Improved error bounds for quantization based numerical schemes for BSDE and nonlinear filtering

Abstract

We take advantage of recent (see [42, 61]) and new results on optimal quantization theory to improve the quadratic optimal quantization error bounds for backward stochastic differential equations (BSDE) and nonlinear filtering problems. For both problems, a first improvement relies on a Pythagoras like Theorem for quantized conditional expectation. While allowing for some locally Lipschitz continuous conditional densities in nonlinear filtering, the analysis of the error brings into play a new robustness result about optimal quantizers, the so-called distortion mismatch property: the -mean quantization error induced by -optimal quantizers of size converges at the same rate for every .

1 Introduction

In this work we propose improved error bounds for quantization based numerical schemes introduced in [4] and [59] to solve BSDEs and nonlinear filtering problems. For BSDE, we consider equations where the driver depends on the “” term (see Equation (1) below) and for nonlinear filtering, we extend existing results to locally Lipschitz continuous densities (see Section 6). For both problems, we also improve the error bounds themselves by using a Pythagoras like theorem for the approximation of conditional expectations introduced in [61] (see also [58]). These problems have a wide range of applications, in particular in Financial Mathematics, when modeling the price of financial derivatives or in stochastic control, in credit risk modeling, etc.

BSDEs were first introduced in [12] but raised a wide interest mostly after their extension in [64]. In this latter paper, the existence and the uniqueness of a solution have been established for the following backward stochastic differential equation with Lipschitz continuous driver (valued in ) and terminal condition :

| (1) |

where is a -dimensional brownian motion. We mean by a solution a pair (valued in ) of square integrable progressively measurable (with respect to the augmented Brownian filtration ) and satisfying Equation (1). Extensions of these existence and uniqueness results have been investigated in more general situations such as: less regular drivers (locally Lipschitz driver, see [1, 43]; quadratic BSDEs, see [50]; rough integrals instead of Lebesgue integrals, see [27]; super-linear quadratic BSDEs, see [51]); randomized horizon, see [63]; introduction of Poisson random measure component subject to constraints on the jump component, see [49, 48]; extension to second order BSDEs, see [56]); non-smooth terminal conditions, see [31, 30, 37].

Since the pioneering work [29] in which the link between BSDE and hedging portfolio of European (and American) derivatives has been first established, various other applications have been developed, as risk-sensitive control problems, risk measure theory, etc.

However, even if it can be established in many cases that a BSDE has a unique solution, this solution admits no closed form in general. This led to devise tractable approximation schemes of the solution. In the Markovian case (see (2) below) for example, where the terminal condition is of the form for some forward diffusion , a first numerical method has been proposed in [28] for a class of forward-backward stochastic differential equations, based on a four step scheme developed later on in [54].

Many other approximation methods of the solutions of some classes of BSDEs have been proposed such as BSDEs with possible path-dependent terminal condition, see [70] and [16], coupled BSDE, see [71], Reflected BSDE, see [46], BSDE for quasilinear PDEs, see [26], BSDE applied to control problems or nonlinear PDEs, see [2]. Higher order schemes have also been considered, see [20] or [6]. As for quadratic BSDE – when the generator has a quadratic growth with respect to – we refer to [21] where the authors consider a slightly modified dynamical programming equation to propose a numerical scheme. They investigate the time discretization error and use optimal quantization to implement their algorithm. However, they do not study the induced quantization error.

In the present work, we consider the following decoupled FBSDE (Forward-Backward SDE),

| (2) |

where is a -dimensional Brownian motion, is a square integrable progressively measurable process taking values in and is a Borel function. We suppose a terminal condition of the form , for a given Borel function , where is the value at time of a Brownian diffusion process , strong solution to the SDE:

| (3) |

In this case, the solution of the BSDE is usually approximated at the points of a time grid and involve in particular the approximation of conditional expectations , where the functions are determined in the recursion. The sequence is either a “sampling" of the diffusion at times or, most often, a discretization scheme of , typically the discrete time Euler scheme, when the solution of (3) is not explicit enough to be simulated in an exact way.

In this paper, we consider an explicit time discretization scheme where the conditioning is performed inside the driver (see also [47]). It is recursively defined in a backward way as:

| (4) | |||||

| (5) | |||||

| (6) |

The process is the discrete time Euler scheme of the diffusion process with step , recursively defined by

Under some smooth assumptions on the coefficients of the diffusions, there exists (see Theorem 3.1 further on for a precise statement, see also [70, 13]) that there is a real constant such that, for every ,

where comes from the martingale representation of

At this stage, since the scheme (4)-(5) involves the computation of conditional expectations for which no analytical expression is available, its solution has in turn to be approximated. A possible approach is to rely on regression methods involving the Monte Carlo simulations, see [13, 34, 36, 35]. Other methods using on line Monte Carlo simulations have been developed in a Malliavin calculus framework (conditional expectations are “regularized” by integration by parts from which “Malliavin” weights come out, see [13, 23, 39, 45, 69]). Among alternative approaches let us cite the least-squares regression methods, the multistep schemes methods (see [8, 40]), the primal-dual approach (see [9]). New approaches have been proposed recently: a combination of Picard iterates and a decomposition in Wiener chaos (see [15]), a “forward" approach in connection with the semi-linear PDE associated to the BSDE (see [44]), an analytic approach in [38].

In this paper, we go back to the optimal quantization tree approach originally introduced in [5] (in fact for Reflected BSDEs) and developed in [4, 3, 7]. This approach is based on an optimally fitting approximation of the Markovian dynamics of the discrete time Markov chain (or a sampling of at discrete times ) with random variables having a finite support. However, we consider a different quantization tree (or quantized scheme) defined recursively by mimicking (4)-(5) as follows:

| (7) | |||||

| (8) | |||||

| (9) |

where , , and is a quantization of on a finite grid , , , where is a Borel “projection" on , . At this stage the function might be any -valued Borel functions. In order to derive better theoretical rates as well as for practical implementation, we will first consider Borel nearest neighbor projections at every time step and then search for grids optimally “fitting” the distribution of minimizing the resulting error among all grids of a prescribed size , see Section 4 for details. This is an explicit inner scheme in the sense that the conditioning is performed inside the driver in contrast with what is usually done in the literature (where implicit or outer explicit schemes are in force). This scheme, though quite natural, seems not to have been extensively analyzed (see however [47] where a first analysis is carried out in the spirit of [4, 3]). It turns out to be well designed to establish our improved rates and shows quite satisfactory numerical performances. Our objective here is two-fold: first include the term in the driver and to dramatically improve the error bounds in [3, 7], especially its dependence in the size of the time discretization mesh.

So, the question of interest will be to estimate the quadratic quantization error induced by the approximation of by , for every , where is the quantized version of given by (7)-(8). Under more general assumptions than [4, 5], we show in Theorem 3.2 that, at every step of the procedure,

| (10) |

for positive real constants depending on and and on the regularity of the coefficients of and the driver which remain bonded as . The presence of the squared quadratic norms on both sides of (10) improves the control of the time discretization effect, compared with [4, 5] in which error bounds of the form are established for . In fact, we switch from a global error (at ) of order to . This theoretical improvement confirms the results of numerical experiments first carried out in [7] though it was in a less favorable framework (with reflection) or in [18, 17] for American options.

