Dynamic Pricing in a Dual Market Environment

Wen (Wendy) Chen

Providence Business School, Providence College, Providence, RI 02908,

wchen@providence.edu

Adam Fleischhacker

Lerner College of Business and Economics, University of Delaware, Newark, DE 19716,

ajf@udel.edu

Michael N. Katehakis

Department of Management Science and Information Systems,

Rutgers University, NJ 08854,

mnk@rutgers.edu

Abstract

This paper is concerned with the determination of pricing strategies for a firm that in each period of a finite horizon receives replenishment quantities of a single product which it sells in two markets, e.g., a long-distance market and an on-site market. The key difference between the two markets is that the long-distance market provides for a one period delay in demand fulfillment. In contrast, on-site orders must be filled immediately as the customer is at the physical on-site location. We model the demands in consecutive periods as independent random variables and their distributions depend on the item’s price in accordance with two general stochastic demand functions: additive or multiplicative. The firm uses a single pool of inventory to fulfill demands from both markets. We investigate properties of the structure of the dynamic pricing strategy that maximizes the total expected discounted profit over the finite time horizon, under fixed or controlled replenishment conditions. Further, we provide conditions under which one market may be the preferred outlet to sale over the other.

1 Introduction

This paper investigates the problem of a firm that in each period of a finite horizon , receives replenishment quantities of a single product that it sells through two markets: i) an on-site market (e.g., physical stores) and ii) a long-distance market (e.g., an online site). The firm aims to maximize its total expected discounted revenue over a finite sales horizon of periods by adjusting the selling prices at the on-site market () and the long-distance market () in each period . Both markets’ price dependent demands are satisfied using inventory that is held at the on-site market location. When inventory is available, the on-site market’s demand is satisfied immediately while the long-distance market’s demand is satisfied after a one period delay. In this way, our scenario mimics one where physical channel customers are fulfilled while in the store and the firm’s online/long-distance customers are fulfilled after a given delay (i.e. we assume they are willing to wait one period before product is shipped). From the firm’s perspective, online orders become a deterministic component of the next period’s demand and hence, prices can be set for the following period while taking advantage of this information. Inventory in our model is exogenously determined and we consider it to be a predetermined supply schedule as is often the case with fashion items. For tractability, we assume excess demands from both markets are fully backlogged at a specified per unit per period penalty cost. For long-distance customers, a reasonable shipping delay of one period is considered palatable.

Examples of dual market strategies using a common pool of inventory are becoming more prevalent. Large retailers like Nordstrom and Macy’s are expanding the role of their stores beyond their traditional role and they are now using a combination of technology and customer service known as omnichannel fulfillment to avoid stockout-driven lost sales from within their stores. In addition to being a shopping destination for local customers, these retailers are transforming stores into online order fulfillment centers and are using store inventory to satisfy an additional market of online shoppers. Firms employing this type of dual market strategy have found dramatic improvements in inventory turns and reduced markdowns because of the enlarged customer base through which store inventory can be sold [15, 59]. In addition, there is currently a trend for U.S. retailers to use their online sales channel and U.S. based inventory to reach customers overseas, e.g., in China [10]. Partnerships with Alipay, a payment processor closely linked to Alibaba Group Holdings, enable U.S. retailers to overcome both economic and regulatory hurdles to enable this type of transactions. In addition, Chinese consumers often prefer the reliability and brand authenticity offered by buying directly from U.S. stores, cf. [58]. The reverse shipping direction is also becoming more common with an inventory pool in China being used to reach Chinese customers living abroad or overseas [62].

As serving dual markets has become easier for firms to achieve, smaller firms are also able to pursue dual market strategies. One such firm, J&R Music, expanded into online sales after the events of September 11, 2001 led to decreased foot traffic at their New York City store [19]. The ability to reach new customers allowed them to offset the reduction in local customers. Gary’s Wine and Marketplace, a local New Jersey wine retailer, attributes their winning of Beverage Dynamic’s 2012 Retailer of the Year to their new online presence [46]. The wine seller now has “10% of the business” coming from its online store that is operated out of the back of its flagship Wayne, NJ retail outlet.

In terms of pricing in dual markets, pricing policies within firms can be either constant across markets or vary by market [72, 41]. In fashion retail, using pricing differences to intensify demand in online and/or physical markets is commonplace.

To provide decision support and insight for this trend towards a single pool of inventory being used to satisfy demand from two markets (channels), we investigate the dynamic pricing policies of a retailer using store-level inventory to serve both its physical in-store customers and an additional market of long distance customers to whom product is shipped. This retailer will use their pricing policies in each market to intensify or reduce expected demand to better match its current and anticipated inventory positions. Since each market’s demand pulls inventory from a common pool, a key distinction between serving these two markets is how inventory can be deployed to fulfill demand without penalty. For customers using the physical channel, demand is preferably satisfied instantaneously while customers in the online channel are more willing to wait for product to be shipped and delivered. As such, the optimal pricing policies developed in this paper regulate each market’s demand intensity to balance the benefits of delivery postponement offered by on-line sales against advantages, such as larger margins or smaller demand variability, that are available through the physical channel.

For example, Ann Taylor, the upscale women’s apparel retailer, often employs such market-specific promotional strategies. In one promotion it may seek to increase online (long-distance market) demand (e.g. Figure 1(a)), with another it seeks to increase in-store (on-site market) demand (e.g. Figure 1(b)), and at other times the firm seeks to increase demand in both markets (e.g. Figure 1(c)).

The paper has the following structure. In Section 2 we review related literature. Our study of dynamic pricing extends the existing single market literature to a dual market environment. In Section 3 we define the notation and state the main assumptions that we will use throughout the paper. In Section 4 we investigate the basic properties of model specified in §3. In Section 4, through exploration of both additive and multiplicative cases of demand variability, we find that a different type of demand variability leads to different pricing policies being optimal. In §4.2, it is shown that the optimal prices for both markets decrease in the inventory level when the on-site market demand noise is additive. However, this property does not hold in the case at which both markets’ demand noise is multiplicative. For the multiplicative case, in §4.3, we show that the firm’s market preference under an optimal policy can be specified by a threshold policy. Special cases for each market’s demand being correlated and for the price in each market being equal are also explored in this section. In Section 5 insights into the managerial implications of the optimal policies are explored and discussed. For example, it is pointed out that at lower inventory levels a firm can prefer sales through the long-distance market even in cases where the marginal profit of the on-site market is significantly higher. We conclude this section with a brief discussion of issues related to adopting alternative or relaxed assumptions to those made in this paper.

2 Literature Review

This paper’s main contribution is the construction of optimal dynamic pricing policies in a dual market environment and the subsequent development of those policies’ managerial implications. Our study of a second additional market extends the vast literature of dynamic pricing studies that have been done in single market environments [see surveys in 13, 31, 60] to provide decision support for this relatively new capability of companies to profitably employ long-distance sales markets; the combination of the internet’s global reach with efficiencies in both domestic and international shipping has ushered in the idea of profitably serving local and long-distance markets from the same pool of inventory.

The single market studies most related to our research are finite time horizon models where a firm uses dynamic pricing to intensify or reduce stochastic demand in response to current and future supply availability. Authors Gallego and van Ryzin [38] called this intensity control and modeled this using a Poisson arrival process with a price-dependent arrival rate. A related earlier study considered a model for joint pricing and ordering with an exogenously determined stocking policy [27], [61]. Our model is a dual market extension to the fully backlogged, periodic review, single market model analyzed by Federgruen and Heching where it is demonstrated how to characterize and compute simultaneous pricing and inventory policies [32]. The work of Chen and Simchi-Levi [24] extends [32] to model an additional fixed cost component to ordering costs as well as more general demand processes. Other extensions include assumptions to accommodate substitute products [30], incorporation of lost sales as opposed to backlogging [57], and the analysis of demand learning with finite capacity [5].

