essential

point, given that the nature of return distributions affects both,

the statistical test types used in the research and the interpretation

of the obtained results [Fama (1970)], [Kan (2006)],

[Kim (2006)].

One of the first models to study the evolution followed by financial

assets prices was developed by Bachelier (1900). This

model assumed that returns of financial assets are identically and

independently distributed with a normal distribution. Here, the price

changes are caused by the sum of a vast number of independent variables

associated with the information used by investors. They can be thought

of as a set of decisions in statistical equilibrium, with properties

relatively similar to a set of particles in statistical mechanics

[Osborne (1959)]. One implication of this is that,

when applying the central limit theorem, the compound returns are

normally distributed. However, the empirical distribution of the price

logarithms does not support the hypothesis of normality.

For the empirical distribution, it is typical to observe queues greater

than those predicted for a normal distribution. That is, the kurtosis

is significantly higher than 3, and the presence of bias is also observed.

It has been suggested that this behavior could be explained by a more

general family of distributions. Specifically, it is proposed that

changes in the logarithms of prices of financial assets can be represented

by Pareto stable distributions [Mandelbrot (1997)].

This type of distribution includes the normal distribution as a special

case and allows consideration of both the leptokurtosis and the bias

observed in the empirical distributions. Different empirical investigations

have concluded that Pareto stable distributions represent a better

description of the daily returns than the normal distribution [Fama (1965)],

[Kanellopoulou and Panas (2008)].

The family of Pareto stable distributions is characterized by four

parameters: The parameter that determines the shape of the

distribution, the parameter associated with the bias, the

parameter related to the scale, and the parameter

linked to the location. When and , the distribution

is normal. The Maldelbrot hypothesis (1963) states that empirical

returns of financial assets can be described by Pareto stable distributions,

with the parameter taking values between 1 and 2. The Pareto

stable distributions have two important properties:

- a)

-

They have stability or invariability under the addition; and

- b)

-

These distributions are the only asymptotic distributions for the sum of independent and identically distributed random variables [Fama (1965)].

However, a major problem arises if the compound returns are distributed

as Pareto stable distributions. In this case, in general, the estimated

parameter is less than 2, and the distribution has an infinite

variance. Therefore, many of the commonly used statistical tools that

assume finite variance, would not provide any conclusions.

In spite of this, most researchers have assumed that continuously

compound returns of financial assets have short-term dependencies

and finite variance, contrary to the behavior of the Pareto stable

distribution processes (for example see, Atchison et al. (1987),

Boudoukh et al. (1994), Lo and MacKinlay (1988) and White and Domowitz (1984)).

It is common to assume that asset returns can be represented as arising

from overlapped mixtures of normal distributions. In this case, returns

may have normal conditional distributions; some concentrated around

the average with lower variance and others with greater variance that

put more weight on the distribution queues.

These mixed distributions can explain the observed empirical unconditional distributions that show greater queues than those predicted by a normal distribution. Given that every moment of these distributions is finite, the central limit theorem applies, and asymptotically the long-term distribution will be normal [Campbell et al. (1997)]. This last argument is very important in making inferences regarding the parameters of each model, because it allows determination of the distribution of asymptotic probabilities of each parameter.

2.3 On non-synchronous trading

It is an empirical fact that the null hypothesis is rejected with

more force by portfolios whose small firms stock are more heavily

weighted than the greater firms stock (see for example Atchison et al. (1987),

Perry (1985), and Cohen et al. (1983)).

Small firms are characterized by the fact that they have trading that

is not synchronized, so different behavior of the CRSP Value-Weighted

and CRSP Equal-Weighted from the 1990s could rest on this fact. This

has led researchers to consider the effect of a non-synchronous trading

over the output of the variance ratio test.

The non-synchronous trading is an effect associated with two or more

time series. As a result, it appears that the transactions or movements

in the prices of different assets are updated at different time intervals.

Consider an asset time series that is recorded at fixed time intervals.

In general, the price time series is updated each time interval as

a result of a subjacent trading process. But typically for small companies,

this process is not necessarily done at each interval. In this way,

the data is not frequently updated by the trading process. This last

situation is called a non-trading effect. For example, in a daily

price series, normally the registered daily price is the closing price.

This closing price is normally the toll of the last transaction made

during the day. Also, if there is no asset trading during that day,

the end price is then the closing price of the previous day.

The non-trading price of an individual asset and the fact that some

assets register their price changes non-synchronously can modify the

estimation of statistical parameters. For instance, the individual

asset autocorrelations or cross-autocorrelations between individual

assets are modified, among other variables.

Non-synchronous trading may induce a significant spurious correlation

in stock returns and create a false impression of predictability in

asset returns. It also affects the results of the variance ratio test

(see for example, Mech (1993), Perry (1985),

Campbell et al. (1997) and Lo and MacKinlay (1988)).

Theoretical models have been proposed to estimate the autocorrelation

based only on the non-synchronous trading effect. These findings indicate

that, the theoretical impact is significantly lower than that which

has been empirically observed. In this way, this effect alone cannot

explain the rejection of the random walk null hypothesis. (see for

example Atchison et al. (1987), Conrad and Kaul (1988),

Lo and MacKinlay (1990) and Mech (1993)). These

models suppose that the individual assets have homogeneous characteristics,

that is, the non-trading probabilities associated with different assets

are identical.

However, in other research, heterogeneous individual asset characteristics

have been considered. For instance, Boudoukh et al. (1994) used

the model of Scholes and Williams (1977) to estimate the theoretical

autocorrelation induced by non-synchronous trading. Here, the non-trading

probabilities were different for each asset included in the portfolio.

They estimated that the autocorrelation induced by non-synchronous

trading for equally weighted portfolios could reach a 17.82%.

These models have also been used to value the impact of non-synchronous trading over the statistical inference process. Specifically, the focus in Lo and MacKinlay (1988) and Lo and MacKinlay (1990) was to determine whether non-synchronous trading can lead to rejection of the random walk null hypothesis. These authors concluded that this effect is so negligible to be the cause of a null hypothesis rejection. It is important to note that these authors considered:

-

•

Asymptotic estimation of the parameters

-

•

Infinite portfolio asset size

-

•

A particular price model as valid and

-

•

In general, individual homogeneous features assets.

All of the above-mentioned studies considered an asymptotic behavior and assumed that the portfolios were efficient. Therefore, there was only systematic risk. However, in practice, statistical inference should be performed with finite-sized samples. In this case, the values of the parameters and their associated errors were estimated with the assumption that the pricing model used was the correct one. This simplified the analysis, but made the inference outcomes dependent on the accuracy of the price model.

2.4 The portfolio effect

The properties of an index depends on the multivariate process followed

by financial assets that constitute them and the individual weight

assigned to each asset.

Consider the typical case in which it is assumed that the return of

assets follow a multivariate normal process , where

is the vector of expected returns of assets and is the covariance

matrix between return of assets. Therefore, to study the behavior

of an asset portfolio, we must estimate values of the average

returns and the values of the covariance matrix

.

When there is non-synchronous trading, the potential bias in the estimation

of parameters are added to the estimation problem. Risk estimation

and non-synchronous trading could have a strong impact on the performance

of asset allocation models.

In addition, when there is non-synchronous trading, crossed autocorrelations

between assets which are detectable even though the subjacent correlation

between assets is just contemporary [Fisher (1966)].

This effect is intensified when the observation interval decreases.

On the other hand, it has been reported that when the observation

period decreases, approaching zero, correlations between assets tends

to be zero [Epps (1979)].

Diverse studies have explored the effects that non-synchronous trading

may have on portfolio autocorrelation. Scholes and Williams (1977),

Dimson (1979), and Cohen et al. (1983) showed that

the non-synchronous trading effect causes an underestimation of the

betas in financial assets. They also proposed methods to mitigate

this effect. Later, Atchison et al. (1987) and Lo and MacKinlay (1990)

estimated the theoretical correlation induced in portfolios by non-synchronous

trading and concluded that it was significantly lower than which had

been empirically observed. In particular, Atchinson et al. (1987)

estimated the theoretical non-trading induced autocorrelation to be:

a) 4% for the NYSE Equal-Weighted Index, and

b) 2% for the NYSE Value-Weighted Index.

The observed empirical correlation values were 28% for the NYSE

Equal Weighted index and 16% for the NYSE Value Weighted index. Similar

results were reported by Lo and MacKinlay (1990).

For the estimation of portfolio autocorrelations, in the above models

it was assumed that the portfolio contained infinite assets and that

it was entirely diversified. Recently, Chelley-Steeley and Steeley (2014)

conducted research on the effects of non-trading on autocorrelations

considering portfolios of finite size. They concluded that the autocorrelation

induced by non-trading was influenced by non-systematic risks.

3 The Model: Specification of the Ratio Variance Test

In the section following, we review the ratio-variance test developed

by Lo and MacKinlay (1988).

Let be the price of a financial asset and the process followed by its logarithm at time t. The null hypothesis that follows a random walk can be expressed through the following recursive relationship:

| (3) |

where is a parameter of arbitrary tendency and

is a random perturbation. It is assumed that for every value of t

the error expected value is zero [].

An important property of a random walk is that its variance grows linearly with the observational time length. That is, the variance of the return of the two periods is twice the variance of one period. This feature is essential to prove the hypothesis of the random walk. It is assumed that time intervals are equally spaced and that there are (2n + 1) observations of in each interval. Therefore, the average and variance can be estimated through the relations:

| (4) |

| (5) |

| (6) |

where and correspond to the maximum likelihood

estimators of and and correspond

to an estimator of that only uses the subset of (n +

1) observations and that formally corresponds

to ½ of the two-period variance.

However, using these estimators for the variance has two drawbacks.

The first one is that these are biased estimators, and the second

one is that when a higher period of observations are utilized, the

sample data length decreases.

To improve these aspects, Lo and MacKinlay (1988, p. 46) proposed using the following estimators for variance:

| (7) |

| (8) |

| (9) |

where is an unbiased estimator of the variance

of a period, is an unbiased estimator of the

variance of q periods, and m is the number of observations used in

the variance estimation less one. This turns the variance estimators

into unbiased ones, and reduces the inaccuracy of estimators when

using data with overlaps [Lo and MacKinlay (1988)].

By using these last expressions, the ratio-variance test (considering the variance of q periods and q times the variance of one period) can be calculated as:

| (10) |

where the statistic must be zero to satisfy the random walk null hypothesis. Additionally, can be expressed as:

| (11) |

where , is the linear autocorrelation of order of the time series, defined by:

| (12) |

Given that there is a growing consensus that the volatility of the

financial series changes over time, it is important to consider this

fact in the inference process for the statistic.

