1. Introduction

Let be a random variable defined on a probability space and let be its distribution function with endpoint

|

|

|

and let its survival function.

Throughout the paper we suppose that . The mean

excess function of is defined by (see, e.g., Kotz and Shanbhag

[6], Hall and Wellner [5], Guess and Proschan [4])

| (1.1) |

|

|

|

A natural way to estimate the mean excess function is achieved by using the plug-in method, that is replacing the survival function in (1.1) by its empirical counterpart, as did Yang [3].

Now consider a sequence of independent copies of

. The plug-in estimator of , for , is

| (1.2) |

|

|

|

where if and otherwise.

For notation convenience, we denote

|

|

|

and

|

|

|

where and is the probability law of .

We also denote by the empirical measure associated with the sample . We have

|

|

|

Formulae (1.1) and (1.2) lead to

|

|

|

and

|

|

|

where .

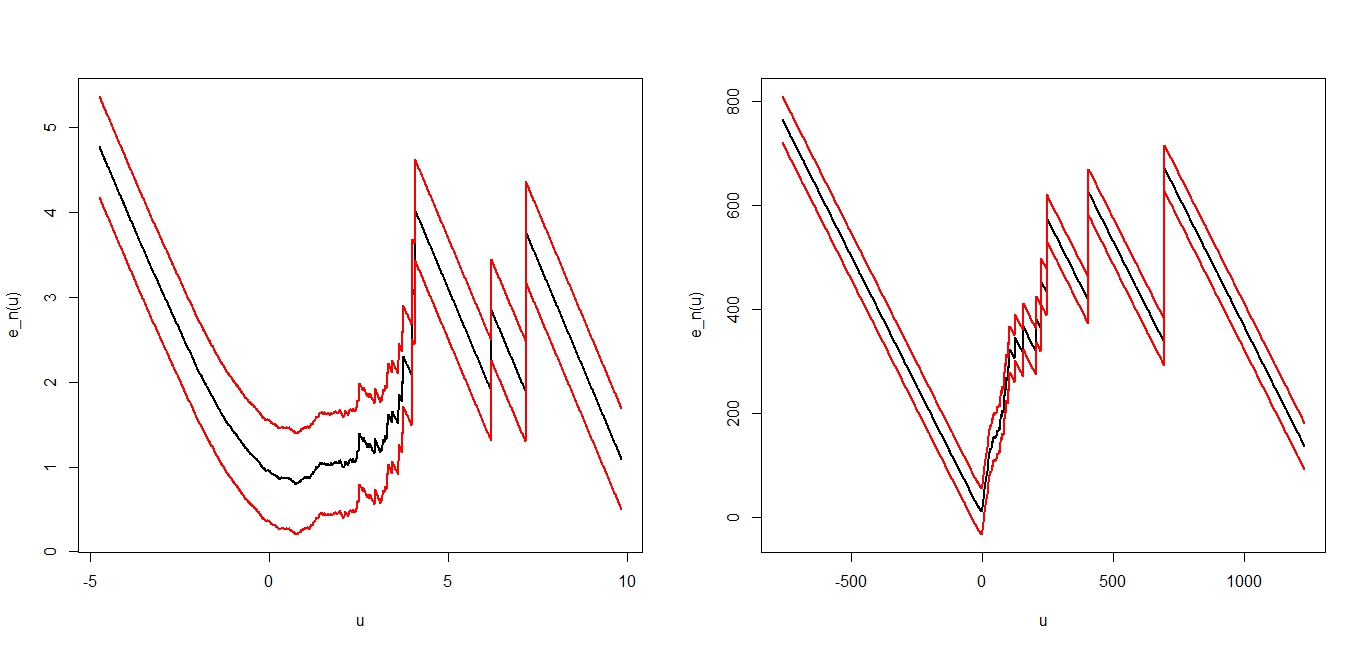

One of the most important motivation of the study of the mean excess

function comes from extreme value theory (EVT). Indeed this function is linear in the threshold when is a Generalized Pareto distribution and this is quite a powerful graphical test for such distributions.

By using the Vapnik-Chervonenkis (VC) classes and the entropy numbers technics, we have been able to establish that the empirical mean excess function converges almost surely and uniformly. We showed that for any less than the upper endpoint of the distribution ,

|

|

|

Next, by using the modern theory of functional empirical process mainly exposed in [10], we proved that the empirical mean excess function also weakly converges, that is

|

|

|

where is a Gaussian process and is a function family to be both precised later.