Chen in [21] provides a model of a firm that may segment its market to gain advanced demand information, as follows. The customer population is assumed to consist of M segments or types, characterized by different reservation prices Poisson arrival processes with different rates. Arriving customers are presented with a price schedule that specifies decreasing prices a customer will pay if he/she agrees to different, increasing, shipping delays. Under sufficient assumptions it is shown how to assign customers to the different market segments so as to maximize the firm’s long-run average profits. In addition in [21] given an optimal price schedule, the author develops a optimal replenishment policy, for a a firm that operates with an -stage supply chain; where Stage 1 (the point from which the product is shipped to customers) is replenished by Stage 2, which is replenished by Stage 3, etc., and Stage N by an outside supplier with ample stock. It is shown that for any price schedule, the optimal replenishment policy (that minimizes long-run average systemwide holding and backorder costs) is to follow an echelon base-stock policy with order-up-to a level that is a function of stage and time. Heuristic computational methods are also provided.

Our study herein focuses on a different problem for a firm in which there is a finite horizon selling season, and prices are dynamically adjusted every period as a function of the “current” inventory level and the number of periods remaining in the season. Other significant differences between the two studies include the demand models we use and the exogenously determined replenishments in our model.

In extending the dynamic pricing literature to dual markets, we adopt assumptions that have been used in previous single market dynamic pricing studies. These assumptions include the modeling of demand, leadtimes, stockouts, and review policies. Our first notable assumption is that demand is a non-stationary linear function of price which includes either an additive or multiplicative stochastic term; the same form that is used in [2, 24]. For the additive type of demand uncertainty,[24] prove the optimality of (s,S) policies, but also show that those results do not hold for more general demand functions (i.e. multiplicative plus additive). In most similar studies, optimal prices are shown to be decreasing in inventory level [see for example 25, 26, 45, 52].

Given the complexity of our model, we adopt the simplifying assumption of a one-period delay (lead time) for the fulfillment of the long-distance market demand. The use of a one period lead time has a long history of being used to facilitate tractability [e.g. 43, 9, 37, 65, 67, 29]. More recently, the assumption has been used in [6] to develop a mechanism of cost evaluation and optimization for a deterministic replenishment lead-time model (also see this paper for a detailed review of continuous-review inventory models), in [68] to analyze the effect of cancellation contracts on buyer ordering and supplier production policies, and in [66] to study a multi-period inventory model in which a supplier provides two alternative lead-time choices to customers, either a short or a long lead time.

Lastly, in regards to our modeling assumptions, we contribute to a long history of studying fully backlogged periodic review inventory systems to yield tractable insights [see 7, 8, 32, 12, 11, for examples]. Other relevant studies employing this assumption include analyzing pricing and inventory decisions when the supply chain includes multiple retail locations [33], Markovian demand [70], and stochastic leadtimes [51].

Many notable models in the literature leverage different assumptions regarding the interplay of demand, price, and inventory and we include some similar works here. These include assumptions of inventory-dependent demand [56, 28] as well as the modeling of perishable inventory where examples include [14] (in the context of a retail chain with coordination among its stores), [35, 74, 50, 47] (whose authors develop a model that incorporates a simple risk measure that can be used to control the probability that revenues are below a minimum acceptable level). Dynamic pricing policies specific to applications in airline seat pricing are also an important application area and readers are encouraged to see [71] and [63] as examples in this space.

Our research is also related to the dual-market research that is widely studied in the information systems (IS) and marketing literature. This work has mainly focused on the benefits of online sales and how the additional sales channel leads to higher valuations for a firm [see e.g. 18, 17, 20]. The key drivers for the higher performance are noted to be better information access and lower setup costs. Other notable work considers the inter-market competition and demand dependencies that may exist when serving two markets [see 36, 16, 42].

The contribution of this paper is important as it provides managerial insight while tackling a level of complexity that has been considered difficult in previous efforts. Specifically, complexity due to the interplay between a retailer’s online and physical channels leads to difficulty crafting optimal dual channel strategies, see review by [1]. In addition, finding the optimal strategy when more than one type of multiplicative uncertainty is considered creates additional complexity [e.g. 4, 23] because a firm cannot always optimally increase price in response to decreasing inventory. Despite this complexity, we can provide structural insights into the optimal pricing policies in two markets and also, provide managerial insights as to the drivers of preferring demand in one market over another. There are several papers, tangential to our own, that have investigated different aspects of this complexity. Similar to our model, [22] model endogenously determined demand in a dual channel environment, but as opposed to manipulating price and/or inventory decisions to intensify demand as we do, the authors restrict attention to policies choosing optimal service levels (as measured by product availability in the physical channel and delivery lead time through the online channel). Similar studies of endogenously determined response times fall under the category of time-based competition [see for example 48, 69]. For other related work we refer to [39], [44], [53], [54] and references therein.

3 The Basic Model

Let denote the finite number of periods in the selling horizon and let denote the posted selling price at market in period

We will use the following price mean demand model. First, we assume that there exists a function that represents the relation between the selling price and the mean amount of demand so that for each period and market . Thus, deciding the selling price is equivalent to deciding the mean amount of demand and conversely setting the mean demand of market at period to is equivalent deciding a price: . Further, it is assumed that where and are known finite lower and upper bounds for the price of market respectively. Thus, and are respectively upper and lower bounds for .

The special cases: (for , , , ) and (for , ,, , ) are well known examples of mean demand models in the literature and the reader is referred to both [52] and [24] for further discussion. Throughout the paper, we often simplify the demand model notation by dropping the explicit functional relationship between demand and price and simply write for .

The expected revenue is assumed to be a strictly increasing concave function and twice-differentiable in . The implication of this assumption is that the retail firm’s revenue increases as the mean demand increases, but does so with diminishing returns to increasing demand, a similar assumption can be found [24].

As in [24], we consider two types of demand stochasticity (i.e demand noise), additive and multiplicative. While the firm can choose mean demand by setting price accordingly, actual demand is a stochastic function that can be expressed as:

| (1) |

Here, is a random variable representing multiplicative demand noise where and , for all . The random variables represent additive demand noise and it is assumed that , for all . Using this expression for stochastic demand, products with price sensitive customers will often exhibit demand realizations consistent with the multiplicative uncertainty model whereas products with less price sensitive customers are best modeled using additive demand uncertainty. To gain insights, we develop most of our results for the more tractable case where each market’s demand is independent of the other. Subsequently, in §4.3.3 we relax this assumption.

In each period, there are inventory holding and backorder costs, their sum we denote by . For our analysis, we adopt the common assumption of a holding cost structure: where . Generally, we call as the unit holding cost and as the unit shortage cost. Unmet demand is fully backlogged.

We note that the backlogging assumption for items of the primary market is an approximation, as in reality (i.e., reasonable values of the pertinent costs) most of the time backlogging will be incurred only for items demanded in the secondary market . Generally, retailers will satisfy backlogged demand prior to replenishing shelves. However, does not distinguish the priority with which backlogged customers are satisfied i.e., failing to satisfy a new customer or a backlogged customer incurs the same per period penalty. In addition even though, replenishment quantity decisions are made exogenously, the holding cost is relevant to the retailer as it represents a measure of cost due to some items being damaged through mishandling, losses due to theft or other record keeping problems, as well as the standard opportunity costs.