For the part which is approximated first by in (6) and whose quantization version is given by (9), we get the following approximation error (see Theorem 3.2)

where are positive constants depending on and and on the regularity of the coefficients of and the driver . So, we switch from to .

We notice here that other quantization based discretization schemes have been devised, especially for Forward-Backward SDEs (see [25]) where the diffusion and the BSDE are fully coupled (including the in the driver) where the grids are the trace of () on an expanding compact as grows. In contrast the Brownian increments are replaced by optimal quantization of the -distribution. But the obtained resulting error bound for the scheme are not of the improved from (10). A multistep approach based on two reference ODEs from the computation of conditional expectation has been developed in a similar framework (coupled and uncoupled) in [71].

In the second part of the paper, we first propose (Section 4) a short background on optimal vector quantization, enriched by a new result, namely Theorem 4.3, which essentially solves the-called distortion mismatch problem. By distortion mismatch we mean the robustness of optimal quantization grids. An optimal (quadratic) quantization grid at level for the distribution of a random vector is such that where denotes a (Borel) nearest neighbor projection on . It exists for every size (or level) as soon as and it follows from Zador’s Theorem that as (see Section 4 for details). The distortion mismatch property established in Theorem 4.3 states that, for every , . This result holds whenever with a distribution satisfying mild additional property. This theorem extends first results established in [42] for various classes of absolutely continuous distributions. Note that all the above properties depend on the distribution of rather than on the random vector itself. This robustness property is the key of the second kind of improvement proposed in this paper, this time for quantization based schemes for non-linear filtering investigated in the third part. In Section 5 we propose numerical illustrations using optimal quantization based schemes for various types of BSDEs which confirm that the improved rates established in the first part are the true ones.

In this third part of the paper (Section 6), we consider a (discrete time) nonlinear filtering problem and improve (in the quadratic setting) the results obtained in [59]. Firstly, we relax the Lipschitz assumption made on the conditional densities then we provide new improved error bounds for the quantization based scheme introduced in [59] to numerically solve a discrete filter by optimal quantization.

In fact, we consider a discrete time nonlinear filtering problem where the signal process is an -valued discrete time Markov process and the observation process is an -valued random vector, both defined on a probability space . The distribution of is given, as well as the transition probabilities of the process . We also suppose that the process is a Markov chain and that for every , the conditional distribution of given has a density . Having a fixed observation , for , we aim at computing the conditional distribution of given . It is well-known that for any bounded and measurable function , is given by the celebrated Kallianpur-Striebel formula (see [59])

| (11) |

where the so-called un-normalized filter is defined for every bounded or non-negative Borel function by

with

Defining the family of transition kernels , , by

| (12) |

for every bounded or non-negative Borel function and setting

one shows that the un-normalized filter may be computed by the following forward induction formula:

| (13) |

with . A useful formulation, especially to establish error bound for the quantization based approximate filter is its backward counterpart defined by setting

where is the final value of the backward recursion:

| (14) |

In order to compute the normalized filter , we just have to compute the transition kernels and to use the recursive formulas (13) or (14). However these kernels have no closed formula in general so that we have to approximate them. Optimal quantization based algorithms for non linear filtering has been introduced in [59] (see also [66, 19, 59, 68] for further developments and contributions). It turned out to be an efficient alternative approach to particle methods (we refer to [24] and the references therein which rely on Monte Carlo simulation of interacting particles) owing to its tractability. For a survey and comparisons between optimal quantization and particle methods, we refer to [68]).

The quantization based approximate filter is designed as follows: denoting for every by a quantization of at level by the grid , we will formally replace in (13) or (14) by . As a consequence the (optimally) quantized approximation of is defined simply by the quantized counterpart of the Kallianpur-Striebel formula: we introduce for every bounded or non-negative Borel function the family of quantized transition kernels , , by and

| (15) | |||||

| (16) | |||||

| (17) | |||||

| (18) |

Then set

| (19) |

or, equivalently,

and with , . As a final step, we approximate the normalized filter by given by

One shows (see [59]) that the un-normalized quantized filter may also be computed by the following backward induction formula, defined by

where is the final value of the backward recursion:

| (20) |

Our aim is then to estimate the quantization error induced by the approximation of by . Note that this problem has been considered in [59] where it has been shown that, for every bounded Borel function , the absolute error is bounded (up to a constant depending in particular on ) by the cumulated sum of the -quantization errors , . In this work, we improve this result in the particular case of the quadratic quantization framework ( ) in two directions. In fact, we first show that, for every bounded Borel function , the squared-absolute error is bounded by the cumulated square-quadratic quantization errors from to , similarly to what we did for BSDEs inducing a similar improvement for dependence in of the error bounds ( the time discretization step if is a discretization step of a diffusion). Once again, this confirms numerical evidences observed in [59, 7]. Secondly, we show that these improved error bounds hold under local Lipschitz continuity assumptions on the conditional density functions (instead of Lipschitz conditions in [59]). The distortion mismatch property established in Theorem 4.3 is the key of this extension.

The paper is divided into three parts. The first part is devoted to the analysis of the optimal quantization error associated to the BSDE algorithm under consideration. We recall first, in Section 2, the discretization scheme we consider for the BSDE. Then, in Section 3, we investigate the error analysis for the time discretization and the quantization scheme. In the second part, some results about optimal quantization are recalled in Section 4 and a new distortion mismatch theorem is established about the robustness of -optimal quantization in for . Some numerical tests confirm and illustrate these improved error bonds in Section 5. The final part, Section 6, is devoted to the nonlinear filtering problem analysis when estimating the nonlinear filter by optimal quantization with new improved error bounds obtained under less than stringent – local – Lipschitz assumptions than in the existing literature.

Notations: denotes the canonical Euclidean norm on .

For every , set and .

If we define the Fröbenius norm of by .

2 Discretization of the BSDE

Let be a -dimensional Brownian motion defined on a probability space and let be its augmented natural filtration. We consider the following stochastic differential equation:

| (21) |

where the drift coefficient and the matrix diffusion coefficient are Lipschitz continuous in . For a fixed horizon (the maturity) , we consider the following Markovian Backward Stochastic Differential Equation (BSDE):

| (22) |

where the function is -Lipschitz continuous, the driver is Lipschitz continuous with respect to , uniformly in , satisfies

| (23) |

Under the previous assumptions on , the BSDE (22) has a unique -valued, -adapted solution satisfying (see [64], see also [55])

Let us consider now , the discrete time Euler scheme with step of the diffusion process :

where , and its continuous time counterpart, sometimes called genuine Euler scheme (we drop the dependence in when no ambiguity) defined as an Itô process by

| (24) |

where when . In particular is an -adapted Itô process satisfying under the above assumptions made on and (see [14]) :

and

for a positive constant .

As a consequence, general existence-uniqueness results for BSDEs entail (see [65]) the existence of a unique solution to the Markovian BSDE having the genuine Euler scheme instead of as a forward process. Then, we can apply the classical comparison result (Proposition 2.1 from [29]) with and which immediately yields the existence of real constants , , such that

Unfortunately, at this stage, the couple is still “intractable" for numerical purposes (it satisfies no Dynamic Programming Principle due to its continuous time nature and there is no possible exact simulation, etc). This is mainly due to about which little is known. By contrast with which is closely connected to a PDE. So we will need to go deeper in the time discretization, by discretizing the term itself. Consequently, we need to perform a second time discretization on the Euler scheme based BSDE, only involving discrete instants , .

