On the Robustness of Regularized Pairwise Learning Methods Based on Kernels†00footnotetext: †Corresponding author: A. Christmann, Email: andreas.christmann@uni-bayreuth.de

The work by A. Christmann described in this paper is partially supported by a grant of the Deutsche

Forschungsgesellschaft [Project No. CH/291/2-1]. The work by D.-X. Zhou described in this paper is supported partially by a grant from the NSFC/RGC Joint Research Scheme [RGC

Project No. N_CityU120/14 and NSFC Project No. 11461161006].

Abstract

Regularized empirical risk minimization including support vector machines plays an important role in machine learning theory. In this paper regularized pairwise learning (RPL) methods based on kernels will be investigated. One example is regularized minimization of the error entropy loss which has recently attracted quite some interest from the viewpoint of consistency and learning rates. This paper shows that such RPL methods have additionally good statistical robustness properties, if the loss function and the kernel are chosen appropriately. We treat two cases of particular interest: (i) a bounded and non-convex loss function and (ii) an unbounded convex loss function satisfying a certain Lipschitz type condition.

Key words and phrases. Machine learning, pairwise loss function, regularized risk, robustness.

1 Introduction

Regularized empirical risk minimization based on kernels have attracted a lot of interest during the last decades in statistical machine learning. To fix ideas, let be a given data set, where the value denotes the input value and denotes the output value of the -the data point. Let be a loss function which is typically of the form , where denotes the predicted value for , when is observed, and the real-valued function is unknown. Many regularized learning methods are then defined as minimizers of the optimization problem

| (1.1) |

where the set consists of real-valued functions , is a regularization constant, and is some regularization term to ovoid overfitting for the case, that is rich. One example is that is a reproducing kernel Hilbert space and , see e.g. Vapnik (1995, 1998), Poggio and Girosi (1998), Wahba (1999), Schölkopf and Smola (2002), Cucker and Zhou (2007), Steinwart and Christmann (2008) and the references cited there.

In recent years there is quite some interest in related learning methods where a pairwise loss function is used, which yields optimization problems like

| (1.2) |

or asymptotically equivalent versions of it. In other words, the estimator for is defined as the minimizer of the sum of a -statistic of degree and the regularizing term , see e.g. Serfling (1980). An example of this class of learning methods occurs when one is interested in minimizing Renyi’s entropy of order 2, see e.g. Hu et al. (2013), Fan et al. (2014), and Ying and Zhou (2015) for consistency and fast learning rates. Another example arises from ranking algorithms, see e.g. Clemencon et al. (2008) and Agarwal and Niyogi (2009). Other examples include gradient learning, and metric and similarity learning, see e.g. Mukherjee and Zhou (2006), Xing et al. (2002), and Cao et al. (2015). However, much less theory is currently known for such regularized learning methods given by (1.2) based on pairwise loss functions than for the more classical problem (1.1) using standard loss functions. This is true in particular for statistical robustness aspects. Statistical robustness is one important facet of a statistical method, especially it the data quality is only moderate or unknown, which is often the case in the so-called big data situation.

The main goal of this paper is to show that such regularized learning methods given by (1.2) have nice statistical robustness properties if a combination of a bounded and continuous kernel used to define and a convex, smooth, and separately Lipschitz continuous (see Definition 2.5) pairwise loss function is used. We also establish a representer theorem for such regularized pairwise learning methods, because we need it for our proofs, but the representer theorem may also be helpful to further research.

The rest of the paper has the following structure. In Section 2, we define pairwise loss functions, their corresponding risks, derive some basic properties of pairwise loss functions and their risks, and give some examples. In Section 3 we define regularized pairwise learning (RPL) methods treated in this paper and derive results on existence and uniqueness. We will show that shifted loss functions (defined in (3.10)) are useful to define RPL methods on the set of all probability measures without making moment assumptions. This is of course desirable, because the probability measure chosen by nature to generate the data is completely unknown in machine learning theory. Section 4 contains a representer theorem for RPL methods, which is our first main result, see Theorem 4.3. This result is interesting in its own, but we will also use it as a tool to prove our statistical robustness results in Section 5. For the case of bounded and not necessarily convex pairwise loss functions we show that RPL methods have a bounded maxbias if a bounded kernel is used. For the case of a convex pairwise loss function which is separately Lipschitz continuous in the sense of Definition 2.5 and a bounded continuous kernel, we can formulate the two other main results of this paper: Theorem 5.3 shows that the RPL operator has a bounded Gâteaux derivative and hence a bounded influence function, see Corollary 5.4, and Theorem 5.5 shows that RPL methods and their empirical bootstrap approximations are qualitatively robust, if some non-stochastic conditions are satisfied. Hence these statistical robustness properties of RPL methods hold for all probability measures provided these conditions on the input and output space, on the kernel, and on the loss function are fulfilled, which can easily be checked by the user. All proofs are given in the Appendix.

2 Pairwise Loss Functions and Basic Properties

If not otherwise mentioned, we will assume the following setup.

Assumption 2.1.

Let be a complete separable metric space and be closed. Let and , , be independent and identically distributed pairs of random quantities with values in . We denote the joint distribution of by , where is the set of all Borel probability measures on the Borel -algebra .

As usual we will denote the realisations of by . For a given data set we denote the empirical distribution by . Furthermore, we write . Hence for the realisations , .

Leading examples on the spaces are of course given by and for binary classification and and for regression, where is some positive integer.

For , we denote the marginal distribution of by and the conditional probability of given by . The -fold product measure of is denoted by or simply by .

The classical definition of a loss function in the machine learning literature is a measurable function from to and one goal is to minimize the expected loss plus some regularization term over a hypothesis space, which is often a reproducing kernel Hilbert space (RKHS), say , defined implicitly by a kernel , see e.g. Vapnik (1995, 1998), Poggio and Girosi (1998), Wahba (1999), Schölkopf and Smola (2002), Cucker and Zhou (2007), Steinwart and Christmann (2008) and the references cited there.

Here we will consider the case that a regularized risk is to be minimized, where the loss function for pairwise learning has six instead of three arguments. I.e., we wish to find a function such that for some non-negative loss function the value is small, if the pair is a good prediction for the pair . The close connection to -statistics and -statistics (both of degree 2) is obvious, see e.g. Serfling (1980, p. 172-174) and Koroljuk and Borovskich (1994).

Definition 2.2.

Let be a measurable space and be closed. Then a function

| (2.1) |

is called a pairwise loss function, or simply a pairwise loss, if it is measurable. A pairwise loss is represented by , if is a measurable function and, for all , for all , and for all ,

| (2.2) |

In the following, we will interpret as the loss when we predict if is observed, but the true outcome is . The smaller the value is, the better predicts by means of . From this it becomes clear that constant loss functions, such as , are rather meaningless for our purposes, since they do not distinguish between good and bad predictions. Therefore, we will only consider non-constant pairwise loss functions.

Let us now recall from the introduction that our major goal is to have a small average loss for future unseen observations . This leads to the following definition.

Definition 2.3.

Let be a pairwise loss function and .

-

(i)

The -risk for a measurable function , i.e. , is defined by

(2.3) -

(ii)

The minimal -risk

(2.4) is called the Bayes risk with respect to and . In addition, a measurable function with is called a Bayes decision function.

Note that the function is measurable by our assumptions, and since it is also non-negative, the above integral always exists, although it is not necessarily finite.

