Universality of market superstatistics

We use a continuous-time random walk (CTRW) to model market fluctuation data from times when traders experience excessive losses or excessive profits. We analytically derive “superstatistics” that accurately model empirical market activity data (supplied by Bogachev, Ludescher, Tsallis, and Bunde) that exhibit transition thresholds. We measure the interevent times between excessive losses and excessive profits, and use the mean interevent time as a control variable to derive a universal description of empirical data collapse. Our superstatistic value is a weighted sum of two components, (i) a power-law corrected by the lower incomplete gamma function, which asymptotically tends toward robustness but initially gives an exponential, and (ii) a power-law damped by the upper incomplete gamma function, which tends toward the power-law only during short interevent times. We find that the scaling shape exponents that drive both components subordinate themselves and a “superscaling” configuration emerges. We use superstatistics to describe the hierarchical activity when component (i) reproduces the negative feedback and component (ii) reproduces the stylized fact of volatility clustering. Our results indicate that there is a functional (but not literal) balance between excessive profits and excessive losses that can be described using the same body of superstatistics, but different calibration values and driving parameters.

1 Introduction

Financial markets fluctuate as traders estimate risk levels and strive to make a profit. The interevent interval between times when market returns are producing excessive profits and times when they are producing excessive losses can be described using a continuous-time random walk (CTRW) formalism (see Refs. (?, ?, ?, ?) and references therein).

Empirical market data on excessive profits and losses (?, ?, ?, ?) define excessive profits as those greater than some positive fixed threshold and excessive losses as those below some negative threshold . The mean interevent time111The term ‘interevent time’ appears in the literature under such names as ‘pausing time’, ‘waiting time’, ‘intertransaction time’ and ‘interoccurrence time’ in the context of different versions of the continuous-time random walk formalism (?, ?, ?, ?, ?). between losses versus has been used as an aggregated basic variable.

Interevent times constitute a universal stochastic measurement of market activity on timescales that range from one minute to one month (?, ?). The mean interevent time can be used as a control variable that produces a universal description of empirical data collapse (?), i.e., the distribution of interevent times for a fixed mean interevent time is a universal statistical quantity unaffected by time scale, type of market, asset, or index.

This distribution can be described using (i) the CTRW valley model (see Refs. (?, ?) and references therein), which treats time intervals as random variables, and (ii) generalized extreme value statistics222Whether the value of losses or profits in the basic stochastic process are statistically independent is irrelevant because any possible correlations between them are absent in our derivations. for stochastic dependent basic processes (?), which are -exponentials not ad hoc statistics (?, ?). Inter-event times in a multifractal structure of financial markets (?, ?) and in the single-step memory in order-book transaction dynamics (?) are foundational in the analysis of double-action market activity.

2 Principal goal

Our principal goal is to model the empirical data333All data fits and drawings were made using Mathematica Ver. 10. associated with single-variable statistics, i.e., (i) the mean inter-event time period between extreme (excessive) losses, defined as those below a negative threshold , as a function of the value444For the sake of simplicity, we will treat losses as positive quantities. and (ii) the distribution of inter-event times between losses , previously described using ad hoc -exponentials.

Because no empirical data associated with item (i) are available, in our study of excessive profits we will focus on item (ii) and use the empirical data provided in Refs. (?, ?, ?, ?). Note that the -exponentials used in Refs. (?, ?, ?, ?) cannot produce the key empirical data in item (i), and thus in our approach we use superstatistics. Because small losses and profits are of little concerm to traders, we focus on medium to high -values. Our goal is to provide market superstatistics that have universality.

3 Basic achievement

We here find an analytical closed form of the mean interevent time period between excessive (extreme) losses that is greater than some threshold , i.e.,

| (1) |

where is a time unit555Later in this text we will set . and the density of returns given by the Weibull distribution of extreme (or excessive) losses (?, ?, ?),

| (2) |

Note that we consider random variable to be an increment of some underlying stochastic process.666For the Weibull distribution the relative mean value and the relative variance are -dependent that is, they are (for fixed exponent ) universal quantities. Values of this random variable can, in general, be dependent (?). Here we consider case (see Table 1) which means that distribution is, for , a decreasing truncated power-law (?).

Reference (?) uses the Weibull distribution to describe the statistics of interevent times between subsequent transactions for a given asset. We use the Weibull distribution and the conditional exponential distribution of the CTRW valley model to derive superstatistics or complex statistics associated with the threshold of excessive losses or profits.

Substituting (2) into (1), we obtain

| (3) |

i.e., increases vs. the relative variable according to a power-law.