In order to incorporate these volatility effects, Lo and MacKinlay

(1988, p. 48) used the approach developed by White (1980)

and White and Domowitz (1984). This is a rather general approach

that does not require normality in returns and allows temporal nonlinear

auto-dependence. It is assumed that temporal nonlinear autocorrelations

approach to zero when the time interval grows. Therefore, Lo and MacKinlay (1988)

assumed that deviations of returns about its mean follow a process

with short-term time dependencies, as used in White (1980)

and White and Domowitz (1984). Explicitly, it is supposed that:

- a)

-

For every t, and for some value of

- b)

-

The is a mixing with coefficients of the size or it is mixing with coefficients , with , such that for every there is some for which

- c)

-

- d)

-

For every t for any

Under these assumptions, we can calculate the statistical ,

which considers asymptotic behavior and in which short-term dependencies

are canceled:

| (13) |

Since is approaching zero under the null hypothesis,

we only need to calculate the value of the asymptotic variance of

this statistic. Considering that this set of hypotheses assumes that

the autocorrelations are asymptotically non-correlated,

it is possible to calculate the asymptotic variances of each autocorrelation

and therefore the variance of the statistical .

This is because according to expressions (10) and (11), the statistical

can be considered a weighted average of the autocorrelations

of the first lags.

Therefore, it is possible to calculate the asymptotic variance of each autocorrelation as:

| (14) |

Then the asymptotic variance of the statistical is calculated as:

| (15) |

Considering the asymptotic theory, a statistical z can be calculated as:

| (16) |

and has a normal distribution. Now this statistical can

be used to test the null hypothesis. Specifically, if the value of

the statistical is outside the limits of

then the hypothesis of random walk is rejected with a 95% confidence

level.

Before using the random walk test, a descriptive statistical analysis of the time series will be carried out.

4 Evolution of result of the variance ratio test

4.1 Data Characterization

The analysis was performed using a weekly data series from January 7, 1950, to March 28, 2013, including

-

•

CRSP SP500 market value-weighted;

-

•

CRSP NYSE/AMEX/NASDAQ/ARCA weighted by market value; and

-

•

CRSP NYSE/AMEX/NASDAQ/ARCA equally weighted.

These indices show the evolution of the weighted average of a significant

part of the shares traded on the New York exchanges. The difference

between indexes depends on two factors:

1. The relative weight of each stock included in the index; and

2. The type of assets that make up the index.

The table below shows some basic statistics of two of the indexes

considered.

| Statistic | CRSP Equally Weighted | CRSP Value Weighted |

|---|---|---|

| Min | -28.8% | -20.24% |

| Max | 14.77% | 12.64% |

| Mean | 0.348% | 0.198% |

| Standard Deviation | 2.095% | 2.080% |

| Skewness | -1.0652 | -0.7826 |

| Kurtosis | 12.0012 | 10.1382 |

It was observed that continuously compounded return of the CRSP Equally

Weighted Index had a higher average, higher standard deviation, higher

bias, and higher kurtosis than the CRSP Value-Weighted Index.

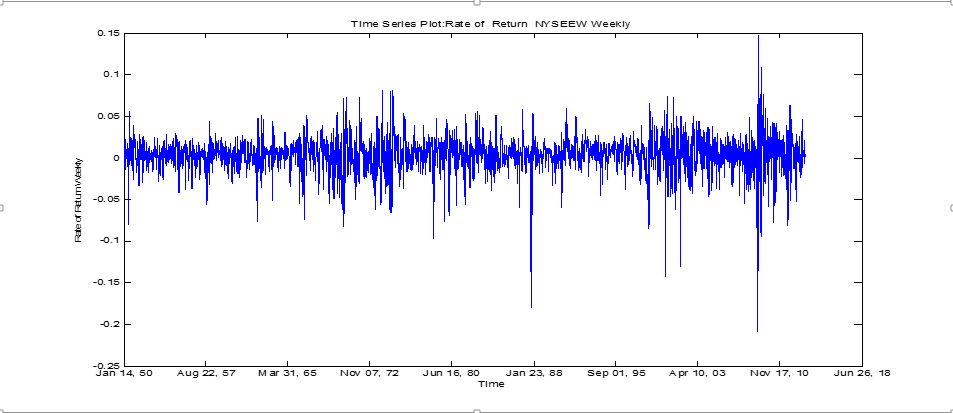

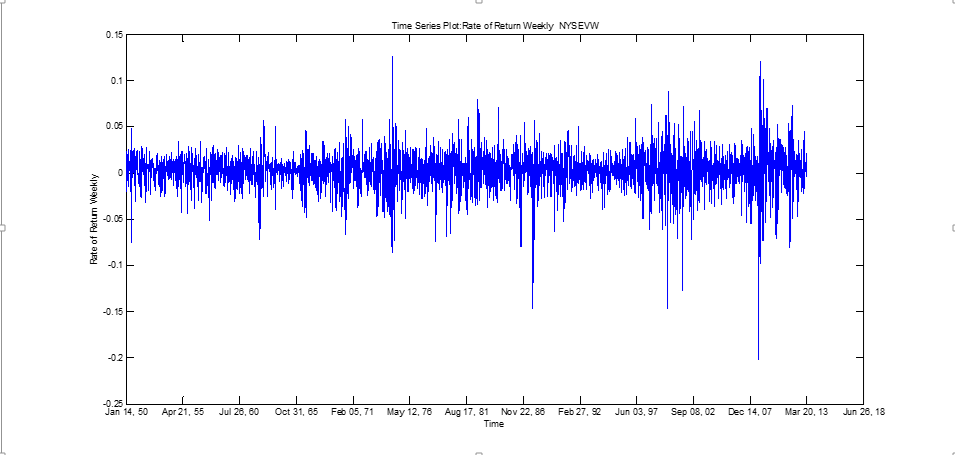

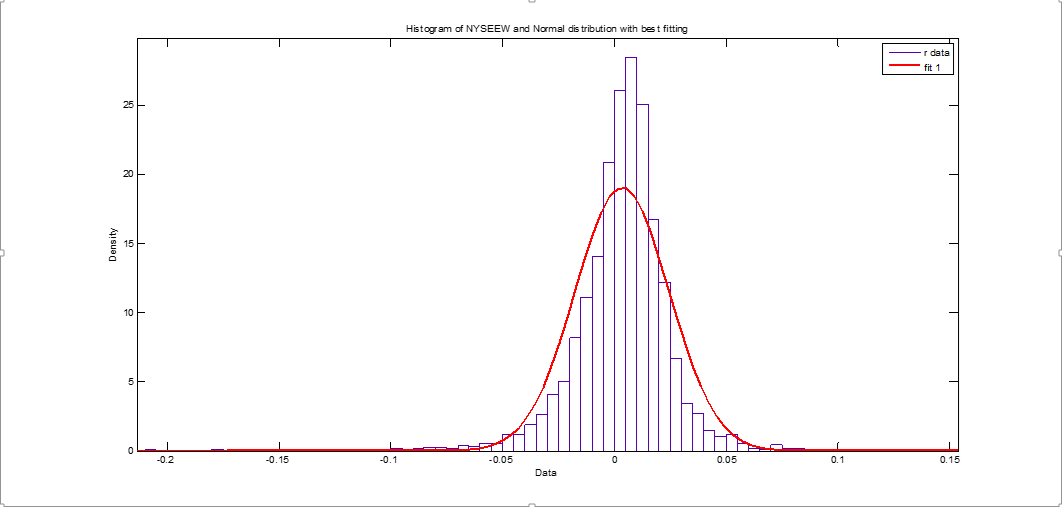

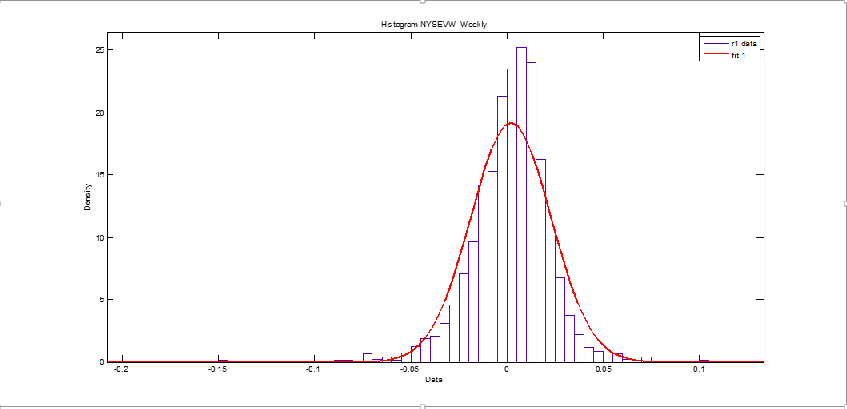

The figures below show time series, histograms, linear autocorrelations,

and quadratic autocorrelations associated with continuously compounded

returns of the CRSP Equal Weighted and CRSP Value Weighted indexes.

From these figures, it is possible to deduce that:

- a)

-

The returns of both indexes have time-dependent volatility variations (Figures 1 and 2);

- b)

-

The empirical distribution of returns moves away from the normal distribution and shows high levels of leptokurtosis (Figures 3 and 4);

- c)