If is a Polish space and is closed, then is a Polish space, too, such that we can split up into the regular conditional probability and the marginal distribution , cf. Dudley (2002, Section 10.2). If we combine this with the Tonelli-Fubini theorem, we can write as

| (2.5) |

For a given sequence , we denote by the empirical measure associated to the data set . The risk of a function with respect to is called the empirical -risk

| (2.6) |

Analogously to (2.6) one can also define modifications in which one only adds terms in (2.6) over all pairs with or over all pairs with . Here we will not investigate these modifications.

We will now introduce some useful properties of pairwise loss functions and their risks in much the same manner than these properties are defined for classical loss functions. The first step is of course measurability.

Lemma 2.4 (Measurability of risks).

Let be a pairwise loss and be a subset that is equipped with a complete and separable metric and its corresponding Borel -algebra. Assume that the metric dominates the pointwise convergence, i.e., implies for all and for all . Then the evaluation map defined by is measurable, and consequently the map defined on and the map defined on are also measurable. Finally, given , the risk functional is measurable.

Obviously, the metric defined by the supremum norm dominates the pointwise convergence for every . It is well-known that the metric of reproducing kernel Hilbert spaces (RKHSs) also dominates the pointwise convergence.

Definition 2.5.

A pairwise loss is called

-

(i)

(strictly) convex, continuous, or differentiable, if

is (strictly) convex, continuous, or (total) differentiable for all , respectively.

-

(ii)

locally separately Lipschitz continuous, if for all there exists a constant such that, for all , we have

(2.7) Moreover, for , the smallest such constant is denoted by . Furthermore, is called separately Lipschitz continuous111We mention that Rio (2013) used the related term “separately 1-Lipschitz” in a different context., if there exists a constant such that, for all , the inequality (2.7) is satisfied, if we replace by .

If is differentiable, we denote by the (total) derivative of at . If is differentiable with respect to the 5th or 6t argument, we denote the corresponding partial derivative by and , respectively.

Let us now consider a few examples of pairwise loss functions.

Example 2.6 (Minimum error entropy (MEE) loss).

Fix . Define the pairwise loss represented by , where , , see e.g. Hu et al. (2013), Fan et al. (2014), and Feng et al. (2015). Some easy calculations show that the first two derivatives and are continuous and bounded. However, is not convex and therefore the MEE loss is not convex in the sense of Definition 2.5.

Example 2.7 (Absolute value type loss).

Define the pairwise loss represented by , where , . Obviously, is Lipschitz continuous, but not differentiable at .

Example 2.8 (Logistic pairwise loss).

Fix some , e.g. or equals the rounding precision of the observations. Denote the cumulative distribution function of the logistic distribution by , . Define the pairwise logistic loss represented by , where

| (2.8) |

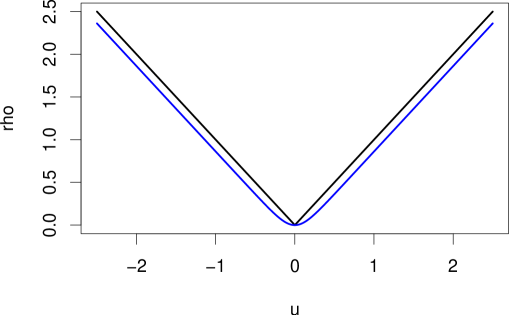

As Figure 1 shows, the pairwise logistic loss can be considered for some small tuning value as a smoothed version of the absolute value type loss. Some calculations show that is Lipschitz continuous with Lipschitz constant and and are continuous and bounded.

Example 2.9 (Squared loss).

Define the pairwise loss represented by , where , . Obviously, is only locally Lipschitz continuous and and are continuous. However, is unbounded.

Example 2.10 (Ranking loss).

Many ranking algorithms can be induced by a pairwise loss of the form with a bivariate function . See e.g. Agarwal and Niyogi (2009), the hinge ranking loss by

and the least squares ranking loss by

where

For further use we mention that the hinge ranking loss is not differentiable and the least squares ranking loss is not separately Lipschitz continuous in the sense of Definition 2.5. In contrast, the logistic ranking loss, which we define by

| (2.9) |

by using the function from (2.8) for some , is a separately Lipschitz continuous, differentiable pairwise loss function with bounded first and second order partial derivatives w.r.t. the last two arguments.

Example 2.11 (Similarity loss).

Some distance metric or similarity learning algorithms for and can be induced by a pairwise loss of the form

or

with a positive semidefinite symmetric matrix and , . See e.g. Cao et al. (2015), a hinge similarity loss by

where

In the same manner as the logistic pairwise loss function considered as a smooth alternative to the classical hinge loss function for binary classification problems, we can define a logistic similarity loss by

| (2.10) |

It will become clear in Theorem 5.3 and in Theorem 5.5, that separate Lipschitz continuity and bounded derivatives are key properties of pairwise loss functions to achieve a RPL method with good robustness properties.

In the following we will often need that the risk functional is convex to achieve uniqueness of the estimator. This can easily be achieved by the following result.

Lemma 2.12 (Convexity of risks).

Let be a (strictly) convex pairwise loss and . Then is (strictly) convex.

We also need some additional relationships between a pairwise loss function and its risk. Such relationships are of course well-known for standard loss functions, see e.g. Steinwart and Christmann (2008).

Lemma 2.13 (Lipschitz continuity of risks).

Let and be a locally separately Lipschitz continuous pairwise loss. Then for all and all with and , we have

Furthermore, the risk functional is well-defined and continuous.

In general, we can not expect that the risk of a differentiable loss function is differentiable. In this paper we are mainly interested in convex, separately Lipschitz continuous and differentiable pairwise loss functions, for which all partial derivatives (up to order one or two) are continuous and uniformly bounded. Such loss functions will yield several desirable statistical robustness properties of the learning methods, as we aim to show. However, we conjecture that similar results can be shown for certain integrable Nemitski losses, see e.g. Steinwart and Christmann (2008, Lem. 2.21) for a result for standard loss functions from .

Lemma 2.14 (Differentiability of risks).

Let and be a differentiable pairwise loss such that, for all and all , the partial derivatives , , are continuous and uniformly bounded by some constant . Then the risk functional is Fréchet differentiable and its derivative at is the bounded linear operator , where equals

Example 2.15 (Logistic pairwise loss; continuing Example 2.8).

For later use, we mention some properties of the pairwise loss , where . Some tedious but straightforward calculations show that is a convex, continuous, differentiable, and separately Lipschitz continuous pairwise loss with and

| (2.11) | |||||

| (2.12) |

where . We note that and , . Hence, all partial derivatives of of order up to two w.r.t. the last two arguments are continuous and bounded. Fix . For any fixed values of define . We have

Hence, if we consider as a function of the last two arguments, the Hessian matrix is given by which is obviously positive semi-definite. Hence, is a convex pairwise loss. Of course, is a continuous pairwise loss , too. Furthermore, using the above formulae of the partial derivatives of , we obtain that is a differentiable pairwise loss with continuous and bounded partial derivatives up to order two (w.r.t. the last two arguments of ). Therefore, Lemma 2.14 yields that the risk functional is Fréchet differentiable and its derivative at is the bounded linear operator , where is given by

where . Since for all , we immediately obtain

Furthermore, some calculations yield that is a separately Lipschitz continuous pairwise loss with for all .

Example 2.16 (-loss; continuing Example 2.9).