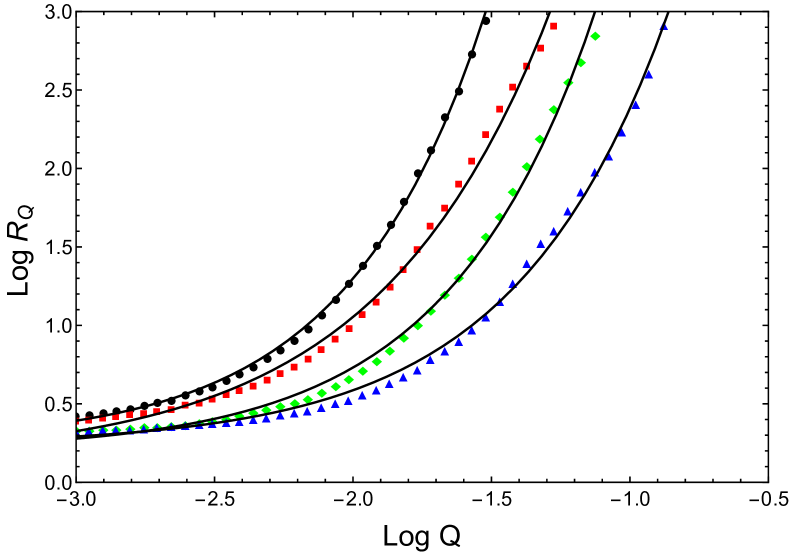

The solid curves in Fig. 1 indicate the predictions generated by (3)777Note that each curve has a slightly different multiplicative calibration parameter that defines its vertical shift. and fit the empirical data (the points are represented by different marks). This basic agreement enables us to construct the corresponding superstatistics and allows us to study the successive empirical data (given in Secs. 4 and 5). Because the statistical error is low we are able to determine and and derive the subsequent parameters that define the shape of the superstatistics. For example, the empirical data in Fig. 1 indicates that the value of the shape parameter exponent is (cf. Table 1), which for large losses or profits (i.e., ) makes the Weibull distribution (2) a stretched exponentially truncated power-law. In contrast, the results presented in Ref. (?) are incomplete because they allow no analogous comparison with theoretical predictions based on the -exponential.

| Index/Par. | ||

|---|---|---|

| US/GBP | 0.87560.0156 | 0.00370.0003 |

| S&P500 | 0.69810.0292 | 0.00350.0005 |

| IBM | 0.82460.0236 | 0.00780.0007 |

| WTI | 0.78550.0182 | 0.01310.0008 |

4 Superstatistics

We next construct an unnormalized, unconditional distribution of the interevent time stochastic variable, , in the form of superstatistics888To normalize the superstatistics given by (4) we divide by or multiply it by . This produces conditional superstatistics limited to profits and losses no smaller then . based on the Weibull distribution used in Sec. 3,

| (4) |

Here we assume the conditional distribution is in the exponential form999The exponential form of the conditional distribution (5) assumes that the losses or profits of a fixed value are statistically independent, which is generally not valid for different values of losses and profits.

| (5) |

Because it is conditional, the next (subsequent) loss is exactly , and the relaxation time is given by the stretched exponential

| (6) |

as a straightforward extension of the exponential relaxation time used in the canonical version of the CTRW introduced by (?, ?, ?, ?) in the context of photocurrent relaxation in amorphous films. Here is a free (-independent) relaxation time, and quantity is independent of variable . Quantity is a formal analog of an inverse temperature and we will later derive its scaling with the control threshold value. We use the exponent in (2) to reduce the number of free exponents in (6) (Ockham’s razor principle) and to derive superstatistics in an exact closed analytical form. Note that the stochastic dependence of interevent time on loss assumed in (5) is confirmed when smaller losses appear more frequently than larger ones. This is described by definition (6) in which mean time is a monotonically increasing function of . This creates an expanding hierarchy of interevent times where larger losses and profits appear less frequently than smaller ones. To make larger losses or profits appear more frequently than smaller ones, we create the opposite hierarchy of losses and profits using

| (7) |

In this opposite case (which is also analytically solvable) we encounter a clustering phenomenon in which shorter time intervals separate the larger values of losses/profits rather than the smaller ones. This complementary case is briefly discussed in Sec. 5.

Substituting (6) and (5) into (4) we finally derive a superstatistics in the searched form

| (8) | |||||

where the scaling shape exponent

| (9) |

and the lower incomplete gamma function

| (10) |

The significant step in the derivation of formula (8) is the replacement of the running variable , present in the integration (4), with a new running variable . This changes the stretched exponential to exponential in the overall function under the integral in (4) making the integration a straightforward (exact and closed) operation. Note that the first equality in (9) gives a straightforward, formal generalization of the corresponding exponent obtained within the canonical CTRW valley model (?, ?, ?, ?), where is the thermodynamic , is the mean valley depth, and the exponent value is .