The sequence of events at each period , can be written as follows. The inventory level, , is reviewed. ii) A quantity of product arrives and is made available in the current period, where is exogenously determined. iii) The retailer sets the demand intensity level (through pricing changes) by choosing the mean demands for the on-site market and the long-distance market . iv) Demand for the on-site market, , is realized, and satisfied immediately up to the extent there is available supply. Unmet demand is fully backlogged. v) Demand for the long distance market, is realized. The long-distance market demand, while known, is neither satisfied nor backlogged in this step. vi) Holding costs and backorder costs that are a function of the on site market ending inventory are incurred:

Note that inventory held to meet the long-distance demand incurs a holding cost charge in this step, since it is not subtracted from the ending inventory in the term ; it is the price the firm pays for delaying the fulfillment of (via shipments) by one period. vii) Demand for the long distance market, is processed and satisfied to the extent inventory is available. Unmet demand is fully backlogged and not distinguished from any on-site demand that has been backlogged.

Let () denote the expected revenue at market , in period . Since unmet demand is backlogged, we have:

The inventory level for period is calculated as follows:

| (2) |

Let be the optimal expected profit from period to the end of horizon. The terminal condition is

The justification of the terminal condition is as follows. At the end of the horizon, i.e., when , if there is a shortage, i.e., when , then shortage incurs is assumed to be supplied by an external supplier at the firm’s expense, of per unit of shortage. If there is remaining inventory, , then any remaining inventory is assumed to have zero salvage value and .

Letting be a discount factor, the dynamic programming equations can be written as follows:

| (3) |

where

| (4) | |||||

The retailer starts each period with a given inventory position and a predetermined shipment, . The retailer’s objective is to control the demand intensities: through price changes, to maximize expected profit over the planning horizon.

Let be the maximizer of Eq. (3). We will use the convenetion that if more than one maximizers exist, the retailer chooses the solution with the smallest sum of each market’s mean demand.

To avoid trivial cases, we make the following assumption:

Assumption 1

For , the following are true

-

1.

.

-

2.

The first statement of Assumption 1 ensures the retailer has incentive to both carry inventory and backlog demand as required by guaranteeing that the marginal revenue is bigger than both the unit holding cost and the unit shortage cost. The second statement of Assumption 1 avoids trivial cases where a retailer chooses to backlog demand towards the end of planning horizon because the outside supplier’s cost is competitive with the firm’s internal manufacturing costs. Due to this high cost of outsourcing supply in the last period, we assume the retailer will not sell products through the long-distant market in the last period ().

4 Structure of Optimal Policies

In this section, we analyze the model specified in §3. In §4.1, we investigate the basic properties of the value function and show how concavity guarantees the existence of an optimal solution to the dual-market dynamic pricing model. In §4.2, we show that the optimal prices for both markets decrease in the inventory level when the on-site market demand noise is additive. However, this property does not hold in the case at which both markets’ demand noise is multiplicative. For the multiplicative case, in §4.3, we show that the firm’s market preference under an optimal policy can be specified by a threshold policy. A resulting insight is the identification of conditions under which a firm prefers to sell products in the long-distance market. Special cases for each market’s demand being correlated and for the price in each market being equal are also explored in this section.

4.1 Concavity and Supermodularity Properties

In the following two lemmas, we state structural results regarding the value function of Eq. (3) and the profit function of Eq. (4). We will use these results in the subsequent analysis. Lemma 1 establishes the concavity of as well as concavity and supermodularity properties for and thus, it ensures the existence of an optimal solution.

Lemma 1

The following statements are true.

-

(i)

.

-

(ii)

is concave in and is, component-wise, concave in each of the variables . .

-

(iii)

is submodular in and supermodular in and in .

The existence of a maximizer follows from the concavity of . Further the concavity of the profit function , in , indicates that the marginal profit decreases in the inventory level.

Combining the concavity results of Lemma 1 and [64], we have is supermodular in and . That is to say, if one market’s mean demand (i.e. price) is considered fixed, then the optimal mean demand in the other market () increases as the inventory level increases.

To find the optimal mean demand levels , we note that the first order partial derivatives can be written as follows:

| (5) | |||||

| (6) |

From the concavity of , , and , we have both and decrease in and . Indeed, note that is differentiable almost every where. is differentiable because demand uncertainty is continuous. First order partial derivatives, as above, can be used because and are both continuous in . Given the concavity of , the optimal solution, , is the solution to the above first order partial derivatives equations. Furthermore, we can obtain the following lemma:

Lemma 2

| (7) |

Lemma 2 implies that at least one of and increases in . Given more inventory on hand, the firm will decrease the sales price in at least one of the two markets. In the following section, we will establish the stronger result that both markets’ selling prices are decreasing in inventory level for the case of additive demand noise.

4.2 Additive Demand Noise

In this section, we consider the case where at least one of the market’s demand distributions are characterized by purely additive demand noise such that either or . For this case, price changes in the market(s) with additive demand noise result in changing the mean of a market’s demand distribution, but not its variability. As discussed in [2], additive demand noise is typical of well-established products where the effect of pricing changes on store traffic is well understood. Uncertainty in these cases tends to be limited to forecasting error. In contrast to what we will see in the next section when the demand uncertainty is multiplicative, a firm’s market preference for selling in one market over another will be unchanged in an additive demand uncertainty environment. The main results of this section, Theorem 1, show that in the additive demand uncertainty environment, the firm prefers to sell more products through both markets when the inventory level or the incoming inventory increases.

Theorem 1

Under the assumptions made and if the demand noise for the on-site market is additive, , for all , then

-

(i)

increases in .

-

(ii)

increases in .

-

(iii)

increases in .

Remark 1

Following similar logic, we can establish the effect of the incoming inventory . If the demand noise for the on-site market is additive, , for all , both and increase in .

Remark 2

Following a similar argument as that of Theorem 1, we can also obtain that both and are increasing in if the demand uncertainty in the long-distance market is additive, , for all .

Theorem 1(i) and (iii) states that inventory level increases are accompanied by decreases in the optimal selling prices for both markets and the firm seeks to simultaneously increase demand in both markets. We show in §4.3 that these results do not hold in the case of multiplicative demand variability. Also under additive demand uncertainty, the desired amount of customers increases less than one unit when inventory increases by one unit (see Theorem 1(ii)). Since the marginal revenue of an additional unit of sales decreases as demand increases, the expected demand must increase less than one unit when the inventory level is increased by one unit.

4.3 Multiplicative Demand Noise

In the multiplicative demand variability case (i.e., for and for all ) demand uncertainty increases with increasing demand and equivalently, it increases with decreasing price. In this section, we will numerically demonstrate that this increased uncertainty leads to non-monotone results. Because of this, characterizing the relationship between inventory and optimal demand levels is more challenging. However, it is still possible to gain insight and in this section, we leverage the existence of threshold policies to characterize: 1) conditions under which a retailer makes product available for sale in each market (§4.3.1), Theorem 2) conditions under which one market is considered preferable because product is made available for sale in that market, but not the other (§4.3.2), Theorem 3) conditions under which one market is considered preferable because its expected demand is higher than the other market which also offers the product for sale (§4.3.2),Theorem 4) the effects of demand correlation on a firm’s market preference (§4.3.3), and Theorem 5) the effects of restricting the price to be equal in both markets on a firm’s market preference (§4.3.4).