For later use, we mention that the pairwise loss is a convex, continuous, and differentiable pairwise loss. All partial derivatives of of order up to two w.r.t. the last two arguments are continuous. For any fixed values of define . We have

Hence, if we consider as a function of the last two arguments, the Hessian matrix is given by which is obviously positive semi-definite. Hence, is a convex pairwise loss . But of course,

| (2.13) |

if . This is in contrast to the separately Lipschitz continuous pairwise loss , as the previous example showed.

3 Regularized Pairwise Learning Methods

Definition 3.1.

Let be a pairwise loss, be the RKHS of a measurable kernel on , and . For , define the regularized risk by . A function which satisfies

| (3.1) |

is called a regularized pairwise learning (RLP) method.

If exists, we have

| (3.2) |

or in other words

| (3.3) |

Let us now investigate under which assumptions there exists an and when it is unique.

Assumption 3.2.

Let be a continuous and bounded kernel with reproducing kernel Hilbert space and define . Denote the canonical feature map by , .

It is well-known that if is a continuous kernel defined on a Polish space, then is continuous, too. This assumption on the kernel is fulfilled e.g., if and is a Gaussian RBF-kernel , an Abel RBF-kernel , where , or a compactly supported kernel, see e.g. Wu (1995) and Wendland (1995).

The following facts, which we will need later on, are well-known for any bounded kernel on with RKHS , all , and all :

| (3.4) | |||||

| (3.5) | |||||

| (3.6) | |||||

| (3.7) |

First, we will derive conditions for the existence of an RPL method.

Lemma 3.3.

Let . If and if the sequence , then there exists a subsequence and such that and

| (3.8) |

Theorem 3.4 (Existence).

If is a separately Lipschitz continuous pairwise loss function, , for some , and be an RKHS with bounded measurable kernel on . Then a minimizer exists for any .

We now address the question of uniqueness.

Lemma 3.5 (Uniqueness).

Let , be a convex pairwise loss with for some , and be the RKHS of a measurable kernel over . Then for all there exists at most one .

Theorem 3.6 (Existence).

Let , be a convex, locally separately Lipschitz continuous pairwise loss function with , and be the RKHS of a bounded measurable kernel over . Then, for all , there exists .

Corollary 3.7 (Existence and Uniqueness).

Let , be a convex, separately Lipschitz continuous pairwise loss function with , and be the RKHS of a bounded measurable kernel over . Then, for all , there exists a uniquely defined and

| (3.9) |

Obviously, we would like to get rid of the moment assumption , because otherwise we can not define on for arbitrary input and output spaces. The idea to shift the loss function by an appropriate function which is independent of the last two arguments of is useful in this respect, as was already used e.g. by Huber (1967) for M-estimators and by Christmann et al. (2009) for support vector machines based on a general loss function and on a general kernel.

Let be a pairwise loss and define the corresponding shifted pairwise loss function (or simply the shifted version of ) by

| (3.10) | |||

| (3.11) |

We adopt the definitions of continuity, (locally) separately Lipschitz continuity, and differentiability of from the same definitions for , i.e. these properties are meant to be valid for the last two arguments, when the first four arguments are arbitratily but held fixed. In the same manner we define the -risk, the regularized -risk, and the RPL method based on by

| (3.12) | |||||

| (3.13) | |||||

| (3.14) |

respectively. Of course, shifting the loss function to changes the objective function, but the minimizers of and coincide for those for which has a minimizer in . I.e., we have

| (3.15) |

Furthermore, (3.15) is valid for all empirical distributions based on a data set consisting of data points , , because exists and is unique since .

Let us now show that shifting a pairwise loss function indeed helps to get rid of the moment assumption which was essential for the Theorems 3.5 and 3.6. Assume that is a separately Lipschitz continuous pairwise loss. Then we obtain, for all ,

without making the moment condition . The assumption can easily be satisfied by choosing a bounded kernel , because then all are bounded due to , see (3.5). Therefore, taking (3.15) into account, the use of a shifted loss function just enlarges the set of probability measures where the minimizer of the regularized risk is well-defined. We will make this observation more precise in the remaining part of this section. The following result gives a relationship between and in terms of convexity and Lipschitz continuity.

Lemma 3.8.

Let be a pairwise loss. Then the following statements are valid.

-

(i)

If is (strictly) convex, then is (strictly) convex.

-

(ii)

If is separately Lipschitz continuous, then is separately Lipschitz continuous. Furthermore, both Lipschitz constants are equal, i.e., .

Lemma 3.9.

Let be a pairwise loss and its shifted version. Then the following assertions are valid.

-

(i)

.

-

(ii)

If is a separately Lipschitz continuous pairwise loss, then for all :

(3.17) (3.18) -

(iii)

and .

-

(iv)

Let be a separately Lipschitz continuous pairwise loss and assume that exists. Then we have

(3.19) If the kernel is additionally bounded, then

(3.20) (3.21) -

(v)

If the partial derivatives and of exist for all and all , then, for all ,

(3.22) (3.23)

The following proposition ensures that the optimization problem to determine is well-posed.

Lemma 3.10.

Let be a separately Lipschitz continuous pairwise loss function and . Then . Moreover, we have for all .

Lemma 3.11 (Convexity of -risks).

Let be a (strictly) convex loss. Then is (strictly) convex and is strictly convex.

Theorem 3.12 (Uniqueness of ).

Let be a convex pairwise loss, be the RKHS of a measurable kernel over , and . Assume that (i) for some and for all or (ii) is separately Lipschitz continuous and for all . Then for all there exists at most one decision function .

Theorem 3.13 (Existence and Uniqueness of ).

Let be a convex, separately Lipschitz continuous pairwise loss, be the RKHS of a bounded measurable kernel , and . Then for all there exists a unique decision function .

4 Representer Theorem for RPL Methods

In this section we establish a representer theorem for a general probability measure . This result is interesting in its own, but also useful to prove several statistical robustness properties of RPL methods. We will often make the following two assumptions to derive our representer theorem and robustness results.

Assumption 4.1.

Let be a separately Lipschitz-continuous, differentiable pairwise loss function for which all partial derivatives up to order 2 with respect to the last two arguments are continuous and uniformly bounded in the sense that there exist constants and with

| (4.1) | |||||

| (4.2) |

Additionally, assume that

| (4.3) |

Of course, does not satisfy the assumption (4.1), whereas e.g. fulfills all conditions in the Assumption 4.1. The assumption (4.3) is quite plausible and is satisfied for almost all loss functions of practical use, e.g. for . If a pairwise loss is represented by , then (4.3) is satisfied if . A ranking loss with also satisfies (4.3).

Assumption 4.2.

Let be a convex pairwise loss function.

We will reconsider these assumptions at the end of Section 5 and it will become clear that these assumptions on and are very plausible to guarantee the existence of a bounded Gâteaux derivative of the map .

As usual we will denote Bochner integrals of an -valued function with respect to some Borel measure by , we refer to Denkowski et al. (2003, p. 365ff). If is a probability measure, we denote the Bochner integral occasionally by .

5 Robustness of RPL Methods

In this section we will show that an RPL method has several desirable statistical robustness properties, if the pairwise loss function and the kernel fulfill weak qualitative assumptions. Because these assumptions are independent of , these assumptions can really be checked in advance. We will start with the case of bounded pairwise loss functions. The case of convex pairwise loss functions will be investigated in Section 5.2.