We consider an explicit inner scheme recursively defined in a backward way as follows:

| (25) | |||||

| (26) | |||||

| (27) |

It slightly differs from the other explicit schemes analyzed in the literature to our knowledge, since the conditioning is applied directly to inside the driver function rather than outside. Note that in many situations, one uses the following more symmetric alternative formula

which is clearly quite natural when thinking of a hedging term as a derivative ( computed in a binomial tree). It also has virtues in terms of variance reduction (see [7]). One easily shows by a backward induction that, for every , since .

Our first aim is to adapt standard comparison theorems to compare the above purely discrete scheme with the original BSDE to derive error bounds similar to those recalled above between and . To this end, like for the Euler scheme, we need to extend into a continuous time process by an appropriate interpolation. We proceed as follows: let

This random variable is in . Hence, by the martingale representation theorem, there exists an -progressively measurable such that

Then . In particular

so that we may define a continuous extension of as follows:

| (28) |

3 Error analysis

3.1 The time discretization error

We provide in the theorem below the quadratic error bound for the inside explicit time discretization scheme defined by (25)-(43) and (28). Claim comes from [70]. The detailed proof of Claim is given in the appendix. Like for most results of this type, the proof of follows the lines of that devised for comparison theorems in [29]. In particular, though slightly more technical at some places, it is close to its counterpart for the standard outer explicit scheme originally established in [3] (in for reflected BSDEs, but without on the driver) or in [70] (in the quadratic case, see also [33] for an extension error bounds in or [13] for implicit scheme).

Theorem 3.1.

Assume the functions is Lipschitz continuous in and that is Lipschitz continuous. Then, there exists a real constant such that, for every ,

where if .

Assume that the functions are continuously differentiable in their spatial variables ( and respectively) with bounded partial derivatives and -Hölder continuous with respect to , that and is uniformly elliptic. Assume is Lipschitz continuous. Then, the process admits a càdlàg modification and

| (29) |

so that there exists a real constant such that, for every ,

| (30) |

Claim as stated comes from [70] (Theorem 3.1 and Lemma 2.5). It admits several variants (see [13]) or improvements in the literature. Thus, in [37] (Theorem 20) it is obtained under a still lighter assumption on the terminal value of fractional type, provided this time and are bounded, , , in space, uniformly -Hölder in time (and uniformly elliptic) and the driver is in in its spatial variable with bounded partial derivatives and . Then, the resulting bound is for a uniform mesh (but can attain for a tailored mesh). See also [26] for a PDE based extension to general forward-backward system when the both forward and backward equations are coupled.

Notations (change of). The previous schemes (25)-(26) involve some quantities and operators which will be the core of what follows and are of discrete time nature. So, in order to simplify the proofs and alleviate the notations, we will identify every time step by and we will denote . Thus, we will switch to

3.2 Error bound for the quantization scheme

In this section, we consider the quantization scheme (7)-(8) and compute the quadratic quantization error induced by the approximation of by , for every . This leads to the following theorem which is the first main result of this paper.

Theorem 3.2.

Assume that the drift and the diffusion coefficient of the diffusion defined by (21) are Lipschitz continuous, that the driver function satisfies (Assumption(23)) and that the function is -Lipschitz continuous. Assume that (in order to provide sharper constants depending on ).

For every ,

| (31) |

where and, for every ,

with

, ,

and

and

| (32) |

For every ,

The proof is divided in two main steps: in the first one we establish the propagation of the Lipschitz property through the functions and involved in the Markov representation (25)-(26) of and , namely and , and to control precisely the propagation of their Lipschitz coefficients (an alternative to this phase can be to consider the Lipschitz properties of the flow of the SDE like in [47]). As a second step, we introduce the quantization based scheme which is the counterpart of (25) and (26) for which we establish a backward recursive inequality satisfied by .

Remark 3.1.

(About the relationship between the temporal and the spatial partitions) Owing to the non-asymptotic bound for the quantization (see Theorem 4.1 further), we deduce from the upper bound of Equation (31) that there exists some constants , (only depending on the coefficients and of the diffusion ) such that for every ,

| (33) |

So, a natural question is to determine how to dispatch optimally the sizes (for a fixed mesh of length , given that is deterministic and, as such, perfectly quantized with ) of the quantization grids under the total “budget” constraint of elementary quantizers (with and , for every ). This amounts (at least at time ) to solving the constrained minimization problem

whose solution reads , . Coming back to (33), and using the Hölder inequality (to get the second inequality below) yields

| (34) |

Notice that for the standard (“non-improved”) error bounds (see the introduction), the same optimal allocation procedure would yield (starting from ),

which emphasizes the improvement of the error bound as concerns the dependence in the time mesh size .

3.2.1 First step toward the proof of Theorem 3.2: Lipschitz operators

As a first step we introduce several operators which appear naturally when representing . We will show that these operators propagate Lipschitz continuity. It is a classical step when establishing a priori error bounds going back to [4, 3], see also more recently [34] (Proposition 3.4). However we do not skip it since it emphasizes the technical specificities induced by our choice of an inner explicit scheme.

To be more precise, we set for every and every Borel function with polynomial growth

| (35) | |||||

| (36) | |||||

| (37) |

One immediately checks that for every ,

Note that the process is an -Markov chain with transitions , . Moreover, it shares the property to propagate the Lipschitz property as established in the Lemma below.

Lemma 3.3.

For every , the transition operator is Lipschitz in the sense that its Lipschitz coefficient defined by is finite. More precisely, it satisfies:

| (38) |

where is given by (32) (see also the comment that follows).

Proof..

We have for every , and for every Lipschitz continuous function

and elementary computations, already carried out in [4], show that

where can be taken equal to provided . It follows that is Lipschitz with Lipschitz constant ∎

Proposition 3.4.

(see [4]) The functions , , defined by the backward induction

satisfies for every . Moreover, where, for every ,

Furthermore, assume that the function is -Lipschitz continuous and that the function is -Lipschitz continuous in , uniformly in . Then, for every , the function is -Lipschitz continuous and there exists real constants , and (where is given by (32)), such that and

| (39) |

In particular, . Moreover the functions are Lipschitz too and

| (40) |

Proof. We proceed by a backward induction using (25) and (26), relying on the fact that is a Markov chain which propagates Lipschitz continuity. In fact, . Assuming that and using Equation (26) and the Markov property, we get

One shows likewise that , .

We also show this claim by a backward induction. In fact, and is -Lipschitz. Suppose that is -Lipschitz continuous. Then, for every , we can write

where and

with and . The function being Lipschitz continuous, one clearly has , , . Now, taking advantage of the linearity of expectation, we get

Then Schwarz’s Inequality yields

Now,

by Lemma 3.3. On the other hand, using that , and ,

Finally, owing to the definition of , we get

is Lipschitz continuous with Lipschitz coefficient satisfying

The conclusion follows by induction. As for the functions , we get for every ,

Hence, using that combined with Schwartz’s Inequality, we get

3.2.2 Second step of the proof of Theorem 3.2

Let be the quantization of the Markov chain , where every quantizer is of size , for every . Recall that the discrete time quantized BSDE process is defined by the following recursive algorithm:

where . Owing to the previous section, we are now in position to prove Theorem 3.2.