Equation (8) asymptotically (for ) takes a power-law form

| (11) |

of the relative interevent time while initially (for ) it takes an exponential form

| (12) |

Note that our approach is based solely on the relaxation time (6) as a function of a single variable . Only , is used, and parameter is the external control threshold, i.e., by using (6) and (3), we obtain

| (14) |

Thus using (9) and (3) we find

| (15) |

Equations (9) and (14) show the decisive role of the relaxation time , but its ab initio derivation is difficult. Note that Fig. 2 and Table 2 show a data collapse for a given (fixed) value of a single control (aggregated) variable .

| Fig. 2(a) | Fig. 2(b) | Fig. 2(c) | Fig. 2(d) | |||||

|---|---|---|---|---|---|---|---|---|

| 2 | 1000 | 1.7699 | 1000 | 1.5436 | 1000 | 1.6129 | 1000 | 1.6129 |

| 5 | 3.50 | 3.125 | 2.30 | 2.70 | 3.30 | 3.330 | 3.60 | 3.70 |

| 10 | 2.10 | 5.0 | 2.0 | 5.0 | 2.0 | 4.550 | 2.10 | 5.0 |

| 30 | - | - | 1.050 | 5.560 | 1.0 | 5.0 | 1.10 | 5.260 |

| 70 | - | - | 0.550 | 4.760 | 0.550 | 6.670 | 0.50 | 5.260 |

We analytically prove that is the control variable that allows a universal form of (8) that depends solely on . This variable was similarly used previously in connection with the -exponential (?). Using this universal form requires that we assume that the in (6) and (9)) depends on in a power-law form, or the relevant scaling relation of scaling variable ,

| (16) |

where prefactor and exponent are -independent positive control parameters. Note that the second equality is a scaling relation having as a scaling variable. Thus from (9), (3), and (16) we obtain the superscaling of the scaling variable (or the scaling of scaling, i.e., the scaling of the scaling exponent),

| (17) |

which we further verify by examining data, e.g., for the IBM company, which are typical of the empirical data used.

From (6), (3), and (15) we next obtain the scaling relation of the scaling variable ,

| (18) |

Note that quantities , , and all depend on the single control variable . We will describe and discuss the -dependence of below, and will use the corresponding empirical data to confirm all the -dependencies.

4.1 Empirical verification of our formulas

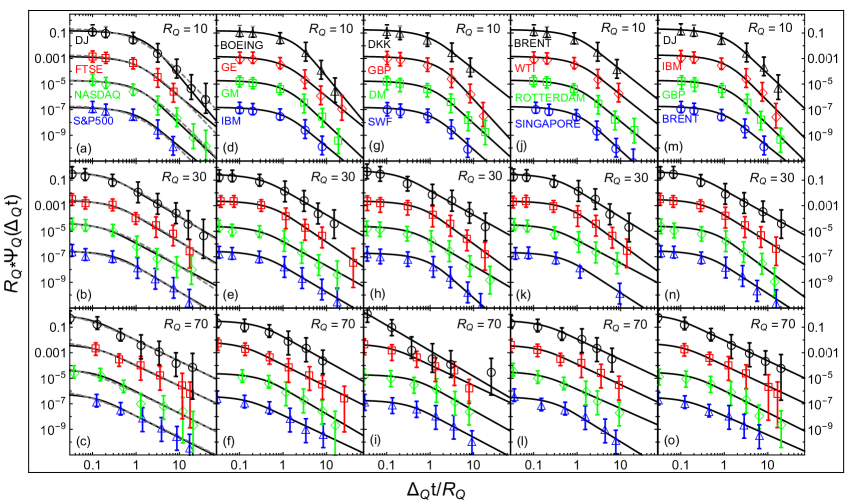

Figure 3 shows the agreement between the predictions of (8) and the empirical data for IBM for , 5, 10, 30, and 70.