5.1 Case 1: Non-convex and Bounded Pairwise Loss

The minimizer typically exists, but it is unfortunately in general not uniquely defined for non-convex pairwise loss functions. However we will show in this subsection, that RPL-methods based on a non-convex and bounded pairwise loss function often yields a statistically robust approximations of the regularized risk. More precisely, we will show that the regularized risk functional has a small bias in neighborhoods defined by the norm of total variation, if is a bounded, but in general non-convex pairwise loss function. This is also valid, if we consider the classical contamination “neighborhoods”, see e.g. Huber (1981, p.11). This result will indicate that we can expect a bounded influence function for the regularized risk operator for non-convex pairwise loss functions under appropriate conditions, provided the influence function exists.

Our most important special case for this section is of course the minimum entropy loss , see Example 2.6.

In this section, let be a bounded pairwise loss function, i.e. we assume

for some constant . Hence the risk for all and there is no need to consider shifted loss functions.

The norm of total variation of two probability measures is defined by

where the supremum is with respect to all with . It is well-known that for all .

Define the function

| (5.1) | |||

Recall that the maximum bias of is defined by

| (5.2) |

where denotes an -neighborhood of , see Huber (1981, p.11, (4.5)). Common examples are the total variation neighborhood

and the so-called contamination “neighborhood”

From a robustness point of view, a statistical method with a bounded maximum bias for sufficiently large positive values of is considered to be robust. If two statistical methods have a bounded maximum bias, the one with the smaller maximum bias is considered to be more robust.

Theorem 5.1 (Bounds for the bias).

Let and . Let be a bounded pairwise loss function satisfying . Consider the regularised risk functional defined in (5.1)

-

(i)

Then

(5.3) and an upper bound for the maximum bias over total variation neighborhoods is given by

uniformly for all .

-

(ii)

If for some , then

(5.4) and the maximum bias over contamination “neighborhoods” satisfies

uniformly for all and .

An obvious consequence of the second part of Theorem 5.1 is, that the limit

| (5.5) |

is bounded by , provided the limit exists. If we specialize to for some , we obtain immediately from (5.5), that has a uniformly bounded influence function in sense of Hampel (1968, 1974), whenever the influence function exists.

Let us now consider an interesting special case of the previous theorem. Define the discrete probability measures and for given data sets with and data points , respectively, let be the Dirac measure for some point , and let . Then we obtain

The ratio is the so-called sensitivity curve at the point , see Tukey (1977) or Hampel et al. (1986, p. 93), and is usually denoted by

It measures the influence which an additional single data point has on the statistical method , if the original data set contains data points. The influence function can under appropriate assumptions be considered as a finite-sample version of the influence function, see Hampel et al. (1986, p. 94). A similar version of the sensitivity curve exists, if we replace one data point from an original data set with data points. An immediate consequence of part (ii) in Theorem 5.1 is, that the sensitivity curve is uniformly bounded by for all data sets and any additional data point , no matter where is located in . If we are interested in the slightly more general problem how to obtain an upper bound for the influence of additional data points, we just define , , and use again part (ii) in Theorem 5.1 to obtain a uniform upper bound.

Example 5.2.

Theorem 5.1 is applicable for the non-convex minimum entropy loss represented by , , where , see Example 2.6. A division by shows that the absolute value of these difference quotients are bounded by or , respectively, which is an immediate consequence of Theorem 5.1. If we additionally assume for the case of contamination “neighborhoods” in Theorem 5.1(ii), that the limit exists, where with being the Dirac measure in , then this limit equals the influence function of at and its absolute value is then bounded by . This is of course desirable from a robustness point of view.

Summarizing, we showed in this subsection that the regularized risk functional based on bounded pairwise loss functions has some desirable robustness properties even if is non-convex and bounded. An example is the minimum error entropy loss.

5.2 Case 2: Convex Pairwise Loss

An immediate consequence of the second part of our representer theorem, see (2), is the inequality

| (5.6) |

which is valid for all and all if the Assumptions 2.1, 3.2, 4.1, and 4.2 are valid.

The goal of this subsection however is to show that the RPL operator

| (5.7) |

has two additional desirable robustness properties, if weak conditions on , , , and are satisfied:

- (i)

-

(ii)

Theorem 5.5 will show that the sequence of RPL estimators are qualitatively robust, which is a kind of equicontinuity described later in more detail. If additionally is a compact metric space, then even the empirical bootstrap approximations are qualitatively robust.

Please note, that the following results of this subsection are all formulated for and not for , because the latter is in general not well-defined for all , as was explained in Section 3. Please recall the obvious equalities and for .

Theorem 5.3 (Bounded Gâteaux derivative).

Please note, that the operator and the first integral of only depend on . Only the second and the third integral in the formula of depend on and describe how the changes, if the probability measure equals the mixture instead of . Of course, we have .

The influence function is an important approach in robust statistics and was proposed by Hampel (1968, 1974); we refer also to the classical textbook by Hampel et al. (1986). The influence function is related to Gâteaux differentiation of the operator in direction of the Dirac measure , where , i.e.

The influence function has the interpretation that it measures the influence of an (infinitesimal) small amout of contamination of the original measure in the direction of a Dirac measure located in the point on the theoretical quantity of interest. Hence, it is desirable that a statistical method has a bounded influence function. If different methods have a bounded influence function, the one with the lower bound is considered to be more robust within this approach.

Corollary 5.4 (Bounded influence function).

We mention that the pairwise loss fulfills the Assumptions 4.1 and 4.2 with and for any , see (2.11) and (2.12). Hence, Theorem 5.3 and Corollary 5.4 are applicable for , if used in combination with a bounded and continuous kernel, e.g. a Gaussian RBF kernel.

Now let us reconsider the assumptions on and we made to establish Theorem 5.3. Due to and the specific form of and , we see that the boundedness of the Gâteaux derivative stems from the fact that is separately Lipschitz continuous and is bounded. One of these properties will in general not be enough to guarantee the boundedness of the Gâteaux derivative in unbounded spaces and . Let us give one simple example. If is unbounded, e.g. , we do not expect a bounded influence function for , if the squared loss is used, because the supremum of the absolute values of the partial derivatives are unbounded in this case, as follows from (2.13). Please note that this is no contraction to Theorem 5.3, because is clearly not separately Lipschitz continuous and is in general not even defined on the set of all Borel probability measures , if is unbounded.

In this sense, Theorem 5.3 and its corollary are in good agreement with results obtained by Christmann and Steinwart (2004, 2007) for the case of support vector machines based on a general loss function and on a general kernel.

Besides the maximum bias over neighbourhoods and a bounded influence function, qualitative robustness is another key notion in robust statistics. Qualitative robustness was proposed by Hampel (1968, 1971) and generalized to more abstract spaces by Cuevas (1988). Define

In this subsection we will show that the sequence of estimators

is qualitatively robust for all probability measures and any fixed regularization parameter . We will also give an analogous qualitative robustness result for the empirical bootstrap approximations.

According to Hampel (1968) and Cuevas (1988) a sequence of estimators is called qualitatively robust at a probability measure if and only if

| (5.10) |

Here and denote the image measures of and by , if all pairs are independent and identically distributed with or , respectively. Another common notation for is . Originally, Hampel (1971) used for the Prohorov metric , but one can also use the bounded Lipschitz metric defined by

in separable metric spaces, where and , see Dudley (2002, Chapter 11.2). The reason for this is that, for any separable metric space – and in our case is separable –, both and metrize the weak convergence for sequences of probability measures, i.e.

| (5.11) |

we refer to Dudley (2002, Thm. 11.3.3, p. 395) for details. Hence, qualitative robustness as defined in (5.10) is a kind of equicontinuity concerning the weak convergence of the image measures of with respect to .