Proof of Theorem 3.2. Using the fact that, for every , , we have

| (41) |

where and are square integrable and orthogonal in . As a consequence, using the Pythagoras theorem for conditional expectation yields

On the other hand, it follows from the definition of the conditional expectation as the best approximation in among square integrable -measurable random vectors that

Let us consider now the last term of the equality (41). We have,

| where | ||||

| and |

As

we deduce that

| (42) | |||||

So, it remains to control each term of the above equality. Considering its last term, it follows from the Lipschitz assumption on the driver that

First, from the very definition of conditional expectation operator as the best quadratic approximation by a Borel function of (or, equivalently, the orthogonal projection on ), we derive that

On the other hand, starting from , (see Proposition 3.4), we get, using again the above characterization of the conditional expectation operator ,

| (43) | |||||

Finally, using the upper-bound for established in Proposition 3.4, we deduce that

| (44) | |||||

since, owing to (39) and (40), we have

, where

| (45) |

To complete the proof, it suffices to control the remaining terms in Equation (42). Using the (conditional) Schwarz inequality yields

Furthermore, using the fact that and owing to the measurability of and with respect to , we get

Then, using the conditional Schwarz inequality and again the contraction property of conditional expectation, we get

| (46) |

Using Schwarz’s Inequality for the -norm, we derive from (41), (42), (44) and (46) that

We first deal with the second term on the right hand side of the above inequality. Using the classical inequality

we derive that

Hence (using that , if ), we obtain, for every ,

| (48) |

where

It follows that, for every ,

Keeping in mind that , we finally derive by a backward induction that

We derive from the very definition of and that

where means that both random variables are -orthogonal. We know from (43) that

On the other hand, as , it is clear that so that

Conditional Schwarz’s Inequality applied with implies that

which in turn implies that

so that, finally,

3.3 Computing the terms

Recall that for every , the -valued random vector reads

with is a Borel function ( is the grid used to quantize ). As we easily derive that the function is defined on by the (-valued) weighted sum

where, for every , is an -valued vector given by

These vector valued “weights" appear as new companion parameters (as well as the original weights of the quantized transition matrices) which can be computed on line when simulating the Euler scheme of the diffusion by a Monte Carlo simulation.

Note that, for every and every ,

As a consequence, an alternative formula for can be

4 Background and new results on optimal vector quantization

It is important to have in mind that all what precedes holds true for any quantizations of the Euler scheme for any sequence of the form where is Borel and is finite. In fact the theory of optimal vector quantization starts when tackling the problem of minimizing the (and more generally the )-mean quantization error induced by this substitution, namely , which in turn will provide the lowest possible error bounds for quantization based numerical schemes. This question is in fact a very old question that goes back to the1940’s, motivated by Signal transmission and processing. These techniques have been imported in Numerical Probability, originally for numerical integration by cubature formulas, in the 1990’s (see [57] or [22]).

4.1 Short background

Let be a random vector lying in , . The -optimal quantization problem of size for (or equivalently for its distribution ) consists in finding the best -approximation of by a random variable taking at most values. The integer is called the quantization level.

First, we associate to every Borel function taking at most values the induced -mean error (where is the usual -norm on induced by the norm on (a priori any norm, but always the canonical Euclidean norm in this paper and in most applications). Note that when , the terms “norm" is an abuse of language since is only a metric space metrized by . As a consequence, finding the best approximation of in the earlier described sense boils down to solve the following minimization problem:

where denotes the cardinality of the set (commonly called grid or codebook depending on the field of application. It is clear that for every grid , for any Borel function ,

Equality holds if and only if is a Borel nearest neighbor projection defined by

where is a Borel partition of satisfying

Such a Borel partition is called a Voronoi partition (induced by ). The random variable is called a Voronoi quantization of induced by . It follows that for every , does not depend on the choice of the Voronoi projection. Thus, we may denote the -mean quantization error induced by the grid (under ). As a consequence, the optimal -mean quantization error finally reads

| (49) |

Note that for every level , the infimum in is in fact a minimum, , it is attained at least at one grid , see [41] or [57]. Any such grid is called an -optimal -quantizer and the resulting Borel nearest neighbor projection is called an -optimal -quantization. It should be noticed as well that is entirely characterized by the distribution of , hence will be often denoted by .

One shows that if then any optimal -quantizer is of full size . Furthermore (see again [41] or [57]), the optimal -mean quantization error at level decreases to as goes to infinity. Its rate of convergence is ruled by the so-called Zador Theorem recalled below, in which, temporarily may denote any norm on .

Theorem 4.1.

Zador’s Theorem Sharp asymptotic rate (see [41]): Let be a random vector such that for some real number and let denote the canonical Lebesgue decomposition of where stands for the singular part of . Then

| (50) |

| (51) |

( denotes the uniform distribution on the hypercube ).

Numerical aspects (few words about). From the numerical probability viewpoint, finding an optimal -quantizer is a challenging task, especially in higher dimension (). In this paper as in many applications we will mainly focus on the quadratic case . Note that, in practice, will be the canonical Euclidean norm on for numerical implementations.

The key property to devise procedures to search for optimal quantizers rely on the following differentiability property of the squared quadratic quantization error (also known as quadratic distortion function) for a fixed level (and with respect to the canonical Euclidean norm). First, we define the distortion function (which is defined on and not on the set of grids of size at most ) by:

| (52) |

To an -tuple we associate its grid of values so that . In particular, it is clear that

since an -tuples can contain repeated values.

Proposition 4.2 (see Theorem 4.2 in [41]).

The function is differentiable at any -tuple having pairwise distinct components and satisfying the following boundary negligibility assumption:

Its gradient is given by

| (53) |

The above negligibility assumption on the Voronoi partition boundaries does not depend on the selected partition. It holds in particular when the distribution of is strongly continuous assigns no mass to hyperplanes and, for any distribution such that , when .

The result is a consequence of the interchange of the differentiation and the integral leading to (53) when formally differentiating (52) (see [41, 57]). Consequently, any -tuple satisfies

Note that this equality also reads, still under the assumption ,

All numerical methods to compute optimal quadratic quantizers are based on this result: recursive procedures like Newton’s algorithm (when ), randomized fixed point procedures like Lloyd’s I algorithms (see [32, 62]) or recursive stochastic gradient descent like the Competitive Learning Vector Quantization (CLVQ) algorithm (see [32, 57] or [60]) in the multidimensional framework. However note that in higher dimension this equation has several solutions (called stationary quantizers) possibly sub-optimal. Optimal quantization grids associated to the multivariate Gaussian random vector can be downloaded from the website www.quantize.math-fi.com. For more details about numerical methods we refer to the recent survey [58] and the references therein.

4.2 Distortion mismatch: -robustness of -optimal quantizers

The distortion mismatch problem is the following: when does an -optimal sequence of quantizers for a random variable remain -rate optimal for some (if ) ? Or in more mathematical terms, if , , when do we have for such a sequence of -optimal quantizers

This problem has obvious applications in numerical probability since, for algorithmic reasons, one usually has access to optimal quadratic quantizers (see the website www.quantize.maths-fi.com) whereas they are currently used in a non quadratic framework. What will be done in Section 6 for nonlinear filtering is precisely to take advantage of this result to strongly relax some growth assumptions on the conditional densities involved in the Kallianpur-Striebel formula.