-

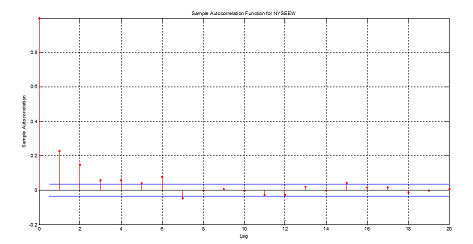

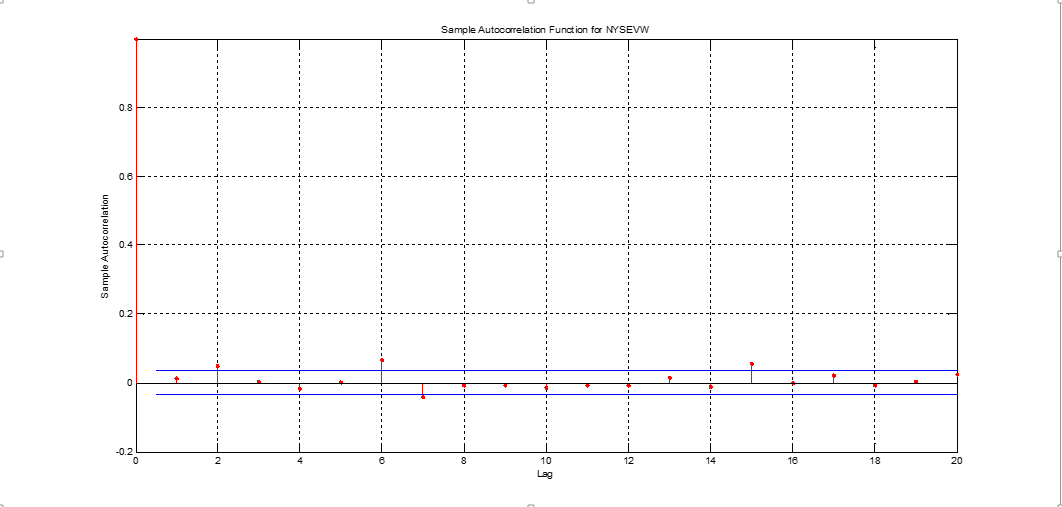

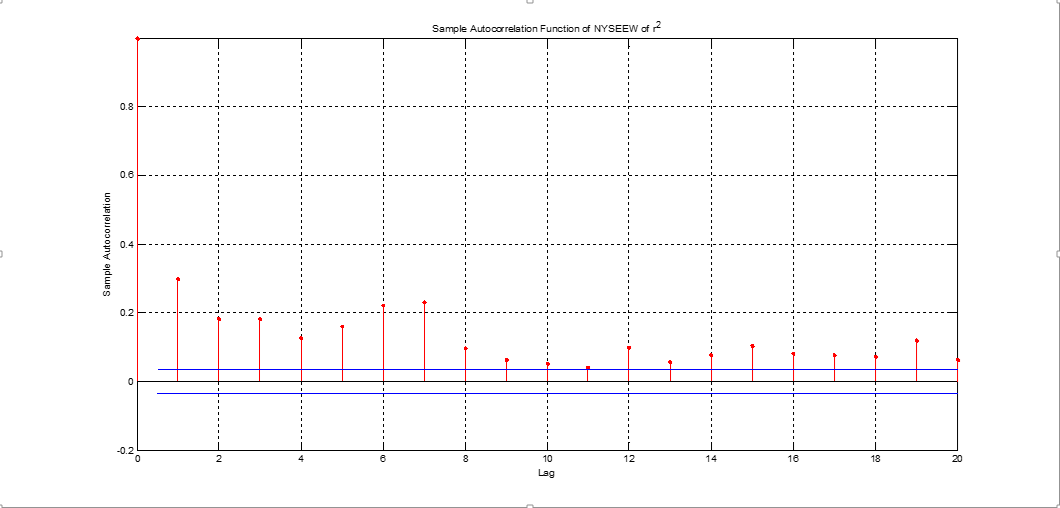

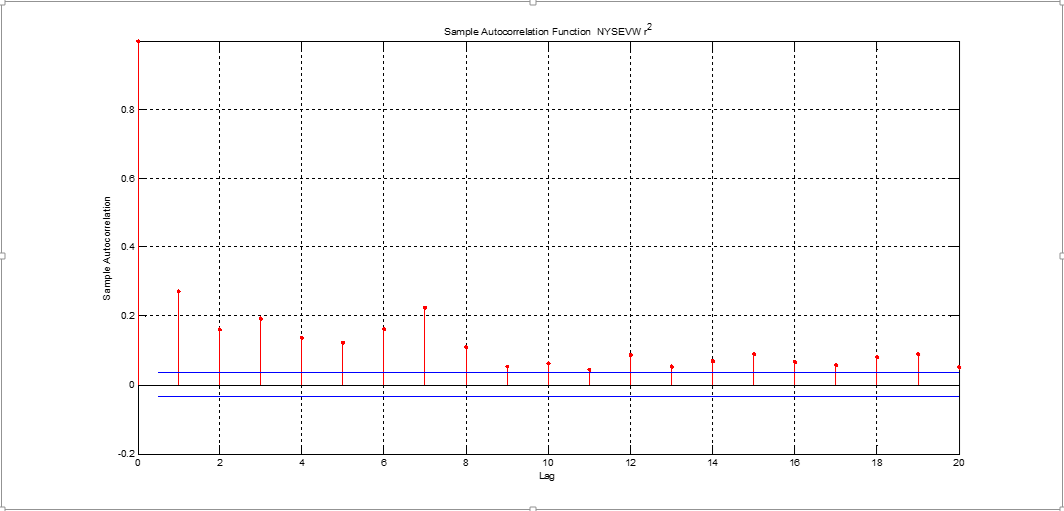

The linear autocorrelations for the CRSP NYSE AMEX NASDAQ ARCA Equally Weighted index show non-zero values at the first time lags (Figure 5)

- d)

-

The linear autocorrelations of the CRSP NYSE AMEX NASDAQ ARCA Value Weighted are negligible for all lags (Figure 6); and

- f)

-

The autocorrelations of the square of the rate of return are higher than zero for both index (Figures 7 and 8). It is possible to estimate that these autocorrelations are still significantly different from zero after 20 lags.

- g)

-

The above-mentioned issues are consistent with a stochastic process in which the variance changes in time with some degree of predictability.

4.2 Analysis of the results

The results of applying the variance ratio test to the indices: CRSP SP500, CRSP NYSE/AMEX/NASDAQ/ARCA Value Weighted and CRSP NYSE AMEX NASDAQ ARCA Equally Weighted are shown below. The variance ratios were calculated using periods of 2, 4, 8, and 16 weeks for weekly data ranging from July 1, 1950 to March 28, 2013.

| q | 2 | 4 | 8 | 16 | |||

|---|---|---|---|---|---|---|---|

| ratio | 0.9795 | 1.0067 | 1.0082 | 0.9975 | |||

| Statistic Z(q) | -0.6635 | 0.1217 | 0.0993 | -0.0212 | |||

| Critical value | (+/-)1.96 | (+/-)1.96 | (+/-)1.96 | (+/-)1.96 | |||

| p-value | 0.507 | 0.9031 | 0.9209 | 0.9831 |

| q | 2 | 4 | 8 | 16 | |||

|---|---|---|---|---|---|---|---|

| ratio | 1.0132 | 1.0716 | 1.115 | 1.1202 | |||

| Statistic Z(q) | 0.4053 | 1.2321 | 1.3199 | 0.98 | |||

| Critical value | (+/-)1.96 | (+/-)1.96 | (+/-)1.96 | (+/-)1.96 | |||

| p-value | 0.6853 | 0.2179 | 0.1869 | 0.3271 |

| q | 2 | 4 | 8 | 16 | |||

|---|---|---|---|---|---|---|---|

| ratio | 1.2295 | 1.5243 | 1.8186 | 1.9693 | |||

| Statistic Z(q) | 6.305 | 8.1302 | 8.5506 | 7.2269 | |||

| Critical value | (+/-)1.96 | (+/-)1.96 | (+/-)1.96 | (+/-)1.96 | |||

| p-value | 0.000 | 0.000 | 0.000 | 0.000 |

The results shown in tables 2, 3, and 4 show that:

-

•

The null hypothesis of the random walk is not rejected for the SP500 and CRSP Value-Weighted indexes (both weighted by market value) with a significance level of 5%.

-

•

The null hypothesis is rejected for the CRSP Equally Weighted index.

These results differ from those reported in Lo and MacKinlay (1988,

pp. 52-54). They indicated that the null hypothesis was rejected for

the CRSP Value-Weighted index and the CRSP Equal-Weighted index. This

happened because they used weekly sample data from June 9, 1962 up

only to December 26, 1985. As will be shown below, until the 1980s,

the null hypothesis, in effect, was rejected for both indices. But,

after the 1990s, the null hypothesis was not rejected for the CRSP

Value-Weighted index.

The evolution of the behavior of the various indices was analyzed

using weekly sample data, from July 1, 1950, until March 28, 2013;

that is, 1,601 weekly windows (subsamples).

The first window began on July 1, 1950, and from that date, the following

1,601 weeks were considered. Then the p-value of the ratio-variance

test was calculated for each subsample. After that, the window moved

a week (the second subsample began on January 14, 1950) and the p-value

of the test was recalculated, and so on until the last window in the

sample.

In the following graphs, the p-values obtained for each of the 1,699

subsamples are reported. The vertical axis indicates the p-value for

each subsample and the horizontal one indicates the last date of each

subsample. We must remember that the null hypothesis is rejected in

the case when the p-value is less than 0.05. In this way, we can see

the evolution in the behavior of each index.