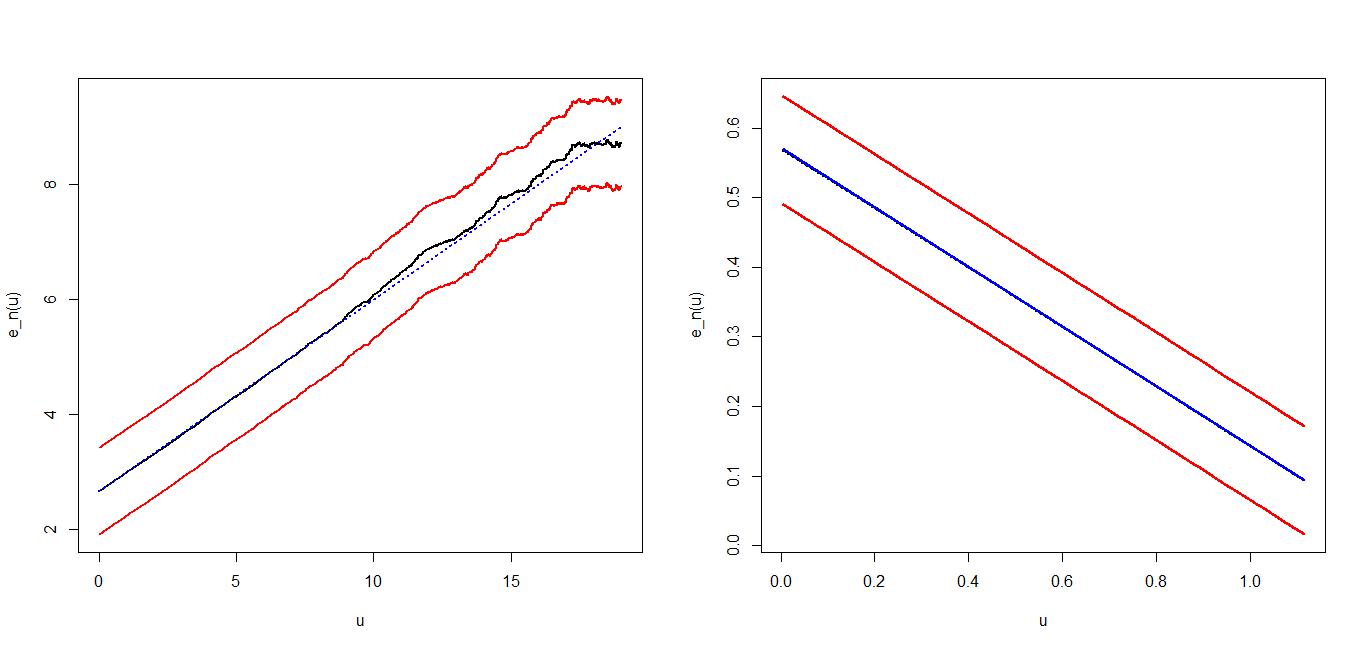

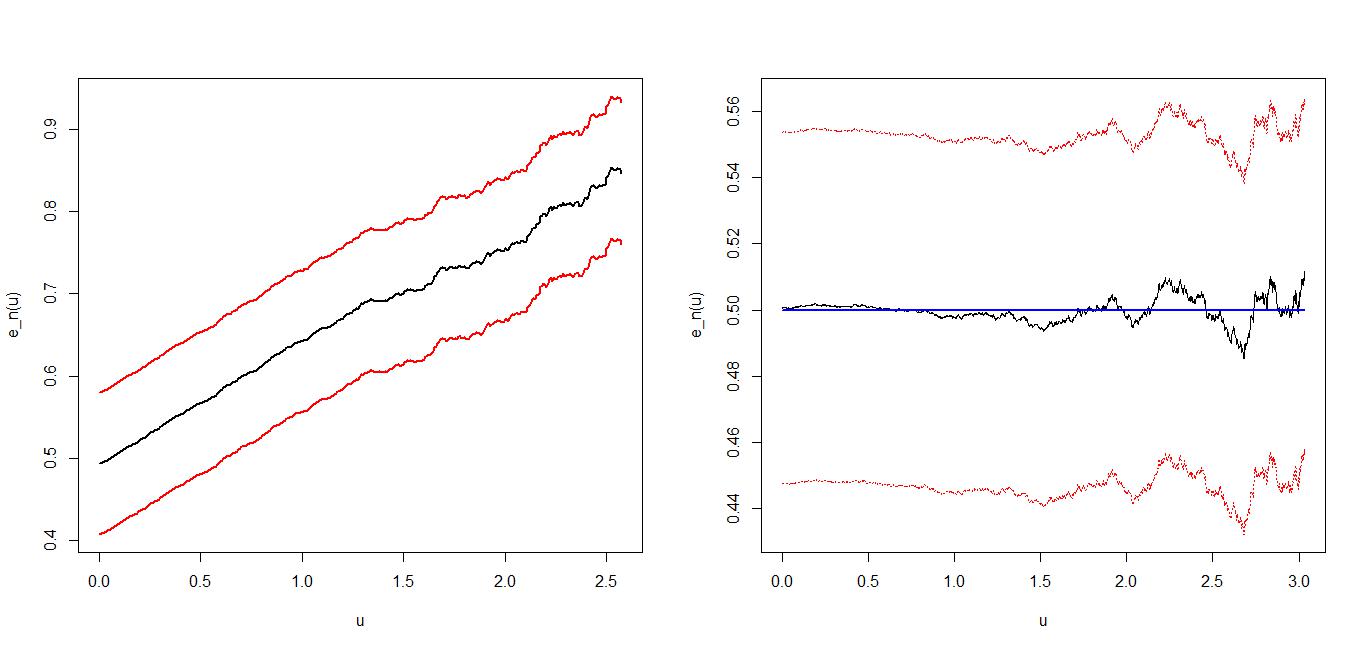

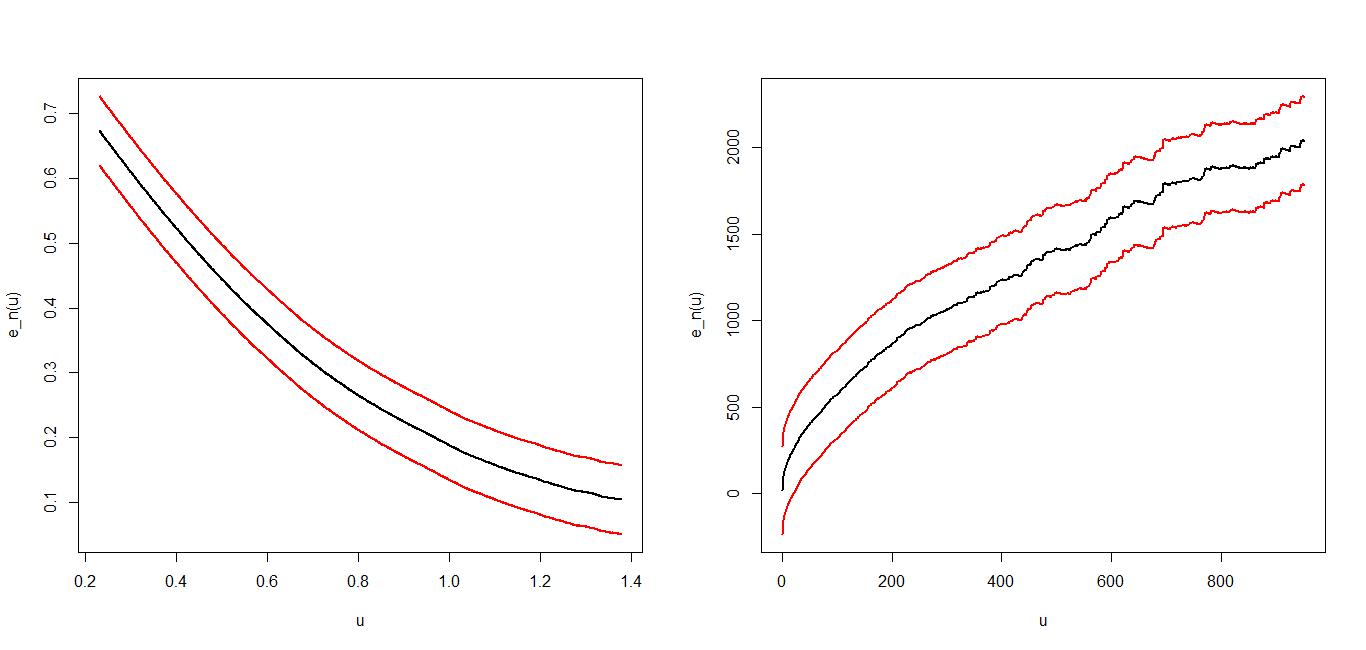

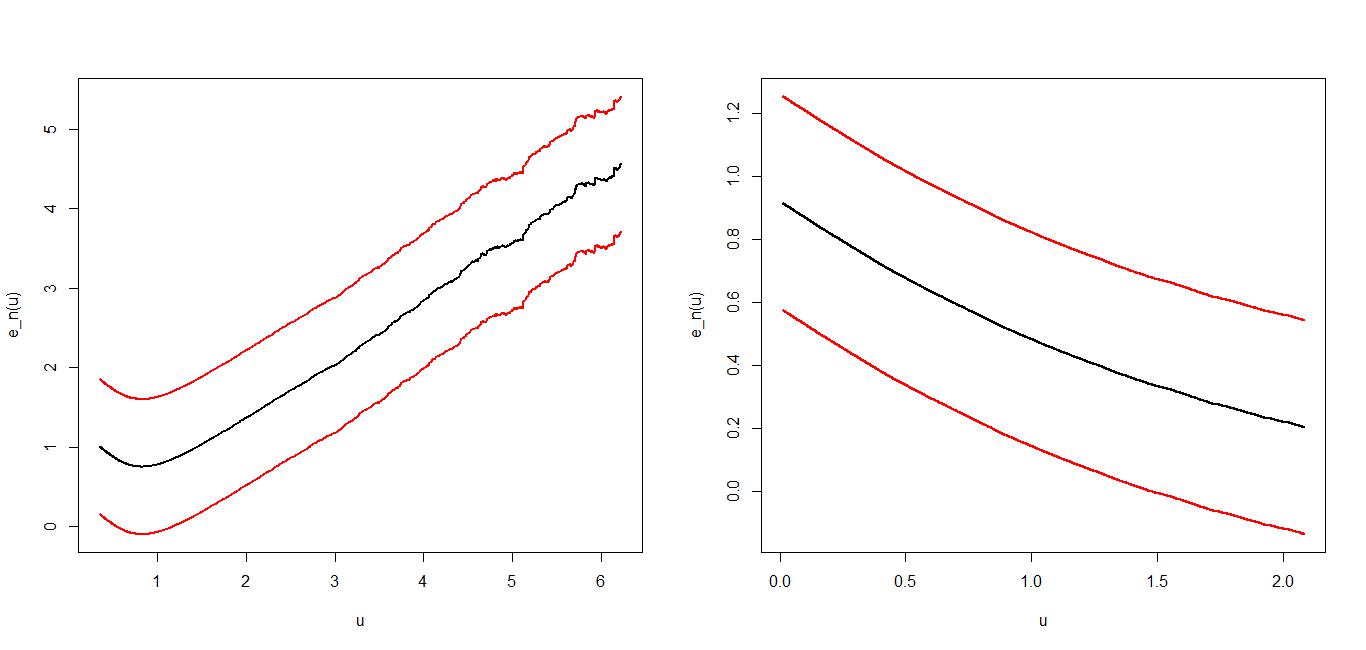

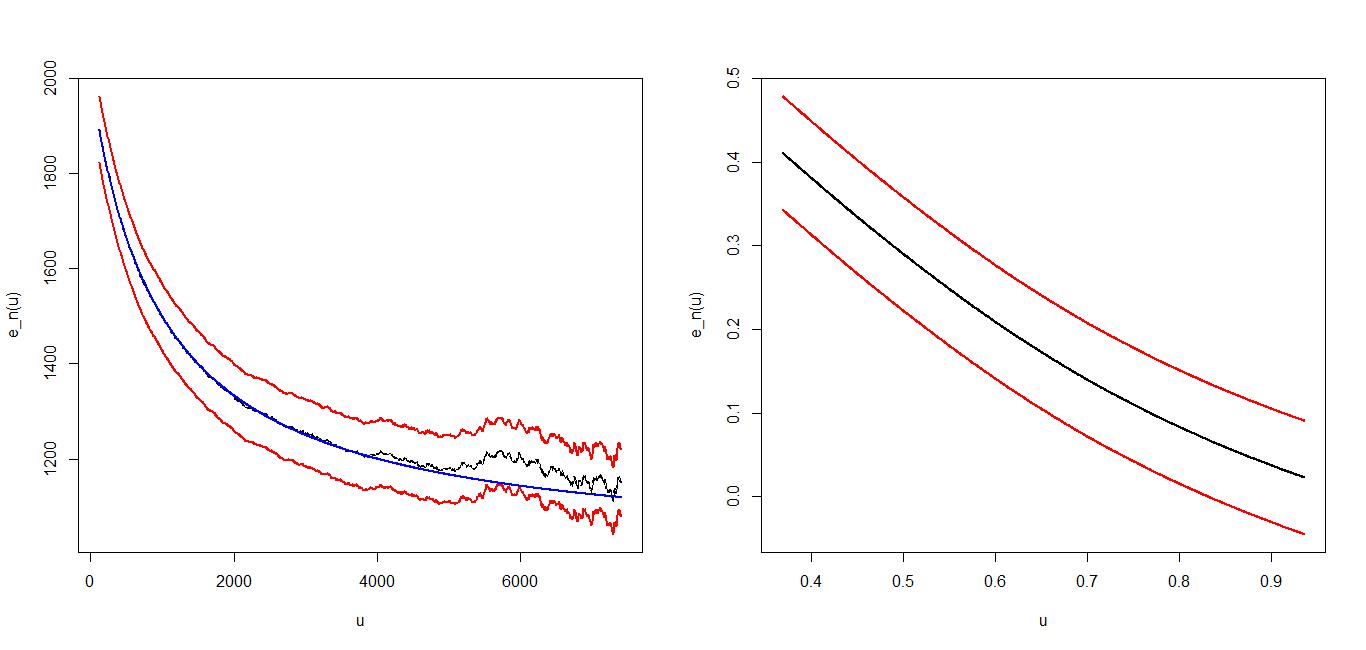

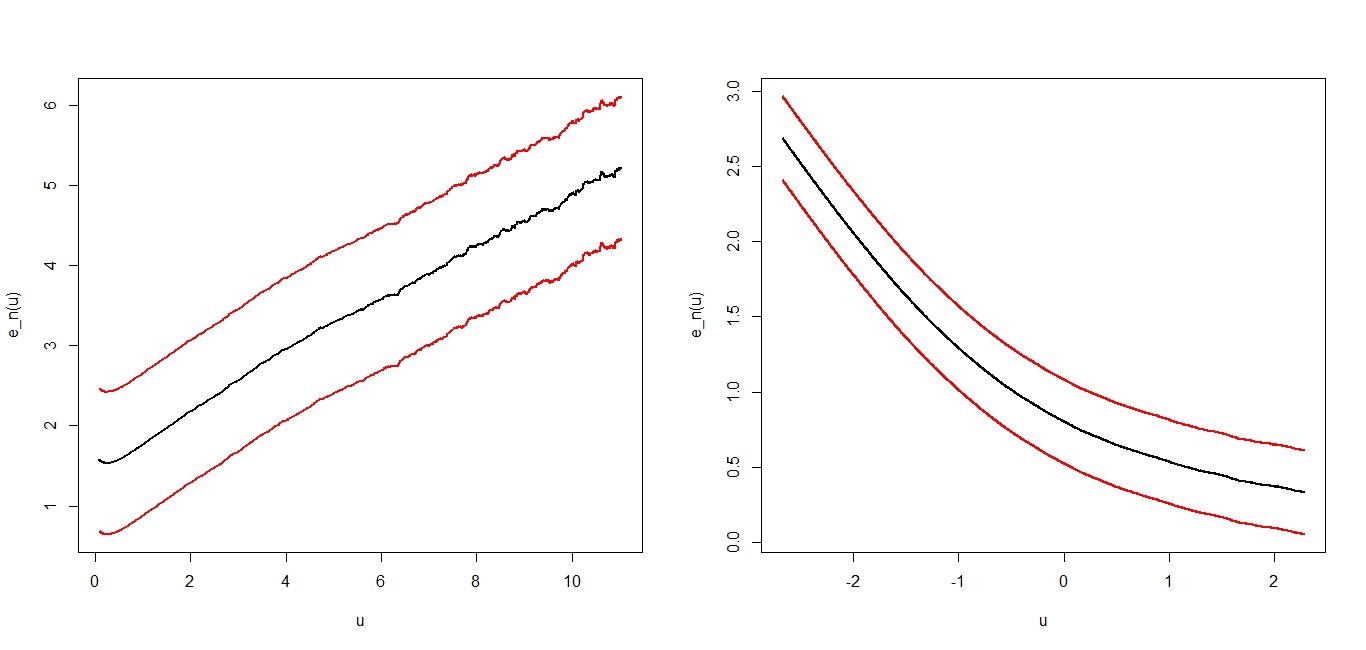

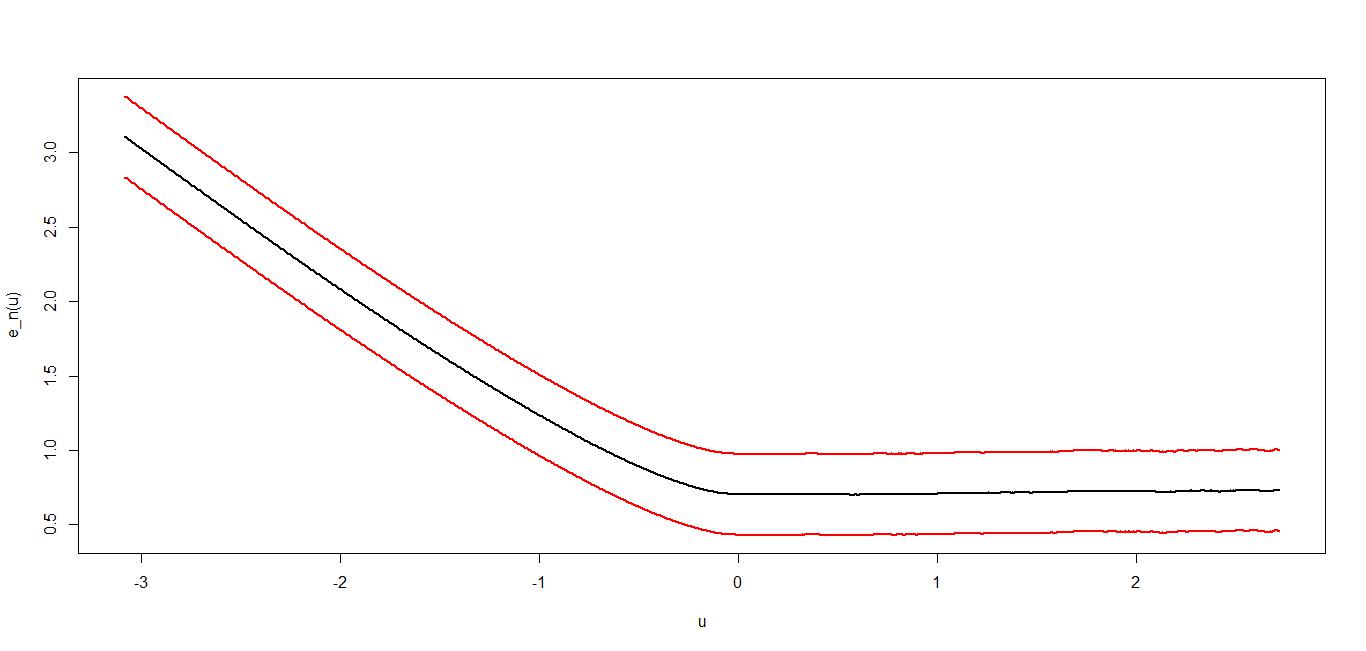

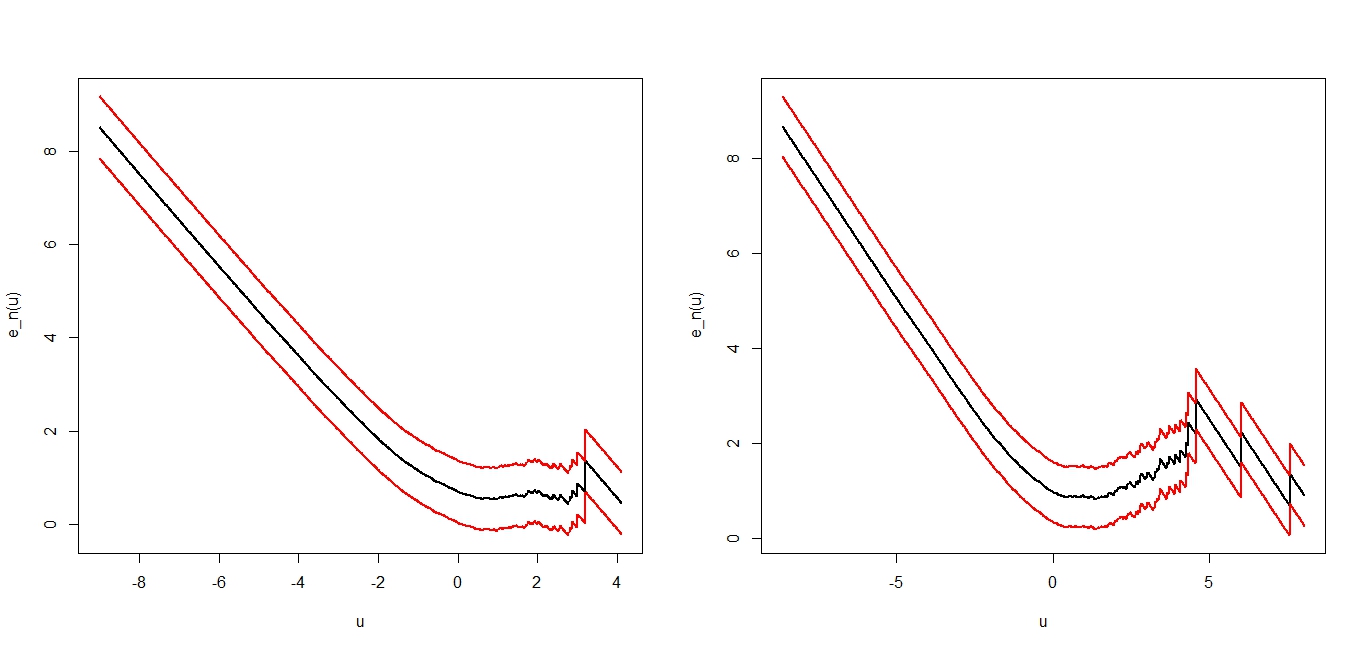

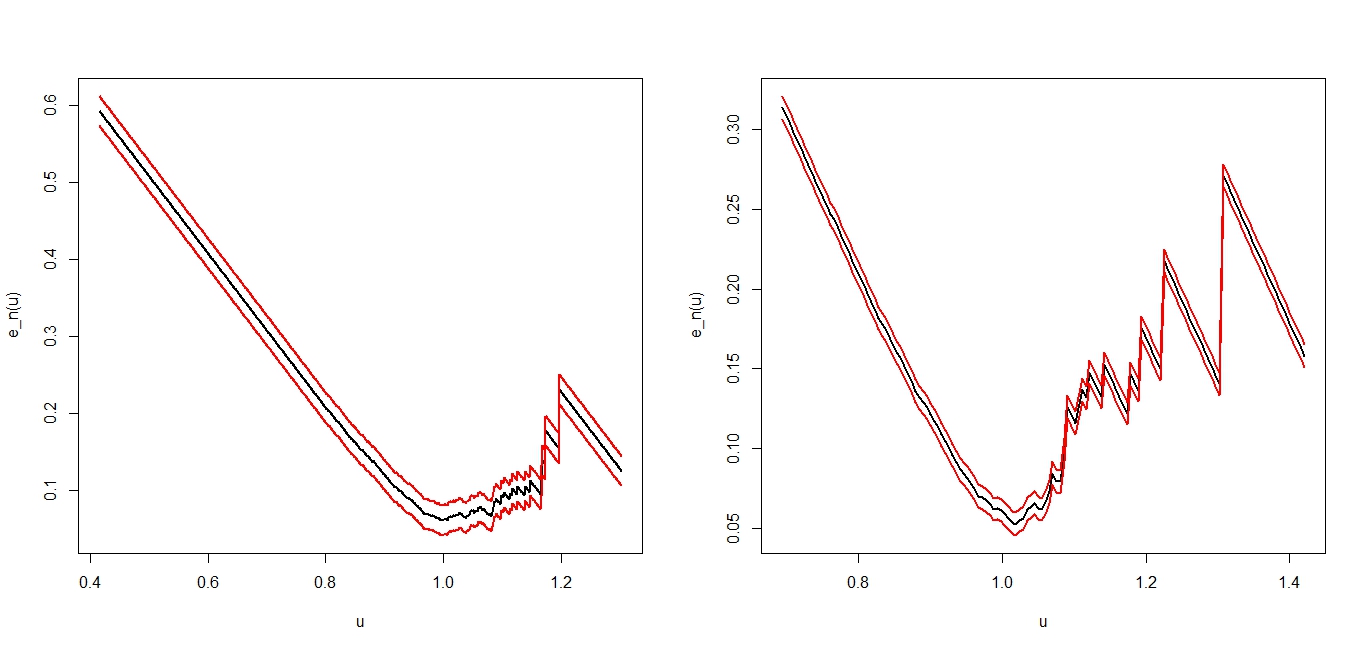

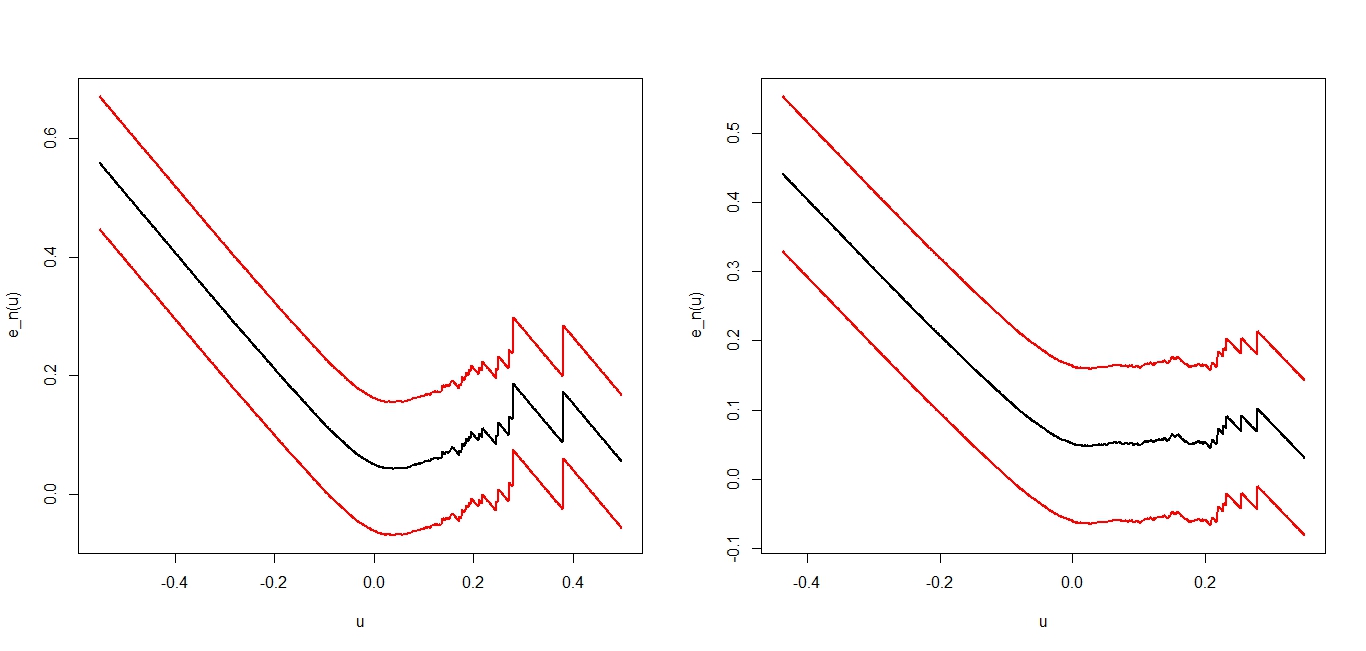

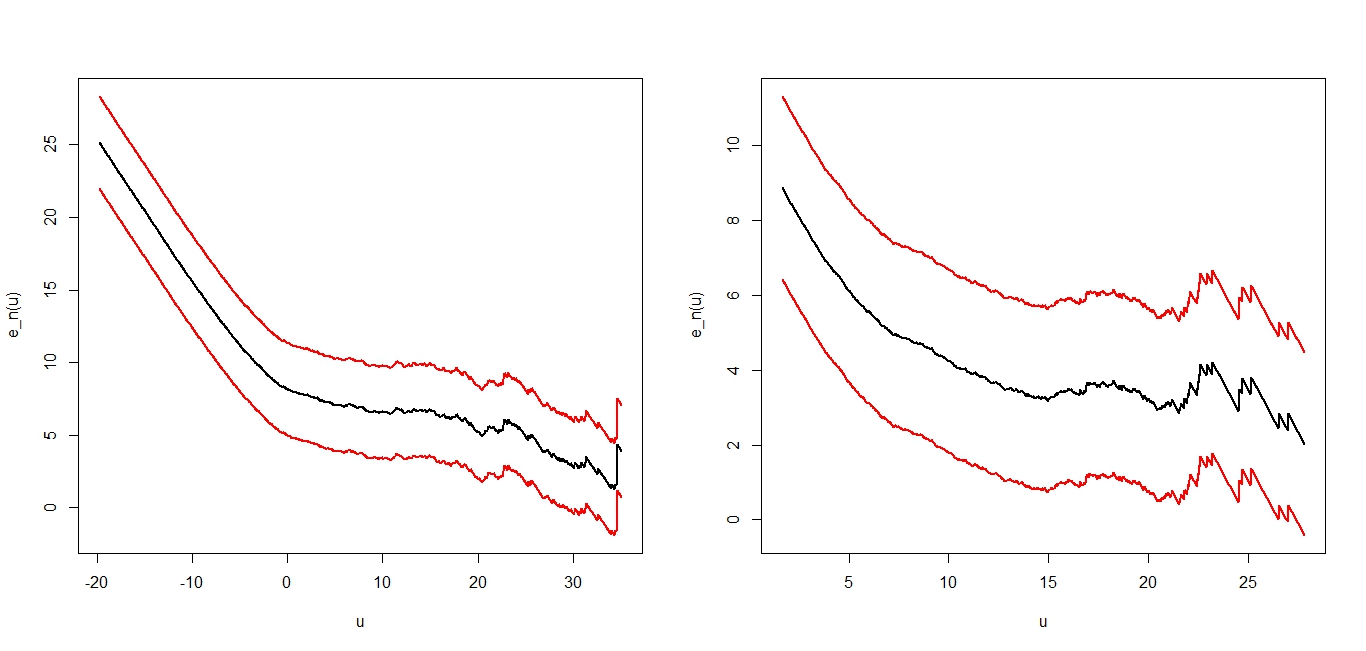

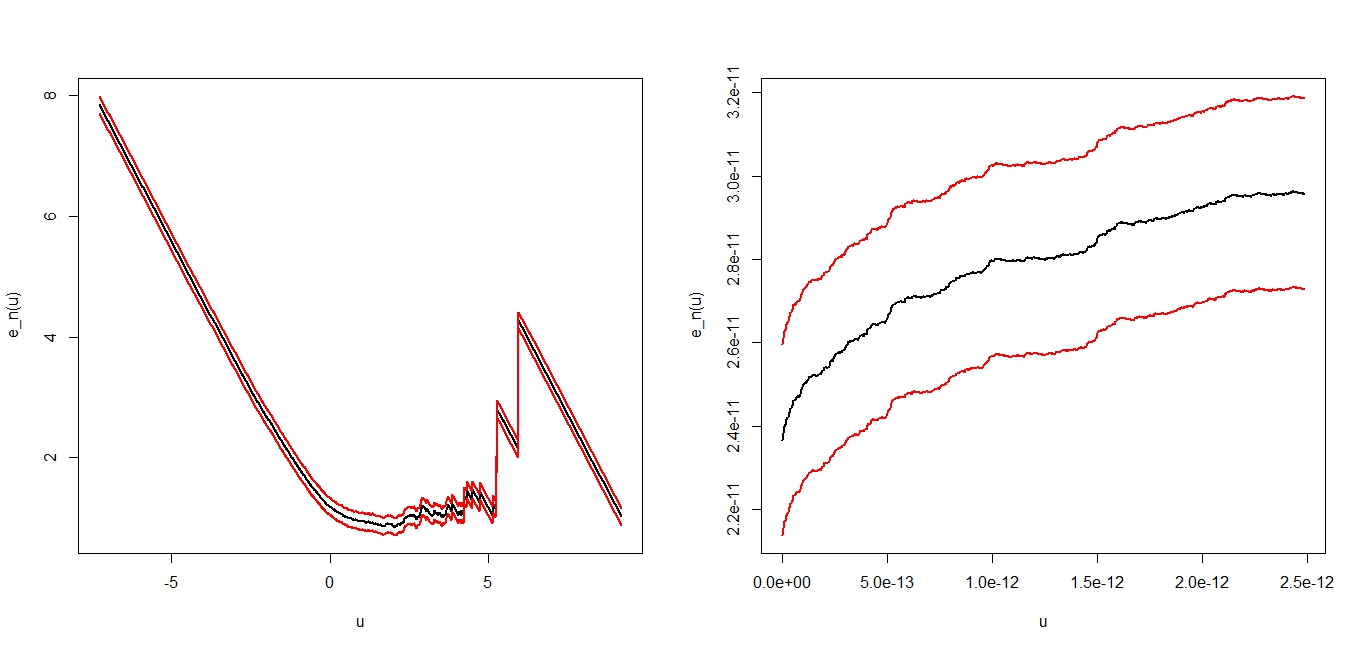

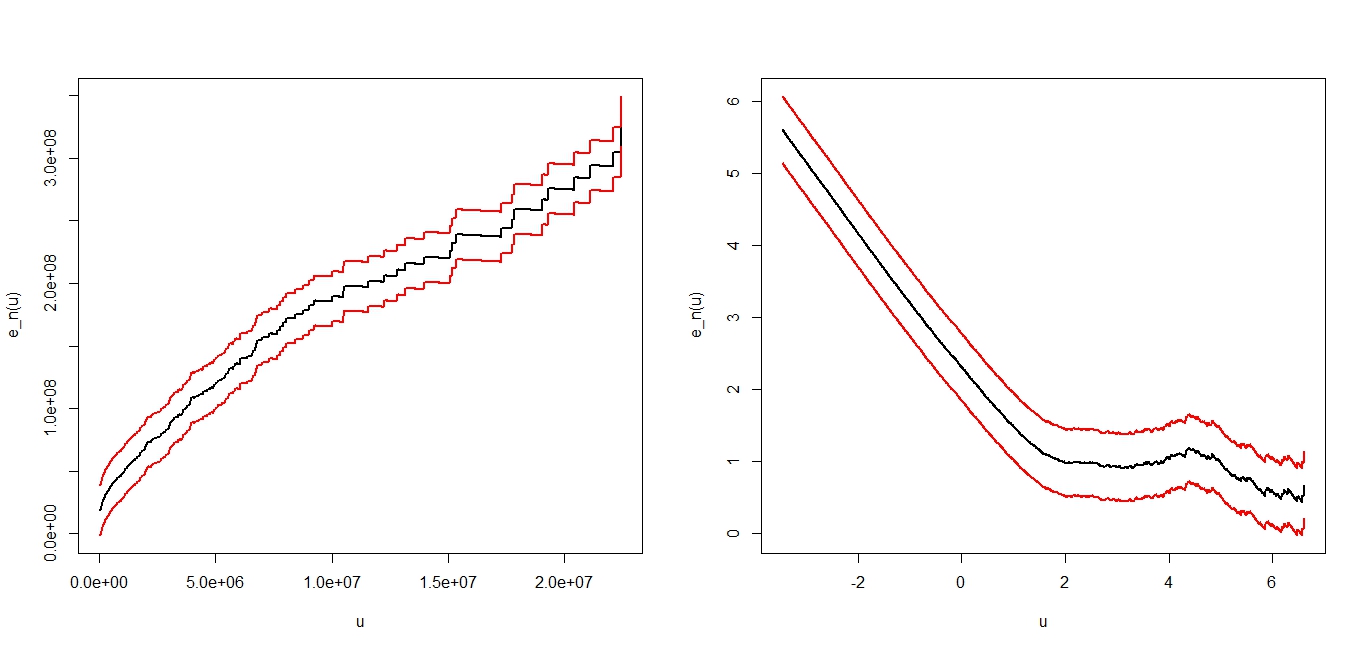

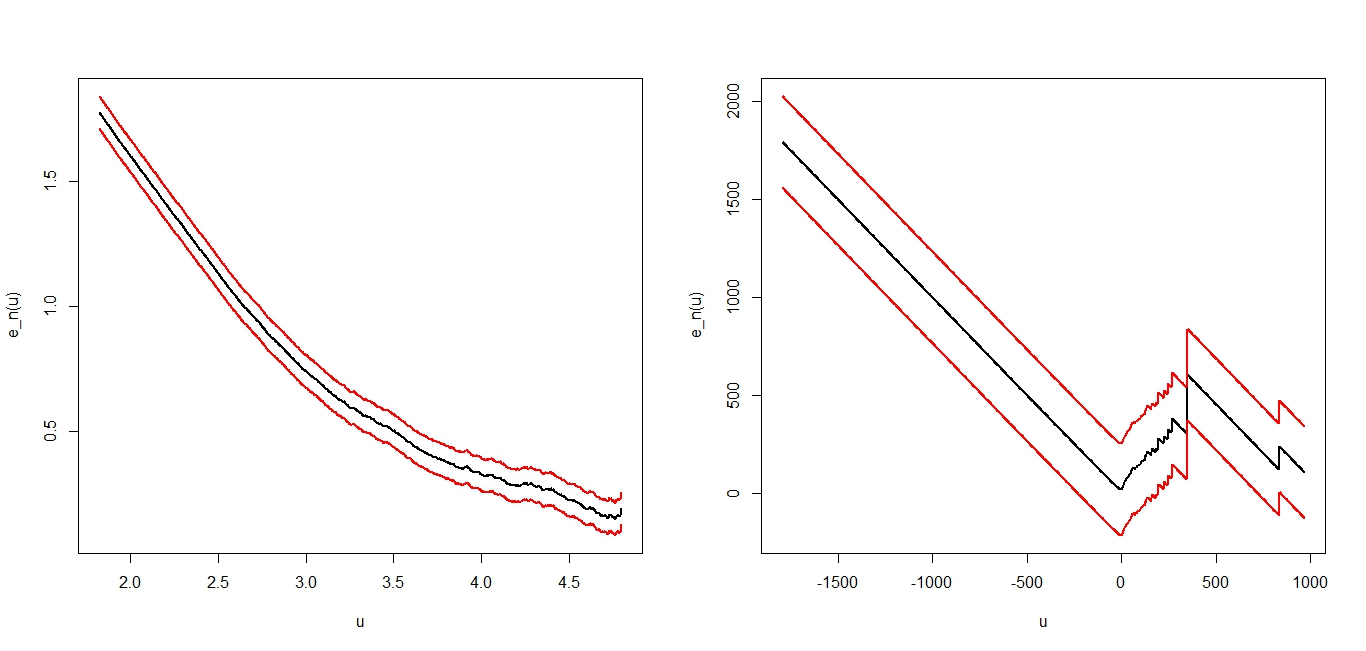

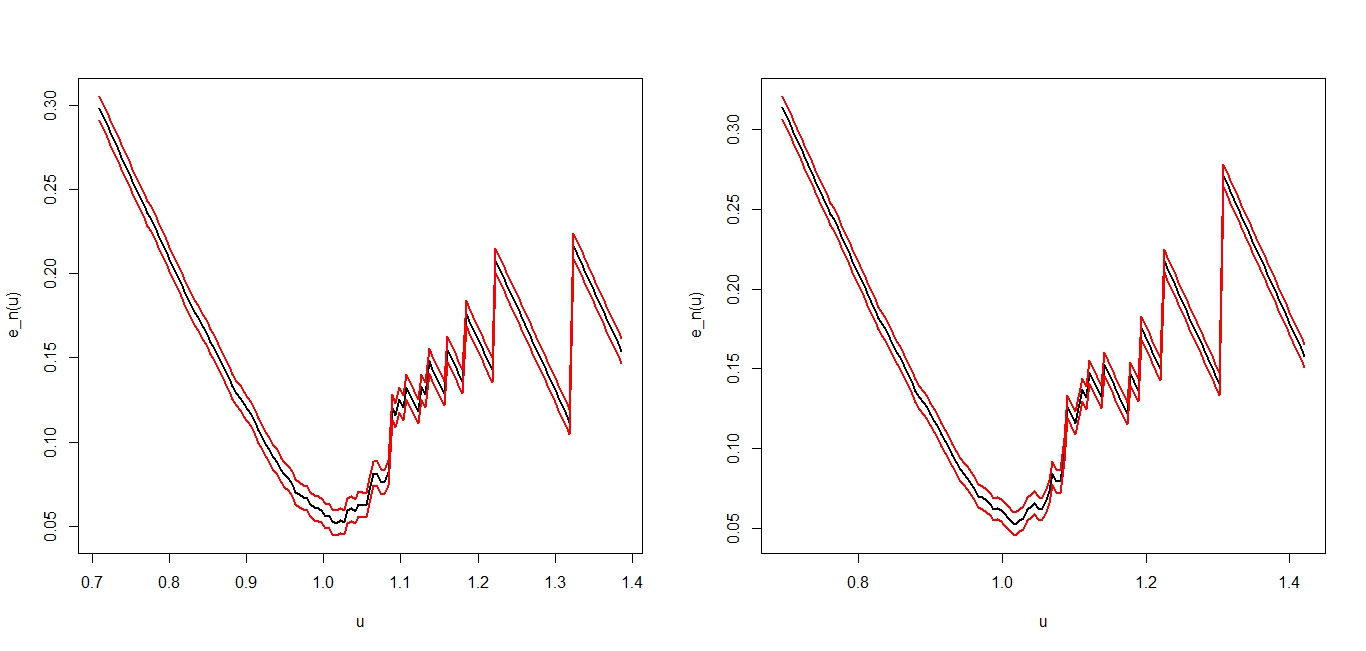

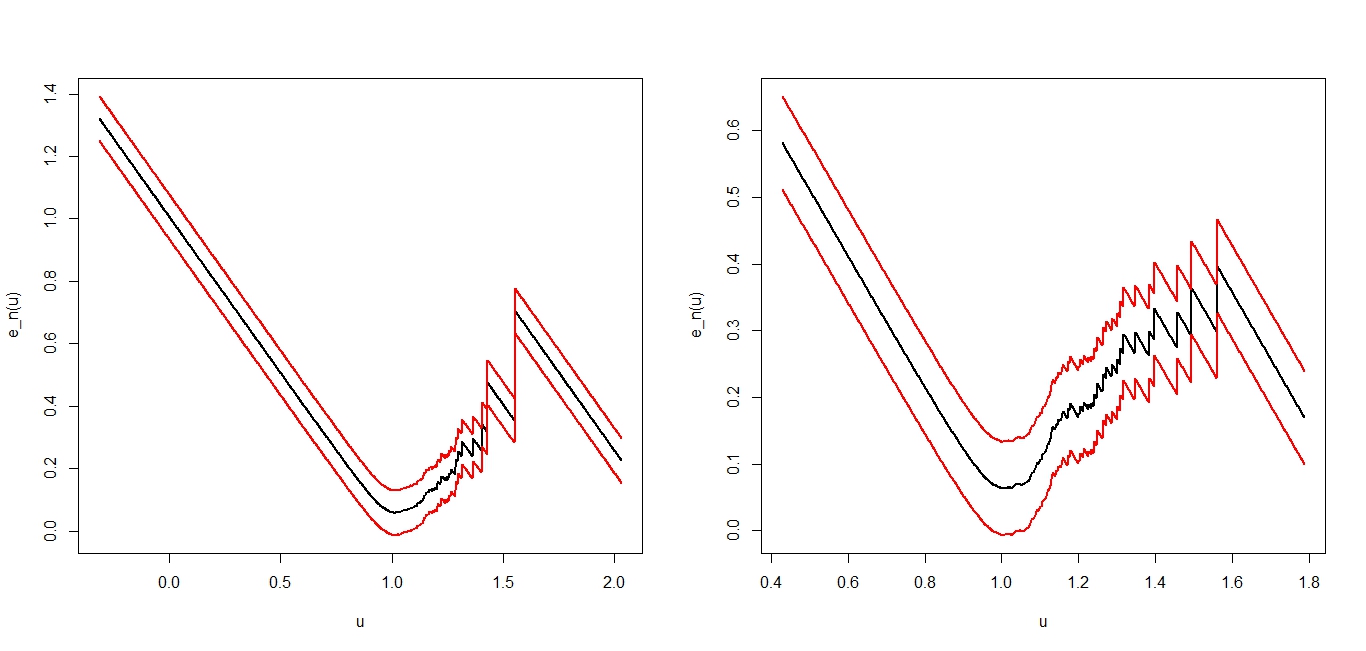

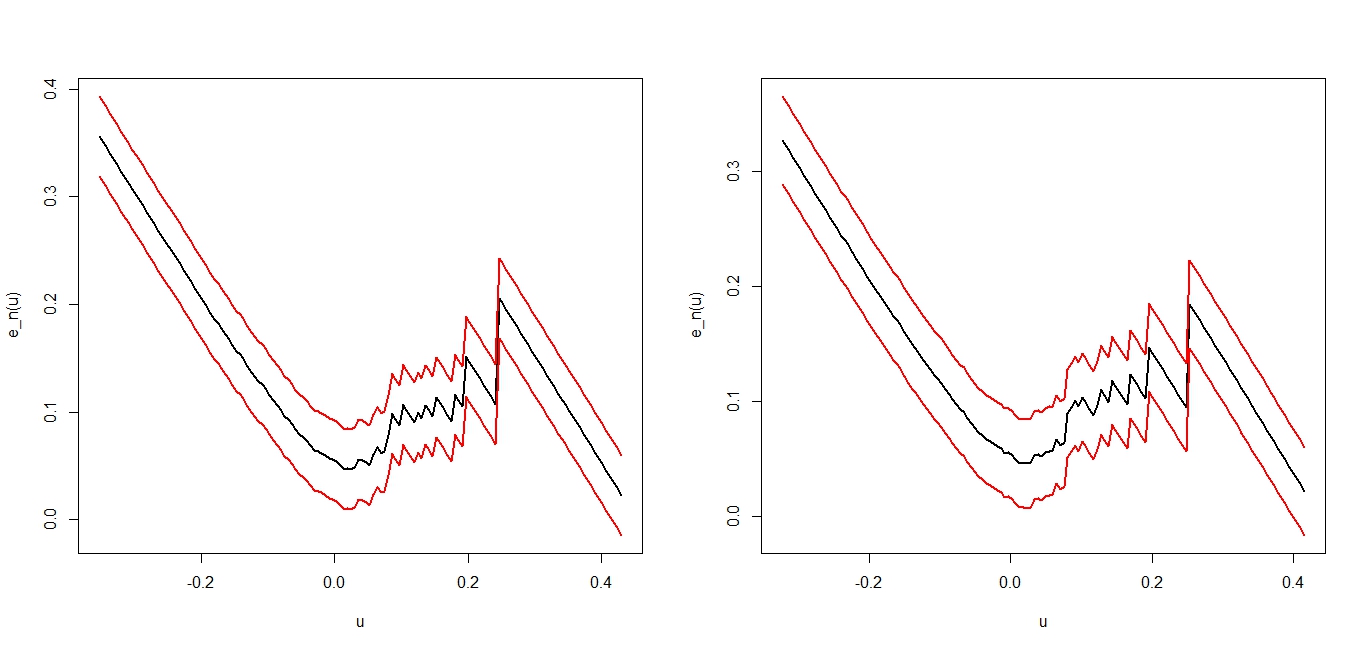

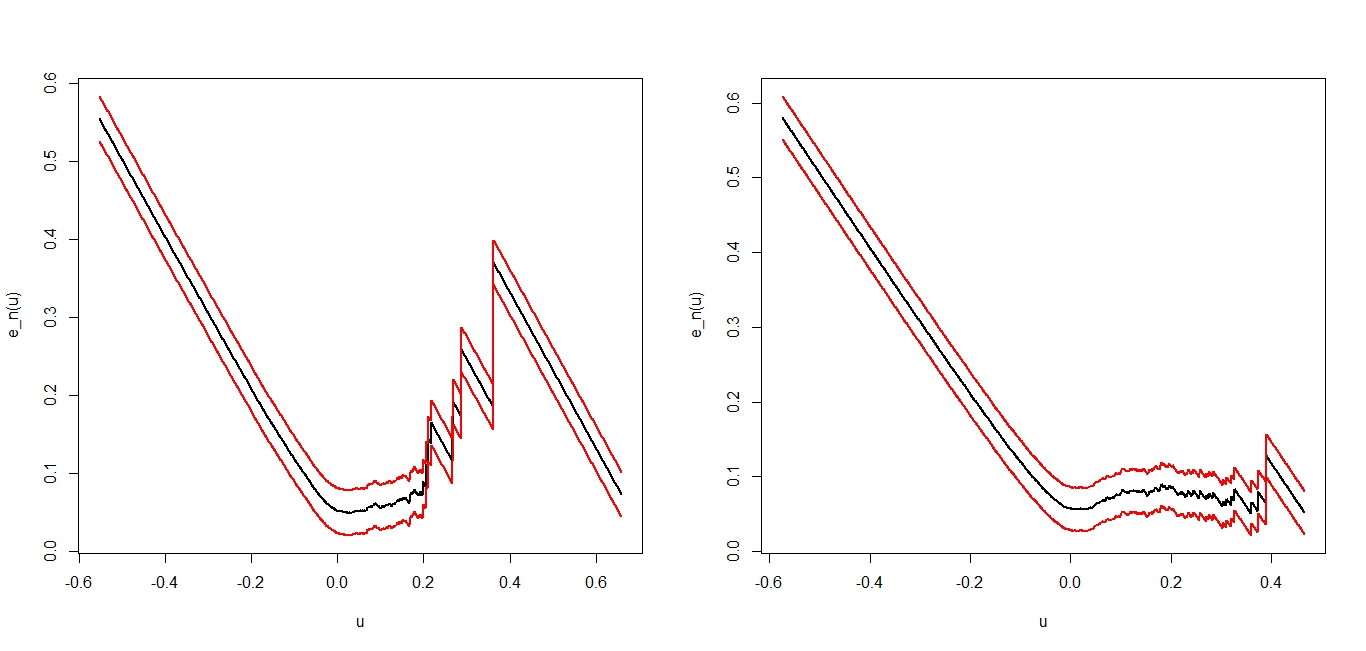

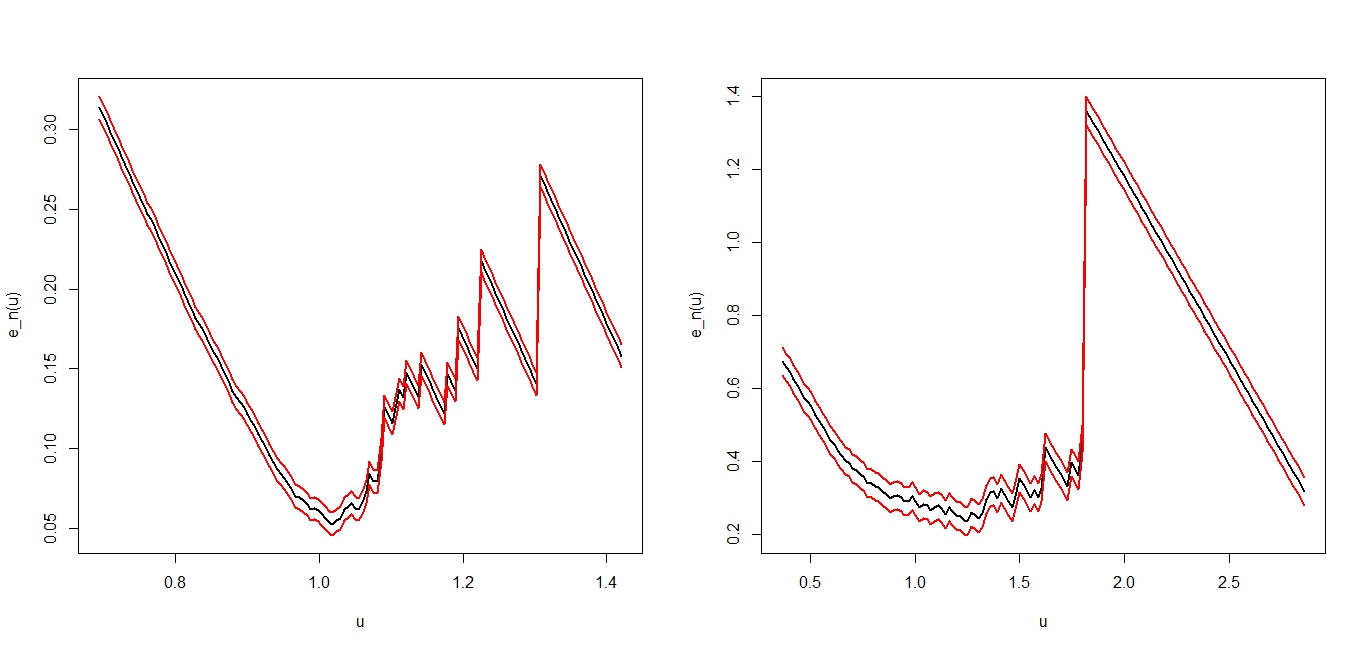

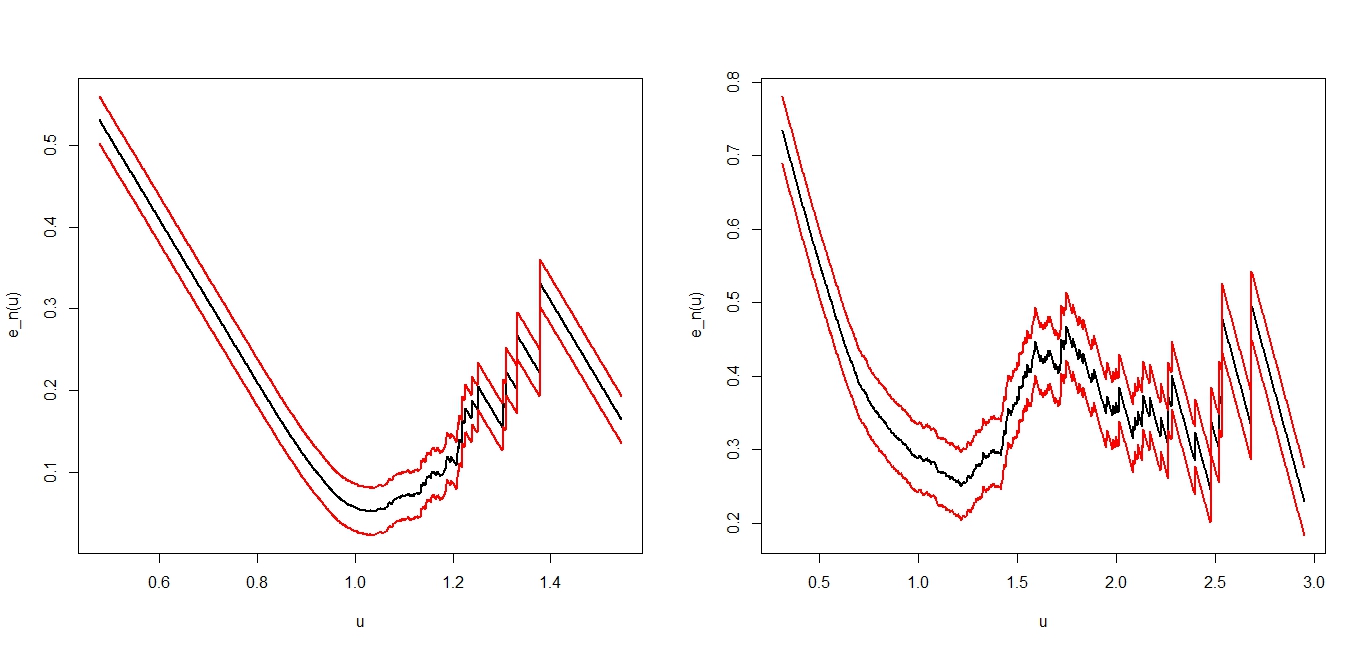

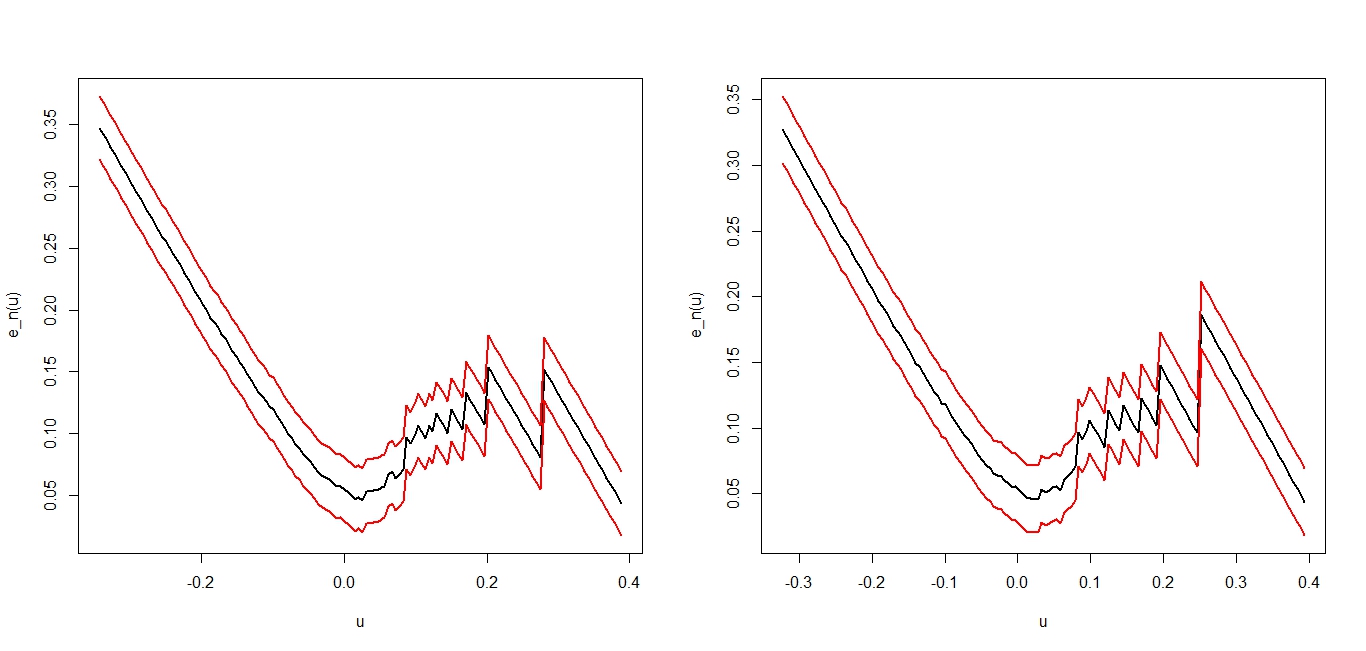

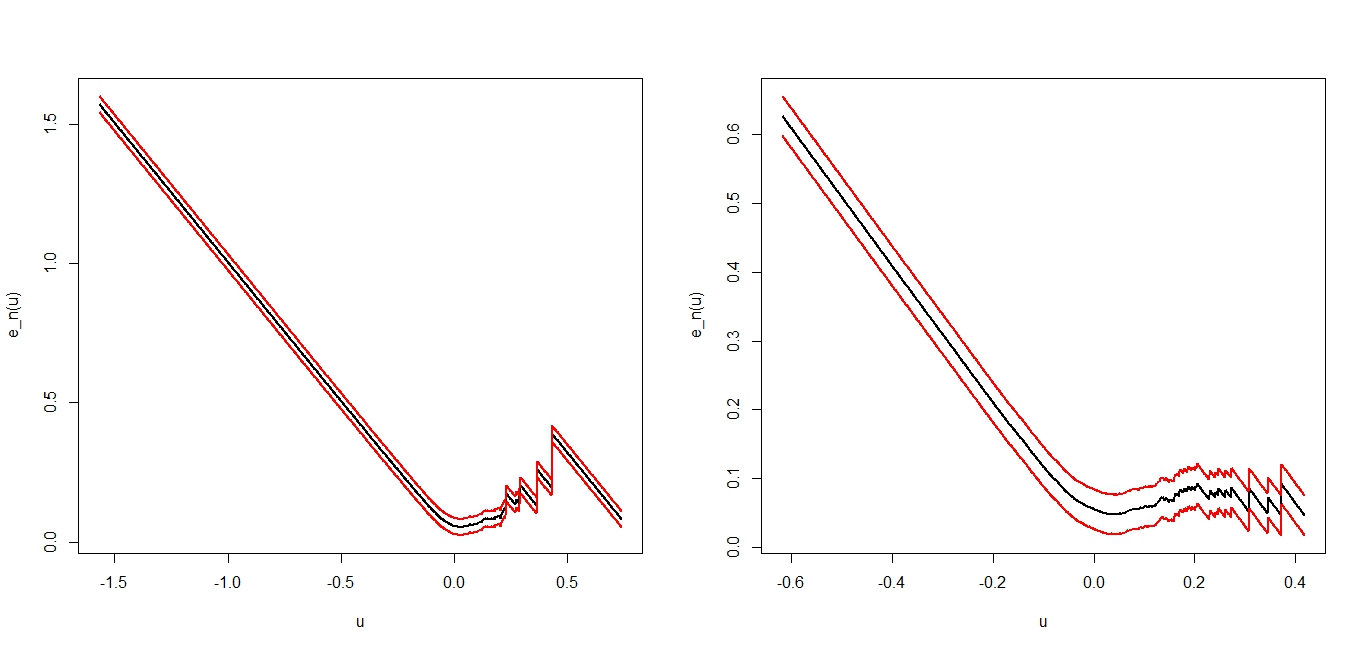

Furthermore, using Talagrand’s inequality (see [8]), and Mason and al. technics (see [9]), we arrived at finding our best achievement: that is finding consistency bands for the mean excess function . Precisely we establish that for any interval , being less than the upper endpoint of and for any , we have for large