The distortion mismatch problem was first addressed in [42] for various classes of distributions on , in particular for distributions having a radial density satisfying (an almost necessary) moment assumption of order higher than . In the theorem below we extend this result to all random vectors satisfying this moment condition.

Theorem 4.3 (--distortion mismatch).

Let be a random vector and let . Assume that the distribution of has a non-zero absolutely continuous component with density . Let be a sequence of -optimal grids and let . If

| (54) |

for some , then

| (55) |

Definition 4.1.

Let and . A random vector has an -distribution (or its distribution is an -distribution) if (55) is satisfied.

Note that if has an -distribution, then it has an distribution for any since the -norm is increasing in .

Thus, the integrability condition (54) appears as a criterion to have an -distribution (see also the first remark after the proof of the theorem). Note that, as expected, so that the preservation of the -property for requires more than -integrability. Finally, if has polynomial moment at any order, then the -property holds for every .

Proof of Theorem 4.3. Step 1 (Control of the distance to the quantizers): Let be a sequence of -optimal quantizers. It is clear that, for every ,

The sequence is bounded since as and . Then there exists a real constant such that for every ,

Step 2 (Micro-macro inequality): The optimality of the grids , , allow to apply to the micro-macro inequality (see Equation (3.2) in the proof of Theorem 2 in [42]), namely : for every real constant and every ,

| (56) |

Let be an auxiliary Borel probability measure on to be specified further on. Set . Integrating the above inequality with respect to yields, owing to Fubini’s Theorem,

Now using that is Lipschitz continuous with coefficient , one derives that

and, still by Fubini’s Theorem,

| (57) |

Let . We set where is a probability density given by

The density shares the following property on balls: let and . If , then

and . Now let such that . As , this in turn implies that . As a consequence

Let . It follows from Equation (57) and the reverse Hölder inequality applied with and that

It follows from the assumption made on (or ) that, for small enough ,

As a consequence

| (58) |

where .

Step 3 (Upper-bound for the quantization error increments): Since the distribution of is absolutely continuous ( admits a density), one derives following the lines of the proof of Theorem 2 in [42] this upper-bound for the increments of the -quantization error: there exists a real constant such that

Combining this inequality with (58) yields

where . This completes the proof by considering the root of the inequality.

Remarks. If is radial, more precisely if where is bounded and non-increasing on and denotes any norm on the above result holds true even if (see [53]).

Criterion (54) is close to optimality for the following reason. It has been established in [42] (Theorem 1) that if , and if is a sequence of -asymptotically optimal quantization grids, then

where is given by (51). Since , by an elementary application of the reverse Hölder inequality (see Equation (2.11) from [42]). On the other hand,

5 Numerical experiments for the BSDE scheme

To illustrate empirically the improved theoretical rate obtained in the previous section, we deal here with two toy examples: a bull-call spread option (in a market where the risk free returns for the borrower and the lender are different) and a multidimensional example with the Brownian motion. Note that our aim is not to make an extensive numerical test with a complete description (or a complexity analysis) of several used algorithms for the optimal grid search. These subjects have extensively been considered in the past and we refer for example to [60] for more details.

Numerical tests are performed using our quantized BSDE algorithm. At each discretization instant , we associate a quantization grid of size , possibly not optimal a priori, and the resulting Voronoi quantization of . Then, we set for every , , , the transition weights (or probabilities)

and, for , , the marginal weights , .

Setting , for every , the quantized BSDE scheme reads as

where for ,

| (59) |

with

We use a time discretization mesh of length for the first example and of length for all dimensions in the second example. In both examples below, the quantizers , (with ) are computed from a scaling of the optimal grid of Gaussian distributions available on the website devoted to quantization

The transition probabilities are approximated using a Monte Carlo simulation of size for all examples (keep in mind that we may have the same precision with a smaller size of Monte Carlo trials but our aim is not to optimize these sizes of the trials). For simplicity reasons, we use a uniform dispatching across the time layers for the quantizers by assigning the same grid size to all at every discretization step , . Once the optimal quantization grids are computed offline, the complexity of our procedure depends on the grid sizes and varies from less than second in lower dimension up to a few minutes in dimension 5, almost entirely devoted to the computation by Monte Carlo simulation of the transition weights. By contrast, the (quantized) dynamic programming descent itself is instantaneous.

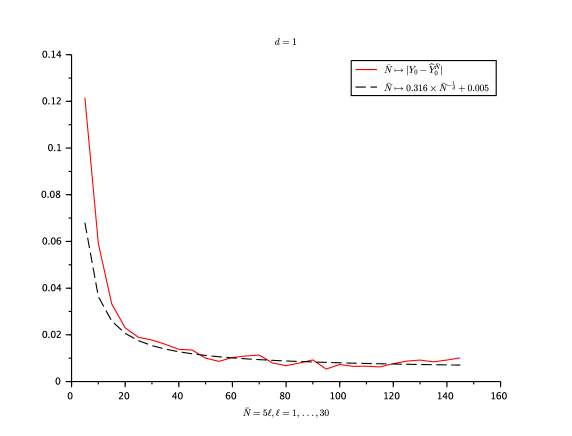

5.1 Bid-ask spread for interest rate

Let us consider a model with two interest rates introduced in [11]: a borrowing rate and a lending rate where the stock price evolves following the Black-Scholes dynamics

Let be the amount of assets held at time . Then, the dynamics of the replicating portfolio is given by

| (60) |

where and the driver function is given by

As in [10], we consider a bull-call spread comprising a long call with strike and two short call with strike , with payoff function

Furthermore, we consider the set of parameters:

The BSDE (60) has no analytical solution. We refer to the reference prices given in [10, 67] where is approximated by . We put and, for every , the grid sizes is constant (keep in mind that ). The quantizers have been obtained by using dilatations of optimal Gaussian quantization grids that we substitute to into the formula .

The numerical convergence rate of the error , , is depicted in Figure 1, including a polynomial regression which emphasizes the empirical order of the convergence rate, namely .

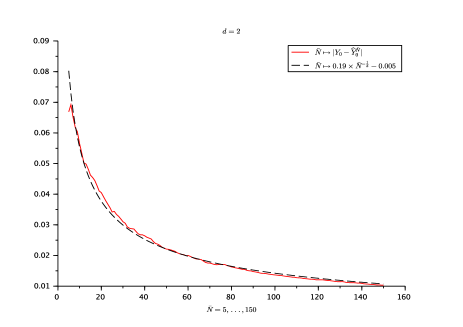

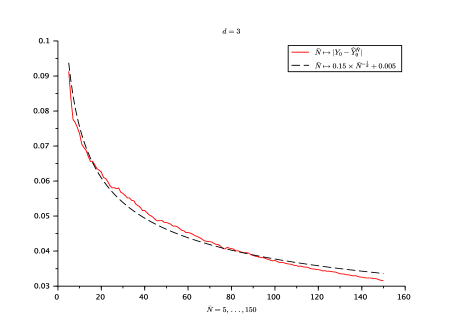

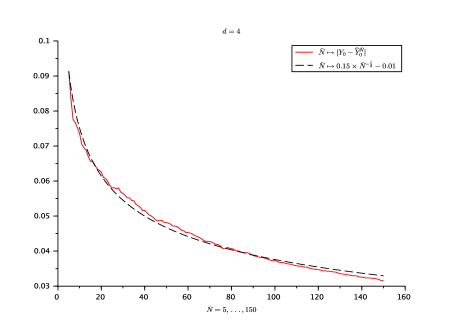

5.2 Multidimensional example

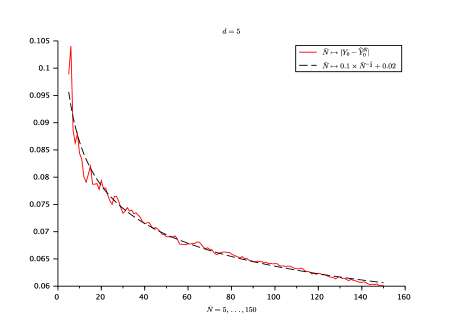

We consider the following non linear BSDE (example due to J.-F. Chassagneux):

where

and is a -dimensional Brownian motion. The solution of this BSDE is

| (61) |

For the numerical experiments, we use the (regular) time discretization mesh with . We choose , , so that and , for every . We depict in Figures 2 and 3, the rates of convergence of towards , for the (constant) layer grid sizes . The graphics in Figures 2 and 3 confirm a rate of convergence of order .