Table 3 shows the fit of quantities and .

| 2 | 0.0050 | 1000 | 1.4286 |

|---|---|---|---|

| 5 | 0.01389 | 3.0 | 3.330 |

| 10 | 0.02145 | 1.90 | 5.0 |

| 30 | 0.03442 | 0.950 | 4.550 |

| 70 | 0.04508 | 0.470 | 3.850 |

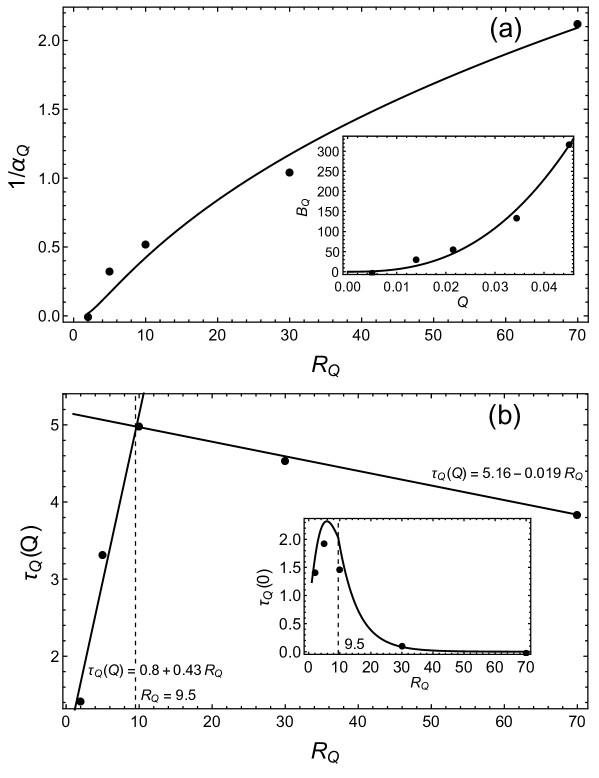

Figure 4(a) shows the good fit of (17) (solid curve) to the data (black circles) also found in the third column in Table 3.

This fit allows us to determine the parameter and exponent (see Table 4).

| 0.04798 | 2.6096 |

The inset plot shows the good agreement between the (16) prediction (solid curve) and the data (black circles). We prepared the data by putting the first equality in (9) into the third column of Table 5, where the and of IBM is supplied in Table 1.

Figure 4(b) shows a plot of vs. , where comes from the fourth column of Table 3. The plot consists of a broken straight line or two crossing straight lines. Table 6 shows the parameters of linear regressions and , with , that define the dependence of both straight lines on . The inset plot uses (15) and (17) to calculate (i) the data points (black circles) with supplied by Table 3, and (ii) the solid curve, using the analytical form of .

| Parameters | ||

|---|---|---|

| 0.430 | -0.019 | |

| 0.80 | 5.160 |

Thus by analytically and empirically proving the -dependence of the superstatistics we explain the empirical data collapse shown in Fig. 2.

5 Discussion and concluding remarks

We find an explicit closed form of the threshold interevent time superstatistics (8) that is valid for excessive losses, is the foundation of the continuous time random walk (CTRW) formalism, and that is useful in the study of a double action market (see (?) and refs. therein). These superstatistics are more credible than the -exponential distribution that is applied ad hoc in this context in Ref. (?, ?), and they agree with the key empirical relation between the mean interevent time and the threshold (see Fig. 1).

We model the empirical data collapse (cf. Fig. 2) using superstatistics as a function of a single aggregated variable and obtain, for example, the scaling shape exponent as a power-law function of and the superscaling form of (17) that is dependent upon universal exponent and prefactor .

Note that (8) accurately describes the empirical statistics of excessive profits. Here defines the threshold for excessive profits instead of excessive losses (see the plots in Fig. 5). We thus can use the same superstatistics to demonstrate the functional but not literal symmetry between excessive losses and profits. The symmetry is not literal because different control parameters and and driving parameters and () are used. Because of large statistical errors in the empirical data, we cannot empirically verify the universality of excessive profit behavior. For example, for exponent and , for we have and , and finally for we have and , which exhibit ranges that are too extended.

Note that if we substitute given by (7)—the case opposite to that defined by (6)—into (5), and use a derivation analogous to the one that produced (8), we obtain a result complementary to (8), i.e.,

| (19) | |||||

where

| (20) | |||||

is the upper gamma function, which for truncates the power-law in (19). In the opposite case of we obtain

| (21) |

which is only formally identical to (11). Figure 3 shows the best predictions of the weighted sum of superstatistics (dashed dotted curves) given by (8) and (19). Note that this continues to agree with the corresponding empirical data for IBM.

We use (2), (6), and (9) to obtain the moment in an explicit closed form,

| (22) | |||||

where the first equality gives the definition101010Here we consider only integer non-negative moments.. Note that the moments of arbitrary order, as well as and , depend solely on . Note also that is finite only for , and that otherwise it diverges. This is in contrast to the behavior of , which, because of its quantile (not momentum) origin, is always finite, e.g., for IBM is finite only for (see Table 3). We thus have two radically different cases, finite interevent time and infinite interevent time , about which there is much in the literature (see, e.g., (?, ?, ?, ?) and refs. therein). Infinite interevent time is particularly interesting when it takes into consideration ergodicity breaking (?, ?).