|

|

|

where is a non-random sequence of real numbers precised in Theorem 3 and where satisfies a very slight condition.

These results allowed us to set graphical goodness of fitting test based on the empirical mean excess function and to apply this test to Dow jones data. We found that the Generalized hyperbolic family distribution reveals, itself, to generally fit financial data.

In this remainder of the text, we are going to detail this outlined results, to demonstrate them, to make simulations studies about them, and finaly to apply them to financial data.

The paper is organized as follows. We state uniform almost sure () convergence results in Section 2 and finite-distribution and functional normality theorems in Section 3.

Section 4 is devoted to setting consistency bands for the mean excess function. In Section 5, simulation studies and data driven applications using Dow Jones data are provided. We finish the paper by a concluding section.

Before we go any further, it is worth mentioning that, in the sequel, all the suprema, taken over are measurable since the functions of that

we consider below, are left or right continuous. This means that we are in

the pointwise-measurability scheme. Thus, even when we use the results and

concepts in [10], we do not need exterior either interior

integrals or convergence in outer probability.

2. Almost Sure Convergence

In this section we are going to prove the uniform almost sure convergence of the empirical mean excess function by using Vapnik-Chervonenkis (VC) classes and bracketing numbers.

Theorem 1.

Suppose that and

then

|

|

|

and

|

|

|

For any fixed for

|

|

|

Proof. We observe that

is a class of monotone real functions with values in . By Theorem 2.7.5 in [10], the

bracketing number

is finite (bounded by , for every probability measure

, any real , and a constant that only depends on ).

Since

for

is functional Glivenko-Cantelli class in the sense of Theorem 2.4.1 in [10], meaning that

| (2.1) |

|

|

|

The class with , is a

Vapnik-Chervonenkis class with index and its

envelop is ). Then it

satisfies the uniform entropy condition 2.4.1 in [10]. Then

is a Donsker class and hence it is a Glivenko Cantelli class, that is

| (2.2) |

|

|

|

To finish, fix Then for and large enough,

we have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Then

| (2.3) |

|

|

|

Let

| (2.4) |