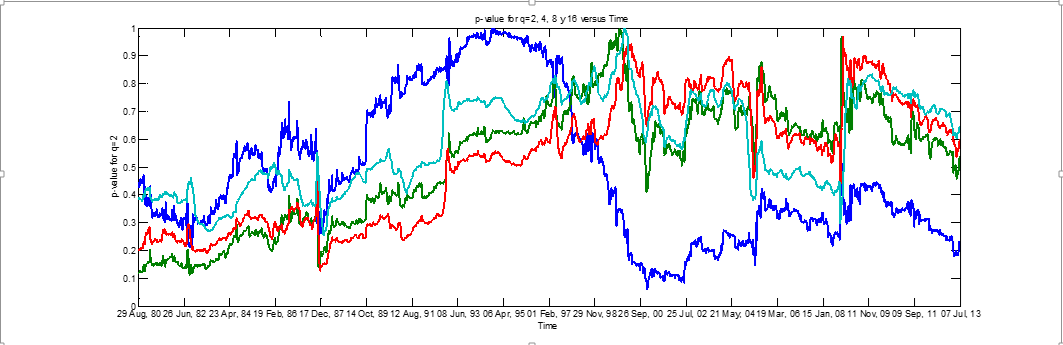

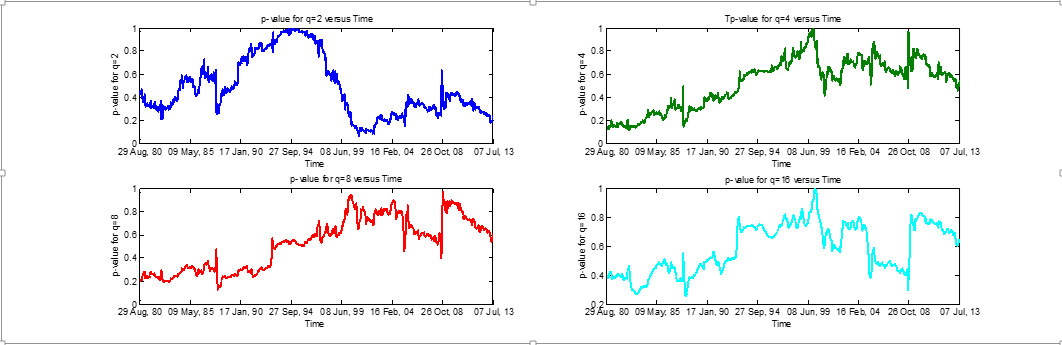

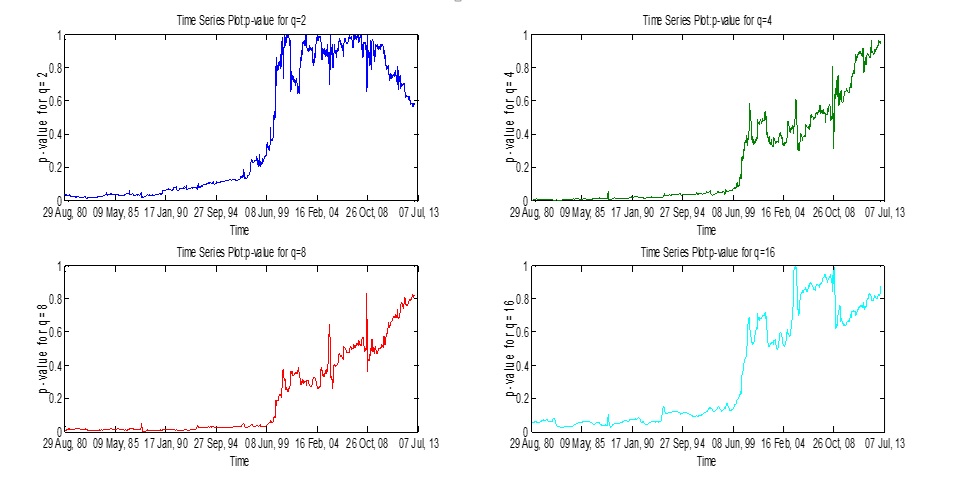

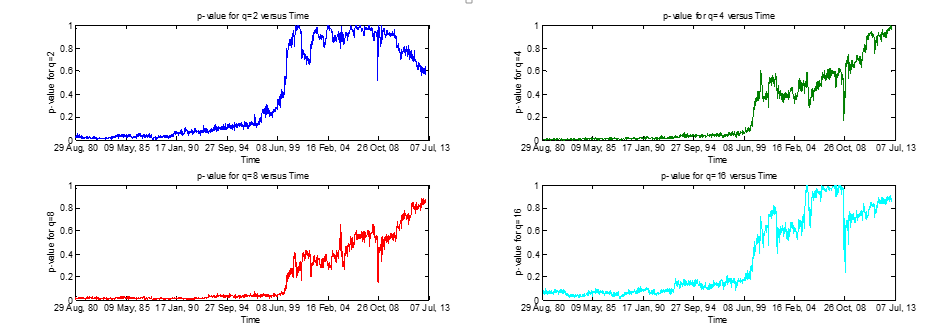

Figures 9 and 10 show the evolution of the performance of the SP500 index. Figure 9 displays the evolution of the p-value for q values equal to 2, 4, 8, and 16. The blue line in Graph 9 corresponds to q = 2, the green one to q = 4, the red one to q = 8, and the light blue one to q = 16. Each figure shows that the p-value of each series is never less than 5%, and therefore the null hypothesis was never rejected for any of the windows considered.

Figures 11 and 12 show the evolution in the behavior of the CRSP Equal-Weighted index. Figure 11 shows the evolution of the p-value for values of q equal to 2, 4, 8, and 16. Both figures show that the p-value of each series is less than 5% for all subsamples. These figures show that the null hypothesis is rejected in each of the windows considered.

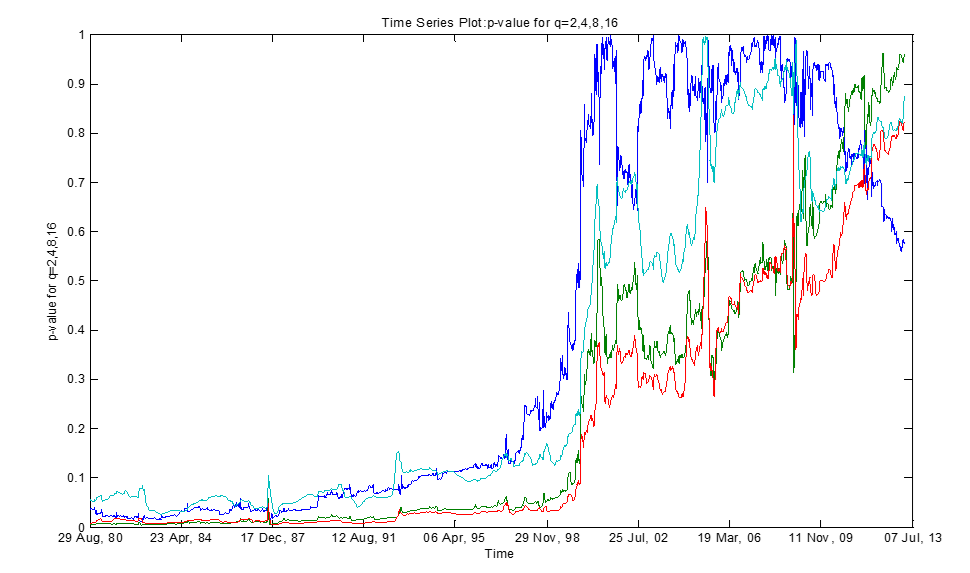

Figures 13 and 14 show the behavior of the CRSP NYSE Value-Weighted

index. These figures display the evolution of the p-value for values

of q equal to 2, 4, 8, and 16. Both figures show that the p-value

of each series is less than 5% until the 1980s. However, from the

end of the 1990s, the null hypothesis is not rejected for all of the

considered windows.

Thus, clearly the various index exhibit different behaviors from the

end of the 1990s. As we have seen, the SP500 and the CRSP NYSE Value-Weighted

are weighted by market value of the shares that constitute them. In

this case, a higher weighting is given to stocks of large corporations

and a low weighting to smaller ones.

On the other hand, for the CRSP NYSE Equal-Weighted index, the same

assets of the CRSP Value-Weighted are included, but this time with

equal weights. For this reason, the different behavior of these two

index starting from the 1990s has our attention.

To explain these divergent behaviors, various factors can be postulated, such as:

- i)

-

Different behaviors between the assets of lower market value and the assets of companies of greater market value;

- ii)

-

A change in the behavior of assets with higher market value;

- iii)

-

Problems with the power of the ratio-variance test when using finite samples and overlapping data; and

- iv)

-

Returns generating processes with different characteristics to those assumed in the null hypothesis test, among other factors.

It is also possible that the cause of this different behavior since

the 1990s is due to problems with the statistical test used. To determine

if this was the case, another test that is statistically more robust

for finite size samples and overlapping data will be used.

Although the implementation of the ratio-variance analysis is relatively straightforward, performing the statistical inference process is not so simple. One of the major complications for this test is the fact that the inference uses:

- a)

-

An asymptotic distribution of the statistic; and

- b)

-

Overlapping data to calculate variances for periods of time exceeding a period.

As we saw above, the use of overlapping data was suggested by Lo and

MacKinlay (1988, p. 46) to improve the power of the test. However,

overlapping data produces difficulties for the inference analysis

[Richardson and Smith (1991)]. In addition, the sample sizes

used were finite. This had the implication that the empirical distribution

of the statistic may have been quite far away from the asymptotic

distribution.

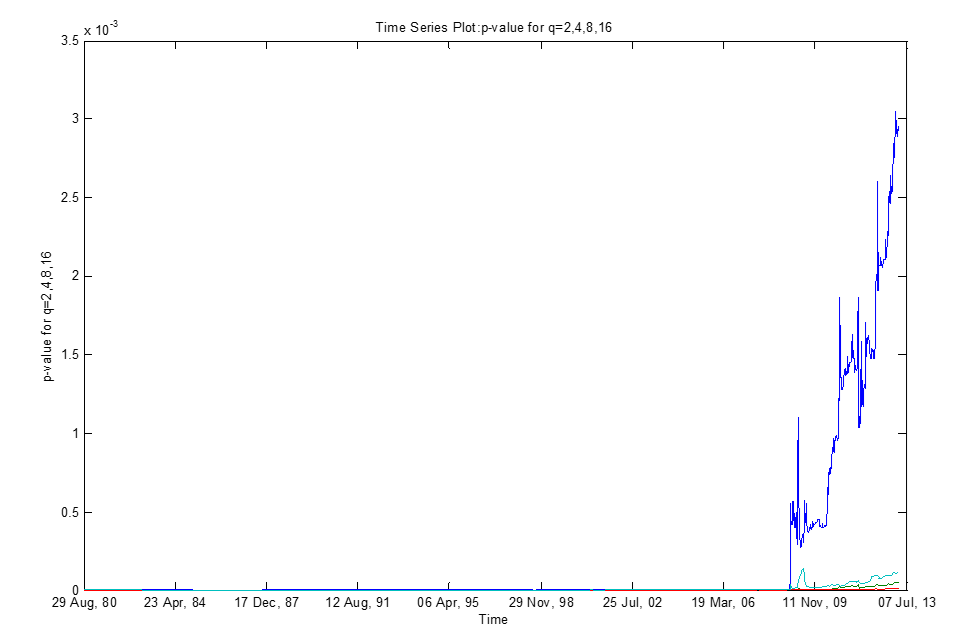

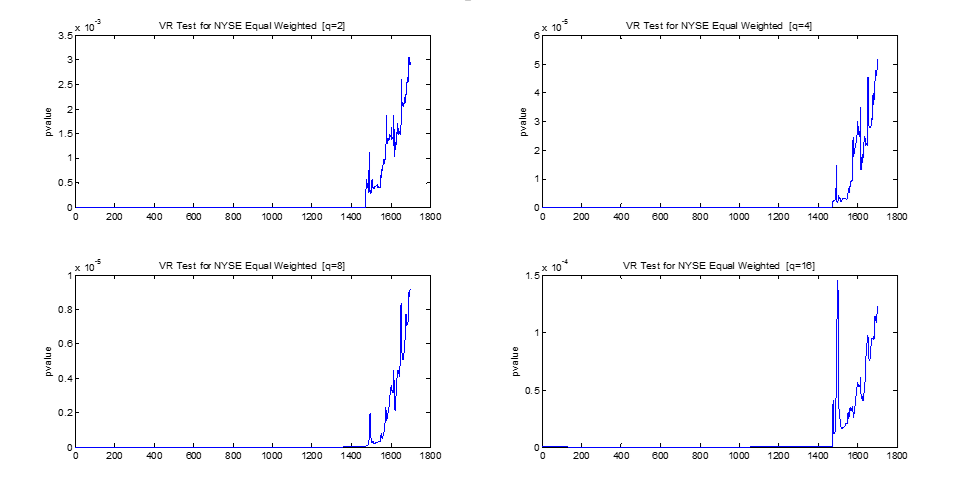

The variance ratio test proposed by Kim (2006) is a robust test for finite sample sizes and overlapping data. This test uses the bootstrapping method to estimate the empirical distribution [Efron (1979)]. Therefore, it makes an inference using the empirical distribution of the statistic and not asymptotic distribution. The consequences of applying this last robust test to the CRSP Value-Weighted indices and the CRSP Equal-Weighted are shown:

Charts 15 and 16 show the results of applying the ratio-variance test

by Kim (2006) to CRSP NYSE Equal-Weighted and CRSP NYSE

Value-Weighted indexes.