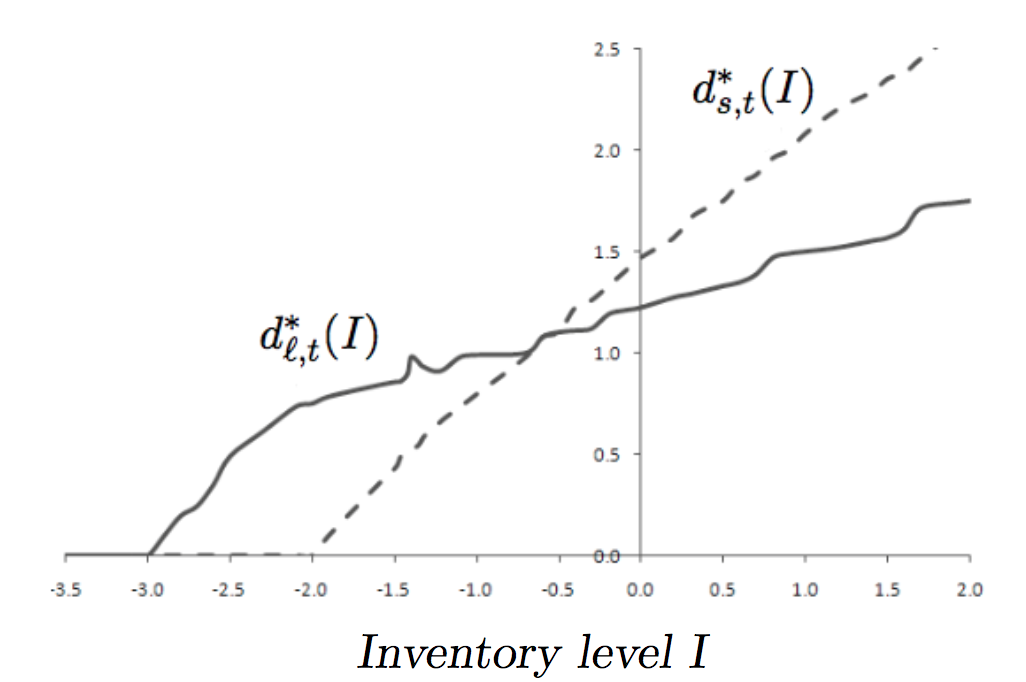

Before we present the analytical treatment of the multiplicative case, we use a numerical example to illustrate the behavior of the optimal average demand as functions of the inventory level. The parameters of this example are specified in Example 1 which is presented along with Figure 2. Three important characteristics of the multiplicative demand noise case are established with this example:

-

1.

The relationship between inventory level and optimal mean demand is non-monotonic. For example, .

-

2.

There appears to be a threshold inventory level for each market at which below that inventory level, sales are not pursued in that market and above that level, sales are pursued. When a market’s optimal demand level is zero, , we say that market is closed (i.e. ).

-

3.

As inventory levels increase, it is possible that the firm’s preference to sell in one market over the other (as indicated by a higher expected demand level) may reverse.

Note that in the multiplicative case, an increase in the mean demand in a particular market is accompanied by an undesirable increase in demand variance ) which makes the characterization of pricing decisions difficult to address. Similar difficulties have been noted by [49] who study an analogous environment with multiplicative yield uncertainty. In the multiplicative demand environment with two markets, increasing mean demand is not always the proper response to higher levels of inventory. In some cases, decreasing demand in one market allows for inventory to build (with the new deliveries) and can be used in subsequent periods.

Example 1

, , , and . follows a truncated normal distribution with , and . follows another truncated normal distribution with , and . The discount factor . and . Figure (2) below illustrates the non-monotonic relationship between the optimal mean demands for each market and the inventory level.

Remark 3

Our insight for the non-monotonicity phenomenon that appears in the case with multiplicative noise, (when with ) is as follows. When the controller increases the expected demand she also increases its variance with . Hence, it is possible that for certain values of inventory increasing implies cost contributions of a shortage that are low relatively to the cost implications of the additional demand variability. This is phenomenon is further amplified by the finite horizon of the selling season. Thus, as it was also noted in the context of a different model in [34], it may be it optimal to target a lower, rather than a higher, expected inventory level after ordering.

4.3.1 Threshold Policies for Market Preferences

The numerical study shows that optimal selling quantities in on-site market or long distance market may increase or decrease as inventory level increases. This lack of monotonicity makes analytical insights more difficult to achieve. Despite this, we characterize optimal pricing policies using the following two simplified benchmark problems:

| (8) | |||||

| (9) | |||||

| (10) | |||||

| (11) | |||||

Let denote the corresponding maximizer in Eq. (8) and denote the corresponding maximizer in Eq. (10) . If there are multiple maximizers, the solution with smallest is chosen .

Note that the above benchmark problems are no longer dynamic programs. They are one-period representations of our original model (§3) that assume that is given and that the demand uncertainty in one of the markets has been eliminated. In the benchmark problem , the long-distance market’s demand uncertainty in the current period is removed. Similarly, removes the on-site market’s demand uncertainty during the current period. For these two benchmark problems, threshold policies prescribing the levels of inventory at which the firm makes product available for sale in each market are established below in Lemmas 3 - 4. These threshold policies are then proven identical to the threshold policies that exist for the original model. Theorem 2, which is proved with Lemmas 3 - 4, establishes this existence and defines threshold inventory levels, , such that and if and only if . We introduce the two benchmark models to yield analytic results by making each market’s optimal demand intensity monotonic in the inventory level. Formally connecting the analytic results of the benchmark problems to the original problem is now shown through Lemmas 3 - 4 and Theorem 2.

Lemma 3

-

(i)

For the benchmark problem (), we have increases in .

-

(ii)

For the benchmark problem (), we have increases in .

Lemma 4

-

(i)

if and only if .

-

(ii)

if and only if .

Theorem 2

If the demand noise for both markets is multiplicative, , for all ,T, then the following are true.

-

i)

There exist numbers , , such that:

(14) -

ii)

Further, satisfies:

(15)

Theorem 2 proves the existence of these threshold inventory levels, , such that and ) if and only if . The theorem also provides a simple characterization of the on-site market’s threshold level in terms of marginal changes of the value function, , and the revenue function, .

Mathematically, choosing which products to sell through which combination of markets is a more challenging problem [73]. Retailers sometimes choose to offer greater assortment through their online channel while other retailers have products tailored to local needs that are not available online. The existence of threshold policies shows that inventory considerations play an important role in this decision. Further characterization of these policies is pursued in subsequent sections.

4.3.2 Market Preference

For any time period , we call the market with the higher demand intensity for a given inventory level, , as the “the preferred market”. At lower inventory levels, the preferred market can also be characterized as the market with the lower threshold inventory as the firm will open only the preferred market and keep the mean demand of the other market at . To differentiate, the market with the lower threshold inventory will be called the “preferred opening market”. As seen in Example 1, market preference may be surprising. In that example, the firm prefers the long-distance market at lower inventory levels even though the on-site market has greater expected revenue (, for all ) and lower demand variability (). Also from that example, we observe that as the inventory level increases, this preference can change. For larger values of , market preference is reversed and the on-site market is preferred as more demand is encouraged through that market, .

We now develop analytic insights into market preferences. From Theorem 2, we know that the marginal profit of the available inventory equals the marginal revenue of opening the on-site market at the on-site market threshold inventory level . Lemma 5 below provides an analogous, albeit complex, expression for the long-distance market threshhold .

Lemma 5

| (16) |

The conditions under which one market is preferred to another when the inventory level is low can now be stated:

Theorem 3

The following two statements are true.

-

i)

If , then .

-

ii)

If , then .

Managerially, Theorem 3 provides conditions for having a clearly preferred opening market. In general, if one market’s opening has an associated marginal expected revenue that sufficiently exceeds the other market’s opening marginal expected revenue, then that market becomes the preferred market. The question is what does it mean to sufficiently exceed the other market’s marginal revenue? For the on-site market to be clearly preferred, then the on-site’s marginal revenue must exceed the long distance market’s revenue by one unit of shortage cost. For the long distance market to be clearly preferred, then the long distance market’s marginal revenue must exceed the on-site market’s revenue by one unit of holding cost. In the next theorem, conditions where the preference is less clear are explored:

Theorem 4

When , the following two statements are true.

-

i)

If , then .

-

ii)

If , then .