|

|

|

From (2.1) and (2.2) above, we have

|

|

|

Now for , we have and from (2.4) ,

|

|

|

|

|

|

since for large enough, then .

We also have

| (2.5) |

|

|

|

Thus

|

|

|

and then

|

|

|

3. Asymptotic normality of

In this section, we are concerned with weak laws of the empirical mean excess

process as a stochastic process. Hereafter denotes a Gaussian centered functional stochastic

process with variance-covariance function

|

|

|

Theorem 2.

Let be iid ’s with common

finite second moment.

Put with and define the functions of

|

|

|

Suppose that is continuous and satisfies

|

|

|

Then the functional empirical processes and

weakly converge respectively to and in

And weakly

converges to

Before we give the proof,

we need this lemma.

Lemma 1.

Let be a finite measurable function defined on such that . Let Define for any fixed and

|

|

|

Let for a fixed

|

|

|

|

|

|

then

|

|

|

Proof of Lemma 1. We fix and

consider Observe that for

|

|

|

Since for all

, we have

|

|

|

it comes that is finite. So for any we can find such that,

| (3.1) |

|

|

|

Now, let . Define for any and consider ,

Let us prove that for

|

|

|

For each let such that

|

|

|

We have,

|

|

|

|

|

|

|

|

|

|

by denoting

|

|

|

We get from (3.1)

|

|

|

For a fixed , as , since the sequence of intervals decreases to the empty set as .

Next, consider the collection points and denote the set of its

distinct values between them as We still have And we surely have for any

|

|

|

and then

|

|

|

and finally

|

|

|

By construction, is non decreasing in . So, by the

Monotone Convergence Theorem, for any fixed for any

| (3.2) |

|

|

|

Put

We have

|

|

|

with

|

|

|

We observe that are partial sums

of i.i.d. centered random variables so that the form a

submartingale. By the maximal inequality form submartingales, for any fixed

|

|

|

|

|

|

|

|

|

|

Since the right hand does not depend on we get by (3.2)

|

|

|

Notice that is a sum of i.i.d centered

random variables with variance

|

|

|

and fourth moment

|

|

|

Simple computations give (see the appendix 7.1 for a simple proof of that)

|

|

|

By putting these facts together, we arrive at

|

|

|

|

|

|

|

|

|

|

Remark that

|

|

|

|

|

|

|

|

|

|

We finally get

|

|

|

whenever and

This achieves the proof of the lemma.