These findings are similar to those mentioned above. Charts 15 and 16 show the same behavior again:

- a)

-

The null hypothesis is rejected in all windows for the CRSP NYSE Equal-Weighted Index.

- b)

-

It is not rejected for index CRSP NYSE Value-Weighted starting from the end of the end of the 1990s.

Thus, these results confirm those obtained with the initially applied test, and therefore the difference between the indexes behaviors is not a problem of the statistical test and must be explained by other factors.

4.3 Summing up the historical evolution of results of variance ratio test

The question of whether the financial asset prices come after a random

walk or are a martingale-type sequence has strong implications on

the efficiency of marketplaces.

If the difference in the logarithm of prices for financial assets

follows a random walk, then returns are not predictable, and investors

are unable to obtain higher profits consistently over time.

Critical studies carried out considering the information up to the

1980s allowed researchers to establish that the main index of the

New York Stock Exchange did not follow a random walk. The null hypothesis

is rejected for two of the major stock index.

However, when this study is carried out with a much wider sample, these conclusions can be refuted. The outcomes of using the ratio variance test on 1,699 1600 rolling windows (each composed of 1,601 weeks) permit us to express the following:

- a)

-

The null hypothesis is rejected for each sub-sample of the equally-weighted index (NYSEEW).

- b)

-

It is never rejected for the SP 500 index.

- c)

-

For the Value-weighted index (NYSEVW), the null hypothesis is rejected until the first part of the 1990s. But it cannot be refuted from that epoch to the present time.

The fact that the random walk null hypothesis is not refuted for the

CRSP Value-Weighted index from the end of the 1990s can have important

connotations and greater significance for investors. In fact, from

the point of view of traditional financial theories, this index is

commonly regarded as an estimator of the market portfolio and therefore

the manner in which investors should place their money in diversified

portfolios.

On the other hand, the CRSP Equal-Weighted index represents the evolution

of a portfolio in which the same amount of money has been put in each

component stock. This final portfolio is in theory seen as an inefficient

portfolio.

These results could endorse the thesis that, from the 1990s, the New York Stock Exchange market followed a random walk. Apparently, a structural change took place in this period in the NYSE.

5 A model of non-synchronous trading and portfolio effects

As shown above, the variance ratio test gives a different result when

applied to the equally weighted index (the null hypothesis is rejected)

from the index weighted by market value (the null hypothesis is not

rejected).

This research offers a simple model that could explain the differences

in behavior of the equally weighted index and index weighted by value.

For this purpose, non-trading, non-synchronous trading, and portfolio

effects will be considered.

The idea of the proposed approach is to study these phenomena considering

that the problem of inference must be performed:

- a)

-

With a finite size sample data,

- b)

-

With a portfolio with finite asset number, and

- c)

-

Without using any model of equilibrium prices.

It is assumed that the set of individual financial assets follows

multivariate normal process. The non-trading effect is introduced

to generate individual returns, and then its impact on the variance

ratio test is analyzed. The implementation of this approach is explained

below.

To capture the non-synchronous trading effect, we used a similar approach

to the one presented by Lo and MacKinlay, 1990, with the difference

that asymptotic behaviors were not considered, but instead the actual

problem of inference, was addressed using finite size samples.

For this, consider a set of assets with unobservable virtual continuously compounded returns at time . It is assumed that the virtual returns are generated by the following vector stochastic process:

| (17) |

where is the mean returns vector and is

constructed from independent and identically distributed random

variables with zero mean and covariance matrix . These virtual

returns would be observed if the asset was regularly traded on each

of the registration periods. It is assumed that, in each period ,

the asset i is traded with constant probability .

For each asset in the period , there is an observed return

, which depends on:

- a)

-

The virtual returns, and

- b)

-

Whether the asset is traded in each period.

The observed return is defined in the follow way:

For example, if the asset was not traded in the last three periods, the observed return would be:

- i)

-

if the asset was traded

- ii)

-

equal to zero if was not traded

On the other hand, the virtual price of a financial asset can be represented as:

| (18) |

and then the accumulated return in t periods shall be equal to:

| (19) |

In this form, the virtual price depends on the sum of all the past returns. However, when the financial asset is not traded, the observed price differs from the virtual price. The observed price is defined by:

| (20) |

and then, by (16) and (17) the accumulated observed return of an asset until the instant is equal to:

| (21) |

From a practical view, the original definition of observed returns is difficult to implement. But one can see that the observed returns and the accumulated observed returns are related by:

| (22) |

This last expression is a friendlier way to realize the simulation

process, and thus it will be used in the following analysis.

The process used to generate samples of time series of observed returns is the following:

- i)

-

A time series sample of virtual returns is generated using a multivariate normal process N(,V).

- ii)

-

Using this sample, another sample of accumulated virtual returns is generated.

- iii)

-

Using Equation (19), the accumulated time series of observed returns is generated.

- iv)

-

Then, with the accumulated observed returns series, a time series of observed returns is generated using equation (20).

The above algorithm is used to introduce the effect of non-synchronous

trading on the virtual returns time series. Note that this model could

be used to study other subjects, such as the incidence of non-synchronous

trading over the selection of portfolios and parameter estimation,

among others. In our case an equilibrium price model is not assumed

as in Atchison et al. (1987), Lo and MacKinlay (1990),

and Boudoukh et al. (1994). Our model allows the study of problems

considering finite size samples, without assuming asymptotic behaviors.

To appreciate the joint effect that non-synchronous trading and the portfolio have on the inference of the variance ratio test when the sample size is finite, several different two asset portfolios were built. Non-trading was introduced to only one of the individual assets. Later on, an estimation of the correlation in weekly profits induced by non-synchronous trading was undertaken, and the same results were obtained for a six-asset portfolio with heterogeneous features similar to those used in Boudoukh et al. (1994).

6 Main results of the effects of trading and portfolio on the VR test

6.1 Case with two financial assets

Estimates are made by means of the Monte Carlo simulation using MATLAB.

Samples of normal multivariate two-asset return series (of 5000 periods

long) were generated. The nontrading effect was applied only to the

second financial asset return series (). The nontrading

probability was set at zero for Asset 1 and 20 for Asset 2.

Samples of series of indexes returns were built according to:

| (23) |

where was the percentage of wealth assigned to the asset

with nontrading effect. The parameter can take the values:

.

We assumed that the mean of the vector returns was =[0.005,0.005],

the standard deviation of asset 1 was 0.005, and the standard deviation

of asset 2 was 0.02. The correlation factor can take values

between -1 and 1 and can change between simulations. We did this to

see what influence the correlation had on the variance ratio test

outcomes.

The simulation process goes as follows:

- i)

-

The correlation parameter took an initial value and would remain fixed, and for each of its values 10,000 multivariate time series simulations were generated.

- ii)

-

Each of these time series incorporated the non-synchronous trading effect.

- iii)

-

With these multivariate time series, one can construct a portfolio set by means of equation (20), so one has 10.000 different possible portfolio return series for each value of the parameter.

- iv)

-

The variance ratio test was applied keeping both and parameters fixed. The p-value was calculated for the 10.000 possibilities.

- v)

-

If the p-value is less than , the null hypothesis of the random walk is rejected.

After that, the reject frequency was plotted versus the and

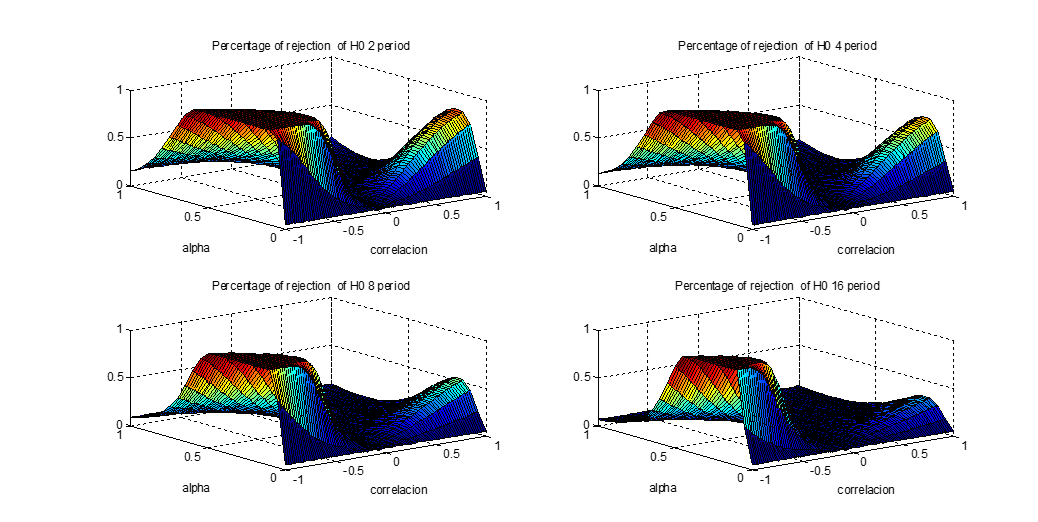

parameter values, as illustrated in Figure 17. It shows

the frequency percentage at which the null hypothesis was rejected

using the variance ratio test. This graphic shows that when the non-trading

effect was introduced, the variance ratio test rejected the null hypothesis

to a higher degree than when non-trading was not present.

It is possible to see in figure that the rejection of the null hypothesis was very strong when the correlation was negative. There was practically no rejection when the correlation was close to zero, and there was a significant increase of the rejection, as the correlation got closer to 1.

Figure 18 shows the frequency percentage at which the null hypothesis was rejected without non-trading effect. Note that when the time series did not consider the non-trading effect, the average value of rejection of the null hypothesis was closer to . More importantly, its value did not depend on the correlation or how to portfolio was built (the parameter).

The sensitivity of the variance ratio test was very strong to the

portfolio and non-trading effects for different correlation values

between assets. The only case in which its impacts were insignificant

was when the correlation between assets was close to zero.

Given that usually the correlation between financial assets is close

to 1, from here we focus on analyzing the portfolio and non-trading

effect for a case in which correlation between assets is equal to

. The case is considered representative of the current situation.