6 Nonlinear filtering problem

We consider in this section the discrete time nonlinear filtering model and the quantization based numerical scheme presented in the introduction. Our aim is two-fold: improving the error bounds like for BSDE on the one hand and, on the other hand, relaxing the Lipschitz continuity on the conditional densities (in favor of a local Lipschitz continuity assumption with polynomial growth). In particular, these new error bounds confirm the results obtained in the survey [68] devoted to a comparison between quantization and particle based numerical methods for non-linear filtering.

6.1 Error analysis

Let us first recall the assumptions made in [59] on the conditional transition density functions and the Markov transitions :

For every there exists such that

The Markov transition operators propagate Lipschitz continuity (in the sense of Lemma 3.3) and

For every , the functions are bounded on and we set

We will relax these Lipschitz assumptions into controlled Lipschitz assumptions. Let us consider, for a fixed non-negative function satisfying,

, .

We make the following -local Lipschitz continuity assumption (which is weaker than ) on the growth of the conditional transition density functions :

There exists such that, for every ,

A standard situation is the sometimes called framework when the satisfy with the function for an , namely

For every there exists such that

When , this framework coincides with the Lipschitz one. To simplify some statement we will introduce

| (62) |

Example. We may consider a model in which the signal process is a discrete time real valued (Markov) process and that the observation process evolves as

where the function is bounded, locally Lipschitz continuous but possibly not Lipschitz. In this case, the conditional density functions do not depend on and read (where denotes the c.d.f. of the )

Thus, if , then will be of -type. This situation extend to any locally Lipschitz bounded function whose derivative has a “-growth" at infinity.

Then we ask the transitions to propagate this -local Lipschitz property as a counterpart of . Let be -locally Lipschitz with a local Lipschitz coefficient defined by

| (63) |

Remark 6.1.

One easily checks that the transition kernels of the Euler scheme with step (and Brownian increments) of a diffusion with Lipschitz continuous drift and diffusion coefficient have the -local Lipschitz property when , .

The following classical lemma is borrowed (and straightforwardly adapted) from [59] (Lemma 3.1).

Lemma 6.1.

Let and be two families of finite and positive measures on a measurable space . Suppose that there exist two symmetric functions and defined on the set of positive finite measures such that, for every bounded -Lipschitz function ,

| (64) |

Then,

| (65) |

In Theorem 6.3 below we will consider Assumption in place of Assumption (considered in [59]) to derive an error bound. This less stringent assumption is compensated by taking advantage of the distortion mismatch property established in Theorem 4.3. More precisely, we will need that the -mean quantization error, for an , associated to any sequence of optimal quadratic quantizers at level still goes to zero at the optimal rate .

The following lemma provides a control of the -local Lipschitz coefficients of the functions defined recursively by (14).

Note that we drop the subscript related to the observations in the conditional densities as well as the function in to alleviate notations in what follows.

Proposition 6.2.

Assume that , and hold and that, for every ,

| (66) |

Let be -locally Lipschitz function. Then, the functions defined by (14) satisfy

| (67) |

where and .

Let be the Markov chain defined as an iterated random map of the form

| (68) |

where is an i.i.d sequence of random variables independent of .

If there exists some such that

| (69) |

then .

In particular, for , the chain satisfies the integrability assumption and (66).

If and, for every , ,

| (70) |

then both and are satisfied. To be more precise

Remark 6.2.

Once again the Euler scheme with step satisfies Assumption (66) with functions , .

Proof.

By the Markov property, we have for every and every ,

| (71) |

It follows that, for every , , so that,

since . Let ; for every ,

Now, still for every ,

so that

Finally, collecting these inequalities, we deduce from Assumption (66) that, for every ,

The conclusion follows by a backward induction (discrete time Gronwall’s Lemma) having in mind that .

Notice that assumptions (66) and (69) hold when is a polynomial convex function and when is the Euler scheme (with step and horizon ) associated with a stochastic differential equation of the form (21).

Theorem 6.3.

Let us make few remarks about the assumptions of the theorem before dealing with the proof.

Remark 6.3.

If is convex and if all are quadratic optimal quantizers, then it is stationary satisfies so that, for every , we have, owing to the convexity of and Jensen’s Inequality,

Suppose that is a Markov chain of iterated random maps

under the assumptions of Proposition 6.2. Assume it satisfies the -local Lipschitz assumption with a function for some real constants . If for some , and the distributions of are absolutely continuous, then, all have an -distribution.

Proof.

Like in [59], the proof relies on the backward formulas (14) and (20) involving the functions and their quantized counterpart whose final values and define the un-normalized filter (applied to the function ) and its quantized counterpart, respectively.

Following the lines of the proof of Theorem 3.1 in [59], one shows by a backward induction taking advantage of the Markov property that the functions , , defined recursively by (14) satisfy and

| (73) |

where

Finally (un-normalized filter applied to ). One shows likewise that the functions defined by (20) satisfy (on the grid ) and

| (74) |

so that finally (quantized un-normalized filter). One shows like for the functions in Proposition 6.2 that . Now, using the definition of conditional expectation as an orthogonal projection (hence an -contraction as well), we have

| (75) | |||||

where we used in the second line the tower property for conditional expectation to show that (the -field ) and the contraction property of .

It follows now from the definition of the conditional expectation as the best approximation in among square integrable -measurable random vectors that

Let , so that for every , . Hölder’s inequality with conjugate exponents and gives

Let us deal now with the second term on the right hand side of (75) and set for convenience

By the triangle inequality and the boundedness of , we get

so that

It follows from , Hölder (still with and ) and Minkowski inequalities that

where .

Plugging these bounds in (75), we finally get that, for every ,

where

(we set by convention so that ). It follows by induction that

where, using the upper-bound for given by (67) (and the definition of that follows),

(we also used the elementary inequality , in the third line). Finally

where

and

We conclude by Lemma 6.1. ∎

The previous theorem highlights the usefulness of the distortion mismatch result: it allows to switch from Lipschitz continuous assumptions on the functions into local Lipschitz assumptions.

Remark 6.4.

Note that if we consider Assumption instead of Assumption in Theorem 6.3 we still improve the upper bound established in Theorem 3.1 of [59] since this amounts to setting and replacing everywhere the “" coefficients by . Then, like for BSDEs, the squared global error appears as the (weighted) cumulated sum of the squared quantization errors.