By Theorem 2.7.5 in [10] applied to and by the fact that is a Vapnik-Chervonenkis class, condition (2.5.1) is satisfied for both and thus and are Donsker classes.

This may be used in a simple manner to get

| (3.3) |

|

|

|

Denote the functional empirical process for any real function by

|

|

|

Remind that for any Donsker class , the functional stochastic process converges in law to a Gaussian and centered stochastic

process whose variance-covariance function is

|

|

|

We have, as

|

|

|

|

|

|

Thus

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

We find

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Since is a Donsker class, then . So

|

|

|

Let us remind that . Then, for , we get

|

|

|

|

|

|

We finally have

| (3.4) |

|

|

|

Lemma 2.

The class is a Donsker Class.

At this step, we want to prove that is a Donsker Class. Since we obviously have, by the Central Limit Theorem, finite distribution

convergence of to the stochastic process in we only need to prove the asymptotic tightness

of

In view of Theorem in

1.5.7 in [10], it is enough to prove that

|

|

|

Here, we apply Lemma 1 for the nondecreasing mesurable function and .

In both cases, we inspect the assumptions of this lemma and see that

if ,

we get for any and thus

|

|

|

|

|

|

|

|

|

|

and

|

|

|

If , the result is obvious.

We can apply Lemma 1 and we will get,

|

|

|

and

|

|

|

But by Theorem 8.3 of Billingsley [2], p.56, and by Theorem 2.2 in Lo

[7], these two previous equalities entail, that

|

|

|

and

|

|

|

Next, we use the following development for

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

We get

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Then

|

|

|

Next

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Also,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For ,

let us use the bounds of , , and

We obtain , , and finally, from (2.5), we get

Thus by using these bounds and (3.3), it comes that

|

|

|

|

|

|

where

|

|

|

Now we observe that

|

|

|

and

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

These quantities go to zero whenever is continuous and hence

uniformly continuous in Putting all these facts together and using (3.3)

yield

|

|

|

Finally is a Donsker class, thus and we get from (3.4) that

|

|

|

This completes the proof.

Now we are going to concentrate on consistency bands for the mean excess function.