The finite sample distribution of RPL estimators is in general unknown. One method to obtain approximations of this finite sample distribution is the empirical bootstrap proposed by Efron (1979, 1982). As the next theorem will also contain a qualitative robustness of empirical bootstrap approximations, we need some more notation. Recall that if all pairs are independent and identically distributed with (abbreviation: ). Furthermore, we denote the distribution of the -valued RPL estimator , by

| (5.12) |

where with . Because is unknown but fixed, this is an unknown, fixed probability measure of an -valued random function. In the same manner we denote the distribution of the -valued RPL estimator , when all pairs , where , by

| (5.13) |

We mention that denotes a distribution which can be considered itself as a random function in an abstract sense because it depends on .

We can now state our result on the qualitative robustness of regularized pairwise learning methods.

Theorem 5.5 (Qualitivative robustness).

Let the Assumptions 2.1, 3.2, 4.1, and 4.2 be valid. Then, for all , we have:

-

(i)

The sequence of RPL estimators , where , is qualitatively robust for all Borel probability measures .

-

(ii)

If the metric space is additionally compact, then the sequence , , of empirical bootstrap approximations of is qualitatively robust for all Borel probability measures .

The proof of Theorem 5.5 is based on the following two results which are interesting in their own.

Theorem 5.6 (Continuity of the operator).

Let the Assumptions 2.1, 3.2, 4.1, and 4.2 be valid. Then, for all Borel probability measures and for all , we have:

-

(i)

The operator , where , is continuous with respect to the weak topology on and the norm topology on .

-

(ii)

The operator , where , is continuous with respect to the weak topology on and the norm topology on .

Corollary 5.7 (Continuity of the estimator).

It is known that support vector machines (SVMs) are qualitatively robust for fixed values of but that they can not be qualitatively robust for the usual null-sequences needed to obtain universal consistency, because universal consistency and qualitatively robustness are under some mild conditions concurrent goals, see Hable and Christmann (2013) for a discussion. Is is known that SVMs can have a somewhat weaker property called finite-sample qualitivative robustness, see Hable and Christmann (2011). It is an open problem, whether a similar result is true for RPL methods, and we will not address this question here.

6 Discussion

In this paper we proved some desirable statistical robustness properties for a broad class of regularized pairwise learning methods based on kernels. Such kernel methods are used in the fields of information theoretic learning, ranking, gradient learning, and metric and similarity learning. In particular, our work complements to some respect earlier work on consistency and learning rates for minimum error entropy principles by Hu et al. (2013), Fan et al. (2014), Hu et al. (2015), for ranking algorithms by Agarwal and Niyogi (2009), for metric and similarity learning problems by Cao et al. (2015), and for gradient learning methods by Mukherjee and Zhou (2006).

The following aspects are beyond the scope of this paper and remain open for further work. (i) We did not address the question of an influence function of regularized pairwise learning methods, if a bounded but non-convex pairwise loss function is used. The main problem seems to be that in this case the function is in general not unique. (ii) We did not add numerical comparisons because it is known from Principe (2010) that for minimum error entropy principles such methods can be computed in an efficient gradient descent manner. (iii) It seems obvious that the results developed here for pairwise learning can in principle be established also to higher order, if one uses - or -statistics of degree . E.g., if , one can consider loss functions with instead of arguments which yields instead of (1.2) the optimization problem

| (6.1) |

We conjecture that the numerical effort to solve such problems will strongly increase with .

7 Appendix

7.1 Appendix A: Some Tools

To improve the readability of the paper, we list some known results which are used in our proofs given in this subsection. The following theorem provides a criterion for the existence of a global minimizer. Ekeland and Turnbull (1983, Prop. 6, p. 75) shows the existence, and the uniqueness is a consequence of the strict convexity.

Theorem 7.1 (Existence of minimizers).

Let be a reflexive Banach space and be a convex and lower semi-continuous map. If there exists an such that is non-empty and bounded, then has a global minimum, i.e., there exists an with for all . Moreover, if is strictly convex, then is the only element minimizing .

Definition 7.2 (Derivatives, see e.g. Denkowski et al. (2003, p. 518f)).

Let and be normed spaces, and be open sets, and be a map. We say that is Gâteaux differentiable at if there exists a bounded linear operator such that

In this case, is called the derivative of at , and since is uniquely determined, we write . Moreover, we say that Fréchet differentiable at if actually satisfies

Furthermore, we say that is (Gâteaux, Fréchet) differentiable if it is (Gâteaux, Fréchet) differentiable at every . Finally, is said to be continuously differentiable if it is Fréchet differentiable and the derivative is continuous.

Theorem 7.3 (Partial Fréchet differentiability, see e.g. Akerkar (1999, Theorem 2.6, p. 37)).

Let , , and be Banach spaces, and be open subsets, and be a continuous map. Then is continuously differentiable if and only if is partially Fréchet differentiable and the partial derivatives and are continuous. In this case, the derivative of at is given by

The proof of our Theorem 5.3 heavily relies on the implicit function theorem in Banach spaces. Recall the following simplified version of this theorem, see Akerkar (1999, Thm. 4.1, Cor. 4.2) Here and throughout this appendix denotes the open unit ball of a Banach space .

Theorem 7.4 (Implicit function theorem).

Let be Banach spaces and be a continuously differentiable map. Suppose that we have such that and is invertible. Then there exists a and a continuously differentiable map such that for all , we have: if and only if . Moreover, the derivative of is given by

| (7.1) |

Definition 7.5 (Bochner integral).

Let be a Banach space and be a -finite measure space. An -valued measurable function is called Bochner -integrable if there exists a sequence of -valued measurable step functions such that . In this case, the limit exists and is called the Bochner integral of . Finally, if is a probability measure, we sometimes write for this integral.

Theorem 7.6 (Dominated convergence theorem, see e.g. Denkowski et al. (2003, Thm. 3.10.12, p. 367)).

Let be a Banach space, be a finite measure space, and be a sequence of Bochner -integrable functions . If for every and if there exists a -integrable function with -almost everywhere for all , then is Bochner -integrable and .

7.2 Appendix B: Proofs

To shorten the notation, we occationally use the abbreviations , , , , , and , for etc.

The proofs for the results given in Section 2 and Section 3 are similar to corresponding results for “classical” loss functions of the form used by support vector machines and related kernel based methods, see e.g. Steinwart and Christmann (2008).

-

Proof of Lemma 2.4.

Since dominates the pointwise convergence, we see that, for fixed , the -valued map defined on is continuous with respect to . Furthermore, implies that, for fixed , the -valued map defined on is measurable. By a well-known result from Carathéodory, see e.g. Castaing and Valadier (1977, p. 70), we then obtain the first assertion. Since this implies that the maps and are measurable, we obtain the second assertion. The third assertion now follows from the measurability statement in Tonelli-Fubini’s theorem, see e.g. Dudley (2002, p. 137). ∎

-

Proof of Lemma 2.12.

Let , , and assume that is a convex pairwise loss. We immediately obtain, for all ,

The linearity of integrals yields the assertion . The case of strict convexity can be shown in an analogous manner. ∎

-

Proof of Lemma 2.13.