References

- [1] K. Bahlali. Existence and uniqueness of solutions for BSDEs with locally lipschitz coefficients. Elect. Comm. in Probab., 7:169–179, 2002.

- [2] V. Bally. An approximation scheme for BSDEs and applications to control and nonlinear PDEs. Prepublication 95-15 du Laboratoire de Statistique et Processus de l’Université du Maine, 1995.

- [3] V. Bally and G. Pagès. Error analysis of the quantization algorithm for obstacle problems. Stochastic Processes & Their Applications, 1:1–40, 2003.

- [4] V. Bally and G. Pagès. A quantization algorithm for solving discrete time multidimensional optimal stopping problems. Bernoulli, 6:1003–1049, 2003.

- [5] V. Bally, G. Pagès, and J. Printems. A stochastic quantization method for non-linear problems. Monte Carlo Methods and Appl., 1:21–34, 2001.

- [6] V. Bally, G. Pagès, and J. Printems. First-order schemes in the numerical quantization method. Math. Finance, 13(1):1–16, 2003. Conference on Applications of Malliavin Calculus in Finance (Rocquencourt, 2001).

- [7] V. Bally, G. Pagès, and J. Printems. A quantization tree method for pricing and hedging multidimensional american options. Mathematical Finance, 15:119–168, 2005.

- [8] C. Bender and R. Denk. A forward scheme for backward SDEs. Stochastic Processes and their Applications, 117(12):1793–1812, 2007.

- [9] C. Bender, N. Schweizer, and J. Zhuo. A primal-dual algorithm for BSDEs. Preprint., 2015.

- [10] C. Bender and J. Steiner. Least-squares Monte Carlo for backward SDEs. Numerical Methods in Finance, 12:257–289, 2012.

- [11] Y. Z. Bergman. Option pricing with differential interest rates. Review of Financial Studies., 8(2):475–500, 1995.

- [12] J. M. Bismut. Conjugate convex functions in optimal stochastic control. J. Math. Anal. Appl., 44:383–404, 1973.

- [13] B. Bouchard and N. Touzi. Discrete-time approximation and Monte-Carlo simulation of backward stochastic differential equations. Stochastic Process. Appl., 111(2):175–206, 2004.

- [14] N. Bouleau and D. Lépingle. Numerical Methods for Stochastic Processes. Wiley-Interscience, 1993.

- [15] P. Briand and C. Labart. Simulation of BSDEs by Wiener chaos expansion. Ann. Appl. Probab., 24(3):1129–1171, 2014.

- [16] P. Briand and C.e Labart. Simulation of BSDEs by Wiener chaos expansion. Ann. Appl. Probab., 24(3):1129–1171, 2014.

- [17] A.-L. Bronstein, G. Pagès, and J. Portès. Multi-asset American options and parallel quantization. Methodol. Comput. Appl. Probab., 15(3):547–561, 2013.

- [18] A.-L. Bronstein, G. Pagès, and B. Wilbertz. How to speed up the quantization tree algorithm with an application to swing options. Quant. Finance, 10(9):995–1007, 2010.

- [19] G. Callegaro and A. Sagna. An application to credit risk of a hybrid Monte Carlo-optimal quantization method. The Journal of Computational Finance, 16:123–156, 2013.

- [20] J. F. Chassagneux and D. Crisan. Runge Kutta schemes for BSDEs. Annals of Applied Probability, 24(2):2679–720, 2014.

- [21] J. F. Chassagneux and A. Richou. Numerical simulation of quadratic BSDEs. Ann. Appl. Probab., 26(1):262–304, 2016.

- [22] E.V. Chernaya. On the optimization of weighted cubature formulae on certain classes of continuous functions. East J. Aprox., 1:47–60, 1995.

- [23] D. Crisan, K. Manolarakis, and N. Touzi. On the Monte Carlo simulation of BSDE’s: an improvement on the malliavin weights. Stochastic Processes and their Applications, 120:1133–1158, 2010.

- [24] P. Del Moral, J. Jacod, and P. Protter. The Monte-Carlo method for filtering with discrete-time observations. Probab. Theory Related Fields, 120(3):346–368, 2001.

- [25] F. Delarue and S. Menozzi. A Forward-Backward stochastic algorithm for quasi-linear PDEs. The Annals of Applied Probability, 16(1):140–184, 2006.

- [26] F. Delarue and S. Menozzi. An interpolated stochastic algorithm for quasi-linear PDEs. Math. Comp., 77(26):125–158, 2008.

- [27] J. Diehl and P. Friz. Backward stochastic differential equations with rough drivers. The Annals of Probability, 40(4):1715–1758, 2012.

- [28] J. Douglas, J. Ma, and P. Protter. Numerical methods for forward-backward stochastic differential equations. Ann. Appl. Probab., 6:940–968, 1996.

- [29] N. El Karoui, S. Peng, and M. C. Quenez. Backward stochastic differential equations in finance. Mathematical Finance, 7(1):1–71, 1997.

- [30] C. Geiss, S. Geiss, and E. Gobet. Generalized fractional smoothness and -variation of BSDEs with non-Lipschitz terminal condition. Stochastic Processes and their Applications, 122(5):2078–2116, 2012.

- [31] C. Geiss and A. Steinicke. -variation of Lévy driven BSDEs with non-smooth terminal conditions. Bernoulli, 22(2):995–1025, 2016.

- [32] A. Gersho and R. Gray. Vector Quantization and Signal Compression. Kluwer Academic Press, Boston, 1992.

- [33] E. Gobet and C. Labart. Error expansion for the discretization of backward stochastic differential equations. Stochastic Processes and their Applications, 117:803–829, 2007.

- [34] E. Gobet, J. P. Lemor, and X. Warin. A regression-based Monte Carlo method to solve backward stochastic differential equations. Ann. Appl. Probab., 15(3):2172–2202, 2005.

- [35] E. Gobet, G. Liu, and J. Zubelli. A non-intrusive stratified resampler for regression Monte Carlo: application to solving non-linear equations. Preprint. HAL Id: hal-01291056, 2016.

- [36] E. Gobet, J. Lopez-Salas, P. Turkedjiev, and C. Vasquez. Stratified regression Monte-Carlo scheme for semilinear PDEs and BSDEs with large scale parallelization on GPUs. SIAM Journal on Scientific Computing, 38(6):C652–C677, 2016.

- [37] E. Gobet and A. Makhlouf. -time regularity of BSDEs with irregular terminal functions. Stochastic Processes and their Applications, 120:1105–1132, 2010.

- [38] E. Gobet and S. Pagliarani. Analytical approximation of BSDEs with nonsmooth driver. SIAM Journal on Financial Mathematics, 6(1):919–958, 2015.

- [39] E. Gobet and P. Turkedjiev. Approximation of backward stochastic differnetial equations using Malliavin weights and least-squares regression. Bernoulli, 22(1):530–562, 2016.

- [40] E. Gobet and P. Turkedjiev. Linear regression MDP scheme for discrete backward stochastic differential equations under general conditions. Mathematics of Computation, 85:1359–1391, 2016.

- [41] S. Graf and H. Luschgy. Foundations of Quantization for Probability Distributions. Lect. Notes in Math. 1730. Springer, Berlin., 2000.