Theorem 4 is best interpreted by examining the effects of shortage costs on the opening market preference. As in Theorem 3, when shortage costs are small and the on-site market provides greater marginal revenue upon market opening, then the on-site market is preferred (Theorem 4(i)). This preference continues until is large enough to meet the conditions of Theorem 4(ii). At this point, the value of delayed fulfillment in the long distance market comes to bear. By fulfilling long-distance orders in the subsequent period, pricing decisions in that subsequent period can be made with less demand uncertainty. And hence, by selling through the long-distance market the firm has less risk of incurring shortage costs than if the on-site market were opened. Notice that the firm still prefers selling in the long-distance market when . That is to say, even though the marginal expected revenue of selling in the long-distance market is less than the marginal expected revenue of selling in the on-site market, the firm still prefers selling in the long-distance market. We again refer the reader to Example 1 where the “counter-intuitive” behavior implied by Theorem 4(ii) is seen. In this example, the on-site market has higher marginal profit (i.e. ) and also lower variability in demand (i.e. ), and seems preferable in all the parameters of our model. Nevertheless, the threshold inventory level for opening the long-distance market is still lower than that of the on-site market; the advanced demand information of the long-distance market is still valuable.

We have seen that the market preference of the firm can change as the current inventory position increases. We study this phenomenon in Theorem 5 for the case of identical demand distributions and revenue functions in each market.

Theorem 5

If for all , and , follow the same distribution, and , then following statements are true.

-

i)

when .

-

ii))

when

Theorem 5 establishes the existence of a specific inventory level where if current inventory is below that level the demand intensity in the on-site market is optimally set higher than the demand intensity in the long-distance market. When current inventory exceeds that specified level, then the long-distance market becomes the preferred sales channel. The key insight is that inventory considerations have significant impact on the optimal selling strategy. In limited inventory situations a retailer prefers selling through an online channel, whereas when inventory is plentiful the on-site market will be the preferred sales channel. Due to the complexity of handling multiplicative demands, additional theoretical results seem intractable. However, the importance of this theorem is that it gives guidance to decision-making in a multi-market environment. The benefit of the long-distance market dominates the retailer’s policy when the inventory level is low. While this paper only analyzes a one period potential for delayed shipment, if a longer delay for the long-distance market is possible, then the advantage of long-distance market is even greater (assuming low inventory).

4.3.3 Correlated Demand

In the previous sections, we made the assumption that demand in each market was independent. We now turn to the significantly more complex case of correlated demands in the two markets. For example, one would expect that for certain short lifecycle products, like fashion or high-tech products, demand in both markets will ebb and flow together with waning or rising consumer sentiment. In the general case of correlated demands, optimal policies may not posses a structure determined by thresholds and insight for this case is not easily achieved. However, we have obtained the result of Proposition 1 below, that provides for a necessary condition for the on-site market to be opened.

Proposition 1

When and are correlated, the following is true:

Next we will discuss the perfect correlation case. Such cases are commonly used in studies of inventory systems with multiple random variables, e.g, [23]. For fixed the demands and exhibit perfect positive (negative) correlation when the variables and are related with Eq. (17), for a constant () .

| (17) |

In this case in Proposition 2 below, we provide provable conditions regarding the on-site market’s threshold inventory level for the case of perfectly correlated demand (negatively or positively correlated).

Proposition 2

When and satisfying that for all , the following are true:

-

•

, if and exhibit perfect positive correlation;

-

•

, if and exhibit perfect negative correlation.

Combining these two propositions, Theorem 6 below, helps us shed light on comparing the correlated demand case and the independent demand case. Specifically, if and exhibit perfect negative correlation, then the firm exhibits similar characterizations of the threshold inventory level for the on-site market.

Theorem 6

If and perfect negative correlated, then there exists a satisfying that and

| (20) |

4.3.4 The Case in which Price is Constrained to be Equal in Both Markets

In this section, examine the case where the two markets must charge the same price in each period as it is a policy many ‘clicks and mortar’ retailers adopt. In this case the demand functions are specified by: and . For period , the optimization is written as follows:

| (21) |

where

| (22) | |||||

Let as the maximizer.

Lemma 6

decreases in .

Lemma 6 proves the intuitive result that a retailer will decrease price in response to inventory level increases. Denote . When the inventory level is lower than , the retailer will stop sales in both markets and hence, a threshold policy can be established. Furthermore, we prove the following:

Theorem 7

Theorem 7 places bounds on the threshold policy when a single price is used in both markets. Interestingly, the retailer will open both markets at an inventory level in between the threshold inventory levels of the two markets in the previous price setting. For example, sales will commence at an inventory level where the retailer in a heterogeneous price setting opens only one market. Likewise, inventory levels where a retailer with greater pricing flexibility would close both markets will also represent an inventory level where the price constrained firm has closed both markets.

When a firm does have the ability to price differently in each market, the results of Theorem 7 can be used to decrease the dimensionality of the retailer’s pricing decision. Insights, such as knowledge of , can provide a starting point for considering the market opening decision. Given and current inventory levels, the firm knows whether opening sales at both markets at the same price is optimal and hence, can use this information as a basis for considering which market should be opened earlier if able to charge different prices in the two markets.

Remark 4

a) We note that when the holding cost approaches zero, the difference between a postponed delivery and immediately shipping disappears. However, the analysis remains meaningful. We note that following interesting special cases.

Case 1. and (i.e., , then in Theorems 2 and 3 .

Case 2. , and (i.e., , then , and if one goes through the steps of the proof of Theorem 3 one can show that . Furthermore, in this case if we assume the conditions of Theorem 5 hold, i.e., , follow the same distribution, then and we have

Case 3. , and (i.e., , then , and if one goes through the steps of the proof of Theorem 3 one can show that . In addition, in this case if we assume the conditions of Theorem 5 hold, i.e., , follow the same distribution, then and we have

b) Backlogging is adopted as a reasonable simplifying assumption. We note that for the primary market in our model (as in reality) most of the time backlogging will be incurred only for items demanded in the secondary market . To see this consider the following realizations (examples), where we take and , , ; recall that

Example 1: , , . Then , i.e., no backlogged units at the end .

Example 2: , , . Then 2 units of the market are backlogged at the end of the 1st period and , i.e., unit of the market is backlogged at the end .

Example 3 (extreme and rare case): , , . Then 26 units (24 of the and 2 of the market) are backlogged at the end of the 1st period and , i.e., units (from period 1) are backlogged all the way to the end and 1 unit from period 2. Our computations confirm that for reasonable choices of the relevant costs, realizations described in Example 3 do not occur. However, allowing them does simplify the analysis of this challenging problem.

5 Discussion and Conclusion

In this paper, we investigated the structure of a retailer’s optimal selling strategies when the retailer is faced with two distinct sales markets and a common pool of replenishable inventory with which to satisfy demand. A summary of the core selling strategies derived in §4 is provided in Table 1. The optimal policies in this table indicate that both inventory and demand uncertainty are key issues in choosing which markets to open up for demand, i.e., choose a price for which the mean market demand is positive. Based on the type of demand uncertainty, it is shown that optimal policies are characterized by inventory level thresholds which determine whether which market will offer the product for sale and at what price.