Because is a locally separately Lipschitz continuous pairwise loss, we have

which gives the assertion. ∎

-

Proof of Lemma 2.14.

Because we consider as a function of its last two arguments, while the first four arguments are held fixed, we define , where and . We first observe that all derivatives are measurable since we assumed continuous partial derivatives. Now let and be a sequence with , , and . Without loss of generality, we additionally assume for later use that for all . For and , we now define

if , and otherwise. We obtain

(7.3) for all , where the well-known relationship , where , was used in (Proof of Lemma 2.14. ). Furthermore, for , the definition of and the definition of the (total) derivative obviously yield

(7.4) Denote the gradient of by . For and with , the mean value theorem for functions from to shows that there exists some with

Because has by assumption uniformly bounded partial derivatives and , to be more precise, there exists a constant such that

If we combine this with the equality in (Proof of Lemma 2.14. ), we obtain

Combining (7.3), (Proof of Lemma 2.14. ), and (Proof of Lemma 2.14. ), we get . Hence, is a non-negative convergent dominating function and the assertion follows from Lebesgue’s theorem. ∎

-

Proof of Lemma 3.3.

Since the closed ball of the Hilbert space is weakly compact, there exists a subsequence weakly converging to some . That is,

(7.7)

-

Proof of Theorem 3.4.

For every , we take a function such that

(7.8) Taking , we find that

and

Now we apply Lemma 3.3. We know that there exists a subsequence and such that and (3.8) is valid.

Consider . By the Lipschitz continuity of , the integrated function is bounded by

The upper bound is integrable with respect to . Also, for any , by the continuity of and (3.8), we have

So by the Lebesgue Dominated Theorem, we have

Then we take on both sides of (7.8) and find from that

It means that is a minimizer . This proves our statement. ∎

-

Proof of Lemma 3.5.

Let us assume that the map has two minimizers with . Recall that the parallelogram law is valid for all points and in a Hilbert space, cf. Denkowski et al. (2003, Thm. 3.7.7, p. 310). Therefore, we have . As is a convex pairwise loss, the map is convex by Lemma 2.12. This together with then shows for that

i.e., is not a minimizer of . Consequently, the assumption that there are two minimizers is false. ∎

-

Proof of Theorem 3.6.

Since the kernel of is measurable, consists of measurable functions, see e.g. Steinwart and Christmann (2008, Lem. 4.24). Moreover, is bounded and thus is continuous, see e.g. Steinwart and Christmann (2008, Lem. 4.23). In addition, we have for all . Recall that every convex function , which is not identically equal to , is continuous on the interior of its effective domain , see e.g. Ekeland and Témam (1999, Cor. 2.3 on p. 12). Hence is a continuous pairwise loss by the convexity of . Therefore, Lemma 2.13 shows that is continuous, and hence is continuous. In addition, Lemma 2.12 provides the convexity of this map. Furthermore, is also convex and continuous, which yields the continuity and the convexity of the map . Now consider the set . We obviously have . In addition, implies , and hence , where denotes the closed unit ball of . Hence is a non-empty and bounded subset of and thus Theorem 7.1 gives the existence of a minimizer . ∎

- Proof of Corollary 3.7.

-

Proof of Lemma 3.8.

Follows immediately from the definition of . ∎

-

Proof of Lemma 3.9.

(i) Obviously, we have

(ii) We have for all that

which proves (3.17). Equation (3.18) follows from .

(iii) As , we obtain and the same reasoning holds for .

(iv) Due to (iii) we have . As we obtainUsing similar arguments as above, we obtain

Furthermore, we obtain

This yields (3.19). Using (3.5), (3.7), and (3.19), we obtain for that

Hence . The case is trivial.

(v) This follows immediately from the definition of , because we just subtract a term, which is constant w.r.t. the last two arguments of . ∎

- Proof of Theorem 3.12.

- Proof of Theorem 3.13.

Before we can prove Theorem 5.3, we need the following results.

Lemma 7.7.

-

Proof of Lemma 7.7.

Because and are fixed, we write to shorten the notation in the proof. Let . We define a continuous function

(7.9) Recall that the partial derivatives of and w.r.t. to the last two arguments are identical because and differ only by the term . Observe that for ,

By the separate Lipschitz continuity of , the absolute value of the above integrand is bounded by

Also, for any , we have

An application of Lebesgue’s dominated convergence theorem yields

Since for any by definition of , we know that the term on the right hand of the above equality is greater or equal to . This inequality is also true for the function . So the desired identity follows. ∎

Definition 7.8.

We define the local modulus of continuity for the second order derivatives of a pairwise loss function with respect to the last two variables as

| (7.10) |

where .

If the sets and are bounded, the continuity of the second order derivatives of implies that uniformly with respect to .

Let and . Define the signed measure . Note that is a probability distribution if .

The key property we need to prove Theorem 5.3 is formulated in the following result.

Theorem 7.9.

-

Proof of Theorem 7.9.

By Theorem 7.3, we only need to show that the partial derivatives and are continuous.

To shorten the notation in the proof, we denote the random functions by and by , respectively. Analogously we denote second order partial derivatives of by , where .

Note that for and ,

Then for and , we have

Here

Applying (3.6) and (4.2) yield

Moreover,

Hence by (4.1) we have

Thus

This proves the continuity of the partial derivative .

The other partial derivative can be expressed with and as

To prove its continuity, we consider first the following difference with

By the definition of the local modulus of continuity for the second order derivatives of , see Definition 7.8, and the bound , if , we obtain the bound

The second difference we need to consider is the following sum of four terms, where the integrands are the same but the factors and the probability measures differ:

Let . Then assumption (4.2) and the bound yield the following inequality for the norm of this difference:

Thus we have

Then the continuity of the partial derivative follows. This proves the continuous differentiability of .

Let . Consider the linear operator . It can be expressed as

It is important to note that by Assumption 4.1 is a twice continuously differentiable pairwise loss function which implies that

Hence for any , the following holds

So the linear operator is symmetric. Hence its spectrum lies in the closed interval where

Now, is a convex pairwise loss function due to Assumption 4.2. Therefore, we obtain, for any ,

Hence, . This shows that the operator is invertible. ∎

We are now ready for the

-

Proof of Theorem 4.3.

We will first prove part (i) using Lemma 7.7. Let . Fix some and define . By the reproducing property (3.4) of the kernel , we have

(7.13) Obviously, we also have and for all . Note that the partial derivatives of and of with respect of the last two arguments are identical, because and its shifted version differ only by the term which is independent of . Therefore, Lemma 7.7 yields for the function the equality

where we used in the last equality the definition of and from (4.5) and (4.6), respectively, and (7.13). From this we easily conclude that, for all ,

which gives the assertion of part (i).

Let us now prove part (ii). As and are fixed, we will use the abbreviations and in the proof. The inequality is trivial, if . Hence let us assume that . Recall the following well-known inequality from convex analysis. If is a convex and total differentiable function with continuous second partial derivatives, then

where is the gradient of at , see Rockafellar (1970, Thm. 25.1, p. 242) for a more general result using subgradients. To apply this result, we define, for any fixed , the function , where and . For any we thus obtain

If we specialize and , we obtain from (7.2) the inequality

where we used in the last step that and differ only a term which does not dependent on the last two arguments. By calculating the corresponding Bochner integral with respect to the product measure , it follows from the reproducing property (3.4) of that

| (7.16) |

where we used in the last step only the definition of and given in (4.5) and (4.6), respectively. Moreover, an easy calculation shows

| (7.17) |

We thus obtain

| (7.19) |

where the term on the left hand side of (7.19) is less than or equal to zero, because the regularized risk with respect to is minimized for . Recall that we have

| (7.20) |

due to (4.4) in the first part of the representer theorem. If we combine these two facts with the Cauchy-Schwarz inequality we obtain from (7.2) that

After multiplication with , which is allowed since , we immediately obtain the assertion. ∎

-

Proof of Theorem 5.1.