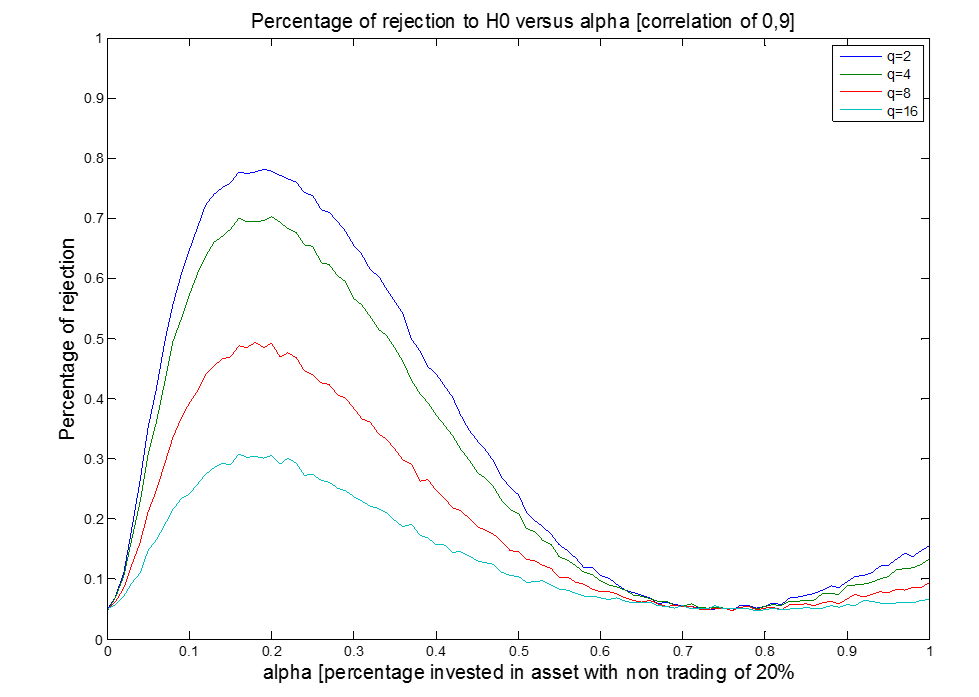

Figure 19 shows the results obtained when restricting the correlation value between the assets to a value equal to . The graphics show the percentage that the null hypothesis for the variance ratio test was rejected. The blue line represents the case of , the green line is the same but for , the red line is for , and finally the magenta line is for periods.

Figure 19 shows that the maximum percentage of null hypothesis rejection

was produced close to the 0.16 for the value. This rejection

was greater for the variance-ratio two-period test. Reasons for rejection

for this value are due to the positive autocorrelation.

The rejection percentage value of the null hypothesis was around 70

for = 0.16.

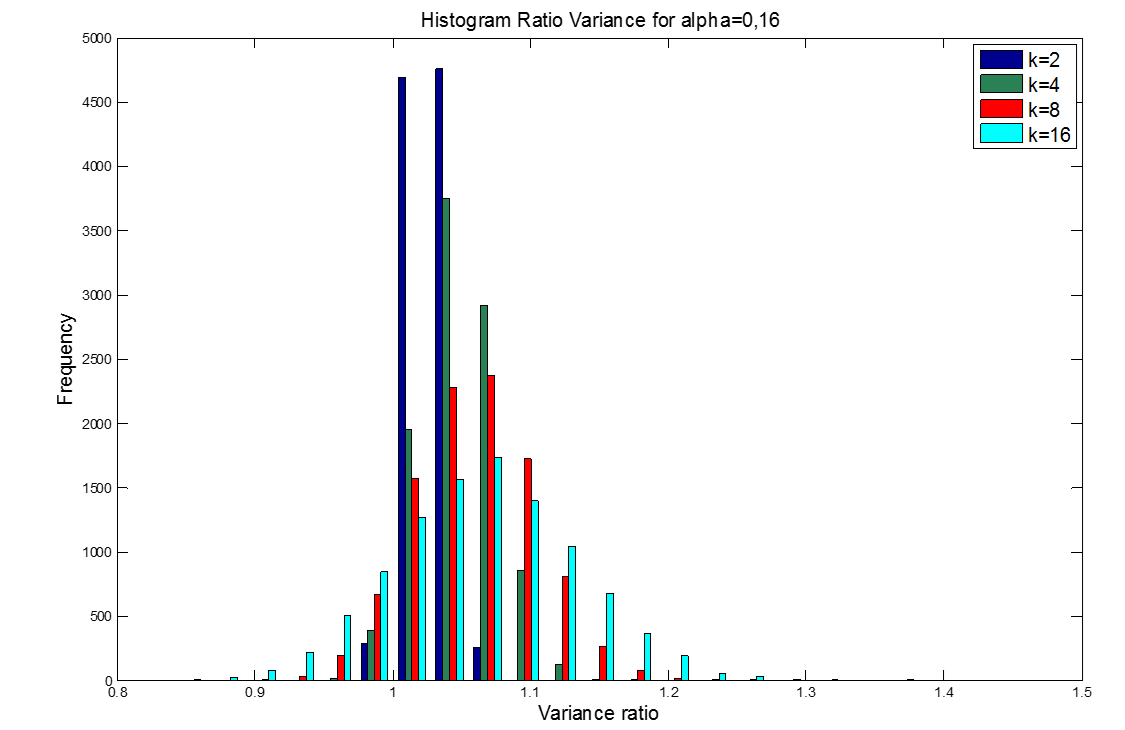

Figure 20 shows the histogram of the variance-ratio value for . The histogram illustrates how the statistical values of variance ratio of the 10.000 simulated trajectories were distributed.

Traditional models such as Lo and MacKinlay (1990) estimated the

theoretical impact that non-synchronous trading had on the inference

problem. These authors used the asymptotic behavior of the variance

ratio test statistic. Nevertheless, in this article, the complete

statistical distribution of the variance-ratio values was obtained.

This approach is more powerful than traditional ones because we can

obtain an average value for the variance ratio test and its frequency

distribution.

In fact, through simulations, one can visualize the different possible frequency distributions of the effect of non-synchronous trading for:

- a)

-

Different asset correlations (one can change the values); and

- b)

-

Different portfolio structures (one can change the values).

For example, in Figure 20, the average ratio-variance value for

was 1.07. But, Figure 20 also shows that in approximately 25

of instances, the variance ratio was larger than 1.1. This last piece

of information is very relevant to the statistical analysis because

it is possible in practice (when a single time series is used) that

the value of the observed variance-ratio statistic will be greater

than its expected value. This last fact can lead to incorrect inferences.

In short we have found out that the performance of the variance ratio

test is severely affected by the aggregated result of non-trading

and portfolio effects. However, it may be interesting to analyze how

the above-mentioned effects alter the statistical distribution of

the parameters associated with the asset return time series.

In order to appreciate the possible effect of non-trading on certain

parameters such as (a) asset correlation, (b) asset autocorrelation,

and (c) asset cross-autocorrelation, a simulation of 100.000 trajectories

based on a normal multivariate return series (of 5.000 observations

each) was carried out. Simulations were initially generated (without

non-trading effects) with a returns correlation between assets of

90.

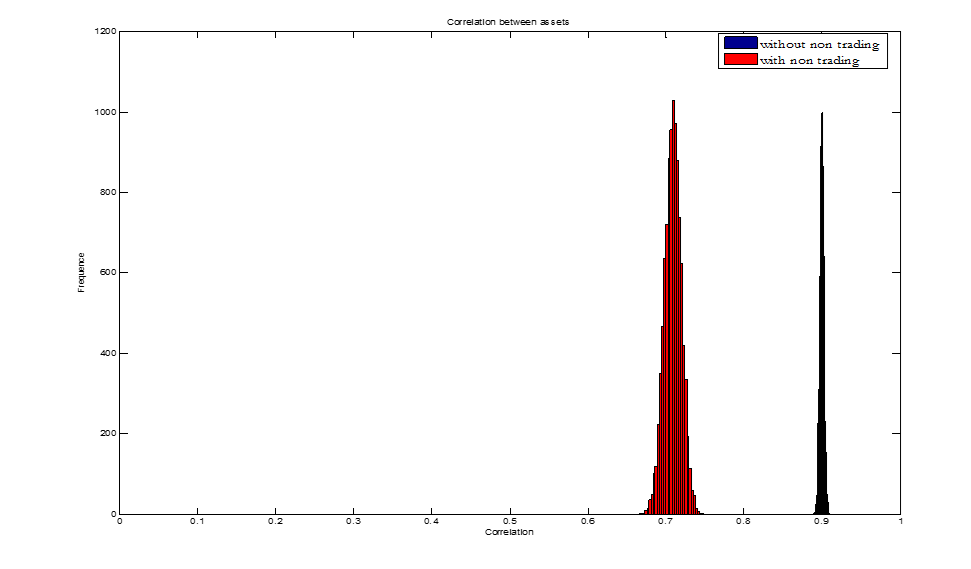

Figure 21 shows that the histogram of the correlation observed without non-trading effect (blue) has a mean of 90 and a standard deviation of 0.006. The histogram also shows the correlation between the assets when non-trading effects are introduced to one of the returns (red), with a non-trading probability equal to 20. In this last case, the average correlation was 0.689, and the standard deviation was 0.0271.

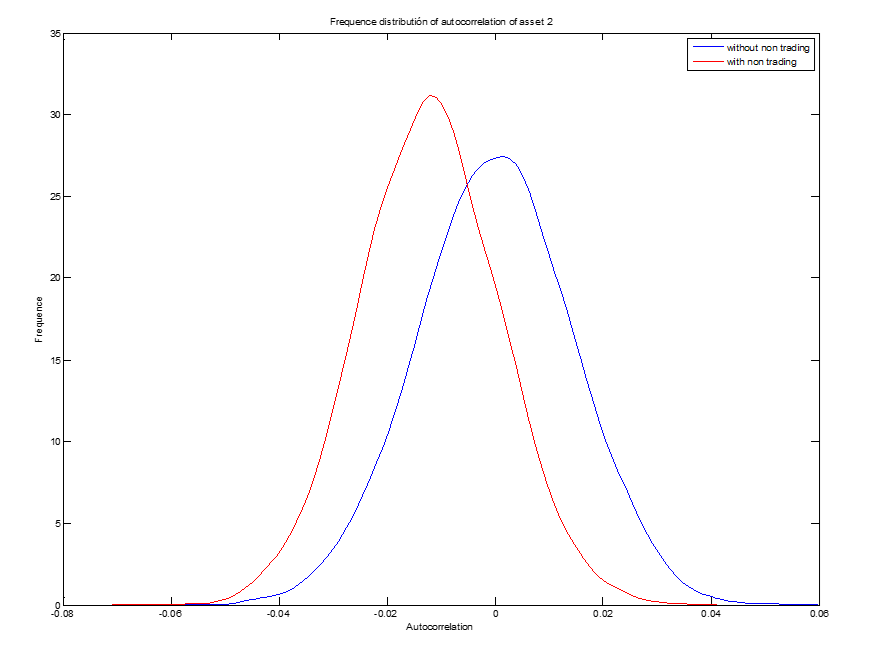

Figure 22 shows that autocorrelation observed in an asset with non-trading was slightly negative. The average autocorrelation without nontrading was -0.001, and the one with non-trading was -0.0453.