Note that using our microscopic model to simulate agent behavior (?, ?) gives results very close to those predicted by (8). An approach using agent-based modeling in this context was recently explored by other authors (?).

It is our hope that this work will constitute a strong contribution to the research effort searching for universal properties in market behavior.

References and Notes

- 1. G. Pfister and H. Scher, Adv. Phys. 27, 747 (1978).

- 2. J. W. Haus and K. W. Kehr, Phys. Rep. 150, 263 (1987).

- 3. R. Kutner and F. Świtała, Quant. Finance 3, 201 (2003).

- 4. T. Sandev, A. Chechkin. H. Kantz. R. Mentzler, An Int. J. Theory and Applications 18, 1006 (2015).

- 5. J. Ludescher, C. Tsallis, A. Bunde, Eur. Phys. Let. 95, 68002 (2011).

- 6. J. Ludescher and A. Bunde, Phys. Rev. E 90, 062809 (2014).

- 7. M. I. Bogachev and A. Bunde, Phys. Rev. E 78, 036114 (2008).

- 8. M. I. Bogachev and Bunde, Phys. Rev. E 80, 026131 (2009).

- 9. K. W. Kehr, R. Kutner, K. Binder, Phys. Rev. B 23, 4931 (1981).

- 10. E. Bertin and M. Clusel, J. Phys. A: Math. Gen. 39, 7607 (2006).

- 11. J. Perelló, J. Masoliver, A. Kasprzak, and R. Kutner, Phys. Rev. E 78, 036108 (2008).

- 12. A. Kasprzak, R. Kutner, J. Perelló, J. Masoliver, Eur. Phys. J. B 76, 513 (2010).

- 13. T. Gubiec and R. Kutner, Phys. Rev. E 82, 046119 (2010).

- 14. Y. Malevergne and D. Sornette, Extreme Financial Risks. From Dependence to Risk Management (Springer-Verlag, Berlin, 2006).

- 15. P. Embrechts, C. Klüppelberg C., Th, Mikosch, Modelling Extremal Events for Insurance and Finance (Springer-Verlag, Berlin, 1997).

- 16. J. Franke, W. Härdle, Ch. Hafner, Statistics of Financial Markets, (Springer-Verlag, Berlin, 2004).

- 17. B. B. Mandelbrot, Fractals and Scaling in Finance (Springer-Verlag, New York, 1997).

- 18. P. Ch. Ivanov, A. Yuen, B. Podobnik, Lee Y. Youngki, Phys. Rev. E 69, 056107 (2004).

- 19. E. W. Montroll and G. H. Weiss, J. Math. Phys. 6, 167 (1965).

- 20. G. H. Weiss, Aspects and Applications of the Random Walk (North-Holland, Amsterdam, 1994).

- 21. H. Scher and E. W. Montroll, Phys. Rev. B 12, 2455 (1975).

- 22. V. Gontis, S. Havlin, A. Kononovicius, B. Podobnik, H. Eugene Stanley, private communication.

- 23. J. H. P. Schulz and E. Barkai, Phys. Rev. E 91, 062129 (2015).

- 24. R. Kutner and M. Regulski, Physica A 264, 84 (1999).

- 25. R. Kutner and M. Regulski, Physica A 264, 107 (1999).

- 26. G. Bel and E. Barkai, Phys. Rev. Lett. 94, 240602 (2005).

- 27. G. Bel and E. Barkai, Phys. Rev. E 73, 016125 (2006).

- 28. M. Denys, T. Gubiec, R. Kutner, Acta Phys. Pol. A 123, 513 (2013).

- 29. M. Denys, T. Gubiec, R. Kutner, arXiv:1411.1689v1[q-fin.ST] (2014).

-

1.

Acknowledgments Two of us (M.J. and T.G.) are grateful to the Foundation for Polish Science for financial support. The work of H.E.S. was supported by NSF Grant CMMI 1125290, DTRA Grant HDTRA1-14-1-0017 and ONR Grant N00014-14-1-0738. One of us (R.K.) is grateful for inspiring discussions with Shlomo Havlin (during The Third Nikkei Econophysics Symposium, Tokyo 2004), Armin Bunde (during his visit at Faculty of Physics University of Warsaw in 2011), and Constantino Tsallis (during the SMSEC2014 in Kobe).