The proof only needs some elementary arguments. For brevity let us use the notation , , , , and , . Denote . Because and , we immediately obtain, for all ,

Hence, there is no need to consider shifted loss functions.

Let us start with part (i). Because and , we have and . Therefore,

where we used in the last inequality that

(7.21) see Hoeffding and Wolfowitz (1958, p.709, (4.4) and (4.5)). Analogously, from and , we conclude and , which yields

If we combine both inequalities, we obtain the assertion from part (i).

To part (ii). Because and , we have and . Therefore,

where we used in (*) that for all . Because and , we have and . Hence, we obtain with the same argumentation as given above that

The combination of both inequalities yields the assertion. ∎

-

Proof of Theorem 5.3.

The proof uses similar arguments than the proof of Theorem 15 in Christmann and Steinwart (2007).

Partial derivatives of with respect to the fifth or sixt argument are denoted by or , respectively. In the same manner we denote partial derivatives of of order two by , where . Recall that due to (3.22), and for .

Fix and . Define and denote the product measure by .

The function defined by

where and , plays a key role in the proof. Since is bounded by Assumption 3.2, we have for all , see (3.5). Additionally the partial derivatives and are continuous and uniformly bounded by Assumption 4.1. Hence we obtain by using and (3.7), that, for all and all ,

Therefore, the map is well-defined and bounded with respect to the -norm. Due to (3.5) we have

Note that for the -valued Bochner integral is with respect to a signed measure. Now for we obtain by using Lemma 2.14 that

(7.22) Since the map is strictly convex for all due to Lemma 2.12 and is continuous, equation (7.22) shows that we have if and only if for such . Our aim is to show the existence of a differentiable function defined on a small interval for some that satisfies for all . Once we have shown the existence of this function we immediately obtain

(7.23) For the existence of this map we have to check by the implicit function theorem (cf. Theorem 7.4) that is continuously differentiable and that is invertible. However, these properties of were shown in Theorem 7.9. Hence we can apply Theorem 7.4 on implicit functions to see that the map is differentiable on a small non-empty interval . Therefore, we obtain

which yields the assertion. ∎

-

Proof of Theorem 5.6.

We will first prove part (i). Let be fixed. Because and are fixed, we will use again the shorter notations

Let , , be a weakly convergence sequence with limit , i.e. . We know from (5.11) that is equivalent to , where denotes the bounded Lipschitz metric, because is separable by Assumption 2.1. Hence the metric space is separable, too. The separability guarantees that

(7.24) see Billingsley (1999, Thm. 2.8 (ii), p. 23). Note that guarantees by definition the convergence for all continuous and bounded real-valued functions . However, we will need a corresponding convergence result of Bochner integrals where the integrand is a special -valued function.

The second part of Theorem 4.3 (representer theorem) yields

(7.25) where and . Because is continuous and bounded by Assumption 3.2, the canonical feature map is continuous and bounded, too, see e.g. Steinwart and Christmann (2008, Lemma 4.23, Lemma 4.29). Furthermore, because the shifted loss function is by Assumption 4.1 twice continuously differentiable and the partial derivatives are uniformly bounded, it follows that, for every fixed and every fixed , the function

(7.27) is continuous and bounded, where . We mention that the -valued function does not depend on . Because is continuous and bounded, we obtain from Bourbaki (2004, p. III.40) the following convergence result for Bochner integrals:

(7.28) see also Hable and Christmann (2011, Thm. A.1, p. 1000). Combining (7.24)–(7.28), we obtain that , which is equivalent to by (5.11), implies , which is the assertion of part (i).

The proof of the second part follows immediately from part (i) and the fact that the inclusion is continuous and bounded, see e.g. Steinwart and Christmann (2008, Lemma 4.28). ∎

-

Proof of Theorem 5.5.

Fix . We will first prove part (i). For any denote its empirical measure by . According to Corollary 5.7, the functions

are continuous and therefore measurable with respect to the corresponding Borel--algebras for every . The mapping

(7.29) is a continuous operator due to Theorem 5.6. Furthermore,

Because is a separable metric space and the kernel is continuous, the RKHS of is separable, see e.g. Steinwart and Christmann (2008, Lemma 4.33, p. 130). Hence is a complete and separable metric space.

Therefore, the sequence of RPL estimators , where , is qualitatively robust for all Borel probability measures according to Cuevas (1988, Thm. 2), which states: If is any sequence of estimators which can be represented via a continuous operator , which maps each probability measure to a value in a complete and separable metric space and satisfies (in our notation) , is qualitatively robust for all . Hence the assertion of part (i) is shown.

Let us now prove part (ii). It follows from the first part of Theorem 5.6, that the operator defined in (7.29) is continuous for all . Hence all conditions of Assumption 16.3 in Christmann et al. (2013) are satisfied, because is a compact metric space by assumption of Theorem 5.5(ii) and is a complete and separable metric space due to the continuity of by Assumption 3.2, e.g. Steinwart and Christmann (2008, Lemma 4.33, p. 130). Hence, Corollary 16.1 by Christmann et al. (2013) is applicable and immediately yields the assertion. We like to note that the compactness of the metric space was used in the proof of the above mentioned Corollary 16.1 to show that the continuous operator is even uniformly continuous for all . ∎

References

- Agarwal and Niyogi (2009) Agarwal, S. and Niyogi, P. (2009). Generalization bounds for ranking algorithms via algorithmic stability. J. Mach. Learn. Res., 10, 441–474.

- Akerkar (1999) Akerkar, R. (1999). Nonlinear Functional Analysis. Narosa Publishing House, New Dehli.

- Billingsley (1999) Billingsley, P. (1999). Convergence of Probability Measures. John Wiley & Sons, New York, 2nd edition.

- Bourbaki (2004) Bourbaki, N. (2004). Integration I. (Translated from the 1959, 1965, and 1967 French originals by Sterling K. Berberian. Chapters 1–6). Springer, Berlin.

- Cao et al. (2015) Cao, Q., Guo, Z. C., and Ying, T. (2015). Generalization bounds for metric and similarity learning. to appear in: Machine Learning, Online First. DOI 10.1007/s10994-015-5499-7.

- Castaing and Valadier (1977) Castaing, C. and Valadier, M. (1977). Convex Analysis and Measurable Multifunctions. Springer, Berlin.

- Christmann and Steinwart (2004) Christmann, A. and Steinwart, I. (2004). On robust properties of convex risk minimization methods for pattern recognition. J. Mach. Learn. Res., 5, 1007–1034.

- Christmann and Steinwart (2007) Christmann, A. and Steinwart, I. (2007). Consistency and robustness of kernel based regression. Bernoulli, 13, 799–819.

- Christmann et al. (2009) Christmann, A., Van Messem, A., and Steinwart, I. (2009). On consistency and robustness properties of support vector machines for heavy-tailed distributions. Statistics and Its Interface, 2, 311–327.