- [42] S. Graf, H. Luschgy, and G. Pagès. Distortion mismatch in the quantization of probability measures. ESAIM Probab. Stat., 12:127–153, 2008.

- [43] S. Hamadène. Equations différentielles stochastiques rétrogrades: le cas localement lipschitz. Ann. Inst. Henri Poincaré, 32(5):645–659, 1996.

- [44] P. Henry-Labordère, X. Tan, and N. Touzi. A numerical algorithm for a class of BSDEs via the branching process. Stochastic Process. Appl., 124(2):1112–1140, 2014.

- [45] Y. Hu, D. Nualart, and X. Song. Malliavin calculus for backward stochastic differential equations and applications to numerical solutions. The Annals of Applied Probability, 21(6):2379–2423, 2011.

- [46] Y. Hu and S. Tang. Multi-dimensional backward stochastic differential equations of diagonally quadratic generators. Stochastic Process. Appl., 126(4):1066–1086, 2016.

- [47] C. Illand. Contrôle stochastique par quantification et application à la finance. PhD thesis, Université Pierre et Marie Curie, 2012.

- [48] I. Kharroubi and R. Elie. Adding constraints to BSDEs with jumps: an alternative to multidimensional reflections. ESAIM, Probability and Statistics, 18:233–250, 2014.

- [49] I. Kharroubi, M. Jin, H. Pham, and J. Zhang. Backward SDEs with constrained jumps and quasi-variational inequalities. The Annals of Probability, 38(2):794–840, 2010.

- [50] M. Kobylanski. Backward stochastic differential equations and partial differential equations with quadratic growth. Annals of Probability, 28:558–602, 2000.

- [51] J.-P. Lepeltier and J. San Martin. On the existence of BSDE with superlinear quadratic coefficient. Stochastics and Stochastic Report, 63:227–240, 1998.

- [52] H. Luschgy and G. Pagès. Functional quantization rate and mean regularity of processes with an application to Lévy processes. Annals of Applied Probability, 18(2):427–469, 2008.

- [53] H. Luschgy and G. Pagès. Marginal and Functional Quantization of Stochastic Processes. book, in progress.

- [54] J. Ma, P. Protter, and J. Yong. Solving forward-backward stochastic differential equations explicitly-a four step scheme. Probab. Theory Related Fields, 98:339–359, 1994.

- [55] J. Ma and J. Yong. Forward-Backward Stochastic Differential Equations and their Applications. Lect. Notes in Math. 1702. Springer., 2007.

- [56] H. Mete Soner, N. Touzi, and J. Zhang. Wellposedness of second order backward SDEs. Probab. Theory Relat. Fields, 153:149–190, 2012.

- [57] G. Pagès. A space vector quantization method for numerical integration. J. Computational and Applied Mathematics, 89:1–38, 1998.

- [58] G. Pagès. Introduction to optimal vector quantization and its applications to numerics. ESAIM Proc. & Survey, 48:29–79, 2015.

- [59] G. Pagès and H. Pham. Optimal quantization methods for nonlinear filtering with discrete time observations. Bernoulli, 11(5):893–932, 2005.

- [60] G. Pagès and J. Printems. Optimal quadratic quantization for numerics: the gaussian case. Monte Carlo Methods and Applications, 9(2):135–165, 2003.

- [61] G. Pagès and B. Wilbertz. Numerical Methods in Finance, chapter Optimal Delaunay and Voronoi Quantization Schemes for Pricing American Style Options, pages 171–213. Springer Proceedings in Mathematics, 2012.

- [62] G. Pagès and J. Yu. Pointwise convergence of the Lloyd I algorithm in higher dimension. SIAM J. Control Optim., 54(5):2354–2382, 2016.

- [63] E. Pardoux. BSDEs, weak convergence and homogenization of semilinear PDEs. Nonlinear Analysis, Differential Equations and Control, NATO Science Series, 528:503–549, 1999.

- [64] E. Pardoux and S. G. Peng. Adapted solutions of backward stochactic differential equation. Systems and Control Letters, 14:55–61, 1990.

- [65] E. Pardoux and S. G. Peng. Backward stochastic differential equations and quasilinear parabolic partial differential equations. Lecture Notes in CIS, 176:200–217, 1992.

- [66] H. Pham, W. Runggaldier, and A. Sellami. Approximation by quantization of the filter process and applications to optimal stopping problems under partial observation. Monte Carlo Methods and Applications, 11:893–932, 2005.

- [67] M. J. Ruijter and Oosterlee C.W. A Fourier cosine method for an efficient computation of solutions to BSDEs. SIAM J. Sci. Computation, 37(2):859–889, 2015.

- [68] A. Sellami. Comparative survey on nonlinear filtering methods: the quantization and the particle filtering approaches. Journal of Statistical Computation and Simulation, 78(2):93–113, 2008.

- [69] P. Turkedjiev. Two algorithms for the discrete time approximation of Markovian backward stochastic differential equations under local conditions. Electron. J. Probab., 20(50):DOI: 10.1214/EJP.v20–3022, 2015.

- [70] J. Zhang. A numerical scheme for BSDEs. Ann. Appl. Probab., 14(1):459–488, 2004.

- [71] W. Zhao, Y. Fu, and T. Zhou. New kind of high-order multi-step schemes for forward backward stochastic differential equations. SIAM J. Sci. Comput., 36(4):A1731–A1751, 2014.

Appendix A Proof of Theorem 3.1

Proof of Theorem 3.1.

Step 1. Temporarily set for convenience for . Applying Itô’s formula we have

As is Lipschitz continuous in , it is straightforward, setting , that

| (76) |

Then, it follows that

Owing to Young’s inequality (, for every and ) we get

After choosing and such that , we take the expectation in both sizes of the previous inequality and use the fact that (owing to conditional Jensen inequality) to get

Owing to the fact that and setting , we have

On the other hand, we have

| (77) |

It follows that

Since , we have

Now, let us choose so that . Owing to the fact that , this implies that . This constraint holds true if . Taking and owing to the fact that as goes to infinity we may consequently choose , for every . Setting

it follows that, for every ,

| (78) |

In particular we have and

| (79) |

Since then and we may show by induction that if then

Now, setting in (78) we get

Furthermore, since (see (77)), we deduce that

where is a positive real constant not depending on .

Step 2. We show that satisfies

In fact, we have for every ,

Then, using Assumption (76) yields

Now, thanks to the previous step we know that

We also know that . As a consequence, there exists a positive real constant such that for every ,

Step 3. Let . It follows from Itô’s formula that

Using the Young inequality: , , yields

| (80) | |||||

The stochastic integral on the right hand side of the previous inequality is a martingale since both and lie in . On the other hand, owing to the error bound for the Euler scheme and the fact that is an Itô process, we get

for some positive real constants and . Then, taking the expectation in (80) and using the fact that

yield

| (81) |

We notice that for every and for every ,

| and | ||||

where means that is an -valued -measurable random vector. Then, using the inequality , we get

Now, owing to the Cauchy-Schwarz inequality, we have

Consequently, taking the expectation in (A) leads to

Coming back to Inequality (81) and setting yields

Owing to Step 2, we have for every , with so that, using the conditional Jensen inequality we get

As a consequence, using that , we have

Let . Then

so that, for large enough , say , since . It follows that

In particular, for every , as ,

Now, setting yields likewise

which completes the proof since one can always satisfy this inequality for by increasing the constant .

∎