The following managerial insight is provided. When demand uncertainty in both markets is additive and inventory is low, selling exclusively through the online market is preferred. As inventory increases beyond a specific threshold, the online market is also opened (offers the item for sale), and the optimal selling strategy is to increase demand intensity in both markets as increases further. However, the problem is more challenging when both markets have multiplicative demand uncertainty. In this case it is shown that the sales in one channel may actually decrease as the inventory level increases. Despite this, we show that the demand intensity in at least one of the markets does indeed increase as the inventory level increases. A key result is provided by the following property we establish in the multiplicative mean demand model case. In this case it is shown that optimal threshold policies can derived from benchmark problems where demand uncertainty in the current period can be ignored. Hence, if a retailer would sell through a particular market assuming no uncertainty in demand in the current period, then they should also open that market when multiplicative uncertainty exists.

| Type of Demand Certainty | ||

| on-site market | long-distance market | Optimal selling strategy |

| There exist an inventory level and a pair of mean demands . | ||

| additive | additive | If , then , and increasing in . |

| If , then and increases as increases. | ||

| There exist an inventory level and a pair of the mean demands . | ||

| additive | multiplicative | If , then , and increasing in . |

| If , then and increases as increases. | ||

| Optimal selling policy is a threshold policy. | ||

| multiplicative | additive | Optimal selling quantities at both on-site market and long-distance market increase as the inventory level increases. |

| Optimal selling policy is a threshold policy. | ||

| multiplicative | multiplicative | Optimal selling quantity at on-site market or long-distance market may increase or decrease as the inventory level increases. |

| Optimal selling quantity at at least one of on-site market and long-distance market increases as inventory level increases. | ||

For a retailer serving two markets from a common pool of inventory, the insights from this paper can be valuable. With limited inventory, the retailer will prefer to sell through only one market. In this limited inventory scenario, analyzing cases where the marginal profit in each market is equal reveals an often overlooked benefit of selling through the online channel; namely, gaining demand information is a truly valuable aspect of serving this market. Evidence of this was shown through characterization of cases where a firm prefers sales through the long-distance market despite the marginal profit of the on-site market being significantly larger.

In conclusion, this study contributes to the literature by providing the first model for a firm’s dual market dynamic pricing problem in the presence of exogenously determined inventory replenishment considerations. Our study of a finite horizon case is consistent with fashion products, whereas the infinite horizon case might provide tractable insight for functional products.

In current and future work, we plan to investigate the effect of relaxing some of our modeling assumptions. For instance, a retailer may choose not to handle online demand in a batch at the end of the period and exploration of flexibility in the long-distance market’s timing of demand satisfaction (e.g. satisfy in this period or the subsequent one) would provide meaningful results. Extensions treating the lost sales case and providing more thorough treatment of the correlation of the two market’s demands are also the subject of future research. Herein, we have provided conditions regarding the on-site market’s threshold inventory level for the case of perfectly (negatively or positively) correlated demands. In the general case, if the two markets demands are correlated, then the threshold structure of an optimal policy may not hold.

References

- [1] Agatz, N. A., Fleischmann, M., Van Nunen, J. A. 2008. E-fulfillment and multi-channel distribution - A review. European Journal of Operational Research, 187(2), 339-356.

- [2] Agrawal, V., and Seshadri, S. 2000. Impact of uncertainty and risk aversion on price and order quantity in the newsvendor problem. Manufacturing and Service Operations Management, 2(4):410–422.

- [3] Ann Taylor. Ann taylor, 2012. Annual report. http://investor.anninc.com/phoenix.zhtml?c=78167&p=irol-reportsannual, 2012.

- [4] Anupindi, R., and R. Akella. 1993. Diversification under supply uncertainty. Management Science, 39(8):944–963.

- [5] Araman V.F., and R. Caldentey. 2009. Dynamic pricing for nonperishable products with demand learning. Operations research, 57(5):1169–1188.

- [6] Arslan, H., Graves, S.C., and T. Roemer. 2007. A single-product inventory model for multiple demand classes. Management Science, 53(9):1486–1500.

- [7] Aviv, Y., and A. Federgruen. 2001. Capacitated multi-item inventory systems with random and seasonally fluctuating demands: Implications for postponement strategies. Management Science, 47(4):512–531.

- [8] Aviv, Y., and A. Federgruen. 2001. Design for postponement: A comprehensive characterization of its benefits under unknown demand distributions. Operations Research, 49(4):578–598.

- [9] Barankin, E.W. 1961. A delivery-lag inventory model with an emergency provision (the single-period case). Naval Research Logistics Quarterly, 8(3):285–311.

- [10] Bensinger, G. 2014. Spreading Black Friday fever to China’s shoppers. http://www.wsj.com/articles/spreading-black-friday-fever-to-chinas-shoppers-1416954943, 2014. Accessed: 2014-12-11, Nov. 25.

- [11] Bernstein, F., and Federgruen, A. 2004. A general equilibrium model for industries with price and service competition. Operations Research, 52(6):868–886.

- [12] Bernstein, F., and Federgruen, A. 2007. Coordination mechanisms for supply chains under price and service competition. Manufacturing and Service Operations Management, 9(3):242–262.

- [13] Bitran, G., and R. Caldentey, R. 2003. Commissioned paper: An overview of pricing models for revenue management. Manufacturing & Service Operations Management, 5(3):203–229.

- [14] Bitran, G., Caldentey, R., and S. Mondschein. 1998. Coordinating clearance markdown sales of seasonal products in retail chains. Operations research, 46(5):609–624.

- [15] Bomberowitz, J. 2012. Ship from store: What retailers can learn from the early adopters. http://connected.retailnetgroup.com/index.php/2012/09/24/ship-from-store-what-retailers-can-learn-from-the-early-adopters/.

- [16] Brynjolfsson, E., Hu, Y., and M. S. Rahman. 2009. Battle of the retail channels: How product selection and geography drive cross-channel competition. Management Science, 55(11):1755–1765.

- [17] Brynjolfsson, E., Hu, Y., and M. D. Smith. 2003. Consumer surplus in the digital economy: Estimating the value of increased product variety at online booksellers. Management Science, 49(11):1580–1596.

- [18] Brynjolfsson E., and M. D. Smith. 2009. Battle of the retail channels: How product selection and geography drive cross-channel competition. Management Science, 46(4):563–585.

- [19] Butler, E. 2005. Orchestrating sept. 11 comeback: J&r music finally regains lost sales with online focus, new product mix. Crain’s New York Business, Jan. 17.

- [20] Campbell, D., and Frei, F. 2010. Cost structure, customer profitability, and retention implications of self-service distribution channels: Evidence from customer behavior in an online banking channel. Management Science, 56(1):4–24.

- [21] Chen, F. 2001. Market segmentation, advanced demand information, and supply chain performance. Manufacturing and Service Operations Management, 3(1):53–67.

- [22] Chen, K.Y., Kaya, M., and O. Ozer. 2008. Dual sales channel management with service competition. Manufacturing and Service Operations Management, 10(4):654–675.

- [23] Chen, W. Feng, Q., and S. Seshadri. 2013. Sourcing from suppliers with random yield for price-dependent demand. Annals of Operations Research, 208(1):557–579.

- [24] Chen, X., and Simchi-Levi, D. 2004. Coordinating inventory control and pricing strategies with random demand and fixed ordering cost: The finite horizon case. Operations Research, 52(6):887–896.

- [25] Chen, X., and Simchi-Levi, D. 2004. Coordinating inventory control and pricing strategies with random demand and fixed ordering cost: the infinite horizon case. Mathematics of Operations Research, 29(3):698–723.

- [26] Chen, X., and Simchi-Levi, D. 2006. Coordinating inventory control and pricing strategies with random demand and fixed ordering cost: the continuous review model. Operations Research Letters, 34:323–332.

- [27] Cohen, M.A. 1977. Joint pricing and ordering policy for exponentially decaying inventory with known demand. Naval Research Logistics Quarterly, 24(2):257–268.

- [28] Datta, T.K., and P. Karabi. 2001 An inventory system with stock-dependent, price-sensitive demand rate. Production planning & control, 12(1):13–20.

- [29] Dave, U., and Y.K. Shah. 1982. A probabilistic inventory model for deteriorating items with lead time equal to one scheduling period. European Journal of Operational Research, 9(3):281–285.