- Christmann et al. (2013) Christmann, A., Salibían-Barrera, M., and Aelst, S. V. (2013). Qualitative robustness of bootstrap approximations for kernel based methods. In C. Becker, R. Fried, and S. Kuhnt, editors, Robustness and Complex Data Structures, pages 277–293. Springer, Heidelberg.

- Clemencon et al. (2008) Clemencon, S., Lugosi, G., and Vayatis, N. (2008). Ranking and empirical minimization of U-statistics. Ann. Statist., 36, 844–874.

- Cucker and Zhou (2007) Cucker, F. and Zhou, D. X. (2007). Learning Theory: An Approximation Theory Viewpoint. Cambridge University Press, Cambridge.

- Cuevas (1988) Cuevas, A. (1988). Qualitative robustness in abstract inference. J. Statist. Plann. Inference, 18, 277–289.

- Denkowski et al. (2003) Denkowski, Z., Migórski, S., and Papageorgiou, N. (2003). An Introduction to Nonlinear Analysis: Theory. Kluwer Academic Publishers, Boston.

- Dudley (2002) Dudley, R. M. (2002). Real Analysis and Probability. Cambridge University Press, Cambridge.

- Efron (1979) Efron, B. (1979). Bootstrap methods: Another look at the jackknife. Ann. Statist., 7, 1–26.

- Efron (1982) Efron, B. (1982). The Jackknife, the Bootstrap, and Other Resampling Plans, volume 38. CBMS Monograph, Society for Industrial and Applied Mathematics, Philadelphia.

- Ekeland and Témam (1999) Ekeland, I. and Témam, R. (1999). Convex Analysis and Variational Problems. SIAM, Philadelphia.

- Ekeland and Turnbull (1983) Ekeland, I. and Turnbull, T. (1983). Infinite-Dimensional Optimization and Convexity. University of Chicago Press, Chicago.

- Fan et al. (2014) Fan, J., Hu, T., Wu, Q., and Zhou, D. X. (2014). Consistency analysis of an empirical minimum error entropy algorithm. to appear in: Appl. Comput. Harmonic Anal., Online first: doi:10.1016/j.acha.2014.12.005.

- Feng et al. (2015) Feng, Y., Huang, X., Shi, L., Yang, Y., and Suykens, J. (2015). Learning with the maximum correntropy criterion induced losses for regression. J. Mach. Learn. Res., 16, 993–1034.

- Hable and Christmann (2011) Hable, R. and Christmann, A. (2011). Qualitative robustness of support vector machines. Journal of Multivariate Analysis, 102, 993–1007.

- Hable and Christmann (2013) Hable, R. and Christmann, A. (2013). Robustness versus consistency in ill-posed classification and regression problems. In A. Giusti, G. Ritter, and M. Vichi, editors, Classification and Data Mining, pages 27–35. Springer, Berlin.

- Hampel (1968) Hampel, F. R. (1968). Contributions to the theory of robust estimation. Unpublished Ph.D. thesis, Department of Statistics, University of California, Berkeley.

- Hampel (1971) Hampel, F. R. (1971). A general qualitative definition of robustness. Ann. Math. Statist., 42, 1887–1896.

- Hampel (1974) Hampel, F. R. (1974). The influence curve and its role in robust estimation. J. Amer. Statist. Assoc., 69, 383–393.

- Hampel et al. (1986) Hampel, F. R., Ronchetti, E. M., Rousseeuw, P. J., and Stahel, W. A. (1986). Robust statistics: The Approach Based on Influence Functions. John Wiley & Sons, New York.

- Hoeffding and Wolfowitz (1958) Hoeffding, W. and Wolfowitz, J. (1958). Distinguishability of sets of distributions. the case of independent and identically distributed chance variables. Ann. Math. Statist., 29, 700–718.

- Hu et al. (2013) Hu, T., Fan, J., Wu, Q., and Zhou, D. X. (2013). Learning theory approach to minimum error entropy criterion. J. Mach. Learn. Res., 14, 377–397.

- Hu et al. (2015) Hu, T., Fan, J., Wu, Q., and Zhou, D. X. (2015). Regularization schemes for minimum error entropy principle. Anal. Appl., 13, 437–455.

- Huber (1967) Huber, P. J. (1967). The behavior of maximum likelihood estimates under nonstandard conditions. Proc. 5th Berkeley Symp., 1, 221–233.

- Huber (1981) Huber, P. J. (1981). Robust Statistics. John Wiley & Sons, New York.

- Koroljuk and Borovskich (1994) Koroljuk, V. and Borovskich, Y. (1994). Theory of -Statistics. Springer, Dordrecht.

- Mukherjee and Zhou (2006) Mukherjee, S. and Zhou, D. X. (2006). Learning coordinate covariances via gradients. J. Mach. Learn. Res., 7, 519–549.

- Poggio and Girosi (1998) Poggio, T. and Girosi, F. (1998). A sparse representation for function approximation. Neural Comput., 10, 1445–1454.

- Principe (2010) Principe, J. (2010). Information Theoretic Learning: Renyi’s Entropy and Kernel Perspectives. Springer, New York.

- Rio (2013) Rio, E. (2013). On McDiarmid’s concentration inequality. Electron. Commun. Probab., 44, 1–011.

- Rockafellar (1970) Rockafellar, R. T. (1970). Convex Analysis. Princeton University Press, Princeton, NJ.

- Schölkopf and Smola (2002) Schölkopf, B. and Smola, A. J. (2002). Learning with Kernels. Support Vector Machines, Regularization, Optimization, and Beyond. MIT Press, Cambridge, MA.

- Serfling (1980) Serfling, R. J. (1980). Approximation Theorems of Mathematical Statistics. John Wiley & Sons, New York.

- Steinwart and Christmann (2008) Steinwart, I. and Christmann, A. (2008). Support Vector Machines. Springer, New York.

- Tukey (1977) Tukey, J. W. (1977). Exploratory Data Analysis. [preliminary edition 1970-1971]. Addison-Wesley, Reading, MA.

- Vapnik (1995) Vapnik, V. N. (1995). The Nature of Statistical Learning Theory. Springer, New York.

- Vapnik (1998) Vapnik, V. N. (1998). Statistical Learning Theory. John Wiley & Sons, New York.

- Wahba (1999) Wahba, G. (1999). Support vector machines, reproducing kernel Hilbert spaces and the randomized GACV. In B. Schölkopf, C. J. C. Burges, and A. Smola, editors, Advances in Kernel Methods–Support Vector Learning, pages 69–88. MIT Press, Cambridge, MA.

- Wendland (1995) Wendland, H. (1995). Piecewise polynomial, positive definite and compactly supported radial basis functions of minimal degree. Adv. Comput. Math., 4, 389–396.

- Wu (1995) Wu, Z. (1995). Compactly supported positive definite radial functions. Adv. Comput. Math., 4, 283–292.

- Xing et al. (2002) Xing, E., Ng, A., Jordan, M., and Russell, S. (2002). Distance metric learning, with application to clustering with side-information. Advances in Neural Information Processing Systems, 15, 505–512.

- Ying and Zhou (2015) Ying, Y. and Zhou, D. X. (2015). Unregularized online learning algorithms with general loss functions. To appear in: Appl. Comput. Harmonic Anal., Online first: doi:10.1016/j.acha.2015.08.007.