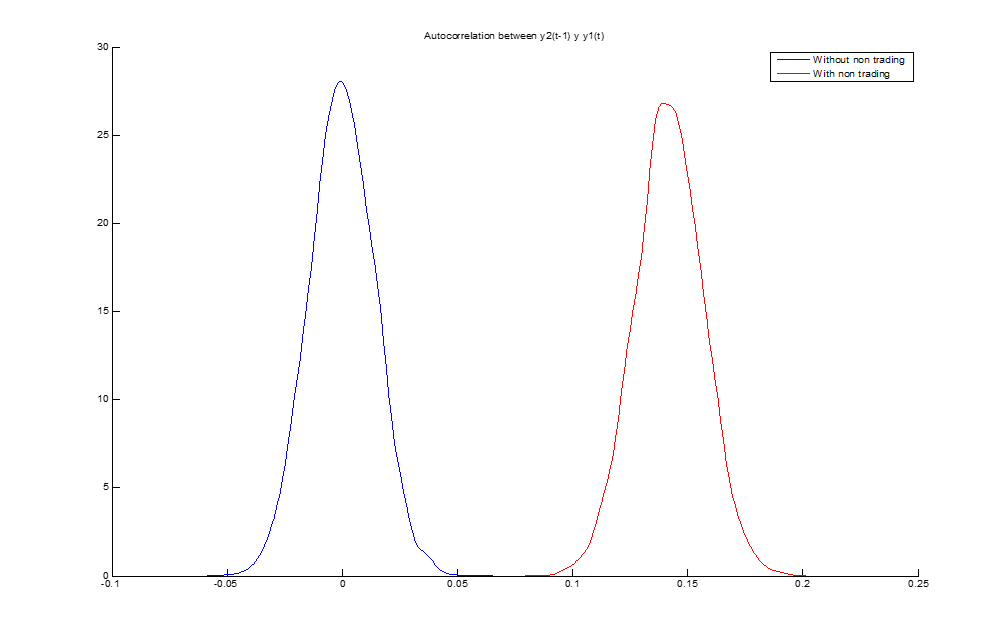

Figure 23 shows the cross-autocorrelation between asset returns and . The blue and red curves show the frequency distribution of cross-autocorrelation without and with non-trading, respectively. Mean crossed autocorrelation without non-trading is approximately zero, and it has a variation range between -0.05 and 0.05. Mean with nontrading is 14.2, with a variation range between 0.09 and 0.2.

6.2 Making sense of the experiment results

As mentioned previously, to prove the random walk hypothesis (for the stock market index) using a variance ratio test is equivalent to showing that portfolio autocorrelations are zero. As was observed, the rejection of the null hypothesis in the index was due to positive asset autocorrelation. To illustrate how non-synchronous trading can induce positive autocorrelation in a portfolio, consider the following expression for a portfolio autocorrelation:

| (24) |

where subject to , that is

| (25) |

Considering the case of an index that contains only two financial assets, the autocorrelation of portfolio is:

| (26) |

To see the incidence of non-synchronous trading in this portfolio, we introduced the non-trading effect on the second asset and then observed what happened with estimated values for some of the most important parameters of the portfolio returns. We assumed that the virtual returns (without non-synchronous trading effect) had a multivariate normal distribution with parameter and

Using these stochastic processes, a simulation of 10.000 trajectories was generated (each one of 5.000 periods) without non-trading. Mean values were calculated for cross-autocorrelations and correlations between individual assets. Also, standard deviations were computed. On average, the autocorrelations were equal to zero, and correlations between assets and variance between assets remained the same. The average values of these parameters is shown in row 2 of Table 5. Next, we will perform the same exercise, but this time we will introduce a 20 non-trading to Asset 2. The average values of this parameter is shown in row 3 of Table 5.

| nontrading | |||||||

|---|---|---|---|---|---|---|---|

| Without | 0.05 | 0.02 | 0.9 | 0.0 | -0.0009 | 0 | -0.0011 |

| With | 0.05 | 0.02 | 0.689 | -0.0008 | 0.1349 | 0 | -0.0453 |

As shown in Table 5, non-trading on the second asset generates:

- a)

-

A slight increase in the standard deviation of asset 2;

- b)

-

A reduction in the asset correlation (from 0.8999 to 0.689);

- c)

-

A significant rise in cross-autocorrelation between assets 2 and 1, growing from -0.0009 to 0.1349; and

- d)

-

A negative autocorrelation in asset 2.

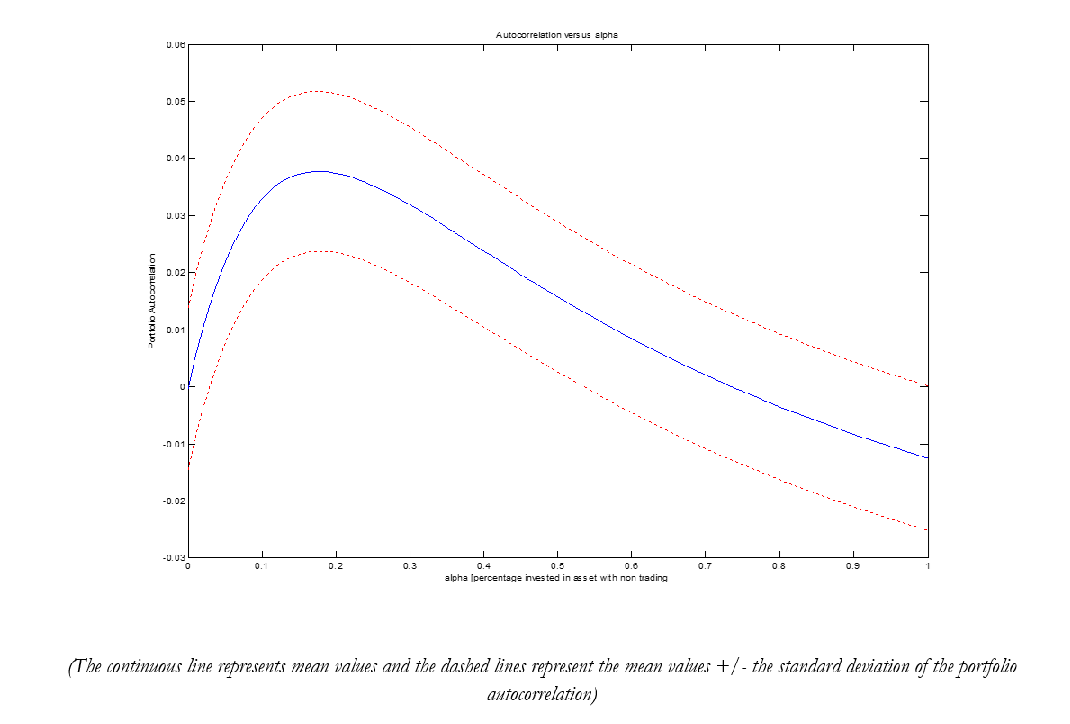

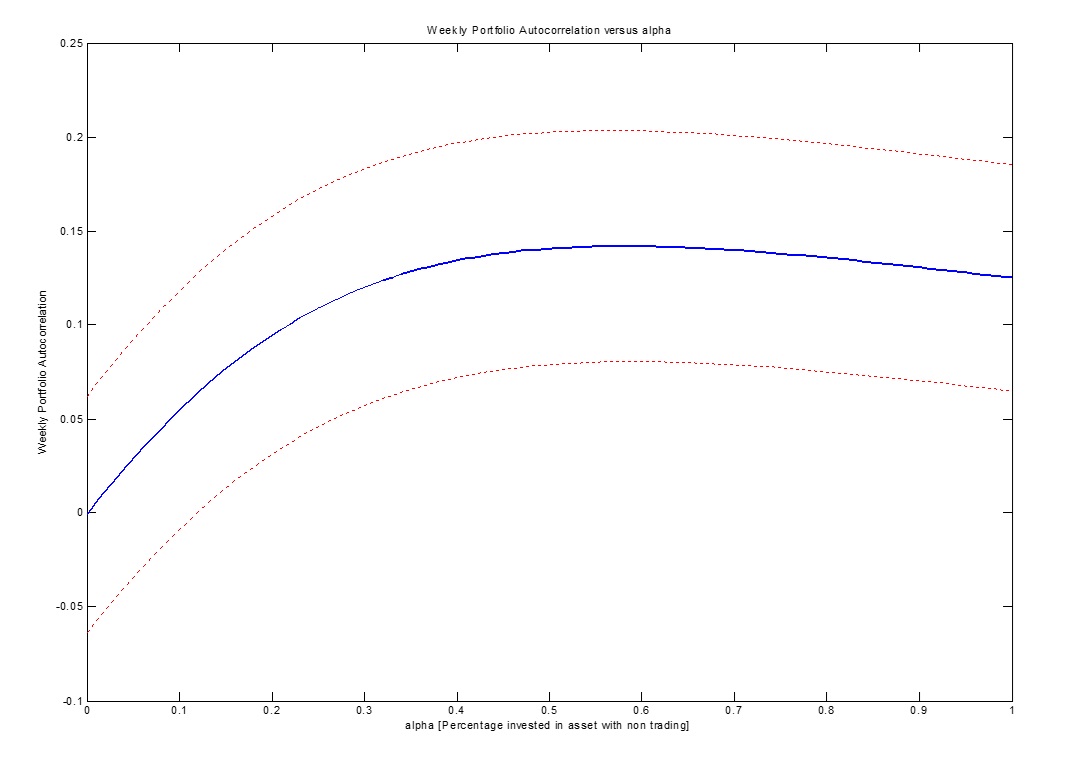

The previous example demonstrated that non-synchronous trading can induce negative autocorrelation in individual assets and it can cause positive cross-autocorrelation between the assets. Furthermore, it can induce positive autocorrelation in the stock market index. With the calculated parameter one can compute the portfolio autocorrelation using equation (25). These values are shown in Figure 24.