- [30] Dong, L., Kouvelis, P., and Z. Tian. 2009. Dynamic pricing and inventory control of substitute products. Manufacturing & Service Operations Management, 11(2):317–339.

- [31] Elmaghraby, W., and P. Keskinocak. 2003. Dynamic pricing in the presence of inventory considerations: Research overview, current practices, and future directions. Management Science, pages 1287–1309.

- [32] Federgruen, A., and A. Heching. 1999. Combined pricing and inventory control under uncertainty. Operations Research, pages 454–475.

- [33] Federgruen, A., and A. Heching. 2002. Multilocation combined pricing and inventory control. Manufacturing & Service Operations Management, 4(4):275–295.

- [34] Federgruen, A., and N. Yang. 2011. Procurement strategies with unreliable suppliers. Operations Research, 59(4):1033–1039.

- [35] Feng, Y., and B. Xiao. 2000. A continuous-time yield management model with multiple prices and reversible price changes. Management Science, 46(5): 644–657.

- [36] Forman, C. Ghose, A., and A. Goldfarb. 2009. Competition between local and electronic markets: How the benefit of buying online depends on where you live. Management Science, 55:47–57.

- [37] Fukuda, Y. 1964. Optimal policies for the inventory problem with negotiable leadtime. Management Science, pages 690–708.

- [38] Gallego, G., and G. J. van Ryzin. 1994. Optimal dynamic pricing of inventories with stochastic demand over finite horizons. Management Science, 40(8):999–1020.

- [39] Heching, A., Gallego, G., and van Ryzin G. 2002. Mark-down pricing: An empirical analysis of policies and revenue potential at one apparel retailer. Journal of Revenue and Pricing Management, 1(2): 139–160.

- [40] Heyman, D. P., and M. J. Sobel. 1984. Stochastic Models in Operations Research, Vol. II. McGraw-Hill, New York.

- [41] Huang, W., and J. M. Swaminathan. 2009. Introduction of a second channel: Implications for pricing and profits. European Journal of Operational Research, 194(1):258–279.

- [42] Pelton. L. E., Pentina, I., and R. W. Hasty. 2009. Performance implications of online entry timing by store-based retailers: A longitudinal investigation. Journal of Retailing, 85(2):177–193.

- [43] Karlin, S., and H. Scarf. 1958. Inventory models of the arrow-harris-marschak type with time lag. Studies in the mathematical theory of inventory and production, pages 155–178.

- [44] Katehakis, M.N. and L.C. Smit. 2012. On computing optimal (q, r) replenishment policies under quantity discounts. Annals of Operations Research 200(1) 279–298.

- [45] Kazaz, B. 2004. Production planning under yield and demand uncertainty with yield-dependent cost and price. Manufacturing and Service Operations Management, 6(3):209–224.

- [46] Khermouch, G. 2012. Retailer of the year. Beverage Dynamics. January/February, available at www.garyswine.com/retailer_year.pdf.

- [47] Levin Y., McGill, J., and M. Nediak. 2008. Risk in revenue management and dynamic pricing. Operations Research, 56(2):326.

- [48] Li, L. 1992. The role of inventory in delivery-time competition. Management Science, 38(2):182–197.

- [49] Li, Q., and S. Zheng. 2006. Joint inventory replenishment and pricing control for systems with uncertain yield and demand. Operations Research, 54:696–705.

- [50] Monahan, G.E, Petruzzi, N.C., and W. Zhao. 2004. The dynamic pricing problem from a newsvendor’s perspective. Manufacturing and Service Operations Management, 6(1):73–91.

- [51] Pang, Z. Chen, F.Y., and Y. Feng. 2012. Technical note—a note on the structure of joint inventory-pricing control with leadtimes. Operations Research, 60(3):581–587.

- [52] Petruzzi, N.C., and M. Dada. 1999. Pricing and the newsvendor problem: A review with extensions. Operations Research, 47(2):183–194.

- [53] Shi, J., Katehakis, M.N., and B. Melamed. 2013. Martingale methods for pricing inventory penalties under continuous replenishment and compound renewal demands. In M.N. Katehakis, S.M. Ross, and J. Yang, editors, Cyrus Derman Memorial Volume I: Optimization under Uncertainty: Costs, Risks and Revenues, volume 208, pages 593–612. Annals of Operations Research, Springer, New York.

- [54] Shi, J., Katehakis, M.N., Melamed, B., and Y. Xia. 2014. Production-inventory systems with lost sales and compound poisson demands. Operations Research, 6(5):1048 – 1063.

- [55] Simchi-Levi, D., Bramel, J., and X. Chen. 2005. The logic of logistics: theory, algorithms, and applications for logistics and supply chain management. Springer Verlag.

- [56] Smith, S. A., and D. D. Achabal. 1998. Clearance pricing and inventory policies for retail chains. Management Science, 44(3):285–300.

- [57] Song, Y., Ray, S., and T. Boyaci. 2009. Technical note—optimal dynamic joint inventory-pricing control for multiplicative demand with fixed order costs and lost sales. Operations Research, 57(1):245–250.

- [58] Spencer S. 2015. China Shops Alibaba for U.S. Goods From Toothbrushes to Nuts Bloomberg Business April 21, 2015 http://www.bloomberg.com/news/articles/2015-04-22/china-shops-alibaba-for-u-s-goods-from-toothbrushes-to-nuts

- [59] Stevens, L. 2013. Retailers turn store clerks into web shippers. http://www.wsj.com/articles/SB10001424052702303332904579228602337333952, Dec. 9 .

- [60] Talluri, K.T., and G. Van Ryzin. 2005. The theory and practice of revenue management, volume 68. Springer Verlag.

- [61] Thomas, L.J. 1974. Technical Note?Price and Production Decisions with Random Demand. Operations Research 22(3):513-518.

- [62] Tong F. 2014. China’s big online marketplaces will ship to overseas Chinese. www.internetretailer.com/2013/07/26/chinas-big-online-marketplaces-will-ship-overseas-chinese.

- [63] Topaloglu, H., Birbil, S.I. Frenk, J.B.G., and N. Noyan. 2012. Tractable open loop policies for joint overbooking and capacity control over a single flight leg with multiple fare classes. Transportation Science, 46(4):460–481.

- [64] Topkis, D. M. 1998. Supermodularity and Complementarity. Princeton University Press, Princeton NJ.

- [65] Veinott A.F. Jr . 1966. The status of mathematical inventory theory. Management Science, 12(1): 745–777.

- [66] Wang, H., and H. Yan. 2009. Inventory management for customers with alternative lead times. Production and Operations Management, 18(6):705–720.

- [67] Wright, G.P. 1968. Optimal policies for a multi-product inventory system with negotiable lead times. Naval Research Logistics Quarterly, 15(3):375–401.

- [68] Xu, N.. 2005. Multi-period dynamic supply contracts with cancellation. Computers and Operations Research, 32(12):3129–3142.

- [69] Yang, B., and Geunes, J. 2007. Inventory and lead time planning with lead-time-sensitive demand. IIE Transactions, 39(5):439–452.

- [70] Yin, R., and K. Rajaram. 2007. Joint pricing and inventory control with a markovian demand model. European Journal of Operational Research, 182(1):113 – 126.

- [71] You, P. S. 1999. Dynamic pricing in airline seat management for flights with multiple legs. Transportation Science, 34(2):192–206.

- [72] Yunchuan, L., Gupta, S., and Z. J. Zhang. 2006. Note on self-restraint as an online entry-deterrence strategy. Management Science, 52(11):1799–1809.