Figure 24 shows that the autocorrelation induced by non-synchronous trading is considerably higher than zero for some portfolios. The blue line plots the average portfolio autocorrelation, and the red dotted lines plot the mean of the portfolio autocorrelation +/- twice its standard deviation. The intensity of this phenomenon increases when the asset number increases within the portfolio.

6.3 Weekly portfolio returns autocorrelation estimation. Six-asset cases.

Hereafter, the estimation of theoretical autocorrelation induced by non-synchronous trading was undertaken considering a six-asset portfolio that had:

- a)

-

Heterogeneous features, and

- b)

-

Non-trading daily probabilities equal to those used by Boudoukh et al. (1994).

In this way, non-trading time series of daily returns were generated. Then, weekly returns were calculated as the sum of 5 daily returns and from them weekly autocorrelations of different portfolios were estimated. The portfolios were built explicitly as222There are multiple ways to construct portfolios with six assets. However, in this case, to illustrate the non-trading and portfolio effects, we chose this particular method.

| (27) |

Table 6 shows the values of parameters used. We assumed that assets 1, 2, and 3 had characteristics similar to assets of bigger firms and that Assets 4, 5, and 6 had characteristics similar to assets of smaller firms333 is the non-trading probability.

| Correlation Matrix | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Assets | |||||||||

| Asset | Return | Volatility | 1 | 2 | 3 | 4 | 5 | 6 | |

| 1 | 0% | 0.5% | 0.5% | 1 | 0.9 | 0.9 | 0.9 | 0.9 | 0.9 |

| 2 | 0% | 0.5% | 1% | 0.9 | 1 | 0.9 | 0.9 | 0.9 | 0.9 |

| 3 | 0% | 0.5% | 1.5% | 0.9 | 0.9 | 1 | 0.9 | 0.9 | 0.9 |

| 4 | 43% | 0.5% | 2% | 0.9 | 0.9 | 0.9 | 1 | 0.9 | 0.9 |

| 5 | 60% | 0.5% | 2.5% | 0.9 | 0.9 | 0.9 | 0.9 | 1 | 0.9 |

| 6 | 85% | 0.5% | 3% | 0.9 | 0.9 | 0.9 | 0.9 | 0.9 | 1 |

The simulation was done for a sample series of 10.000 daily returns, which consisted of 5.000 time points. Figure 25 shows the weekly autocorrelation induced by non-trading for the six-asset portfolio444The continuous blue line represents the mean values, and the dashed red lines the mean values two standard deviations associated with the portfolio autocorrelation.

As can be seen in Figure 25, the weekly portfolio autocorrelation depended on the portfolio structure. However, it is possible to see portfolios in which weekly autocorrelation induced by non-synchronous trading can reach values of 20 for some portfolios and autocorrelations lower than -5 for other ones. Given the latter facts, we can point out that the joint effect of portfolio and non-synchronous trading can explain both:

- a)

-

The high autocorrelations empirically observed in the CRSP NYSE equal weighted index (), and

- b)

-

The lower autocorrelations for the CRSP NYSE value-weighted index ()

7 Conclusions

In this paper, we analyzed the historical evolution of the acceptance

or rejection of the random walk hypothesis applied to the main stock

exchange index of NYSE. It has been shown that the random walk hypothesis

is rejected for each of the windows for 1601 weeks from 1950-2013

for the equally weighted index. However, for the index weighted by

market value, the hypothesis fails to be rejected from the late 1990s.

This shows a significant change in the behavior of the stock market

in New York.

The posibility that this divergent behavior between these index ought

to be explained by the combined effect of non-synchronous trading

and the portfolio, was explored. To investigate the feasibility of

this explanation we simulated the effects of these factors over two

and six assets portfolios . The samples were of finite size and the

characteristics of assets were assumed to be heterogeneous.

It was found that the combined non-trading and portfolio effects

seriously affected the performance of the variance ratio test. For

the case of the two-asset portfolio, the only case in which the variance

ratio test outcomes were independent of the non-trading process was

when the correlation parameter was close to zero.

The results show that when the correlation between assets was not

zero, the value of the statistical variance ratio test depended explicitly

on the way the asset portfolio was built, that is, it presented an

dependence.

The same conclusions were obtained for the six-asset portfolio. In

addition, it was found that the heterogeneity in the characteristics

of the individual assets increased the autocorrelation induced by

the non-synchronous trading.

Lastly, we can point out that the joint effect of portfolio and non-synchronous trading can explain both:

- a)

-

The high autocorrelations empirically observed in the CRSP NYSE equal weighted index (), and

- b)

-

The lower autocorrelations for the CRSP NYSE value-weighted index ()

References

- Atchison et al. [1987] Michael D Atchison, Kirt C Butler, and Richard R Simonds. Nonsynchronous security trading and market index autocorrelation. Journal of Finance, pages 111–118, 1987.

- Bachelier [1900] Louis Bachelier. Théorie de la spéculation. Gauthier-Villars, 1900.

- Bollerslev [1986] Tim Bollerslev. Generalized autoregressive conditional heteroskedasticity. Journal of econometrics, 31(3):307–327, 1986.

- Boudoukh et al. [1994] Jacob Boudoukh, Matthew P Richardson, and RE Whitelaw. A tale of three schools: Insights on autocorrelations of short-horizon stock returns. Review of financial studies, 7(3):539–573, 1994.

- Campbell et al. [1997] John Y Campbell, Andrew Wen-Chuan Lo, Archie Craig MacKinlay, et al. The econometrics of financial markets, volume 2. princeton University press Princeton, NJ, 1997.

- Cecchetti and Lam [1994] Stephen G Cecchetti and Pok-sang Lam. Variance-ratio tests: small-sample properties with an application to international output data. Journal of Business & Economic Statistics, 12(2):177–186, 1994.

- Chelley-Steeley and Steeley [2014] Patricia L Chelley-Steeley and James M Steeley. Portfolio size, non-trading frequency and portfolio return autocorrelation. Journal of international financial markets, institutions and money, 33:56–77, 2014.

- Chen and Deo [2006] Willa W Chen and Rohit S Deo. The variance ratio statistic at large horizons. Econometric Theory, 22(02):206–234, 2006.

- Chow and Denning [1993] K Victor Chow and Karen C Denning. A simple multiple variance ratio test. Journal of Econometrics, 58(3):385–401, 1993.

- Cohen et al. [1983] Kalman J Cohen, Gabriel A Hawawini, Steven F Maier, Robert A Schwartz, and David K Whitcomb. Friction in the trading process and the estimation of systematic risk. Journal of Financial Economics, 12(2):263–278, 1983.

- Conrad and Kaul [1988] Jennifer Conrad and Gautam Kaul. Time-variation in expected returns. Journal of business, pages 409–425, 1988.

- Dimson [1979] Elroy Dimson. Risk measurement when shares are subject to infrequent trading. Journal of Financial Economics, 7(2):197–226, 1979.

- Efron [1979] Bradley Efron. Bootstrap methods: another look at the jackknife. The annals of Statistics, pages 1–26, 1979.

- Engle [1982] Robert F Engle. Autoregressive conditional heteroscedasticity with estimates of the variance of united kingdom inflation. Econometrica: Journal of the Econometric Society, pages 987–1007, 1982.

- Epps [1979] Thomas W Epps. Comovements in stock prices in the very short run. Journal of the American Statistical Association, 74(366a):291–298, 1979.

- Fama [1965] Eugene F Fama. The behavior of stock-market prices. Journal of business, pages 34–105, 1965.

- Fama [1970] Eugene F Fama. Efficient capital markets: A review of theory and empirical work. The journal of Finance, 25(2):383–417, 1970.

- Fama [1991] Eugene F Fama. Efficient capital markets: Ii. The journal of finance, 46(5):1575–1617, 1991.

- Fisher [1966] Lawrence Fisher. Some new stock-market indexes. Journal of Business, pages 191–225, 1966.

- Grossman and Stiglitz [1980] Sanford J Grossman and Joseph E Stiglitz. On the impossibility of informationally efficient markets. The American economic review, pages 393–408, 1980.

- Jensen [1978] Michael C Jensen. Some anomalous evidence regarding market efficiency. Journal of financial economics, 6(2):95–101, 1978.

- Kan [2006] Raymond Kan. Exact variance ratio test with overlapping data. Available at SSRN 891680, 2006.

- Kanellopoulou and Panas [2008] Stella Kanellopoulou and Epaminondas Panas. Empirical distributions of stock returns: Paris stock market, 1980–2003. Applied Financial Economics, 18(16):1289–1302, 2008.

- Kim [2006] Jae H Kim. Wild bootstrapping variance ratio tests. Economics letters, 92(1):38–43, 2006.

- Lo and MacKinlay [1988] Andrew W Lo and A Craig MacKinlay. Stock market prices do not follow random walks: Evidence from a simple specification test. Review of financial studies, 1(1):41–66, 1988.

- Lo and MacKinlay [1990] Andrew W Lo and A Craig MacKinlay. An econometric analysis of nonsynchronous trading. Journal of Econometrics, 45(1):181–211, 1990.

- Mandelbrot [1997] Benoit B Mandelbrot. The variation of certain speculative prices. Springer, 1997.

- Mech [1993] Timothy S Mech. Portfolio return autocorrelation. Journal of Financial Economics, 34(3):307–344, 1993.

- Osborne [1959] MF Maury Osborne. Brownian motion in the stock market. Operations research, 7(2):145–173, 1959.

- Perry [1985] Philip R Perry. Portfolio serial correlation and nonsynchronous trading. Journal of Financial and Quantitative Analysis, 20(04):517–523, 1985.

- Richardson and Smith [1991] Matthew Richardson and Tom Smith. Tests of financial models in the presence of overlapping observations. Review of Financial Studies, 4(2):227–254, 1991.

- Robert [1967] Robert. Statistical versus clinical prediction of the stock market. Unpublished manuscript, 1967.

- Scholes and Williams [1977] Myron Scholes and Joseph Williams. Estimating betas from nonsynchronous data. Journal of financial economics, 5(3):309–327, 1977.

- Whang and Kim [2003] Yoon-Jae Whang and Jinho Kim. A multiple variance ratio test using subsampling. Economics Letters, 79(2):225–230, 2003.

- White [1980] Halbert White. A heteroskedasticity-consistent covariance matrix estimator and a direct test for heteroskedasticity. Econometrica: Journal of the Econometric Society, pages 817–838, 1980.

- White and Domowitz [1984] Halbert White and Ian Domowitz. Nonlinear regression with dependent observations. Econometrica: Journal of the Econometric Society, pages 143–161, 1984.

- Wright [2000] Jonathan H Wright. Alternative variance-ratio tests using ranks and signs. Journal of Business & Economic Statistics, 18(1):1–9, 2000.