- [73] Zhang, J., Farris, P.W., Irvin, J.W., Kushwaha, T., Steenburgh, T., and B. A. Weitz. 2010. Crafting integrated multichannel retailing strategies. Journal of Interactive Marketing, 24(2):168–180.

- [74] Zhao W., and Y.-S. Zheng. 2000. Optimal dynamic pricing for perishable assets with nonhomogeneous demand. Management Science, 46(3):375–388.

Appendix A Appendix: Proofs

In this section we will use the following simplified definition of supermodularity (i.e., “increasing differences”) of a real function on given in Definition A.1 below. A comprehensive exposition of the topic of supermodularity and its application in sequential decision problems is given in [64].

Definition A.1

A real function is supermodular in if

for all and .

If the inequality above is reversed, the function is called submodular.

Lemma A.1 below summarizes properties of supermodular functions that we will use, we refer the reader to [64] (Theorem 2.6.2) and [55] for proofs.

Lemma A.1

(Topkis 1998)

-

1.

If is concave, then

is submodular in and

is supermodular in .

-

2.

If is supermodular (submodular) in and

then is increasing (decreasing) in .

Proof of Lemma 1. We first clarify the existence of optimality. The existence of the optimality follows from the continuity of the value function and boundary condition of . Denote . First, we have Also, The proof is easy to complete using induction and Eq. (3).

Second, we will show that is concave in . From the terminal condition that for all , it is clear is concave. If we assume is concave, then because the linear combination of two concave functions is concave, we have that is concave in . Given that concavity is preserved under maximization [40], we obtain that is concave. The second statement of Lemma 1 also follows by induction. The last statement follows from the concavity of , , and and Lemma A.1.

Proof of Lemma 2. We only need to show that if and then . We can write

as

Because and are concave, is supermodular in and submodular in . Now, from Lemma A.1, we have increases in and decreases in . Hence, from and , we can obtain .

Proof of Theorem 1. To see part , from (3) and (4), we first have that

| (23) |

| where | (24) |

Because is concave and concavity is preserved under maximization, is concave. We can show that the right side of Eq. (23) is supermodular in . The first term depends only on and it is clearly submodular in . The supermodularity of the second and the third terms follows from the concavity of , and linear combination of Therefore, from from Lemman A.1 we have increases in

To see part ii), we denote and . From (3), we have

| (25) |

Following a similar argument as in the proof of part , we can show that increases in

To establish part iii), we note that the right side of Eq. (24) is supermodular in . The first term depends only on and it is clearly supermodular in . The supermodularity of the second term follows from the concavity of and linear combination of . Therefore, we have is increasing in . Combining this with the result of part , we have that increases in .

Proof of Remark 1. At time consider two forthcoming order quantities , with and let , and denote the optimal profit, objective function and optimal selling price corresponding to the forthcoming order quantities , . From Eq. (4) it follows that for all and . Now using Lemma 1, we obtain: for .

Proof of Lemma 3. To prove part i), we use the first order partial derivatives. From the supermodularity of in , we have increases in if . For the case in which , we will show that . Because and is a random variable with a continuous distribution, almost everywhere, we only need to focus on the interval where and exist and we note that almost everywhere.

From the first order partial derivatives, we have that when and ,

and with almost everywhere, we have

To simplify the notation, denote

From the strict concavity of and and the concavity of and , we have

| (28) |

We can rewrite (LABEL:eqn_eqn_lm_BL_BS_Monotone_q04) and (LABEL:eqn_eqn_lm_BL_BS_Monotone_q05) as follows.

From above two equations, we have

| (29) |

From the Cauchy-Schwarz inequality, we have

| (30) |

Combining this result with Ineqs. (28), we have:

and

The above together with Eq. (29), imply that . That is to say, .

To see Part (ii), we rewrite objective function as follows

where

First, we have is concave in . Hence, is supermodular in . Further,

is supermodular in . Therefore, is increasing in .

Proof of Lemma 4. First, we show that if then . For all , , we have

| (31) |

The inequality follows from the concavity of and Jensen’s inequality.

If , we can obtain that

| (32) |

The first inequality follows from the optimality of . The second inequality follows from Ineq. (31). Notice that we always pick up the the maximizer with the smallest . Therefore, we have from (32).

Below, we will show that if , then and prove the statement by contradiction. Suppose and . From , we can find and a positive number satisfying the conditions that and for all . We still notice that

| (33) |

| (34) |

Hence, we have

| (35) |

In the above three cases, we can get . However, from Lemma 3, we have and thus, have a contradiction. Therefore, we reach if and only if .

To see part (ii), we can get that if and only if by similar argument as the part (i).

Proof of Theorem 2. From Lemmas 3 and 4, there exist satisfying that , if and if . Follow the same logic, we have there exist satisfying that , if and if .

From the envelop theorem and (5), we also have that when ,

Hence, .

Proof of Lemma 5. From , we have

| (36) |

From the first order partial derivatives and Theorem 2, we also have

| (37) | |||||

Proof of Theorem 4. The first statement follows directly from Theorem 3 and thus, we focus on proving the second statement. Instead of proving the second statement directly, we will use mathematic induction to prove that if , then for all ,

| (38) |

First, we will show that relations (38) are true at .

For all and , we have

The inequality follows from . Hence, for all .

For every , we have that . Hence for all . Therefore and .

Combining the above with the condition, , we have , i.e., . Hence, we can find a satisfying the following:

From the concavity of , we have that for any realization

If , then . Taking the expectations of both sides of the above inequality, we have

| (39) |

Hence, . It is to say , .

Next we will show that by contradiction. Suppose , then

Hence, which contradicts our assumption and therefore . We still have that

The first inequality follows from and the concavity of .

Assume . We will show that and . From , we will have . Hence, we can find a satisfying the inequality below

Note that for any realization with , we have:

| (40) |

In addition, for any realization the following inequality holds.

| (41) |

Inequality (41), is due to the the concavity of , which implies:

Hence, , i.e.,

We next show that by contradiction. Suppose , Then

Hence, which contradicts our assumption. Hence, we have . We still have that

The first inequality follows from and the concavity of . Hence, we obtain (38). The proof is now complete.

Proof of Theorem 5. We need to consider the following three cases:

a) when .

b) when .

c) when .

a) We prove case a) by contradiction. Suppose . If , then we can find satisfying that

| (43) |

From the concavity of and , we have

That is to say,

| (44) |

Meanwhile, from the concavity of and , we have

| (45) | |||||

Together with Ineqs. (43) and (44), we have

which contradicts with the optimality of .

b) The proof of case b) is also by contradiction. Suppose . If , then we can find satisfying that

| (46) |

From the concavity of and , we have

That is to say,

| (47) |

Meanwhile, from the concavity of and , we have:

| (48) | |||||

Together with (46) and (47), we have

and this also leads to a contradiction with the optimality of .

c) To prove case c), we simply point to the continuity of and the results of cases a) and b).

Proof of Proposition 1. When , we have for every realization

| (49) |

Hence, we have

The second inequality follows from Jensen’s inequality. The second inequality follows from ( 49).

Proof of Proposition 2. If , then from the first order partial derivatives we have: Notice that

Notice that if and are perfect positive correlated, then from the concavity of we have

If and are perfect negative correlated, then from the concavity of we have

Therefore if and perfect positive correlated and if and perfect negative correlated

Follow the similar logic, we can obtain the statement is true when . We conclude the proof.

Proof of Lemma 6. From the concavity of and the linear combination form of the demand functions, we have is submodular in . Hence, decreases in

Taking first order partial derivatives of with respect of ,

To compare , and , we discuss two cases: (i) ; (ii) .

To see (i), we need to prove that . According to first order partial derivatives of with respect to and .

Hence, and . From the decreasing proposition of , we have .

Following a similar argument, this result is also true for Case (ii) and we conclude the proof.